Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

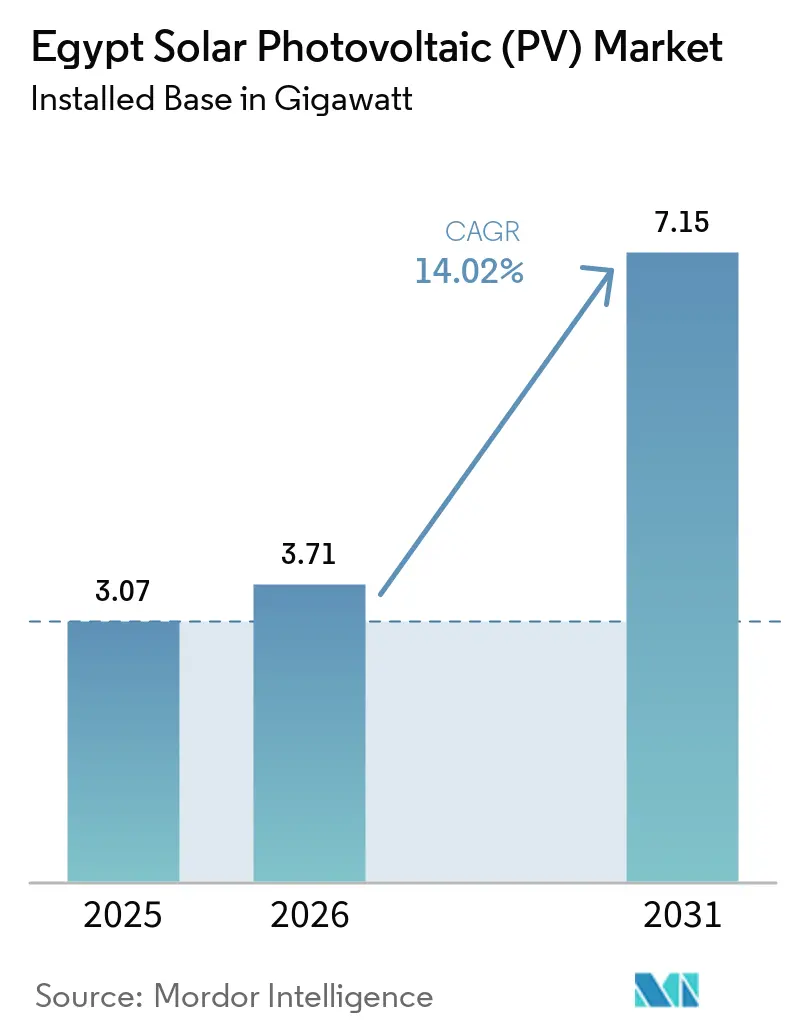

| Base Year Market Size (2025) | 3.07 gigawatt |

| Market Volume (2026) | 3.71 gigawatt |

| Market Volume (2031) | 7.15 gigawatt |

| Growth Rate (2026 - 2031) | 14.02% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Solar Photovoltaic (PV) Market Analysis by Mordor Intelligence

The Egypt Solar Photovoltaic Market size in terms of installed base was valued at 3.07 gigawatt in 2025 and is estimated to grow from 3.71 gigawatt in 2026 to reach 7.15 gigawatt by 2031, at a CAGR of 14.02% during the forecast period (2026-2031).

Egypt’s pivot toward renewable generation is accelerated by falling domestic gas output, a five-year tariff freeze for industrial users, and a binding 42% renewables mandate that is front-loading utility-scale solar and hybrid tenders. Sovereign-backed, United States-dollar PPAs continue to crowd in concessional finance, yet local-currency contracts are emerging where developers accept exchange-rate risk in return for faster approvals. Battery storage is gaining parity with generation assets as dispatchable hybrids now secure tariff premiums and transmission access ahead of intermittent projects. Intensifying competition from onshore wind in the Gulf of Suez is pressing solar developers to differentiate through storage integration, local manufacturing, and agrivoltaics that sidestep grid bottlenecks.

Key Report Takeaways

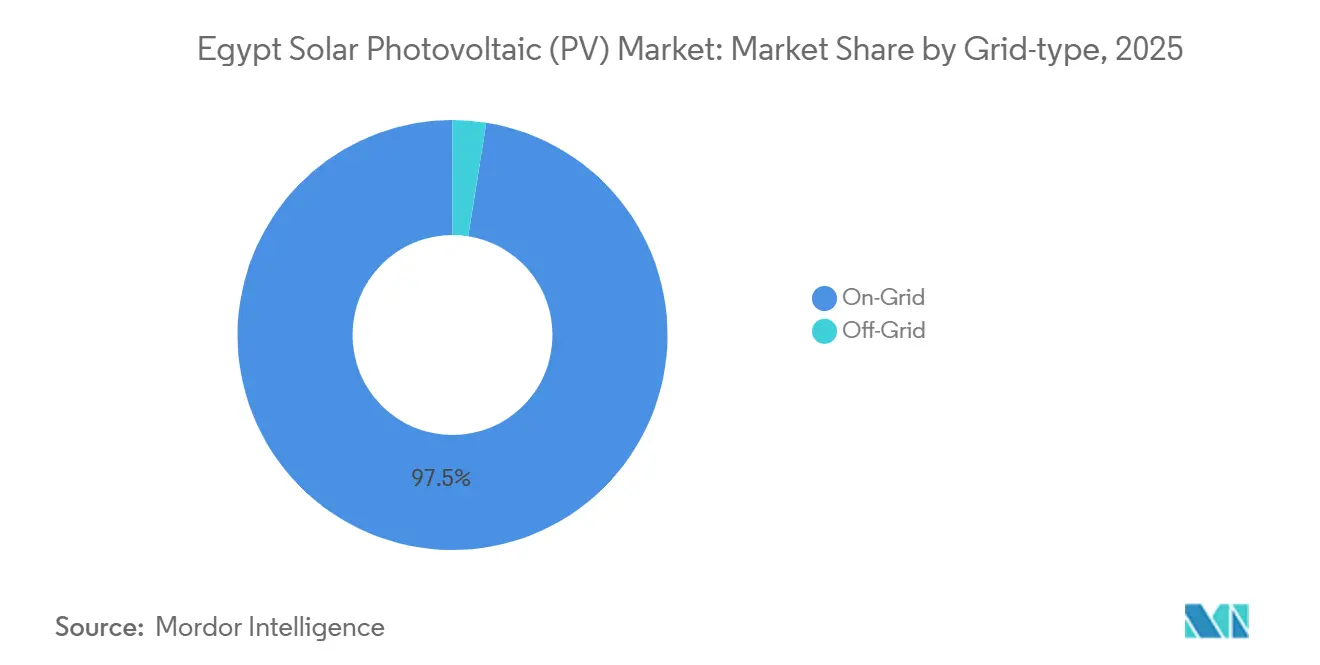

- By grid type, on-grid installations commanded 97.5% of capacity in 2025, while off-grid systems are projected to expand at 22.4% CAGR through 2031.

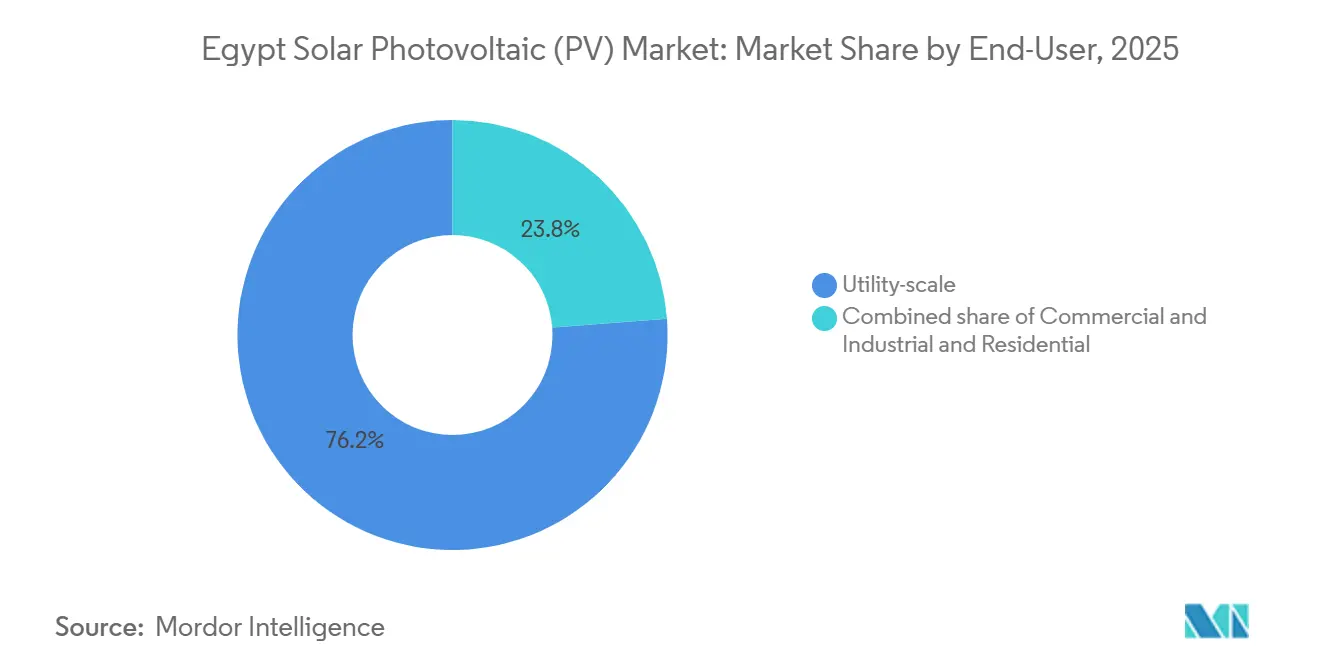

- By end-user, utility-scale plants held 76.2% of the Egyptian solar photovoltaic (PV) market share in 2025, whereas the commercial and industrial segment is expected to grow at 23.8% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Egypt Solar Photovoltaic (PV) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining PV module prices | +2.1% | National, spillover to MENA via exports | Medium term (2-4 years) |

| Government-backed 42%-by-2035 renewables target | +3.5% | Aswan, Qena, Minya, Benban clusters | Long term (≥4 years) |

| Surge in utility-scale projects | +2.8% | Upper Egypt with grid effects in Cairo and Alexandria | Medium term (2-4 years) |

| Growing foreign direct investment & green finance | +2.3% | Suez Canal Economic Zone, Nile Delta | Medium term (2-4 years) |

| Emergence of local PV manufacturing capacity | +1.9% | Ain Sokhna, Suez Canal Economic Zone | Long term (≥4 years) |

| Agri-PV pilots in Nile Delta | +1.2% | Nile Delta, Western Desert oases | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Declining PV Module Prices

Solar modules fell to record lows as Chinese polysilicon oversupply and bifacial efficiencies converged, making utility-scale solar Egypt’s cheapest daytime source. Elite Solar’s 5 GW complex in Ain Sokhna started ramp-up in Q1 2026 with 90% local content, positioning the country to export competitively across Africa.[1]Egypt Oil & Gas, “Elite Solar Commissions 5 GW Integrated Solar Manufacturing Complex in Egypt,” egyptoil-gas.com Atom Solar’s parallel USD 220 million facility underpins a domestic supply of 8 GW modules by 2027, insulating developers from currency swings.[2]PV Magazine, “Egypt Inaugurates 5 GW Solar Manufacturing Complex,” pv-magazine.com Duty exemptions under Decree No. 203/2014 widen landed-cost gaps that Chinese suppliers capture through joint ventures rather than direct shipment.[3]IEA, “Egypt Renewable Energy Law (Decree No 203/2014) – Policies,” iea.org Developers increasingly bundle domestic modules inside turnkey EPC packages to satisfy the New and Renewable Energy Authority’s 60% local-content rule, hedging against import volatility. This trend locks in module pricing before any global rebound and underwrites aggressive bid tariffs.

Government-Backed 42%-by-2035 Renewables Target

The Integrated Sustainable Energy Strategy codifies a 42% renewable share by 2030, effectively reserving 10 GW for new solar and wind capacity. Ministerial statements in 2026 confirm that 3 GW solar and 600 MW storage will enter service before the summer peak, tightening space for fossil additions.[4]TaiyangNews, “Egypt To Bring Online 3 GW Solar Energy in 2026,” taiyangnews.info Compliance is tracked by quarterly disclosure under Circular No. 3-2023, giving investors granular visibility into governorate-level saturation. Planned retirement of 5 GW gas generation by 2030 reinforces demand for dispatchable hybrids that serve evening peaks. Multilateral lenders align concessional tranches with the NWFE platform, blending grants with private capital to maintain debt sustainability.

Surge in Utility-Scale Projects

Benban’s 1.8 GW base and Kom Ombo’s 500 MW set precedents for phased build-own-operate models financed at 80% leverage. AMEA Power’s Abydos 2 (1 GW solar plus 600 MWh storage) entered operation in June 2026, marking Egypt’s first large-scale solar-plus-storage asset. Scatec’s Obelisk hybrid secured USD 479.1 million non-recourse debt at close in June 2025, demonstrating the bankability of multi-hour storage. The Upper Egypt pipeline now strains the 500 kV Aswan-Qena-Sohag corridor, prompting USD 3.2 billion in transmission upgrades by 2030. Developers fund substation expansions upfront, embedding grid costs into PPA bids.

Growing Foreign Direct Investment & Green-Finance Inflows

Egypt attracted USD 15.6 billion in renewable finance between 2020 and May 2025, of which USD 4 billion supports solar under NWFE. Scatec’s 1.95 GW solar-plus-3.9 GWh storage PPA signed in January 2026 carries no upfront subsidy, shifting performance risk entirely to the developer. British International Investment coupled USD 300 million debt with a USD 15 million grant to reduce battery costs, signaling a pivot from subsidizing generation to de-risking storage. Belt and Road channels see LONGi, TBEA, and Sungrow embed manufacturing lines that mitigate currency risk and deepen local supply chains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising competitiveness of on-shore wind in Gulf of Suez | -1.4% | Gulf of Suez (Ras Ghareb, Gabal el-Zeit, Ras Shukeir), with grid-balancing effects in Cairo and Alexandria | Medium term (2-4 years) |

| Currency-driven import cost volatility for modules & inverters | -1.8% | National, with acute impact on projects lacking US dollar-denominated PPAs or local-content mandates | Short term (≤ 2 years) |

| Limited transmission corridor availability in Upper Egypt | -1.3% | Upper Egypt (Aswan, Qena, Sohag), affecting Benban and Kom Ombo solar clusters with spillover to grid-connection queues nationally | Medium term (2-4 years) |

| High water demand for panel cleaning amid chronic scarcity | -0.8% | Desert installations in Aswan, Qena, Western Desert oases, and Benban Solar Park zones where water access is limited | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Competitiveness of On-Shore Wind in Gulf of Suez

Wind tariffs between USD 0.0237 and USD 0.0268 per kWh now undercut many solar bids along the Gulf, driven by ACWA Power’s 1.1 GW project that closed financing in 2025. Developers pivot by co-locating wind and solar to maximize transmission use, as seen in Voltalia and Taqa Arabia’s 3 GW Zafarana hybrid slated for 2028. EETC prioritizes wind evacuations owing to higher evening output, delaying solar interconnections in Benban and Kom Ombo. Access to the Egypt-Saudi 3 GW interconnector further boosts wind export revenues, tilting capital allocation toward the Gulf corridor.

Currency-Driven Import Cost Volatility for Modules & Inverters

The Egyptian pound lost 38% of its value in 2024, lifting module costs from EGP 15.4 per W to EGP 21.3 per W. Projects with USD PPAs, such as Scatec’s 1.95 GW deal, remain insulated, while local-currency contracts face margin erosion. Developers hedge by sourcing Egyptian-made modules that price in pounds, trimming exposure by up to 70% for projects clearing the 60% domestic-content threshold. Net-metered C&I plants endure partial currency risk because 85% of payments float at spot rates, a structure that deters foreign capital.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grid Type: Off-Grid Gains Traction in Irrigation

Off-grid systems are projected to advance at 22.4% CAGR through 2031, nearly twice the expansion of on-grid deployments. On-grid still held 97.5% of capacity in 2025, reflecting sovereign-backed PPAs and economies of scale. Yet off-grid avoids EETC integration fees and the 1,000 MW cap on distributed generation, creating a regulatory arbitrage. The Egypt solar photovoltaic (PV) market size for off-grid applications could reach 200 MW by 2028 once 4,000 irrigation wells are solarized, reflecting 2.8% of the total installed base. Chinese suppliers are moving turnkey pump-plus-module kits that guarantee 65% operating-cost cuts and three-year paybacks, unlocking microfinance channels. On-grid developers bear 6- to 12-month interconnection queues and must co-fund substations, challenges that push some investors toward isolated systems targeting agrarian loads.

By End-User: C&I Segment Accelerates on Tariff-Freeze Arbitrage

Utility-scale plants captured 76.2% Egypt solar photovoltaic (PV) market share in 2025, anchored by Benban, Abydos, and Obelisk clusters. However, the commercial and industrial segment is forecast to grow at 23.8% CAGR, exploiting the current tariff freeze that lets factories lock in savings before 2026 adjustments. Egypt Aluminum’s 1 GW captive solar PPA with Scatec exemplifies the shift toward direct industrial offtake. C&I projects face 10%-12% borrowing costs, yet they bypass grid bottlenecks and avoid integration charges. Residential uptake remains below 2% of capacity due to low buyback rates and the 300 MW national cap. Post-freeze tariff escalations are expected to restore 15%-20% annual hikes, reinforcing the appeal of behind-the-meter arrays.

Geography Analysis

Upper Egypt’s Aswan and Qena hosted over 60% of utility-scale capacity in 2025, drawn by 2,400 kWh/m² irradiation and land availability. Congestion at Benban and Kom Ombo, however, delays new projects up to one year until the 500 kV Aswan-Qena-Sohag line is completed in 2028. This bottleneck steers capital toward the Gulf of Suez, where existing lines can evacuate wind-heavy hybrids and export surpluses via the Egypt-Saudi link. The Nile Delta emerges as a distributed-generation pocket where agrivoltaics bypasses grid hurdles and serves irrigation wells that consume 2 TWh yearly. Western Desert oases host high-yield solar-diesel hybrids for mining outfits and farms, leveraging licensing exemptions below 500 kW.

The Suez Canal Economic Zone is positioning itself as a manufacturing hub rather than a generation site. Elite Solar, Sungrow, and soon GCL will tap AfCFTA tariff-free corridors to export modules and batteries into Sub-Saharan Africa. Cairo and Alexandria, Egypt’s twin demand centers, contribute less than 5% of installed capacity due to land scarcity and a near-saturated 1.5% net-metering cap per distributor. Nonetheless, rooftop arrays on malls, factories, and logistics centers added 150 MW since 2024, exploiting stable industrial tariffs.

The Egypt solar photovoltaic (PV) market size in Upper Egypt is forecast to double by 2031 once new transmission eases current constraints. Meanwhile, off-grid deployments in the Delta and Western Desert are projected to represent 4%-5% of national capacity, a trend underpinned by Ministry of Agriculture incentives and accessible microfinance.

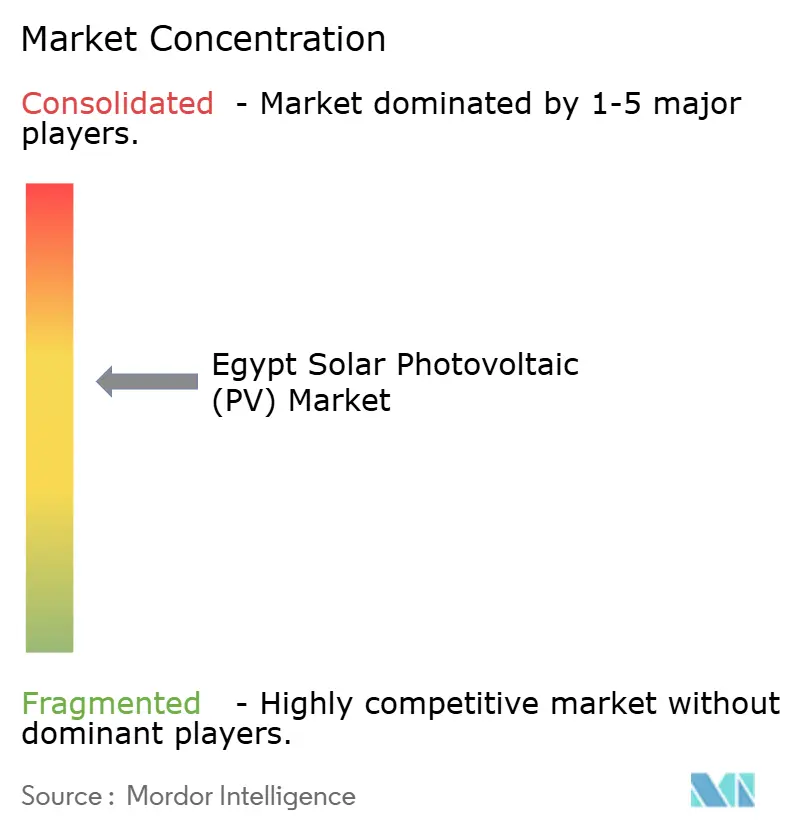

Competitive Landscape

The top five developers control roughly 55% of the utility pipeline, signaling moderate concentration. Scatec alone operates, builds, or finances 1.95 GW solar and 3.9 GWh storage, wielding turnkey EPC and O&M services that capture 70% of project value. AMEA Power, Infinity Power, ACWA Power, and Masdar round out the leading cohort, yet local integrators Elite Solar and Atom Solar are pressing module prices 12%-15% below imports. Chinese suppliers LONGi, Jinko, and Trina lock in multi-gigawatt agreements denominated in renminbi to hedge currency swings, squeezing EPC margins.

Hybrid solar-plus-storage configurations are the new differentiator; AMEA’s 300 MWh system at Kom Ombo demonstrates viable economics in Egypt’s heat. Compliance with IEC 62619 battery standards, mandated for systems above 100 kWh, filters out smaller integrators lacking certification, further consolidating market power around established brands like Trina Storage, Sungrow, and Huawei. Tracker adoption increases addressable share for U.S. and European OEMs; GameChange’s 1.25 GW deal is Africa’s largest to date. White-space persists in the C&I and agrivoltaic niches, which together remain under-penetrated despite regulatory incentives.

Egypt Solar Photovoltaic (PV) Industry Leaders

Egyptian Electricity Holding Company

KarmSolar

Scatec ASA

Infinity Power (Infinity + Masdar JV)

ACWA Power

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Egypt signed renewable‑energy agreements valued at about $18 billion, centered on large‑scale solar PV development to accelerate its clean‑energy transition. The program includes multi‑gigawatt solar projects in high‑irradiance desert regions, contributing significantly to Egypt’s PV expansion and supporting its 2030 renewable‑energy target of 42%.

- September 2025: KarmSolar expanded its Cyprus operations with a 7.6 MW solar project financed by EUR 5 million (approximately USD 5.4 million) from Eurobank, marking the company's first international deployment and demonstrating its capacity to replicate Egypt-proven business models in Mediterranean markets.

- March 2025: Scatec signed a 25-year power-purchase agreement with Egypt Aluminium for a 1.1 GW solar installation paired with 100 MW/200 MWh battery energy storage, representing a USD 650 million investment that will supply the aluminum smelter's baseload demand and reduce reliance on grid electricity.

- March 2025: EDF Renouvelables acquired a strategic equity stake in KarmSolar for USD 25 million, providing the Egyptian developer with balance-sheet support to scale its agrivoltaic and off-grid portfolio while transferring French technical expertise in hybrid solar-storage configurations.

Egypt Solar Photovoltaic (PV) Market Report Scope

Solar photovoltaic (PV) technology directly transforms sunlight into electricity through the photovoltaic effect. In this process, solar cells absorb photons, generating an electric current. These solar cells are assembled into panels, producing DC power. This power can either directly energize homes and equipment or be converted to AC power for integration into grid-tied systems.

The Egyptian Solar Photovoltaic Market is segmented by grid type and end-user. By grid type, the market is segmented into on-grid and off-grid. By end-user, the market is segmented into utility-scale, commercial and industrial (C&I), and residential. The report also covers the market size and forecasts for Egypt.

For each segment, the market sizing and forecasts have been done based on the installed capacity (GW).

By Grid Type

| On-Grid |

| Off-Grid |

By End-User

| Utility-scale |

| Commercial and Industrial (C&I) |

| Residential |

By Component (Qualitative Analysis)

| Solar Modules/Panels |

| Inverters (String, Central, Micro) |

| Mounting and Tracking Systems |

| Balance-of-System and Electricals |

| Energy Storage and Hybrid Integration |

| By Grid Type | On-Grid |

| Off-Grid | |

| By End-User | Utility-scale |

| Commercial and Industrial (C&I) | |

| Residential | |

| By Component (Qualitative Analysis) | Solar Modules/Panels |

| Inverters (String, Central, Micro) | |

| Mounting and Tracking Systems | |

| Balance-of-System and Electricals | |

| Energy Storage and Hybrid Integration |

Key Questions Answered in the Report

How much solar PV capacity does Egypt expect to have online by 2031?

Installed capacity is projected to reach 7.15 GW, up from 3.71 GW in 2026, reflecting a 14.02% CAGR over 2026-2031.

What policy is driving the rapid build-out of large-scale solar projects in Egypt?

The Integrated Sustainable Energy Strategy mandates a 42% renewable share in the national power mix by 2030, anchoring at least 10 GW of new solar and wind additions.

Why are commercial and industrial users accelerating their shift to on-site solar?

A five-year electricity-tariff freeze for high-voltage customers allows factories to lock in power costs, and net-metering reforms let them monetize excess generation, together supporting a 23.8% CAGR for the C&I segment through 2031.

How is local manufacturing helping developers cope with currency volatility?

New integrated plants totaling 5-8 GW of annual module capacity price equipment in Egyptian pounds, reducing exposure to exchange-rate swings that previously inflated imported modules by nearly 38% in 2024.

What role will battery storage play in Egypt's solar build-out this decade?

Multi-hour lithium-iron-phosphate systems have moved from optional extras to tender requirements, earning 15-20% tariff premiums and already surpassing 300 MWh of commissioned capacity.

Which regions offer near-term growth for off-grid solar solutions?

Agrivoltaic pilots in the Nile Delta and Western Desert oases target 40,000 irrigation wells, aiming to add about 200 MW of off-grid capacity by 2028 while cutting diesel use and saving water.

Page last updated on: