Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

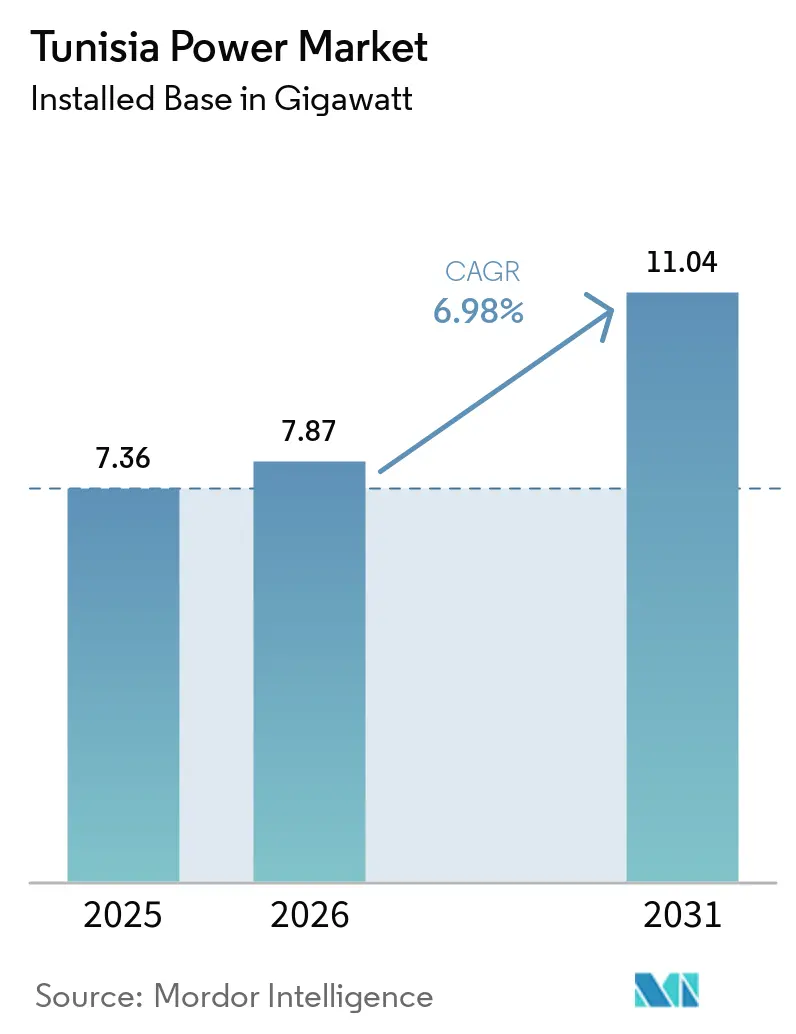

| Base Year Market Size (2025) | 7.36 gigawatt |

| Market Volume (2026) | 7.87 gigawatt |

| Market Volume (2031) | 11.04 gigawatt |

| Growth Rate (2026 - 2031) | 6.98% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tunisia Power Market Analysis by Mordor Intelligence

Tunisia Power Market size in 2026 is estimated at 7.87 gigawatt, growing from 2025 value of 7.36 gigawatt with 2031 projections showing 11.04 gigawatt, growing at 6.98% CAGR over 2026-2031.

Robust auction pipelines, multilateral funding, and the forthcoming 600 MW ELMED interconnector draw international developers into the Tunisia power market, even as a high sovereign-risk premium raises financing costs for independent power producers. A 1.7 GW solar-and-wind tender series, grid-modernization loans from the African Development Bank (AfDB) and KfW, and net-metering reforms are accelerating renewable penetration. Meanwhile, STEG’s aging gas fleet and euro-denominated debt exposure temper private investment appetite. Corporate power purchase agreements in phosphate and data-center clusters are emerging, yet open-access rules remain absent, perpetuating STEG’s dominance in the Tunisia power market.

Key Report Takeaways

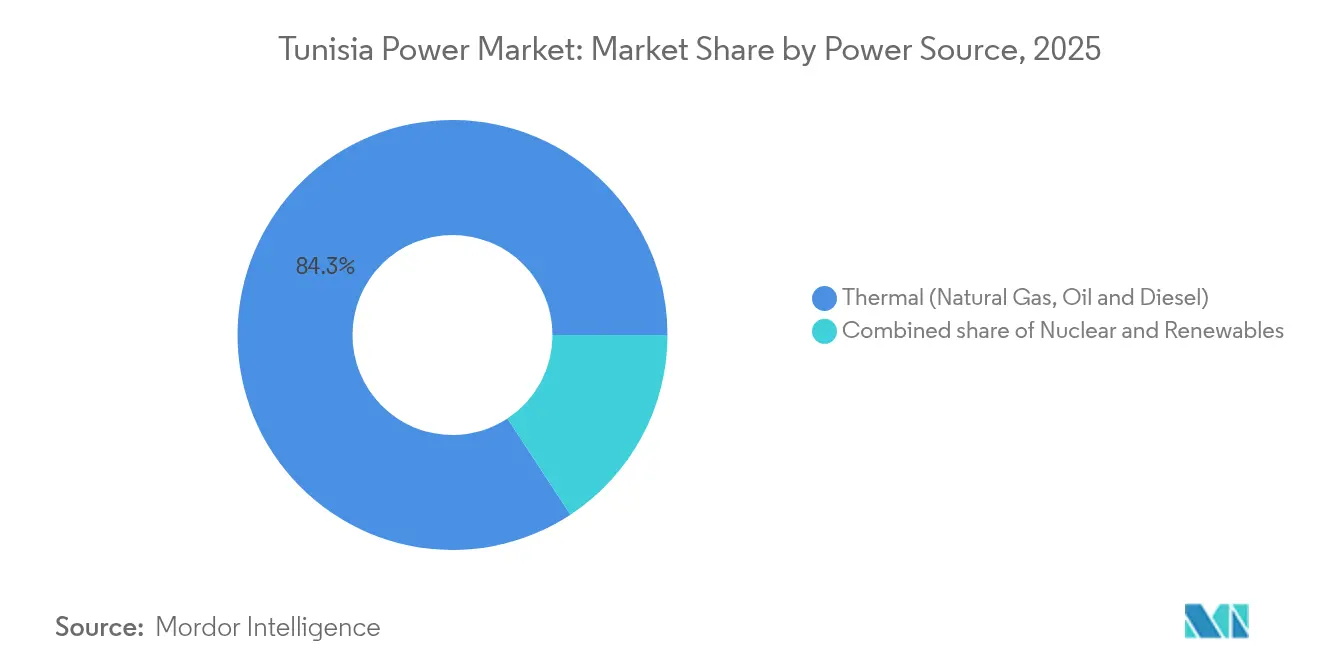

- By power source, thermal generation held 84.25% of the Tunisia power market share in 2025; renewables are projected to advance at a 24.6% CAGR through 2031.

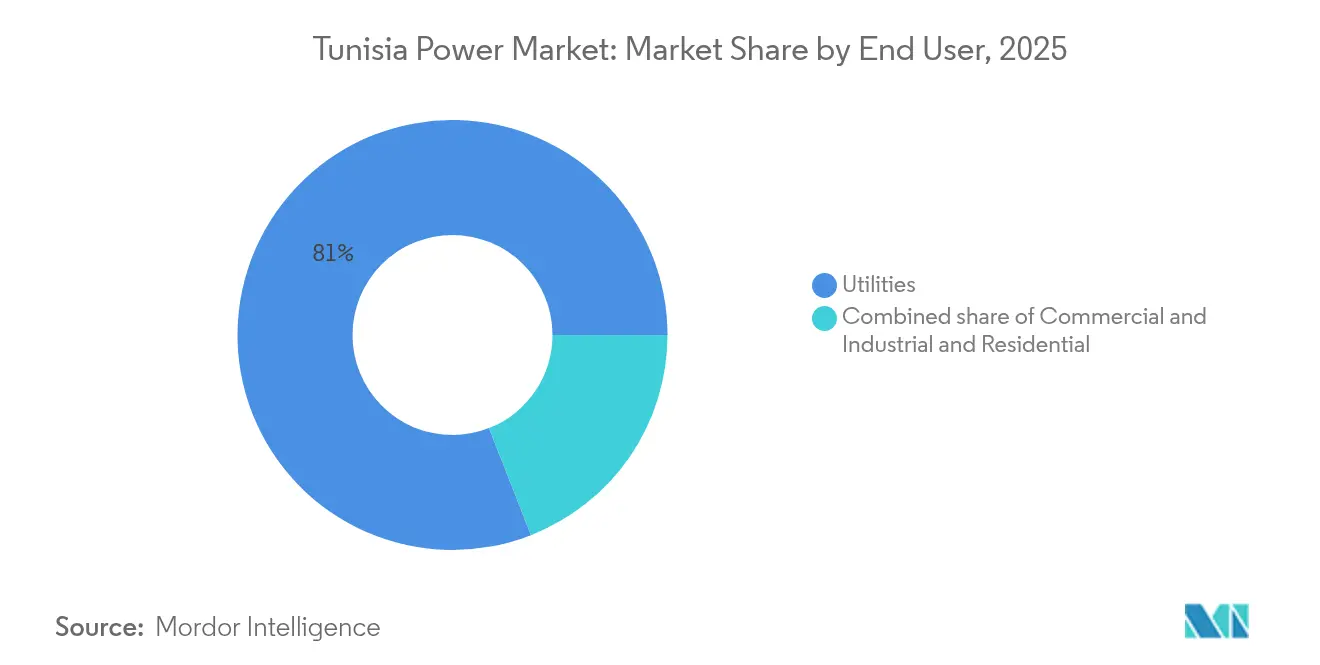

- By end user, utilities captured an 80.95% share of the Tunisia power market size in 2025, while the same segment is forecast to expand at a 9.25% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Tunisia Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gas-fired build-out under Plan Solaire Tunisien 2030 | +2.1% | Coastal hubs in Tunis, Sfax, Sousse | Medium term (2-4 years) |

| Renewable-energy auctions (1 GW 2024-2026 pipeline) | +1.8% | Kairouan, Sidi Bouzid, Tataouine | Short term (≤ 2 years) |

| Grid modernization loans from AfDB & KfW | +0.9% | National backbone, pilot zones in Sfax, Sousse, Le Kram | Long term (≥ 4 years) |

| Regional interconnector with Italy (ELMED) | +1.2% | National, with EU trade implications | Long term (≥ 4 years) |

| Corporate PPAs from phosphate & data-center sector | +0.7% | Gafsa, coastal data-center corridors | Medium term (2-4 years) |

| Decentralized rooftop-solar boom | +0.8% | Tunis metro, Sfax, Sousse | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Gas-Fired Build-Out Under Plan Solaire Tunisien 2030

Tunisia aims for 30% renewable penetration by 2030, yet dispatchable gas remains essential for balancing intermittent output. STEG is refurbishing combined-cycle plants and adding quick-ramping gas turbines that operate 15-20 percentage points more efficiently than legacy units, lowering heat rates and curbing curtailment.[1]African Development Bank, “AfDB Approves Loan for Kairouan Solar Plant,” afdb.org The AfDB’s 2024 co-financing of the 100 MW Kairouan solar plant signals donor support for hybrid portfolios pairing renewables with flexible thermal assets. The World Bank’s 2025 TEREG program channels USD 430 million into 2.8 GW of solar-and-wind capacity while conditioning disbursements on storage and grid-flexibility investments, underscoring the interdependence between renewables and gas back-up.[2]World Bank, “World Bank Supports Tunisia’s Energy Transition with $430 Million Program,” worldbank.org Algeria’s gas-supply uncertainty amplifies the need for efficient turbines, yet continued reliance on imports heightens fuel-price exposure. Without these gas upgrades, renewable penetration beyond 35% would jeopardize grid stability in the Tunisia power market.

Renewable-Energy Auctions (1 GW 2024-2026 Pipeline)

A 1.7 GW tender series placed Tunisia among North Africa’s most competitive auction venues. In December 2024, Qair, Scatec, and Voltalia secured 498 MW at tariffs near USD 0.031 /kWh, reflecting global PV module deflation and intense bidding. A 500 MW solar round advanced in March 2025, selecting four firms at comparable prices. Scatec’s 120 MW Sidi Bouzid II project reached a 25-year PPA in 2025, with EUR 87 million capex financed on a 50-50 basis with Toyota Tsusho’s Aeolus unit.[3]Scatec, “Scatec Signs PPA for 120 MW Solar Project,” scatec.com Local-content thresholds of 30-40% postpone financial close by up to nine months, pushing developers to source mounting structures and inverters domestically. Despite compressed margins, auction cadence must accelerate because currently contracted volumes cover only 14% of the 2030 renewable target in the Tunisia power market.

Grid Modernization Loans from AfDB & KfW

STEG’s grid-modernization agenda hinges on a EUR 113 million Siemens-led smart-grid pilot across Sfax, Sousse, and Le Kram, scheduled to finish in 2025. AfDB extended EUR 120 million for nationwide meter roll-outs, targeting 5 million electricity and 1 million gas meters by 2029. The European Investment Bank added EUR 65.8 million to bolster substation capacity and reduce technical losses exceeding 15% in some feeders. Real-time data will enable time-of-use tariffs that align solar-heavy midday generation with flexible demand. Yet tender approvals remain slow, and replicating pilot success across the Tunisia power market requires strong project-management discipline.

Regional Interconnector with Italy (ELMED)

The 600 MW ELMED high-voltage DC link, budgeted at EUR 921 million, connects Tunisia to Italy in 2028, co-financed by the European Investment Bank, KfW, and World Bank grants. It will export surplus solar into the EU and import evening-peak power, unlocking carbon-credit eligibility. A EUR 12 million EIB technical-assistance grant in 2025 underlines execution risk and STEG's euro-denominated debt exposure. Critics warn of "green colonialism," but the cable can shave Tunisia's Algerian-gas dependence and create a new revenue stream for Tunisia's power market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising sovereign-risk premium on IPP finance | -1.4% | National, affects all tenders | Short term (≤ 2 years) |

| Aged thermal fleet > 25 years, efficiency drag | -0.9% | Coastal thermal clusters | Medium term (2-4 years) |

| Grid curtailment risk beyond 35% renewables | -0.6% | High-solar interior regions | Long term (≥ 4 years) |

| Local-content rules delaying solar tenders | -0.5% | Nationwide procurement | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Sovereign-Risk Premium on IPP Finance

Credit ratings of B- (Fitch) and CCC+ (S&P) impose 300-400 bp financing spreads over investment-grade markets, shrinking developer returns. IMF subsidy-reform stalemates stall sovereign backstops, and STEG’s arrears exceed USD 1 billion annually, elevating offtaker risk. EBRD’s EUR 300 million loan delivered emergency liquidity, but the utility’s deficit persists. Consequently, developers demand sovereign guarantees or partial-risk insurance, delaying financial close and slowing renewable build-out in the Tunisia power market.

Aged Thermal Fleet > 25 Years—Efficiency Drag

Many gas turbines date to the 1990s, consuming 10-15% more fuel per MWh than modern combined-cycle units. Deferred maintenance has cut capacity factors to 50-60%, constraining ramping flexibility when solar output plunges at dusk. Fleet renewal needs USD 1-2 billion, but no financing vehicle exists. The efficiency gap worsens carbon intensity, jeopardizing potential EU carbon-credit revenue once ELMED goes live. World Bank disbursements now require parallel thermal upgrades, linking legacy-plant health to the long-term CAGR of the Tunisia power market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Source: Renewables Gain Momentum Within a Thermal-Led Mix

Thermal units commanded 84.25% of the Tunisia power market share in 2025, reaffirming the centrality of gas-fired output in meeting peak demand. Renewables, anchored by solar PV and coastal wind farms, are advancing at a 24.6% CAGR, propelling the Tunisia power market size for clean electricity to an anticipated 4.85 GW by 2031. Steady module price declines and concessionary World Bank funding underpin tariff bids below USD 0.032 /kWh. Smart-grid pilots will enable flexible loads to align with solar peaks, while the 400-600 MW pumped-hydro project offers swing capacity to prevent curtailment. Yet a euro-denominated debt burden from ELMED and gas-import volatility sustains thermal lock-in.

In parallel, ACWA Power’s green-hydrogen roadmap envisions 12 GW of renewable capacity feeding electrolyzers, which could triple domestic renewable build-rates if wheeling reforms emerge. Until then, STEG continues life-extension overhauls of Rades and Sousse turbines to hedge against renewable intermittency. Hydro and biomass remain peripheral, and no nuclear program is planned. Overall, rising renewable output narrows the fossil share but leaves gas-fired flexibility indispensable to the Tunisia power market.

By End User: Utilities Retain Dominance Amid Nascent Corporate Demand

Utilities held 80.95% of the Tunisia power market size in 2025 and are trending at a 9.25% CAGR through 2031 as STEG signs 20-25-year PPAs with auction winners. Commercial and industrial users, led by phosphates, cement, and textiles, seek direct PPAs but remain captive to bundled tariffs. The absence of open-access regulations limits corporate renewable procurement, though data-center investors lobby for change. Residential demand grows slowly but now hosts a 300 MW rooftop fleet that trims daytime grid load.

Looking forward, corporate offtake could accelerate once grid-code amendments permit wheeling, unlocking latent demand near Gafsa’s phosphate belt and coastal data hubs. Until then, the Tunisia power market depends on STEG’s balance-sheet resilience and multilateral backstops to scale renewable investment while sustaining universal service obligations.

Geography Analysis

Electricity use clusters along the Tunis-Sousse-Sfax coastal corridor, which consumes roughly 70% of the national load. Tunis alone absorbs 40%, driven by public buildings and service-sector activity. Sfax and Sousse host textiles, agrifood, and cement works needing a reliable baseload supply. Interior governorates, Kairouan, Sidi Bouzid, and Tataouine, offer world-class solar irradiance above 2,000 kWh/m², attracting auctioned PV farms supported by AfDB and World Bank capital.

Transmission upgrades are vital because 220 kV circuits funneling inland generation to coastal loads face thermal constraints during summer peaks. The 600 MW ELMED link anchors a future West-Med ring enabling exports, while potential Libya and Algeria tie-ins remain politically contingent. Eni’s 200 kW Tataouine school-solar initiative illustrates donor outreach to underserved south-desert communities. Rural electrification gains, however, add modest volume relative to heavy industrial loads.

By 2030, grid reinforcement around Kairouan and Sidi Bouzid should unlock 1 GW of inland solar. Pumped-hydro at Oued El Melah near Tabarka leverages favorable topography for 600 MW of storage, balancing north-coast demand swings. Spatial mismatch between load and resource underscores the strategic value of multipoint interconnections in stabilizing the Tunisia power market.

Competitive Landscape

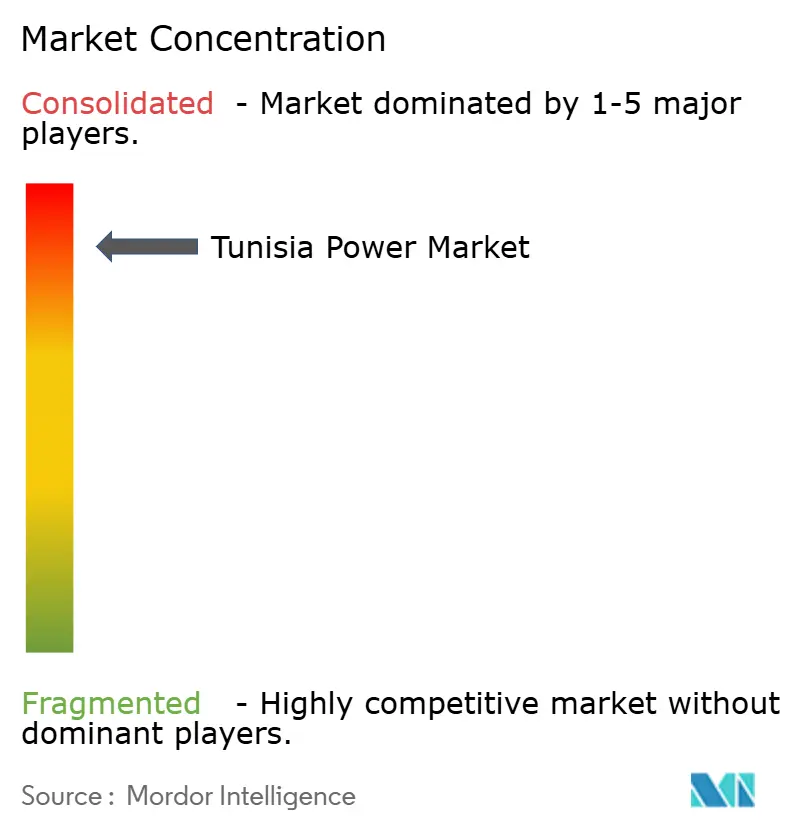

Tunisia Power Market is consolidated. STEG’s statutory monopoly over transmission and distribution shapes a moderately concentrated landscape. European IPPs, Scatec, Qair, Voltalia, and Enel Green Power, dominate solar auctions, while ACWA Power readies hydrogen megaprojects. Tariffs near USD 0.031 /kWh position the Tunisia power market as the continent’s second-cheapest solar venue after Egypt.

Equipment vendors compete on grid and generation packages: Siemens leads smart-grid pilots; GE and Ansaldo supply gas-turbine upgrades; Vestas and Siemens Gamesa target wind pipelines; ABB and Elsewedy pursue substation contracts. Local-content rules spur joint ventures with Tunisian fabricators, yet supply-chain immaturity prolongs delivery. Rising interest in co-located storage, battery, or pumped hydro, favors integrators offering turnkey flexibility.

Strategically, IPPs align with multilateral lenders to mitigate currency and offtaker risks. EBRD’s blended-finance structures underpin several 2025 solar closings, while the EIB’s ELMED grant enhances visibility for trans-Med trade flows. Domestic manufacturers eye inverter and mounting-structure niches as auction volumes scale, suggesting a gradual deepening of the Tunisia power market’s local ecosystem.

Tunisia Power Industry Leaders

Tunisian Company of Electricity & Gas (STEG)

Carthage Power Company

Ansaldo Energia (O&M for Rades C)

Nur Energie (TuNur Solar+)

ACWA Power

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Through the Tunisia Energy Reliability, Efficiency, and Governance Improvement Program (TEREG), the World Bank has partnered with the Government of Tunisia to modernize the nation's energy sector. Over the next five years, this initiative, backed by a financing agreement of US$430 million, which includes US$30 million in concessional financing from the Climate Investment Funds, seeks to ensure Tunisia provides a sustainable, reliable, and affordable electricity supply.

- March 2025: Qair, a French independent power producer (IPP), secured power purchase agreements (PPAs) with Tunisia's state utility, Société Tunisienne de l’Electricité et du Gaz (STEG), for a total of 298MW of solar PV. These agreements cover the 100MW Gafsa and 198MW El Khobna solar PV power plants, both situated in the heart of Tunisia.

- December 2024: Empower New Energy (ENE) has made its inaugural solar investment in Tunis, partnering with the Mall of Sousse. The two organizations underscored their dedication to sustainable innovation by signing a Power Support Agreement (PSA), setting the stage for an ambitious solar energy project. Central to this endeavor is a cutting-edge 948 kWp solar roof system.

- May 2024: ACWA Power, a Saudi-listed leader in energy transition and a pioneer in green hydrogen, inked a memorandum of understanding (MoU) with the Tunisian Government. The agreement, represented by the Ministry of Industry, Mines and Energy, aims to explore a project with the potential to produce up to 600,000 tonnes of green hydrogen annually, in three distinct phases.

Tunisia Power Market Report Scope

The power industry, often referred to as the electricity sector, encompasses the entire value chain of electricity - from generation and transmission to distribution and sale. This sector integrates organizations, technologies, and infrastructure, ensuring that primary energy sources are efficiently and safely transformed into electrical energy for end users.

The Tunisia power market is segmented by power sources, end-users, and T&D voltage level (Qualitative analysis only). By power source, the market is segmented into thermal, nuclear, and renewable. By end-user, it is categorized into utilities, commercial and industrial, and residential. Furthermore, the report delves into transmission and distribution (T&D) voltage levels, offering qualitative insights on high-voltage transmission, sub-transmission, medium-voltage distribution, and low-voltage distribution.

By Power Source

| Thermal (Coal, Natural Gas, Oil and Diesel) |

| Nuclear |

| Renewables (Solar, Wind, Hydro, Geothermal, Biomass & Waste, Tidal) |

By End User

| Utilities |

| Commercial and Industrial |

| Residential |

By T&D Voltage Level (Qualitative Analysis only)

| High-Voltage Transmission (Above 230 kV) |

| Sub-Transmission (69 to 161 kV) |

| Medium-Voltage Distribution (13.2 to 34.5 kV) |

| Low-Voltage Distribution (Up to 1 kV) |

| By Power Source | Thermal (Coal, Natural Gas, Oil and Diesel) |

| Nuclear | |

| Renewables (Solar, Wind, Hydro, Geothermal, Biomass & Waste, Tidal) | |

| By End User | Utilities |

| Commercial and Industrial | |

| Residential | |

| By T&D Voltage Level (Qualitative Analysis only) | High-Voltage Transmission (Above 230 kV) |

| Sub-Transmission (69 to 161 kV) | |

| Medium-Voltage Distribution (13.2 to 34.5 kV) | |

| Low-Voltage Distribution (Up to 1 kV) |

Key Questions Answered in the Report

How fast is overall installed capacity in Tunisia expected to grow by 2031?

National capacity is projected to rise from 7.87 GW in 2026 to 11.04 GW by 2031, implying a 6.98% CAGR over 2026-2031.

When will the 600 MW ELMED interconnector with Italy come online?

Current schedules put commissioning in 2028, after construction backed by EIB, KfW, and World Bank funding.

What tariff levels have recent solar auctions achieved?

December 2024 and March 2025 rounds cleared near USD 0.031 /kWh, among the lowest prices recorded in North Africa.

Are corporate power-purchase agreements allowed in Tunisia yet?

Direct corporate PPAs remain limited because STEG holds exclusive grid access, though phosphate and data-center operators are lobbying for open-access rules.

How much rooftop solar has been installed under the net-metering reform?

By end-2024, about 300 MW had been deployed across 90,000 homes, supported by a TND 370 million (USD 121 million) rebate program.

What is the focus of STEG’s grid-modernization plan?

A Siemens-led pilot is installing smart meters and automation in Sfax, Sousse, and Le Kram to cut technical losses and enable time-of-use tariffs, with national roll-out targeted by 2029.

Page last updated on: