Castrate Resistant Prostate Cancer Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 13.88 Billion |

| Market Size (2031) | USD 21.09 Billion |

| Growth Rate (2026 - 2031) | 8.74% CAGR |

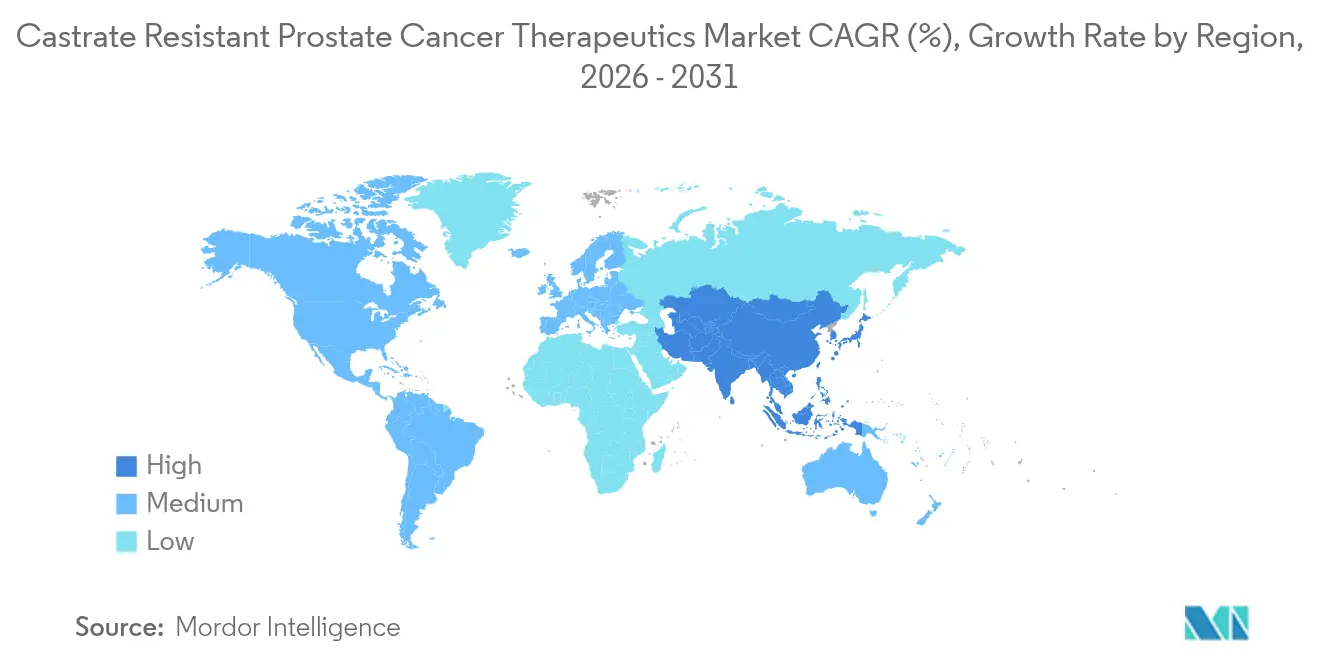

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

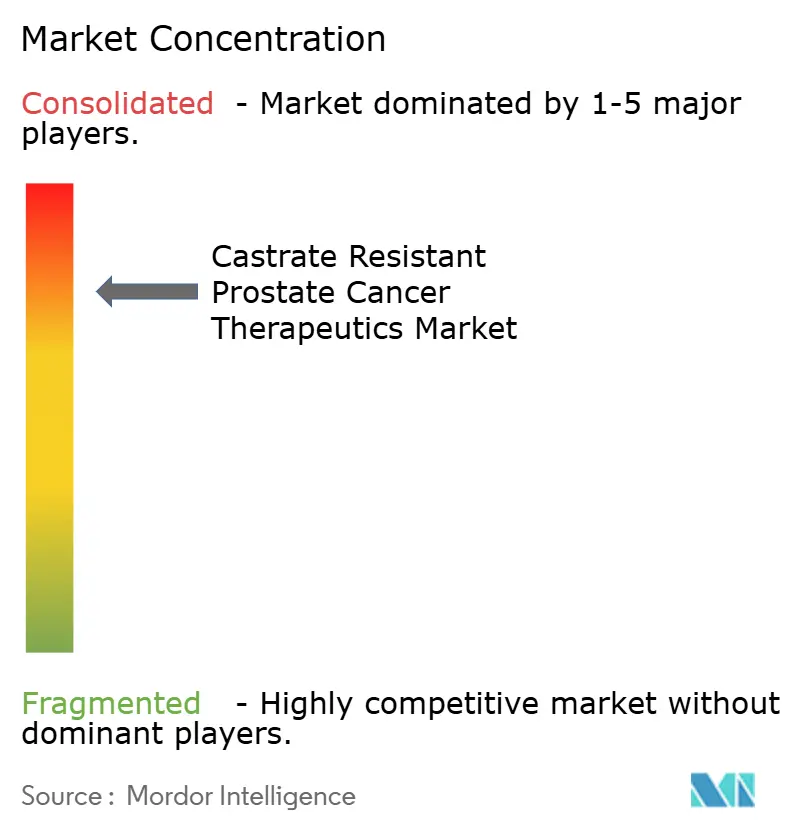

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Castrate Resistant Prostate Cancer Therapeutics Market Analysis by Mordor Intelligence

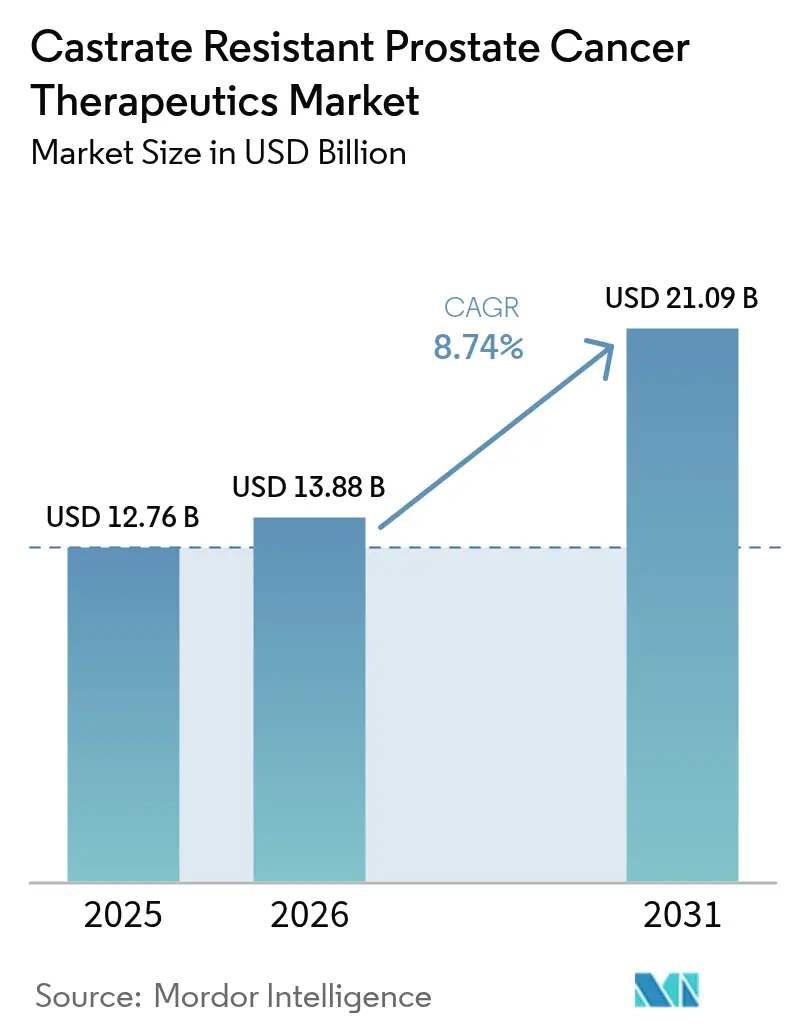

The Castrate Resistant Prostate Cancer Therapeutics market size is expected to grow from USD 12.76 billion in 2025 to USD 13.88 billion in 2026 and is forecast to reach USD 21.09 billion by 2031 at 8.74% CAGR over 2026-2031. Demand rises as global male longevity drives a steady increase in prostate cancer prevalence, while next-generation androgen-receptor (AR) inhibitors and radioligand therapies secure regulatory approvals. Precision medicine, particularly through PARP inhibitors in homologous-recombination-deficient patients, accelerates adoption. Companies strengthen clinical pipelines around combination regimens that integrate hormonal agents with DNA-damage response modulators, and governments fund screening programs that encourage earlier diagnoses. Together, these elements deepen therapeutic demand and sustain the CRPC therapeutics market’s robust growth trajectory.

Key Report Takeaways

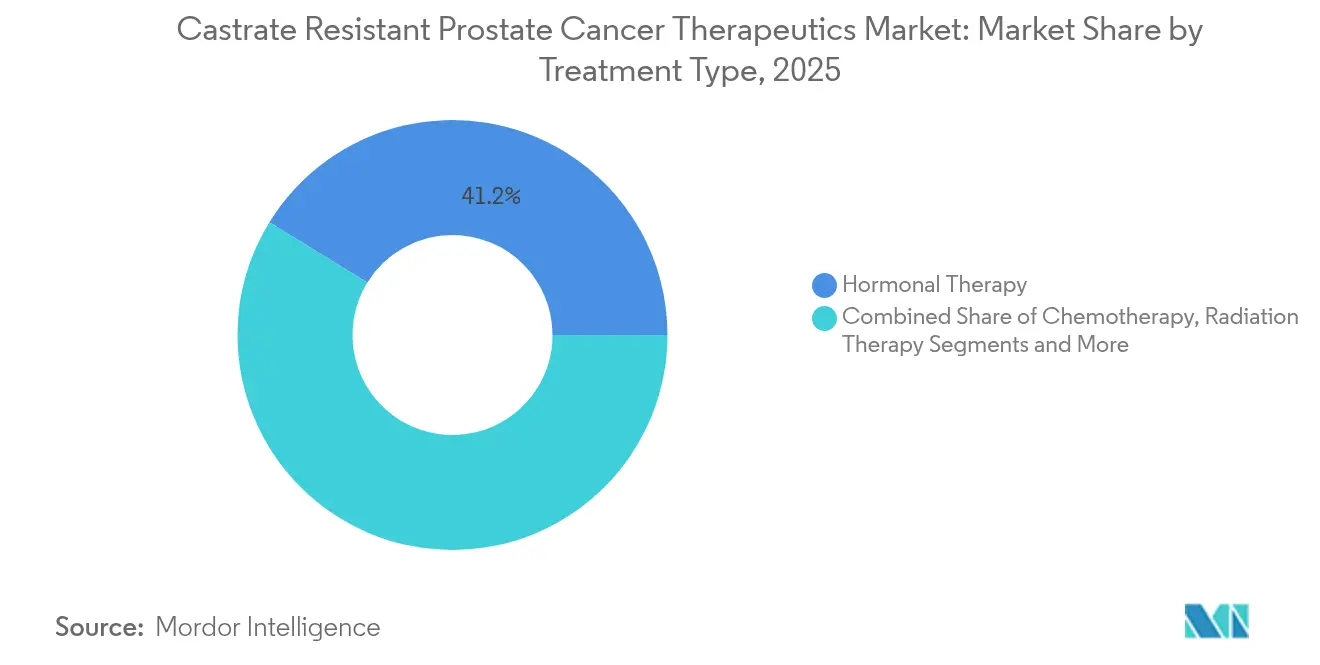

- By treatment type, hormonal therapy led with 41.22% revenue share in 2025; radiation therapy is advancing at an 10.62% CAGR through 2031.

- By mechanism of action, AR-signaling inhibitors accounted for 36.55% of the CRPC therapeutics market share in 2025, while DNA-damage response modulators are expanding at a 10.22% CAGR to 2031.

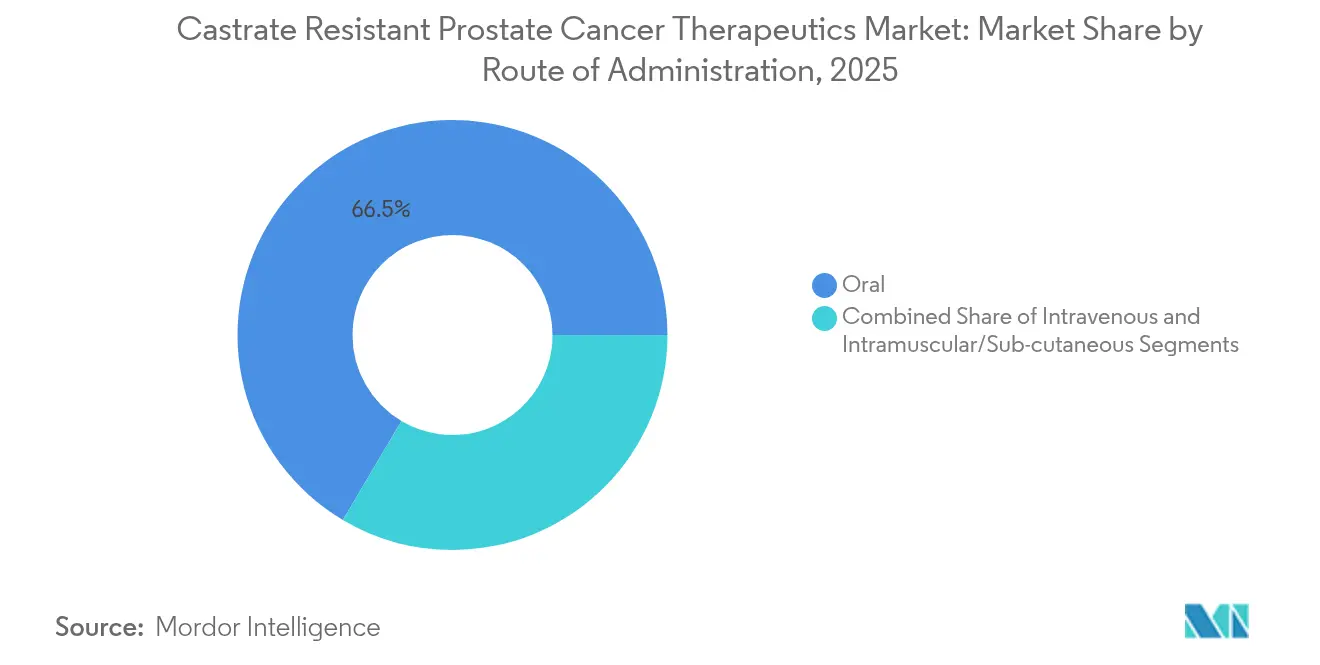

- By route of administration, oral therapies commanded 66.48% share of the CRPC therapeutics market size in 2025 and intravenous formulations are growing at a 9.92% CAGR through 2031.

- By geography, North America retained 40.10% share in 2025, whereas Asia-Pacific registers the fastest regional CAGR at 10.77% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Castrate Resistant Prostate Cancer Therapeutics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Aging Male Population & CRPC Prevalence | +2.1% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Wave of Next-Gen Androgen-Receptor (AR) Inhibitors | +1.8% | Global, led by North America & Europe | Medium term (2-4 years) |

| Favorable Survival Data For PARP-Inhibitors in HR-Mutated Patients | +1.5% | Global, with early adoption in North America | Medium term (2-4 years) |

| Government-Funded Screening & Awareness Programs | +1.2% | Europe & Asia-Pacific, expanding to emerging markets | Long term (≥ 4 years) |

| AI-Enabled Multi-Omics Stratification Driving Responder Identification | +0.9% | North America & Europe, with Asia-Pacific following | Medium term (2-4 years) |

| Rapid Scale-Up In Lu-177 & Ac-225 Isotope Supply For PSMA-Radioligand Therapy | +0.8% | Global, with manufacturing concentrated in North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Aging Male Population & CRPC Prevalence

The demographic tsunami of aging populations represents the most fundamental driver reshaping the CRPC therapeutics landscape. Global prostate cancer incidence is on course to double by 2040, with 10-20% of patients progressing to castrate-resistant disease despite initial hormone control. The aging population's impact extends beyond case volume to treatment complexity, as older patients often present with multiple comorbidities requiring sophisticated therapeutic approaches that balance efficacy with tolerability. Healthcare systems are responding by expanding geriatric oncology capabilities and developing age-appropriate treatment protocols that account for physiological changes in drug metabolism and toxicity profiles.

Wave of Next-Generation AR Inhibitors

Next-generation AR inhibitors have fundamentally altered CRPC treatment paradigms. Darolutamide and apalutamide prolong survival while offering lower seizure risk, leading to accelerated use in both metastatic castration-sensitive and resistant settings. Continuous R&D investment targets AR degraders and dual-pathway inhibitors that further improve clinical durability. The market impact extends beyond efficacy to include improved quality of life metrics, which are increasingly important in regulatory approval decisions and reimbursement negotiations.

Favorable Survival Data for PARP Inhibitors in HR-Mutated Patients

PARP inhibitors have emerged as precision medicine exemplars in CRPC treatment, with clinical trials demonstrating significant survival benefits in patients harboring homologous recombination deficiency mutations. Olaparib’s approval for BRCA-mutated metastatic CRPC established widespread germline and somatic testing. Trials pairing PARP inhibitors with AR antagonists or immunotherapy seek to widen treatment benefit to the 20-25% of patients harboring DNA-repair defects.[1]Source: Office of the Commissioner, “Good Clinical Practice: ICH E6(R3),” U.S. Food and Drug Administration, fda.gov This precision medicine approach has catalyzed investment in companion diagnostics development, with companies developing comprehensive genomic profiling platforms that can identify optimal treatment candidates and predict therapeutic response patterns.

Government-Funded Screening & Awareness Programs

Government initiatives to expand prostate cancer screening and awareness have created significant market expansion opportunities, particularly in underserved populations and emerging markets. Population-based screening across parts of Europe facilitates earlier detection, widens the candidate pool for advanced interventions, and trims long-term palliative costs. Emerging economies mirror these models to curb late-stage presentations. Government initiatives to expand prostate cancer screening and awareness have created significant market expansion opportunities, particularly in underserved populations and emerging markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Lifetime Treatment Cost (>$150k/Patient) | -1.4% | Global, most pronounced in emerging markets | Long term (≥ 4 years) |

| <15% Phase-III Success Rate for Novel Agents | -1.1% | Global, affecting all pharmaceutical companies | Medium term (2-4 years) |

| Global Shortfall of Medical-Grade Isotopes for Radiopharmaceuticals | -0.7% | Global, with regional variations in supply access | Short term (≤ 2 years) |

| Uneven Reimbursement for Next-Gen Genomic Companion Diagnostics | -0.6% | Variable by region, most challenging in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Lifetime Treatment Cost

The substantial financial burden of CRPC treatment creates significant access barriers that limit market expansion, particularly in price-sensitive healthcare systems and emerging markets. Long-term therapy sequences, genomic testing, and adverse-event management push lifetime spend above USD 150,000. Outcome-based contracts and patient-support schemes aim to expand access in price-sensitive regions. The substantial financial burden of CRPC treatment creates significant access barriers that limit market expansion, particularly in price-sensitive healthcare systems and emerging markets.

Less Than 15% Phase-III Success Rate for Novel Agents

The persistently low success rate for novel CRPC agents in Phase III trials represents a fundamental challenge that constrains innovation and increases development costs across the industry. Resistance heterogeneity leaves most late-stage programs short of primary endpoints, keeping development risk elevated and curbing pipeline breadth. Adaptive designs and biomarker-driven enrollment seek to lift success odds.[2]Source: U.S. Food and Drug Administration, “Core Patient-Reported Outcomes in Cancer Clinical Trials,” fda.gov The economic impact of high failure rates extends beyond individual companies to affect overall industry investment in CRPC research, creating potential long-term consequences for innovation and patient access to new therapies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Hormonal Therapy Dominance Faces Radiation Surge

Hormonal therapy contributed 41.22% of CRPC therapeutics market revenue in 2025 due to its entrenched role in androgen suppression. Radiation therapy, buoyed by PSMA-targeted radioligand successes, records the fastest 10.62% CAGR and is expected to capture increasing share of the CRPC therapeutics market size by 2031. Chemotherapy remains a later-line option while immunotherapy and targeted agents broaden treatment diversity.

Clinicians now tailor sequencing around molecular profiling, often introducing radioligand therapy after AR-signaling inhibitor failure. Integration of AI decision tools refines patient selection and aligns therapy with individual disease biology, thereby enhancing response rates and sustaining the CRPC therapeutics market’s progression. This technological advancement is particularly important in CRPC management, where treatment resistance mechanisms are complex and require personalized approaches to achieve optimal outcomes.

By Mechanism of Action: AR Signaling Inhibitors Lead While DNA-Damage Response Modulators Accelerate

AR-signaling inhibitors held 36.55% CRPC therapeutics market share in 2025 as darolutamide and apalutamide gained acceptance for their survival and safety benefits. DNA-damage response modulators, chiefly PARP inhibitors, exhibit a 10.22% CAGR through 2031 and will expand the CRPC therapeutics market size among genomically defined patients. CYP17 inhibitors maintain steady market presence, while PSMA-targeted therapies and immune checkpoint inhibitors represent emerging opportunities with significant growth potential.

Pipeline diversity widens with ATR and DNA-PK inhibitors, PROTAC AR degraders, and PSMA-directed antibody-drug conjugates that collectively address resistance mechanisms and open avenues for combination regimens. These technological advances are supported by improved understanding of prostate cancer biology and the development of sophisticated biomarker strategies that enable optimal patient selection and treatment sequencing.

By Route of Administration: Oral Preference Meets IV Innovation

Oral formulations dominated at 66.48% share in 2025, promoting adherence and reducing clinic visits. Intravenous therapies grow fastest at 9.92% CAGR as radioligand, antibody-drug conjugate, and cell-based modalities penetrate earlier treatment lines, expanding the CRPC therapeutics market. Intramuscular and subcutaneous routes represent smaller segments but offer opportunities for depot formulations and extended-release preparations that improve dosing convenience.

The route of administration preferences are influenced by evolving treatment paradigms that emphasize precision medicine and personalized therapy approaches. The development of innovative delivery technologies, including nanoparticle formulations and targeted drug delivery systems, is creating new opportunities to optimize therapeutic outcomes while minimizing systemic toxicity. These technological advances are particularly relevant in CRPC treatment, where patients often require multiple therapy lines and may experience cumulative toxicity from sequential treatments.

Geography Analysis

North America accounted for 40.10% of CRPC therapeutics market revenue in 2025, backed by comprehensive insurance coverage, leading research centers, and swift adoption of FDA-approved innovations. Robust clinical-trial density and an established companion diagnostics ecosystem reinforce regional dominance.

Asia-Pacific registers an 10.77% CAGR, the fastest worldwide. China benefits from large patient pools and state-supported oncology infrastructure expansions, while Japan and Australia maintain high baseline adoption of advanced treatments. Growing molecular diagnostic penetration, coupled with national reimbursement adjustments, nudges the CRPC therapeutics market towards higher regional uptake.

Europe remains mature yet opportunity-rich, led by Germany, the United Kingdom, and France. Stringent health-technology assessments enforce real-world evidence requirements, prompting companies to document cost-effectiveness alongside clinical gains. Eastern European health-system upgrades and EU-wide prostate cancer awareness campaigns also contribute to incremental growth.

Regulatory Landscape

Regulation in castrate-resistant prostate cancer (CRPC) therapeutics continues to move toward biomarker-defined labels and combination regimens, with major agencies tying eligibility to validated genomic and imaging selection tools. In the United States, the FDA granted regular approval in December 2025 for rucaparib (Rubraca) in metastatic CRPC with deleterious BRCA mutations after prior androgen receptor-directed therapy, reinforcing homologous recombination repair testing as a practical gatekeeper for PARP inhibitor use.

Across other major markets, regulators have expanded access and added competitive generics while tightening companion diagnostic requirements for targeted and radioligand pathways. Japan's PMDA approved Pluvicto (lutetium 177 Lu vipivotide tetraxetan) and its companion diagnostic in September 2025 for PSMA-positive mCRPC. In March 2026, it approved a new indication for talazoparib (Talzenna) in mCRPC, underscoring the role of precision oncology in label expansions. In Europe, the European Commission granted marketing authorization in July 2025 for darolutamide (Nubeqa) in combination with ADT for metastatic hormone-sensitive prostate cancer, while the EMA granted marketing authorization in January 2026 for Enzalutamide Accordpharma, supporting broader access through additional branded and generic/authorized-generic options.

Competitive Landscape

The CRPC therapeutics market features moderate consolidation. Global leaders such as Johnson & Johnson, Bayer, Pfizer, and Sanofi leverage multibillion-dollar R&D budgets to pursue parallel programs in AR signaling, DNA repair, and radioligand spaces. These firms complement internal innovation with external partnerships, exemplified by Merck’s licensing of the CYP11A1 inhibitor opevesostat to strengthen hormonal-pathway coverage.

Biotechnology entrants intensify competition through focused modalities including PROTAC degraders, bispecific T-cell engagers, and PSMA-antibody-drug conjugates. Their agility attracts larger companies to acquisition or co-development deals, widening technology access while sustaining pipeline breadth.

Strategic priorities revolve around precision medicine and combination architectures. Leading players align with diagnostics firms to embed genomic testing in treatment algorithms, and they co-develop radioligand-plus-AR inhibitor or PARP-plus-AR inhibitor regimens to extend franchise exclusivity. Collectively, these moves channel substantial capital into late-stage assets that reinforce scale advantages without markedly raising market concentration levels.

Castrate Resistant Prostate Cancer Therapeutics Industry Leaders

-

Sanofi

-

Johnson & Johnson

-

Bayer AG

-

Dendreon Pharmaceuticals LLC

-

Pfizer Inc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are centered on precision-led sequencing and combination strategies that address resistance while expanding treatable subgroups across earlier and later lines. The PEACE-3 phase III readout shared by EORTC (February 2026) reported an overall survival benefit for enzalutamide combined with radium-223 in mCRPC patients with bone metastases (24% reduction in risk of death versus enzalutamide alone). This highlights room for regimen designs that pair established AR pathway inhibitors with bone-targeted radiopharmaceuticals in metastatic patterns seen in routine care.

A second set of opportunities comes from the widening modality mix beyond oral AR signaling inhibitors, including antibody-drug conjugates, bispecific/T-cell engager approaches, and next-generation AR agents for post-chemotherapy or post-ARPI populations. In July 2026, ORIC initiated the registrational Himalayas-1 phase III trial evaluating rinzimetostat with Bayer's darolutamide in previously treated mCRPC, reflecting continued investment in combination backbones anchored by standard AR inhibitors. Activity is also visible in pivotal ADC development: Duality Biotherapeutics and BioNTech dosed the first patient in May 2026 in a global phase III trial of DB-1311/BNT324 for mCRPC in a pre-taxane setting. Together, these moves point to commercial whitespace for differentiated IV oncology platforms that can be integrated into sequencing algorithms supported by molecular and clinical stratification.

Recent Industry Developments

- July 2026: ORIC Pharmaceuticals initiated the global Phase 3 Himalayas-1 registrational trial evaluating rinzimetostat in combination with Bayer's NUBEQA (darolutamide) for metastatic castration-resistant prostate cancer patients previously treated with abiraterone. The trial design focuses on combination sequencing around an established AR inhibitor backbone, highlighting competitive emphasis on extending durability after standard hormonal therapy exposure.

- May 2026: Duality Biotherapeutics and BioNTech reported dosing of the first patient in a global pivotal Phase 3 trial of the B7-H3 antibody-drug conjugate DB-1311/BNT324 in metastatic castration-resistant prostate cancer patients who have not received taxane-based chemotherapy. Advancing an ADC into a pivotal, earlier-line mCRPC population increases competitive pressure on intravenous targeted modalities and reinforces investment in clinic-delivered oncology platforms alongside oral standards of care.

- April 2026: Vir Biotechnology announced the closing of its global strategic collaboration with Astellas to advance the investigational PSMA-targeting dual-masked T-cell engager VIR-5500 for prostate cancer. The partnership structure shows how large pharma is using collaborations to accelerate entry into PSMA-directed immune modalities that can complement or compete with radioligand and AR-pathway regimens across advanced disease settings.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers prescription drug revenues generated from therapies used to treat castrate-resistant prostate cancer, including treatment in both metastatic and non-metastatic settings where CRPC is clinically diagnosed and managed.

Scope exclusions: Supportive care medicines that do not treat CRPC biology (such as pain-only regimens), diagnostic tests, and procedures are not counted as part of this therapeutics market.

Segmentation Overview

-

By Treatment Type

- Chemotherapy

- Hormonal Therapy

- Radiation Therapy

- Other Treatment Types

-

By Mechanism of Action

- AR Signalling Inhibitors

- CYP17 Inhibitors

- PSMA-Targeted Therapies

- DNA-Damage Response Modulators

- Immune Checkpoint Inhibitors

-

By Route of Administration

- Oral

- Intravenous

- Intramuscular/Sub-cutaneous

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with mapping the treated patient pool and how it moves through key CRPC treatment lines, before we translate that flow into revenue. Public sources help anchor these building blocks, including cancer incidence and mortality releases from bodies such as the WHO and national cancer registries, payer and utilization statistics from agencies such as the US CDC and CMS, and drug approval and labeling information from regulators such as the FDA and EMA.

We also use peer-reviewed oncology journals and conference abstracts to cross-check adoption patterns for newer mechanisms of action, plus company filings, investor decks, and reputable press for therapy launches and commercial commentary. In parallel, we reference paid subscriptions for company financial intelligence, patent tracking, and, where helpful, shipment-level import or export signals for selected drug categories. The sources cited here are illustrative only, and many other public and paid references are also used to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary inputs are used to sanity-check the treated cohort logic, line-of-therapy shares, and the real-world mix of mechanisms of action used across patient types. We speak with clinicians, hospital and specialty pharmacy stakeholders, payers, and industry participants across Americas, EMEA, and APAC so that regional reimbursement and practice patterns are reflected rather than averaged away.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 19% | APAC: 48% |

| Mid tier: 48% | Functional/Unit leaders: 30% | EMEA: 33% |

| Smaller Players: 19% | Managers: 51% | Americas: 19% |

Market-Sizing & Forecasting

Sizing is built using a demand-pool view, where epidemiology and treatment rates are used to reconstruct the number of treated CRPC patients, and then multiplied by regimen mix and annualized therapy cost ranges. To keep it practical, we focus on a few repeatable inputs, such as CRPC prevalence and progression assumptions, share of patients receiving active drug treatment by line of therapy, uptake of key drug classes (for example AR pathway inhibitors, chemotherapy, radioligand therapy, and PARP inhibitors), average duration of therapy, and country-level pricing and currency timing.

We corroborate totals with selective bottom-up checks, including roll-ups from publicly reported therapy sales where available, channel feedback on demand shifts, and sampled price-times-volume checks for representative countries. Where public data is thin, which is common in smaller markets, we handle gaps by using proxy markets with similar reimbursement levels and validating the implied per-patient spending with experts.

For forecasting, we use scenario analysis because growth depends heavily on launch timing, label expansions, and payer access changes. Assumptions on adoption curves, therapy switching, and price erosion are pressure-tested with primary respondents, then applied consistently across regions so year-to-year movement remains explainable.

Data Validation & Update Cycle

Outputs are checked against independent signals, including therapy class growth direction, published epidemiology, and internal consistency of implied spending per treated patient. When a country result looks unusual, we re-review the drivers, followed by targeted re-contact with respondents to confirm whether the variance is real or model-led.

Before sign-off, a second analyst reviews key assumptions, conversion steps, and arithmetic to catch definition drift and unit errors. Reports are refreshed annually, and interim updates are made when material events occur, such as a major approval, safety restriction, or a meaningful reimbursement change. Right before delivery, we run a final pass so clients receive the latest aligned view.

Mordor Intelligence's Castrate Resistant Prostate Cancer Therapeutics Market Market Estimate Compared With Other Published Estimates

Published market values for CRPC therapeutics often do not match, even when they appear to be describing the same disease area. The spread typically comes from differences in what is counted as therapy revenue, how the treated patient pool is constructed, and whether pricing and uptake reflect recent access and label changes.

Supportive care drugs used alongside CRPC regimens sit outside Mordor Intelligence's scope, which can pull totals below studies that bundle oncology symptom management into the same number. Gaps also appear when some publishers assume faster uptake for newer modalities, apply global average prices to mixed-income regions, or keep older currency rates and launch timing assumptions that do not align with current practice feedback.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 13.88 B (2026) | |

| Industry Publisher A | USD 8.50 B (2023) | Uses an earlier base year and often applies a narrower treated cohort build, which can understate later-line therapy intensity and newer class contribution in the total. |

| Research Outlet B | USD 5.63 B (2025) | Relies on simplified therapy grouping and limited regional price differentiation, which can reduce implied annual revenue per treated patient across higher-cost markets. |

The table indicates that base-year selection and scope items included in therapy revenue explain much of the spread, while uptake and pricing assumptions shape the remaining gap. By keeping inputs tied to treated patients, regimen mix, and realistic price ranges, results remain transparent and repeatable with clear checks.

Key Questions Answered in the Report

What is the current value of the CRPC therapeutics market?

The market stands at USD 13.88 billion in 2026.

How fast is the CRPC therapeutics market expected to grow?

It is projected to post a 8.74% CAGR between 2026 and 2031.

Which treatment type leads the market?

Hormonal therapy holds 41.22% revenue share as of 2025.

Which region exhibits the fastest growth?

Asia-Pacific records the highest regional CAGR at 10.77% through 2031.

Why are PARP inhibitors important in CRPC?

They provide notable survival benefits for patients with homologous-recombination-deficient tumors, expanding precision-medicine adoption.

Page last updated on: