Benign Prostatic Hyperplasia Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 8.26 Billion |

| Market Size (2031) | USD 10.61 Billion |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

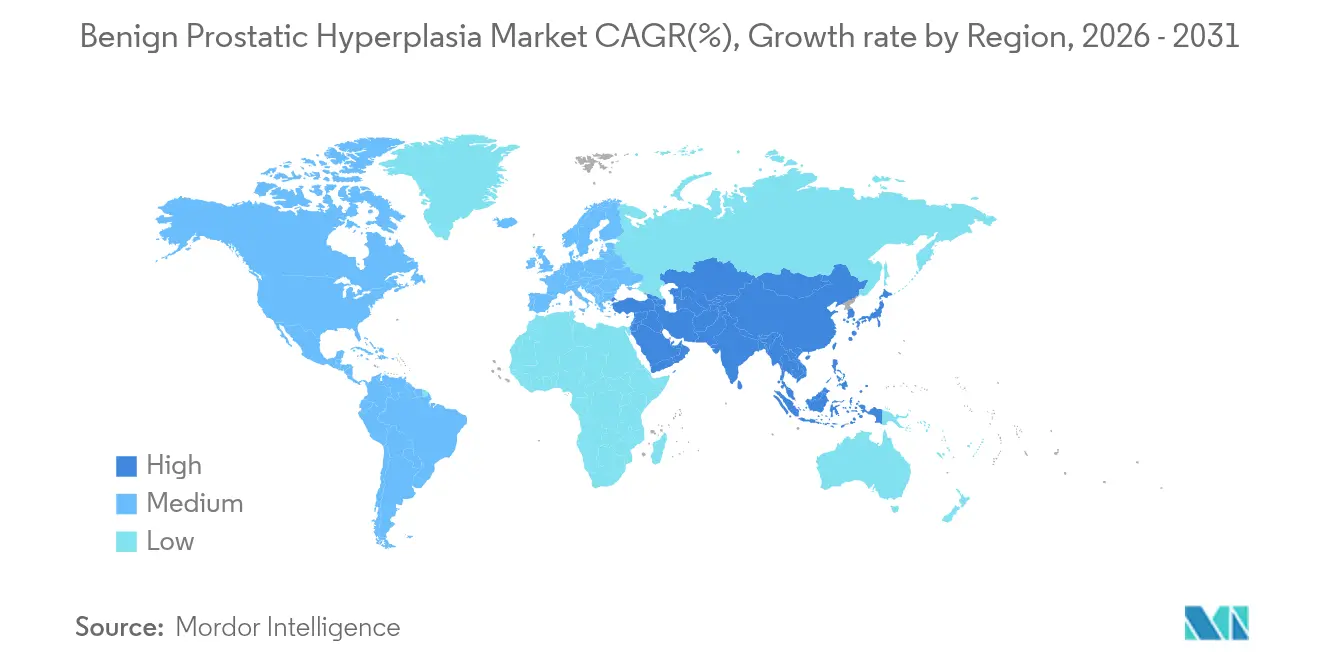

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Benign Prostatic Hyperplasia Market Analysis by Mordor Intelligence

The Benign Prostatic Hyperplasia market size is expected to grow from USD 7.86 billion in 2025 to USD 8.26 billion in 2026 and is forecast to reach USD 10.61 billion by 2031 at 5.12% CAGR over 2026-2031.

Growth stems from the rising global population of men aged ≥ 50, rapid uptake of tele-urology services, and the steady migration toward fixed-dose combination (FDC) products that promise faster symptom relief with fewer sexual side effects. North America remains the largest regional opportunity, supported by integrated electronic health records that streamline renewal prescriptions, while Asia-Pacific is advancing the fastest as China’s national screening campaigns accelerate early diagnosis. Competition is intensifying as minimally invasive surgical therapies (MISTs) such as Aquablation and UroLift win payer backing, prompting drug makers to emphasize real-world evidence around quality-of-life improvement. In parallel, e-commerce pharmacies are widening patient access and nudging adherence rates upward by enabling discreet home delivery and automated refill reminders.

Key Report Takeaways

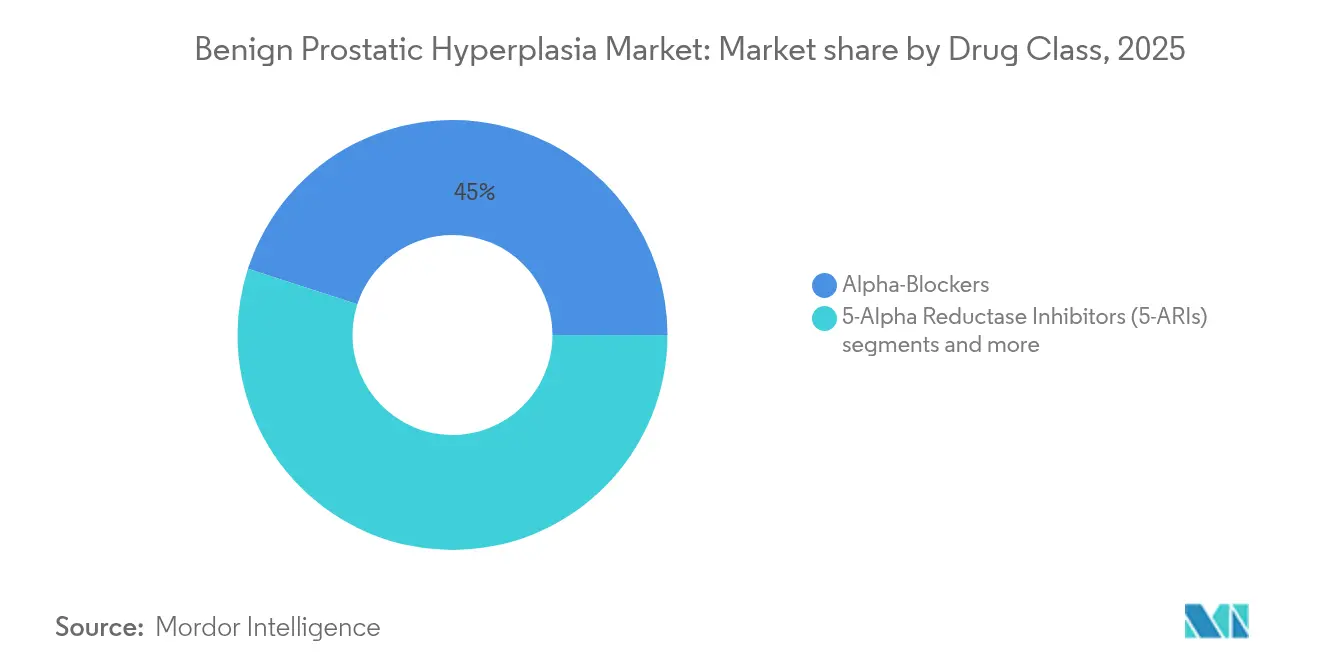

- By Drug Class, Alpha-Blockers led with 45.02% market share in 2025; PDE-5 Inhibitors are forecast to expand at a 6.74% CAGR through 2031.

- By Dosage Form, Immediate-Release Tablets/Capsules held 57.43% of the market share in 2025, while Orally Disintegrating Tablets recorded the highest projected CAGR at 5.49% through 2031.

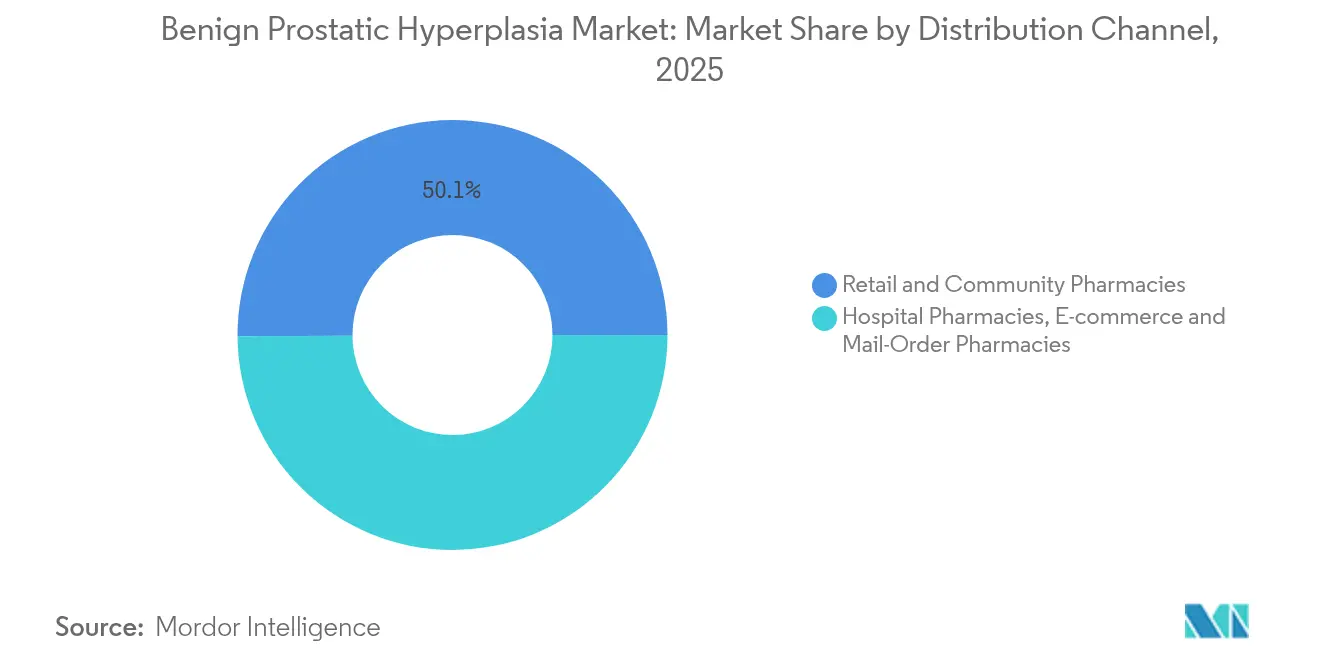

- By Distribution Channel, Retail & Community Pharmacies accounted for 50.10% share of the BPH drugs market in 2025; E-commerce & Mail-Order is advancing at a 5.86% CAGR through 2031.

- By Geography, North America commanded 39.55% of the market share in 2025, while Asia-Pacific recorded the fastest projected CAGR at 6.78% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Benign Prostatic Hyperplasia Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge of Tele-urology Platforms Expanding Prescription Volumes in North America | +1.20% | North America, with spillover to Europe | Medium term (2-4 years) |

| National Prostate Health Screening Campaigns Elevating Diagnosis Rates in China | +1.50% | China, with influence across Asia-Pacific | Medium term (2-4 years) |

| Government Price Caps on Generic Drugs | +0.70% | Global, with emphasis on emerging markets | Short term (≤ 2 years) |

| Reimbursement Expansion for Dutasteride/Tamsulosin FDC | +1.10% | North America, Europe | Medium term (2-4 years) |

| Rising Preference for Combination α-Blocker/5-ARI Fixed-Dose Pills in Europe | +1.00% | Europe, with expansion to North America | Medium term (2-4 years) |

| Accelerated Private Urology Clinic Build-outs Across GCC Nations | +0.80% | GCC countries, with spillover to Middle East | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge of Tele-urology Platforms Expanding Prescription Volumes in North America

Telehealth now manages up to 30% of outpatient urology visits with patient-satisfaction levels above 85% Scientific Reports. Rural areas benefit most; earlier care access has narrowed the historical 20% urban–rural mortality gap tied to prostate conditions[1]Source: David Sheyn, “Rural Health Disparities in Urologic Care,” auanews.net . Integrated data feeds let clinicians track International Prostate Symptom Score (IPSS) trends remotely, facilitating timely shifts to combination therapy once monotherapies plateau. Automated refill alerts on these platforms curtail the 30% discontinuation rate historically linked to adverse sexual effects, thereby elevating lifetime prescription volume.

National Prostate Health Screening Campaigns Elevating Diagnosis Rates in China

Under Healthy China 2030, municipal clinics conduct routine prostate checks, markedly increasing early-stage BPH detection bayer.com. Acceptance of foreign clinical dossiers has shortened launch timelines for innovative therapies, giving global manufacturers faster on-ramp to the world’s largest patient pool. Enhanced reimbursement from the National Medical Security Bureau further supports medicine uptake, extending therapy duration before surgical referral and inflating cumulative drug spending.

Government Price Caps on Generic Drugs

Policy actions such as the U.S. Medicare Prescription Drug Inflation Rebate Program are flattening list-price escalations, squeezing margins on tamsulosin and finasteride generics govinfo.gov. Branded FDCs are shielded by clinical differentiation, prompting manufacturers to position them within value-based agreements tying payer spend to reduction in acute urinary retention episodes. In emerging markets, volume-based procurement offsets margin pressure for firms with efficient supply chains.

Reimbursement Expansion for Dutasteride/Tamsulosin FDC

Clinical evidence from the CombAT study shows superior symptom relief versus monotherapies, pushing payers to widen FDC coverage ca.gsk.com. Despite isolated formulary removals such as Blue Cross Blue Shield of Massachusetts delisting Jalyn effective 2025 bluecrossma.org, real-world data demonstrate fewer surgical conversions, encouraging value-based contracts that favor FDCs in capitated systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Finasteride Sexual-Side-Effect Concerns Dampening Adherence | -0.90% | Global, with higher impact in developed markets | Long term (≥ 4 years) |

| Rising Preference for Minimally Invasive Procedures Cannibalizing Drug Revenues | -1.30% | North America, Europe, developed Asia | Medium term (2-4 years) |

| Shortage of Fellowship-Trained Endourologists in Sub-Saharan Africa | -0.70% | Sub-Saharan Africa, with spillover to emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Finasteride Sexual-Side-Effect Concerns Dampening Adherence

Post-marketing surveillance links finasteride to persistent erectile dysfunction and reduced libido, prompting hazard-ratio-verified follow-up visits well after cessation. Younger cohorts place a premium on sexual function, elevating discontinuation to near 30%. The trend is steering prescribers toward alpha-blockers or FDCs that combine finasteride with tadalafil, a PDE-5 inhibitor shown to mitigate sexual adverse events.

Rising Preference for Minimally Invasive Procedures Cannibalizing Drug Revenues

UroLift, Rezūm, and Aquablation promise durable symptom relief and preserve sexual function. Two randomized trials presented at AUA 2025 showed UroLift delivering superior IPSS reduction within three months compared with tamsulosin, prompting 70% of medication-only patients to cross over to the device arm [2]Source: Teleflex Incorporated, “New Clinical Data Presented at AUA 2025,” urolift.com . Cost-effectiveness models position prostatic artery embolization at USD 64,842 per QALY versus long-term pharmacotherapy, encouraging insurers to pre-authorize MISTs earlier in the care continuum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Combination Therapies Edge Toward Mainstream

Alpha-blockers generated the largest revenue base in 2025, holding 45.02% of benign prostatic hyperplasia drugs market share. Tamsulosin 0.4 mg remains the anchor therapy given its rapid onset and favorable cardiovascular profile. Yet, PDE-5 inhibitors are pacing the highest 6.74% CAGR, benefiting from dual urological and sexual-health indications that enhance compliance. FDCs such as dutasteride/tamsulosin (Jalyn) and finasteride/tadalafil (ENTADFI) integrate prostate-volume reduction with erectile-function support, expanding their addressable audience among sexually active patients. Network meta-analyses confirm that alpha-blocker + PDE-5 inhibitor regimens significantly outscore monotherapies on IPSS and quality-of-life scales.

By Dosage Form: Orally Disintegrating Tablet Adoption Gathers Pace

Immediate-release tablets accounted for 57.43% of benign prostatic hyperplasia drugs market size in 2025, reflecting established production lines and low unit costs. Softgel technology remains central to dutasteride delivery, optimizing solubility of lipophilic actives. Patient-centric innovation is now tilting development toward orally disintegrating tablets (ODTs). Tadalafil ODT (Chewtadzy) debuted in mid-2024, offering swallow-free administration that appeals to older adults with dysphagia. Taste-masking and moisture-barrier advances are enabling life-cycle extension strategies, with multiple ODT filings under review for 2026 launch.

By Distribution Channel: Digital Dispensing Accelerates

Retail pharmacies supplied half of all prescriptions in 2025, aided by counseling services and real-time benefits checks that streamline reimbursement. Hospital pharmacies underpin initiation during acute urinary retention episodes, particularly when inpatient status facilitates baseline labs and blood-pressure monitoring. E-commerce and mail-order outlets are the breakout channel, targeting a 5.86% CAGR as tele-urology scripts are routed directly to partnered fulfillment centers. Early evidence shows that automated refill scheduling via online portals lifts medication-possession ratios above 80%, a threshold seldom achieved in brick-and-mortar settings.

Geography Analysis

North America commanded 39.55% of 2025 revenue, underpinned by broad insurance coverage and high diagnostic penetration. The U.S. Inflation Rebate Program tempers list-price inflation yet sustains access to combination products viewed as reducing downstream surgical costs. Formularies remain fluid; the 2025 Blue Cross Blue Shield of Massachusetts exclusion of Jalyn and Entadfi underscores the need for sophisticated market-access strategies bluecrossma.org. Canada benefits from pan-provincial prostate-health campaigns, while Mexico’s Seguro Popular expansion propels generic uptake.

Asia-Pacific is the fastest-growing geography at 6.78% CAGR. China’s Healthy China 2030 initiative has normalized annual prostate screening in community clinics, tripling early-stage diagnosis rates and filling the therapy funnel. Japan's prescription volume for alpha-1 blockers increased, reflecting greater physician comfort with pharmacologic management. India and South Korea show momentum as public-sector hospitals integrate tele-urology pilots that shorten specialist waitlists.

Europe maintains a solid installed base, but rigorous health-technology assessments compress price–volume corridors. Germany and France favor FDCs with documented reduction in acute urinary retention, while the UK’s National Institute for Health and Care Excellence (NICE) is reassessing cost utility of MISTs versus lifelong medication. In the Middle East & Africa, Gulf Cooperation Council states are investing in urology centers that import branded alpha-blockers, whereas most sub-Saharan systems rely on low-cost generics, leaving pockets of unmet need. South America, led by Brazil, is widening insurance formularies for dutasteride after domestic real-world studies linked therapy persistence to lower hospitalization.

Regulatory Landscape

In the United States, BPH pharmacotherapies such as alpha-adrenergic antagonists and 5-alpha-reductase inhibitors continue to operate under established FDA labeling and pharmacovigilance requirements, with prescribing information standardized through FDA-approved product labeling (for example, via DailyMed). FDA also tightened device expectations for temporary urethral interventions, publishing a final classification in May 2025 for a temporarily placed urethral opening system for BPH as a class II device with special controls (codified under 21 CFR 876.5510), which sets clearer evidentiary and design-control expectations for manufacturers.

In Europe, drugs such as silodosin are regulated through the European Medicines Agency (EMA) centralized procedures, with European Public Assessment Reports (EPARs) supporting benefit-risk assessment and approved product information. Together, these tracks leave companies managing both modalities balancing mature, well-defined drug pathways against more prescriptive class II special-control routes for minimally invasive urethral or prostatic systems, which can affect development planning and compliance costs.

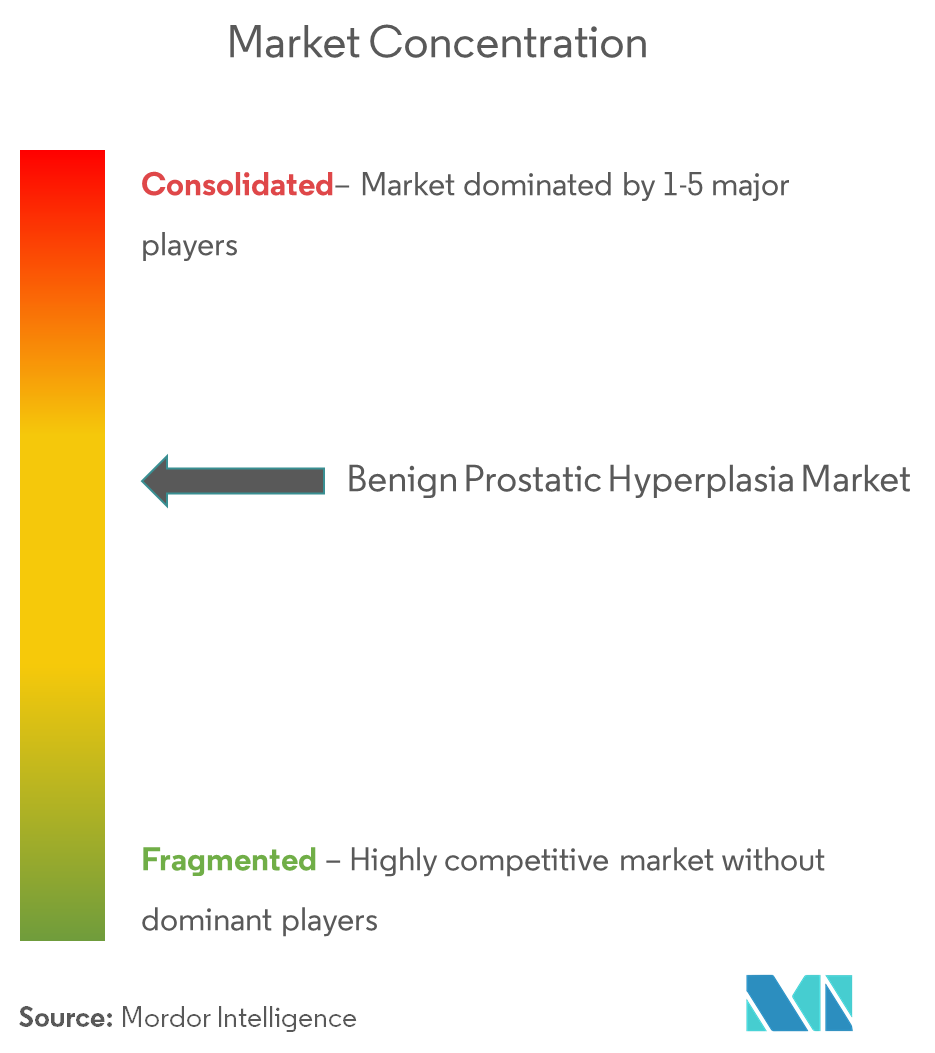

Competitive Landscape

The competitive field is moderately concentrated. GlaxoSmithKline, Viatris, and Astellas anchor incumbency with deep distribution and portfolios spanning monotherapies and FDCs. Innovation focus has shifted to patient-centric formulations and digital-health companions that boost adherence. Teleflex’s UroLift System strengthened its value proposition with 2025 data showing superior early IPSS and sexual-function outcomes versus Rezūm and tamsulosin urolift.com. PROCEPT BioRobotics logged a 57% revenue jump in Q4 2024 on Aquablation console uptake, signaling accelerating competition from surgical modalities.

Pharma responses include lifecycle-management tactics: GSK is exploring once-weekly dutasteride implants, while Astellas pilots app-based IPSS trackers that feed dosing-adjustment algorithms. Reimbursement turbulence drives diversification; Buckeye Health Plan’s 2025 shift of silodosin from Part D to Part B demands new billing workflows yet positions office-dispensed therapy favorably for urologists. Emerging players such as Medicus Pharma aim to introduce Teverelix, a GnRH antagonist targeting acute urinary retention prevention, broadening mechanism diversity in the benign prostatic hyperplasia drugs market.

Benign Prostatic Hyperplasia Industry Leaders

Allergan PLC

Eli Lilly and Company

Merck & Co., Inc.

Boehringer Ingelheim

Astellas Pharma Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term whitespace sits at the interface of BPH therapy and coexisting storage symptoms, where add-on pharmacology and combination regimens can reduce symptom burden without shifting patients to procedural care. A concrete signal came with the December 2024 FDA approval of GEMTESA (vibegron) for men with overactive bladder symptoms receiving pharmacological therapy for BPH, expanding the labeled toolbox for clinicians managing mixed LUTS phenotypes and supporting broader co-prescribing alongside alpha-blockers, 5-ARIs, PDE-5 inhibitors, and fixed-dose combinations.

There is also ongoing opportunity in formulation and channel work that improves persistence and reduces friction for older patients, including orally disintegrating tablets and digitally routed refills via tele-urology workflows. At the same time, clinical development activity around localized approaches, including intraprostatic drug-elution platform presentations at AUA 2026 and publication of VAPOR 2 pivotal-trial results in The Journal of Urology (June 2026), is raising expectations for time-to-relief and sexual-function preservation. Drug manufacturers and payers can respond by updating real-world evidence packages, strengthening adherence tooling, and using value-based positioning to defend the long-duration medication segment as earlier procedural crossover becomes more salient.

Recent Industry Developments

- May 2026: Rivermark Medical raised USD 20 million in a Series D financing led by Andera Partners to support its BPH treatment solutions. The funding provides additional runway for clinical and commercialization activities in a crowded LUTS landscape. It also signals continued investor appetite for differentiated BPH modalities even as pharmacotherapy faces substitution pressure from minimally invasive care.

- April 2025: Medicus Pharma signed a USD 75 million agreement to acquire Antev and secure Teverelix, a GnRH antagonist program positioned around acute urinary retention prevention linked to BPH. The transaction broadened Medicus Pharma’s mechanism mix beyond established alpha-blocker and 5-ARI pathways. It also highlighted ongoing M&A interest in differentiated, non-traditional pharmacologic approaches tied to clinically meaningful BPH complications.

- January 2024: Sumitomo Pharma America received FDA approval for GEMTESA (vibegron) for men with overactive bladder symptoms receiving pharmacological therapy for BPH. The label expansion reinforced the clinical need to address storage symptoms that persist alongside standard BPH drug regimens. It supports combination prescribing strategies and can shift treatment algorithms toward earlier management of mixed LUTS presentations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenue generated from prescription medicines used to manage benign prostatic hyperplasia (BPH) symptoms in adult men. The scope is focused on commonly prescribed oral or soft-gel therapies used in routine clinical care and dispensed through standard pharmacy channels.

Scope exclusions: This sizing excludes minimally invasive and surgical therapy revenues, energy-based treatment devices, supplements, and catheter sales.

Segmentation Overview

- By Drug Class

- Alpha-Blockers

- 5-Alpha Reductase Inhibitors (5-ARIs)

- Phosphodiesterase-5 (PDE-5) Inhibitors

- Combination Therapies (α-Blocker + 5-ARI / PDE-5)

- Others

- By Dosage Form

- Oral Immediate-Release Tablets / Capsules

- Oral Extended-Release Tablets

- Softgel Capsules

- Orally Disintegrating Tablets (ODT)

- By Distribution Channel

- Hospital Pharmacies

- Retail & Community Pharmacies

- E-commerce & Mail-Order Pharmacies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the boundaries of what counts as BPH drug revenue and to anchor the epidemiology and treatment pathway assumptions that sit behind demand. Public sources, such as the World Health Organization, the US CDC, the US FDA drug-label and safety update pages, and OECD health statistics, helped us align on patient age bands, diagnosis rates, and how treatment decisions typically move from watchful waiting to prescription therapy.

We also reviewed treatment guidelines and clinical evidence from sources such as the American Urological Association and peer-reviewed urology journals to confirm which drug classes are routinely used and how persistence and switching affect volumes over time. Company annual reports, investor presentations, and reputable press were referenced to cross-check therapy-mix changes and regional commercialization signals. Where needed, paid subscriptions for company financials and patent databases were used selectively to validate product pipelines and maturity. These sources are illustrative only, and additional public materials were reviewed to fill gaps, confirm assumptions, and clarify data points.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with urologists, hospital pharmacy stakeholders, and industry managers involved in BPH therapy commercialization and market access. We used these inputs to confirm treated-patient shares, typical dosing and duration, channel split across hospital, retail, and e-pharmacy, and the practical pace at which prescribing shifts between drug classes across major regions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 12% | APAC: 43% |

| Mid tier: 41% | Functional/Unit leaders: 28% | EMEA: 30% |

| Smaller Players: 20% | Managers: 60% | Americas: 27% |

Market-Sizing & Forecasting

The market model starts with a top-down demand pool build-up. Adult men population by age is converted into an addressable BPH group using prevalence and diagnosis rates, then filtered to the treated cohort that receives prescription therapy. Because the scope is drug-only, volumes are tied back to therapy adoption for key drug classes, and spending is derived by applying class-level pricing and mix assumptions across hospital, retail, and e-pharmacy channels.

To keep the totals realistic, results are corroborated with selective bottom-up approximations, including sampled prescription volume signals, channel checks on typical monthly therapy cost, and supplier revenue sanity checks in countries where reporting is clearer. Inputs tracked include the share of men aged 40 and above, physician preference shifts between alpha-blockers, 5-alpha-reductase inhibitors, PDE-5 inhibitors, and fixed-dose combinations, average duration of therapy, and inflation-adjusted price progression by country and channel. For forecasting, scenario analysis was used to reflect different uptake paths for combination therapy and persistence, with assumptions tuned through what clinicians and access experts indicated was most likely in the next few years. Where country-level inputs were thin, proxy countries with similar clinical practice and reimbursement patterns were used, then adjusted based on interview feedback.

Data Validation & Update Cycle

Validation is handled through repeated cross-checks across independent signals, followed by a structured review before sign-off. Outputs are compared against epidemiology expectations, observed therapy-mix direction from guidelines and publications, and country-level pricing and channel realities shared during interviews. Any sharp jumps are investigated before being accepted.

If a data point materially changes, such as a new safety update, a guideline shift, or a pricing event in a large country, we re-contact relevant experts so the assumption can be re-tested. Reports are refreshed annually, with interim updates when major events can change demand or pricing. Before delivery, a final analyst pass is completed so clients get the most current view available at that time.

Mordor Intelligence's Benign Prostatic Hyperplasia Market Size Versus Other Published Estimates

Published market sizes for BPH often do not match because the underlying scope is not always the same, and even small changes in what is counted can move the total by billions. Differences typically show up around whether procedures and devices are included, which geographies are covered, and how pricing is converted and trended across years.

Prescription class mix, treated-patient share, and therapy duration are the gap drivers that matter most in this market, since they directly change the volume and spend implied by a model. Some publishers also report an all-treatment view that blends drugs with minimally invasive and surgical revenue, which naturally inflates the headline number. Others keep prices in constant currency or apply a different inflation path, which shifts the current-year value.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 8.26 B (2026) | |

| Global Publisher A | USD 13.13 B (2025) | Uses a broader BPH treatment scope that can combine pharmaceuticals with procedure or device-led care pathways, and the year reference differs, which makes the size look materially higher even before adjusting for currency timing. |

| Industry Publisher B | USD 13.05 B (2025) | Covers a wider care bundle that includes procedures and device-based interventions alongside drugs, and the demand pool is not restricted to prescription drug revenues only, so the total captures adjacent spending categories. |

Prescription volume signals and class-level guideline consistency are the checks that keep Mordor Intelligence's estimate tied to BPH drug revenues only, which is why the number is lower than treatment-wide totals that blend in procedures and devices. After adjusting for year and scope, the remaining spread mainly comes from how treated-patient share and price progression are set, so a clearly stated boundary plus repeatable inputs makes the comparison easier to interpret.

Key Questions Answered in the Report

What is the current Benign Prostatic Hyperplasia Market size?

The Benign Prostatic Hyperplasia Market is projected to register a CAGR of 5.12% during the forecast period (2026-2031)

What is the current benign prostatic hyperplasia drugs market size?

The benign prostatic hyperplasia drugs market size is USD 8.26 billion in 2026 and is projected to reach USD 10.61 billion by 2031.

Which region is growing fastest in BPH drug sales?

Asia-Pacific leads growth with a 6.78% CAGR forecast for 2026-2031, driven primarily by China’s nationwide prostate-health initiatives.

Which drug class dominates prescription volume?

Alpha-blockers remain the largest class, accounting for 45.02% of benign prostatic hyperplasia drugs market share in 2025.

Why are minimally invasive procedures affecting drug demand?

Procedures such as UroLift and Aquablation deliver rapid symptom relief while preserving sexual function, encouraging some patients to switch away from lifelong medication.

How is telemedicine influencing BPH drug adherence?

Tele-urology platforms integrate refill reminders and remote IPSS tracking, cutting discontinuation rates and expanding prescription volumes, especially in rural areas.

Page last updated on: