Animal Feed Micronutrients Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 1.7 Billion |

| Market Size (2030) | USD 2.70 Billion |

| Growth Rate (2025 - 2030) | 9.60% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

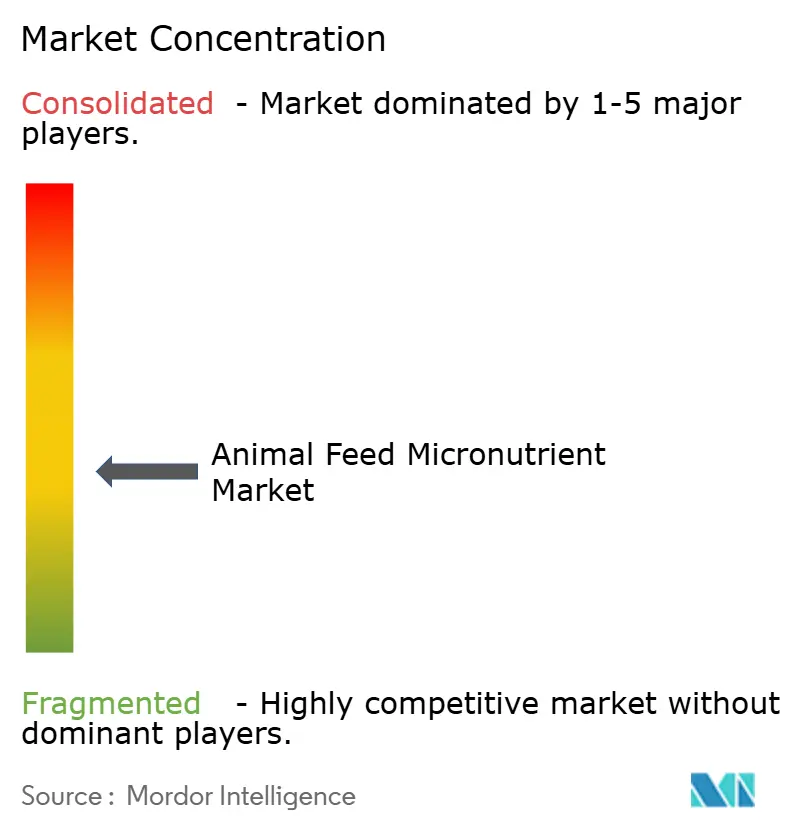

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Animal Feed Micronutrients Market Analysis by Mordor Intelligence

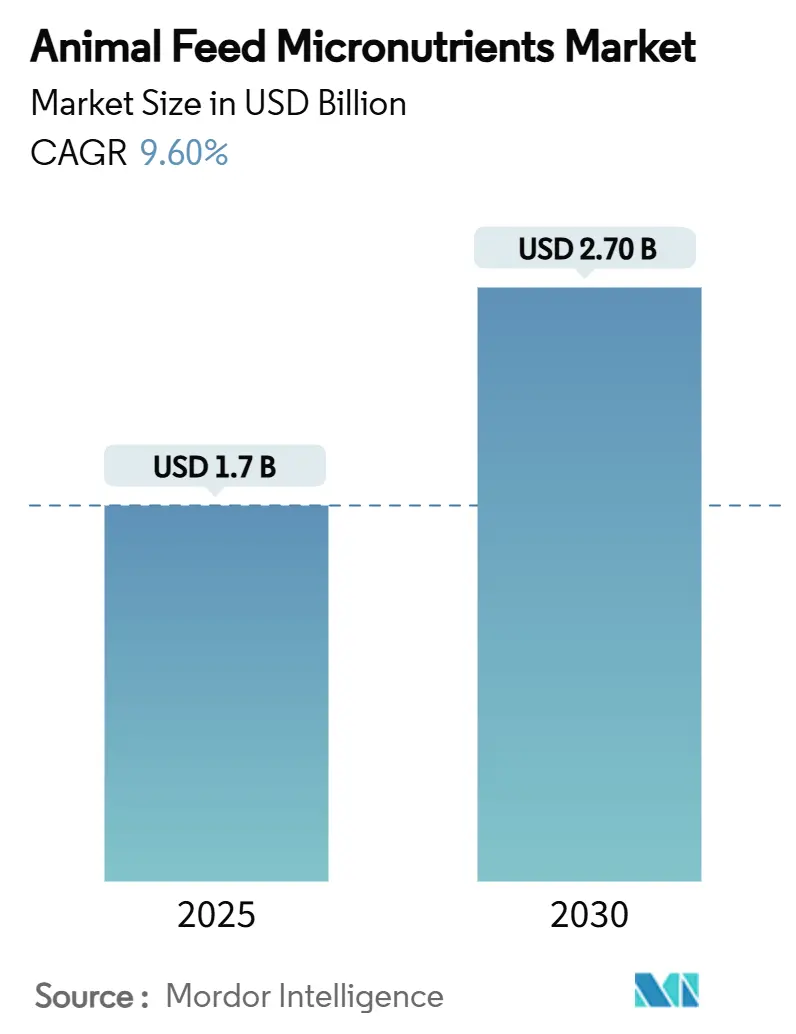

The animal feed micronutrients market size was USD 1.7 billion in 2025 and is projected to reach USD 2.7 billion by 2030, growing at a 9.6% CAGR over the forecast period [1]Source: U.S. Food and Drug Administration, “Evaluation of FDA Pre-Market Animal Food Programs and Plan for Consultations,” fda.gov. A steady shift toward precision nutrition in intensive livestock operations, stricter regulations on feed safety, and expanding protein demand in emerging economies underpin this growth trajectory. Regulatory modernization in the United States and the European Union is accelerating the approval of innovative formulations, while producers in the Asia-Pacific region are scaling up micronutrient use to meet the rising demand for meat and aquaculture products. Supply-chain disruptions in 2024 exposed vulnerabilities in the global vitamin supply base, catalyzing strategic sourcing partnerships and capacity diversification among feed manufacturers. Meanwhile, data-driven feeding systems are enhancing demand for micronutrients deliverable through sensor-enabled precision dosage platforms.

Key Report Takeaways

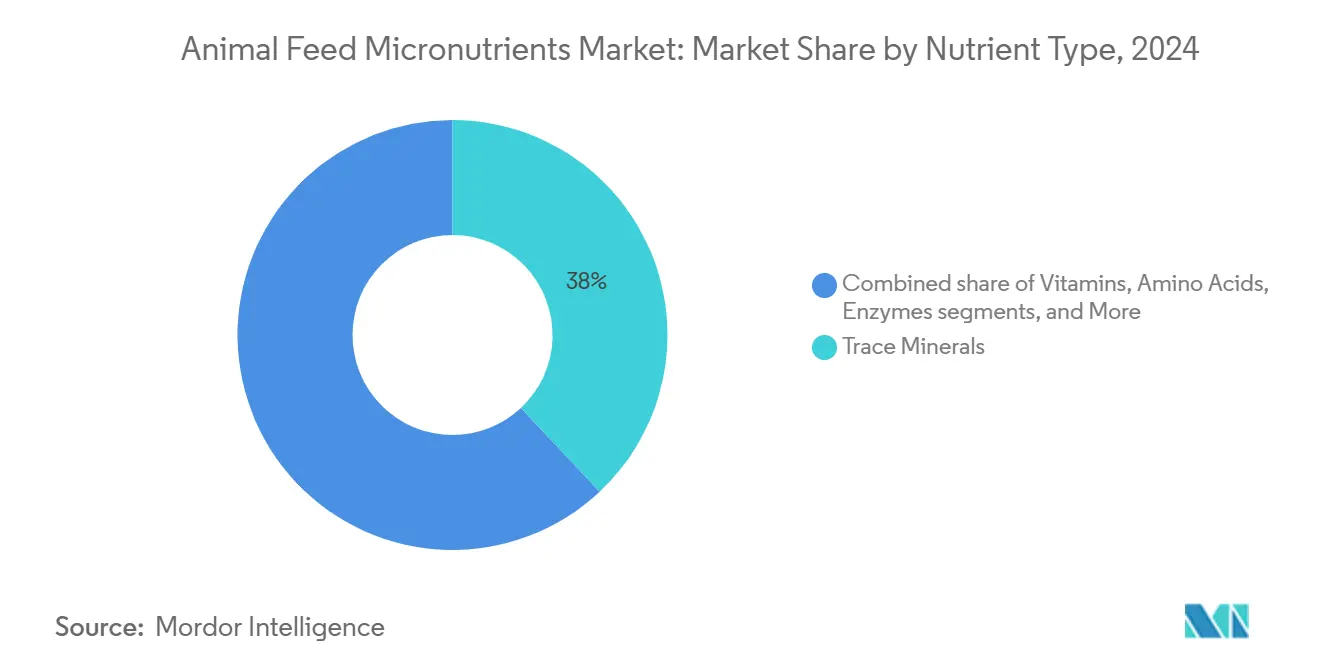

- By nutrient type, trace minerals led with 38% of the animal feed micronutrients market share in 2024, while enzymes are projected to advance at a 12.8% CAGR through 2030.

- By livestock, poultry held a 29% share of the animal feed micronutrients market size in 2024, while aquaculture is forecast to expand at an 11.6% CAGR to 2030.

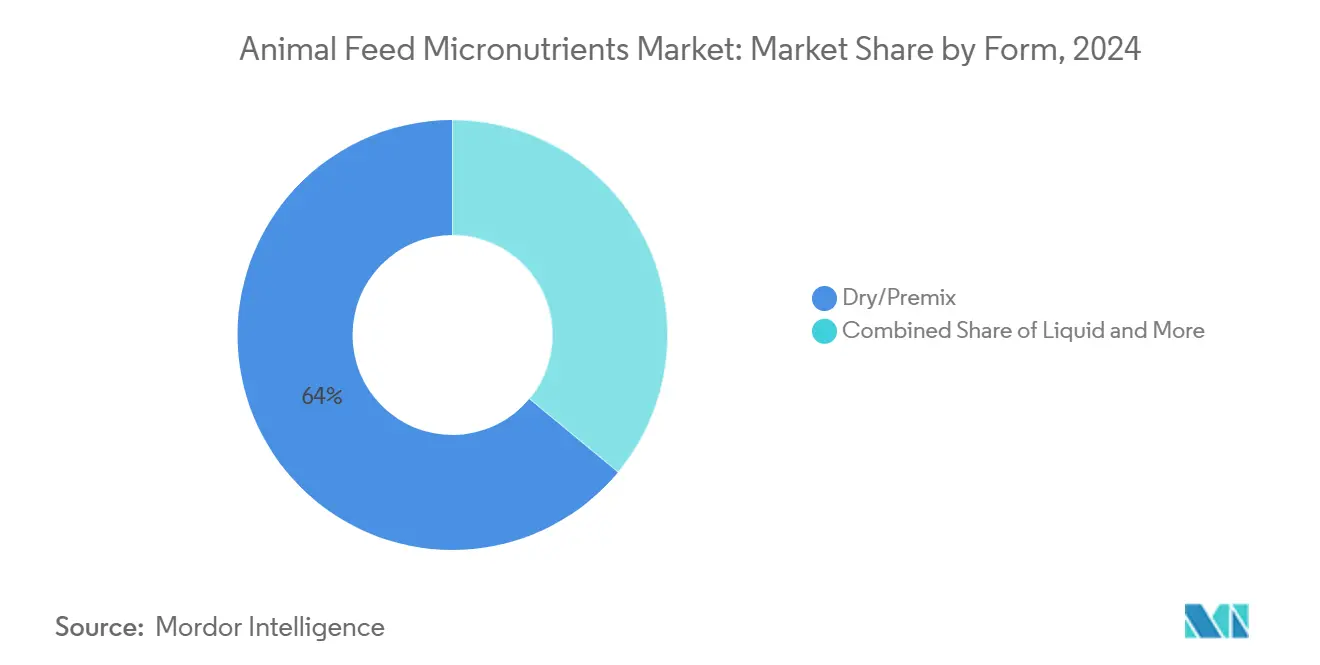

- By form, dry premix commanded 64% of the animal feed micronutrients market size in 2024, and liquid delivery is set to grow at an 11.1% CAGR between 2025 and 2030.

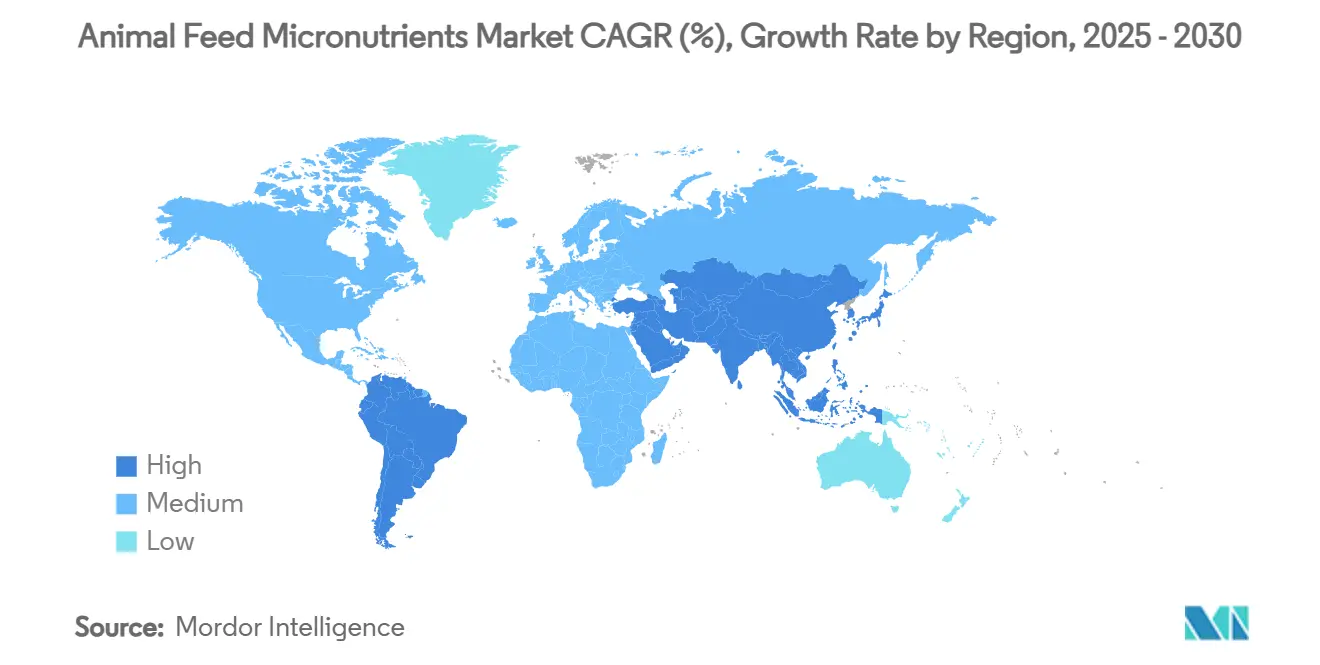

- By geography, Asia-Pacific led with a 42% share of the animal feed micronutrients market in 2024 and represents the fastest-growing region at 10.4% CAGR to 2030.

- The Cargill, Incorporated, ADM, DSM-Firmenich, BASF SE, and Nutreco N.V. (SHV Holdings N.V.) together commanded 40.6% combined market share in 2024.

Global Animal Feed Micronutrients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying industrial livestock production worldwide | +2.1% | Asia-Pacific and South America | Medium term (2-4 years) |

| Rising demand for animal protein and quality meat | +1.8% | Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Regulatory emphasis on feed quality and safety | +1.4% | North America and Europe | Short term (≤ 2 years) |

| Growing awareness of micronutrient-deficiency impacts on herd productivity | +1.2% | Global | Medium term (2-4 years) |

| Shift toward precision-nutrition feed additive blends using real-time herd data | +1.0% | North America and Europe | Long term (≥ 4 years) |

| Expansion of insect-protein farming creating new premix demand | +0.8% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensifying Industrial Livestock Production Worldwide

Commercial farming consolidation drives standardized premix adoption because large operations require consistent nutrient profiles across high-volume rations. Vertical integration is amplifying demand for customized trace mineral blends tailored to specific genetic lines, while automated feeders enable exact dosing that minimizes wastage. Investments in mega-poultry complexes across China, Brazil, and India incorporate micronutrient optimization software into feed formulation workflows. Producers prioritizing feed conversion efficiency report measurable gains from chelated mineral programs that cut the time to market weight by two to three days. Technology vendors now bundle sensors, analytics, and micronutrient recommendations, creating integrated value propositions for enterprise farms.

Rising Demand for Animal Protein and Quality Meat

Middle-income populations in Asia, the Middle East, and parts of Africa are purchasing premium poultry and pork differentiated by nutrient-enhanced profiles. Retailers respond by requiring suppliers to document feed programs that support superior meat texture, shelf life, and micronutrient density. Specialty blends rich in selenium, vitamin E, and organic zinc are becoming standard for producers targeting export markets with strict residue controls. In tandem, government nutrition campaigns emphasize the role of balanced animal diets in safeguarding food security, reinforcing demand for fortified feed premixes. Manufacturers are also positioning micronutrient offerings as enablers of antibiotic-free production, thereby commanding price premiums.

Regulatory Emphasis on Feed Quality and Safety

The 2024 launch of the Animal Food Ingredient Consultation process shortened administrative review windows but raised dossier depth requirements for new additives in the United States[2]Source: U.S. Food and Drug Administration, “Evaluation of FDA Pre-Market Animal Food Programs and Plan for Consultations,” fda.gov . In Europe, the updated green feed labeling code mandates transparency on origin, purity, and environmental footprint, prompting investments in traceability software that links raw-material batches to finished products. China’s pending revision of import regulations tightens manufacturer registration and risk-management obligations, favoring suppliers with globally harmonized quality systems. Although compliance costs are substantial, early adopters anticipate increased customer loyalty and quicker market entry.

Growing Awareness of Micronutrient-Deficiency Impacts on Herd Productivity

Subclinical deficiencies can erode feed efficiency by up to 15%, pushing producers to adopt diagnostic platforms such as Verax that pair blood biomarker analysis with targeted supplementation plans. Academic outreach programs highlight correlations between trace mineral status and immune resilience, encouraging adoption of organic mineral forms that demonstrate higher bioavailability. Empirical data show reduced lameness in dairy herds supplemented with complexed copper and zinc, underscoring the return on investment of precision micronutrition. Insurance companies in some markets now offer lower premiums to farms implementing certified micronutrient programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in raw-material prices for chelated minerals and vitamins | -1.6% | Global | Short term (≤ 2 years) |

| Stringent approval timelines for novel feed additives | -1.2% | North America and Europe | Medium term (2-4 years) |

| Competitive inclusion of multifunctional phytogenics lowering standalone micronutrient usage | -0.8% | Europe and North America | Long term (≥ 4 years) |

| Supply-chain fragility for rare trace elements (e.g., cobalt) due to ESG-driven mine closures | -0.7% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Raw-Material Prices for Chelated Minerals and Vitamins

A fire at a major European vitamin plant in 2024 caused spot prices of vitamins A, E, and D3 to spike by 80-140% within weeks, disrupting feed formulations worldwide. Chelated mineral costs also rose when organic ligand suppliers in Southeast Asia experienced energy-driven production curtailments. Large integrators executed forward contracts and secured alternative sources, yet smaller mills struggled, prompting ration reformulation that temporarily tempered micronutrient inclusion rates. Industry federations now advocate for on-shore vitamin synthesis to mitigate future shocks.

Stringent Approval Timelines for Novel Feed Additives

Despite regulatory streamlining, comprehensive toxicology and efficacy dossiers still demand multi-year investment before market entry, discouraging smaller firms from pursuing frontier technologies. The European Food Safety Authority’s updated guidance requires demonstration of utility under real-world farming conditions, amplifying trial costs. Consequently, pipeline innovation favors larger incumbents capable of financing extended validation programs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Nutrient Type: Trace Minerals Anchor the Portfolio While Enzymes Outpace in Growth

Trace minerals remained the largest contributor, accounting for 38% of the animal feed micronutrients market share in 2024, as livestock of all species require zinc, copper, manganese, and selenium for metabolic and immune functions. Adoption of organic and chelated forms surged because they demonstrate higher bioavailability and reduced environmental excretion. Vitamins followed with a lead share, inclusion rates are rising in regions shifting to antibiotic-free production, where antioxidant support mitigates stress-induced performance dips. Amino acids held a notable share, driven primarily by lysine and methionine demand in sow and broiler rations, where protein conversion efficiency remains pivotal to profitability.

Enzymes, although representing a smaller revenue base, recorded the highest 12.8% CAGR projection to 2030. Phytase, xylanase, and protease blends unlock bound phosphorus and protein fractions, lowering feed costs while shrinking the nutrient footprint. Their uptake complements mineral supplementation strategies by improving utilization of native feed minerals, indirectly reducing required inclusion rates of expensive trace elements. Niche micronutrients such as organic acids and botanicals occupy a minimal share. Combined products that merge these with trace minerals are gaining prominence as integrators seek simplified procurement.

By Livestock: Poultry Dominates but Aquaculture Leads in Acceleration

The poultry segment continues to dominate the animal feed micronutrients market with 29% of the market share, driven by intensive broiler and layer operations with strict feed conversion requirements. Feed manufacturers use complexed zinc and manganese to reduce leg disorders and enhance eggshell quality. The swine segment requires increased supplementation in first-parity sow diets to improve litter survival rates. The ruminant segment sees dairy farmers increasingly using chelated mineral boluses to improve reproductive efficiency.

Aquaculture demonstrates the highest growth rate at 11.6% CAGR through 2030, driven by increasing global seafood demand and expansion of salmon, shrimp, and tilapia farming operations. Micronutrient formulations designed for plant protein-based feeds help mitigate anti-nutritional factors, improving growth performance and fillet quality. The equine and specialty segments focus on performance horses and specialty livestock, with specific nutritional requirements for optimal health and athletic performance.

By Form: Dry Premix Holds Sway, Liquid Systems Gain Speed

Dry premix captured the leading share with 64% as of the 2024 animal feed micronutrients market because it provides long shelf life, uniform distribution in mash and pellet feeds, and compatibility with existing manufacturing infrastructure. Large mills value the ability to integrate multi-component mixes, minimizing micro-ingredient scalers and dusting risk. However, as precision feeding technology proliferates, liquid formulations emerge as a nimble alternative with 11.1%, especially where real-time nutrient adjustment confers economic advantage.

Liquid systems inclusions supported by automated pumps that meter vitamins and minerals directly into recirculating aquaculture systems or dairy TMR lines. Encapsulated and slow-release forms roughly occupy a lesser revenue share, address targeted delivery challenges, protecting heat-sensitive vitamins during pelleting or releasing trace minerals post-rumen for improved absorption.

Geography Analysis

Asia-Pacific retained leadership with a 42% revenue share in 2024, underpinned by China’s capacity expansion plans to add 50 million metric tons of grain by 2030, of which 60% is slated for feed. The regional animal feed micronutrients market is projected to grow at a 10.4% CAGR, propelled by poultry industrialization in India and aquaculture intensification in Vietnam and Indonesia. Governments are simultaneously tightening residue limits and mandating nutrient management plans, compelling producers to adopt higher-quality mineral and vitamin packages.

Europe maintains its position as a reflecting mature livestock sectors and stringent sustainability mandates that elevate demand for low-excretion mineral sources and life-cycle-audited premixes. The region's growth underscores incremental but steady progression as processors pursue eco-scores and carbon labeling that credit optimized micronutrient regimes. Recent authorizations of juniper essential oil and ginseng tincture illustrate a policy environment supportive of novel nutrient categories [3]Source: European Commission, “Commission Implementing Regulation (EU) 2024/2414 Concerning the Authorisation of Juniper Essential Oil and Juniper Tincture,” eur-lex.europa.eu.

North America demonstrates steady market expansion for feed micronutrients, as regulatory measures promoting antibiotic-free meat production and reduced heavy metal concentrations in animal manure create opportunities for enhanced nutritional supplementation in animal feed. Precision agriculture’s penetration into Midwestern hog and dairy operations fuels the adoption of sensor-linked micronutrient delivery, while regulatory partnerships with universities seek to accelerate the approval of next-generation additives. The American Feed Industry Association’s lobbying for domestic vitamin production could shift sourcing dynamics and enhance supply security.

Competitive Landscape

The animal feed micronutrients market shows moderate concentration, with the top five players controlling 40.6% of global revenue. Cargill leads the market through integrated sourcing, in-house premix production, and an expanding geographic footprint supported by its 2025 acquisition of two United States feed mills. BASF maintains diversified vitamin capacity on three continents, providing resilience amid regional disruptions. ADM and Nutreco leverage proprietary enzymes and specialty minerals to differentiate, while Novus International pushes MINTREX chelated minerals into selective segments.

Strategic focus areas include supply-chain redundancy after the 2024 vitamin crisis, digital nutrition platforms that bundle data analytics, and mergers that extend species coverage. DSM-Firmenich’s decision to divest its animal nutrition business in 2025 will redistribute the vitamin market share and potentially spark a bidding contest among existing majors or private equity investors. Smaller innovators concentrate on high-margin niches. Zinpro specializes in trace mineral proteinates, and Huvepharma advances protected vitamin C for aquafeed.

Price competition remains intense in commoditized vitamins. However, value-added products such as chelated copper or synergistic vitamin-mineral blends command premiums of 10-25%. Intellectual property, manufacturing know-how, and regulatory dossiers form high entry barriers. Firms with multi-continental plants and backward integration into key raw materials enjoy cost advantages and faster customer service, reinforcing their competitive positions.

Animal Feed Micronutrients Industry Leaders

Cargill, Incorporated

ADM

DSM-Firmenich

BASF SE

Nutreco N.V. (SHV Holdings N.V.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: The American Feed Industry Association, in collaboration with Kansas State University, established a new regulatory pathway to expedite ingredient approval submissions, which is anticipated to accelerate the market entry of new feed micronutrients and enhance the availability of innovative nutritional solutions for animal feed manufacturers.

- November 2024: Granite Creek Capital provided funding for the management buyout of Global Animal Products, strengthening the animal feed micronutrients market by ensuring continued supply of essential specialty trace minerals to feed manufacturers.

- September 2024: Anpario acquired Bio-Vet Inc. for EUR 8.2 million (USD 8.7 million). This strategic acquisition strengthens Anpario's capabilities in feed micronutrients by incorporating Bio-Vet's expertise in direct-fed microbials, which are essential for enhancing nutrient absorption and improving overall feed efficiency in animal nutrition.

Global Animal Feed Micronutrients Market Report Scope

| Trace Minerals |

| Vitamins |

| Amino Acids |

| Enzymes |

| Other Micronutrients |

| Poultry |

| Ruminants |

| Swine |

| Aquaculture |

| Equine |

| Other Livestock |

| Dry/Premix |

| Liquid |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Nutrient Type | Trace Minerals | |

| Vitamins | ||

| Amino Acids | ||

| Enzymes | ||

| Other Micronutrients | ||

| By Livestock | Poultry | |

| Ruminants | ||

| Swine | ||

| Aquaculture | ||

| Equine | ||

| Other Livestock | ||

| By Form | Dry/Premix | |

| Liquid | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the animal feed micronutrients market in 2030?

The market is forecast to reach USD 2.7 billion by 2030, reflecting a 9.6% CAGR from 2025.

Which nutrient type currently holds the largest share?

Trace minerals lead with a 38% share due to universal inclusion across livestock species.

Why is are enzymes the fastest-growing segment?

Enzymes deliver cost savings and sustainability benefits by enhancing nutrient digestibility, driving a 12.8% CAGR outlook.

Which region dominates demand?

Asia-Pacific commands 42% of revenue, propelled by intensive livestock expansion and tightening quality standards.

How concentrated is supplier power in the industry?

The top five companies control 40.6% of global revenue, giving the market a concentration score of 4.

What recent regulation is reshaping the U.S. feed additive space?

The Animal Food Ingredient Consultation process, introduced in 2024, streamlines but intensifies data requirements for new products.

Page last updated on: