Vegetable Extracts Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

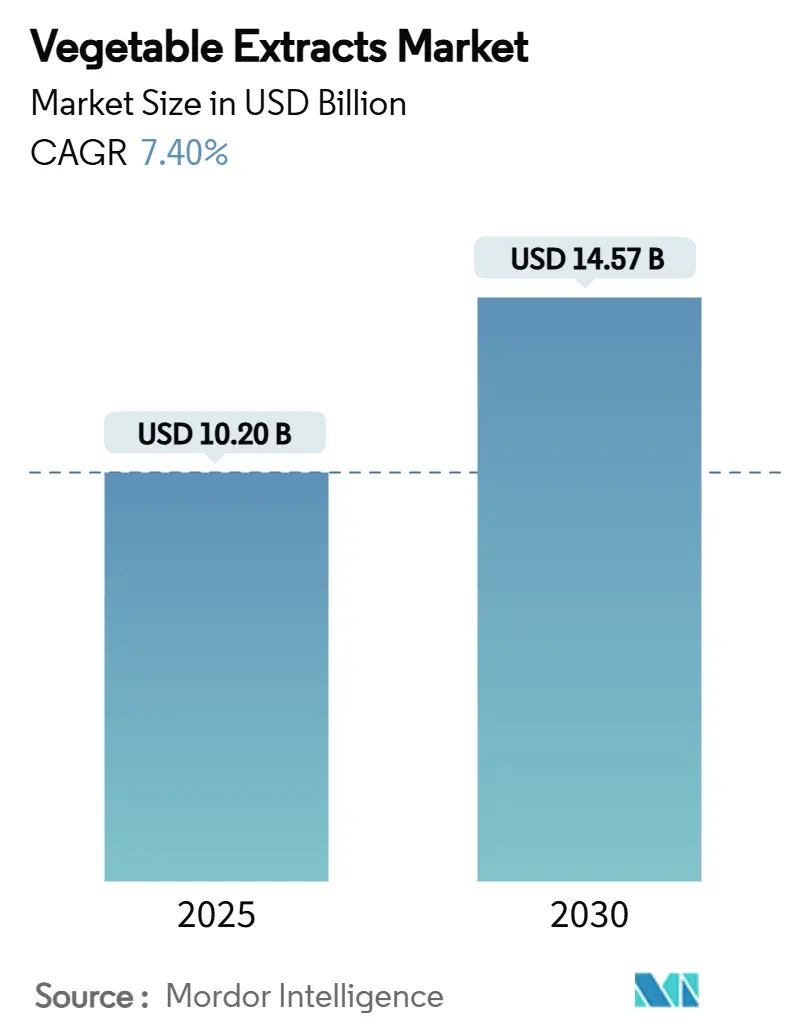

| Market Size (2025) | USD 10.20 Billion |

| Market Size (2030) | USD 14.57 Billion |

| Growth Rate (2025 - 2030) | 7.40% CAGR |

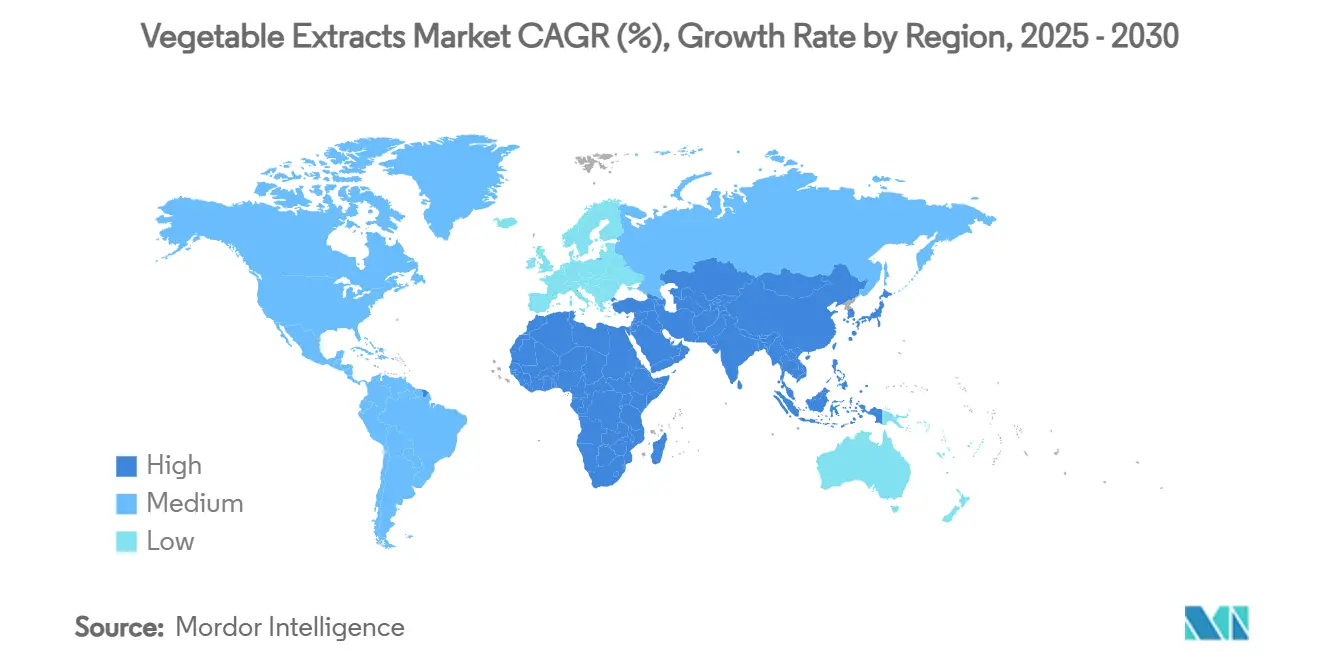

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Vegetable Extracts Market Analysis by Mordor Intelligence

The vegetable extracts market size reached USD 10.2 billion in 2025 and is forecast to grow at a 7.40% CAGR to USD 14.57 billion by 2030. This expansion rests on sustained demand for clean-label ingredients, regulatory moves away from synthetic additives, and cost reductions achieved through supercritical CO₂ and microwave-assisted extraction technologies. Consumer health consciousness, the rise of functional foods, and steady innovations in green processing methods together nourish a virtuous cycle of product development and market acceptance. Producers are reinvesting the resulting margin gains in R&D, thereby accelerating the pace at which niche botanicals progress from academic discovery to commercial launch. Although raw material cost volatility and complex approval pathways pose headwinds, suppliers able to secure diversified sourcing and maintain regulatory fluency continue to capture incremental market share within the vegetable extracts market.

Key Report Takeaways

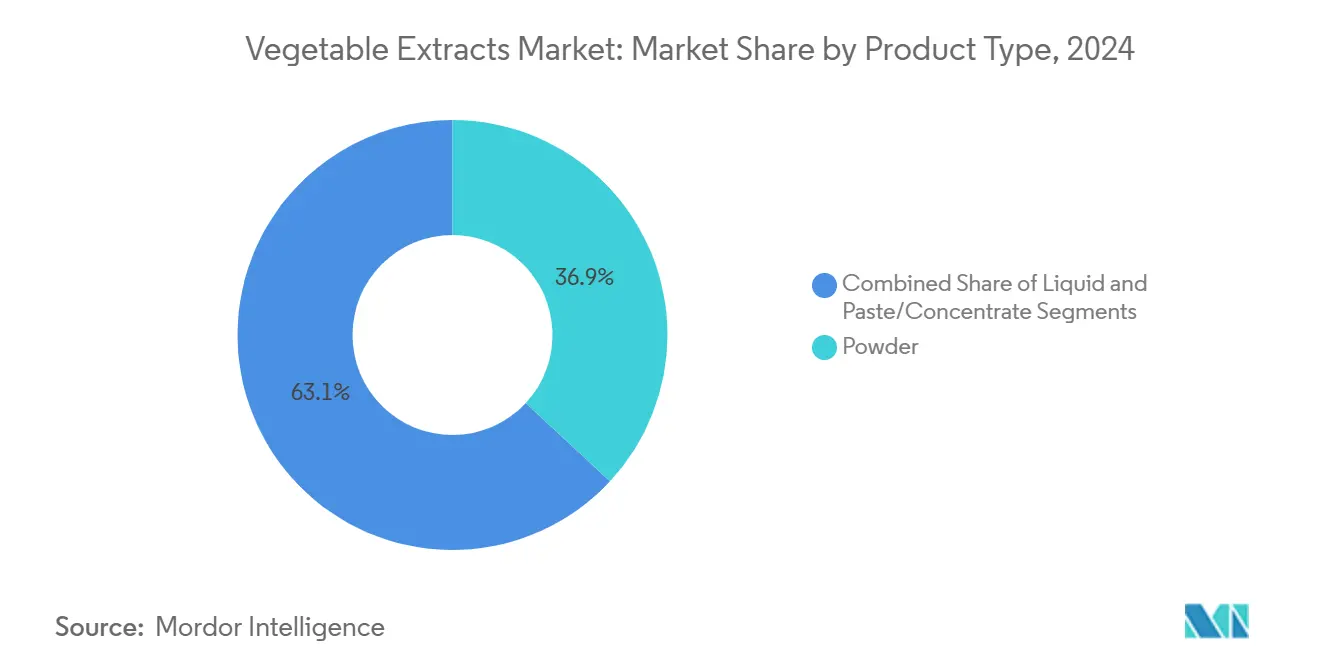

- By product type, powder formulations accounted for 37.28% of the vegetable extracts market share in 2024, while liquid extracts are projected to expand at an 8.48% CAGR through 2030.

- By source, leafy greens commanded 27.19% of the vegetable extracts market size in 2024; brassicas are forecast to post a 9.26% CAGR to 2030.

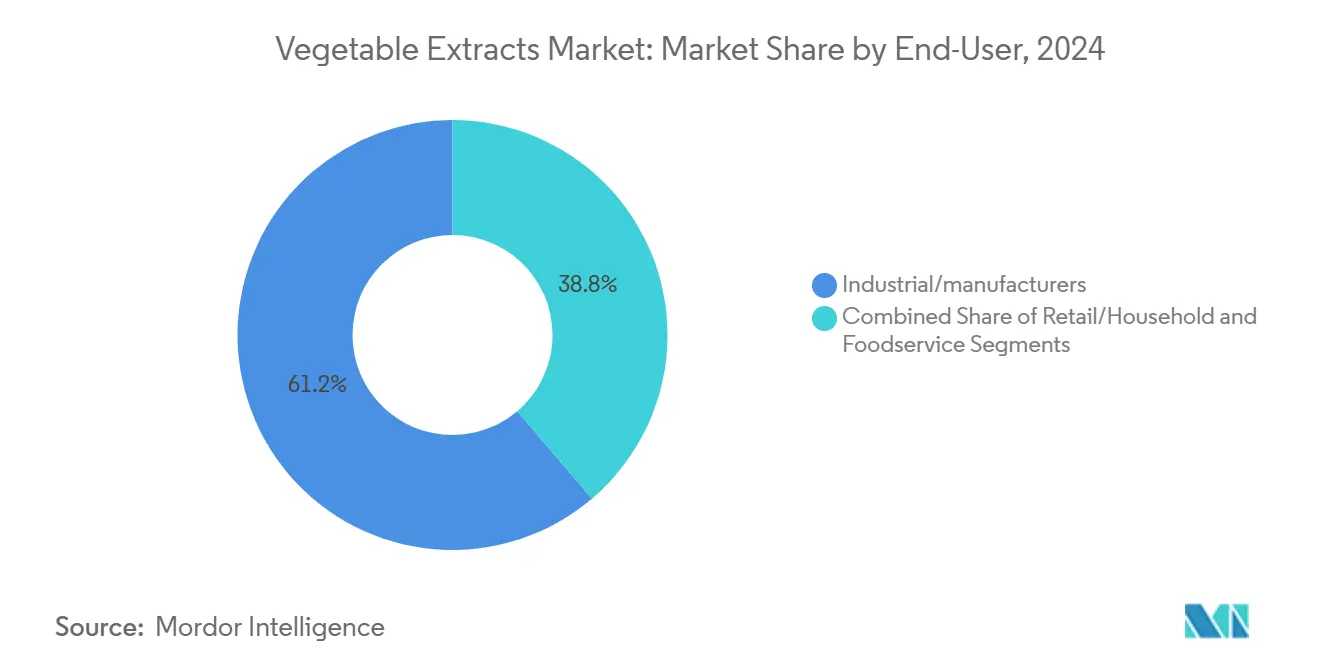

- By end-user, industrial and manufacturing applications led with a 61.84% share in 2024, whereas retail and household demand is advancing at a 9.71% CAGR between 2025 and 2030.

- By geography, Asia-Pacific held 33.07% of the vegetable extracts market in 2024; Africa is poised for a 10.18% CAGR over the forecast period.

Global Vegetable Extracts Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for clean-label ingredients | +1.8% | Global, with strongest adoption in North America & EU | Medium term (2-4 years) |

| Increasing health consciousness & functional foods | +1.5% | Global, led by developed markets, expanding to APAC | Long term (≥ 4 years) |

| Growth of nutraceutical & dietary supplement sector | +1.2% | North America, Europe, Asia-Pacific core markets | Long term (≥ 4 years) |

| Expansion of natural cosmetics & personal care | +0.9% | Global, with premium market focus in EU & North America | Medium term (2-4 years) |

| Surplus vegetable waste upcycling in circular supply chains | +0.7% | EU leading, expanding to North America & developed APAC | Medium term (2-4 years) |

| Green extraction tech lowering cost (supercritical CO₂, microwave) | +0.6% | Global, with early adoption in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising demand for clean-label ingredients

In the U.S., a significant 94% of consumers advocate for more fresh produce in restaurants, a sentiment echoed by 91% of restaurant operators. This growing preference isn't limited to foodservice; it's making waves in the packaged goods sector. Manufacturers are under increasing pressure to reformulate their products with ingredients that consumers can easily recognize. The FDA's recent withdrawal of authorization for FD&C Red 3, coupled with state-level bans on artificial dyes—most notably led by California—are hastening the industry's pivot towards natural alternatives[1]Burton, Norah. "What's driving the move to natural colors in the US?" Oterra, March 5, 2025. https://oterra.com/article/whats-driving-the-move-to-natural-colors-in-the-us. Across the Atlantic, European consumers are even more vocal about their preference for clean labels. As a result, food producers are transitioning from synthetic to natural food colorings, not just to align with regulatory mandates but also to cater to consumer demands. The financial implications are significant: brands that embrace natural ingredients not only enjoy premium pricing but also cultivate deeper consumer loyalty, giving them a competitive edge in the market.

Increasing health consciousness and functional foods

The convergence of aging demographics with preventive healthcare awareness has transformed vegetable extracts from commodity ingredients into targeted wellness solutions. Microgreens markets are expanding at 7-9% CAGR, driven by concentrated bioactive compound profiles that deliver measurable health benefits in smaller serving sizes[2]Aftab, A., Haider, M., Ali, Q., and Malik, A. "Revealing the power of green leafy vegetables: Cultivating diversity for health, environmental benefits, and sustainability." ScienceDirect, December 1, 2024. https://www.sciencedirect.com/science/article/pii/S2211912424000786. Brassicaceae vegetables, particularly broccoli and kale, have gained scientific validation for their glucosinolate content, which converts to isothiocyanates linked to cancer protection and cognitive function improvement.. The European nutraceutical market's projected growth from USD 83 billion in 2025 to USD 111.83 billion by 2030 reflects this trend, with countries like Italy showing 80% supplement consumption rates among the population.[3]Berry, Francesca. "A country-by-country blueprint for nutraceutical success in Europe." Informa Markets, May 20, 2025. https://www.nutritionaloutlook.com/view/a-country-by-country-blueprint-for-nutraceutical-success-in-europe This creates sustained demand for standardized, bioactive-rich vegetable extracts that can deliver consistent therapeutic benefits across diverse product formulations.

Growth of nutraceutical & dietary supplement sector

As the nutraceutical industry matures, supply chains are evolving, now emphasizing bioavailability and therapeutic efficacy over mere nutritional content. From 2021 to 2022, patent activity in Lamiaceae bioactives surged, signaling a heightened commercial interest in plant-derived compounds, particularly for applications in metabolic health, anti-aging, and cognitive functions. Innovations from Japan, such as TIME TRAVELER's parsley-derived exosome supplements, underscore the industry's shift towards advanced delivery mechanisms. Each capsule boasts 50 billion exosomes, specifically targeting aging support. Reflecting this technological evolution, the Asia-Pacific nutraceuticals market is projected to hit USD 34.68 billion by 2030. Notably, companies like Barentz are making strategic moves, exemplified by their acquisition of China's Fengli Group, to tap into specialized extraction capabilities and gain insights into the local market.

Expansion of natural cosmetics & personal care

In the beauty industry, the use of botanical ingredients is not just a marketing gimmick; it's a response to the genuine efficacy demands of informed consumers. Givaudan's push for vegan botanical extracts in cosmetics underscores a commitment to sustainability and natural origins, highlighting a blend of environmental awareness and performance demands. Fermentation technologies are boosting the stability and bioavailability of plant-based cosmetic ingredients. For instance, patented formulations like FERMENZA showcase superior antimicrobial and antioxidant properties over traditional extracts. The natural food preservatives show evident potential for vegetable extracts to serve both cosmetic and preservation roles. This dual capability paves the way for suppliers to command premium prices, provided they meet both aesthetic and functional performance benchmarks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material cost volatility | -1.1% | Global, with acute impact in import-dependent regions | Short term (≤ 2 years) |

| Regulatory approval & labeling complexity | -0.8% | EU & North America leading, expanding globally | Medium term (2-4 years) |

| Limited heat stability in high-temp processes | -0.6% | Global manufacturing, particularly processed foods | Long term (≥ 4 years) |

| Competition from bio-identical precision-fermentation compounds | -0.4% | Developed markets with advanced biotech capabilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-material cost volatility

Climate change and geopolitical tensions have intensified traditional seasonal fluctuations, leading to unprecedented volatility in vegetable raw material pricing. In 2025, a 25% tariff on Mexican imports, crucial for US winter vegetables, exerted immediate cost pressures on extraction facilities reliant on steady feedstock. Complicating matters, the Chinese herbal market faces tariffs soaring to 35-45%, and a new centralized procurement program may restrict international access. Over the past five years, the vegetable sector grappled with extreme weather and escalating costs, curbing global production growth to a mere 1.2% annually, even as trade expanded by 3% each year. This unpredictability has compelled manufacturers to hold larger inventories and adopt advanced hedging strategies, straining working capital and complicating operations.

Regulatory approval & labeling complexity

Botanical ingredients now navigate a labyrinthine regulatory landscape, where divergent approval pathways lead to market fragmentation and heightened compliance costs. Under the EU's Novel Foods Regulation (2015/2283), ingredients without a pre-1997 usage history face stringent safety assessments, often stretching approval timelines beyond 18 months. Meanwhile, the FDA's potential move to abolish self-affirmed GRAS pathways injects uncertainty into U.S. market strategies, possibly steering new ingredients towards pricier FDA-notified alternatives. Adding to the complexity, European Member States exhibit inconsistent regulations; some have set up independent approval processes that clash with the overarching EU framework. Such regulatory disparities not only inflate market entry costs but also favor established players with prior approvals, stifling innovation from smaller extraction firms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Liquid Forms Drive Innovation

In 2024, powder formulations held a 37.28% share of the market, thanks to their advantages in shelf stability, transportation efficiency, and versatility across various food applications. Meanwhile, liquid extracts are on a rapid ascent, boasting an 8.48% CAGR from 2025 to 2030, fueled by their superior bioavailability and the rising trend of direct-to-consumer sales. Paste and concentrate forms, with their high potency and controlled release features, carve out specialized niches in industrial applications, commanding premium pricing.

Technological strides in stabilization and preservation are reshaping the landscape, addressing the limitations of yesteryears. A case in point: Newcastle University has pioneered reusable biocatalysts for producing flavor esters without solvents, underscoring the innovations bolstering liquid extract efficiencies. While powder formats reign supreme in bakeries—prioritizing moisture control and shelf longevity—liquid extracts are making waves in beverages and supplements, where quick absorption and sensory allure captivate consumers.

By Source Vegetable: Brassicas Challenge Leafy Green Dominance

In 2024, leafy greens commanded a dominant market share of 27.19%, buoyed by robust supply chains and the well-recognized nutritional benefits of staples like spinach, kale, and niche microgreens. Meanwhile, brassicas are on the rise, boasting a 9.26% CAGR through 2030, thanks to increasing scientific endorsement of their glucosinolate compounds and the resultant bioactive isothiocyanates. Nightshades, along with roots and tubers, find their niche in the natural coloring and functional ingredient sectors. At the same time, the "Others" category is making waves with new botanical sources and innovative extraction targets.

The tug-of-war between leafy greens and brassicas underscores a shift in consumer awareness and scientific insights. Recent studies spotlighting 16 glucosinolates and 7 volatile breakdown products in Brassicaceae baby leafy greens have amplified their market value, transcending conventional nutritional assessments. Varieties like red cabbage and purple broccoli, rich in anthocyanins, not only serve as natural colorants but also as health-enhancing ingredients, paving the way for premium market positioning. While leafy greens benefit from established processing systems and consumer recognition, the enhanced bioactive profile of brassicas sets them on a fast track for adoption in lucrative nutraceutical markets.

By End-User: Retail Segment Disrupts Industrial Dominance

Industrial and manufacturing applications dominated with 61.84% market share in 2024, encompassing food & beverages, nutraceuticals & supplements, cosmetics & personal care, pharmaceuticals, and animal nutrition sectors. The retail and household segment, while smaller in absolute terms, demonstrates the highest growth trajectory at 9.71% CAGR for 2025-2030, reflecting direct-to-consumer trends and increased home cooking sophistication. Foodservice applications occupy a middle position, benefiting from the restaurant industry recovery and consumer demand for fresh, natural ingredients in dining experiences.

The retail segment's acceleration reflects fundamental shifts in consumer behavior and product accessibility. The 94% consumer preference for restaurants featuring more fresh produce indicates underlying demand that extends to home consumption patterns. Industrial applications maintain scale advantages and established procurement relationships, but face margin pressure from increasing raw material costs and regulatory compliance requirements. Foodservice recovery creates opportunities for specialized extract formulations that deliver consistent flavor profiles and nutritional benefits across varying preparation methods, while retail growth enables premium pricing for consumer-facing products with clear health positioning and convenience benefits.

Geography Analysis

In 2024, Asia-Pacific commanded a dominant 33.07% share of the market, capitalizing on its well-established botanical extraction infrastructure, supportive regulations for traditional ingredients, and easy access to a variety of vegetable sources. Herbalife's investment in a botanical extraction facility in Changsha, China, underscores the region's manufacturing prowess and market accessibility. With an outlay of USD 28-33 million, the facility processes a substantial 8,000 metric tons annually. Ingredion's USD 140 million bet on plant-based protein production in Asia-Pacific underscores the region's promising growth trajectory.

Meanwhile, Africa is set to be the region with the most rapid growth, boasting a projected 10.18% CAGR from 2025 to 2030. This surge is fueled by the industrialization of food processing, an uptick in consumer purchasing power, and proactive government measures aimed at enhancing agricultural value. Highlighting Africa's burgeoning potential, Nigeria stands out as the continent's largest food market. Contributing 22.5% to the manufacturing sector's value and accounting for 4.6% of the GDP, Nigeria's growth is propelled by urbanization and a burgeoning middle class, both driving the demand for processed foods. Simultaneously, Africa's push towards agricultural transformation hints at a bright future, especially in bolstering local extraction capacities.

North America and Europe showcase stable demand patterns, indicative of their maturity in the market. In contrast, South America and the Middle East exhibit moderate growth potential, albeit hampered by infrastructural challenges and regulatory ambiguities.

Competitive Landscape

The vegetable extracts market, with a concentration index of 4 out of 10, showcases moderate fragmentation. This balance allows both multinational ingredient suppliers and specialized extraction companies to vie for market share. While market leaders capitalize on scale advantages in procurement and distribution, smaller entities carve out niches through proprietary extraction technologies, organic certifications, and unique botanical sources.

A notable trend is the emphasis on vertical integration; for instance, Givaudan has made strides by investing in sustainable sourcing programs, ensuring that 85% of its natural portfolio is channeled through responsible means. Consolidation activities underscore the industry's maturation and the pressing need for technological convergence. A prime example is the Axxence-Natural Advantage merger, which birthed a EUR 60 million revenue entity boasting a global footprint in 45 countries. This move highlights how mid-tier players can scale up through strategic alliances.

Furthermore, a spike in patent activity from 2021-2022, especially concerning Lamiaceae bioactives in functional food innovation, points to a burgeoning R&D competition and a keen focus on intellectual property. Emerging avenues like precision fermentation, cellular agriculture, and waste-to-value extraction technologies present lucrative opportunities, promising cost benefits while aligning with sustainability goals.

Vegetable Extracts Industry Leaders

-

Givaudan S.A

-

Döhler

-

Sensient Technologies

-

International Flavors & Fragrances Inc.

-

Symrise

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Probi®, a global leader in probiotics, has teamed up with Nomura Dairy Products to introduce its flagship strain to Japan. The collaboration has birthed the nation's inaugural fermented drink, enhanced with LP299V®. This novel beverage melds the inherent advantages of carrot juice with the established digestive benefits of LP299V. This launch not only signifies a pivotal advancement for Probi in the Asian market but also brings scientifically validated gut health solutions to the forefront for Japanese consumers.

- July 2024: Deerland Enzymes & Probiotics, a global leader in enzyme and probiotic dietary supplements, unveiled its latest branded offering, Solarplast. Solarplast, derived from organic dark leafy greens, undergoes a unique enzymatic enhancement through a proprietary manufacturing process. Harnessing the power of chloroplasts from these greens, Solarplast emerges as a potent source of molecular chaperones and antioxidants, all enveloped in a naturally occurring lipid protective coating.

Global Vegetable Extracts Market Report Scope

| Powder |

| Liquid |

| Paste/Concentrate |

| Leafy Greens |

| Roots & Tubers |

| Nightshades |

| Brassicas |

| Others |

| Foodservice | |

| Industrial/Manufacturers | Food & Beverages |

| Nutraceuticals & Supplements | |

| Cosmetics & Personal Care | |

| Pharmaceuticals | |

| Animal Nutrition | |

| Retail/Household |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Iran | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Powder | |

| Liquid | ||

| Paste/Concentrate | ||

| By Source Vegetable | Leafy Greens | |

| Roots & Tubers | ||

| Nightshades | ||

| Brassicas | ||

| Others | ||

| By End-User | Foodservice | |

| Industrial/Manufacturers | Food & Beverages | |

| Nutraceuticals & Supplements | ||

| Cosmetics & Personal Care | ||

| Pharmaceuticals | ||

| Animal Nutrition | ||

| Retail/Household | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Iran | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is the vegetable extracts market expected to grow to 2030?

It is projected to log a 7.40% CAGR, climbing from USD 10.2 billion in 2025 to USD 14.57 billion by 2030.

Which region currently leads global demand for vegetable-derived extracts?

Asia-Pacific holds the largest share at 33.07%, supported by mature extraction infrastructure and botanical heritage.

What product form shows the strongest momentum?

Liquid extracts are on track for an 8.48% CAGR through 2030 thanks to better bioavailability and consumer convenience.

Why are brassica vegetables gaining popularity in extraction?

Scientific validation of glucosinolates and dual roles as natural colorants lift brassica extracts ahead of leafy green incumbents.

What is the biggest regulatory hurdle for new plant extracts in Europe?

Ingredients without a pre-1997 history must undergo the EU Novel Foods approval process, which can exceed 18 months.

Page last updated on: