Anthrax Vaccine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

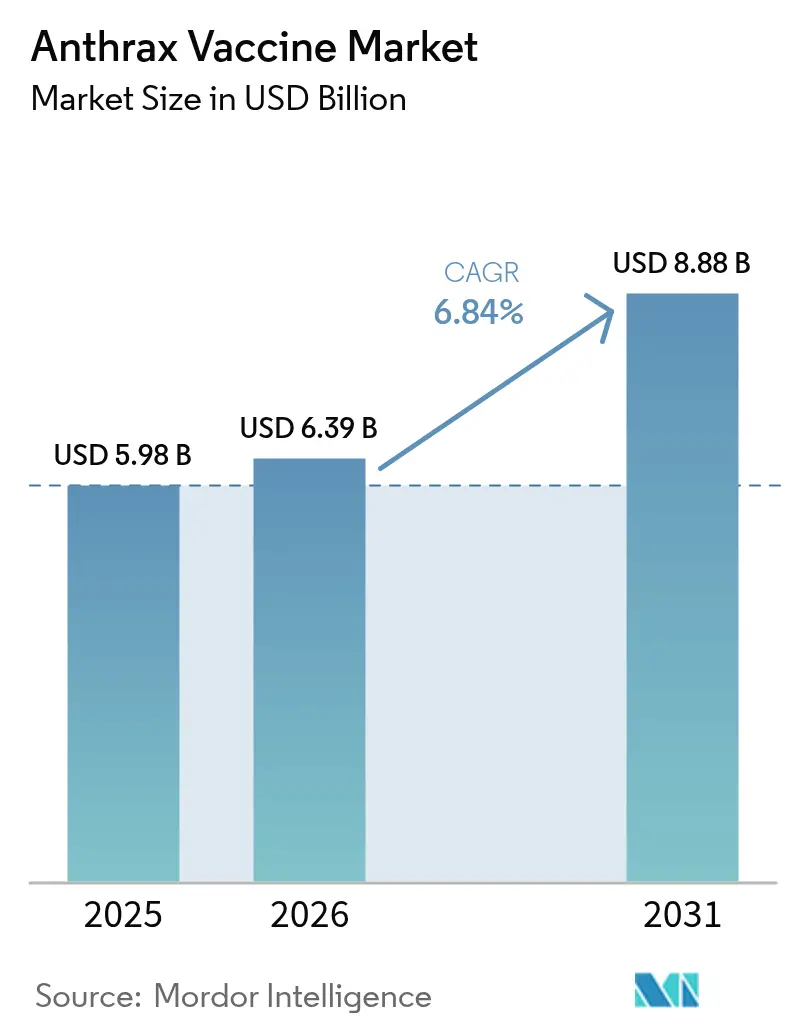

| Market Size (2026) | USD 6.39 Billion |

| Market Size (2031) | USD 8.88 Billion |

| Growth Rate (2026 - 2031) | 6.84% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anthrax Vaccine Market Analysis by Mordor Intelligence

The anthrax vaccine market size is expected to grow from USD 5.98 billion in 2025 to USD 6.39 billion in 2026 and is forecast to reach USD 8.88 billion by 2031 at 6.84% CAGR over 2026-2031. Demand holds firm as national stockpiling programs allocate multi-year budgets, exemplified by the United States’ USD 79.5 billion PHEMCE plan that assigns USD 1.3 billion to CYFENDUS procurement[1]Source: Innovation, Science and Economic Development Canada, “Federal government launches Health Emergency Readiness Canada,” canada.ca. Military vaccination mandates, such as the Department of Defense’s USD 235.8 million BioThrax agreement through 2033, secure predictable offtake. Regulatory momentum continues with FDA approval of CYFENDUS and South Korea’s clearance of the recombinant GC-1109 vaccine, signaling broader acceptance of next-generation formulations. Manufacturing investments, including the USD 2 billion BioMaP-Consortium, aim to diversify supply amid facility realignments by incumbents. Geopolitical tensions keep the threat of bioterrorism in policy focus, translating into steady requisitions across allied regions.

Key Report Takeaways

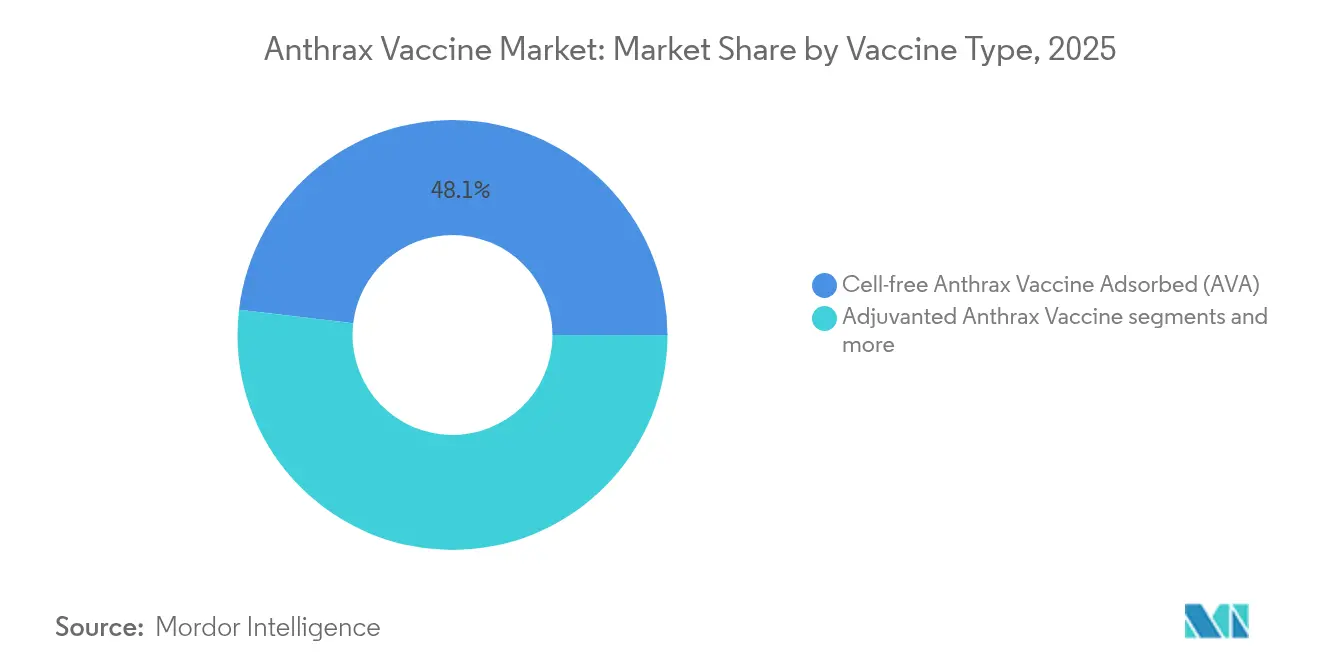

- By vaccine type, Cell-free Anthrax Vaccine Adsorbed led with 48.12% of anthrax vaccine market share in 2025; Adjuvanted AV7909 is projected to grow at an 8.01% CAGR to 2031.

- By end user, the Military & Defense segment held 55.02% of the anthrax vaccine market size in 2025, while Government Civilian Agencies expand fastest at 8.32% CAGR through 2031.

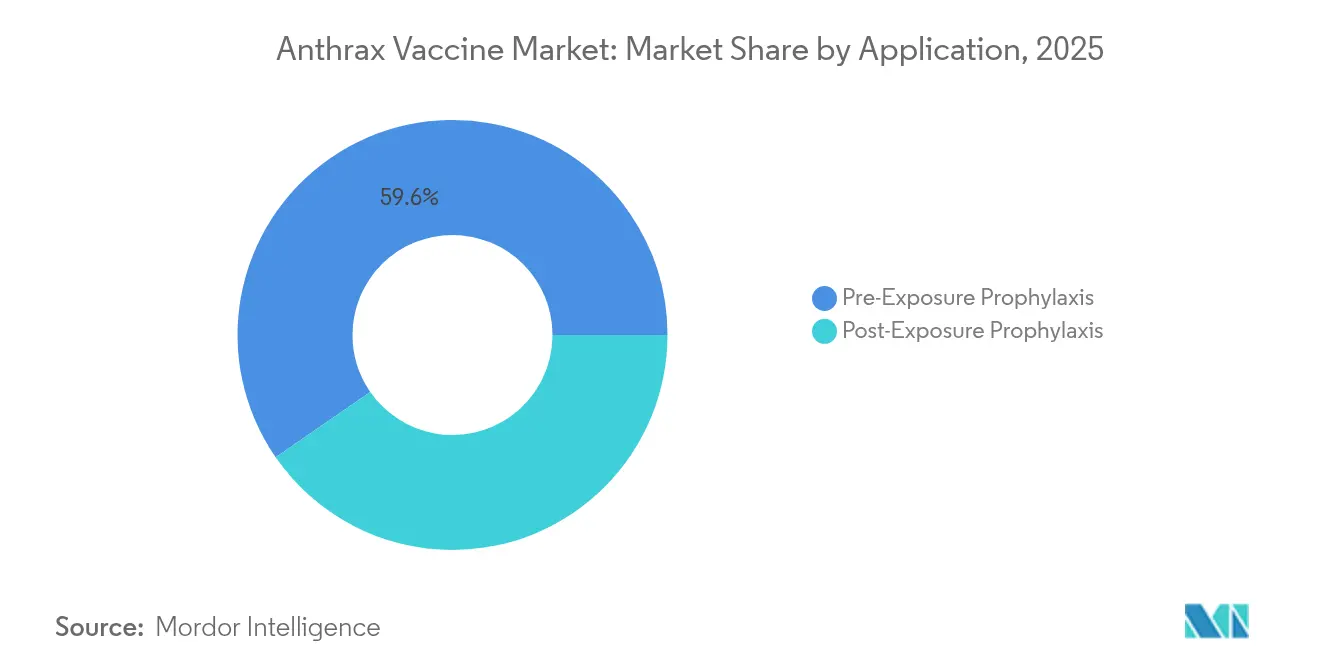

- By application, Pre-Exposure prophylaxis accounted for 59.63% of the anthrax vaccine market size in 2025 and is forecast to advance at a 7.45% CAGR to 2031.

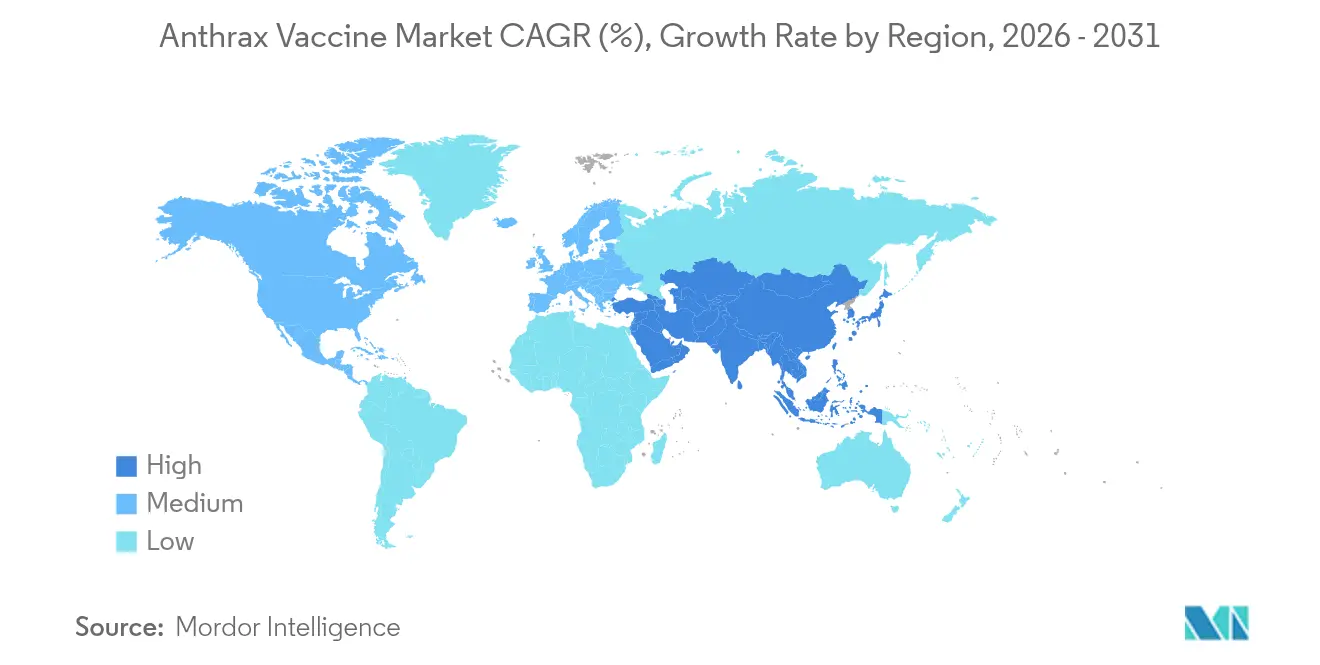

- By geography, North America dominated with 58.05% anthrax vaccine market share in 2025; Asia-Pacific is poised for the highest regional CAGR at 9.35% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Anthrax Vaccine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government biodefense stockpiling budgets increasing post-COVID | +2.1% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Mandatory vaccination programs for military & high-risk lab personnel | +1.8% | Global, led by North America, expanding to APAC | Long term (≥ 4 years) |

| Regulatory approvals of next-generation vaccines (e.g., CYFENDUS) | +1.5% | North America & EU primary, APAC emerging | Short term (≤ 2 years) |

| Rising geopolitical bioterrorism threat perception globally | +1.2% | Global, with regional hotspots in APAC & MEA | Long term (≥ 4 years) |

| Thermostable dry-powder vaccines enabling LMIC procurement | +0.9% | APAC, MEA, Latin America | Medium term (2-4 years) |

| Synthetic-biology platforms cutting cost & lead-time | +0.7% | Global, with early adoption in North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Biodefense Stockpiling Budgets Increasing Post-COVID

National budgets reclassified anthrax countermeasures as core security assets. The U.S. Strategic National Stockpile expanded multi-year contracts, including a USD 250 million modification covering CYFENDUS, highlighting lessons from pandemic supply bottlenecks. Canada’s Health Emergency Readiness Canada initiative adds regional alignment with domestic manufacturing capacity[2]Source: U.S. Department of Health and Human Services, “PHEMCE Multiyear Budget: Fiscal Years 2023–2027,” aspr.hhs.gov. Defense Threat Reduction Agency grants of USD 26.3 million sustain R&D pipelines, ensuring that the anthrax vaccine market remains integrated into broader chemical–biological defense funding.

Mandatory Vaccination Programs for Military & High-Risk Lab Personnel

Compulsory protocols broaden beyond troops to laboratory and emergency response staff, reinforcing the anthrax vaccine market in established buying centers. The CDC’s 2023 guideline update enlarges the eligible workforce, while an FDA-approved five-dose schedule improves adherence logistics. NATO interoperability standards likewise push adoption across allied forces.

Regulatory Approvals of Next-Generation Vaccines (e.g., CYFENDUS)

The FDA’s 2023 clearance of CYFENDUS validated fast-acting adjuvanted formulations with a two-dose post-exposure protocol. South Korea’s 2025 approval of recombinant GC-1109 underscores global regulatory receptivity to synthetic biology platforms. BARDA’s Target Product Profiles now prioritize single-dose efficacy, incentivizing R&D toward simplified regimens.

Rising Geopolitical Bioterrorism Threat Perception Globally

Regional security briefs cite potential weaponization of Bacillus anthracis, prompting increased procurement. South Korea’s readiness plans against North Korean capabilities and U.S. intelligence on dual-use biotech in China illustrate the strategic value placed on rapid-response vaccines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse-event profile & litigation risk limits civilian uptake | -1.4% | Global, with highest impact in North America & EU | Medium term (2-4 years) |

| Dependence on a single dominant supplier creates supply risk | -0.8% | Global, with critical exposure in North America | Short term (≤ 2 years) |

| Limited commercial demand outside government contracts | -0.6% | Global, with concentration in developed markets | Long term (≥ 4 years) |

| Emerging mAb & small-molecule alternatives divert funding | -0.4% | North America & EU primary, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Adverse-Event Profile & Litigation Risk Limits Civilian Uptake

Injection-site reactions and past legal disputes dampen broad-based demand. Civilian insurers seldom reimburse preventive doses, and no pediatric indication exists, narrowing the anthrax vaccine market beyond government channels.

Dependence on a Single Dominant Supplier Creates Supply Risk

Emergent BioSolutions’ facility closures in 2024 exposed fragility in an almost single-supplier ecosystem, prompting governments to hedge through recombinant and contract-manufacture alternatives

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vaccine Type: Cell-Free Dominance Faces Adjuvanted Challenge

Cell-free formulations commanded 48.12% anthrax vaccine market share in 2025 as longstanding familiarity drove procurement. Adjuvanted AV7909, led by CYFENDUS, grows at 8.01% CAGR on faster seroconversion that meets emergency timelines. Manufacturing strategies pivot toward recombinant antigens, evidenced by GC-1109’s licensure, easing biosafety constraints inherent in culture-based production. Patent filings for thermostable spray-dried doses aim to remove cold-chain costs and widen reach in low-resource markets.

A future pipeline that includes mRNA and viral-vector concepts remains preclinical but could disrupt the anthrax vaccine industry if single-dose efficacy targets are met. Cross-sector lessons from COVID-19 have validated adjuvant dose-sparing frameworks, likely accelerating platform diversification.

By End User: Military Dominance Yields to Civilian Growth

Military & Defense held 55.02% of the anthrax vaccine market size in 2025, anchored by locked-in contracts and deployment protocols. Civilian agencies expand at 8.32% CAGR, propelled by CDC guidance encompassing lab workers and first responders. Veterinary and One Health programs grow where endemic livestock outbreaks occur, linking animal health budgets to human countermeasure funding.

International collaborations, such as India’s BioThrax partnership with Biological E., bring supply closer to regional civilian buyers, easing import reliance and raising baseline demand across South Asia investors.emergentbiosolutions.com. Research institutions also raise call-off volumes to satisfy biosafety clearances for anthrax-related experimentation.

By Application: Pre-Exposure Protocols Drive Current Demand

Pre-Exposure vaccination secured 59.63% of the anthrax vaccine market size in 2025 on embedded military schedules. Post-Exposure demand accelerates at 8.78% CAGR as CYFENDUS enables two-dose prophylaxis, meeting BARDA’s rapid-response benchmarks. Integrated stockpile strategies purchase both antibiotics and vaccines, creating bundled contracts that reward suppliers with diversified portfolios.

Therapeutic applications stay exploratory. However, synthetic biology efforts hint at dual-action constructs that might blur the line between prophylaxis and treatment, expanding future addressable volumes for the anthrax vaccine market.

By Distribution Channel: Direct Procurement Maintains Control

Direct Government Procurement accounted for 69.10% market share in 2025 as security protocols dictate centralized buying. Allied nations increasingly arrange direct-order agreements under mutual-defense frameworks, giving Direct Order Suppliers a 9.12% CAGR outlook. Commercial pharmacy distribution remains negligible except under emergency use authorizations, reflecting controlled-substance status of biodefense countermeasures.

Facility realignments have inspired interest in multi-site contract manufacturing; Scorpius BioManufacturing’s plan to produce Anthim antitoxin in Kansas signals emerging redundancy in the supply chain.

Geography Analysis

North America retained 58.05% anthrax vaccine market share in 2025, supported by the Strategic National Stockpile’s rolling replenishments and consistent FDA approvals. A USD 2 billion domestic manufacturing drive under the BioMaP-Consortium strengthens regional self-reliance, while Canada’s HERC program aligns cross-border capacity.

Asia-Pacific posts the fastest CAGR at 9.35% to 2031. South Korea’s GC-1109 breakthrough and India’s BioThrax approval embed local production, diminishing sole dependence on U.S. supply and amplifying regional orders. Thailand’s 2025 anthrax outbreak response highlighted the urgency for wider livestock and human vaccine availability, prompting ASEAN regulators to discuss harmonized fast-track pathways.

Europe sustains moderate growth as the EU’s Health Technology Assessment Regulation targets synchronized member-state decisions on critical vaccines. Recent African outbreaks drive donor-funded procurements, although constrained budgets limit immediate volume. Latin American interest rises slowly, awaiting structured financing mechanisms that could tap into regional development banks.

Regulatory Landscape

Anthrax vaccines are regulated as biologics, with U.S. oversight centered on the FDA Center for Biologics Evaluation and Research (CBER) under the Public Health Service Act (Section 351(a)) and cGMP requirements. In the United States, BioThrax and CYFENDUS form the core of the licensed anthrax vaccine portfolio for preparedness use, and CYFENDUS was approved under 21 CFR 601 Subpart H (Animal Rule), which supports the pathway for next-generation countermeasures that depend on controlled manufacturing and post-licensure commitments.

Procurement-linked regulatory touchpoints also influence deployability, including lot release, labeling, and storage requirements for stockpile use. A notable milestone was the FDA approval of a supplemental BLA for CYFENDUS in November 2025 to update storage, handling, and labeling, which is designed to support broader field logistics for the Strategic National Stockpile and other government-managed inventories coordinated through the Public Health Emergency Medical Countermeasures Enterprise (PHEMCE).

Value Chain Analysis

The value chain is anchored by government-driven demand signals that translate into multi-year R&D, procurement, and replenishment cycles. In the United States, procurement flows are dominated by the Department of Defense (for pre-exposure readiness) and HHS/ASPR BARDA (for stockpile building), using long-term IDIQ structures such as the JPEO-CBRND contract awarded in January 2024 for BioThrax supply through September 2033, complemented by BARDA options and modifications for CYFENDUS deliveries.

Upstream suppliers rely on specialized biologics inputs (antigens, adjuvants, sterile fill-finish components) and controlled production environments. Midstream bottlenecks include validation, cGMP compliance, and government lot release timelines, while downstream activity is primarily direct government procurement into national stockpiles and military medical logistics channels, with limited commercial pathways. Diversification is emerging as countries such as South Korea add domestic recombinant production capacity via GC Biopharma's Barythrax (GC-1109), reducing reliance on a single external supplier for national stockpile needs.

Competitive Landscape

The anthrax vaccine market remains concentrated. Emergent BioSolutions controls the only two FDA-licensed vaccines, but facility closures and 2024 revenue volatility reveal operational risk. Its USD 9 million acquisition of raxibacumab monoclonal antibody, underpinned by a USD 130 million BARDA contract, reinforces portfolio breadth.

Challengers leverage synthetic biology. GC Biopharma entered the market with a recombinant vaccine, while iBio applies AI-guided antibody design to accelerate pipeline candidates. Contract manufacturing partnerships, such as Scorpius BioManufacturing’s Anthim arrangement, diversify source options beyond traditional incumbents.

Patent filings for IL-33 adjuvant systems, thermostable formulations, and spray-drying techniques suggest a pipeline pivot toward shelf-stable products suitable for global south logistics uspto.report. Government buyers continue to reward readiness, yet supplier diversification is likely as regulators approve more platforms and national security policies prioritize redundancy.

Anthrax Vaccine Industry Leaders

Colondo Serum Company

Merck Co, Inc. (MSD Animal Health)

Emergent BioSolutions Inc.

Proton Biopharma Ltd

Altimmune (Pharmathene Inc.)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A primary opportunity is supplier and platform diversification tied to preparedness mandates and stockpile sustainment, where procurement actions reflect active budgeted demand rather than episodic buying. The U.S. market continues to be refreshed through repeat ordering mechanisms under long-duration contracts, including the DoD IDIQ framework for BioThrax extending to 2033, along with BARDA contracting actions that have funded CYFENDUS deliveries into the stockpile system. This procurement environment favors vendors that can meet cGMP, lot release, and surge delivery requirements.

Regional manufacturing sovereignty, particularly in Asia-Pacific, is progressing as regulatory approvals and facility-backed programs translate into domestic supply capability. South Korea's approval of GC Biopharma's recombinant Barythrax (GC-1109) supports a local production base for national stockpiling (with reported output range of 150,000 to 300,000 doses), creating room for additional recombinant entrants, contract manufacturing participation, and adjacent enabling services (fill-finish, cold-chain optimization, and validated storage and handling systems) that meet government procurement specifications.

Recent Industry Developments

- January 2026: Emergent BioSolutions received a delivery order under its BioThrax IDIQ to supply BioThrax for U.S. government requirements in 2026. The award reinforces recurring military-led procurement and sustains baseline manufacturing utilization tied to readiness planning.

- September 2025: Emergent BioSolutions was awarded a USD 30 million contract modification from BARDA to supply CYFENDUS (Anthrax Vaccine Adsorbed, Adjuvanted), with deliveries completed by March 2026. The action underlines continued stockpile replenishment for a two-dose post-exposure regimen and highlights the role of BARDA contracting in shaping product mix.

- December 2024: Emergent BioSolutions received a USD 50 million contract option from BARDA for the procurement of CYFENDUS doses, with deliveries completed by April 2025. This procurement step expanded near-term stockpile coverage and supported continuity for post-exposure preparedness inventories.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of anthrax vaccines sold for human and animal use, including procurement through public health, defense, and routine veterinary channels. We count revenues generated within the defined geography and time period.

Scope exclusions: We exclude antibiotics, antitoxins, diagnostic testing, and general biodefense services that do not represent vaccine product revenue.

Segmentation Overview

- By Vaccine Type (Value)

- Cell-free Anthrax Vaccine Adsorbed (AVA)

- Adjuvanted Anthrax Vaccine (AV7909/CYFENDUS)

- Recombinant Protective Antigen Vaccine

- Others

- By End User (Value)

- Military & Defense

- Government Civilian Agencies

- Healthcare Workers & First Responders

- Veterinary Sector

- General Population High-risk Travelers

- By Application (Value)

- Pre-Exposure Prophylaxis

- Post-Exposure Prophylaxis

- By Distribution Channel (Value)

- Direct Government Procurement

- Hospital & Clinic Pharmacies

- Direct Order Suppliers

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with mapping the real demand pool, where most volume is shaped by biodefense planning and prevention policies. We leaned on public sources such as CDC guidance and vaccination recommendations, WHO technical notes, national procurement and budget documents where available, and regulatory disclosures from the US FDA and the European Medicines Agency.

To make the model usable, we also reviewed company annual reports and investor presentations to understand product focus, manufacturing scale signals, and revenue mix. We then checked reputable press coverage for contract awards and delivery timelines. Supporting checks were added using patent databases for development activity and, where needed, a paid subscription source for company financials and news screening. These examples are not exhaustive, and we referenced other public sources for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test procurement cycles, stockpile replenishment timing, and realistic pricing ranges, since published statistics rarely show these clearly for this niche. We spoke with a mix of vaccine manufacturers, distributors, public sector buyers, and clinical or biodefense stakeholders across major regions so assumptions could be adjusted to local policy and funding patterns. Where answers varied, we did follow-ups to confirm what was driving the difference, for example booster schedules or contract delivery phasing.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 18% | APAC: 44% |

| Mid tier: 49% | Functional/Unit leaders: 37% | EMEA: 29% |

| Smaller Players: 20% | Managers: 45% | Americas: 27% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up blend, where the top-down view starts from the addressable protected population and stockpile policies, then is reconstructed through expected dosing schedules, replenishment intervals, and procurement timing. We corroborated this with selective bottom-up approximations, such as supplier revenue signals, sampled price per dose ranges by contract type, and channel checks on public tenders. These inputs were used to refine totals when early outputs looked unrealistic.

Key inputs used in the model included government biodefense funding direction, stockpile rotation or shelf life replacement needs, the share of demand tied to military versus civilian programs, dose regimen assumptions (primary and booster), and the split between human and veterinary use where relevant. Forecasting was run through scenario analysis because procurement can be lumpy. The final growth path was then aligned to the most consistent view shared by interviewees on contract cadence and replenishment behavior. When supplier level data was incomplete, gaps were handled through conservative penetration assumptions and cross checks against known purchasing mechanisms before the final number was locked.

Data Validation & Update Cycle

Outputs were checked against independent signals, including known procurement patterns, policy updates, and whether implied doses and pricing stayed within realistic bounds. Variance flags were reviewed in steps, first by the analyst building the model and then by a second analyst who rechecked key inputs, formulas, and unit conversions.

If a major variance was detected, we re-contacted relevant respondents or revisited the underlying public documents to confirm the assumption that caused it. Reports are refreshed annually, and interim updates are made when material events occur, such as a large contract award, a policy shift, or a notable supply change. Before delivery, we complete a final pass so clients receive the latest updated view.

Mordor Intelligence's Anthra Vaccine Market Size Compared Against Other Published Estimates

Published values for this market can look far apart because groups often treat government stockpile purchasing differently, and they also vary on whether animal use is counted in the same total. Timing also matters, since a single multi-year contract can pull revenue forward or push it out, depending on how deliveries are recognized.

Another common gap comes from pricing and regimen assumptions, where a fixed price per dose is applied even though contract terms, booster schedules, and replenishment cycles can shift the real average. The spread is also influenced by currency timing and update cadence, where older estimates miss newer procurement signals and the implied market total stays anchored to a prior award cycle that is handled differently by Mordor Intelligence.

Another source of variance is how each publisher converts procurement orders into delivered, billed revenue, especially when contract phasing spans multiple periods.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.39 B (2026) | |

| Trade Journal A | USD 0.76 B (2024) | Uses a narrower scope focused on reported commercial sales and dose shipments, which typically leaves out multi year government procurement value and often excludes veterinary demand. |

| Global Consultancy B | USD 0.52 B (2025) | Applies a conservative base case with limited stockpile replenishment and a simplified pricing assumption, which can understate revenue when procurement cycles and delivery phasing are treated as one year purchases. |

The comparison suggests that scope and procurement timing decisions explain most of the difference, more than any single growth assumption. By keeping the value pool tied to who buys, how often replenishment happens, and what a realistic contract price range looks like, the resulting market number stays traceable and repeatable for planning.

Key Questions Answered in the Report

What is the current Global Anthrax Vaccine Market size?

The Global Anthrax Vaccine Market is projected to register a CAGR of 6.84% during the forecast period (2026-2031)

What is the current value of the anthrax vaccine market?

The anthrax vaccine market stands at USD 6.39 billion in 2026 and is projected to reach USD 8.88 billion by 2031.

Which region leads the anthrax vaccine market?

North America holds 58.05% market share in 2025 due to Strategic National Stockpile purchases and recent FDA approvals.

Which vaccine type is growing fastest?

Adjuvanted AV7909, driven by CYFENDUS, posts an 8.01% CAGR for 2026-2031.

Why are civilian agencies becoming important buyers?

Expanded CDC guidelines now include lab workers and first responders, pushing Government Civilian Agencies to the fastest growth rate at 8.32% CAGR.

Page last updated on: