Animal Digest Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

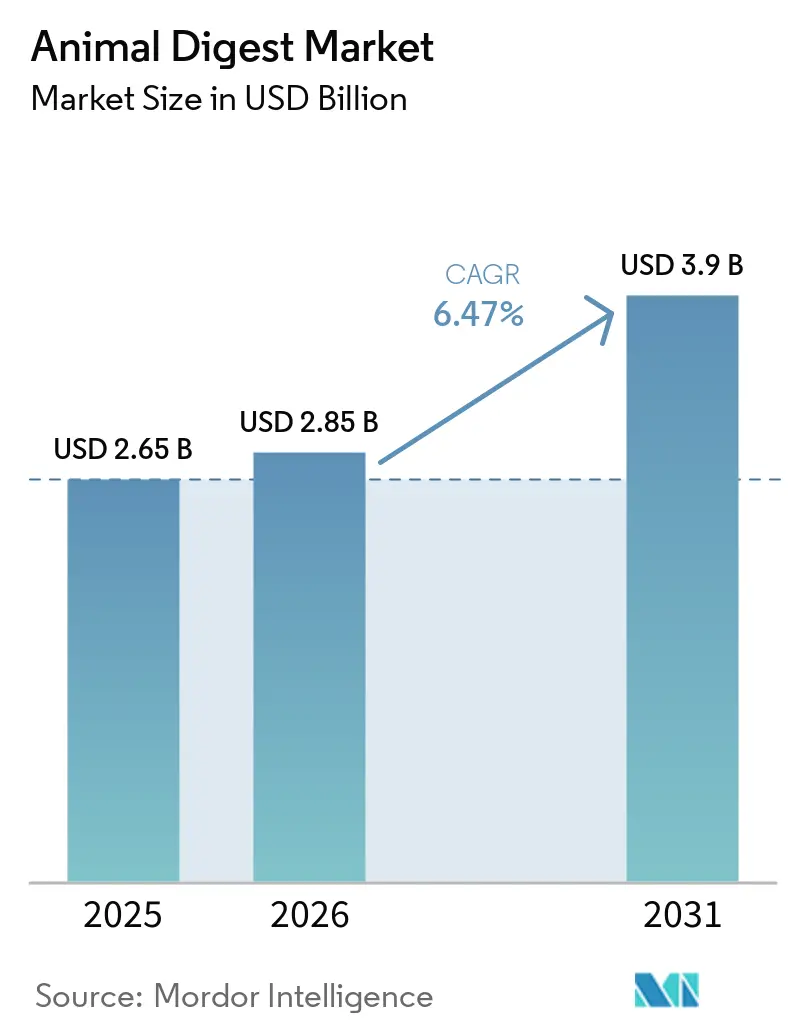

| Market Size (2026) | USD 2.85 Billion |

| Market Size (2031) | USD 3.9 Billion |

| Growth Rate (2026 - 2031) | 6.47% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Animal Digest Market Analysis by Mordor Intelligence

The animal digest market size is projected to expand from USD 2.65 billion in 2025 and USD 2.85 billion in 2026 to USD 3.90 billion by 2031, registering a 6.47% CAGR over 2026-2031. Demand is shifting away from low-cost commodity palatants toward precision nutrition products that support premium pet food, aquaculture intensification, and sustainability mandates. Poultry-sourced digest remains the largest input because the global poultry sector provides reliable volumes of rendered by-products, yet insect-based alternatives are scaling quickly as regulations in the European Union and North America clarify the use of novel proteins. Manufacturers are also moving toward liquid formulations to improve spray-on uniformity and reduce dust during processing. In parallel, North American producers face raw-material volatility from disease outbreaks, which are encouraging multi-species blending strategies and increased interest in insect and single-protein digest options.

Key Report Takeaways

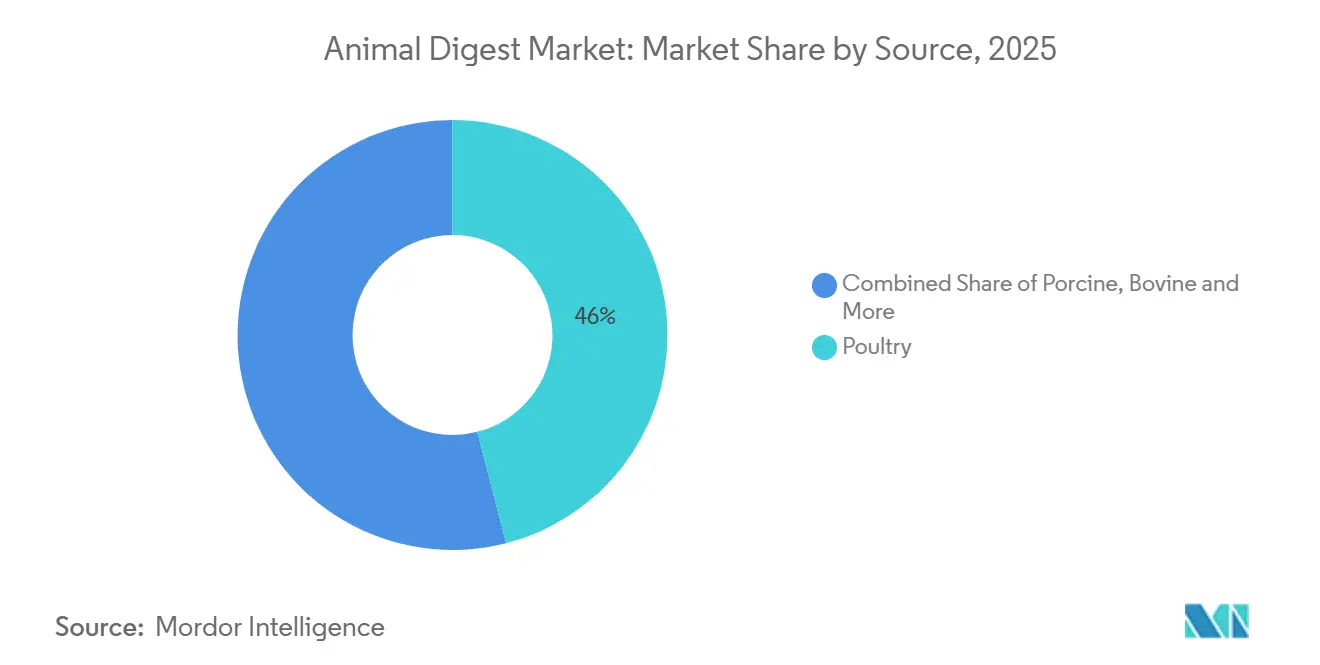

- By source, poultry captured the largest 46.0% animal digest market share in 2025, whereas insect variants are forecast to record the fastest 10.9% CAGR through 2031

- By form, powder commanded the largest 61.5% of the animal digest market size in 2025, while liquid digest is advancing at the fastest 8.4% CAGR during 2026-2031

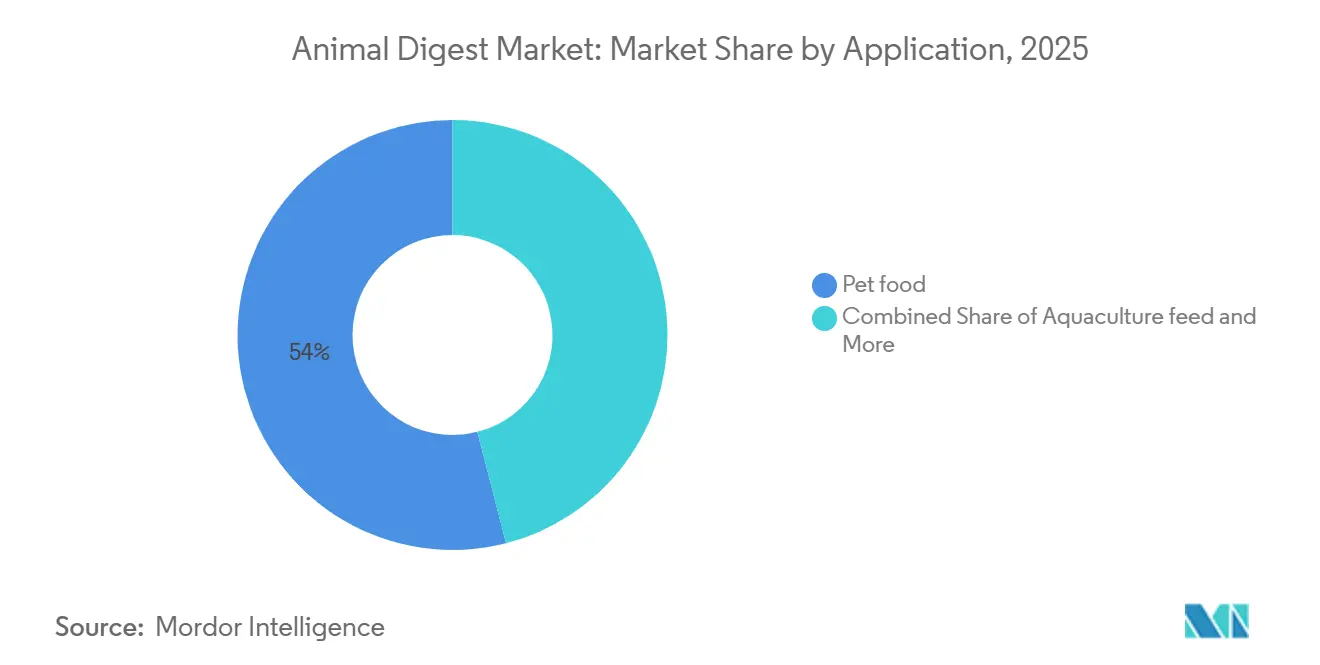

- By application, pet food led with the largest share, accounted for 54.0% of the animal digest market share in 2025, whereas aquaculture feed is projected to achieve the fastest 9.5% CAGR through 2026-2031.

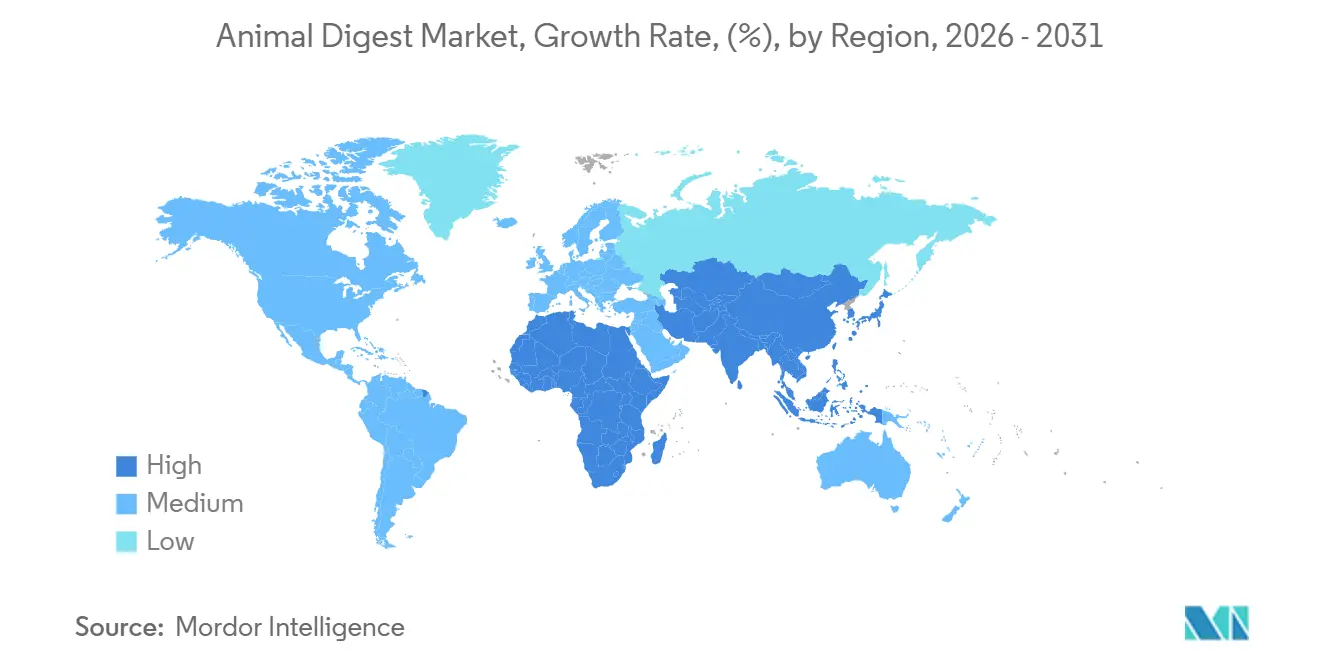

- By geography, North America accounted for the largest 38.0% share of the animal digest market in 2025, whereas Asia-Pacific is poised to expand at a 7.8% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Animal Digest Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in premium pet food, positioning animal digest as a palatability enhancer | +1.8% | North America and Europe, spillover into China, Japan, and South Korea | Medium term (2-4 years) |

| Rapid expansion of aquaculture feed applications | +1.5% | Thailand, Vietnam, Indonesia, India, Brazil, and Ecuador | Long term (≥ 4 years) |

| Cost advantage over synthetic flavor alternatives | +1.2% | Global, with heightened effect in South America, the Middle East, and Africa | Short term (≤ 2 years) |

| Surge in single-protein diets for companion animals | +0.9% | North America and Europe's premium segments | Medium term (2-4 years) |

| Emerging insect-based animal digest production technologies | +0.7% | Europe, Thailand, Malaysia, South Korea, and early adoption in North America | Long term (≥ 4 years) |

| Upcycling waste streams from cultured-meat production | +0.4% | Singapore, the United States, and Israel | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth in Premium Pet Food, Positioning Animal Digest as a Palatability Enhancer

Pet food manufacturers are redesigning recipes to elevate animal digest from a filler to a functional flavor driver, because consumer willingness to pay for taste has intensified since 2025. Nestlé Purina PetCare Company (Nestlé S.A.) is investing over EURO 150 million (approximately USD 200 million) to upgrade its Wisbech, United Kingdom, plant. Scheduled for completion by early 2025, the project aims to modernize production lines, enhance automation, improve energy efficiency, and reduce carbon emissions. AFB International (The Ensign-Bickford Industries, Inc.) deployed USD 79 million in Columbus, Georgia, in 2024 and opened a Thailand hub in 2024 to serve Asia-Pacific premium tiers. Formulation data show premium dry dog food now contains 2% - 4% digest, versus 0.5% - 1.5% in economy kibble, lifting raw-material costs per kilogram by USD 0.15-0.30 and proving manufacturers can absorb higher input costs when palatability drives brand loyalty.

Rapid Expansion of Aquaculture Feed Applications

Shrimp and finfish farmers are blending animal digest to overcome off-flavors associated with higher soy or insect meal inclusion rates. Symrise AG markets fish and crustacean hydrolysates such as Actipal that improve acceptance rates in intensive ponds. A 2026 US Grains and Bioproducts Council-reviewed trial on Pacific white shrimp showed 2% fish protein digest raised feed intake 8% and weight gain 5% versus a control diet[1]Source: Thomas Wilson, “Literature Review Report: DDGS and CFP in Aquafeed,” U.S. Grains Council, grains.org. Vietnam’s VNF and France’s Adisseo supply shrimp-derived peptides that target the same outcome, while Kemin opened an Italy headquarters in 2025 to deepen aquafeed research and development. Asia-Pacific now delivers more than 85% of global aquaculture output, guaranteeing persistent demand tailwinds for digest inclusion[2]Source: Food and Agriculture Organization of the United Nations, “FAO Fisheries and Aquaculture Statistics,” FAO, fao.org.

Cost Advantage Over Synthetic Flavor Alternatives

Rendered animal digest is 25%-40% less expensive than chemically synthesized flavors, a cost difference that is significant in price-sensitive markets. The North American Renderers Association reported a 22% decline in rendered product prices in 2024, as slaughter volumes grew and fats were diverted to biofuel, lowering the opportunity cost of protein meal. The United States exported 1.37 million metric tons of animal protein meal in 2024, with Vietnam accounting for 272,223 metric tons, representing an 80% year-over-year increase. This growth can be attributed to the cost advantage over synthetic flavor alternatives, driving demand[3]Source: United States Department of Agriculture Economic Research Service, “Livestock, Dairy, and Poultry Outlook,” ERS USDA, ers.usda.gov. Brazil processes 13.9 million metric tons of by-products annually, generating 3.8 million metric tons of meals to support a strong domestic digest sector, which benefits from cost advantages and efficient utilization of these by-products.

Surge in Single-Protein Diets for Companion Animals

Veterinarians often prescribe single-protein diets to control allergies, so brands increasingly request chicken-only or salmon-only digest. The American Association of Feed Control Officials clarified species-specific labeling in its 2024 regulations, reducing ambiguity for marketers. Single-protein digest commands a 15%-25% premium because segregation and traceability add fixed cost. Kerry Group achieved growth by rolling out single-species palatants across its Taste and Nutrition portfolio, which generated EUR 6.1 billion (USD 6.5 billion) in revenue in 2024. Market surveys show that premium and therapeutic diets featuring single-protein claims are expanding shelf presence in United States pet specialty retailers through 2025, reinforcing demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent rendering by-product regulations in Europe and North America | -0.8% | European Union, United States, Canada | Medium term (2-4 years) |

| Volatility in poultry and porcine by-product supply | -0.7% | Global, acute in North America and the Caribbean | Short term (≤ 2 years) |

| Negative consumer perception of “digest” labeling | -0.5% | North America and Europe's premium segments | Medium term (2-4 years) |

| Competition from clean-label plant hydrolysates | -0.4% | North America and Europe, emerging in urban Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Rendering By-product Regulations in Europe and North America

European Union Regulation 1069/2009 mandates Category 3 controls that heighten traceability, heat treatment, and testing, thereby lifting compliance costs by USD 0.05-0.12 per kilogram. The European Food Safety Authority tightened microbiological criteria in several 2024-2025 opinions, compelling more frequent audits. Canada’s Food Inspection Agency introduced updated RG-4 guidance in July 2024 that intensified documentation requirements, a burden that smaller renderers find difficult to amortize. In January 2025 the United States Food and Drug Administration issued its Animal Food Ingredient Compendium, expanding process scrutiny and increasing capital outlays for quality systems. These overlapping rules consolidate power among scale operators, enabling them to spread fixed compliance investments across larger volumes.

Volatility in Poultry and Porcine By-product Supply

Highly pathogenic avian influenza and African swine fever create sporadic raw-material shortages, forcing formulators to pivot to alternative species or pay premiums. The United States Department of Agriculture Animal and Plant Health Inspection Service reported 1,616 infected poultry flocks as of February 2025, with 44 million layers culled since October 2024. African swine fever outbreaks in the Dominican Republic increased to 58 monthly incidents between February and July 2025, reducing pork production by 15% compared to 2021 levels. In February 2026, a Federal Order restricted the movement of live hogs from Puerto Rico, underscoring the ongoing risk of contagion. This instability is driving pet and aqua feed producers to explore multi-species or insect-based digest alternatives, though scaling these new sources requires significant time and investment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Poultry Dominates, Insect Variants Accelerate

Poultry digest is projected to account for 46.0% of the animal digest market in 2025, driven by global broiler production reaching 47.1 billion pounds (23.55 million metric tons) that year. This ensures a stable supply of by-products, according to the United States Department of Agriculture (USDA) Economic Research Service (ERS). Porcine digest ranks second because of its amino-acid profile and high canine acceptance, although African swine fever causes periodic shortages. Bovine digest serves niche hypoallergenic diets and certain aquaculture formulations that value specific peptide ranges. Fish digest is essential in marine cat food and high-performance shrimp feed, where omega-3 content and umami flavor boost palatability. Insect digest, while small today, is forecast to be the fastest-growing segment, with a 10.9% CAGR, as European and Asian regulators approve black soldier fly and mealworm hydrolysates and capital flows resume into new plants.

Poultry’s dominance within the animal digest market size reflects integrated rendering networks that convert offal and spent hens into cost-competitive hydrolysates. United States renderers rely on automated temperature-time systems that meet both domestic and export microbiological standards, which supports consistent quality. In contrast, insect producers must build specialized hydrolysis lines and invest in downstream spray dryers, delaying cost parity with traditional sources. Patent activity filed in June 2025 for an insect protein hydrolysate demonstrates technical advances, yet commercialization awaits higher production volumes and stable financing. Brands focused on clean-label or novel-protein claims already formulate with insect digest at inclusion levels of 0.5% to 1%, positioning the segment for outsized growth once capacity expands.

By Form: Powder Leads, Liquid Gains in Wet Food

Powder styles held 61.5% of the animal digest market in 2025, owing to shelf stability and compatibility with extrusion and pelleting lines. Spray-drying allows manufacturers to deliver free-flowing particles that blend homogeneously in dry kibble and aquafeed mesh sizes. Liquid digest occupies a smaller base but expands at 8.4% CAGR over 2026-2031 as wet pet food producers seek even surface coverage on chunks and pâté. AFB International (The Ensign-Bickford Industries, Inc.)’s Georgia plant, operational since 2024, devotes several lines to liquid formats in anticipation of this shift. Paste and slurry versions remain niche for high-viscosity aqua pellets that demand strong binding and water resistance.

Powder’s leadership in the animal digest market share persists because many pet food lines still favor dry kibble that requires low-moisture palatants. However, liquid digest now benefits from reduced dust, shorter mixing cycles, and the ability to incorporate emulsifiers that stabilize flavor volatiles. Regions enforcing stricter dust exposure limits in factories, notably the European Union, further encourage the uptake of liquids. Symrise AG’s South Carolina palatant site added dual-format capability in 2025 to serve clients that flex between powder and liquid purchases. Equipment suppliers report rising orders for liquid application nozzles rated to deliver uniform coat weights on high-speed conveyors, supporting continued growth.

By Application: Pet Food Anchors, Aquaculture Surges

Pet food accounted for 54.0% of global consumption in 2025, as dogs and cats drive high-value retail sales that require robust palatability. Canine diets consume greater tonnage, while feline formulations often use higher inclusion rates because cats exhibit picky feeding behavior. Nestlé Purina PetCare Company (Nestlé S.A.)’s Williamsburg Township, Ohio, plant, under construction since 2024, includes digest dosing systems sized for 1.3 million square feet of production, underlining pet food’s anchor position. Therapeutic and functional diets also rely on digestive enzymes to mask the taste of supplements and hydrolyzed proteins. Treat manufacturers, meanwhile, incorporate digest coatings to differentiate flavor lines.

Aquaculture feed is forecast to be the fastest-growing application, with a 9.5% CAGR to 2031, as shrimp and finfish operators must offset lower fishmeal inclusion by improving feed acceptance. The animal digest market for aquaculture is growing sharply in Vietnam, Thailand, and Indonesia, which are now importing animal protein meals at record levels. Digest inclusion at 1%-2% can improve feed conversion ratios by up to 5%, offering farmers an attractive economic return. Livestock starter feeds use digest to jump-start intake in newly weaned pigs and poultry chicks, despite the segment’s smaller overall volume. Experimental uses linked to cultured-meat by-products remain speculative until cell-culture capacity scales.

Geography Analysis

North America captured 38.0% of the animal digest market in 2025, driven by multinational pet food headquarters, sophisticated rendering operations, and high pet ownership rates. The United States Department of Agriculture measured cattle and calf plus hog and pig output at 39.22 million metric tons in 2024, a stable feedstock base for digests. Nestlé Purina PetCare Company (Nestlé S.A.), Mars Petcare, and The J.M. Smucker Company each operate multiple plants with on-site palatant spray lines, reinforcing regional demand. Disease outbreaks continue to pose risks, such as avian influenza leading to poultry depopulations and African swine fever threats from the Caribbean, which resulted in a 2026 Federal Order restricting hog movement. Growth in North America is expected, driven by increasing premiumization, therapeutic diets, and single-protein claims, which help counterbalance market maturity.

Asia-Pacific is projected to be the fastest-growing region at a 7.8% CAGR during 2026-2031, driven by rising pet adoption in China and India, and by converging aquaculture growth in Southeast Asia. China’s chicken production is set to hit 17,300 thousand metric tons in 2026, with exports at 1,400 thousand metric tons, expanding rendering inputs. AFB International (The Ensign-Bickford Industries, Inc.) opened a Thailand headquarters in 2024 for local palatant production, while Symrise AG markets ActiTuna Oil and Actipal to shrimp growers across the region. India, though smaller, is seeing urban consumers migrate from table scraps to commercial kibble, lifting digest demand. Regulatory clarity on insect proteins is advancing in South Korea and Thailand, opening the way for future digest supply from black soldier fly processors.

Europe remains a key consumer market, driven by large pet food clusters in Germany, France, and the United Kingdom. However, growth is constrained by Regulation 1069/2009, which imposes additional costs and discourages smaller market entrants. Kerry Group's 2024 revenue reflected continued growth in its Taste and Nutrition unit, which supplies palatants. In 2024-2025, the European Food Safety Authority issued several opinions confirming the safety of black soldier fly and mealworm hydrolysates, facilitating the introduction of insect digest products. Despite this, short-term supply flexibility may be affected by volatility in the pork market in Eastern Europe and by stricter Category 3 documentation requirements.

Competitive Landscape

The animal digest market is moderately concentrated, with the top five suppliers including Kemin Industries, Inc., AFB International (The Ensign-Bickford Industries, Inc.), Symrise AG, Nestlé Purina PetCare Company (Nestlé S.A.), and BHJ A/S (Danish Crown A/S), accounting for majority share of the animal digest market size in 2025, and their scale confers bargaining power with global pet food multinationals. Kemin Industries, Inc., AFB International (The Ensign-Bickford Industries, Inc.), and Symrise AG operate multi-continent manufacturing networks that secure consistent volume and quality for customers. Darling Ingredients leverages vertical integration across rendering, gelatin, and specialty ingredients to optimize margin across its feed segment, which booked USD 713.5 million revenue in Q1 2025. Saria’s 2024 takeover of BHJ expanded its footprint in spray-dried digest inside Europe, complementing its EUR 3 billion (USD 3.2 billion) revenue base. Nestlé Purina PetCare Company (Nestlé S.A.) still produces digest partly in-house, reducing external procurement exposure and controlling flavor IP for its brands.

Innovation is turning into a competitive lever. AFB International (The Ensign-Bickford Industries, Inc.) presented an artificial-intelligence palatability prediction platform at Petfood Forum 2026 that models flavor acceptance to shorten research and development cycles. As per the World Intellectual Property Organization (WIPO), patent filings for insect protein hydrolysate in June 2025 and for black soldier fly frass methane reduction in March 2026 signal diversification beyond conventional meat sources. Symrise AG invests in sensory science that pairs digest peptides with yeast extracts to meet clean-label demands without sacrificing taste. Capital constraints have impacted certain insect ventures. Protix paused its Nebraska rollout in April 2026, while Innovafeed suspended a United States pilot in August 2025, shifting its focus to operations in France and Southeast Asia. These developments present opportunities for regional startups capable of addressing regulatory challenges and securing funding.to address regulatory challenges and secure

Regulatory complexity also shapes market power. Larger processors can amortize Category 3 compliance investments and Food and Drug Administration audits across higher tonnage, whereas smaller renderers struggle to do so, encouraging consolidation. Clean-label trends intensify competition from plant protein hydrolysates offered by Kerry Group and Symrise AG, but price premiums and lingering palatability gaps keep animal digest dominant in mainstream categories. Disease-driven raw-material volatility incentivizes strategic multi-species sourcing; incumbents with global rendering alliances can swap inputs rapidly to preserve service levels, reinforcing customer stickiness despite rising sustainability reporting demands.

Animal Digest Industry Leaders

Kemin Industries, Inc.

AFB International (The Ensign-Bickford Industries, Inc.)

Symrise AG

Nestlé Purina PetCare Company (Nestlé S.A.)

BHJ A/S (Danish Crown A/S)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Protix placed its Nebraska insect protein facility on hold and pivoted to Southeast Asia, signing a memorandum with South Korea’s Reco to identify sites in Thailand, Malaysia, Vietnam, and Indonesia. This redeployment channels funding toward the world’s fastest-growing aquafeed corridor, likely accelerating insect digest supply for Asian manufacturers while slowing short-term capacity gains in North America.

- October 2025: Kemin Industries opened a new headquarters and laboratory in Italy to enhance European research and development for pet food and aquafeed ingredients. The facility strengthens local formulation support and is anticipated to accelerate the commercial rollout of customized digest solutions, underpinning regional demand growth for functional palatants.

- August 2025: Innovafeed has suspended its pilot operations in the United States and redirected resources to its Nesle plant in France, which underwent a fivefold expansion in July 2024. This consolidation of production enhances the near-term availability of insect digest for European pet food and aquaculture markets. However, it restricts supply diversification in North America, potentially leading to tighter regional volumes and higher prices.

Global Animal Digest Market Report Scope

The Animal Digest Market encompasses the industry that produces and supplies concentrated flavoring and nutritional additives used in pet foods and animal feeds. It is primarily driven by the demand for palatable, high-quality ingredients made from clean, enzymatically or chemically broken-down animal tissues.

The Animal Digest Market Report is Segmented by Source (Poultry, Porcine, Bovine, Fish, Others), by Form (Powder, Liquid, Paste/Slurry), by Application (Pet Food, Aquaculture Feed, Livestock Feed, Others), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Poultry |

| Porcine |

| Bovine |

| Fish |

| Others |

| Powder |

| Liquid |

| Paste/Slurry |

| Pet Food |

| Aquaculture Feed |

| Livestock Feed |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Kenya | |

| Rest of Africa |

| By Source | Poultry | |

| Porcine | ||

| Bovine | ||

| Fish | ||

| Others | ||

| By Form | Powder | |

| Liquid | ||

| Paste/Slurry | ||

| By Application | Pet Food | |

| Aquaculture Feed | ||

| Livestock Feed | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the animal digest market be by 2031?

The animal digest market size is forecast to reach USD 3.90 billion by 2031.

Which source currently dominates demand?

Poultry digest commanded 46.0% animal digest market share in 2025 because of abundant global broiler by-products and mature rendering infrastructure.

Which application segment is expanding the fastest?

Aquaculture feed is projected to rise at the fastest 9.5% CAGR through 2031 as Asian shrimp and finfish producers seek palatability enhancers.

What is the major regional growth engine?

Asia-Pacific is forecast to expand at 7.8% CAGR during 2026-2031 on the back of rising pet ownership in China and India and intensive aquaculture in Southeast Asia.

How concentrated is supplier competition?

The top five suppliers indicate moderate concentration, favoring firms that control rendering feedstock and proprietary hydrolysis technology.

Are insect-based digests commercially viable?

Insect digest remains small today but is tipped for a 10.9% CAGR through 2026-2031 as black soldier fly and mealworm operations secure regulatory approval and scale production, particularly in Europe.

Page last updated on: