Herbal Extract Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 17.52 Billion |

| Market Size (2031) | USD 25.43 Billion |

| Growth Rate (2026 - 2031) | 7.74% CAGR |

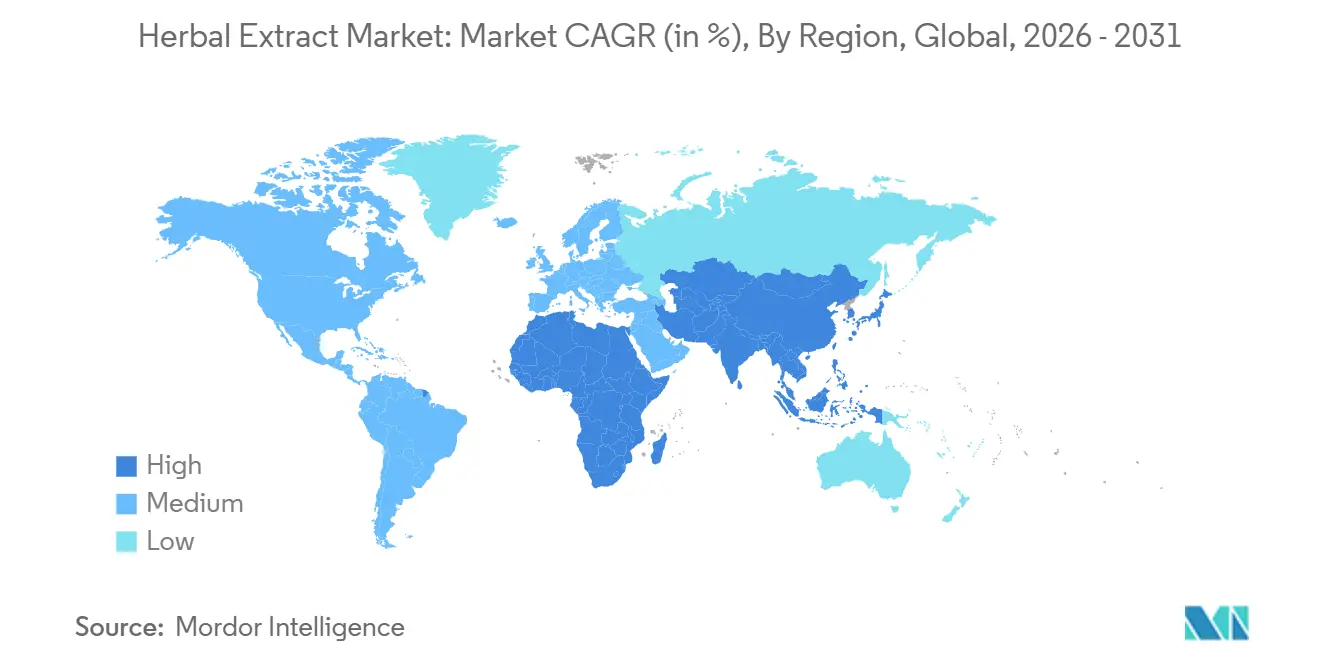

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

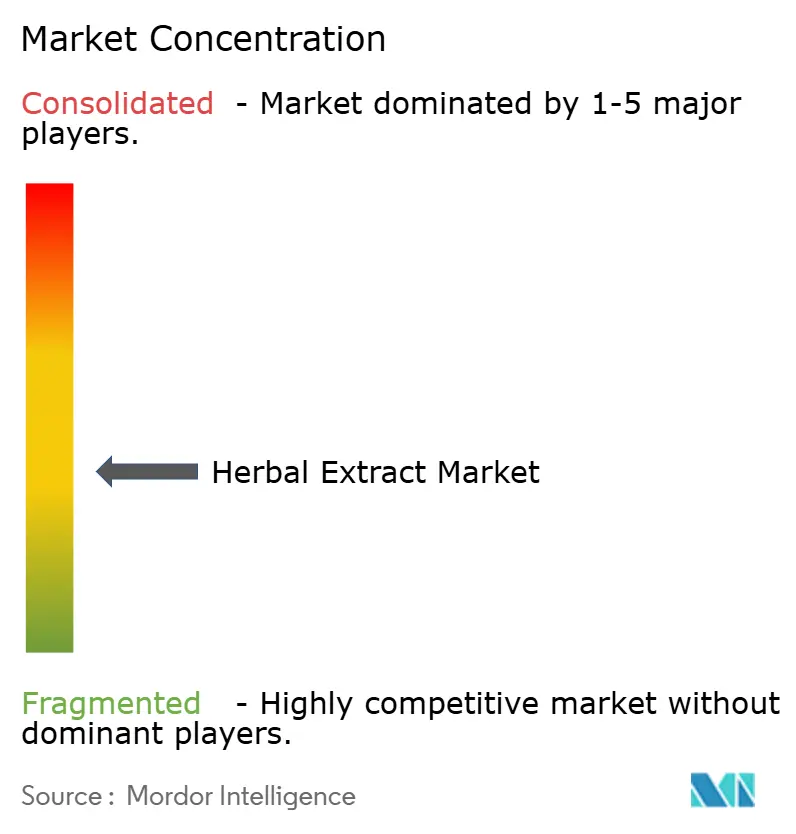

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Herbal Extract Market Analysis by Mordor Intelligence

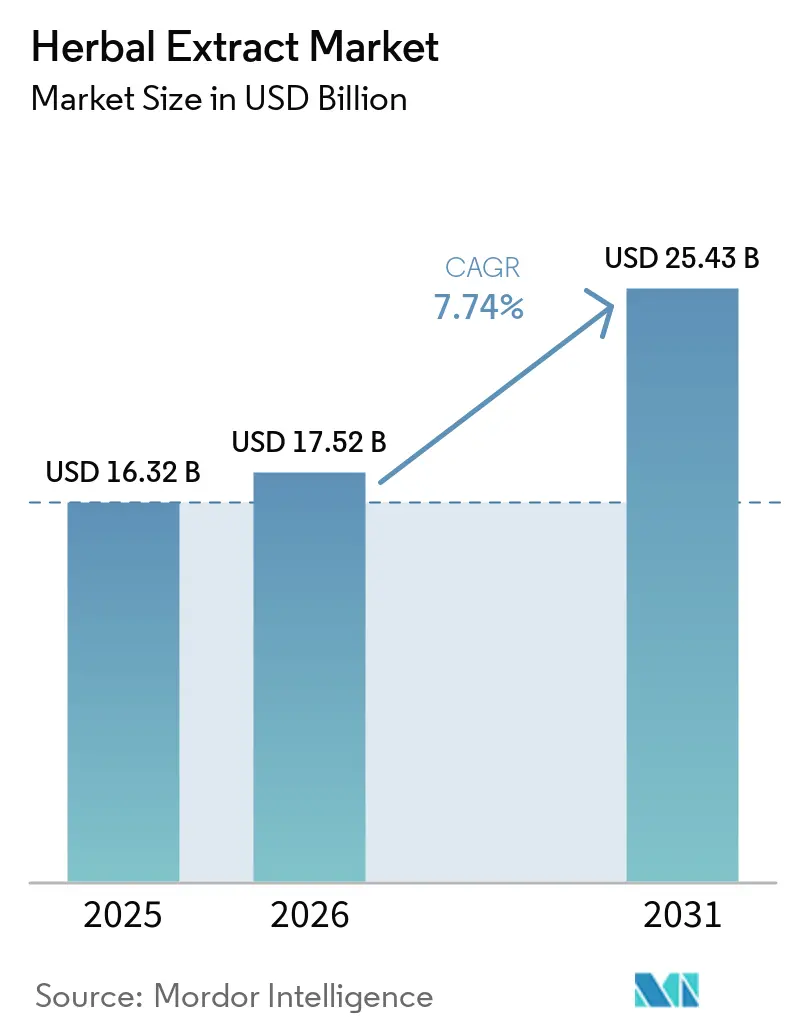

The herbal extract market size is expected to grow from USD 16.32 billion in 2025 to USD 17.52 billion in 2026 and is forecast to reach USD 25.43 billion by 2031 at a 7.74% CAGR over 2026-2031. The global herbal extract market is driven by the growing consumer preference for natural, plant-based ingredients across various industries, including food, beverages, pharmaceuticals, cosmetics, and dietary supplements. Increased awareness of preventive healthcare and the health benefits of botanicals, such as immune support, digestive health, cognitive function, and stress management, is fostering the integration of herbal extracts into daily nutrition. The rise of clean-label and organic product trends has led manufacturers to replace synthetic additives with herbal alternatives, aligning with consumer demands for transparency and sustainability. Additionally, advancements in extraction technologies, such as supercritical fluid and enzyme-assisted extraction, are enhancing the purity, potency, and consistency of herbal extracts, making them suitable for high-value applications. The growing demand for functional foods, personalized nutrition, and plant-based formulations, along with the increasing acceptance of traditional medicinal systems like Ayurveda and Traditional Chinese Medicine, is further driving market growth. Furthermore, investments in sustainable cultivation practices, standardization of botanical ingredients, and research validating the efficacy of herbal compounds are bolstering consumer confidence and creating new opportunities for the global herbal extract market.

Key Report Takeaways

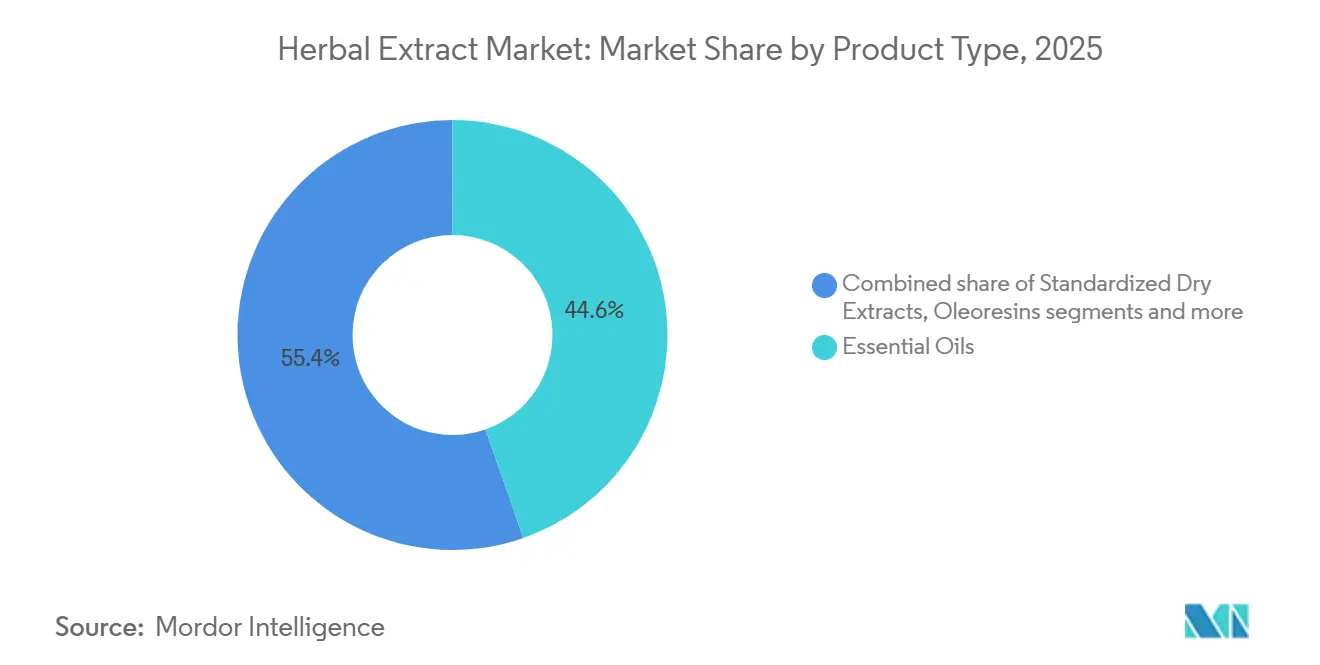

- By product type, essential oils led with 44.64% revenue share in 2025, while phytochemicals and isolates are projected to grow at 8.22% CAGR through 2031.

- By source, herbs and spices held 46.32% share in 2025, while flowers are forecast to expand at 8.64% CAGR through 2031.

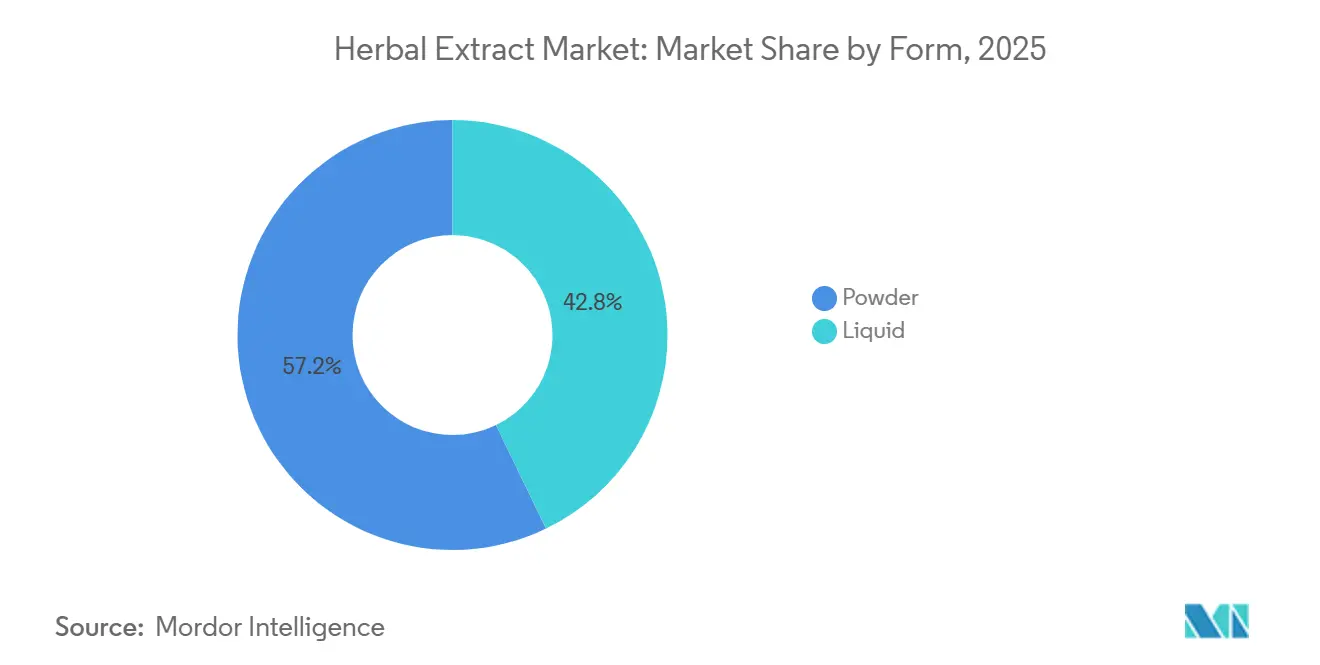

- By form, powder accounted for 57.17% of market value in 2025, while liquid is projected to record 8.11% CAGR through 2031.

- By end use, pharmaceuticals held 51.12% revenue share in 2025, while cosmetics and personal care is expected to advance at 9.10% CAGR through 2031.

- By geography, Asia-Pacific held 37.33% of the global herbal extracts market in 2025 and is also projected to record the fastest growth at 8.57% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Herbal Extract Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer preference for natural and clean-label ingredients | +2.1% | Global | Medium term (2-4 years) |

| Expanding use in functional foods and beverages | +1.8% | Global, particularly North America and Asia-Pacific | Medium term (2-4 years) |

| Technological advancements in extraction methods | +1.4% | Global, particularly North America and Europe | Long term (≥ 4 years) |

| Rising popularity of traditional and herbal medicine systems | +1.2% | Asia-Pacific core, spill-over to Middle East and Africa and North America | Medium term (2-4 years) |

| Expansion of sustainable and organic herbal cultivation | +0.7% | Asia-Pacific, South America, Europe | Long term (≥ 4 years) |

| Wider adoption in nutraceuticals and phytomedicines | +0.8% | North America and European Union, with early gains in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing consumer preference for natural and clean-label ingredients

Increasing consumer preference for natural and clean-label ingredients is a key factor driving the global herbal extract market. With growing awareness of product composition and potential health effects, consumers are opting for foods, beverages, dietary supplements, cosmetics, and personal care products made with plant-based ingredients rather than synthetic additives. Herbal extracts are valued for their natural origin, functional benefits, and suitability for clean-label product development, making them a preferred choice for manufacturers aiming to align with changing consumer expectations. This trend is prompting companies to diversify their offerings with botanical formulations that prioritize transparency, minimal processing, and easily recognizable ingredient lists. Supporting this development, the 2025 IFIC Food & Health Survey reported that approximately 41% of Americans actively seek "natural" label claims when purchasing food products, underscoring the increasing significance of natural ingredient positioning[1]Source: International Food Information Council, "2025 IFIC Food & Health Survey," ific.org. As global demand for clean-label products grows, the use of herbal extracts is anticipated to expand across various end-use industries, driving sustained market growth.

Expanding use in functional foods and beverages

The increasing incorporation of herbal extracts in functional foods and beverages is a key factor driving the growth of the global herbal extract market. Consumers are prioritizing products that offer health benefits beyond basic nutrition, prompting manufacturers to include botanical extracts in beverages, dairy products, snacks, nutrition bars, herbal teas, and fortified foods. Commonly used ingredients such as turmeric, ginger, green tea, ashwagandha, elderberry, and ginseng are valued for their antioxidant, anti-inflammatory, immune-supporting, digestive, and stress-management properties. This trend is reinforced by the rising focus on preventive healthcare, active lifestyles, and personalized nutrition, encouraging food and beverage companies to create innovative formulations using scientifically validated plant-based ingredients. Furthermore, the preference for natural functional ingredients over synthetic additives aligns with the clean-label movement, positioning herbal extracts as a critical component in the development of next-generation functional food and beverage products. As consumer demand for convenient, wellness-oriented nutrition grows, the use of herbal extracts in the functional food and beverage industry is anticipated to increase, driving sustained market expansion.

Rising popularity of traditional and herbal medicine systems

The increasing popularity of traditional and herbal medicine systems is a significant driver of the global herbal extract market, as consumers show a growing preference for plant-based remedies in preventive healthcare and overall well-being. Established medical systems such as Ayurveda, Traditional Chinese Medicine (TCM), Unani, and other botanical healing practices are gaining broader acceptance beyond their countries of origin. This is attributed to factors such as scientific validation, heightened consumer awareness, and a preference for natural therapeutic solutions. Consequently, pharmaceutical, nutraceutical, and wellness companies are incorporating standardized herbal extracts into a wide range of health products. The rising international demand is evident in India's herbal trade performance, with exports of AYUSH and herbal products increasing by 6.11%, from USD 649.2 million in 2023–24 to USD 688.89 million in 2024–25. The establishment of AYUSHEXCIL has further enhanced global outreach, promoting the international adoption of India's traditional medicine and herbal products[2]Source: Ministry of Commerce & Industry, "Ayush Export Promotion Council observes 4th Establishment Anniversary in New Delhi," pib.gov.in . This growing global recognition of herbal medicine systems continues to fuel demand for high-quality herbal extracts across healthcare, dietary supplements, and functional wellness applications.

Expansion of sustainable and organic herbal cultivation

The growth of sustainable and organic herbal cultivation is a key factor driving the global herbal extract market. Consumers and manufacturers are increasingly focusing on environmentally responsible sourcing and chemical-free botanical ingredients. Practices such as organic farming, regenerative agriculture, and sustainable harvesting enhance the quality, traceability, and long-term availability of medicinal plants while minimizing environmental impact. In response, manufacturers are investing in certified organic supply chains to meet the growing demand for herbal extracts in food, beverages, dietary supplements, pharmaceuticals, and personal care products. Consumer behavior aligns with this trend, as highlighted by the 2025 IFIC Food & Health Survey, which indicates that 30% of Americans actively seek products with "organic" label claims, and 21% prefer those labeled as "sustainably sourced."[3]Source: International Food Information Council, "2025 IFIC Food & Health Survey," ific.org These preferences are driving companies to strengthen sustainable cultivation partnerships and expand their organic herbal ingredient offerings, thereby fostering the adoption of herbal extracts across various industries and supporting long-term market growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Variability in raw material quality and phytochemical content | -0.5% | Global, higher risk in Asia-Pacific sourcing hubs | Short term (≤ 2 years) |

| Stringent and diverse global regulatory requirements | -0.4% | North America and European Union | Medium term (2-4 years) |

| Risk of adulteration and ingredient authenticity issues | -0.3% | Global, concentrated in unregulated supply chains | Short term (≤ 2 years) |

| Seasonal dependence and agricultural supply variability | -0.2% | Asia-Pacific core, South America, Middle East and Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Variability in raw material quality and phytochemical content

Variability in raw material quality and phytochemical content poses a significant restraint on the global herbal extract market. The concentration of bioactive compounds in medicinal plants can vary widely due to factors such as plant species, geographic origin, soil composition, climate, cultivation practices, harvesting time, and post-harvest handling. These natural variations create challenges for manufacturers in maintaining consistent extract quality, potency, and efficacy across production batches. Consequently, companies are required to invest in extensive quality testing, standardization processes, and advanced analytical techniques to ensure uniformity and compliance with regulatory standards. This issue is particularly critical for pharmaceutical, nutraceutical, and functional food applications, where precise concentrations of active ingredients are essential for product performance and consumer safety. Additionally, inconsistent raw material quality can disrupt supply chains, increase production costs, and diminish consumer confidence, thereby hindering the broader adoption and commercialization of herbal extracts in global markets.

Risk of adulteration and ingredient authenticity issues

The risk of adulteration and ingredient authenticity issues poses a significant challenge for the global herbal extract market. Complex supply chains and inconsistent sourcing practices increase the chances of contamination, substitution, or dilution of botanical raw materials. High-value medicinal herbs are particularly susceptible to adulteration, involving lower-cost plant species, synthetic compounds, fillers, or undeclared ingredients. Such practices compromise product quality, efficacy, and safety, undermining consumer confidence and exposing manufacturers to product recalls, regulatory actions, and reputational harm. To mitigate these risks, companies must adopt advanced authentication methods, including DNA barcoding, chromatographic analysis, spectroscopic techniques, and comprehensive traceability systems, which contribute to higher operational costs. Smaller manufacturers often face greater difficulties in implementing these quality assurance measures, reducing their competitiveness. As a result, concerns over ingredient authenticity and supply chain integrity continue to limit the widespread adoption of herbal extracts in pharmaceutical, nutraceutical, food, beverage, and personal care applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Pharmaceutical-Grade Specificity Elevating Phytochemical Demand

Essential oils accounted for a 44.64% revenue share in the herbal extracts market in 2025, driven by increasing consumer preference for natural ingredients in personal care, cosmetics, aromatherapy, food and beverages, and wellness products. The growing awareness of the therapeutic properties of essential oils, such as antimicrobial, anti-inflammatory, antioxidant, and stress-relieving benefits, has led to their integration into skincare products, natural fragrances, household cleaning solutions, and functional beverages. The rising adoption of aromatherapy for relaxation, sleep enhancement, and mental well-being has further boosted demand, as consumers increasingly seek holistic health management solutions. Additionally, manufacturers are replacing synthetic flavors and fragrances with plant-derived essential oils to meet clean-label and sustainability demands. Technological advancements in steam distillation, cold pressing, and supercritical fluid extraction have improved oil purity, yield, and consistency, facilitating their use in premium consumer products. These factors collectively support the robust growth of the essential oils segment within the global herbal extracts market.

Phytochemicals and isolates, the smallest product category, are projected to achieve the highest CAGR of 8.22% through 2031, driven by rising demand for standardized, high-purity bioactive compounds in pharmaceuticals, nutraceuticals, functional foods, and dietary supplements. Manufacturers are increasingly isolating specific plant-derived compounds, such as polyphenols, flavonoids, alkaloids, carotenoids, and terpenoids, to create products with consistent potency, scientifically validated efficacy, and targeted health benefits. Growing consumer interest in preventive healthcare and evidence-based botanical ingredients has accelerated research into phytochemicals for applications in immune health, cardiovascular wellness, cognitive function, metabolic health, and healthy aging. Pharmaceutical companies prefer standardized isolates due to their precise dosing, improved quality control, and greater regulatory acceptance compared to crude botanical extracts. Advancements in extraction, purification, and analytical technologies have further enhanced the commercial production of high-value phytochemicals, enabling their incorporation into innovative formulations and solidifying their position as a rapidly expanding segment of the global herbal extracts market.

By Source: Flower-Derived Extracts Open a Premium Ingredient Frontier

Herbs and spices accounted for a 46.32% share of the herbal extracts market by source in 2025, driven by the extensive use of botanicals such as turmeric, ginger, cinnamon, black pepper, oregano, basil, rosemary, and thyme across the food, nutraceutical, pharmaceutical, and personal care industries. Increasing consumer preference for natural ingredients with scientifically validated health benefits has fueled demand for extracts rich in antioxidants, anti-inflammatory compounds, and bioactive phytochemicals. The growth of functional foods, herbal supplements, clean-label seasonings, and natural preservatives has further boosted the utilization of herb- and spice-derived extracts. Additionally, the rising focus on preventive healthcare and traditional medicinal practices has encouraged manufacturers to create value-added products featuring concentrated botanical extracts. Advancements in cultivation methods and extraction technologies have improved product quality, stability, and standardization, solidifying herbs and spices as a commercially significant source category in the global herbal extract market.

Flowers are projected to be the fastest-growing source in the herbal extracts market, with a CAGR of 8.64% through 2031. This growth is attributed to the increasing demand for botanical ingredients in cosmetics, personal care, functional beverages, dietary supplements, and natural wellness products. Extracts from flowers such as chamomile, hibiscus, lavender, calendula, elderflower, jasmine, and rose are highly valued for their antioxidant, soothing, anti-inflammatory, and aromatic properties, making them ideal for applications in skincare, haircare, relaxation products, herbal teas, and premium food items. The rising popularity of aromatherapy, natural beauty products, and plant-based wellness solutions has further driven demand for flower extracts. Manufacturers are increasingly incorporating floral botanicals into clean-label formulations to enhance product appeal through natural color, fragrance, and functional benefits while minimizing the use of synthetic ingredients. Growing consumer interest in holistic health, coupled with innovations in gentle extraction techniques that preserve delicate bioactive compounds and volatile aromas, continues to support the expansion of flower-sourced herbal extracts across various industries.

By Form: Powder's Formulation Utility Faces Liquid Innovation

Powder form accounted for 57.17% of the herbal extracts market by value in 2025, driven by its stability, extended shelf life, ease of transportation, and versatility across various end-use industries. These extracts are widely utilized in dietary supplements, functional foods, beverage premixes, pharmaceutical formulations, sports nutrition products, and cosmetics due to their precise dosing, high concentration of active compounds, and compatibility with dry formulations. Manufacturers prefer powdered extracts as they require less storage space, reduce transportation costs, and are less prone to microbial growth compared to liquid extracts. Technological advancements in spray drying, freeze drying, and encapsulation have further enhanced the retention of bioactive compounds, solubility, and product consistency. The growing consumer demand for convenient wellness products, such as capsules, tablets, sachets, and powdered drink mixes, continues to drive the adoption of powdered herbal extracts, positioning this segment as one of the largest and fastest-growing in the global herbal extract market.

The liquid form segment is expected to grow at a CAGR of 8.11% through 2031, attributed to its rapid absorption, high bioavailability, and ease of use in beverages, syrups, tinctures, oral drops, and liquid dietary supplements. Consumers increasingly favor liquid formulations for their convenience, particularly for children, older adults, and individuals who face challenges swallowing tablets or capsules. The food and beverage industry leverages liquid extracts to deliver natural flavors, colors, and functional ingredients in products such as juices, wellness shots, herbal drinks, and fortified beverages. Additionally, cosmetic and personal care manufacturers utilize liquid botanical extracts in creams, serums, shampoos, and topical formulations due to their ease of blending and consistent performance. Advances in extraction techniques, preservation technologies, and packaging solutions have improved the stability and shelf life of liquid herbal extracts, supporting their growing application across pharmaceutical, nutraceutical, food, beverage, and personal care industries.

By End Use: Pharmaceutical Anchor, Cosmetic Catalyst

Pharmaceuticals accounted for a 51.12% revenue share in 2025, driven by the growing demand for plant-derived active ingredients in preventive and therapeutic healthcare. Pharmaceutical companies are increasingly incorporating standardized herbal extracts into formulations targeting immune health, cardiovascular disorders, digestive health, metabolic conditions, respiratory ailments, and stress management. This trend is supported by the well-documented bioactive properties and favorable safety profiles of these extracts. Advances in scientific research validating the efficacy of botanical compounds, along with improvements in extraction and standardization technologies, have enhanced the consistency and quality of herbal ingredients for pharmaceutical applications. Additionally, factors such as the rising prevalence of chronic diseases, an aging global population, and growing consumer preference for complementary and integrative medicine are fostering the adoption of herbal-based medicines. Government initiatives promoting traditional medicine systems and stricter quality standards for botanical ingredients are further bolstering the role of herbal extracts in pharmaceutical product development, driving sustained growth in this segment.

The cosmetics and personal care segment is projected to record the fastest CAGR of 9.10% through 2031, reflecting strong growth in the herbal extract market. Consumers are increasingly seeking natural, plant-based ingredients that offer functional benefits and align with clean-label preferences. Herbal extracts are widely used in skincare, haircare, oral care, and beauty products due to their antioxidant, anti-inflammatory, antimicrobial, moisturizing, and soothing properties. These properties address concerns such as skin aging, acne, irritation, pigmentation, and scalp health. Botanicals like aloe vera, green tea, chamomile, calendula, lavender, rosemary, and licorice are progressively replacing synthetic ingredients in premium formulations. Rising consumer awareness about ingredient transparency, sustainability, and the potential side effects of harsh chemicals has prompted cosmetic manufacturers to expand their botanical-based product portfolios. Moreover, advancements in extraction technologies have enhanced the stability and efficacy of herbal ingredients, enabling their broader application in high-performance personal care formulations and supporting the continued growth of this segment within the global herbal extract market.

Geography Analysis

Asia-Pacific is both the world's largest botanical production hub and its fastest-growing consumption market, which held a 37.33% market share in 2025 and is expected to grow at a CAGR of 8.57% through 2031. The region's herbal extract market is expanding rapidly due to abundant botanical resources, traditional medicine systems, and increasing consumer awareness of natural healthcare solutions. Countries like China, India, Japan, and South Korea have long-standing traditions of using medicinal plants through systems such as Traditional Chinese Medicine and Ayurveda, establishing a strong foundation for herbal extract consumption. Rising disposable incomes, urbanization, and growing health consciousness are driving demand for herbal supplements, functional foods, beverages, pharmaceuticals, and botanical cosmetics. Additionally, Asia-Pacific is a major global supplier of medicinal herbs and plant-derived ingredients, supported by favorable climatic conditions, large-scale cultivation, and cost-effective manufacturing. Government initiatives promoting traditional medicine, increased research on botanical ingredients, and expanding export opportunities further solidify the region's position as a leading producer and consumer of herbal extracts.

The North American herbal extract market is fueled by strong consumer demand for natural health products, clean-label foods, dietary supplements, and plant-based personal care formulations. Rising awareness of preventive healthcare and the increasing prevalence of lifestyle-related diseases have encouraged consumers to integrate botanical ingredients into their wellness routines. The region's well-established nutraceutical, functional food, pharmaceutical, and cosmetic industries are expanding the use of standardized herbal extracts in products targeting immune health, cognitive function, digestive wellness, and healthy aging. Additionally, growing demand for organic and sustainably sourced ingredients, supported by transparent labeling practices, has led manufacturers to invest in high-quality herbal extract formulations. Continuous product innovation, advanced extraction technologies, and a strong regulatory focus on ingredient quality and safety are further driving market growth in the United States and Canada.

The herbal extract market in Europe, South America, and the Middle East & Africa is driven by increasing consumer preference for natural health products and the growing use of botanical ingredients in food, beverages, pharmaceuticals, and cosmetics. In Europe, stringent regulations promoting ingredient transparency, along with high demand for organic, clean-label, and scientifically validated botanical products, are fostering innovation in herbal extract formulations. South America leverages its rich biodiversity and abundant medicinal plant resources to develop herbal ingredients for both domestic consumption and export, creating opportunities for sustainable cultivation and value-added processing. In the Middle East & Africa, rising health awareness, growing adoption of traditional herbal remedies, expanding halal-certified wellness products, and investments in pharmaceutical and nutraceutical manufacturing are boosting demand for herbal extracts. Across these regions, ongoing research on botanical bioactives, advancements in extraction technologies, and a focus on sustainable sourcing are collectively supporting the long-term growth of the herbal extract market.

Competitive Landscape

The global herbal extract market is moderately consolidated, with competition distributed among large multinational ingredient manufacturers, specialized botanical extract producers, and numerous regional processors in the Asia-Pacific and South America. Market participants compete based on product quality, sourcing capabilities, extraction technologies, regulatory compliance, and their ability to deliver standardized botanical ingredients for applications in food, beverages, pharmaceuticals, nutraceuticals, and personal care. As customer demand increasingly favors traceable and sustainable botanical ingredients, companies are differentiating themselves by investing in vertically integrated supply chains. These investments provide greater control over cultivation, harvesting, extraction, and quality assurance while mitigating risks associated with raw material supply.

A significant competitive trend in the market is the expansion of integrated botanical platforms through acquisitions, strategic partnerships, and business restructuring. Companies are enhancing their portfolios by combining botanical sourcing, standardized herbal extracts, formulation expertise, and finished product development within a unified operational framework. This integrated approach allows manufacturers to offer end-to-end solutions, reduce product development timelines, improve customer collaboration, and strengthen long-term commercial relationships. Concurrently, increased investments in sustainable cultivation practices, certified sourcing programs, and advanced extraction technologies are enabling suppliers to meet growing customer demands for transparency, ingredient consistency, and environmental responsibility.

Innovation is emerging as a critical factor in market differentiation, particularly in precision extraction, botanical authentication, and clinically validated herbal ingredients. Manufacturers are adopting advanced technologies such as supercritical fluid extraction, artificial intelligence-assisted process optimization, molecular fingerprinting, and real-time analytical testing to enhance extract purity, standardization, and traceability. Additionally, stricter global quality regulations and a growing focus on pharmacopoeial-grade botanical ingredients are driving suppliers to strengthen their analytical capabilities and regulatory compliance. Ongoing research into novel delivery systems that improve the bioavailability and stability of herbal compounds is also creating opportunities for product differentiation. These advancements position technology-driven innovation and scientific validation as key factors influencing long-term competition in the herbal extract market.

Herbal Extract Industry Leaders

-

Symrise AG

-

Synthite Industries Pvt. Ltd.

-

MartinBauer

-

Döhler GmbH

-

Kalsec Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: MartinBauer Nutraceuticals launched AnnurTriComplex® at Vitafoods Europe 2026, a clinically backed hair growth complex sourced from Protected Geographical Indication (PGI)-certified Annurca apples (Melannurca Campana) from Campania, Italy. Pre-clinical and in vivo studies demonstrated enhanced hair follicle activity and keratin synthesis

- March 2026: MartinBauer united its Finzelberg and MB-Med entities under a new, dedicated Nutraceutical Unit, creating a single botanical platform with stated intent to expand capabilities in functional foods, supplements, personalized nutrition, and precision formulations, with targeted geographic expansion in North America and Asia-Pacific.

- October 2025: MartinBauer acquired American Botanicals, a leading U.S. supplier of wildcrafted botanical ingredients with a 33,000-acre Appalachian sourcing footprint and longstanding grower partnerships. The acquisition extended MartinBauer's North American agricultural supply chain and deepened its portfolio of sustainably wildcrafted herbs and spices.

Global Herbal Extract Market Report Scope

| Essential Oils |

| Standardized Dry Extracts |

| Oleoresins |

| Phytochemicals and Isolates |

| Herbs and Spices |

| Flowers |

| Fruits and Vegetables |

| Others |

| Powder |

| Liquid |

| Pharmaceuticals |

| Dietary Supplements |

| Food and Beverages |

| Cosmetics and Personal Care |

| Animal Feed and Veterinary Care |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Rest of Middle East and Africa |

| By Product Type | Essential Oils | |

| Standardized Dry Extracts | ||

| Oleoresins | ||

| Phytochemicals and Isolates | ||

| By Source | Herbs and Spices | |

| Flowers | ||

| Fruits and Vegetables | ||

| Others | ||

| By Form | Powder | |

| Liquid | ||

| By End Use | Pharmaceuticals | |

| Dietary Supplements | ||

| Food and Beverages | ||

| Cosmetics and Personal Care | ||

| Animal Feed and Veterinary Care | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the herbal extracts sector in 2026 and where is it headed by 2031?

The herbal extracts market is valued at USD 17.52 billion in 2026 and is projected to reach USD 25.43 billion by 2031 at a 7.74% CAGR.

Which product type leads global demand for herbal extracts?

Essential oils led in 2025 with 44.64% revenue share because they are widely used across flavor, fragrance, topical, and pharmaceutical-support applications.

Which end-use category is growing the fastest for botanical extracts?

Cosmetics and personal care is the fastest-growing end-use segment and is projected to expand at 9.10% CAGR through 2031 as clean-beauty reformulation gains pace.

What is driving higher demand for flower-based extracts?

Flowers are projected to grow at 8.64% CAGR through 2031 as beverage, fragrance, and cosmetic formulators seek differentiated botanical inputs such as lavender, chamomile, rose, and butterfly pea.

Page last updated on: