Anal Cancer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

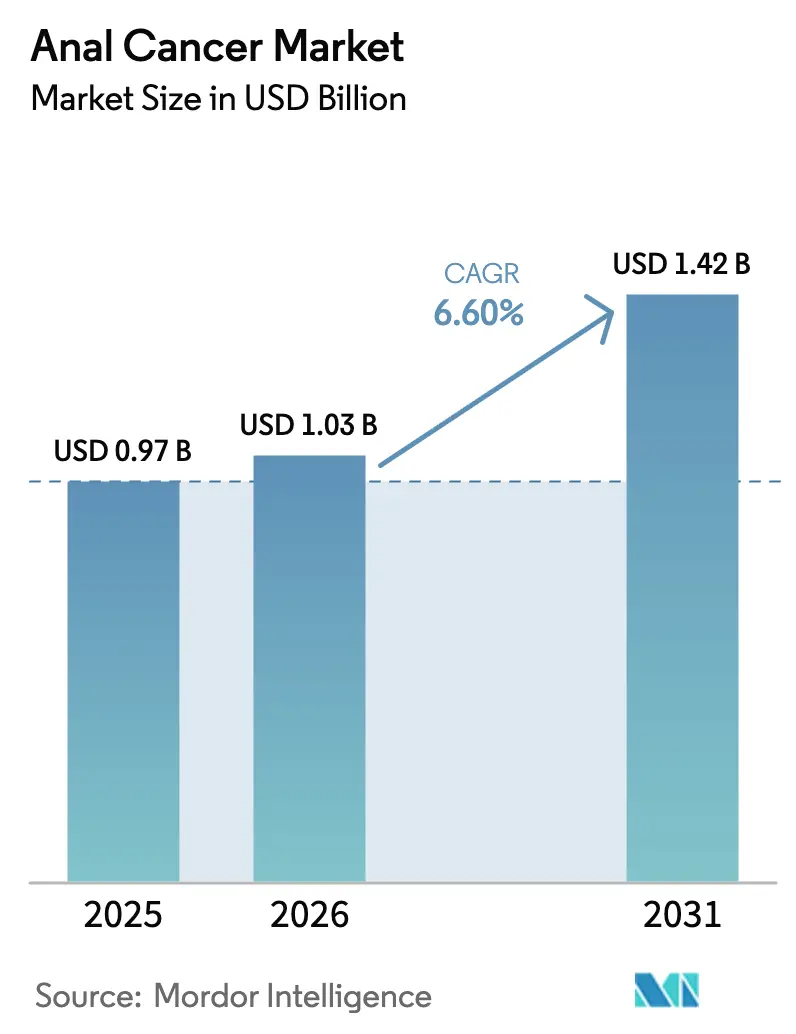

| Market Size (2026) | USD 1.03 Billion |

| Market Size (2031) | USD 1.42 Billion |

| Growth Rate (2026 - 2031) | 6.60% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anal Cancer Market Analysis by Mordor Intelligence

Anal Cancer Market size in 2026 is estimated at USD 1.03 billion, growing from 2025 value of USD 0.97 billion with 2031 projections showing USD 1.42 billion, growing at 6.60% CAGR over 2026-2031.

Demand rises as HPV-linked cases climb, immunotherapy becomes first-line care, and high-resolution anoscopy (HRA) screening broadens clinical detection. The May 2025 FDA clearance of Zynyz resets therapeutic expectations and stimulates pipeline investment [1]U.S. Food and Drug Administration, “FDA Approves Retifanlimab-dlwr for Advanced Squamous Cell Carcinoma of the Anal Canal,” fda.gov , while new ASTRO radiation guidelines harmonize chemoradiation protocols and accelerate community-wide adoption [2]American Society for Radiation Oncology, “ASTRO Issues First Guideline on Anal Cancer Radiation Therapy,” astro.org . North American payers continue to reimburse checkpoint inhibitors, yet staffing shortages in radiation oncology slow capacity expansion. Asia-Pacific grows fastest as HPV vaccination coverage improves and screening infrastructure scales, particularly in Japan and China.

Key Report Takeaways

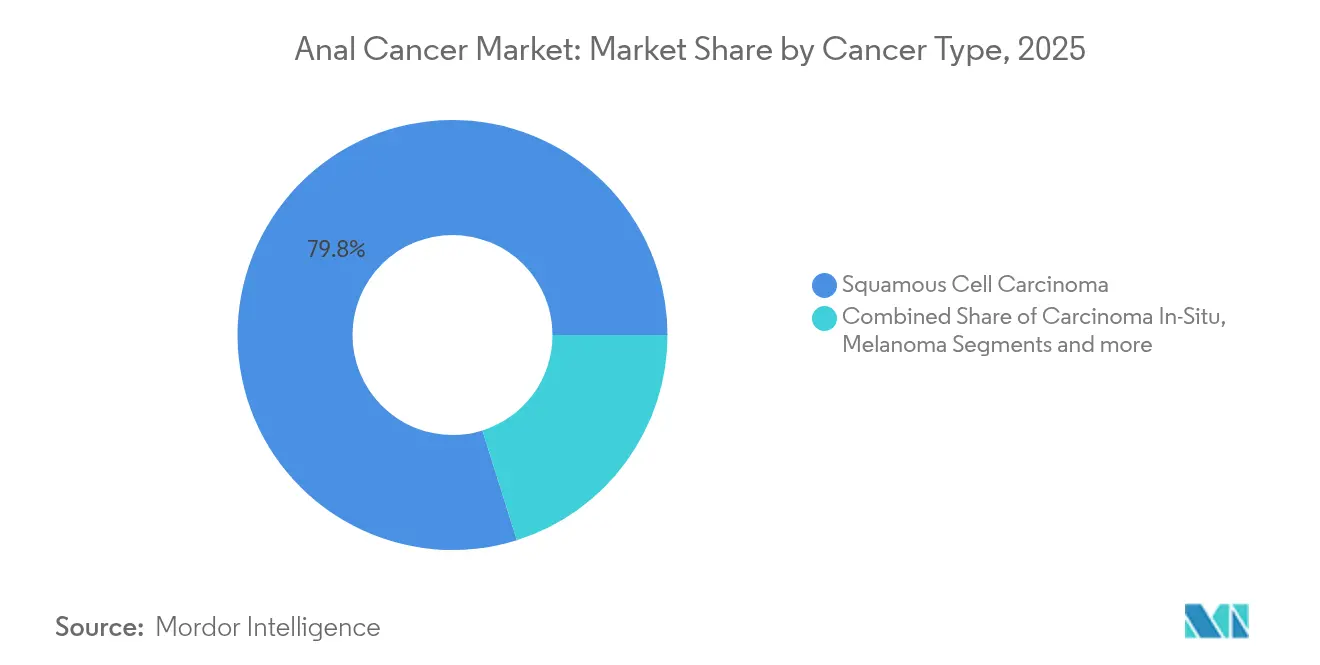

- By cancer type, squamous cell carcinoma led with 79.84% revenue share in 2025; carcinoma in situ is forecast to expand at a 7.14% CAGR through 2031.

- By disease stage, Stage III accounted for 50.88% of the anal cancer market share in 2025, while recurrent disease records the highest projected CAGR at 7.23% to 2031.

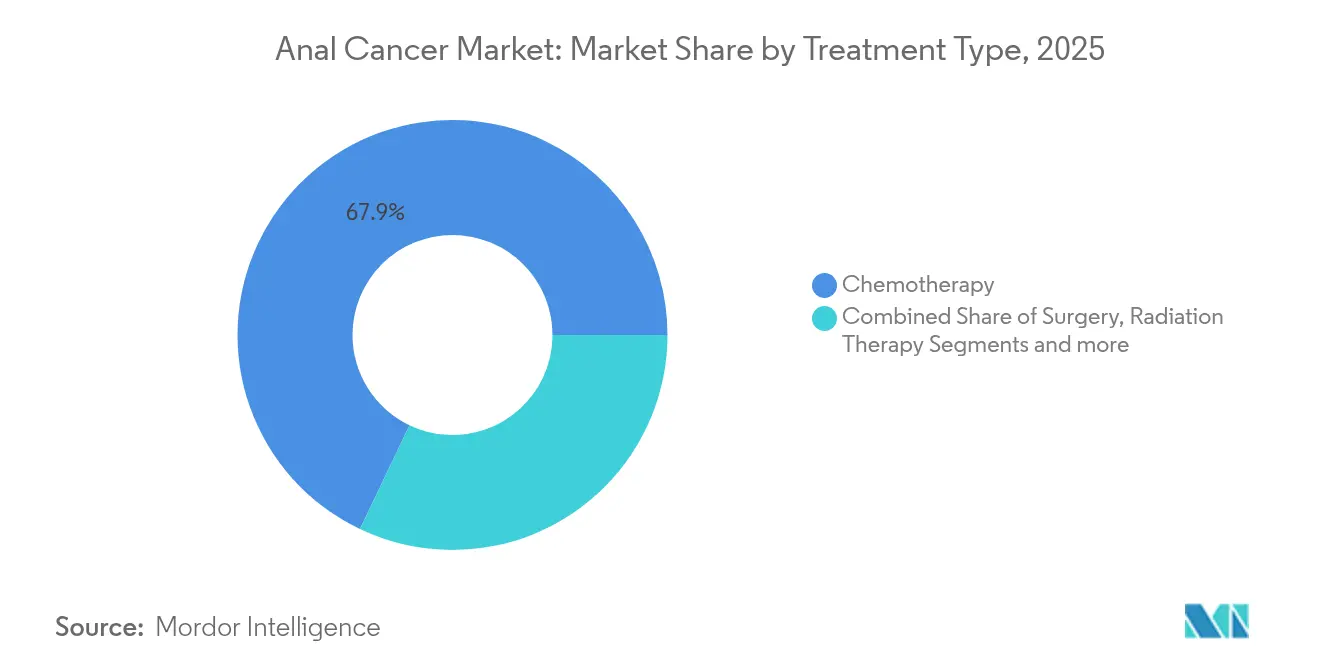

- By treatment type, chemotherapy held 67.92% of the anal cancer market size in 2025; radiation therapy advances at a 7.34% CAGR on guideline-driven intensity-modulated techniques.

- By end-user, hospitals and clinics captured 69.76% share in 2025; research and academic institutes grow fastest at 7.38% CAGR.

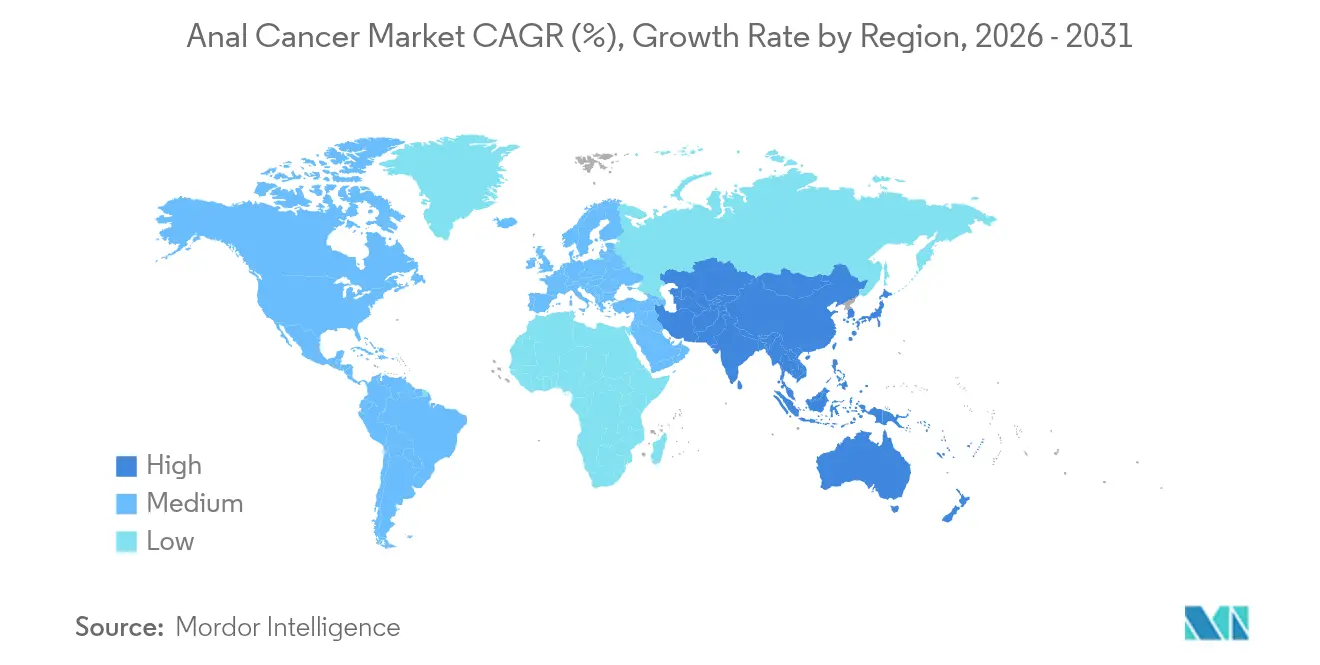

- By geography, North America commanded 40.42% of the anal cancer market share in 2025; Asia-Pacific is set to expand at a 7.49% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Anal Cancer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence of HPV-Linked STDs & Anal Cancer | +1.8% | Global; highest in North America & Europe | Medium term (2-4 years) |

| Increasing R&D Funding for HPV-Positive Tumor Immunotherapy | +1.5% | North America & EU; spill-over to APAC | Long term (≥4 years) |

| Growing Acceptance of Chemoradiation Organ-Preservation Protocols | +1.2% | Global; early gains in US, EU, Japan | Short term (≤2 years) |

| Reimbursement Expansion for Checkpoint Inhibitors | +0.9% | North America & core EU markets | Medium term (2-4 years) |

| AI-Guided Molecular Profiling Accelerating Trial Recruitment | +0.7% | Global; concentrated in major cancer centers | Long term (≥4 years) |

| Launch of High-Resolution Anoscopy Screening Clinics | +0.6% | North America & EU; expanding to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising HPV-Linked Anal Cancer Incidence

Annual case growth now reaches 2.9% in women and 1.6% in men, with white women over 65 registering 11.4 cases per 100,000 in 2021 [3]Digestive Disease Week Press Office, “New Data Show Rising Anal Cancer Incidence in Older Women,” ddw.org . More than 90% of tumors harbor oncogenic HPV strains, making vaccination programs both a preventive tool and a long-run demand modulator. Current US screening guidelines omit most older women, widening a diagnostic gap that pushes market participants to expand HRA services. Rising incidence in previously low-risk segments enlarges the treatable population and elevates baseline procedure volumes for the anal cancer market. Hospital systems therefore invest in training and equipment to accommodate wider screening recommendations.

R&D Funding for HPV-Positive Tumor Immunotherapy

Checkpoint inhibitors continue to attract capital as HPV-positive tumors display dense immune infiltration and PD-L1 expression that predict response. Keytruda’s strong sales reinforce confidence in combination protocols that merge immunotherapy with chemoradiation, spurring companies to co-develop companion biomarkers. Long-term funding cycles favor collaborative trials in North America and Europe, but sites in Japan and Australia are also enrolling. Industry analysts expect expanded biomarker-guided regimens to lift five-year survival and lengthen treatment courses, supporting sustained revenue growth in the anal cancer market.

Acceptance of Chemoradiation Organ-Preservation Protocols

ASTRO’s 2025 guideline endorses intensity-modulated radiation with concurrent 5-FU and mitomycin, improving local control while preserving sphincter function. The standard now applies across community centers, cutting referral delays and reducing colostomy rates. Five-year survival for early-stage cases exceeds 85%, driving clinician confidence and payer acceptance. Uniform protocols simplify reimbursement coding, streamlining payer approval cycles. Collectively, these shifts enhance access and support broader uptake of treatment within the anal cancer market.

Reimbursement Expansion for Checkpoint Inhibitors

Payer policies in the United States and Germany now reimburse first-line PD-1 blockade for inoperable disease, trimming out-of-pocket costs and smoothing uptake of Zynyz. Coverage clarity stimulates hospital formularies to stock immunotherapies and encourages oncologists to adopt combination regimens earlier. As health technology assessments in France and the United Kingdom revisit cost-effectiveness models, positive reimbursement decisions could extend momentum across other European markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Treatment Cost & Systemic Side-Effects | -1.4% | Global; most pronounced in emerging markets | Short term (≤2 years) |

| Low Disease Prevalence Limiting ROI for New Entrants | -0.8% | Global; affects smaller biotech companies | Long term (≥4 years) |

| Shortage of Pelvic Radiation Oncologists | -0.6% | North America & EU; expanding to APAC | Medium term (2-4 years) |

| Reimbursement Gaps for Preventive HRA Screening | -0.4% | Global; most acute in emerging markets | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Treatment Cost and Systemic Side-Effects

Annual immunotherapy bills often exceed USD 150,000, pushing total care costs for advanced disease above USD 200,000 when hospitalizations and supportive therapy are included. Adverse-event management further raises resource needs, demanding multidisciplinary expertise that is scarce outside tertiary centers. Prior-authorization hurdles prolong treatment starts, adding administrative overhead for providers. Insurers in Brazil and India offer partial coverage only, forcing patients into financial toxicity that limits drug uptake and restrains the anal cancer market.

Low Disease Prevalence Limiting ROI for New Entrants

Roughly 10,930 new US cases per year confine the immediate addressable pool, challenging biotechs that cannot amortize development costs across larger indications. Although orphan-drug incentives shorten review times, they only partly offset the USD 1-3 billion needed for full development. Clinical trial enrollment is slow; rare histologies and stage heterogeneity complicate protocols and extend timelines. Consequently, smaller firms often partner with multinationals that already dominate the anal cancer industry, reinforcing existing competitive hierarchies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cancer Type: Squamous Cell Carcinoma Drives Market Leadership

Squamous cell disease captured 79.84% of the anal cancer market share in 2025 and anchors revenue visibility through 2031. Carcinoma in situ enjoys 7.14% CAGR on the back of expanding HRA programs that intercept lesions earlier, while melanoma remains niche but benefits from checkpoint-inhibitor successes reported in mucosal sites. Squamous tumors’ strong link to HPV 16 and 18 secures stable patient inflow and standardizes chemoradiation regimens. Adenocarcinoma and basal-cell variants leverage advances in colorectal and dermatologic oncology to refine care pathways. Improving molecular profiling identifies actionable mutations across histologies, hinting at future precision-therapy add-ons that could enlarge the anal cancer market.

Carcinoma in situ growth also reflects rising vaccination awareness; vaccinated cohorts present fewer invasive tumors and more pre-invasive lesions, prompting elective ablation procedures. As pathology labs integrate digital image analysis, detection sensitivity climbs and reinforces early-treatment volumes. Meanwhile, translational research into viral oncogene expression informs next-generation vaccine boosters, potentially shrinking long-term incidence yet enlarging surveillance and diagnostic subsegments tied to the anal cancer market.

By Disease Stage: Advanced Disease Complexity Drives Innovation

Stage III disease accounted for 50.88% of 2025 diagnoses, underscoring late detection trends that fuel aggressive multimodal regimens. Recurrent disease leads growth at 7.23% CAGR as improved survival unmask late failures requiring salvage approaches. Patients with Stage I-II disease benefit from 85% five-year survival under guideline-directed chemoradiation, reinforcing confidence in early-stage management. Integration of total neoadjuvant therapy, successful in rectal cancer, is under active investigation for Stage III, aiming to curb progression to metastasis within the anal cancer market.

Stage IV presentations, although fewer, drive per-patient spending and focus industry attention on immunotherapeutic combinations. The 2025 Zynyz approval establishes a PD-1 backbone for metastatic management and may catalyze triplet regimens with oncolytic viruses or IL-15 agonists. Clinical data collection through national registries improves understanding of relapse kinetics and informs adjuvant-trial design, supporting continued expansion of the anal cancer market size for advanced therapeutics.

By Treatment Type: Chemotherapy Dominance Faces Radiation Innovation

Chemotherapy held 67.92% of the anal cancer market size in 2025, sustained by its dual role in definitive and metastatic settings. Yet radiation therapy records 7.34% CAGR through 2031 as intensity-modulated platforms widen eligibility and cut toxicities. IMRT adoption climbs among community centers as payers accept guideline-driven dosing schemas. Surgery remains limited to salvage cases but benefits from minimally invasive techniques that lower morbidity across the anal cancer market.

Immunotherapy is the fastest-moving subsegment, building on checkpoint agents’ durable responses in HPV-positive tumors. Combination protocols blending carboplatin-paclitaxel with PD-1 blockade have moved to first-line status, creating opportunities for supportive biologics that mitigate immune-related adverse events. Targeted therapies aimed at PI3K and EGFR pathways enter Phase II studies, while adoptive T-cell approaches progress in academic trials, together broadening therapeutic diversity within the anal cancer market.

By End-User: Hospital Dominance Challenged by Academic Innovation

Hospitals and clinics owned 69.76% of revenue in 2025 as multidisciplinary teams concentrate chemoradiation, surgery, and inpatient management under one roof. Workforce shortages—11.3% among medical dosimetrists—however cap expansion and push some services toward outpatient hubs. Academic centers grow at 7.38% CAGR in the anal cancer market by acting as trial nodes and molecular-profiling pioneers.

AI-driven diagnostics facilitate remote triage, allowing community sites to link with tertiary centers for complex decision making. HRA screening clinics increasingly cluster within universities because of equipment costs and expertise needs. This concentration, while improving care quality, necessitates referral networks and telehealth follow-up models that balance access with resource constraints in the anal cancer industry.

Geography Analysis

North America retained 40.42% of the anal cancer market share in 2025 on the strength of organized screening, robust payer coverage, and FDA fast-track pathways that cut time-to-market for innovations. U-S-based cancer centers execute most pivotal trials, accelerating domestic uptake of new regimens. Yet looming reimbursement cuts for radiation services could reduce provider margins and slow hardware upgrades. Canada’s universal vaccine program already lowered anogenital wart rates, foreshadowing future incidence declines that may temper long-term procedure growth.

Europe contributes significant volume as national health systems standardize chemoradiation protocols and negotiate drug pricing. EMA’s approval of Gardasil 9 underpins prevention policy, with tendering driving HPV vaccine prices below EUR 30 per dose in Italy. Eastern European nations lag in immunotherapy access, creating two-tier outcomes that the EU Beating Cancer Plan aims to narrow. Pan-European cancer cases rose 58% between 1995 and 2022, ensuring sustained demand for oncologic infrastructure.

Asia-Pacific is the fastest-growing region at 7.49% CAGR, fueled by expanding insurance coverage, increasing HPV immunization, and large untreated populations. Japan documents 1,056 new cases yearly and faces urgent catch-up vaccination drives after a decade-long program pause. China’s multi-billion-dollar HPV vaccine opportunity motivates local manufacturers to pursue WHO pre-qualification, which would slash costs and boost uptake. India invests in radiation-oncology training consortia to mitigate staffing deficits, fostering regional demand for linear accelerators and planning systems essential to the anal cancer market.

Competitive Landscape

The anal cancer market features a moderate concentration anchored by oncology multinationals. Merck integrates Gardasil prevention with Keytruda therapy, positioning itself across the disease continuum. Bristol-Myers Squibb leverages nivolumab-based combinations, while Roche explores atezolizumab plus radiation in investigator-initiated trials. Incyte’s 2025 approval of Zynyz as first-line therapy reshapes competitive dynamics and validates focused development in rare tumors.

Strategic moves cluster around combination regimens: Merck collaborates with Adaptive Biotechnologies on neoantigen discovery, aiming to personalize vaccine-immunotherapy cocktails; Bristol-Myers backs AI-guided trial matching to enrich responder populations; Roche pursues circulating-tumor-DNA diagnostics to monitor minimal residual disease. Companies also form supply-chain alliances to secure GMP-grade mitomycin, a backbone chemoradiation agent under periodic shortage.

New entrants emphasize niche modalities—oncolytic viruses, IL-15 agonists, adoptive NK cells—often in partnership with academic centers that supply translational expertise. Larger players deploy patient-support programs to offset therapy costs and defend share as generic chemotherapeutics pressure pricing. Intellectual-property portfolios center on PD-(L)1 pathways, yet next-generation checkpoints (LAG-3, TIGIT) are advancing, foreshadowing a layered competitive field that sustains innovation in the anal cancer market.

Anal Cancer Industry Leaders

Amgen Inc.

Bristol Myers Squibb

Celgene Corporation

Eli Lilly and Company

F. Hoffman La Roche Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: ImmunityBio received FDA expanded-access authorization for ANKTIVA to treat lymphopenia in solid-tumor patients, including anal cancer.

- May 2025: FDA approved Zynyz (retifanlimab-dlwr) as the first first-line therapy for advanced squamous cell carcinoma of the anal canal.

- February 2025: ASTRO issued its inaugural guideline standardizing intensity-modulated radiation with concurrent chemotherapy for anal cancer.

- February 2025: Oncolytics Biotech advanced pancreatic and anal cancer trials evaluating pelareorep with checkpoint inhibitors.

Global Anal Cancer Market Report Scope

According to the scope, anal cancer is an abnormal growth of cells in or around the anus or anal canal.

The anal cancer market is segmented by cancer type (carcinoma in situ, squamous cell carcinoma, melanoma, adenocarcinoma, basal cell carcinoma, and other cancer types), treatment type (chemotherapy, surgery, radiation therapy, and immunotherapy), end-users (hospitals and clinics, research and academic institutes, and other end-users) and geography (North America, Europe, Asia-Pacific, the Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally.

The report offers a value of USD for the above segments.

| Carcinoma In-Situ |

| Squamous Cell Carcinoma |

| Melanoma |

| Adenocarcinoma |

| Basal Cell Carcinoma |

| Other Cancer Types |

| Stage I-II |

| Stage III |

| Stage IV |

| Recurrent Disease |

| Chemotherapy |

| Surgery |

| Radiation Therapy |

| Immunotherapy |

| Hospitals and Clinics |

| Research and Academic Institutes |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Cancer Type | Carcinoma In-Situ | |

| Squamous Cell Carcinoma | ||

| Melanoma | ||

| Adenocarcinoma | ||

| Basal Cell Carcinoma | ||

| Other Cancer Types | ||

| By Disease Stage | Stage I-II | |

| Stage III | ||

| Stage IV | ||

| Recurrent Disease | ||

| By Treatment Type | Chemotherapy | |

| Surgery | ||

| Radiation Therapy | ||

| Immunotherapy | ||

| By End-User | Hospitals and Clinics | |

| Research and Academic Institutes | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the anal cancer market?

The anal cancer market stands at USD 1.03 billion in 2026, with expectations to reach USD 1.42 billion by 2031.

Which cancer type holds the largest share?

Squamous cell carcinoma accounts for 79.84% of global revenue, making it the leading histology segment.

Why is Asia-Pacific the fastest-growing region?

Rapid HPV vaccination roll-out, expanding insurance coverage, and increasing screening capacity push Asia-Pacific growth to a 7.49% CAGR.

What recent therapy received first-line approval?

In May 2025 the FDA cleared Zynyz (retifanlimab-dlwr) as the first first-line therapy for advanced anal cancer, establishing a new standard of care.

How do workforce shortages affect treatment capacity?

Radiation-therapy vacancies exceeding 11% in 2024 restrict expansion of IMRT services, limiting patient throughput, especially in community centers.

Which treatment modality is growing fastest?

Radiation therapy leads growth at 7.34% CAGR, propelled by guideline-driven adoption of intensity-modulated techniques that lower toxicity and improve outcomes.

Page last updated on: