Retail Stores Pet Food Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 93.10 Billion |

| Market Size (2031) | USD 115.90 Billion |

| Growth Rate (2026 - 2031) | 4.50% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Retail Stores Pet Food Market Analysis by Mordor Intelligence

The retail stores pet food market size was valued at USD 88.70 billion in 2025 and is projected to grow from USD 93.10 billion in 2026 to USD 115.90 billion by 2031, registering a CAGR of 4.5% from 2026 to 2031. The market is primarily influenced by the trend of pet humanization, where pet owners increasingly apply food, wellness, and nutrition standards traditionally reserved for humans to their pets. This trend is driving higher average basket values across pet specialty stores, supermarkets, and mass retailers, as consumers opt for higher-protein, life-stage-specific, and function-focused products. Additionally, the market is benefiting from the growing acceptance of fresh and refrigerated pet food formats, which is expanding premium shelf space in mainstream retail chains beyond specialty outlets. However, the market faces challenges such as competition from online auto-ship programs, compliance costs associated with fresh and raw formats, and slower volume growth, which emphasizes the importance of value mix over unit expansion. Competition in the market is driven by factors such as branded shelf control, premium private label offerings, store format differentiation, and effective cold-chain management. These factors underscore the continued relevance of physical retail, even as digital replenishment gains traction.

Key Report Takeaways

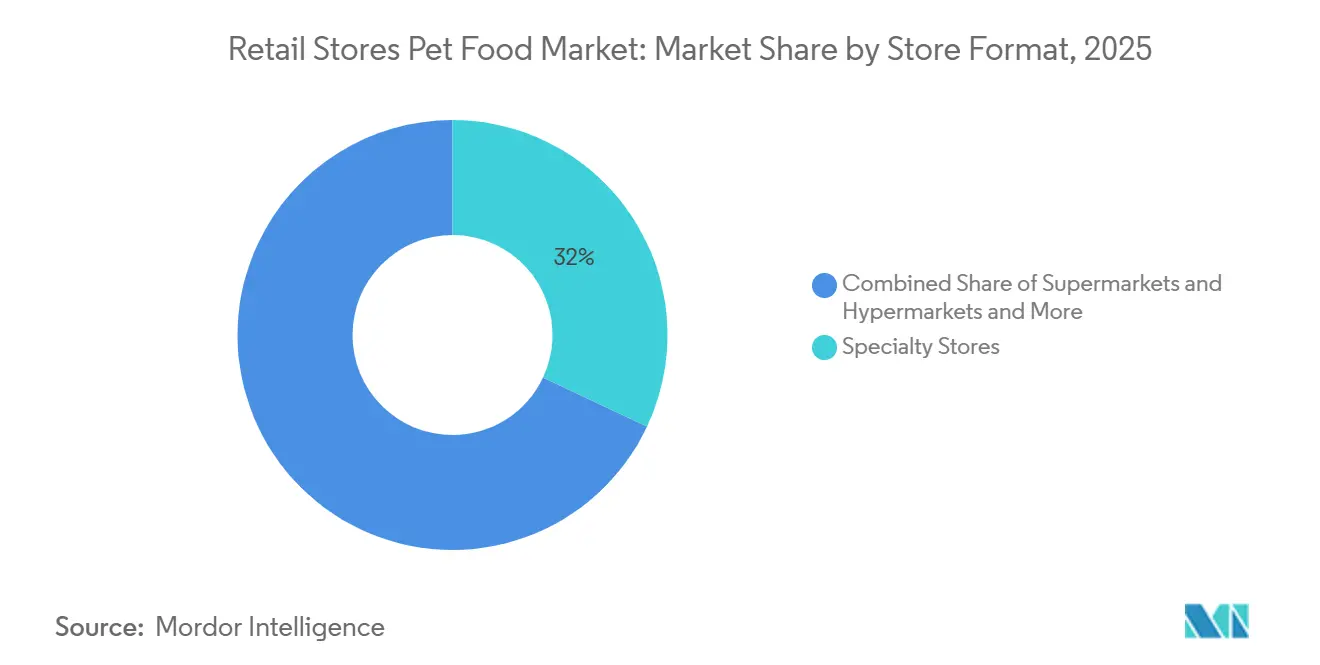

- By store format, the retail stores pet food market for pet specialty stores accounted for the largest 32.0% in 2025, and it is also the fastest segment projected to grow at a CAGR of 5.6% from 2026 to 2031.

- By pet type, dog food was the largest segment with 49.8% share in 2025, while cat food is forecast to grow at the fastest CAGR of 5.8% CAGR from 2026 to 2031.

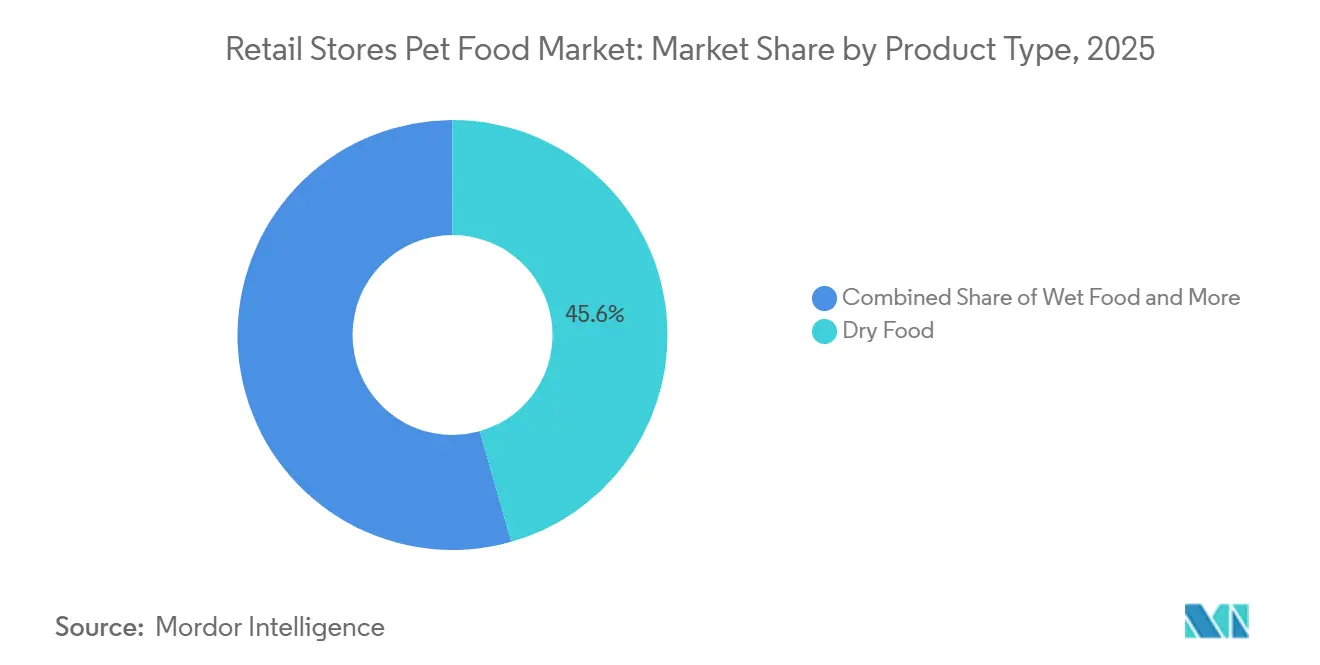

- By product type, dry food accounted for the largest 45.6% revenue share in 2025, while fresh and refrigerated food is projected to grow at the fastest CAGR of 8.5% from 2026 to 2031.

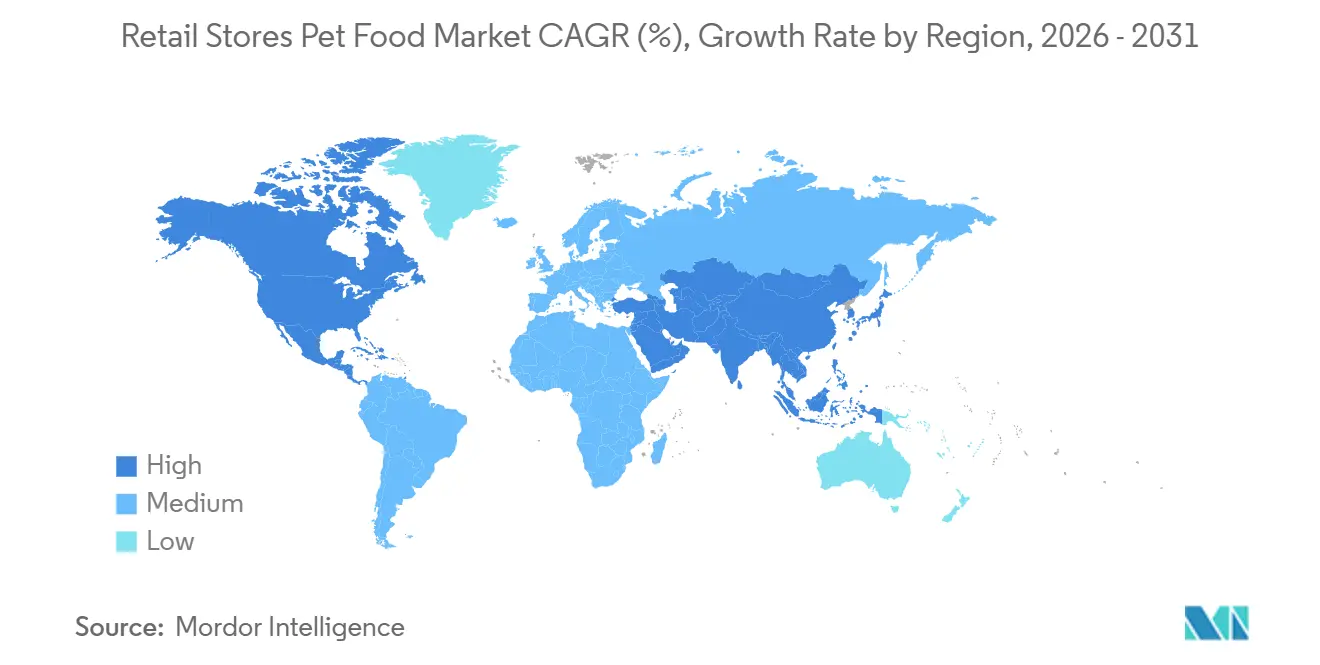

- By geography, North America held the largest 45.3% revenue share in 2025, while Asia-Pacific is forecast to grow at the fastest CAGR of 6.2% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Retail Stores Pet Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization and pet humanization lift store baskets | +1.2% | Global | Short term (≤ 2 years) |

| Functional and science-backed nutrition accelerate trade-up | +0.9% | North America and Europe | Medium term (2-4 years) |

| Cat-care mix expansion improves category productivity | +0.5% | Global, particularly Asia-Pacific and Europe | Medium term (2-4 years) |

| Pet specialty expansion and premium private label widen in-store choice | +0.6% | North America and Asia-Pacific | Short term (≤ 2 years) |

| Refrigerated fixture rollout unlocks fresh-food conversion | +0.7% | North America, emerging Asia-Pacific, and Europe | Medium term (2-4 years) |

| AI-led assortment localization improves on-shelf relevance and sell-through | +0.4% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premiumization and Pet Humanization Lift Store Baskets

The retail stores pet food market is experiencing growth due to the increasing trend of pet humanization, where pet owners treat pets as family members and prioritize their health and well-being. This has led to a rise in the purchase of premium, specialized, and health-focused pet food products through physical retail outlets. Furthermore, the growing pet population is driving demand. According to the UK Pet Food survey, in 2026, the pet population in the United Kingdom reached 36.5 million, an increase of approximately half a million compared to two years prior, highlighting the expanding consumer base for pet-related products[1]Source: UK Pet Food, “UK Pet Population,” ukpetfood.org.. As pet ownership grows and demand for higher-quality nutrition increases, retailers are allocating more shelf space to premium products and enhancing in-store merchandising strategies.

Functional and Science-Backed Nutrition Accelerate Trade-Up

The retail stores pet food market is experiencing growth due to rising demand for nutrition products that provide specific health benefits, such as digestive support, immunity enhancement, improved mobility, and healthy aging. Pet owners are increasingly prioritizing ingredient quality and scientifically validated formulations, driving a shift toward premium and specialized pet food categories. Physical retail channels continue to play a significant role, as they enable consumers to compare products, assess nutritional claims, and seek expert advice before making a purchase. According to BENEO, in 2024, a survey revealed that over one-third of pet owners provide their pets with products featuring digestive health claims, reflecting a growing preference for function-focused nutrition. As health-oriented feeding becomes more prevalent, retailers are dedicating more shelf space to premium and science-based pet food products.

Refrigerated Fixture Rollout Unlocks Fresh-Food Conversion

The retail stores pet food market is transforming due to the expansion of refrigerated retail infrastructure, which enhances consumer access to fresh and minimally processed pet food products. Fresh pet food depends on visible and reliable cold-chain placement to attract customers and encourage repeat purchases, making refrigerated fixtures essential for category growth. As retailers expand refrigerated pet food sections, consumers are increasingly exposed to fresh nutrition options during routine shopping trips. In April 2025, JustFoodForDogs expanded its fresh-frozen dog food line to over 900 PetSmart locations across the United States, significantly boosting the in-store availability of fresh pet food products. This expansion highlights how broader refrigerated distribution can drive consumer adoption and create new purchasing opportunities within retail stores.

AI-Led Assortment Localization Improves On-Shelf Relevance and Sell-Through

The retail stores pet food market is experiencing growth through the adoption of artificial intelligence and advanced analytics, which are being utilized to optimize assortment planning, inventory allocation, and merchandising strategies. Retailers and manufacturers are employing these technologies to analyze local purchasing patterns and customize product selections to meet the specific demands of individual stores and communities. This data-driven approach enhances product availability, minimizes stock inefficiencies, and ensures the relevance of on-shelf offerings. By making more precise assortment decisions, retailers can increase shelf productivity, improve customer satisfaction, and achieve higher sell-through rates across premium, functional, and specialized pet food categories.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce auto-ship erodes routine store replenishment | -1.2% | North America and Europe, emerging in Asia-Pacific | Short term (≤ 2 years) |

| Ingredient and packaging cost volatility compress margins | -0.8% | Global | Medium term (2-4 years) |

| Shrink and damaged-bag losses weaken bulky kibble economics | -0.5% | North America and Europe | Short term (≤ 2 years) |

| Fresh and raw compliance burden raises cold-chain costs | -0.3% | North America, Europe, and Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Auto-Ship Erodes Routine Store Replenishment

The retail stores pet food market is under growing pressure from online purchasing models that diminish the necessity for routine store visits. Subscription programs, auto-replenishment services, and digital marketplaces provide convenience and predictable delivery schedules, making them appealing for frequently purchased pet food products. Once consumers adopt recurring online purchasing habits, physical retailers face increased challenges in maintaining repeat traffic for routine replenishment purchases. This trend is particularly noticeable in China, where digital commerce plays a significant role in pet product sales. According to the United States Department of Agriculture Foreign Agricultural Service, online channels were a key driver of China's pet industry growth in 2025, fueled by consumers' rising preference for digital engagement and e-commerce purchasing[2]Source: United States Department of Agriculture Foreign Agricultural Service, “Pet Food Market Update 2026,” apps.fas.usda.gov.. As online penetration continues to grow, traditional retail stores may see a decline in visit frequency and fewer opportunities for routine pet food sales.

Ingredient and Packaging Cost Volatility Compress Margins

The retail stores pet food market faces challenges due to persistent volatility in ingredient and packaging costs, complicating price management for both retailers and manufacturers. Wet food and canned products are particularly affected, as they rely heavily on metal packaging, which is highly sensitive to fluctuations in raw material and manufacturing costs. When retail prices fail to fully absorb these cost increases, margin pressures intensify, especially for smaller brands with limited purchasing power. Data from the Federal Reserve Bank of St. Louis indicates that the Producer Price Index for Aluminum Cans and Can Components rose from 171.2 in November 2025 to 188.7 in April 2026, underscoring the growing cost pressures within the supply chain[3]Source: Federal Reserve Bank of St. Louis, “Producer Price Index by Commodity: Metals and Metal Products: Aluminum Cans and Can Components,” fred.stlouisfed.org.. These fluctuations can reduce profitability, restrict pricing flexibility, and hinder growth in the retail stores pet food market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Store Format: Pet Specialty Stores Drive a Dual-Speed Advantage

The retail stores pet food market share for the pet specialty stores held the largest 32.0% in 2025, representing the largest share among retail channels. This dominance is attributed to their ability to offer curated assortments, category expertise, and a superior shopping experience compared to broader retail formats. These stores excel in merchandising premium, super-premium, and function-focused pet food products, which often require product education and guided purchasing decisions. Additionally, they provide manufacturers with greater flexibility to showcase innovative and differentiated offerings. As consumer preferences shift toward specialized nutrition and premium feeding solutions, pet specialty stores continue to solidify their position within the retail distribution landscape.

The retail stores pet food market size for the pet specialty stores is projected to grow at the fastest CAGR of 5.6% from 2026 to 2031. This growth is driven by increasing consumer interest in premium nutrition, personalized product recommendations, and specialized pet care solutions. The format's ability to offer a deeper category selection and a more consultative shopping environment than mass retail channels further supports its expansion. Pet owners seeking functional nutrition, breed-specific products, and premium feeding options often favor specialty retailers due to their focused assortments and expertise. As premiumization trends persist across pet food categories, specialty stores are well-positioned to capture additional consumer spending and enhance customer loyalty.

By Pet Type: Dog Food Anchors Volume, Cat Food Drives Incremental Value

Dog food held the largest segment, accounting for 49.8% of the market in 2025. Its leading position is supported by a broad product portfolio spanning breed-specific nutrition, life-stage formulations, treats, fresh meals, and functional feeding solutions. Dog food maintains strong visibility across all major retail formats, including pet specialty stores, supermarkets, mass merchandisers, and convenience stores. The category also remains a primary focus for product innovation and promotional activity. Its extensive distribution network and wide consumer appeal continue to make dog food the foundation of retail pet food sales and category planning.

Cat food is anticipated to grow at the fastest CAGR of 5.8% from 2026 to 2031. This growth is driven by increasing urbanization, rising cat ownership in smaller households, and heightened demand for premium nutrition products. Cat owners are increasingly drawn to specialized formulations, including functional, wet, grain-free, and health-focused diets. The segment also benefits from shifting feeding preferences that emphasize convenience and nutritional quality. As manufacturers expand premium product offerings and retailers dedicate more shelf space to specialized cat nutrition, the category is well-positioned for significant value growth across retail distribution channels.

By Product Type: Dry Food Holds the Base and Fresh Formats Expand the Edge

Dry food held the largest 45.6% revenue share in 2025. This segment remains a key component of retail pet food distribution due to its affordability, long shelf life, ease of storage, and widespread consumer acceptance. Dry food is compatible with all major retail formats and facilitates efficient inventory management for retailers. Its broad availability and diverse product range consistently attract store traffic. Additionally, the format plays a significant role in private-label development and promotional initiatives, underscoring its importance within the retail pet food market.

Fresh and refrigerated food is projected to grow at the fastest CAGR of 8.5% from 2026 to 2031. This growth is driven by increasing consumer demand for minimally processed nutrition, ingredient transparency, and premium feeding options. The expansion of refrigerated infrastructure across retail channels is enhancing product availability and exposing more consumers to fresh pet food options. Retailers are dedicating more shelf space to fresh and refrigerated products as shoppers explore alternatives to traditional dry food. With growing awareness of fresh feeding, this category is gaining popularity among pet owners seeking higher-quality and specialized nutritional solutions.

Geography Analysis

North America held the largest 45.3% revenue share in 2025. The region benefits from high pet ownership, strong consumer spending on pet care, and a well-developed retail infrastructure that supports premium and functional pet food products. Pet specialty stores, supermarkets, and mass merchandisers provide extensive market coverage and broad product availability. Consumers in the region demonstrate strong interest in premium nutrition, fresh food, and specialized feeding solutions, encouraging continuous product innovation. The combination of mature retail networks, high product penetration, and advanced merchandising capabilities continues to reinforce North America's leadership position.

Asia-Pacific is projected to grow at the fastest CAGR of 6.2% from 2026 to 2031. Growth is being driven by rising pet ownership, expanding middle-class populations, increasing urbanization, and greater awareness of commercial pet nutrition. Consumers across the region are increasingly interested in branded, premium, and health-focused pet food products. Markets such as China, Japan, South Korea, Australia, and India are contributing to category expansion through different stages of market development. This combination of mature premium markets and emerging adoption opportunities provides significant momentum for retail pet food sales across the region.

Europe remains a significant market for retail pet food stores, driven by high pet ownership rates, established retail distribution networks, and strong consumer demand for premium pet nutrition products. According to the European Pet Food Industry Federation (FEDIAF), annual pet food sales in Europe reached EUR 29.3 billion (USD 33.7 billion) in 2025, representing a 9% year-over-year growth. This reflects increased consumer spending on pet food and also growth in the sales across supermarkets, hypermarkets, pet specialty stores, and other retail channels. This growth has prompted retailers to expand premium product assortments, allocate more shelf space, and enhance in-store offerings.

Competitive Landscape

The retail stores pet food market is moderately consolidated, with major players including Mars, Incorporated, Nestlé S.A., Colgate-Palmolive Company, General Mills, Inc., and The J. M. Smucker Company. The competitive structure is dominated by multinational manufacturers with extensive product portfolios and broad retail distribution networks. Key players compete across categories such as dry food, wet food, treats, veterinary nutrition, and premium products, leveraging strong brand recognition and established relationships with retailers. Competitive differentiation increasingly relies on product innovation, premium positioning, and category expertise. Additionally, private-label products are gaining significance as retailers enhance product quality and strengthen their value propositions. This combination of branded leadership and retailer participation sustains a dynamic competitive environment in global markets.

Competition is increasingly focused on premium nutrition, functional formulations, and unique product formats. Manufacturers are broadening their offerings to emphasize health benefits, ingredient transparency, and specialized nutritional requirements, aiming to attract higher-value consumer spending. Fresh, refrigerated, freeze-dried, and minimally processed products are gaining importance as consumer preferences shift away from traditional feeding formats. Retailers are facilitating this transition by allocating more shelf space, implementing premium merchandising strategies, and enhancing in-store product education. Consequently, innovation in nutrition and product presentation continues to shape competitive positioning within the industry.

Distribution expansion is a critical competitive strategy for companies aiming to enhance consumer access and shelf visibility. In December 2025, Stella and Chewy's extended its freeze-dried raw pet food portfolio to 464 Sprouts Farmers Market stores across the United States, significantly increasing availability through a prominent grocery retail network. Expanding distribution improves product visibility, enhances consumer accessibility, and promotes the adoption of premium categories beyond specialty retail channels. Combined with investments in merchandising, retail partnerships, and product innovation, distribution growth remains a key factor influencing competitive dynamics and market share within the industry.

Retail Stores Pet Food Industry Leaders

Mars, Incorporated

Nestlé S.A.

Colgate-Palmolive Company

General Mills, Inc.

The J. M. Smucker Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Mars, Incorporated partnered with Big Idea Ventures, AAK, Bühler, Givaudan, and Ingredion to launch the 2026 Global Pet Food Innovation Program. This program aims to develop advanced nutrition solutions for future pet food products. It is projected to drive product innovation and premiumization within retail pet food channels.

- March 2026: Nestlé S.A. has inaugurated a new wet pet food manufacturing facility in Vargeão, Brazil, to enhance production capacity for dog and cat food products distributed through retail channels. This investment aims to improve product availability across supermarkets, pet specialty stores, and other retail outlets.

- October 2025: General Mills, Inc. introduced Blue Buffalo Love Made Fresh nationwide, marking the brand's entry into the fresh pet food category. This launch established Blue Buffalo as the largest pet food brand in the United States to offer dry, wet, and fresh feeding solutions, while increasing the availability of fresh pet food through major retail channels.

Global Retail Stores Pet Food Market Report Scope

Retail store pet food refers to pet food products available through physical retail channels such as pet specialty stores, supermarkets, hypermarkets, convenience stores, and other brick-and-mortar outlets. These channels allow consumers to purchase pet nutrition products directly in-store. The Retail Stores Pet Food Market Report is Segmented by Store Format (Pet Specialty Stores, Supermarkets and Hypermarkets, and More), by Pet Type (Dog Food, Cat Food, Bird Food, and More), by Product Type (Dry Food, Wet Food, Treats and Toppers, Fresh and Refrigerated Food, and More), and by Geography (North America, South America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Pet Specialty Stores |

| Supermarkets and Hypermarkets |

| Mass Merchandisers and Club Stores |

| Convenience Stores |

| Other Retail Stores |

| Dog Food |

| Cat Food |

| Bird Food |

| Fish Food |

| Small Mammal and Reptile Food |

| Other Pets |

| Dry Food |

| Wet Food |

| Treats and Toppers |

| Fresh and Refrigerated Food |

| Frozen and Freeze-Dried Food |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Indonesia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Store Format | Pet Specialty Stores | |

| Supermarkets and Hypermarkets | ||

| Mass Merchandisers and Club Stores | ||

| Convenience Stores | ||

| Other Retail Stores | ||

| By Pet Type | Dog Food | |

| Cat Food | ||

| Bird Food | ||

| Fish Food | ||

| Small Mammal and Reptile Food | ||

| Other Pets | ||

| By Product Type | Dry Food | |

| Wet Food | ||

| Treats and Toppers | ||

| Fresh and Refrigerated Food | ||

| Frozen and Freeze-Dried Food | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is driving growth in retail stores pet food sales through 2031?

Growth is being supported mainly by pet humanization, stronger premiumization, function-led nutrition, and wider acceptance of fresh and refrigerated products in physical retail.

What is the market value of retail stores pet food market in 2025?

The retail stores pet food market size was valued at USD 88.70 billion in 2025.

Which store format leads physical pet food sales?

Pet specialty stores are the largest format with 32.0% market share in 2025.

Why is cat food growing faster than dog food in stores?

Cat food is projected to grow at the fastest CAGR of 5.8% from 2026 to 2031, driven by urban living trends, smaller household sizes, and the increasing demand for premium wet and functional formats, which are contributing to faster value growth.

Page last updated on: