North America Food Antimicrobial And Antioxidants Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

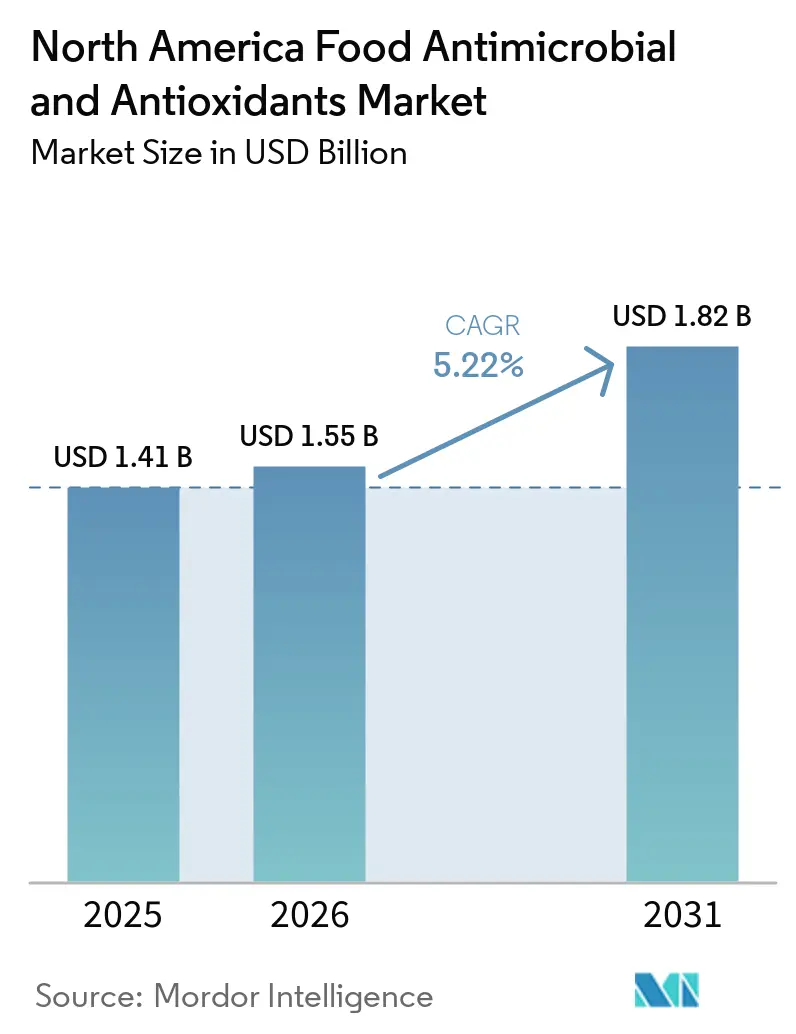

| Base Year Market Size (2025) | USD 1.41 Billion |

| Market Size (2026) | USD 1.55 Billion |

| Market Size (2031) | USD 1.82 Billion |

| Growth Rate (2026 - 2031) | 5.22% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Food Antimicrobial And Antioxidants Market Analysis by Mordor Intelligence

The North America food antioxidants and antimicrobials market size is projected to be USD 1.55 billion in 2026 from USD 1.41 billion in 2025, and is expected to reach USD 1.82 billion by 2031, growing at a 5.22% CAGR from 2026 to 2031. Structural shifts away from legacy synthetics toward fermentation-derived and plant-based solutions are accelerating as California-style additive bans ripple across the region and multinational brands embed clean-label guardrails into new-product briefs. Natural antioxidants, principally tocopherols, ascorbic acid, citric acid, and rosemary extract, are displacing BHA, BHT, propyl gallate, and TBHQ in industrial bakery, meat, and dairy formulations because they satisfy both safety perceptions and simpler label declarations. Ingredient suppliers are responding with encapsulation, enzyme-assisted extraction, and precision-fermentation platforms that raise heat stability, solubility, and supply security. Meanwhile, natural antimicrobials such as lactic acid, nisin, and natamycin are gaining ground as processors seek dual-function systems that control rancidity and microbial spoilage with one ingredient set. Tightening regulations, rising e-commerce distribution windows, and the surge of plant-based meat analogs collectively underpin robust demand for clean-label shelf-life solutions throughout the forecast horizon.

Key Report Takeaways

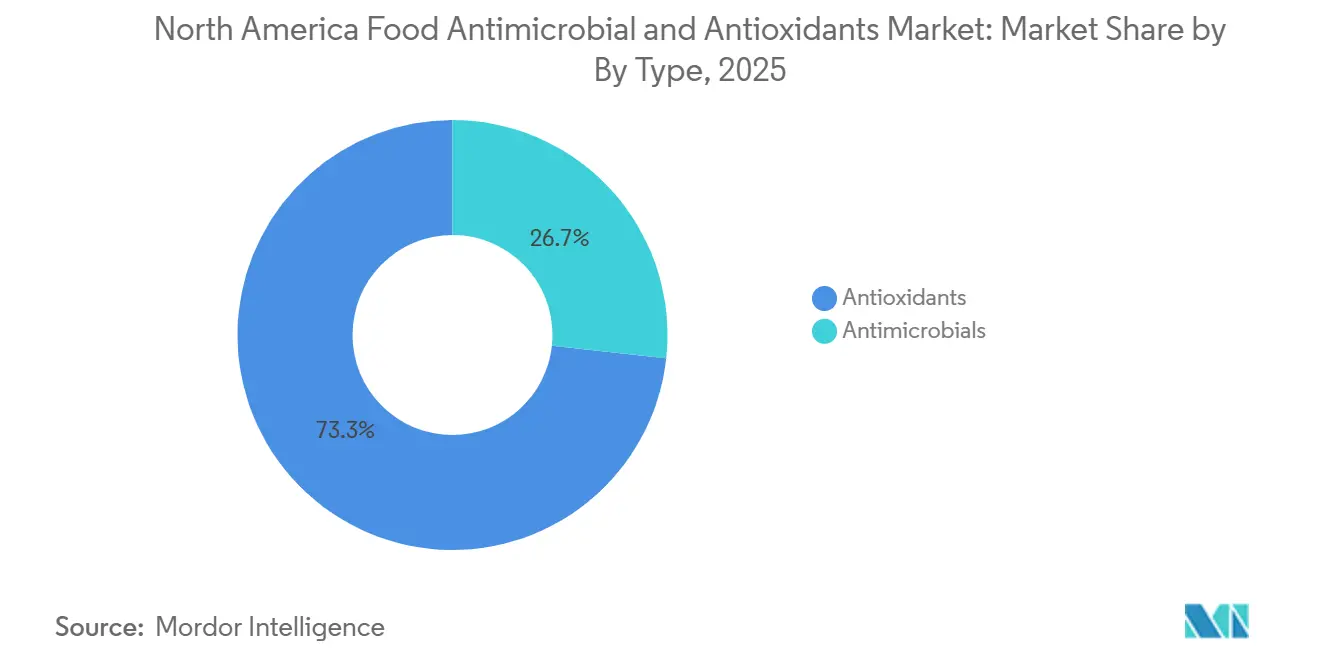

- By type, antioxidants held 73.28% of the North America food antioxidants and antimicrobials market share in 2025, whereas antimicrobials are advancing at a 7.12% CAGR to 2031.

- By source, plant extracts contributed 48.21% to the North America food antioxidants and antimicrobials market size in 2025, but algae-based alternatives are expanding at an 8.02% CAGR through 2031.

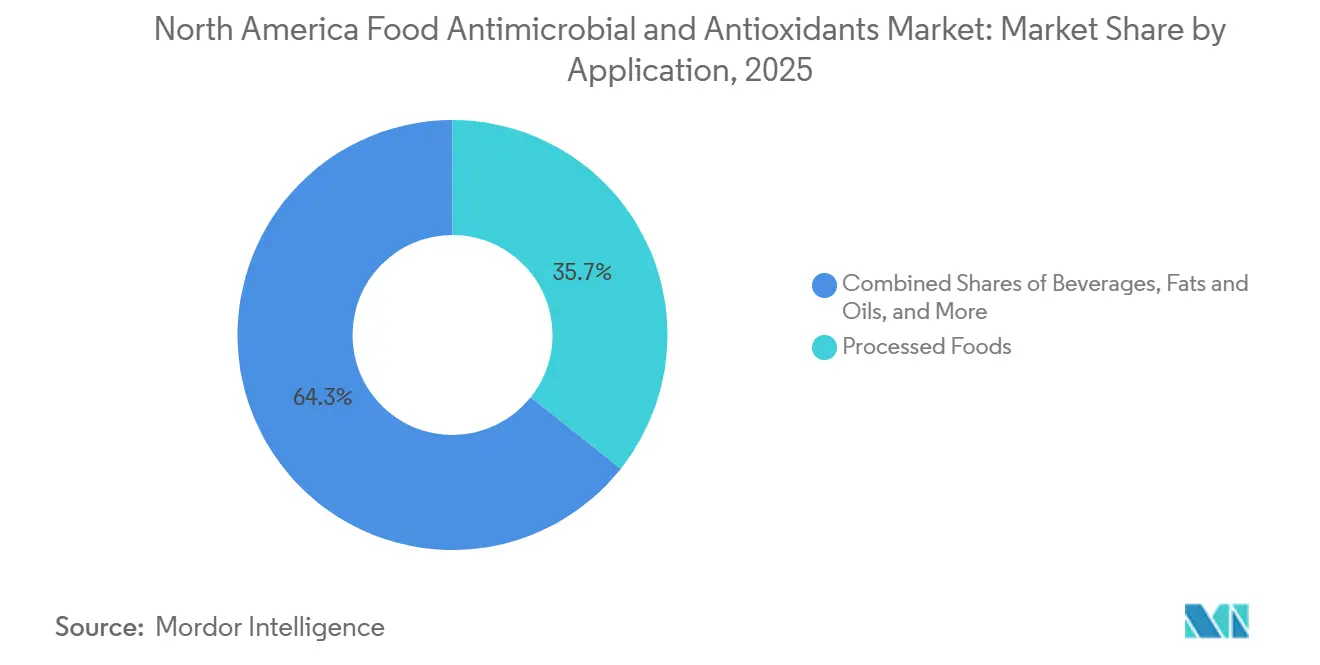

- By application, processed foods commanded 35.68% of the North America food antioxidants and antimicrobials market size in 2025, while beverages are forecast to rise at a 6.68% CAGR to 2031.

- By geography, the United States captured 69.38% revenue in 2025, and Mexico is set to grow at a 7.38% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Food Antimicrobial And Antioxidants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Processed and Convenience Food Requiring Extended Shelf-Life | +1.2% | United States, Canada, Mexico | Medium term (2-4 years) |

| Regulatory Approvals Widening Antioxidant Usage Across Emerging Markets | +0.8% | United States, Canada, Mexico (COFEPRIS alignment) | Short term (≤ 2 years) |

| Growing Functional Food And Nutraceutical Launches Formulated With Antioxidants | +0.9% | United States, Canada | Medium term (2-4 years) |

| Rising Awareness About Oxidative Stress And Age‑Related Disorders | +0.6% | North America (consumer health focus) | Long term (≥ 4 years) |

| Growing Innovations In Food Processing And Antioxidant Formulations | +0.7% | United States, Canada (R&D hubs) | Medium term (2-4 years) |

| Rising Consumer Demand For Natural Antioxidants In Clean‑Label Foods | +1.3% | United States, Canada, Mexico | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion of Processed and Convenience Food Requiring Extended Shelf-Life

Processed food consumption in the United States reached 58% of total caloric intake in 2024, with ultra-processed categories, ready meals, packaged snacks, and shelf-stable bakery, accounting for the majority of antioxidant and antimicrobial demand, according to the USDA Economic Research Service[1]Source: U.S. Department of Agriculture Economic Research Service, “Processed Food Consumption Data,” ERS.usda.gov. Shelf-life extension requirements have intensified as e-commerce grocery penetration crossed 12% of total food retail in 2025, necessitating formulations that withstand temperature fluctuations during last-mile delivery and maintain sensory attributes over extended distribution windows. Natural antioxidants such as rosemary extract and mixed tocopherols are displacing synthetic alternatives in meat and poultry applications, where lipid oxidation directly impacts color stability and off-flavor development; a 2025 peer-reviewed study demonstrated that rosemary extract at 0.1% concentration extended the shelf life of omega-3-enriched margarine by 40% compared to BHA controls. The proliferation of plant-based meat analogs, projected to exceed USD 3 billion in North American sales by 2027, has created acute demand for antioxidant systems that protect polyunsaturated fatty acids from oxidative rancidity without imparting off-notes, driving innovation in encapsulated tocopherol and citric acid blends. Convenience food manufacturers are increasingly adopting dual-function preservative systems that combine antioxidants with organic acid antimicrobials, reducing ingredient declaration complexity and aligning with clean-label mandates while achieving target shelf-life benchmarks of 90-180 days for refrigerated prepared meals.

Regulatory Approvals Widening Antioxidant Usage Across Emerging Markets

Health Canada's December 2025 proposal to authorize rosemary extract as a food additive represents a watershed moment for botanical antioxidants in North America, as it establishes a regulatory precedent that could accelerate approvals for green tea extract, grape seed polyphenols, and other phenolic compounds currently restricted to GRAS self-affirmation pathways. The FDA issued a GRAS notice acknowledgment in 2025 for glycolipid-based antimicrobials derived from microbial fermentation, expanding the toolkit for natural preservation beyond conventional organic acids and signaling regulatory receptivity to biotechnology-enabled ingredients[2]Source: FDA Center for Food Safety, “GRAS Notices,” FDA.gov. Mexico's COFEPRIS has harmonized its food additive approval framework with Codex Alimentarius standards, reducing approval timelines from 24 months to 12-15 months for natural antioxidants with established safety dossiers in the U.S. or EU, thereby lowering market-entry barriers for ingredient suppliers targeting the Mexican processed food sector. The FDA's 21 CFR Part 172 regulations specify maximum use levels for synthetic antioxidants—200 ppm for BHA and BHT in fats and oils—but impose no quantitative limits on GRAS-affirmed natural antioxidants such as ascorbic acid and tocopherols, creating a regulatory arbitrage opportunity that favors botanical and fermentation-derived solutions. This regulatory divergence is reshaping product portfolios, as multinational ingredient suppliers prioritize R&D investments in natural antioxidant platforms that can secure approvals across North American jurisdictions without triggering the pre-market notification requirements that apply to novel synthetic compounds.

Growing Functional Food and Nutraceutical Launches Formulated with Antioxidants

Functional food launches incorporating antioxidants surged 34% year-over-year in North America during 2024-2025, with immune health and cognitive function positioning driving formulation strategies that combine tocopherols, ascorbic acid, and polyphenolic extracts with probiotics and omega-3 fatty acids. The infant and clinical nutrition segment has emerged as a high-value application for antioxidants, as FDA regulations under 21 CFR Part 107 mandate minimum levels of vitamin E (tocopherols) and vitamin C (ascorbic acid) in infant formula to prevent oxidative degradation of lipids and ensure nutrient stability throughout shelf life, FDA 21 CFR 107. DSM-Firmenich launched Dry Vit A Palmitate for Early Life Nutrition in 2025, a clean-label vitamin A ingredient stabilized exclusively with mixed tocopherols, addressing parental concerns about synthetic antioxidants in infant products. A survey cited by the company found 67% of parents prioritize minimal additive use in baby food. Nutraceutical brands are leveraging antioxidant health claims permitted under the FDA's structure-function claim framework, with products emphasizing "cellular protection" and "free radical defense" proliferating in sports nutrition and active aging categories. The convergence of functional food and clean-label trends has created demand for antioxidant blends that deliver both technological functionality, preventing lipid oxidation, and bioactive health benefits, exemplified by formulations combining rosemary extract for shelf-life extension with astaxanthin for its purported anti-inflammatory properties. This dual-purpose positioning allows manufacturers to command premium pricing while satisfying both food technologists and marketing teams seeking differentiation in crowded supplement and functional beverage markets.

Rising Awareness About Oxidative Stress and Age-Related Disorders

Consumer awareness of oxidative stress as a contributor to cardiovascular disease, neurodegenerative disorders, and metabolic syndrome has escalated, fueled by health advocacy campaigns and clinical research linking dietary antioxidants to reduced disease risk. A 2025 Nature Medicine review synthesized evidence from longitudinal cohort studies demonstrating that diets rich in polyphenolic antioxidants, found in berries, green tea, and dark chocolate, correlate with 15-20% lower incidence of age-related cognitive decline among adults over 60. This epidemiological evidence has translated into commercial opportunity, as food and beverage brands incorporate antioxidant-rich ingredients into products targeting aging consumers, with "brain health" and "heart health" positioning becoming ubiquitous in functional snack and beverage categories. The U.S. National Institutes of Health's ongoing research into the role of reactive oxygen species in chronic disease progression has lent scientific credibility to antioxidant supplementation, driving demand for high-ORAC (oxygen radical absorbance capacity) ingredients such as acai, blueberry, and pomegranate extracts in nutraceutical formulations. Pharmaceutical-grade antioxidants are gaining traction in clinical nutrition applications, where oxidative stress management is critical for patients undergoing chemotherapy or managing diabetes; ascorbic acid and alpha-tocopherol are standard components of enteral and parenteral nutrition formulations designed to mitigate oxidative damage in immunocompromised populations. The intersection of aging demographics, adults over 65 will comprise 21% of the North American population by 2030, and heightened health consciousness is sustaining long-term demand for antioxidant-fortified foods, though the market remains vulnerable to shifts in nutritional science consensus and regulatory scrutiny of health claim substantiation.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict Government Limits On Synthetic Antimicrobials Like Benzoates And Propionates | -0.5% | United States (state-level bans), Canada | Short term (≤ 2 years) |

| Competition From Non‑Chemical Preservation Methods | -0.4% | United States, Canada (premium segments) | Medium term (2-4 years) |

| Regulatory Approval Processes For Novel Additive | -0.3% | United States (FDA), Canada (Health Canada), Mexico (COFEPRIS) | Medium term (2-4 years) |

| Public Health Concerns Over Long‑Term Additive Effects | -0.6% | North America (consumer advocacy) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Strict Government Limits on Synthetic Antimicrobials Like Benzoates and Propionates

In February 2026, the FDA began a formal review of butylated hydroxyanisole (BHA) following the National Toxicology Program's classification of BHA as a "reasonably anticipated human carcinogen." This represents the most significant regulatory action in the synthetic antioxidant market in over a decade, driving major food manufacturers to rapidly reformulate their products. While federal actions have been impactful, state-level initiatives have progressed more quickly. In 2025, 38 U.S. states introduced 140 bills targeting food additives. Notably, some proposals aimed to prohibit sodium benzoate and calcium propionate in school meal programs and restrict their use in products marketed to children. Additionally, in December 2025, Health Canada submitted a GRAS reform proposal to the Office of Information and Regulatory Affairs[3]Source: Health Canada, “Proposal to Authorize Rosemary Extract as a Food Additive,” Canada.ca. This proposal seeks to enforce mandatory pre-market safety reviews for all food additives, including those currently self-affirmed as GRAS, potentially subjecting synthetic antimicrobials to stricter scrutiny and longer approval timelines. Under current 21 CFR Part 172 regulations, maximum use levels are set for certain synthetic antimicrobials: 0.1% for sodium benzoate in beverages and 0.3% for calcium propionate in baked goods. However, no comparable quantitative limits exist for natural antimicrobials like lactic acid and nisin, creating a regulatory disparity that favors natural options. In response to this tightening regulatory environment, ingredient suppliers are accelerating their research and development of natural antimicrobials. For example, Corbion partnered with BRAIN Biotech in August 2025 to develop biobased antimicrobial compounds using enzyme technology and microbial strain optimization. These compounds are specifically designed to replace synthetic preservatives that are increasingly facing regulatory challenges.

Competition from Non-Chemical Preservation Methods

High-pressure processing, pulsed electric field, and cold plasma technologies are capturing market share in premium fresh-prepared meal and juice segments, where consumers prioritize "minimally processed" claims and are willing to pay 30-50% premiums for products preserved without chemical additives. HPP-treated products, which achieve microbial inactivation via hydrostatic pressure rather than thermal or chemical means, grew at 18% CAGR in the North American ready-to-eat meal category during 2023-2025, outpacing the broader prepared food market and eroding addressable demand for antimicrobial additives. Pulsed electric field systems, which use short bursts of high-voltage electricity to disrupt microbial cell membranes, are gaining traction in cold-pressed juice and liquid egg applications, where thermal pasteurization degrades sensory attributes and HPP's capital intensity limits adoption by smaller processors. The capital expenditure required for HPP equipment, USD 500,000 to USD 2 million per unit, has historically constrained adoption, but the emergence of contract HPP tolling services is lowering barriers to entry and enabling mid-sized food companies to access non-thermal preservation without upfront capital commitments. Cold plasma technology, which generates reactive oxygen and nitrogen species to inactivate surface microorganisms, is being commercialized for dry and semi-moist foods such as nuts, spices, and dried fruits, where traditional antimicrobials are ineffective and thermal treatments compromise quality.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Antimicrobials Outpace Antioxidants on Dual-Function Demand

In 2025, antioxidants accounted for 73.28% of the market value, underscoring their critical role in preventing lipid oxidation in fats, oils, bakery products, and snacks. However, antimicrobials are projected to grow at a 7.12% CAGR through 2031, outpacing the overall market as manufacturers increasingly seek solutions that address both oxidative rancidity and microbial spoilage. Natural antioxidants, including tocopherols, citric acid, ascorbic acid, and rosemary extract, are steadily replacing synthetic alternatives such as BHA, BHT, propyl gallate, and TBHQ due to clean-label demands and stricter regulations. A 2025 peer-reviewed study demonstrated that rosemary extract, at a 0.1% concentration, extended the shelf life of omega-3-enriched margarine by 40% compared to BHA controls, highlighting the technical effectiveness of botanical solutions (Journal of Food Science). In the antimicrobials segment, natural options like lactic acid, gluconic acid, acetic acid, and glucono delta lactone are gaining market share over synthetic preservatives such as benzoates, sorbates, and propionates.

In February 2026, the FDA launched a formal review of BHA following its classification by the National Toxicology Program as a "reasonably anticipated human carcinogen." The agency also announced plans to review BHT and azodicarbonamide. Lactic acid bacteria-based antimicrobials are emerging as a high-growth category, leveraging bacteriocin production and competitive exclusion to inhibit pathogens like Listeria monocytogenes and Salmonella. These antimicrobials are particularly effective in ready-to-eat meat and dairy applications. Novonesis, formed through the 2024 merger of Novozymes and Chr. Hansen is focusing on shelf-life extension and food safety cultures in its 2025-2026 product rollout. The integration of antioxidant and antimicrobial functionalities is driving innovation in hybrid preservative systems. For example, combining rosemary extract with lactic acid provides synergistic protection against oxidative and microbial degradation while simplifying ingredient declarations. This strategy is especially prevalent in plant-based meat analogs, which are highly susceptible to oxidation due to their polyunsaturated fatty acid content.

By Source: Algae-Based Solutions Surge on Bioavailability Edge

In 2025, plant extracts accounted for 48.21% of the market, highlighting the maturity of antioxidants from rosemary, green tea, and citrus. Algae-based solutions are expected to grow at an 8.02% CAGR through 2031, driven by bioavailability benefits and sustainability goals. Kemin Industries' NaturFORT, FORTIUM RGT, and GT-FORT lines enhance the heat stability and solubility of rosemary, green tea, and spearmint extracts. These innovations address thermal degradation issues that have limited natural antioxidant use in high-temperature processing. Algae-based antioxidants like astaxanthin and phycocyanin are gaining popularity in functional beverages and nutraceuticals due to their superior ORAC and anti-inflammatory properties.

Precision fermentation is transforming algae-derived antioxidant production through microbial biosynthesis, offering supply-chain resilience and consistent quality. This method outperforms photosynthetic cultivation, which is prone to seasonal and contamination risks. Cargill's EverSweet, a fermentation-derived stevia approved by EFSA in 2024, demonstrates the potential for fermentation in producing high-value antioxidants like astaxanthin. The "other" source category, including animal-derived antioxidants and synthetic fermentation products, remains niche but is attracting R&D investments. Algae-based solutions align with ESG goals due to minimal land and water use, but their higher costs limit adoption to premium and functional food segments.

By Application: Beverages Lead Growth on Functional Positioning

In 2025, processed foods accounted for 35.68% of the application value, highlighting their significance in bakery, confectionery, snacks, meat, poultry, and dairy. Beverages are expected to grow at a 6.68% CAGR through 2031, driven by functional drinks combining natural preservatives with immune-boosting postbiotics and adaptogens. Bakery and confectionery dominate antioxidant demand, with tocopherols and ascorbic acid preventing lipid oxidation in high-fat products and extending the shelf life of cookies, cakes, and pastries. The rise of plant-based bakery products using sunflower and canola oils with high polyunsaturated fatty acid content has increased oxidation challenges, encouraging the use of natural antioxidant blends. Meat and poultry processors are shifting from synthetic antimicrobials like sodium benzoate to natural options such as lactic acid and nisin due to state-level additive bans and consumer demand for clean labels.

Beverage applications are evolving as formulators use natural antimicrobials like nisin and natamycin to prevent yeast and mold in cold-pressed juices and kombucha, where thermal pasteurization could harm probiotic viability and sensory quality. The infant and clinical nutrition segment is growing, with FDA regulations under 21 CFR Part 107 requiring minimum levels of vitamin E and vitamin C in infant formula to ensure lipid stability and nutrient preservation. DSM-Firmenich launched Dry Vit A Palmitate for Early Life Nutrition in 2025, stabilized with mixed tocopherols to address parental concerns about synthetic antioxidants. Survey data showed 67% of parents prioritize minimal additives in baby food. Fats and oils remain a key market for antioxidants, as tocopherols and rosemary extract prevent rancidity in cooking oils, margarine, and shortening, though growth is limited compared to functional beverages and nutraceuticals. The "other" category, including pet food, animal feed, and pharmaceutical excipients, is gaining attention as ingredient suppliers diversify beyond human food applications, with natural antioxidants like mixed tocopherols gaining popularity in premium pet food marketed with clean-label and human-grade claims.

Geography Analysis

In 2025, the U.S. dominated North America's food antioxidants and antimicrobials market, claiming a substantial 69.38% share. This dominance underscores the vastness of the U.S. processed food industry, a consistent demand from sectors like industrial baking and meat processing, and a regulatory push towards cleaner label reformulations. In 2025, state-level. legislative actions surged, with 140 bills concerning additives introduced across 38 states. This legislative flurry has driven national brands to swiftly pivot towards natural alternatives, sidestepping the challenges of managing distinct SKUs in states like California, which has stringent additive regulations. Highlighting the regulatory landscape, the FDA initiated a formal review of BHA in February 2026. This move came on the heels of the National Toxicology Program labeling BHA as a "reasonably anticipated human carcinogen." This scrutiny has spurred major food manufacturers to promptly reformulate their products, indicating potential regulatory challenges ahead for traditional synthetic antioxidants.

In a strategic move, ADM invested USD 26 million in its Erlanger, Kentucky, facility in January 2026, following a USD 15 million expansion in 2025. This investment emphasizes ADM's commitment to scaling up naturally derived color and flavor solutions, catering to the rising demand for reformulations. Notably, proprietary research from ADM reveals that over 80% of U.S. consumers support reformulation, with 52% deeming it essential for brands Perishable News. Forecasted to grow at a robust 7.38% CAGR through 2031, Mexico is set to outpace its North American counterparts. This growth is attributed to COFEPRIS aligning its regulations with Codex Alimentarius standards, a burgeoning middle-class appetite for packaged convenience foods, and the increasing presence of multinational food companies establishing manufacturing bases in Mexico. COFEPRIS has expedited the approval process for natural antioxidants, cutting down the timeline from 24 months to a swift 12 to 15 months. This acceleration is granted to those with safety dossiers already recognized in the U.S. or EU, thus easing market entry hurdles for ingredient suppliers and hastening the commercialization of botanical preservatives in Mexico.

As modern retail formats like supermarkets and convenience stores proliferate in Mexico's urban hubs, there is a surging demand for shelf-stable packaged foods. These products, needing antioxidant and antimicrobial systems, are essential to endure ambient distribution temperatures and meet extended shelf life demands. Canada's regulatory environment is witnessing significant shifts. A December 2025 proposal from Health Canada to endorse rosemary extract as a food additive marks a pivotal moment for botanical antioxidants. This move could pave the way for quicker approvals of other compounds like green tea extract and grape seed polyphenols. While Canada's alignment with the FDA's GRAS pathways positions it as a prime testing ground for innovative antimicrobial formulations, especially for food manufacturers eyeing exports, there is a caveat. Health Canada's pre-market approval process for novel food additives, which mandates extensive multi-generation animal studies and human clinical data, results in longer 36 to 48 month and costlier timelines compared to the U.S.'s GRAS self-affirmation. Meanwhile, the Caribbean and Central American markets, though minor players in North America's revenue landscape, are gradually embracing natural preservatives. This shift is largely driven by the food service sectors, buoyed by tourism, and export-oriented processors striving to meet global food safety and quality benchmarks.

Competitive Landscape

The North American market for food antioxidants and antimicrobials is moderate. This indicates that no single supplier holds a dominant share, and competitive intensity remains high among ingredient suppliers, contract manufacturers, and vertically integrated food conglomerates. Strategic patterns highlight a divide: on one side are multinational ingredient giants such as DSM Firmenich, Kerry, Corbion, Kemin, IFF, and Cargill competing on the breadth of their portfolios, technical service capabilities, and regulatory expertise. On the other side are specialized biosolutions firms employing precision fermentation, enzyme-assisted extraction, and microalgae cultivation to target high-value segments in functional foods and nutraceuticals.

A case in point is Corbion's partnership with BRAIN Biotech in August 2025, aimed at co-developing biobased antimicrobial compounds through enzyme technology and microbial strain optimization. This move underscores a strategic pivot towards biotechnology-driven preservation platforms, which are being positioned as alternatives to synthetic preservatives, especially those facing regulatory scrutiny. There are untapped opportunities in fermentation-derived antimicrobials such as nisin, natamycin, and bacteriocins, which boast clean label positioning and regulatory benefits over their synthetic counterparts. However, these antimicrobials remain underutilized in mainstream processed foods due to their cost premiums and formulation complexities. Emerging players, particularly microalgae start-ups, are pushing the boundaries by commercializing astaxanthin and phycocyanin for functional beverages. Yet, their challenge lies in scaling production and achieving cost parity with traditional plant extracts. The competitive landscape is evolving, with ingredient suppliers increasingly turning to technologies like encapsulation, nanoemulsions, and controlled release systems. These innovations not only boost the efficacy and sensory appeal of natural antioxidants but also simplify the clean label reformulation process, broadening the market's reach.

The surge in patent activity surrounding enzyme-assisted extraction and precision fermentation highlights a growing R and D race. Suppliers are keen on securing intellectual property rights for novel production techniques that promise cost or performance benefits over traditional methods like solvent extraction and agricultural sourcing. Meanwhile, the FDA's GRAS reform initiative poses challenges. By suggesting mandatory pre-market notifications for all food additives self-affirmed as GRAS, the initiative could burden natural antioxidants such as rosemary extract and mixed tocopherols. This shift may advantage larger suppliers with robust regulatory capabilities while sidelining smaller innovators who grapple with the complexities of the approval process.

North America Food Antimicrobial And Antioxidants Industry Leaders

DSM-Firmenich

Corbion N.V.

International Flavors & Fragrances (IFF)

Archer Daniels Midland Company(ADM)

Kerry Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Martin Bauer united its operations with Finzelberg and MB-Med into a single, specialized Nutraceutical Unit to streamline the development of botanical solutions and nutraceuticals. The products include natural antioxidants and others.

- October 2025: Martin Bauer Group acquired American Botanicals, the leading supplier of wildcrafted botanicals in the US. This strategic addition expanded Martin Bauer's agricultural footprint in the United States and added stewardship of 33,000 acres of land in the Appalachian region.

- September 2024: Bio-Botanica Inc. entered into an exclusive distribution agreement with Gillco Ingredients (an Azelis company) to supply its botanical extract portfolio to U.S. companies in the food, beverage, and dietary supplement markets. Under this partnership, Gillco serves as the sole distributor of Bio-Botanica’s ingredients in these markets, leveraging Bio-Botanica’s expertise in botanical extract manufacturing alongside Gillco’s distribution network and technical sales capabilities.

North America Food Antimicrobial And Antioxidants Market Report Scope

Food antimicrobials and antioxidants are used to preserve food from spoilage and pathogenic microorganisms. Furthermore, the North American food antimicrobial and antioxidants market is segmented by type, application, and geography. By type, the market is segmented into antimicrobial and antioxidants. Antimicrobial is sub-segmented into natural and synthetic. Furthermore, natural is sub-categorized into nissin, natamycin, vinegar, and other natural types. Synthetic is sub-categorized into benzoates, propionates, lactates, acetates, and other synthetic types. Based on application, the market is segmented into bakery, dairy and desserts, beverages, meat and meat products, snacks and savory, margarine and spreads, and other applications. The report outlines the insights of major countries of the region, including the United States, Canada, Mexico, and the Rest of North America. For each segment, market sizing and forecasts have been done on the basis of value (USD million).

| Natural Antioxidants | Tocopherols |

| Citric acid | |

| Ascorbic acid | |

| Rosemary extract | |

| Others | |

| Synthetic Antioxidants | Butylated hydroxyanisole (BHA) |

| Butylated hydroxytoluene (BHT) | |

| Propyl Gallate (PG) | |

| Tertiary butyl hydroquinone (TBHQ) | |

| Others | |

| Natural Antimicrobials | Lactic acid |

| Gluconic Acid | |

| Acetic acid | |

| Glucono Delta Lactone (GDL) | |

| Others | |

| Synthetic Antimicrobials | Phosphates |

| Sorbates | |

| Benzoates | |

| Propionates | |

| Others |

| Plant-Extracts |

| Algae-Based |

| Others |

| Processed Foods | Bakery and Confectionery |

| Snack Products | |

| Meat and Poultry | |

| Dairy and Frozen Desserts | |

| Other Processed Foods | |

| Beverages | |

| Fats and Oils | |

| Infant and Clinical Nutrition | |

| Others |

| United States |

| Canada |

| Mexico |

| Rest of North America |

| Type | Natural Antioxidants | Tocopherols |

| Citric acid | ||

| Ascorbic acid | ||

| Rosemary extract | ||

| Others | ||

| Synthetic Antioxidants | Butylated hydroxyanisole (BHA) | |

| Butylated hydroxytoluene (BHT) | ||

| Propyl Gallate (PG) | ||

| Tertiary butyl hydroquinone (TBHQ) | ||

| Others | ||

| Natural Antimicrobials | Lactic acid | |

| Gluconic Acid | ||

| Acetic acid | ||

| Glucono Delta Lactone (GDL) | ||

| Others | ||

| Synthetic Antimicrobials | Phosphates | |

| Sorbates | ||

| Benzoates | ||

| Propionates | ||

| Others | ||

| Source | Plant-Extracts | |

| Algae-Based | ||

| Others | ||

| Application | Processed Foods | Bakery and Confectionery |

| Snack Products | ||

| Meat and Poultry | ||

| Dairy and Frozen Desserts | ||

| Other Processed Foods | ||

| Beverages | ||

| Fats and Oils | ||

| Infant and Clinical Nutrition | ||

| Others | ||

| Geography | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Key Questions Answered in the Report

What is the market size for North America food antimicrobial and antioxidants market?

The North America food antioxidants and antimicrobials market size is projected to be USD 1.55 billion in 2026 and reach USD 1.82 billion by 2031.

Why are algae-based antioxidants gaining attention?

Haematococcus astaxanthin and spirulina phycocyanin offer superior ORAC scores, sustainability credentials, and emerging fermentation production pathways, driving 8.02% CAGR growth.

How does high-pressure processing affect additive demand?

HPP delivers pathogen control without chemicals, expanding 18% CAGR in ready-to-eat meals and reducing the need for antimicrobial additives in premium SKUs.

Which country will post the fastest growth in the region?

Mexico leads with a forecast 7.38% CAGR to 2031, aided by COFEPRIS alignment with Codex and rising packaged-food consumption.

Page last updated on: