Animal Feed Trace Minerals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 5.33 Billion |

| Market Size (2031) | USD 7.30 Billion |

| Growth Rate (2026 - 2031) | 6.50% CAGR |

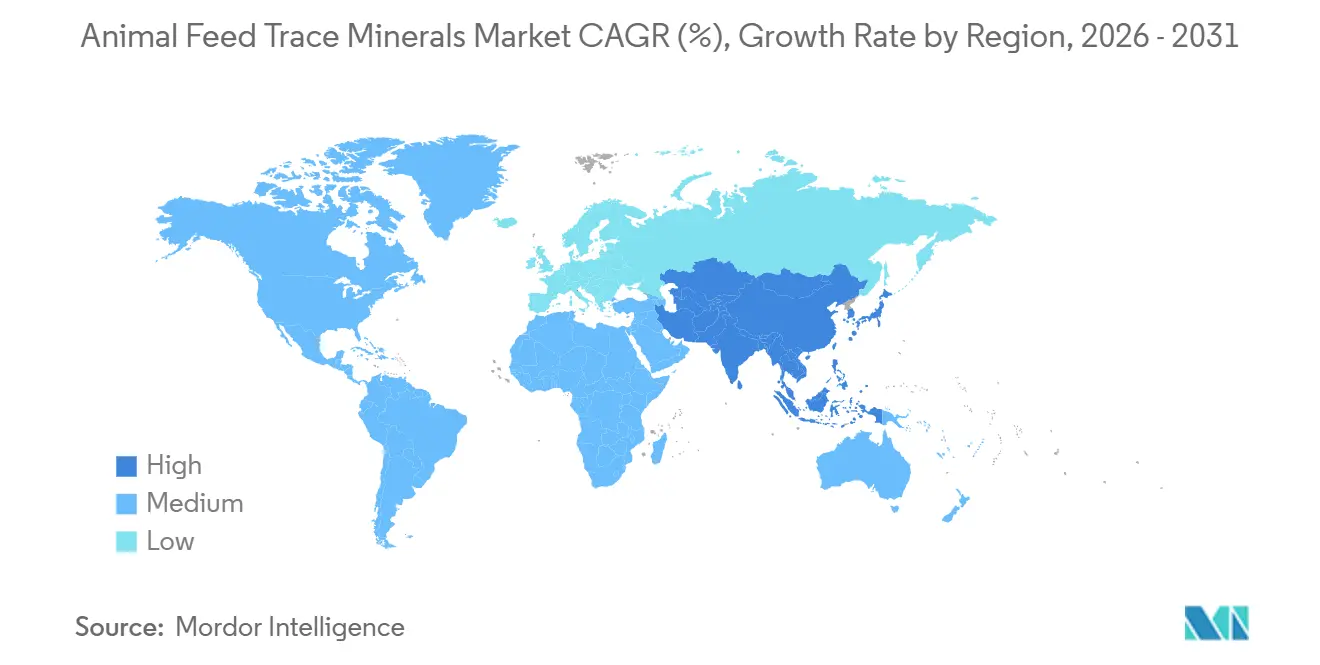

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

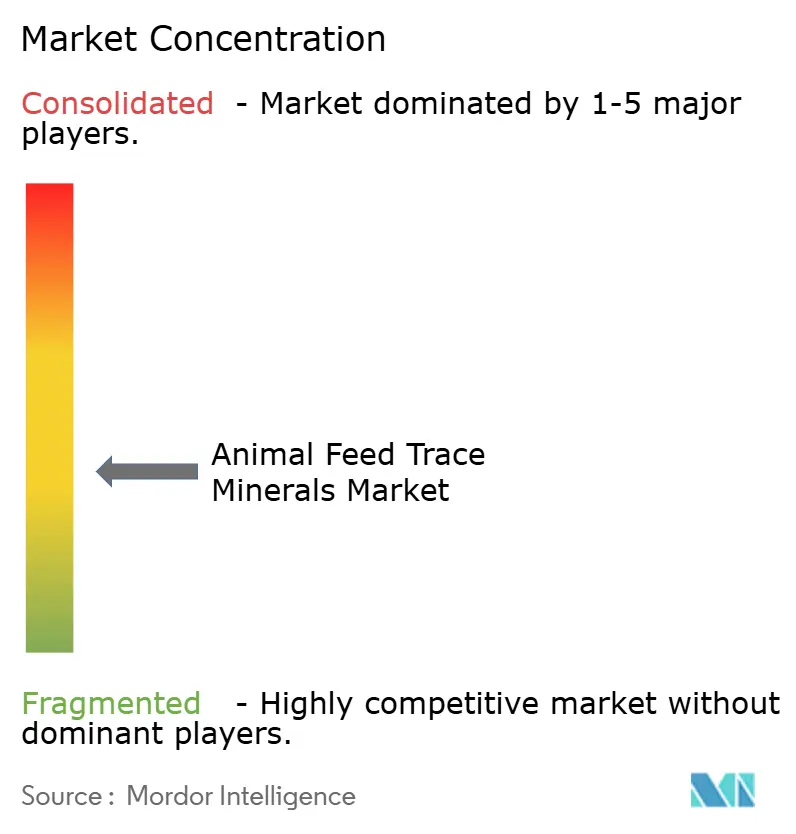

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Animal Feed Trace Minerals Market Analysis by Mordor Intelligence

The animal feed trace minerals market size is USD 5.33 billion in 2026 and is projected to reach approximately USD 7.3 billion by 2031, growing at a 6.5% CAGR over the forecast period. Rising global demand for affordable animal protein, the phase-down of antibiotic growth promoters, and rapid uptake of nutrient-efficiency technologies are the leading forces behind this expansion. Zinc retained dominance due to its central role in immune modulation, while selenium is gaining traction on the back of its antioxidant benefits that support high-stress production systems. Producers are pivoting toward organic or chelated mineral forms to capture feed-conversion gains that partly offset their 30-50% price premium. Regional momentum is strongest in the Asia Pacific, where the recovery of aquaculture and the hog sector is driving feed mills to reformulate their products around higher bioavailability inputs.

Key Report Takeaways

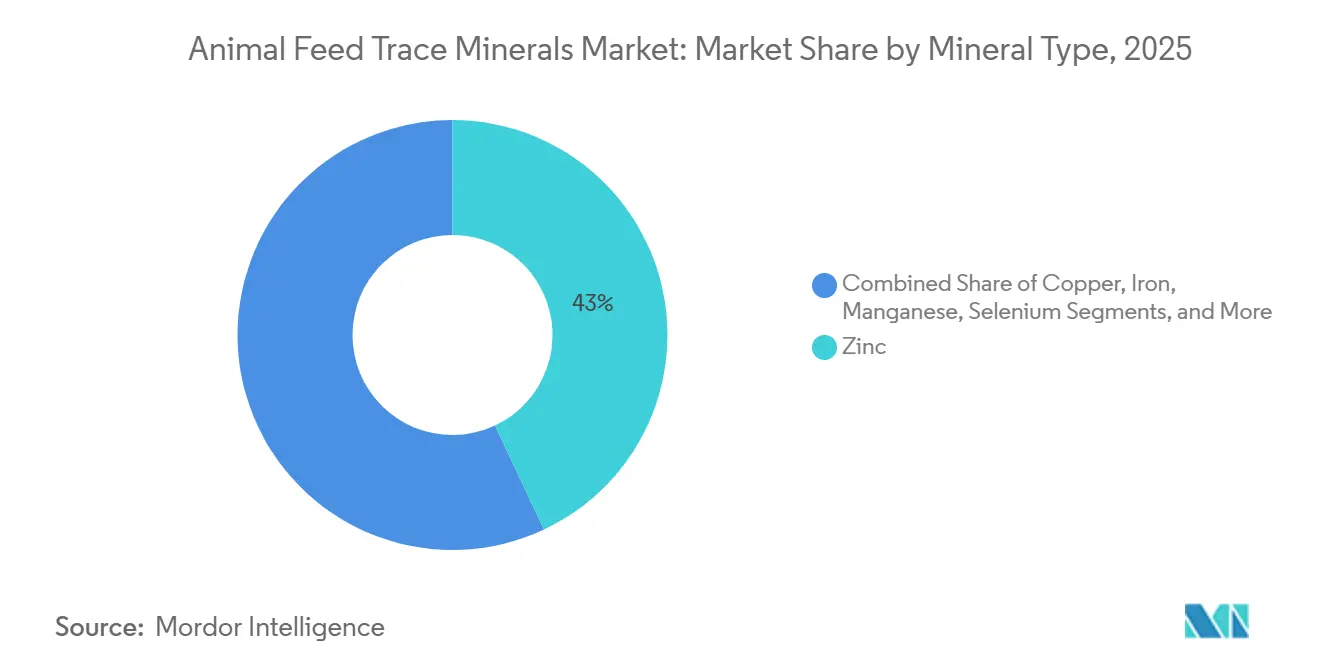

- By mineral type, zinc held 43% of the animal feed trace minerals market share in 2025, whereas selenium is forecast to expand at a 9.5% CAGR through 2031.

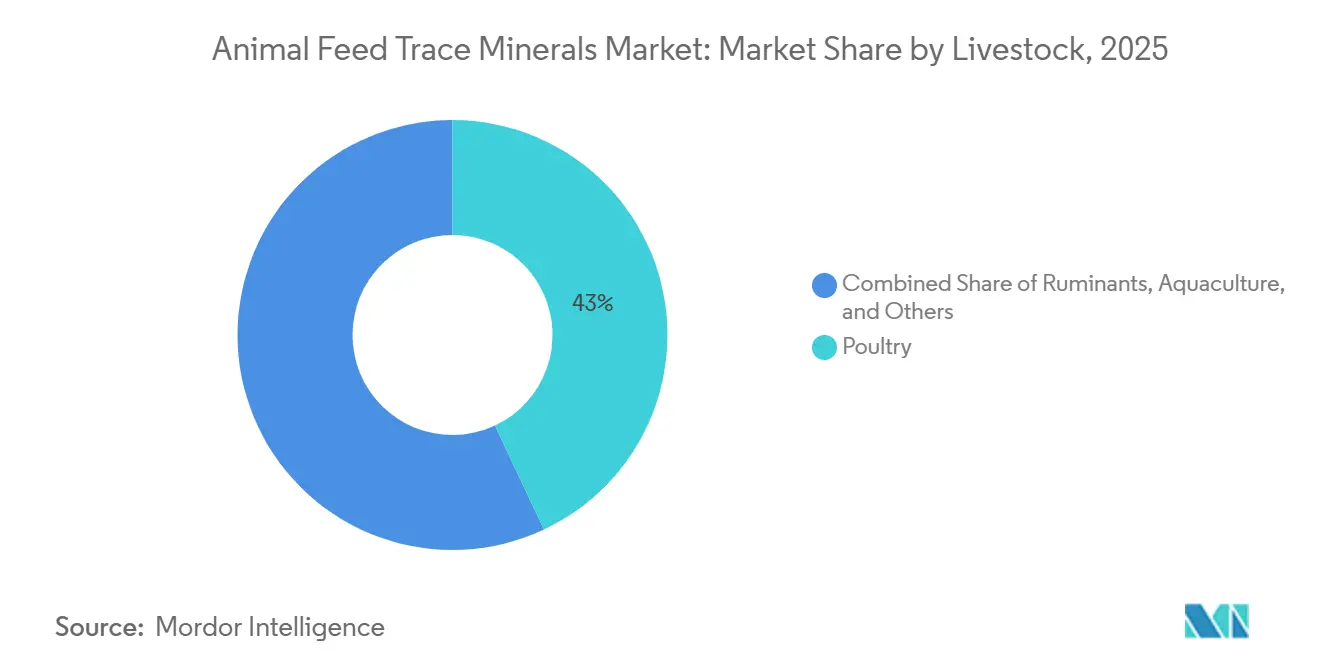

- By livestock, poultry accounted for 43% of demand in 2025, while aquaculture is projected to post the fastest growth, at a 10.2% CAGR from 2026 to 2031.

- By source type, inorganic salts accounted for 70% of revenue in 2025, and the organic and chelated segment is projected to rise at a 9% CAGR over the forecast period.

- By form, dry products captured 65% of the 2025 volume, whereas liquid blends are projected to advance at an 8.7% CAGR through 2031.

- By geography, North America generated 35% of sales in 2025, and Asia Pacific is set to grow the fastest at an 8.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Animal Feed Trace Minerals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global demand for animal protein | +1.8% | Asia Pacific, Middle East, worldwide spillover | Long term (≥ 4 years) |

| Superior bioavailability of organic minerals | +1.5% | North America and Europe, expanding premium Asia Pacific | Medium term (2-4 years) |

| Regulatory curbs on antibiotic growth promoters | +1.2% | The United States and Europe, and South America | Medium term (2-4 years) |

| Environmental benefits of reduced mineral excretion | +0.9% | European Union and North America, early uptake in Australia and New Zealand | Long term (≥ 4 years) |

| Precision feeding and sensor analytics adoption | +0.7% | North America and European Union, pilots in China and Brazil | Short term (≤ 2 years) |

| Circular-economy sourcing of trace minerals | +0.4% | European Union and select United States states, limited Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Demand for Animal Protein

In 2024, global meat production is estimated to have risen by 1.3%, reaching 365 million metric tons. This growth was largely driven by poultry meat, with increases in beef output also contributing, while pig and sheep meat production remained stable. Significant growth in meat production occurred in Australia, Brazil, the European Union, and the United States. Moreover, the OECD and FAO outlook pegs consumption to reach 47.9 million metric tons by 2031, emphasizing the need for denser, mineral-fortified rations that sustain output without expanding farmland. According to the Ministry of Agriculture and Rural Affairs of China, China’s hog inventory rebounded to 39 million heads in 2025, driving a 22% jump in compound-feed production that pulls zinc, copper, and manganese at inclusion rates of 80-120 parts per million. India’s poultry industry increased broiler placements by 8% in the same year, aided by government support for biosecure housing and aligned mineral supplementation. Both Saudi Arabia and the United Arab Emirates are witnessing significant investments by poultry companies, which is accelerating the demand for chelated selenium and zinc in export-quality feed. Sub-Saharan Africa still lags behind the World Health Organization’s protein benchmark by approximately 15 grams per person per day, prompting donor-funded starter-feed programs that require mineral fortification. Across these regions, each additional kilogram of meat consumed translates into roughly 14 grams of supplemental trace minerals, a ratio that supports long-term volume growth. Rising urban incomes, changing dietary preferences, and supermarket expansion also stimulate the purchase of higher-quality animal protein, which favors mineral-dense feed. The global push for food security further encourages governments to subsidize feed inputs, indirectly lifting mineral utilization. Combined, these factors provide the animal feed trace minerals market with a durable, volume-driven growth that remains intact throughout the forecast horizon.

Superior Bioavailability of Organic Minerals

Amino-acid chelates and proteinates demonstrate 20-40% higher absorption efficiency than inorganic sulfates or oxides, allowing nutritionists to reduce inclusion rates while maintaining optimal tissue concentrations and trimming feed costs by USD 0.50-1.20 per metric ton in large operations. In Brazil, Zinpro’s Availa program, which involved 1.2 million broilers in 2025, improved feed conversion ratios by 12%, enabling producers to reach target weights 3.5 days sooner. The European Food Safety Authority adopted updated bioavailability coefficients in 2024, which effectively account for organic minerals in maximum-limit calculations, encouraging reformulation. Hybrid strategies are gaining ground in Southeast Asia, where integrators blend 30% organic chelates with 70% inorganics and increase organic penetration to 25% by 2027. Improved immune competence and lower oxidative stress observed in chelate-fed flocks reduce morbidity costs, further justifying the premium. As precision-feeding tools quantify performance in real-time, the economic benefits of organic minerals become easier to prove, driving faster adoption. Sustainability-linked loans that reward lower mineral excretion also steer buyers toward chelates. Taken together, these dynamics ensure organic minerals will keep chipping away at the dominance of inorganic salts inside the animal feed trace minerals market.

Regulatory Curbs on Antibiotic Growth Promoters

The United States Veterinary Feed Directive, fully enforced by 2023, removed over-the-counter access to medically important antibiotics, nudging producers toward mineral-based immune support such as zinc and copper. European Union Regulation 2019/6 banned the use of prophylactic antibiotics in livestock as of 2022 and capped zinc oxide at 150 parts per million, forcing formulators to adopt more bioavailable organic zinc to sustain gut health. India’s updated National Action Plan on Antimicrobial Resistance prompted leading poultry and swine players to lift trace-mineral spending 8-12% to compensate for lower antibiotic coverage. The World Organisation for Animal Health finds that a 1% fall in antibiotic usage correlates with a 0.3-0.5% increase in mineral supplementation. As retail chains tighten residue standards, buyers specify antibiotic-free labels that compel higher mineral density in diets. Financial institutions now link loan pricing to antimicrobial reduction metrics, indirectly favoring mineral fortification. Rapid diagnostics that measure gut-health biomarkers make mineral substitution more targeted and efficient. Collectively, these policies and market signals embed a structural growth kicker for the animal feed trace minerals market through at least the medium term.

Environmental Benefits of Reduced Mineral Excretion

Livestock manure accounts for 60-70% of copper and zinc entering soils in intensive regions, prompting the Netherlands to tighten zinc application to 12 kilograms per hectare per year as of 2024. Denmark’s 2025 nitrate plan ties manure-application permits to mineral excretion, triggering penalties of USD 16 (EUR 15) per metric ton for farms that exceed limits. In Wisconsin, Balchem’s chelated copper program reduced phosphorous by 42% in 2025, enabling dairies to avoid expensive manure hauling fees. Australia’s National Livestock Methane Action Plan identifies trace-mineral optimization as one of the methods, in conjunction with other methods, used to improve efficiency, resulting in a 4-6% lower enteric methane emission per kilogram of meat when feed efficiency improves. Wageningen University’s 2025 life-cycle study revealed that replacing inorganic trace minerals with organic chelates in broiler diets can improve sustainability by reducing mineral excretion and lowering environmental impacts. Food retailers pursuing Scope 3 emission goals prefer suppliers who document lower mineral excretion, which reinforces demand for organic products. Certification bodies now incorporate mineral-management metrics into sustainability labels, pressuring integrators to upgrade formulations. Regulators in Canada and Germany are piloting digital manure passports that publicize trace-mineral loads, adding reputational risk to excessive excretion. These combined forces position environmentally efficient chelates as an attractive lever to meet both compliance and brand goals, supporting continued expansion of the animal feed trace minerals market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost premium of organic trace minerals | -1.2% | Global, most acute in price-sensitive Asia Pacific and Africa | Medium term (2-4 years) |

| Stringent multi-region registration processes | -0.8% | European Union, China, India, global exporters | Long term (≥ 4 years) |

| Emerging soil-load caps on heavy metals | -0.6% | European Union core, expanding to North America and Australia | Medium term (2-4 years) |

| Specialty-chelate supply-chain fragility | -0.4% | Global, concentrated in amino-acid precursor supply | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost Premium of Organic Trace Minerals

Chelated zinc and copper command a 30-50% premium over sulfate forms, increasing finished-feed costs by USD 2.50-4.00 per metric ton in commodity poultry and swine systems, where net margins average USD 15-25 per metric ton. In India, 70% of mills serve smallholders with tight cash flow, limiting organic-mineral penetration to 12% by 2025. Sub-Saharan African import tariffs of 15-25% and logistics markups of 8-12% keep chelates out of reach for 80% of producers. Brazil’s real depreciated 12% against the dollar in 2025, inflating chelate costs and prompting integrators such as BRF S.A. and JBS S.A. to cap organic inclusion at 20%. Hybrid blends, which utilize 60% inorganic salts and 40% chelates, capture approximately 66.67% of the bioavailability benefit while halving the premium, sustaining 6% annual organic segment growth even amid sticker shock. Feed additive makers are investing in local chelate production to reduce freight costs, but scaling remains a capital-intensive process. Until economies of scale emerge or ingredient prices normalize, the cost hurdle will continue to dampen adoption and slow the market's growth.

Stringent Multi-Region Registration Processes

European Union Regulation 1831/2003 requires dossiers costing EUR 0.57-1.72 million (USD 0.66-2.01 million) and approximately 36 months for review, discouraging mid-sized firms from advancing new chelation chemistries. China’s revised 2024 feed-additive standard requires 90-day trials in three livestock species, increasing compliance costs to CNY 8 million (USD 1.1 million) and extending timelines to 48 months. India’s Food Safety and Standards Authority insists on separate approvals for each mineral-ligand combination, so Zinpro’s methionine chelates gained clearance while glycinate variants have remained pending since 2023. Codex Alimentarius updates in 2024 failed to achieve mutual recognition, leaving exporters to navigate 15-20 divergent regimes that add 8-12% to the landed cost. Such friction slows innovation, limits product choice, and modestly tempers the growth curve of the animal feed trace minerals market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mineral Type: Zinc Leads, Selenium Accelerates

In 2025, Zinc accounted for 43% of the animal feed trace minerals market revenue. Its critical role in immune modulation and skeletal growth made it essential in diets for poultry, swine, and ruminants. Copper followed, primarily due to its use in nursery swine rations, where pharmacological dosing helps stabilize gut health during weaning stress. Manganese usage is driven by its inclusion in breeder and layer formulations to maintain eggshell integrity in high-turnover flocks. Iron's growth is supported by its use in creep-feed supplements to prevent anemia in piglets. Selenium is experiencing rapid growth as heat-stress mitigation becomes increasingly important in tropical livestock operations.

Selenium is projected to post a 9.5% CAGR through 2031 as organic yeast and selenomethionine forms deliver higher tissue retention and antioxidant capacity in high-metabolic livestock. Organic zinc and nano-encapsulated variants that achieve up to 90% intestinal absorption are reducing inclusion rates, thereby lowering fecal output and facilitating compliance with new soil-load rules in Europe. Copper demand remains steady in regions without stringent environmental regulations, but average dietary levels are declining in the European Union as chelated forms enable a 30% reduction while sustaining growth[1]Source: European Food Safety Authority, “Scientific Opinion on Trace Minerals in Feed 2024,” efsa.europa.eu. Intensifying R&D in amino-acid chelation and nano-delivery promises further efficiency gains that will keep the animal feed trace minerals market on a technology-driven upgrade path.

By Livestock: Poultry Dominates, Aquaculture Surges

Poultry commanded 43% in 2025 and represented the largest single share of the animal feed trace minerals market share, reflecting the sector’s 130 billion-bird global population and fast production cycles that demand consistent mineral intake for uniform carcass yields. Ruminants are growing as high-producing dairy cows and feedlot cattle rely on zinc and manganese for hoof strength and reproductive efficiency. Swine contributes significantly, as copper and zinc still function as growth promoters in many Asian and South American nurseries, despite mounting regulatory pressure. Aquaculture is experiencing the fastest growth trajectory, with a 10.2% CAGR, driven by shrimp, tilapia, and salmon farms that require elevated levels of selenium and zinc to mitigate oxidative stress in recirculating systems.

Aquaculture’s rapid ascent is underpinned by farmed-fish output that hit 88 million metric tons in 2025, surpassing wild catch for the first time and triggering specialized trace-mineral formulations matched to species-specific osmoregulatory needs. Poultry integrators are shifting toward micro-encapsulated zinc, which reduces dust loss and improves mixing uniformity in high-speed mills, thereby supporting performance contracts with processors that penalize weight variance. Swine producers in China and Vietnam continue to dose copper at 150-250 parts per million to offset post-weaning diarrhea. However, rising soil-load caps will likely push them toward more bioavailable chelates over the outlook period. Premium pet food brands are also lifting chelated mineral levels to support joint health and immune function in aging companion animals, adding a small but profitable revenue stream for the animal feed trace minerals market.

By Source Type: Inorganic Retains Scale, Organic Gains Momentum

Inorganic salts accounted for 70% of the market in 2025, aligning with the economic requirements of commodity feed mills in price-sensitive regions. Organic and chelated minerals are growing at a high rate, driven by documented 2-4% feed-conversion improvements that offset part of their 30-50% price premium. Nano and encapsulated products are expanding at an 11% CAGR, driven by their ability to bypass rumen degradation and target uptake sites in monogastric animals. In 2024, the European Union revised bioavailability coefficients, favoring chelates in maximum-limit calculations and prompting reformulation across 12,000 intensive livestock operations.

Hybrid premixes, combining 40% chelates with 60% sulfates, are gaining traction in Southeast Asia, delivering two-thirds of the performance benefits at half the cost premium. In North America, integrators are increasingly adopting performance-based supply contracts, where chelate providers share in the benefits if feed efficiency targets are achieved, aligning incentives for value optimization. Local chelate production in Brazil and China is scaling up to mitigate foreign-exchange risks and freight costs, a development anticipated to reduce delivered prices by 5-7% by 2028. As regulatory attention shifts to manure nutrient loading, the superior absorption efficiency of chelates is projected to strengthen their long-term position in the animal feed trace minerals market.

By Form: Dry Prevails, Liquid Accelerates

Dry powders, granules, and premixes accounted for 65% of 2025 shipments, as they integrate seamlessly with batch mixers and remain stable in humid storage conditions. Liquid blends are advancing at an 8.7% CAGR, driven by the spread of precision-dosing systems that meter minerals in real-time and reduce over-formulation by 10-15%. Occupational safety rules tightening zinc oxide dust limits in 2024 have accelerated a shift toward liquid forms within the United States and European mills. Post-pelleting spray application also avoids thermal degradation and improves uniformity in micro-inclusion settings below 10 parts per million.

Freight penalties for liquids remain 20-30% higher than those for dry goods due to the added weight and refrigeration requirements, which constrain shipments to tropical markets in Africa and South Asia, where cold-chain infrastructure is limited. Encapsulated dry minerals that coat particles with lipid or polysaccharide matrices bridge performance and logistics, capturing 8% of the European ruminant segment under brands such as Selisseo. Sensor-driven layer houses in the Midwest United States have begun integrating liquid chelated zinc via inline injectors, resulting in a 3% improvement in eggshell thickness and a six-day extension in flock cycles. As return-on-investment analytics become standard, producers will allocate more capital to systems that unlock liquid-form efficiency, thereby lifting the animal feed trace minerals market in its next growth phase.

Geography Analysis

North America generated 35% of global revenue in 2025, primarily driven by the United States' broiler and cattle herds, which consumed 1.2 million metric tons of mineral additives. The region is projected to expand at a steady growth rate through 2031. Adoption of liquid chelates in precision-fed dairies rose to 42% of herds in Canada, while Mexico’s heat-stress challenges lifted organic selenium inclusion across Jalisco and Veracruz flocks. Sensor analytics penetration reached 18% of commercial operations, supporting data-driven mineral adjustments that protect margins as corn and soybean prices fluctuate[2]Source: Ministry of Agriculture and Rural Affairs, “Fourteenth Five-Year Plan for Modern Agriculture,” moa.gov.cn.

The Asia Pacific is advancing at an 8.2% CAGR through 2031, the fastest regional pace, driven by China’s recovery of its hog herd and India’s poultry expansion, which together increase the region’s animal feed trace minerals market size each year. Subsidies worth CNY 15 billion (USD 2.1 billion) for modernized feed mills in China favor chelated minerals, raising organic penetration from 14% in 2023 to 22% in 2025. India’s National Livestock Mission mandates mineralized rations for smallholder dairies, creating a captive base for cost-effective inorganic salts while leaving headroom for premium chelates in organized dairies. Southeast Asia’s aquaculture boom absorbs selenium and zinc at inclusion rates 20-30% higher than those of terrestrial livestock, underpinning double-digit growth in Vietnam and Indonesia.

Europe is estimated to grow at a high CAGR, as static animal numbers are offset by sustainability mandates that require lower excretion profiles. Regulation 2023/915 prompted feed mills to adopt chelated zinc and copper or incur manure export costs of EUR 30-50 (USD 32-53) per metric ton, thereby steering demand toward higher-priced organic solutions. The United Kingdom accelerated additive approvals post-Brexit, shortening market entry for Balchem’s chelated manganese by fourteen months and signaling a regulatory change for innovators.

Competitive Landscape

The animal trace minerals market is characterized by a moderate degree of consolidation, with leading global players such as Cargill Incorporated, Alltech, Inc., Archer Daniels Midland Company, DSM-Firmenich AG, and Zinpro Corporation maintaining significant influence through integrated supply chains and proprietary chelation technologies. These top-tier companies leverage extensive R&D investments to develop highly bioavailable mineral forms, such as amino acid chelates and hydroxy-trace minerals, which offer superior stability and improved absorption rates compared to traditional inorganic salts. Cargill held a major share in 2025, driven by captive metal sourcing, multi-continent premix plants, and a service model that integrates precision-feeding software with chelated blends[3]Source: Cargill Inc., “Animal Nutrition Press Release March 2025,”cargill.com.

ADM followed, leveraging its soybean-crushing network to incorporate trace minerals into integrated soy meal contracts, securing feed-mill customers for three-year terms. DSM-Firmenich has supported the filing of fourteen patents since 2023 on glycinate and methionine-hydroxy analogue complexes targeting aquaculture and high-yielding ruminants, which are willing to pay a 40-60% premium for proven bioavailability. To maintain market share, companies like Kemin Industries and Novus International are emphasizing these environmental benefits alongside traditional metrics such as improved feed efficiency and disease resistance to justify the premium pricing of organic trace minerals over their inorganic counterparts.

Zinpro, through its vertically integrated Minnesota facility, which synthesizes methionine and completes chelation in a single location, reduces unit costs and lead times for organic zinc and copper. Alltech is scaling proprietary selenium-yeast fermentation, which prices organic selenium 15% below competitors. This achievement secured multi-year supply agreements with major U.S. poultry producers in 2025. Along with this, competitive dynamics are shifting as global nutrition majors partner with local formulators in these emerging markets to better serve smallholder farmers and large-scale commercial operations alike.

Animal Feed Trace Minerals Industry Leaders

Cargill Incorporated

Alltech, Inc

DSM-Firmenich AG

Zinpro Corporation

Archer Daniels Midland Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Barentz acquired Fengli Group in China. This strategic move significantly expanded Barentz's footprint in the Asia-Pacific region, specifically targeting the pharmaceutical, animal nutraceutical, and health product markets.

- June 2025: The Swanson Family of Companies purchased D&D Ingredient Distributors, enlarging capacity for feed additives, including trace minerals.

- September 2024: Novus International, Inc. and Ginkgo Bioworks formed a partnership to develop feed additives, including trace minerals, for the animal agriculture industry.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study sizes the animal feed trace minerals market as annual sales of zinc, copper, iron, manganese, selenium, cobalt, iodine, and other micro-minerals blended into complete feed, premixes, or stand-alone supplements for poultry, ruminants, swine, aquaculture, pets, and equine. Mordor Intelligence counts both inorganic salts and organically chelated forms, in dry or liquid formats, inside scope.

Scope exclusion: macrominerals and combined vitamin-mineral premixes are not included.

Segmentation Overview

- By Mineral Type

- Zinc

- Copper

- Manganese

- Iron

- Selenium

- Others

- By Livestock

- Poultry

- Ruminant

- Swine

- Aquaculture

- Pets and Other

- By Source Type

- Inorganic Salts

- Organic/Chelated

- Nano/Encapsulated

- By Form

- Dry

- Liquid

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Analysts spoke with feed-mill nutritionists, veterinary faculty, and purchasing heads across Asia-Pacific, Europe, and the Americas. Their insight tested assumed inclusion rates, confirmed organic price premiums, and sharpened growth drivers.

Desk Research

We linked FAO feed-output tables, USDA-FAS trade sheets, Eurostat Prodcom codes, and Volza customs logs with price cues from Dow Jones Factiva and public 10-Ks. Peer-reviewed nutrition journals, plus International Feed Industry Federation papers, fixed inclusion ranges, while D&B Hoovers mapped supplier splits. These references illustrate, not exhaust, the evidence pool used for validation.

Market-Sizing & Forecasting

A top-down build converts national feed tonnage (factory and home-mix) into mineral demand pools, then multiplies them by livestock-specific inclusion factors. Targeted supplier roll-ups and channel calls act as bottom-up spot checks that tune totals. Five fingerprints: feed output, inclusion rate, chelated share, herd shifts, and copper-sulfate prices power a multivariate regression that projects 2025-2030 values. Regional price-volume grids plug data gaps before sign-off.

Data Validation & Update Cycle

Before release, Mordor analysts run variance scans, revisit experts when anomalies surface, and align currency translations. Reports refresh yearly, with interim updates when disease outbreaks or new heavy-metal limits materially shift demand.

Why Our Animal Feed Trace Minerals Baseline Is Dependable

Published estimates often diverge because each firm chooses its own scope, price ladder, and refresh rhythm.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 425.3 m (2025) | Mordor Intelligence | - |

| USD 570.1 m (2023) | Global Consultancy A | Bundles premix income, older base |

| USD 827.2 m (2024) | Trade Journal B | Counts organic only, flat 8 % ASP uplift |

By refreshing annually, separating premix revenue, and rooting ASPs in verified invoices, we give decision-makers a balanced, transparent baseline they can trust.

Key Questions Answered in the Report

What is the forecast size of the animal feed trace minerals market by 2031?

The market is projected to reach about USD 7.3 billion by 2031, expanding at a 6.5% CAGR.

Which mineral currently leads global revenue?

Zinc led with 43% share in 2025 due to its central role in immune and skeletal functions.

Which livestock segment is anticipated to grow fastest?

Aquaculture is poised to advance at roughly 10.2% CAGR through 2031 as shrimp and salmon output accelerates.

How are regulations influencing mineral demand?

Phase-downs of antibiotic growth promoters worldwide are prompting integrators to raise zinc, copper, and selenium inclusion for immune support.

Why are organic or chelated minerals gaining traction?

They deliver 20-40% higher absorption, lower environmental excretion, and increasingly satisfy soil-load limits and sustainability audits.

What technologies support efficient mineral usage?

Precision-feeding platforms with sensors and cloud analytics adjust mineral dosing in real time, cutting over-formulation and improving feed conversion.

Page last updated on: