South Africa Distribution Boards Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

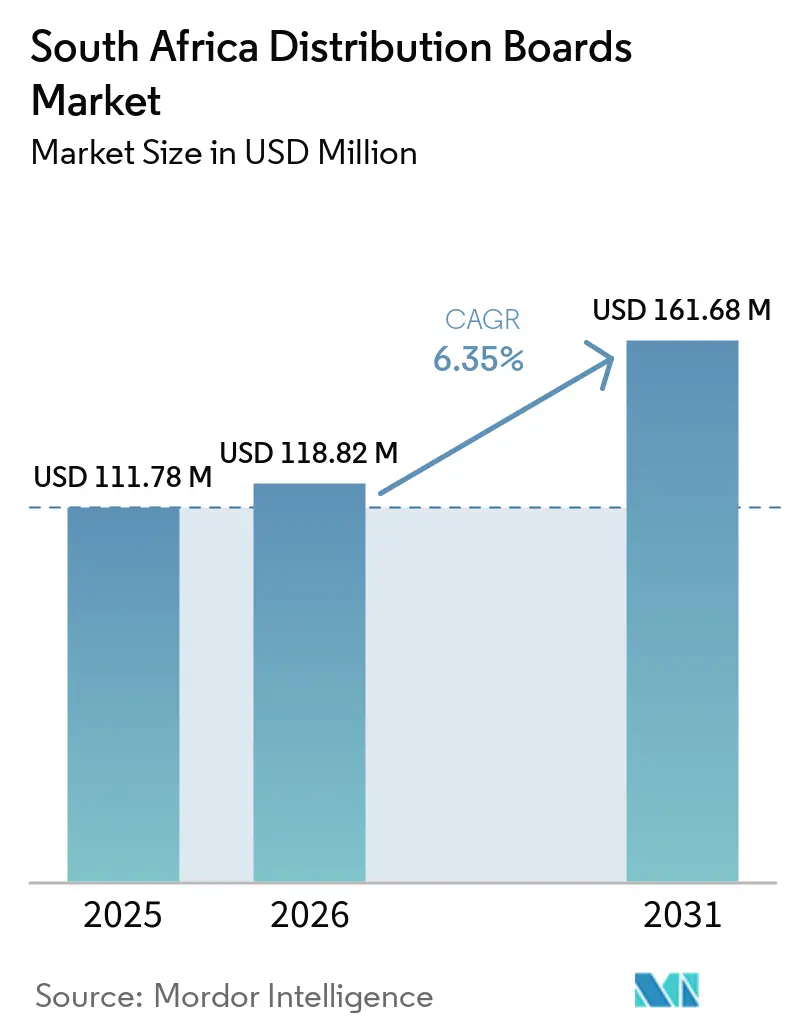

| Base Year Market Size (2025) | USD 111.78 Million |

| Market Size (2026) | USD 118.82 Million |

| Market Size (2031) | USD 161.68 Million |

| Growth Rate (2026 - 2031) | 6.35% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Distribution Boards Market Analysis by Mordor Intelligence

The South Africa Distribution Boards Market size is projected to expand from USD 111.78 million in 2025 and USD 118.82 million in 2026 to USD 161.68 million by 2031, registering a CAGR of 6.35% between 2026 to 2031. The South Africa distribution boards market is being supported by private embedded-generation rollout, data-center construction, and Eskom's phased grid modernization program. Purchasing behavior has moved away from short-term backup responses and toward permanent power-quality and distribution-architecture upgrades, because private generation is now part of the built environment rather than a temporary fix. Eskom reported that load-shedding fell from 329 days in FY2024 to 13 days in FY2025, yet electrical infrastructure spending kept rising as private and grid power sources were integrated into permanent systems.[1]Eskom, “Operational Performance and Load-Shedding Update,” Eskom, eskom.co.za The South Africa distribution boards market is also shaped by a split competitive structure, where multinational brands lead in high-specification projects while local assemblers compete through standards knowledge, local assembly, and procurement alignment. This keeps the South Africa distribution boards market exposed to opportunities in compliance-driven replacement, wheeling-linked board upgrades, and smarter monitoring architectures, even while metal costs and approval delays still affect project timing.

Key Report Takeaways

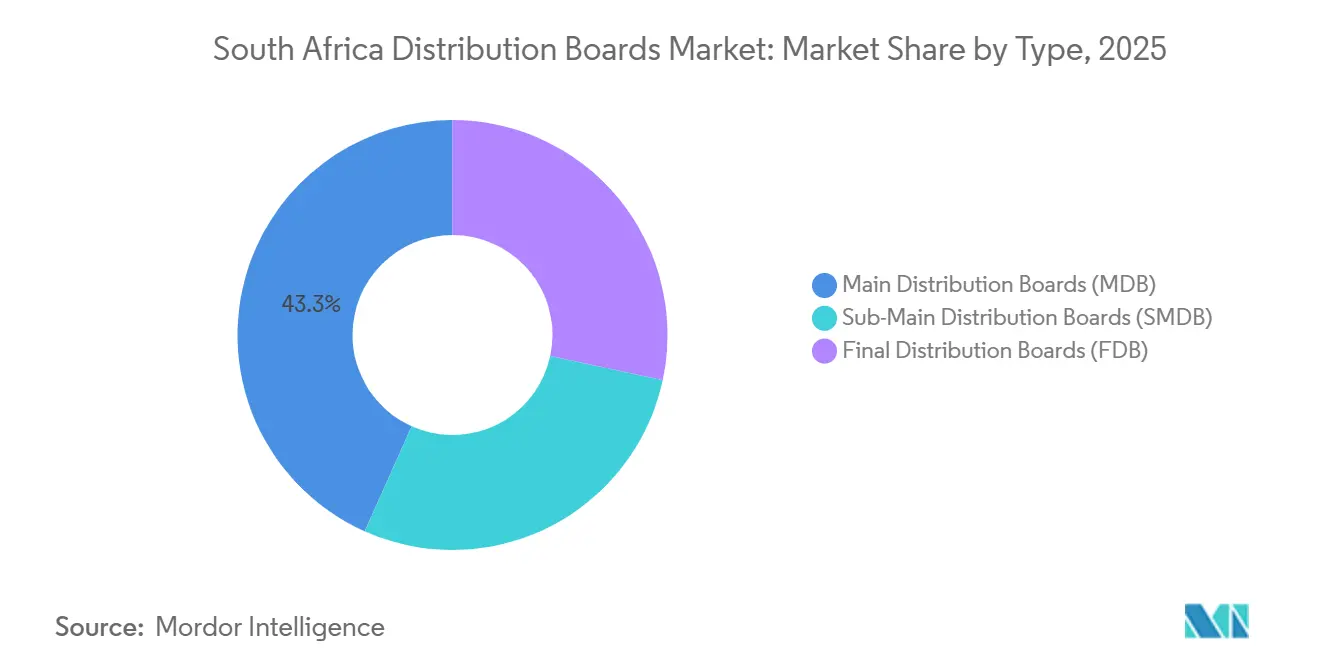

- By type, Main Distribution Boards led with 43.3% revenue share in 2025, while Final Distribution Boards are forecast to expand at an 8.7% CAGR through 2031.

- By technology, conventional boards accounted for 71.2% of revenue in 2025, while smart or Internet of Things (IoT)-enabled boards are expected to grow at 10.5% CAGR through 2031.

- By mounting type, wall-mounted boards held a 59.3% share in 2025, while floor or free-standing boards are projected to grow at an 8.1% CAGR through 2031.

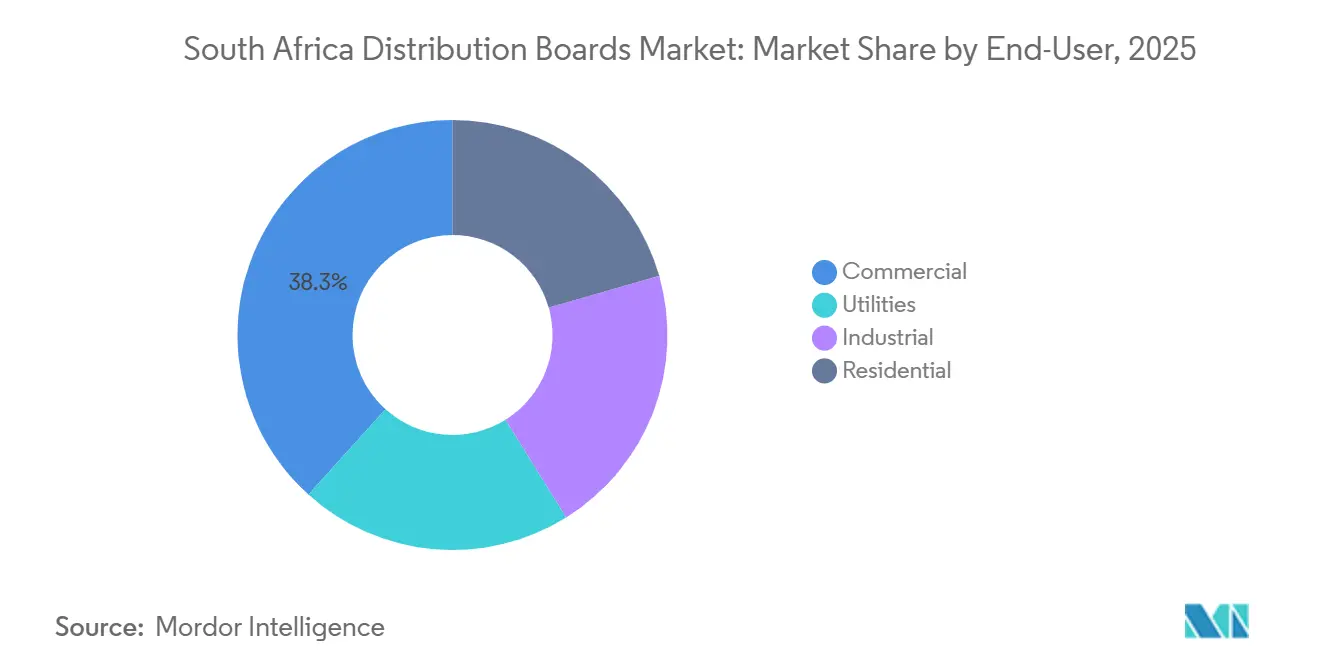

- By end user, commercial applications captured 38.3% of revenue in 2025, while residential demand is projected to advance at an 8.3% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Africa Distribution Boards Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commercial And Industrial Embedded Solar Plus Behind-The-Meter (BTM) Storage Rollout | +2.0% | Gauteng, Western Cape, KwaZulu-Natal | Short term (≤ 2 years) |

| Data-Center And AI-Ready Power Infrastructure Build-Out | +1.5% | Gauteng, Western Cape, KwaZulu-Natal | Medium term (2-4 years) |

| Utility And Municipal Grid Refurbishment Plus Localization Spend | +1.2% | National, priority in Gauteng, Mpumalanga, Free State | Medium term (2-4 years) |

| South African National Standard (SANS) 10142 And PV Compliance Refresh Cycle | +0.7% | National, concentrated in residential metros | Short term (≤ 2 years) |

| Low-Voltage (LV)-To-Medium-Voltage (MV) Migration For Solar And Wheeling Sites Above 1 Megavolt-Ampere (MVA) | +0.5% | Western Cape, Gauteng, KwaZulu-Natal | Medium term (2-4 years) |

| Modular Containerized Panel Adoption For Faster Project Delivery | +0.3% | Northern Cape, Mpumalanga | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Commercial and Industrial Embedded Solar Plus BTM Storage Rollout

The South Africa distribution boards market is benefiting from a steady rise in embedded solar and behind-the-meter storage across commercial and industrial sites. Each solar-plus-storage project creates a board upgrade event, because compliant installations need dedicated circuit protection, isolation devices, and DC-rated components that many legacy boards do not contain. SANS 10142-1 Edition 3.2, released in August 2024, formalized updated PV cable requirements and added provisions for hybrid energy systems, which turned many upgrades into compliance-led purchases rather than optional replacements.[2]South African Bureau of Standards, “SANS 10142-1 Edition 3.2,” SABS, sabs.co.za Sungrow and Herholdt's Group signed an agreement in March 2026 to deploy 1,155 MWh of commercial and industrial Battery Energy Storage System (BESS) across South Africa, showing the scale of new installations that require purpose-specified low-voltage board interfaces. Retrofitted sites often also need thermal derating checks when higher-rated protection is introduced into old enclosures, which adds follow-on demand for Sub-Main Distribution Board (SMDB) and Final Distribution Board (FDB) replacements alongside the main-board change.

Data-Center and AI-Ready Power Infrastructure Build-Out

The South Africa distribution boards market is seeing concentrated demand from data-center construction and power-hungry digital workloads. Data centers use tiered power distribution from medium-voltage rooms to row-level final boards, so one facility buildout generates multiple board layers rather than a single procurement package. These sites also require dual-bus redundancy, independent protection paths, and continuous monitoring, which raises the preference for smart distribution boards over conventional panels. IEC 61439-compliant assemblies are the baseline expectation in this environment, and suppliers that cannot meet this standard face a narrow participation window in premium projects. As a result, demand growth in this part of the South Africa distribution boards market is concentrated, specification-led, and favorable to firms with tested systems and monitoring capability.

Utility and Municipal Grid Refurbishment Plus Localization Spend

The South Africa distribution boards market is also supported by grid refurbishment and localization spending across utility and municipal networks. Eskom's 2025 capital plan allocated 41.2% of its FY2026 to FY2030 spending to grid-related investment, which supports secondary-side low-voltage board replacement in substations and municipal switchrooms. National Transmission Company of South Africa (NTCSA) also committed to 14,500 km of new transmission lines and 210 transformers through 2030, which expands the installed base that requires downstream low-voltage protection and distribution equipment. Localization rules within Eskom procurement continue to favor domestic assembly, which gives local panel builders some pricing protection even when imported components become more expensive. ACTOM's 2025 inverter-integrated transformer skid combined a locally built transformer, inverter, low-voltage combiner box, and medium-voltage ring main unit, showing how local suppliers are moving toward factory-tested integrated packages.

SANS 10142 and PV Compliance Refresh Cycle

The South Africa distribution boards market is being lifted by a rolling compliance refresh tied to SANS 10142 and rooftop solar adoption. Edition 3.2 introduced revised busbar requirements, updated PV cable specifications, DC fault-current calculations, and stronger protection rules for solar-fed circuits, all of which directly affect board selection and replacement. Electricians issuing Certificates of Compliance must verify that installed boards meet the updated clauses, which turns inspections, property transfers, and insurance checks into replacement triggers. Electrical Contractors' Association (SA) (ECA(SA)) opened public comment for Edition 3.3 on 30 January 2026, showing that code updates are continuing through the forecast period rather than ending with the 2024 revision. Residential final boards are especially exposed because combined grid-plus-generation fault levels often exceed what legacy units were designed to handle, which accelerates replacements in solar-adopting homes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-Connection Capacity Bottlenecks And Approval Delays | -1.8% | National, acute in Gauteng metro-fringe and Western Cape growth corridors | Short term (≤ 2 years) |

| Copper, Steel And Imported Component Cost Volatility | -1.5% | National, greater impact on import-dependent mid-market assemblers | Medium term (2-4 years) |

| Type-Tested Panel Modification Risk And Thermal Derating Burden | -0.9% | National | Medium term (2-4 years) |

| National Regulator for Compulsory Specifications (NRCS) LoA And Specialist Sign-Off Friction For Compliant Installs | -0.7% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Grid-Connection Capacity Bottlenecks and Approval Delays

The South Africa distribution boards market still faces timing risk from grid-connection bottlenecks and approval delays. The national wheeling framework was gazetted in March 2025, but project execution still depends on connection processes across Eskom and municipal networks, which can differ in pace and documentation standards. OECD's 2025 Economic Survey of South Africa identified grid expansion as a binding constraint on renewable deployment, which supports the view that electrical projects can be delayed even when board specifications are finalized. For panel suppliers, this means procurement orders can be placed and then pushed out for months when commissioning dates move, which ties up working capital and production slots. Municipal capital restrictions in areas under structured utility interventions can further defer discretionary MDB and SMDB upgrades, which slows near-term replacement volume.

Copper, Steel and Imported Component Cost Volatility

The South Africa distribution boards market has direct cost exposure to copper, steel, and imported protection components. The International Energy Agency (IEA) reported that copper smelter treatment and refining charges settled at USD 0 per tonne in January 2026, which reflected tight global supply conditions linked to electrification and renewable demand. Local assemblers that import breakers, residual current devices, and enclosure hardware also face exchange-rate risk, which can compress margins in the price-sensitive mid-market. This problem becomes harder when type-tested panel configurations require original-specification components, because cost-driven brand substitutions can invalidate certification and force retesting. As a result, material volatility does not just raise prices in the South Africa distribution boards market; it can also extend lead times and complicate compliance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Main Boards Anchor Revenue While FDB Outpaces Expansion

Main Distribution Boards held 43.3% of the South Africa distribution boards market share in 2025, making them the largest product category in the South Africa distribution boards market. This position came from large commercial builds, industrial refurbishments, and the need for a central protection layer in hybrid solar-plus-grid systems. Commercial facilities, which represented 38.3% of demand by end user in 2025, create a steady base for high-rated main boards because office parks, retail sites, and hospitality assets need coordination across multiple power sources. Sub-Main Distribution Boards sit in the middle of the hierarchy and are increasingly linked to sub-zone metering and control requirements in larger buildings.

Final Distribution Boards are projected to grow at 8.7% CAGR through 2031, making them the fastest-expanding type within the South Africa distribution boards market. NTCSA said South Africa's rooftop solar base reached 7,300 MW by September 2025, which widened the installed base that now needs compliant sub-circuit protection at the residential and light-commercial level. National Treasury's smart-metering program targets 250,000 sub-meters across 19 municipalities by 2027/28, and that creates a parallel upgrade cycle for boards that must accommodate metering sub-systems and revised wiring layouts. In the South Africa distribution boards industry, this combination keeps MDBs central to current revenue while pushing FDBs to the front of the replacement cycle.

By Technology: Conventional Boards Dominate, Smart Adoption Accelerates at the Top End

Conventional boards retained a 71.2% share in 2025, so they remained the largest technology group in the South Africa distribution boards market. Their lead reflects the size of the installed base and the cost sensitivity of residential and small commercial buyers. This replacement stream is steady because many buyers still prioritize reliable protection and compliance over advanced monitoring features. It also means legacy products continue to generate long-tail demand even as higher-spec projects move in a different direction.

Smart or IoT-enabled boards are forecast to expand at 10.5% CAGR through 2031, the fastest rate across all segmentation types and a growing part of the South Africa distribution boards market size. Data centers and advanced commercial facilities are the main catalysts because they require real-time energy monitoring, fault visibility, and remote isolation within strict reliability frameworks. Landis+Gyr introduced its E480 DIN-rail smart meter at Enlit Africa 2025 with Narrowband IoT (NB-IoT) connectivity and two-way communication, reflecting how circuit-level intelligence is moving deeper into low-voltage distribution architecture. In the South Africa distribution boards industry, higher electricity costs and closer energy management are also widening the commercial case for smart-board adoption beyond premium facilities.

By Mounting Type: Wall-Mounted Panels Lead, Floor-Standing Formats Gain in Tier-1 Projects

Wall-mounted boards held 59.3% of South Africa's distribution board market share in 2025, which kept them ahead of free-standing formats. Their lead comes from residential upgrades, light commercial installations, and office fit-outs, where space limits and unit volumes favor compact enclosures. SANS 10142-1 Edition 3.2 added revised neutral-earth bonding and busbar requirements, and these changes have sustained a steady replacement flow in older wall-mounted installations that no longer comply. This part of the South Africa distribution boards market remains volume-led, with compliance and refurbishment activity doing more work than new-build megaprojects.

Floor or free-standing boards are forecast to grow at an 8.1% CAGR through 2031, supported by industrial expansions, data-center electrical rooms, and large commercial substations. These projects often exceed practical wall-mounting limits, so buyers shift toward higher-rated floor-standing assemblies with stronger fault-level performance and easier cable management. ACTOM's locally manufactured motor control centers and low-voltage distribution switchboards, built to SANS 1973-1 and type-tested for high fault ratings, show how domestic suppliers compete in this specification-heavy segment. Modular containerized electrical rooms for renewable projects are adding further support to this format, because factory-built free-standing assemblies shorten site installation time and simplify coordination.

By End-User: Commercial Anchors Demand, Residential Delivers the Fastest Growth

Commercial end users accounted for 38.3% of the South Africa distribution boards market in 2025, so this group remained the main demand anchor. Office, retail, hospitality, healthcare, and mixed-use assets continue to upgrade electrical systems as they pursue greener operations and more stable on-site power architectures. Commercial buildings also absorb a large share of embedded generation and battery storage retrofits, which lifts demand for upgraded main and sub-main boards rather than simple component swaps. Industrial users form the next major layer of demand, especially in mining, chemicals, food processing, and fabrication, where board ratings, fault performance, and uptime matter more than initial cost.

Residential applications are projected to grow at an 8.3% CAGR through 2031, making them one of the fastest-moving parts of the South Africa distribution boards market size. Over 1 million South African homes had solar installations by 2025, and compliant hybrid setups need dedicated AC and DC protection zones that many legacy final boards do not provide. SANS 10142-1 Edition 3.2 strengthened these replacement triggers by tightening fault-current and busbar requirements for grid-plus-generation installations. Utilities remain a meaningful buyer as well, because substation refurbishment and transformer secondary-side upgrades continue to create board demand outside the building segment.

Geography Analysis

Gauteng accounts for the largest provincial concentration of demand in the South Africa distribution boards market. Its position reflects the country's deepest mix of commercial space, industrial refurbishment, and digital infrastructure investment. The province also carries a dense pipeline of commercial and industrial solar and storage retrofits, which keeps demand strong for MDBs, SMDBs, and smarter monitoring-ready boards. Eskom's utility intervention activity in municipalities around Ekurhuleni and Tshwane adds another layer of replacement need as aging low-voltage assets are renewed.

Western Cape is the fastest-growing provincial demand node in the South Africa distribution boards market, especially for technology-led and renewable-linked applications. The province combines strong commercial development with active private power adoption, which raises demand for generation-integrated board architectures across offices, mixed-use assets, and service facilities. National Energy Regulator of South Africa (NERSA)'s wheeling framework is particularly relevant here because private generators and commercial buyers are increasingly using network access models that require coordinated protection between low-voltage and medium-voltage systems. A relatively efficient contractor ecosystem also helps shorten the time between project approval and procurement, which supports faster board ordering than in more congested regions. These factors keep the Western Cape near the front of the South Africa distribution boards market as projects shift from emergency backup systems to permanent hybrid energy designs.

KwaZulu-Natal and the remaining provinces make up a smaller but still important part of the South Africa distribution boards market. KwaZulu-Natal supports demand through port-linked commerce, manufacturing, healthcare, and renewable integration, all of which require a mix of wall-mounted, free-standing, and MV interface panels. The Integrated National Electrification Programme (INEP) Action Plan targets universal electricity access by 2030 through grid extensions and microgrid deployment across provinces such as Limpopo, Mpumalanga, and North West, which keeps entry-level and mid-tier board demand active beyond the major metros. Free State and Northern Cape renewable corridors also support utility-grade installations, and Gauteng, Western Cape, and KwaZulu-Natal are expected to hold the dominant value share through 2031.

Competitive Landscape

The South Africa distribution boards market is moderately fragmented. The South Africa distribution boards market shows a dual-tier structure rather than a single uniform competitive field. ABB, Siemens, Schneider Electric, Eaton, and Legrand lead the high-specification side, where data centers, mining, utilities, and large commercial projects demand type-tested systems and established service support. ACTOM, CBi-electric: low voltage, Voltex MV/LV Solutions, and regional panel builders hold a strong position in the mid-market, where response time, standards familiarity, and local assembly matter more. Voltex MV/LV Solutions illustrates this model with SABS-approved low-voltage boards that integrate switchgear from ABB, Schneider Electric, and Siemens within locally assembled configurations. This makes the South Africa distribution boards market competitive by application tier, not only by brand scale.

The strongest contest is forming around data centers, embedded solar, and smarter commercial retrofits, because these jobs reward suppliers that can combine hardware, monitoring, and lifecycle service in one offer. Localization pressure within Eskom and municipal procurement also protects part of the addressable demand for domestic assemblers that can meet content rules and lead-time expectations. The NRCS Letter of Authority process remains a meaningful barrier for new entrants, because suppliers with approved product ranges can move faster than rivals that still need compliance clearance under VC 8036. White-space opportunities remain in smart boards for sub-1 MVA retrofits and in containerized electrical rooms for renewable projects, where no single domestic specialist has clear control.

ABB highlighted UniGear Digital ZS1 smart switchgear and related substation control technologies at AMEU 2025 and Enlit Africa 2026, which shows a clear push toward digitally monitored distribution assets. ACTOM launched an inverter-integrated transformer skid in 2025 that combined a locally built transformer, inverter, low-voltage combiner box, and medium-voltage ring main unit in one factory-tested package. Sungrow and Herholdt's Group also signed a 1,155 MWh commercial and industrial BESS rollout agreement in March 2026, which expands the installed base that will need dedicated low-voltage protection and board coordination at each site. CHINT's growing presence adds pricing pressure in the mid-market, so both multinationals and local assemblers will need to defend share through standards compliance, local support, and product breadth.

South Africa Distribution Boards Industry Leaders

Schneider Electric SE

ABB Ltd.

Siemens AG

ACTOM (Pty) Ltd.

Legrand SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Sungrow and Herholdt's Group have entered into an agreement to deploy 1,155 MWh of Commercial and Industrial (C&I) Battery Energy Storage Systems (BESS) across South Africa through phased rollouts. Each deployment site necessitates a purpose-designed low-voltage (LV) distribution board with dedicated storage circuit protection, creating substantial hardware demand for local panel suppliers.

- January 2026: SANS 10142-1 Edition 3.3 has entered a public comment phase with an expedited one-month consultation period, targeting publication by mid-2026. This edition builds on the photovoltaic (PV) and hybrid-system board protections introduced in Edition 3.2. The revision aims to further enhance fault-level calculation requirements and refine distribution board selection criteria.

South Africa Distribution Boards Market Report Scope

A distribution board (DB), also referred to as an electrical panel, breaker box, or fuse box, serves as the central component of an electrical system. It receives the main power supply from the grid and distributes it into smaller subsidiary circuits, ensuring safe and efficient power delivery to lights, outlets, and appliances within a building.

The South Africa Distribution Boards Market is segmented into type, technology, mounting type, and end user. By type, the market is segmented into main distribution boards (MDB), sub-main distribution boards (SMDB), and final distribution boards (FDB). By technology, the market is segmented into conventional boards and smart/IoT-enabled boards. By mounting type, the market is segmented into wall-mounted and floor/free-standing. By end user, the market is segmented into utilities, industrial, commercial, and residential. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Main Distribution Boards (MDB) |

| Sub-Main Distribution Boards (SMDB) |

| Final Distribution Boards (FDB) |

| Conventional Boards |

| Smart/IoT-enabled Boards |

| Wall-Mounted |

| Floor/Free-Standing |

| Utilities |

| Industrial |

| Commercial |

| Residential |

| By Type | Main Distribution Boards (MDB) |

| Sub-Main Distribution Boards (SMDB) | |

| Final Distribution Boards (FDB) | |

| By Technology | Conventional Boards |

| Smart/IoT-enabled Boards | |

| By Mounting Type | Wall-Mounted |

| Floor/Free-Standing | |

| By End-User | Utilities |

| Industrial | |

| Commercial | |

| Residential |

Key Questions Answered in the Report

What is the expected value of South Africa distribution boards demand by 2031?

The South Africa Distribution Boards Market size is projected to expand from USD 111.78 million in 2025 and USD 118.82 million in 2026 to USD 161.68 million by 2031, registering a CAGR of 6.35% between 2026 to 2031.

Which product category leads current revenue and which one is growing fastest?

Main Distribution Boards led with 43.3% share in 2025, while Final Distribution Boards are projected to grow the fastest at 8.7% CAGR through 2031.

Why are residential board replacements increasing in South Africa?

Rooftop solar adoption has crossed 1 million homes, and SANS 10142-1 Edition 3.2 requires compliant AC and DC protection, busbar suitability, and fault-current handling that many legacy final boards do not meet.

How is the wheeling framework affecting electrical board demand?

The March 2025 wheeling framework is pushing more projects toward coordinated low-voltage and medium-voltage protection layouts, especially for sites above 1 MVA that need upgraded MDB and SMDB configurations.

Which provinces are driving the strongest demand?

Gauteng remains the largest demand center, Western Cape is the fastest-growing node, and KwaZulu-Natal remains important through commercial, industrial, and network-linked applications.

Which technology trend is changing panel specifications the most?

Smart and IoT-enabled boards are reshaping premium projects, especially in data centers and advanced commercial sites, and this segment is projected to expand at 10.5% CAGR through 2031.

Page last updated on: