Animal Feed Organic Trace Minerals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

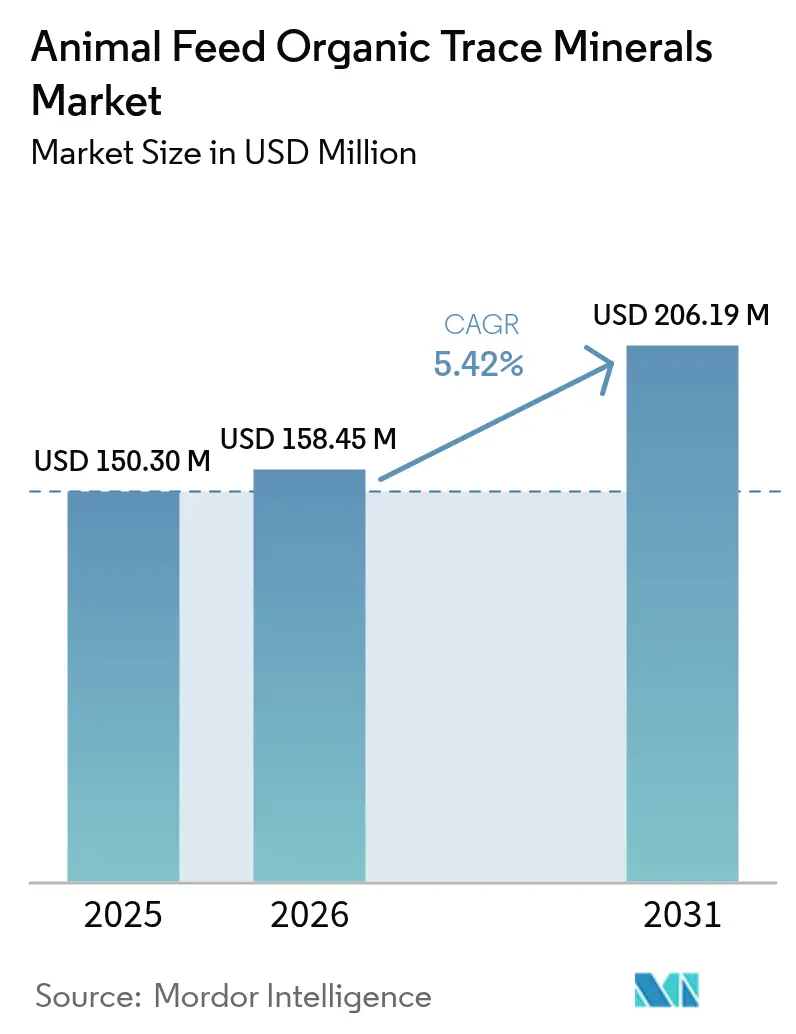

| Market Size (2026) | USD 158.45 Million |

| Market Size (2031) | USD 206.19 Million |

| Growth Rate (2026 - 2031) | 5.42% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Animal Feed Organic Trace Minerals Market Analysis by Mordor Intelligence

The animal feed organic trace minerals market size is expected to grow from USD 150.3 million in 2025 to USD 158.45 million in 2026 and is forecast to reach USD 206.19 million by 2031 at 5.42% CAGR over 2026-2031. The market expansion is driven by the transition from antibiotic growth promoters to bioavailable mineral solutions that comply with discharge regulations while maintaining productivity. Chelated minerals provide 2-3 times higher absorption compared to inorganic variants, allowing reduced inclusion rates without affecting animal performance. The adoption of digital feed-formulation technologies enhances dosage accuracy and demonstrates clear returns on investment. Market competition focuses on developing proprietary chelation technologies, implementing AI-based nutrition systems, and expanding regional production capacity to reduce supply chain vulnerabilities and protect customers from raw material price fluctuations.

Key Report Takeaways

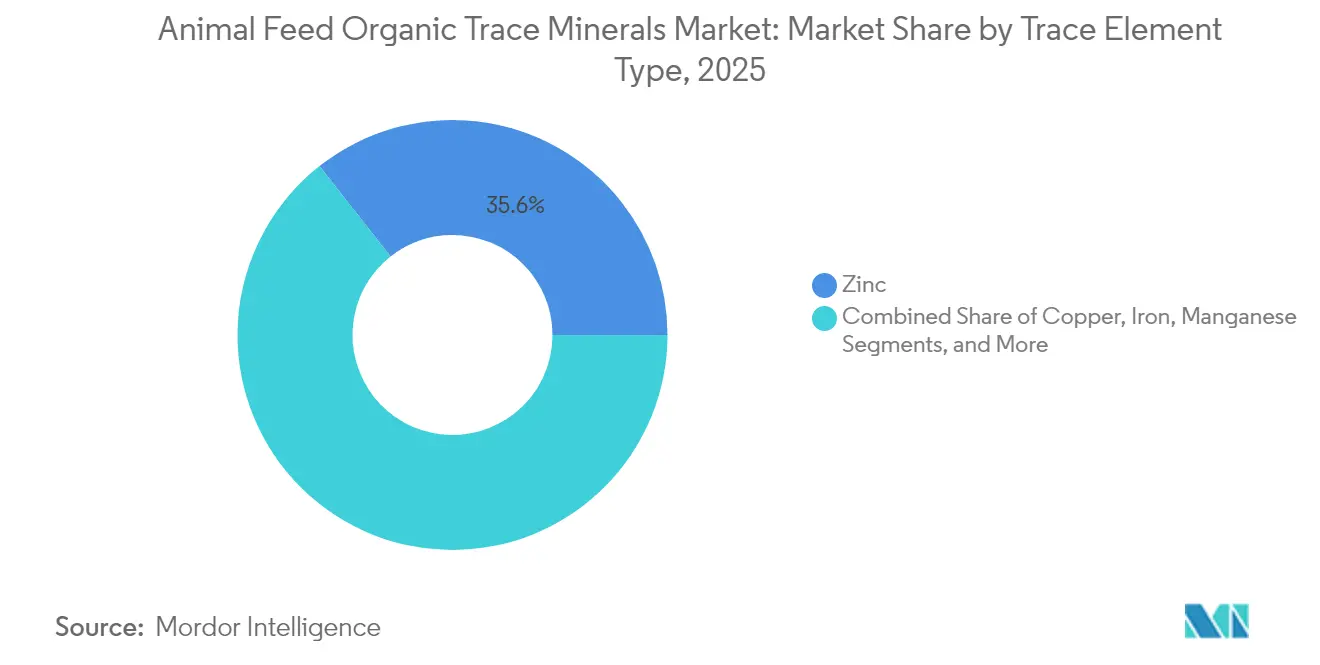

- By trace element type, zinc led with 35.62% of the animal feed organic trace minerals market share in 2025, while selenium is growing fastest at an 7.78% CAGR through 2031.

- By chelation type, amino-acid chelates controlled 39.74% revenue in 2025; hydroxy-trace minerals are advancing at a 9.74% CAGR through 2031.

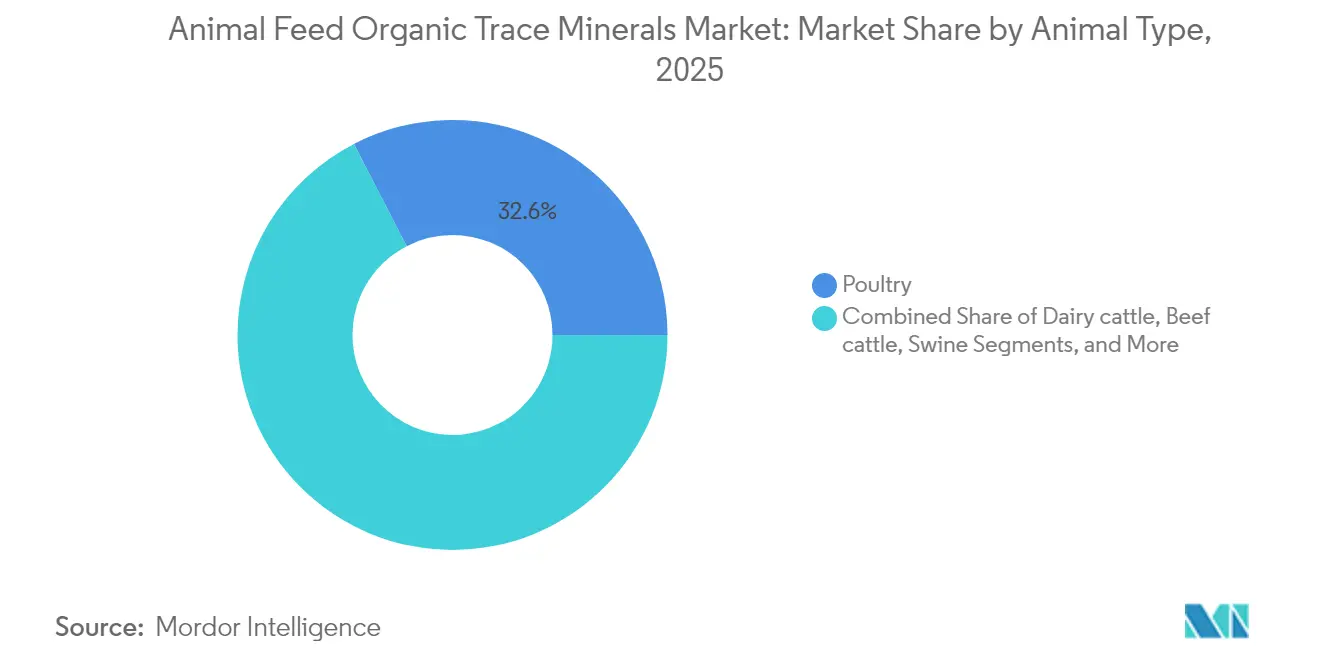

- By animal type, poultry captured 32.58% of 2025 revenue, and the aquaculture is expanding at a 8.92% CAGR to 2031.

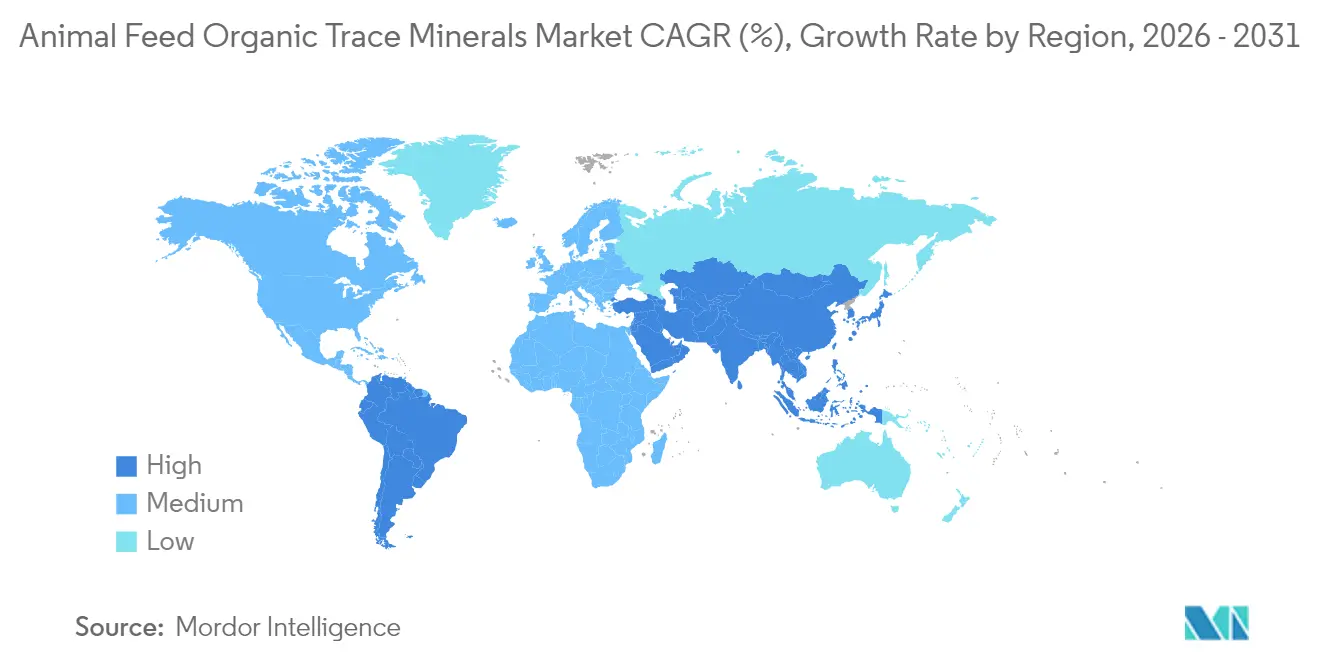

- By geography, Asia-Pacific accounted for 43.65% of revenue in 2025; the Middle East is accelerating at an 7.82% CAGR through 2031.

- The market shows moderate concentration, with five major companies accounting for 44% of annual revenue. Cargill, Incorporated leads with a 12% market share, followed by DSM-Firmenich (9.1%), Zinpro (8.2%), SHV (Nutreco NV) (A Bluestar Company) (7.6%), and Adisseo (6.9%).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Animal Feed Organic Trace Minerals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating demand for high-quality animal protein | +1.8% | Global, with concentration in Asia-Pacific and South America | Medium term (2–4 years) |

| Stringent bans on Antibiotic Growth Promoters (AGPs) | +1.5% | North America and Europe; expanding to Asia-Pacific | Short term (≤ 2 years) |

| Tighter manure-phosphorus and heavy-metal discharge regulations | +1.2% | North America and Europe; adoption emerging in Asia-Pacific | Medium term (2–4 years) |

| Rapid adoption of precision-chelation and micro-encapsulation technology | +0.9% | Global, led by developed markets | Long term (≥ 4 years) |

| Livestock carbon footprint measurement and dietary impact | +0.7% | Europe and North America, with pilot programs in Asia-Pacific | Long term (≥ 4 years) |

| AI-driven digital feed-formulation platforms standardizing organic trace minerals | +0.6% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Demand for High-Quality Animal Protein

The increasing disposable income in Asia-Pacific and South America has elevated the consumption of premium meat, milk, fish, and eggs, prompting producers to focus on nutritional value enhancement rather than volume production. The use of chelated selenium and zinc improves antioxidant levels, extends product shelf-life, and enhances sensory characteristics, enabling higher retail prices. Research indicates that bioavailable minerals deliver 3-5% better feed conversion compared to inorganic salts, compensating for higher additive costs while meeting lean-meat requirements. Retail chains include mineral-enrichment specifications in supplier agreements, driving adoption throughout integrated supply chains. Additionally, governments in regions with protein deficiency promote mineral optimization as part of their food security initiatives.

Stringent Bans on Antibiotic Growth Promoters (AGPs)

The ban on routine in-feed antibiotics by North American and European regulators, along with upcoming phase-out policies in Asia-Pacific markets, has created a productivity challenge in animal farming. Zinc and copper chelates have emerged as crucial alternatives, as they help maintain gut health and enhance immune function. Field trials conducted after the antibiotic ban demonstrate that organic mineral supplementation programs can achieve up to 90% of previous weight-gain performance, helping maintain profitability in intensive farming operations. Feed manufacturers are now combining chelated minerals with phytogenic compounds to develop antibiotic-free feed concentrates at premium price points. The implementation of antibiotic restrictions across emerging economies is expanding the market potential for animal feed organic trace minerals.

Tighter Manure-Phosphorus and Heavy-Metal Discharge Regulations

The Environmental Protection Agency's CAFO regulations and corresponding European Union directives establish strict limits on zinc, copper, and phosphorus excretion.[1]Environmental Protection Agency, “National Pollutant Discharge Elimination System, Concentrated Animal Feeding Operations,” epa.gov Chelated minerals reduce fecal losses by 20-40%, enabling producers to maintain compliance without compromising growth performance. Non-compliance results in financial penalties and damage to reputation, prompting integrators to implement precision-nutrition audits for verifying inclusion rates and excretion coefficients. Multiple U.S. states connect nutrient-management funding to verified reductions in mineral discharge, providing additional incentives for early adoption. These environmental requirements generate sustained demand that strengthens the growth prospects of the animal feed organic trace minerals market.

Rapid Adoption of Precision-Chelation and Micro-Encapsulation Technology

Hydroxy-trace minerals and next-generation chelates maintain their stability through acidic gut conditions, improving absorption and reducing antagonistic losses. Encapsulation protects sensitive ligands during pelleting and extrusion processes, ensuring nutrient consistency in high-temperature feed production. Producers report reduced mortality rates and more consistent weight distributions in broilers and shrimp, which is significant for processors operating with narrow margins. Technology providers integrate artificial intelligence-based formulation systems with real-time sensor data, enabling nutritionists to adjust chelated mineral levels based on weather conditions, water quality, and disease indicators. Analysis of total ownership costs demonstrates net cost advantages compared to inorganic programs when accounting for waste management expenses and performance improvements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing versus inorganic counterparts | -1.4% | Global; highest sensitivity in price-conscious markets | Short term (≤ 2 years) |

| Limited awareness among smallholder farmers | -1.1% | Asia-Pacific, Africa, and South America | Medium term (2–4 years) |

| Supply bottlenecks for key chelating ligands | -0.8% | Global, with concentration in amino acid supply chains | Short term (≤ 2 years) |

| Regulatory fragmentation across organic-livestock certification bodies | -0.6% | Global, with particular complexity in cross-border trade | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premium Pricing Versus Inorganic Counterparts

Organic trace minerals cost 2-4 times more than oxides or sulfates, which limits their adoption in the poultry and pig sectors, where feed represents over 70% of production costs. The volatility in corn and soybean meal prices increases scrutiny of feed additives. Producers require a return on investment analyses supported by data before implementing chelated mineral programs. Nutrition companies offer tiered product lines, volume rebates, and bundled formulations to distribute costs across multiple performance benefits. Digital calculators that convert inclusion rates into carcass-yield gains help demonstrate value beyond feed cost considerations.

Limited Awareness Among Smallholder Farmers

Family-operated herds and ponds constitute the primary livestock production systems across Asia-Pacific, Africa, and South America. The extension systems lack adequate resources to disseminate advanced mineral-nutrition knowledge. Limited understanding of proper dosage, compatibility, and return on investment restricts adoption, concentrating sales among commercial integrators. The information gap is narrowing through language-specific manuals, radio programming, and demonstration farm trials. The animal feed organic trace minerals market is expanding through emerging partnerships between mineral suppliers, local cooperatives, and microfinance institutions that combine technical training with product access.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Trace Element Type: Zinc Dominance Amid Selenium Surge

Zinc maintained 35.62% of the animal feed organic trace minerals market share in 2025, supported by its essential role in over 80 metalloenzymes that influence immune function, epithelial integrity, and reproduction. The higher bioavailability of organic zinc enables producers to reduce dietary inclusion rates while meeting environmental excretion limits, resulting in lower environmental fees and improved profit margins. Selenium, despite its minimal dietary requirement, achieved the highest growth rate at 7.78% CAGR, driven by processors seeking enhanced antioxidant properties to extend the shelf-life of chilled meat, particularly in aquaculture fillets susceptible to oxidative deterioration during maritime transport. Copper, manganese, and iron remain essential nutrients but face strict inclusion limits, increasing the demand for chelated forms that maintain performance at reduced concentrations.

The distribution of trace elements reflects both biological requirements and regulatory constraints. While zinc maintains market dominance, selenium commands higher prices and benefits from marketing advantages through "selenium-enriched" product labeling. Cobalt and chromium serve specific functions in rumen metabolism and glucose utilization, while iodine and molybdenum address regional deficiency issues. Market growth favors elements that improve product quality while helping meet waste management regulations. These factors create an interconnected foundation for the animal feed organic trace minerals market.

By Chelation Type: Amino-Acid Supremacy Challenged by Hydroxy Innovation

Amino-acid chelates accounted for 39.74% of revenue in 2025, driven by established production methods, widespread regulatory approval, and compatibility with existing formulation matrices. These remain the preferred choice for poultry operations focused on established cost-effectiveness. While the animal feed organic trace minerals market for amino-acid chelates continues to grow, hydroxy-trace minerals are gaining momentum with a 9.74% CAGR, attributed to their enhanced stability in acidic gut environments and reduced mineral interactions.

Proteinates and polysaccharide complexes maintain specific market segments where taste preferences or controlled-release properties offer distinct benefits, particularly in ruminant total mixed rations and fish-feed pellets. Yeast-based mineral complexes combine probiotic benefits with mineral supplementation, appealing to customers seeking to reduce additive components. Propionate chelates serve certified-organic operations that avoid synthetic amino acids. Market competition centers on patent development for ligand ratios, particle characteristics, and coating methods to achieve specific release patterns. These technological developments will continue to shape the animal feed organic trace minerals market through 2031.

By Animal Type: Poultry Leadership Amid Aquaculture Acceleration

Poultry accounted for 32.58% of 2025 revenue, driven by vertically integrated broiler and layer operations that require precise mineral specifications to optimize feed conversion and egg shell integrity. The use of organic zinc, copper, and manganese improves bone strength and eggshell quality, which reduces cull rates and increases economic efficiency. The aquaculture segment is growing at a 8.92% CAGR, the highest in the animal feed organic trace minerals market, as fish and shrimp farms increase stocking densities and focus on mineral optimization to reduce disease outbreaks and avoid water pollution penalties.

The dairy cattle segment maintains a significant market share due to extended lactation periods that require optimal mineral levels for reproductive performance and milk quality control. Swine producers use organic minerals to reduce post-weaning diarrhea and enhance growth in antibiotic-free facilities. Pet food manufacturers incorporate chelated minerals in premium and therapeutic diets to meet the growing consumer demand for functional benefits. While equine and specialty species contribute to market demand, the primary volume competition remains between intensive poultry operations and expanding aquaculture facilities.

Geography Analysis

Asia-Pacific holds 43.65% of the 2025 revenue in the animal feed organic trace minerals market, driven by China's aquaculture production and India's growing broiler and shrimp industries. Government subsidies for domestic feed additives increase the adoption of high-absorption mineral formats. The region's market size benefits from concentrated production clusters that reduce logistics costs and enable direct relationships between suppliers and integrators. Japan and South Korea's technical expertise and research capabilities support the implementation of advanced chelates with proven environmental benefits.

The Middle East market projects an 7.82% CAGR through 2031, supported by government investments in protein production capacity, including Saudi Arabia's target of 600,000 metric tons of fish by 2030. The region's water scarcity necessitates precise mineral feeding to reduce effluent discharge. Feed mills positioned near coastal farming centers minimize oxidation during transport, increasing demand for temperature-resistant trace mineral formats.

North America and Europe represent established markets where regulatory requirements and sustainability commitments generate steady growth. The FDA's Veterinary Feed Directive and European restrictions on antibiotic usage encourage organic mineral supplementation to maintain animal performance. Environmental regulations on mineral discharge promote the use of highly bioavailable forms. South America shows growth potential as swine and poultry integrators enhance nutrition programs to comply with export market requirements, balancing cost considerations with increased adoption of chelated minerals. These regional developments indicate diverse growth opportunities in the animal feed organic trace minerals market.

Competitive Landscape

The market demonstrates moderate concentration with five major players controlling 44% of annual revenue. Cargill, Incorporated holds 12% market share, followed by DSM-Firmenich at 9.1%, Zinpro at 8.2%, SHV (Nutreco NV) (A Bluestar Company) at 7.6%, and Adisseo at 6.9%. The remaining market share provides opportunities for mid-sized specialists and regional companies. Industry consolidation continues, as evidenced by Nutreco's 2024 acquisition of Micronutrients (now Selko), which consolidated its chelation portfolio and distribution. Cargill expanded its market presence through mill acquisitions and a Saudi aquaculture venture, strengthening its feed-to-fork capabilities while increasing demand for its mineral products.

Innovation drives competitive differentiation in the market. DSM-Firmenich increased its regional capacity by 100,000 metric tons with its Sete Lagoas plant, which includes analytics laboratories for developing mineral premixes suited to Brazil's diverse climate zones. Zinpro introduced TruCare LQ Zn, a water-soluble zinc product for stressed piglets that complies with large barn biosecurity requirements. Second-tier suppliers focus their research and development on polysaccharide or yeast-based complexes, often collaborating with local universities to validate effectiveness across different species.

Market entry barriers include regulatory requirements, specialized application knowledge, and global logistics capabilities. Companies that integrate patented chemical formulations with AI-supported formulation software and comprehensive technical support establish long-term customer relationships. Leading food companies increasingly require sustainability audits and carbon-footprint monitoring, benefiting mineral suppliers that can demonstrate reduced waste and transparent sourcing practices. These factors shape the animal feed organic trace minerals market structure.

Animal Feed Organic Trace Minerals Industry Leaders

Cargill, Incorporated

DSM-Firmenich

Zinpro

SHV (Nutreco NV)

Adisseo (A Bluestar Company)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Biochem developed BetaTrace, a patent-pending organic source of zinc, copper, manganese, and iron formulated for use across all animal species.

- November 2024: AgroCares and Trouw Nutrition renewed cooperation on NutriOpt On-site Adviser, linking NIR scanner data with nutrient databases for rapid feed assessment.

- October 2024: DSM-Firmenich opened a 100,000 metric tons animal-nutrition factory in Sete Lagoas, Brazil, enhancing South America supply resilience.

- September 2024: Cargill launched the USD 3 million NutriHarvest initiative to bolster food security for 119,000 farmers in India, Kenya, Tanzania, and Guatemala.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the animal feed organic trace minerals market as the sale of zinc, copper, iron, manganese, selenium, cobalt, chromium, and related chelated complexes (amino-acid, proteinate, polysaccharide, hydroxy, yeast based, and propionate) that are intentionally blended into commercial feed or premixes to increase mineral bioavailability and improve livestock growth, fertility, immunity, and feed efficiency across poultry, ruminant, swine, aquaculture, pet, and equine segments worldwide.

Exclusion: products containing purely inorganic salts or nano-mineral formulations are outside this scope.

Segmentation Overview

- By Trace Element Type

- Zinc

- Copper

- Iron

- Manganese

- Selenium

- Cobalt

- Chromium

- Others

- By Chelation Type

- Amino-Acid Chelates

- Proteinates

- Polysaccharide Complexes

- Hydroxy-Trace Minerals

- Propionates

- Yeast-Based Complexes

- Others

- By Animal Type

- Dairy cattle

- Beef cattle

- Poultry

- Swine

- Aquaculture

- Pets

- Equine

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Middle East

- Saudi Arabia

- Turkey

- UAE

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Kenya

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview nutritionists at leading feed mills, veterinarians in Asia, Europe, and the Americas, and regional distributors who track monthly premix pricing. Surveys with poultry and dairy producers clarify inclusion rates and anticipated switching from inorganic to organic variants, filling gaps left by desk research and stress-testing early model outputs.

Desk Research

We begin with granular trade and production statistics from FAO FAOSTAT, UN Comtrade, and USDA FAS that reveal mineral content in compound feed flows across more than 120 countries. Industry association data, such as IFIF feed tonnage, CLAL dairy numbers, and European Feed Manufacturers Federation (FEFAC) ingredient splits, help us map livestock species demand patterns. Academic journals on chelation bio-efficacy, patent filings retrieved via Questel, and company 10-Ks round out the scientific and commercial context. D&B Hoovers and Dow Jones Factiva supply revenue splits that anchor supplier roll-ups. This list is illustrative; several other open and subscription sources are reviewed for validation.

Market-Sizing & Forecasting

We employ a top-down feed-tonnage reconstruction. National feed output is multiplied by species-level mineral inclusion norms and organic substitution ratios, which are then priced using region-specific average selling prices collected in primary calls. Supplier revenue roll-ups and channel checks serve as selective bottom-up counterpoints that fine-tune totals. Key drivers include feed production growth, chelate penetration rates, average chelated mineral dosages, regulatory limits on heavy-metal excretion, species mix shifts, and chelate price differentials versus inorganic salts. Forecasts to 2030 rely on multivariate regression and scenario analysis tied to livestock herd projections, commodity price indices, and announced capacity additions, with expert consensus guiding final scenario weighting.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated variance screens, peer analyst audits, and senior-review sign-off. Any variance above predefined thresholds triggers re-contact with sources. Models refresh annually, and interim updates occur when regulation, disease outbreaks, or major capacity changes materially affect baselines.

Why Mordor's Animal Feed Organic Trace Minerals Baseline Is Dependable

Published estimates differ because firms choose dissimilar product mixes, livestock coverage, and update cadences. Our disciplined scope, substitution-ratio tracking, and annual refresh minimize such divergence.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 150.3 M | Mordor Intelligence | - |

| USD 794.7 M (2024) | Global Consultancy A | broader ingredient basket includes inorganic salts and vitamin blends; limited primary validation |

| USD 802.3 M (2024) | Industry Publication B | assumes uniform chelate pricing across regions and static substitution rates |

| USD 846.2 M (2025) | Regional Consultancy C | inflates base year by using feed production forecasts rather than reported production for baseline |

The comparison shows how differing scopes and untested assumptions can inflate values five-fold. By grounding our model in verified feed tonnage, real-world substitution ratios, and continual source feedback, Mordor delivers a transparent, balanced baseline that decision-makers can rely on.

Key Questions Answered in the Report

What is the current size of the animal feed organic trace minerals market?

The market generated USD 158.45 million in 2026 and is forecast to reach USD 206.19 million by 2031 at a 5.42% CAGR.

Which trace element dominates sales?

Zinc leads with 35.62% revenue share in 2025, reflecting its central role in immune and metabolic functions.

Why are hydroxy-trace minerals growing faster than other chelation types?

Their superior stability in acidic gut conditions and lower antagonistic interactions underpin a 9.74% CAGR through 2031.

Which animal type segment shows the highest growth?

Aquaculture registers a 8.92% CAGR as intensive fish and shrimp farms adopt bioavailable minerals to manage health and water quality.

How do environmental regulations influence adoption?

Stricter discharge limits on zinc, copper, and phosphorus favor chelated minerals that slash fecal excretion by up to 40%, aiding compliance and lowering fines.

Page last updated on: