Algeria Distribution Boards Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

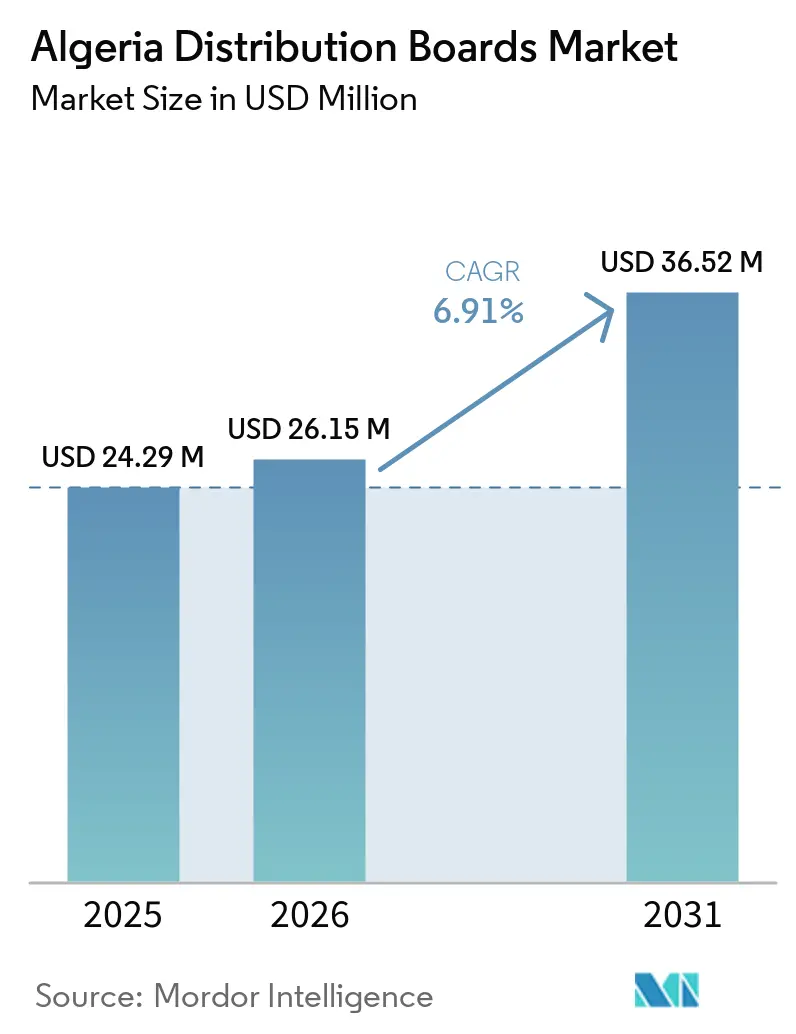

| Base Year Market Size (2025) | USD 24.29 Million |

| Market Size (2026) | USD 26.15 Million |

| Market Size (2031) | USD 36.52 Million |

| Growth Rate (2026 - 2031) | 6.91% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Algeria Distribution Boards Market Analysis by Mordor Intelligence

The Algeria Distribution Boards Market size is expected to grow from USD 24.29 million in 2025 to USD 26.15 million in 2026 and is forecast to reach USD 36.52 million by 2031 at 6.91% CAGR over 2026-2031. The Algeria distribution boards market is being supported by steady public spending on housing, electricity infrastructure, and industrial expansion, which is creating demand across residential, commercial, utility, and industrial projects. The Algeria distribution boards market is also moving toward more compliant and more intelligent panel configurations as grid modernization, digital monitoring, and renewable integration raise technical requirements for new installations.[1]Source: European Commission, “Strategic Partnership Between the People’s Democratic Republic of Algeria and the European Union in the Field of Energy,” European Commission, energy.ec.europa.eu Local assemblers are improving their position in the Algeria distribution boards market because shorter lead times, project-specific customization, and local approvals matter more when project schedules are tight. Large multinational Original Equipment Manufacturers (OEMs) still hold an advantage in premium applications because they provide approved product ranges, established distributor networks, and deeper technical support. Import dependence on breakers, busbars, and related switching parts remains the main execution risk in the Algeria distribution boards market and keeps supply chain control at the center of competition.[2]Source: European Commission, “EU Launches Arbitration Proceedings Against Algeria’s Trade and Investment Restrictions,” European Commission, policy.trade.ec.europa.eu

Key Report Takeaways

- By type, Main Distribution Boards held 44.2% share in 2025, while Final Distribution Boards are forecast to grow at 8.7% CAGR through 2031.

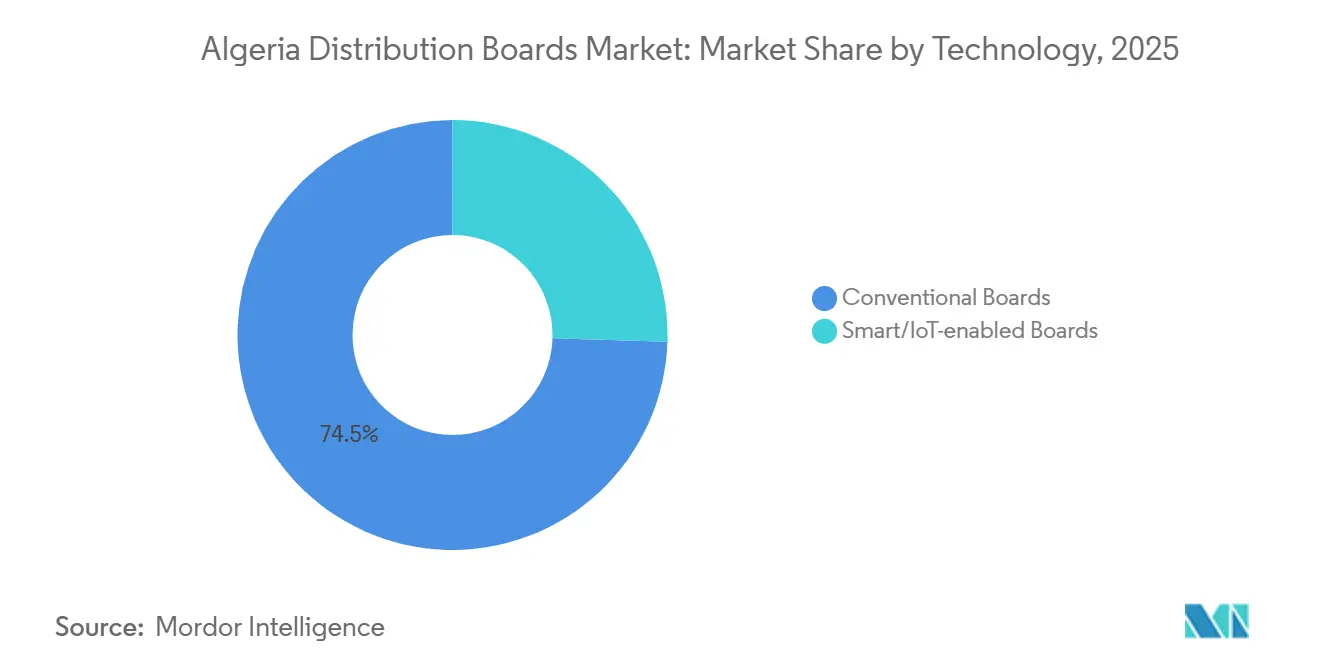

- By technology, conventional boards accounted for 74.5% share in 2025, while smart or Internet of Things (IoT) -enabled boards are projected to expand at 11.2% CAGR through 2031.

- By mounting type, wall-mounted boards held 62.8% share in 2025, while floor or free-standing boards are expected to grow at 8.1% CAGR through 2031.

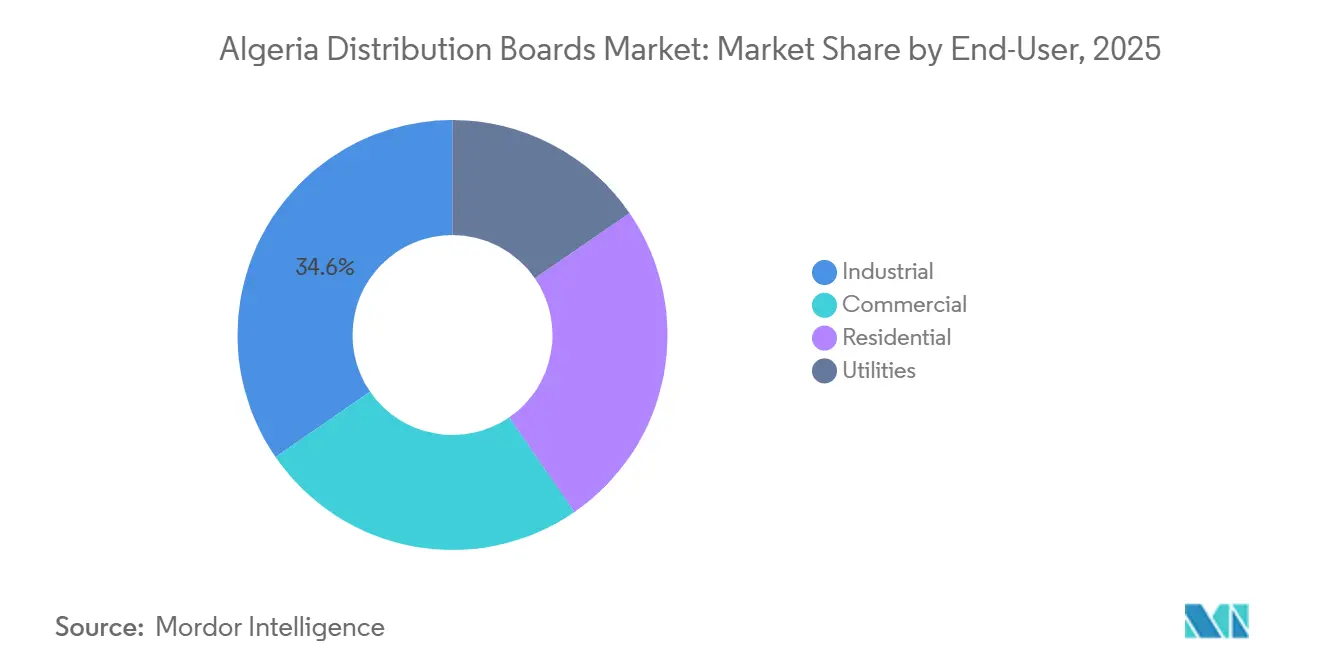

- By end-user, industrial users accounted for 34.6% share in 2025, while commercial users are projected to advance at 9.0% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Algeria Distribution Boards Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction and Public-Building Pipeline | +2.0% | National, with peak activity in Algiers, Oran, Constantine, and Agence Nationale de l'Amélioration et du Développement du Logement (AADL) 3 wilaya clusters | Short term (≤ 2 years) |

| Industrial and Activity-Zone Electrification | +1.4% | Hassi Messaoud, Berkine, Arzew, and AAPI zones in Djelfa, Tiaret, Tlemcen, Sidi Bel Abbès, and Constantine | Medium term (2-4 years) |

| Grid Modernization and Renewable Integration | +1.2% | National, with early gains in major urban control centers and southern solar corridors | Medium term (2-4 years) |

| Smart Metering and Digital Power Monitoring | +0.7% | Algiers, Oran, and Constantine urban clusters | Medium term (2-4 years) |

| Local Panel Assembly and Customization Ecosystem | +0.6% | Mostaganem, Algiers, Sidi Rached, Sidi Bel Abbès, and Ain Defla | Long term (≥ 4 years) |

| North-South Grid Hardening for Remote Loads | +0.5% | Tindouf, Ouargla, Ghardaïa, Béchar, and Adrar | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Construction and Public-Building Pipeline Sustains Front-End Demand

The Algeria distribution boards market is seeing its broadest near-term pull from public housing and public-building activity. Large housing programs are creating repeatable demand for final boards and sub-main panels because every apartment block, service core, and common area needs a defined electrical distribution layout. Demand is not limited to unit count because a higher in-building electrical load also changes the panel mix and pushes module counts higher in newer projects. The first deliveries under the current housing cycle are taking place in 2026, which keeps procurement linked to installation schedules rather than only to announced budgets. This matters for the Algeria distribution boards market because deliveries convert planning into real panel orders, not just future intent. The effect is strongest in large urban wilayas, but the spread of projects across the country keeps volume demand broad and helps sustain production runs for standard residential configurations.

Industrial and Activity-Zone Electrification Widens the Addressable Market for Industrial Distribution Panels

The Algeria distribution boards market is also benefiting from industrial land activation and utility connections to new production zones. AAPI opened new industrial land opportunities in several wilayas during 2026, which support future factories, logistics sites, and processing facilities that need higher-capacity power distribution equipment.[3]Source: Agence Algérienne de Promotion de l’Investissement, “AAPI Unlocks New Industrial Land for Investors Nationwide,” Horizons, horizons.dz Industrial demand differs from housing demand because board ratings are higher, site conditions are harsher, and customization is more common. The Hassi Messaoud refinery buildout and related oil and gas infrastructure keep large-format Main Distribution Boards and control-oriented panel packages in demand over longer project cycles. This changes the value profile of the Algeria distribution boards market because industrial projects usually support higher unit values than residential work. As more activity zones move from land allocation to utility-ready operation, procurement is likely to shift from isolated replacement orders to capacity-led orders tied to entirely new sites.

Grid Modernization and Renewable Integration Reshape Procurement Specifications

The Algeria distribution boards market is moving toward higher technical specifications as utilities modernize control systems and integrate more variable generation. Grid upgrades increase the need for boards that can host metering, protection, and energy management functions in a more organized and compliant assembly. The wider IEC 61439 framework is important here because buyers increasingly expect tested assemblies and clearer documentation, especially where uptime and safety are critical.[4]Source: International Electrotechnical Commission, “IEC 61439-3 2024, Low-Voltage Switchgear and Controlgear Assemblies, Part 3,” IEC Webstore, webstore.iec.ch Renewable additions in southern corridors also raise the need for distribution interfaces that can operate reliably in demanding environmental conditions. This is pushing the Algeria distribution boards market away from purely conventional specifications in some projects and toward smarter main boards, better enclosure design, and improved monitoring. Suppliers that can assemble locally and document compliance clearly are in a better position when projects move from concept to tender.

Smart Metering and Digital Power Monitoring Open Margin-Rich Applications

The Algeria distribution boards market has a smaller smart-board base today, but this category is becoming more attractive because digital monitoring raises the value of each installed panel. Smart metering and digital power architecture require communication-ready terminals, data capture capability, and cleaner integration of protection and monitoring devices. This creates better pricing opportunities than standard low-feature boards, especially in urban commercial buildings and more advanced utility applications. Digital infrastructure also supports the shift, as Algeria continues to place attention on data centers, ICT capacity, and modern electrical reliability standards for critical sites. The Algeria distribution boards market, therefore, gains not only from higher unit volumes but also from richer specifications in selected applications. Over time, this should widen the gap between basic assembled products and boards that include communication, logging, and power-quality visibility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Import Dependence on Critical Switching Components | -1.2% | National, with stronger pressure in projects requiring premium International Electrotechnical Commission (IEC) -rated components from EU and Asian suppliers | Short term (≤ 2 years) |

| Utility and IEC Certification Complexity | -0.8% | National, with greater difficulty in remote wilaya projects that have less field engineering support | Medium term (2-4 years) |

| Foreign-Exchange and Import Approval Delays | -0.9% | National, with sharper effects on smaller assembly firms | Short term (≤ 2 years) |

| Limited Field Capability for Smart-Board Deployment | -0.5% | Smaller wilayas and rural deployments outside the main urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Import Dependence for Critical Switching Components Compresses Domestic Value Retention

The Algeria distribution boards market still depends heavily on imported switching parts, and that limits the amount of value retained inside the country. Breakers, busbar systems, and related assemblies remain exposed to customs timing, shipping disruption, and supplier-side delays. The EU opened arbitration proceedings against Algeria in July 2025 over trade and investment restrictions, which shows that import procedures remain an active policy issue rather than a short-lived disruption. Algeria’s main import relationships for electrical goods include France, China, Turkey, and Germany, so any change in policy or logistics across those lanes can affect local panel assembly schedules. This keeps the Algeria distribution boards market vulnerable when projects are on fixed delivery dates and imported cartridges or accessories arrive late. It also explains why local production depth, not only local assembly, is becoming more important in long-term competition.

Foreign-Exchange and Import Approval Delays Introduce Execution Risk

The Algeria distribution boards market faces a second pressure point in the form of import administration and financing procedures. Algeria held foreign exchange reserves of USD 70 billion at the end of 2024, which supports the country’s broad import capacity at the macro level. Even so, project execution can still slow down when import approvals, documentation, or bank processes do not move at the same speed as construction milestones. This is a bigger issue for smaller assembly workshops because they have less buffer stock, weaker purchasing leverage, and less room to absorb a delayed shipment. The Algeria distribution boards market, therefore, carries an operational gap between announced demand and deliverable demand, especially during peak public construction periods. When housing, utility, and industrial projects all move at once, that gap can turn into missed commissioning windows and lost share for slower suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Final Boards Outpace the Mainstream as Housing Delivery Scales

Main Distribution Boards held 44.2% of Algeria distribution boards market share in 2025, while Final Distribution Boards are projected to grow at 8.7% CAGR through 2031. This split shows that the Algeria distribution boards market still derives a large part of its value from utility substations, industrial power centers, and large commercial supply points. Sub-Main Distribution Boards sit between those two ends of the system and provide a steady middle layer of demand in hospitals, multi-floor office buildings, and larger public facilities. Final boards are rising faster because residential delivery programs create repeatable and standardized order volumes at the apartment and block level.

Within the Algeria distribution boards market size outlook, Final Distribution Boards carry the strongest growth profile because current housing delivery is larger and electrically more demanding than earlier phases. The inclusion of added in-unit load, including heating-related circuits in newer projects, lifts panel module counts and supports better average selling values per installation. The Algeria distribution boards industry is also becoming more selective on compliance, and boards for ordinary residential use are being judged against clearer assembly expectations under IEC 61439-3. Local suppliers that combine CREDEG familiarity with TEDJ-backed credibility can improve their position in mass housing tenders because certification now supports both acceptance and buyer confidence.

By Technology: Conventional Boards Hold Ground While Smart Adoption Approaches an Inflection

Conventional boards retained 74.5% share in 2025, while smart or Internet of Things (IoT)-enabled boards are forecast to expand at 11.2% CAGR through 2031. That means the Algeria distribution boards market is still led by standard products, but the faster growth is already shifting toward monitored and communication-ready systems. Price sensitivity and field capability still favor conventional boards in many projects, especially outside the largest cities. At the same time, utilities, commercial buildings, and critical facilities are creating a clearer path for smart boards because those sites benefit more directly from monitoring, alarms, and data visibility.

The Algeria distribution boards market size for smart or IoT-enabled boards is rising because digital grid management and metering programs need distribution points that can support data and control functions, not only switching. Loss reduction, fault isolation, and power monitoring all become easier when boards provide better visibility at the panel level. The Algeria distribution boards industry also benefits from the growth of digital infrastructure because data centers and Information and Communications Technology (ICT) sites need cleaner redundancy logic and more disciplined panel architecture than standard buildings. This does not mean conventional boards will lose relevance soon, but it does mean the value mix in the Algeria distribution boards market should continue to shift toward more advanced configurations in selected urban and utility-linked projects.

By Mounting Type: Floor-Standing Boards Track the Industrial Expansion Cycle

Wall-mounted boards held 62.8% share in 2025, while floor or free-standing boards are projected to grow at 8.1% CAGR through 2031. Wall-mounted units dominate the Algeria distribution boards market because they fit the standard needs of apartments, smaller commercial sites, and many routine building installations. Their compact size, lower installation complexity, and familiarity among contractors support high shipment volumes. Floor-standing systems are growing faster because heavy industrial sites, larger utility interfaces, and advanced commercial infrastructure need higher current ratings and larger enclosure formats.

The Algeria distribution boards market size for floor or free-standing boards is expanding because industrial plants and data-centered commercial sites often cannot rely on compact wall-mounted assemblies. Oil and gas facilities in particular need ruggedized products, and some applications also require explosion-protected design logic that reduces the number of qualified suppliers. This raises average selling value for free-standing units and makes the segment more attractive on a revenue basis even when volumes are lower. In the Algeria distribution boards market, that pricing difference is important because margin-rich industrial and critical-power projects can shift competitive positioning even when the largest shipment counts still come from wall-mounted residential products.

By End-User: Commercial End-Users Drive the Next Growth Wave Beyond the Industrial Base

Industrial end-users held 34.6% share in 2025, while commercial end-users are forecast to grow at 9.0% CAGR through 2031. Industrial demand leads the Algeria distribution boards market because oil and gas, heavy processing, and utility-linked infrastructure all use larger and higher-value panel packages than standard buildings. Utilities remain a major buyer group because substations and network interfaces require more sophisticated assemblies than typical small-site installations. Residential users generate very high unit volumes, but their average panel values remain lower than those seen in industrial and advanced commercial projects.

The Algeria distribution boards market size for commercial users is increasing faster because new retail, mixed-use, office, telecom, and digital infrastructure projects require more complex low-voltage distribution layouts than basic residential blocks. This creates room for better specification, stronger monitoring capability, and more demand for sub-main and final boards with higher reliability requirements. Interest in Information and Communications Technology (ICT) and data-center development supports this shift and broadens commercial demand beyond traditional office and retail categories. In the Algeria distribution boards market, that means the next growth wave is not replacing industrial demand, but adding a second strong growth pillar alongside it.

Geography Analysis

The northern corridor generated the largest part of demand in the Algeria distribution boards market during 2025. This zone combines dense population, active housing delivery, commercial construction, and the strongest concentration of approved contractors and distributors. Algiers remains the main center for higher-specification commercial and institutional work, while Oran continues to build a stronger commercial project base. BESEE Oran’s local offering for commercial electrical solutions reflects rising activity in that western market and supports the view that the Algeria distribution boards market is no longer concentrated in Algiers alone.

The Saharan south forms a separate operating environment in the Algeria distribution boards market and requires a different board mix. Demand there is tied more closely to oilfields, mining-linked power systems, farm electrification, remote pumping loads, and long-distance network extension. These projects need boards that can handle dust, heat, and distance-related maintenance constraints, which changes enclosure choice and raises the value of ruggedized solutions. ATEX (Atmosphères Explosibles) -sensitive oil and gas sites narrow the supplier pool further because only a limited number of firms can serve those specifications credibly. As the south attracts more capital, the Algeria distribution boards market gains a second growth geography that is less about building density and more about project complexity.

Algeria’s position in the wider Mediterranean energy corridor strengthens the Algeria distribution boards market because hydrocarbon revenue supports public spending on power, housing, and utility works. The EU and Algeria deepened their strategic energy cooperation in 2026 through work covering electricity grids, green hydrogen, and energy efficiency under the TaqatHy+ framework. That cooperation improves technical readiness for more advanced electrical systems and supports the country’s ability to absorb smarter panel specifications. The result is a market where the north remains the volume center, the south is becoming the tougher premium zone, and national energy cooperation continues to widen the technical ceiling for future demand.

Competitive Landscape

The Algeria distribution boards market remains moderately fragmented, with multinational OEMs and locally rooted assemblers serving different parts of the opportunity set. Schneider Electric, ABB, Legrand, Eaton, and Hager are well-positioned in the Algeria distribution boards market because they have recognized product families, compliance track records, and established distributor relationships. Schneider Electric has an added advantage from long local manufacturing presence, which supports lead time control and local project alignment. This matters because government and utility buyers increasingly weigh delivery certainty and local content alongside brand strength.

Local companies are gaining more ground in the Algeria distribution boards market by competing on speed, customization, and familiarity with local approvals. GISB Electric, EDIEL, and Elsewedy Electric Algeria are becoming more visible as local or locally anchored players that can respond to project-specific requirements without the same import delay exposure as pure trading models. EDIEL’s own positioning shows a national client base that includes Sonelgaz, Sonatrach, and hydraulic infrastructure, which highlights how the competitive field extends well beyond imported catalog products. GISB’s export agreement in West Africa and Elsewedy’s planned industrial investments also show that the local manufacturing base is becoming more ambitious, not only more defensive. In the Algeria distribution boards market, that trend supports a gradual shift from simple assembly toward broader domestic capability.

Competition is also being shaped by policy and supply chains in the Algeria distribution boards market. EU arbitration over Algeria’s trade restrictions underlines how sensitive imported electrical equipment remains to regulation and market access rules. That pressure gives an edge to suppliers that can localize more of their offer, whether through direct manufacturing, local sourcing, or stronger stocking strategies. Strategic moves by leading companies already point in that direction, including Schneider Electric’s deeper local production footprint, GISB’s export-led scale building, and Elsewedy’s broader industrial investment push. The competitive picture, therefore, remains open, but it is moving toward firms that can combine approvals, supply certainty, and local execution discipline.

Algeria Distribution Boards Industry Leaders

Schneider Electric SE

Legrand SA

ABB Ltd.

Hager Group

EDIEL SPA

- *Disclaimer: Major Players sorted in no particular order

Geopolitical Scenario of War Around the World and Its Impact on the Algeria Distribution Boards Market

The Algeria distribution boards market has been affected by recent geopolitical tensions through both demand and supply. The Russia-Ukraine war increased Europe’s focus on secure pipeline-linked gas suppliers, and Algeria’s stronger role in that setting helped reinforce state spending capacity for energy and infrastructure works. Higher hydrocarbon income supports utility investment and public construction, which then feeds into panel demand through housing, grid, and industrial projects. At the same time, commodity and component cost pressure moved higher for imported electrical inputs, which reduced some of the benefit for local assemblers. The EU-Algeria High-Level Energy Dialogue in February 2026 confirmed deeper cooperation on grids, efficiency, and future energy systems, which supports the longer-term technical outlook for the Algeria distribution boards market.

Recent Industry Developments

- April 2026: AAPI initiated an investor solicitation program targeting industrial land parcels in five key wilayas: Constantine, Sidi Bel Abbès, Tlemcen, Djelfa–Médéa, and Tiaret. This initiative creates new opportunities for distribution panel suppliers in industrial zone electrification.

- February 2026: The sixth EU–Algeria High-Level Energy Dialogue reaffirmed Algeria's position as a strategic and reliable gas partner. It also initiated consultations under the TaqatHy+ grid and energy efficiency cooperation program, valued at EUR 28 million, which directly supports the development of smart distribution infrastructure.

Algeria Distribution Boards Market Report Scope

A distribution board, also known as a panelboard, breaker panel, or electric panel, is a component of an electricity supply system that distributes electrical power into subsidiary circuits while providing protective fuses or circuit breakers. The distribution board market involves the production, distribution, and sale of these panels, serving residential, commercial, industrial, and utility sectors, from small consumer units in homes to large switchboards in industrial facilities.

The Algeria Distribution Boards Market is segmented into type, technology, mounting type, and end-user. By type, the market is segmented into main distribution boards, sub-main distribution boards, and final distribution boards. By technology, the market is segmented into conventional boards and smart/IoT-enabled boards. By mounting type, the market is segmented into wall-mounted and floor/free-standing boards. By end-user, the market is segmented into utilities, industrial, commercial, and residential sectors. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Main Distribution Boards (MDB) |

| Sub-Main Distribution Boards (SMDB) |

| Final Distribution Boards (FDB) |

| Conventional Boards |

| Smart/IoT-enabled Boards |

| Wall-Mounted |

| Floor/Free-Standing |

| Utilities |

| Industrial |

| Commercial |

| Residential |

| By Type | Main Distribution Boards (MDB) |

| Sub-Main Distribution Boards (SMDB) | |

| Final Distribution Boards (FDB) | |

| By Technology | Conventional Boards |

| Smart/IoT-enabled Boards | |

| By Mounting Type | Wall-Mounted |

| Floor/Free-Standing | |

| By End-User | Utilities |

| Industrial | |

| Commercial | |

| Residential |

Key Questions Answered in the Report

What is the current size and growth outlook for distribution boards in Algeria?

The Algeria Distribution Boards Market size is expected to grow from USD 24.29 million in 2025 to USD 26.15 million in 2026 and is forecast to reach USD 36.52 million by 2031 at 6.91% CAGR over 2026-2031.

Which product type is leading demand in Algeria?

Main Distribution Boards led value demand with a 44.2% share in 2025, supported by utility and industrial installations.

Which category is growing the fastest through 2031?

Smart or IoT-enabled boards are the fastest-growing technology at 11.2% CAGR, while Final Distribution Boards are the fastest-growing type at 8.7% CAGR.

Why is commercial demand rising faster than many other end-users?

Commercial demand is forecast to grow at 9.0% CAGR because retail, mixed-use, telecom, and digital infrastructure projects require more complex and higher-value electrical distribution layouts.

Which part of Algeria generates the most demand today?

The northern corridor remains the main demand center because it combines housing delivery, commercial construction, and stronger contractor and distributor presence.

What is the biggest operational risk for suppliers?

Import dependence on critical switching components remains the main risk because delays in imported breakers, busbars, and related parts can slow project delivery even when demand is strong.

Page last updated on: