Nigeria Distribution Boards Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

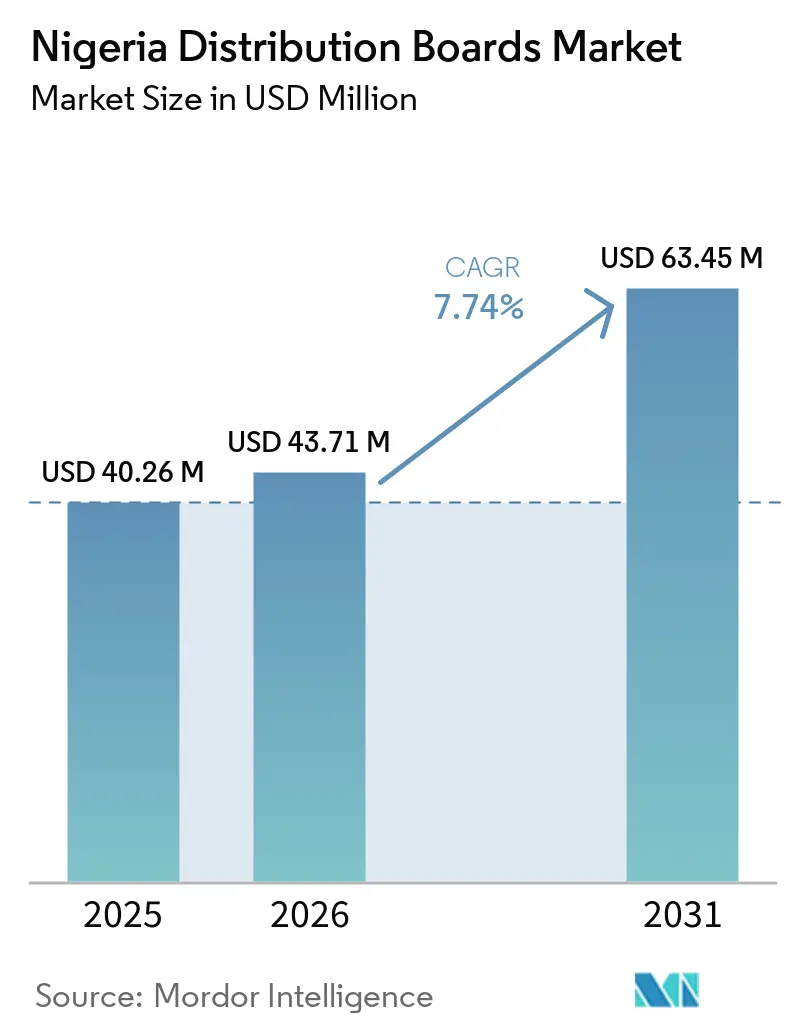

| Base Year Market Size (2025) | USD 40.26 Million |

| Market Size (2026) | USD 43.71 Million |

| Market Size (2031) | USD 63.45 Million |

| Growth Rate (2026 - 2031) | 7.74% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nigeria Distribution Boards Market Analysis by Mordor Intelligence

The Nigeria Distribution Boards Market size is expected to grow from USD 40.26 million in 2025 to USD 43.71 million in 2026 and is forecast to reach USD 63.45 million by 2031 at 7.74% CAGR over 2026-2031. The Nigeria distribution boards market is being supported by a large housing deficit, persistent power losses across the grid, and wider use of captive generation by industrial users, which together keep demand active across residential, commercial, utility, and self-supply installations.[1]Source: Federal Ministry of Housing and Urban Development, “FG’s Technical Committee Releases New Housing Data, Pegs Deficit at 15 Million Units,” Federal Ministry of Information and National Orientation, fmino.gov.ng The market is also gaining from utility rehabilitation programs and state-level electricity market rollout, which are widening procurement channels beyond the traditional federal pipeline.[2]Source: FGN Power Company, “FGN Power Company Signs Contract with Elsewedy and Power China for Distribution Lines Rehabilitation and Construction,” FGN Power Company, fgnpowerco.ng Smart product adoption remains smaller in the installed base, but its growth rate is higher because metering programs, service-quality enforcement, and captive plants all favor better monitoring and control. Competition is split between global brands that serve higher-spec projects and local assemblers that win on lead time and price, which keeps the Nigeria distribution boards market open to both certified import-based assembly and branded system integration. Import dependence, currency volatility, and tighter inspection rules still weigh on project timing and component costs, but the demand base remains durable enough to support the forecast expansion.

Key Report Takeaways

- By type, Final Distribution Boards held 46.8% of Nigeria distribution boards market size in 2025, while Sub-Main Distribution Boards are forecast to grow at a 7.9% CAGR through 2031.

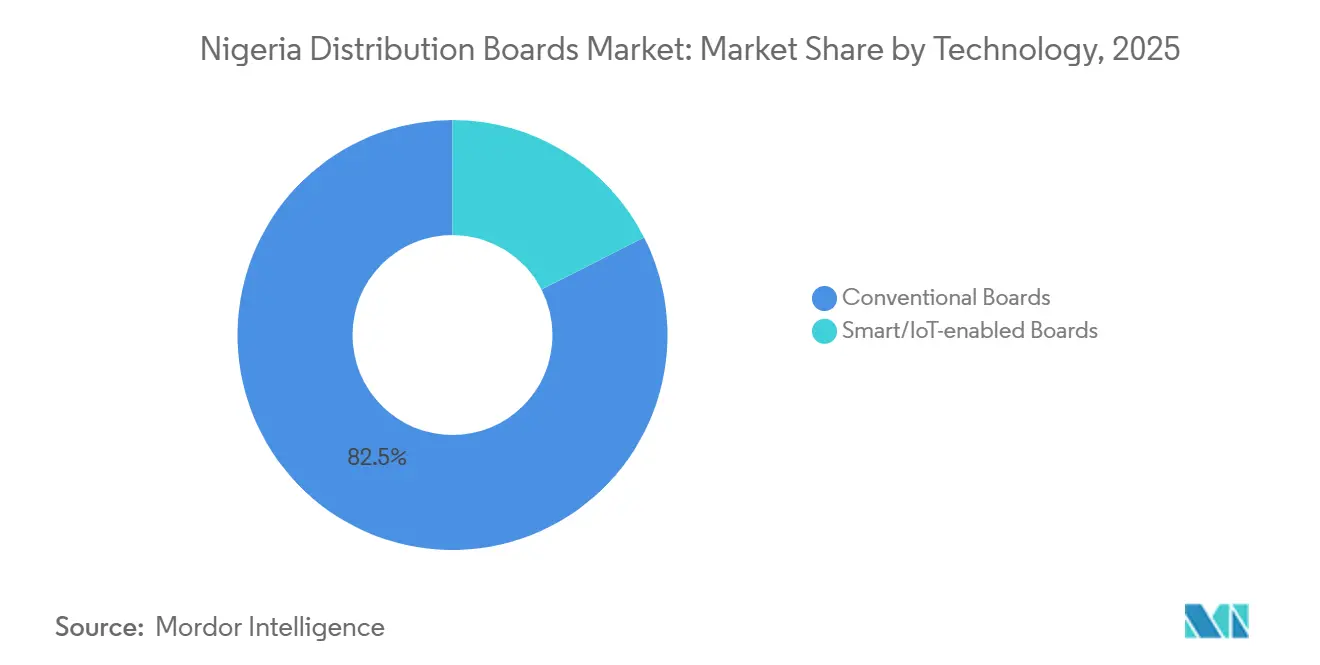

- By technology, conventional boards accounted for 82.5% of Nigeria distribution boards market size in 2025, while smart or Internet of Things (IoT)-enabled boards are projected to expand at an 11.6% CAGR through 2031.

- By mounting type, wall-mounted boards held 71.4% of Nigeria distribution boards market share in 2025, while floor or free-standing boards are expected to grow at an 8.1% CAGR through 2031.

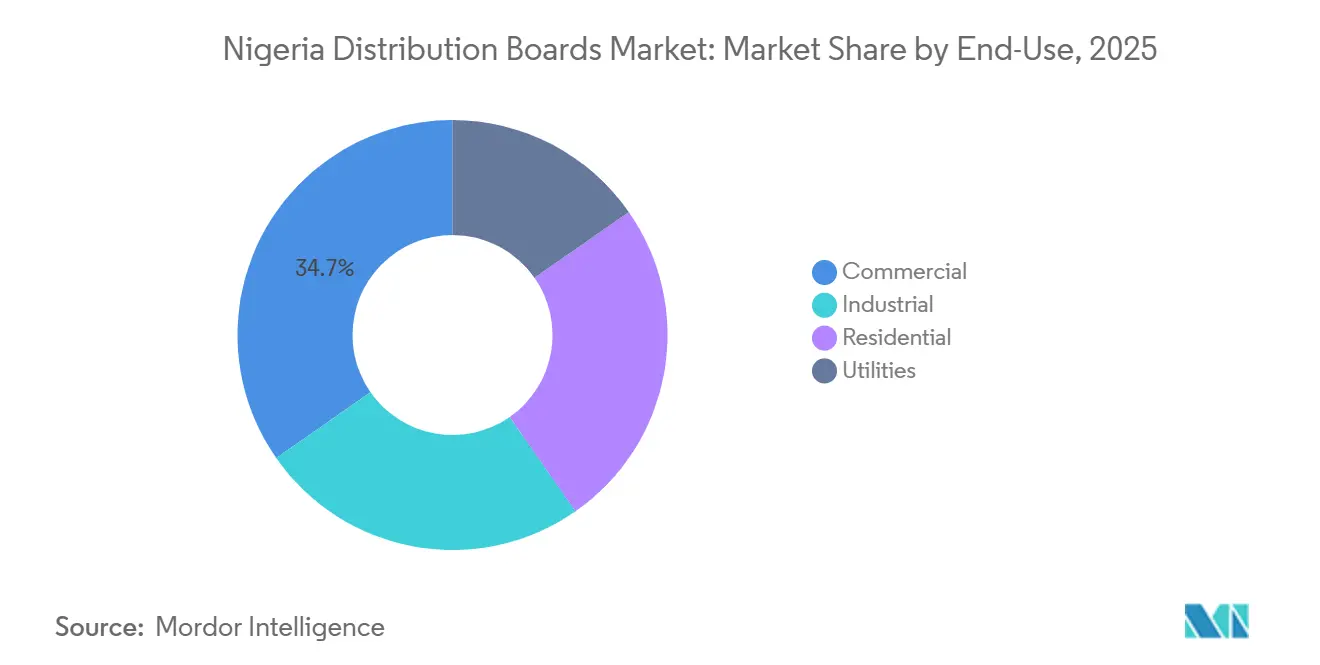

- By end-user, the commercial segment held 34.7% of Nigeria distribution boards market share in 2025, while utilities are projected to record the fastest CAGR at 9.3% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Nigeria Distribution Boards Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Housing backlog and new-build electrical fit-outs | +1.8% | South-West, FCT Abuja, South-East, with spillover to all states | Medium term (2-4 years) |

| Commercial and industrial captive-power expansion | +2.1% | Lagos, Ogun, Rivers, Delta industrial corridors, with early gains in Abuja CBD | Short term (≤ 2 years) |

| Smart metering and Aggregate Technical, Commercial and Collection (ATC&C)-loss reduction programs | +1.3% | National, strongest in South-West and South-East Distribution Company (DisCo) franchises | Medium term (2-4 years) |

| Renewable mini-grids and feeder hybridization | +0.9% | North-Central, North-East, South-South off-grid communities, scaling to interconnected feeders nationwide | Long term (≥ 4 years) |

| State electricity market rollout under the Electricity Act | +0.7% | Lagos, Enugu, Ekiti, Ondo, Oyo, Edo, Kogi and other states with active regulatory commissions | Medium term (2-4 years) |

| Local panel assembly and Nigerian-content partnerships | +0.5% | Port Harcourt, Lagos, Ogun manufacturing corridor | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Housing Backlog and New-Build Electrical Fit-Outs

Nigeria’s housing deficit is creating a steady installation base for final distribution boards across new homes and retrofit work. The National Housing Data Technical Committee put the housing deficit at 14.925 million units in 2025, which keeps residential electrical fit-out demand structurally active.[3]Source: Federal Ministry of Housing and Urban Development, “FG’s Technical Committee Releases New Housing Data, Pegs Deficit at 15 Million Units,” Federal Ministry of Information and National Orientation, fmino.gov.ng This matters for the Nigeria distribution boards market because every new dwelling needs a compliant final board at handover, and larger estates often add riser-level sub-main panels as well. The retrofit angle also matters because deficient existing stock does not only delay demand, but it also shifts it into replacement and refurbishment cycles. That raises unit demand for FDBs and lifts the role of SMDB panels in multi-family buildings where shared power distribution is becoming more common.

Commercial and Industrial Captive-Power Expansion

Captive generation has moved from a backup decision to a core operating requirement for many industrial users. In 2025, 23 companies obtained permits to generate 1,183 MW of captive power, and 11 more companies secured 130.2 MW in Q4 alone, which points to a widening self-supply pipeline outside the national grid. Each of these installations needs a main distribution board or a sub-main switchboard at the generation interface, usually with transfer switching and metered outgoing circuits. That creates direct procurement between project owners and panel builders, which reduces dependence on grid-led utility replacement cycles. The Nigeria distribution boards market therefore gains from a parallel infrastructure layer that is being built inside industrial estates, logistics clusters, and larger commercial compounds. This dynamic is especially visible in Lagos, Ogun, Rivers, and Delta, where reliable internal power has become a site-selection factor for industrial occupancy.

Smart Metering and ATC&C-Loss Reduction Programs

Loss reduction and metering reform are turning ordinary panel upgrades into monitored distribution assets. ATC&C losses stood at 39.6% in Q1 2025 against a 20.5% benchmark, which keeps pressure on utilities to improve visibility and control at feeder and substation level. The World Bank-backed DISREP program was launched to deploy 3.2 million smart meters, while the wider metering drive added a 7 million target that extends the scale of supporting infrastructure needs. The Nigeria distribution boards market benefits because metering alone is not enough, utilities also need compliant, remotely visible boards around transformer and feeder points. NEMSA’s 2025 alliance with NISO added another layer by tying testing and certification more closely to commissioning of new infrastructure. Remote monitoring is therefore shifting from a premium option to a practical commercial requirement in the higher-value part of the market.

Renewable Mini-Grids and Feeder Hybridization

Mini grids are creating a different demand channel from the conventional urban grid. Nigeria had more than 200 mini-grids in operation in 2025, and 40 interconnected mini-grid projects totaling 288 MW were also being developed under the revised framework. The DARES program targets 1,350 mini-grids and service for 17.5 million Nigerians, which widens long-run procurement for boards that manage solar input, storage, backup generation, and feeder circuits. The Nigeria distribution boards market also gets value from feeder hybridization because interconnected sites need more advanced protection and bidirectional control than a basic off-grid panel. That lifts demand for higher-spec SMDB and MDB configurations in projects that would otherwise appear small on headline capacity data. The effect is strongest in off-grid and weak-grid regions, but the specification logic is gradually moving into mainstream utility feeder upgrades as well.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Import dependence and FX-driven component inflation | -1.6% | National; most acute for small-to-medium panel builders in Lagos and Port Harcourt | Short term (≤ 2 years) |

| High maintenance burden in unstable-grid conditions | -0.8% | North-East and North-West regions where ATC&C losses exceed 60%; spill-over to all zones | Medium term (2–4 years) |

| Compliance and certification burden under tighter enforcement | -0.5% | National; highest compliance pressure in Lagos commercial corridor, Port Harcourt oil & gas sector, and utility-adjacent procurement across all DisCo franchises | Medium term (2–4 years) |

| Limited digital-board commissioning capability | -0.3% | Most severe in secondary cities (Kano, Ibadan, Enugu) and northern states; persists as a broader national constraint outside the Lagos–Abuja–Port Harcourt triangle | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Import Dependence and FX-Driven Component Inflation

Imported inputs still set the cost floor for a large share of locally assembled boards. Nigeria’s raw material import bill reached NGN 3.53 trillion, equivalent to USD 2.5 billion, in H1 2025, and more than 70% of manufacturing inputs were still externally sourced. Manufacturers also reported FX losses rising to NGN 1.62 trillion, or USD 1.1 billion, in 2024, which showed how earlier currency weakness passed through to industrial cost structures. Even though the naira was firmer at NGN 1,416.52 per USD in January 2026, the Nigeria distribution boards market still faces embedded exposure in imported breakers, busbars, terminals, and sheet steel. Standards Organization of Nigeria Conformity Assessment Program (SONCAP) adds another cost and timing layer because offshore conformity checks affect shipment release cycles. Local assembly helps at the final stage, but the upstream exposure remains in place because domestic production of critical breaker categories is still limited.

High Maintenance Burden in Unstable-Grid Conditions

Unstable power quality raises the ownership cost of a board long after the initial purchase. Voltage swings, phase imbalance, and repeated system disturbances accelerate wear on breakers, busbars, and neutral paths, which is most visible in weaker northern franchises. Nigerian Electricity Regulatory Commission (NERC)’s Q2 2025 reporting showed ATC&C losses above 60% for Kaduna Electric, Jos Electricity Distribution Company PLC, and Yola Electricity Distribution Company, which points to stressed operating conditions in those networks. The maintenance burden matters in the Nigeria distribution boards market because it suppresses premium product uptake where commissioning skills are scarce and failure risk is harder to manage. It also delays replacement demand in regions where customer economics are already weak, even when the installed need is clear. This is one reason growth stays concentrated in Lagos and the South-West, where grid conditions, technical support, and project execution capacity are relatively stronger than in the higher-deficit northern zones.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Final Boards Drive Volume, Sub-Main Boards Drive Value Growth

Final Distribution Boards accounted for 46.8% of market value in 2025, which gave them the largest product position in the Nigeria distribution boards market. This share reflects the volume intensity of residential construction and the need for at least one compliant board in every completed dwelling. The official housing deficit of 14.925 million units supports that volume case, especially where new estates and apartment schemes continue to move from shell construction into electrical fit-out.[4]Source: Federal Ministry of Housing and Urban Development, “FG’s Technical Committee Releases New Housing Data, Pegs Deficit at 15 Million Units,” Federal Ministry of Information and National Orientation, fmino.gov.ng The Nigeria distribution boards industry also benefits from retrofits because structurally weak or outdated housing stock still requires final-board replacement before broader wiring upgrades can be completed. Main Distribution Boards kept a meaningful position because large industrial sites and utility substations still need higher-rated distribution architecture. That role is reinforced by grid rehabilitation works under the Presidential Power Initiative and related federal contracts.

Sub-Main Distribution Boards are the fastest-growing product type at a 7.9% CAGR through 2031, which shows where value is shifting inside the Nigeria distribution boards market. Multi-tenant commercial buildings, industrial compounds, and logistics parks need layered power distribution, and that places SMDBs between the main incomer and the final load points. This change matters because SMDBs usually carry higher average selling prices than basic Final Distribution Boards (FDBs). It means revenue is rising faster than unit count in parts of the Nigeria distribution boards industry where electrical layouts are becoming more complex. Local manufacturing plans also support this tier. Tranos began construction of a large solar and power distribution panel manufacturing campus in Ogun State in April 2026, which points to added domestic capacity in higher-value board categories. Corustar’s use of BS EN 61439-2 for low voltage (LV) panel assemblies also shows that local players are aligning with the compliance needs of commercial and industrial buyers

By Technology: Conventional Boards Dominate, Smart Boards Structurally Repriced

Conventional boards commanded 82.5% of the market value in 2025, which kept them dominant across the Nigeria distribution boards market. Their lead reflects cost sensitivity among residential contractors and smaller commercial buyers who still prioritize purchase price over monitoring capability. Procurement also remains informal in a large part of the market, with many contractors buying through distributor relationships rather than strict engineering specifications. That pattern favors established conventional products and simple locally assembled configurations. It also explains why adoption outside Lagos and other large cities remains slower where skilled commissioning support is thinner. For many projects, the simpler board is still the lower-risk procurement choice because it is easier to source, install, and service.

Smart or IoT-enabled boards are forecast to grow at an 11.6% CAGR through 2031, which makes them the fastest-growing segment in the Nigeria distribution boards market. The shift is strongest in utility upgrades, captive-power plants, and data-heavy commercial sites that value remote visibility and automated switching. Distribution Sector Recovery Program (DISREP) and the wider meter rollout support this move because feeder-level control and monitoring work better when the associated boards can communicate and report. The market is also being pulled by industrial self-supply because load management becomes more important when generation, storage, and demand all sit behind the same site boundary. CHINT’s 2026 reporting highlighted its Nigeria presence and wider African manufacturing footprint, which underlines how global suppliers are positioning for this higher-spec demand layer. Even where current penetration looks modest, the use case is stronger than the headline share suggests because these products are concentrated on larger and technically demanding projects.

By Mounting Type: Wall-Mounted Boards Anchor Mass Market, Floor-Standing Gains in Industrial Corridors

Wall-mounted boards held 71.4% of market value in 2025, which gave them the largest form-factor position in the Nigeria distribution boards market. This result tracks with the dominance of residential and light commercial applications where flush and surface-mounted enclosures are the standard choice. The retrofit base also supports demand because lower-cost wall-mounted boards fit the economics of housing upgrades better than larger free-standing systems. Local assembly helps here because semi-knocked-down kits shorten lead times and help keep the delivered cost competitive. That cost advantage matters in projects where the board is treated as a necessary fit-out item rather than a premium electrical asset. The format therefore remains central to mass-market demand even as specification standards gradually improve.

Floor or free-standing boards are forecast to expand at an 8.1% CAGR through 2031, which shows the stronger momentum in larger technical installations. Captive plants, mini-grid control rooms, and industrial facilities need more internal space for metering, transfer switching, protection devices, and heavier cable termination. That gives free-standing systems a clear role in the higher-value slice of the Nigeria distribution boards market. Port Harcourt remains important in this category because oil and gas specifications support heavier-duty assemblies and system integration. Collective Power’s Port Harcourt facility was recognized by the Nigerian Content Development and Monitoring Board for low-voltage panel assembly, medium voltage (MV) switchgear, and power distribution transformer capabilities, which reflects the shift toward more localized industrial supply. The segment is still smaller by installed base, but its growth comes from projects with better pricing power and more demanding board architecture.

By End-User: Commercial Leadership Challenged by Utility Acceleration

The commercial segment held 34.7% of market value in 2025, which made it the largest end-user group in the Nigeria distribution boards market. Lagos remains the main anchor because office, retail, hospitality, logistics, and mixed-use developments require layered board installations across tenants and common-service areas. This part of the market also benefits from stronger enforcement of installation quality because insurers, developers, and larger contractors are less willing to accept uncertified electrical work. Commercial projects typically buy multiple board types on a single site, which raises total project value beyond a basic residential installation. That helps explain why the segment leads to value even though residential construction often leads on unit count. The Nigeria distribution boards industry therefore gains a steady premium from commercial schemes that need coordinated distribution architecture across substations, risers, and final circuits.

Utilities are the fastest-growing end-user segment, with a 9.3% CAGR forecast through 2031, which points to a stronger public-network procurement cycle. Federal contracts for transmission and distribution rehabilitation are already expanding the pipeline for board replacements and new installations at substations and feeder nodes. The Electricity Act 2023 also matters because more states are taking regulatory authority and moving ahead with local market structures, which can speed project approval and procurement relative to older federal routes. Residential demand remains broad but price-sensitive, while industrial demand rises and falls with captive plant and self-supply project pipelines. Utilities therefore stand out because they combine compliance pressure, network rehabilitation, and wider metering-linked board upgrades in one demand stream. This mix gives the Nigeria distribution boards market a stronger medium-term base than a residential-only demand profile would have delivered.

Geography Analysis

The South-West remains the largest demand center in the Nigeria distribution boards market, with Lagos at the core of both consumption and assembly activity. Lagos has 14 licensed private electricity operators and a stated target of 97.5% supply availability by 2030, which supports a larger pipeline of substation, feeder, industrial, and commercial installations than any other state. The Lagos and Ogun corridor also anchors local supply because panel assembly, wholesale distribution, and project engineering are concentrated there. International Finance Corporation (IFC)’s February 2025 equity investment of up to USD 50 million in Lagos Free Zone adds to that corridor by supporting industrial and logistics build-out tied to power distribution needs. Lagos also benefits from active intra-state market development, which increases the number of projects that can procure boards for localized generation and distribution infrastructure. This makes the South-West the clearest reference point for pricing, specification, and product availability across the country.

The Federal Capital Territory and the South-East show a different demand pattern inside the Nigeria distribution boards market. Abuja’s commercial and government-linked real estate pipeline continues to support medium- and higher-spec board demand where developers are less likely to cut electrical scope. The South-East has a more connected consumer base, so the opportunity includes both new installations and replacement demand in already electrified areas. Enugu also matters because early progress on state-level electricity regulation gives it a stronger route to localized infrastructure upgrades. Port Harcourt and the wider South-South remain the premium end of the market because oil and gas-linked specifications support higher-rated and more customized boards.

Northern Nigeria presents the largest gap between theoretical need and near-term realizable demand. Lower electrification, weaker distribution performance, and heavier maintenance stress limit the pace of conventional grid-led board demand in many northern networks. At the same time, the region is central to off-grid growth because mini-grids and distributed power programs are directed toward communities with the deepest access deficit. That means the geography outlook for the Nigeria distribution boards market in the North is being shaped less by DisCo replacement cycles and more by donor-backed and development-financed deployment channels. Projects in Niger, Kogi, and Nasarawa under the ENGIE and CrossBoundary arrangement show how board demand can emerge through mini-grid control houses and feeder interface panels rather than traditional urban substations. The North therefore remains a long-run growth case, but the timing depends more on program execution and disbursement pace than on standard tariff reform.

Competitive Landscape

The Nigeria distribution boards market operates through two visible competitive layers. The upper tier is led by multinational brands such as Schneider Electric, ABB, Siemens, Eaton, Hager, and CHINT, which compete on technical compliance, installed reliability, and service support for larger projects. These suppliers are strong where utility, industrial, data center, and high-value commercial work requires type-tested systems and branded components. The lower tier remains fragmented across local assemblers in Lagos, Port Harcourt, and Abuja that build around imported components and semi-knocked-down kits. This split means no single route to market dominates the full Nigeria distribution boards market. Buyers at the premium end usually want certified systems and engineering backing, while buyers in the mass market often prioritize lead time, availability, and cost.

Schneider Electric remains one of the deeper ecosystem players because it combines product sales with training and channel development in Nigeria. Its EcoXpert model and local partner relationships support board specification in projects where commissioning quality matters, and its distributor-integrator agreement with Collective Power strengthens reach in the Port Harcourt industrial base. CHINT is pushing from the mid-market side with a wide African footprint and a Nigeria presence backed by manufacturing activity elsewhere on the continent, which helps it stay price-competitive without fully exiting the branded segment. Siemens is pursuing a more infrastructure-linked path because the Presidential Power Initiative creates downstream pull for compatible board solutions through rehabilitation and new network assets. Eaton also stays relevant where modular and resilient power systems are needed, especially in data-led or off-grid commercial settings.

For local players, the most important battleground is the middle layer between commodity FDB assembly and high-spec MDB manufacture. Custom SMDBs for multi-tenant buildings, transfer-switch panels for captive generators, and monitored boards for utility feeder upgrades all sit in this space. Firms that can document compliance to BS EN 61439-2 or ISO 9001:2015 gain an advantage because certification is becoming a practical entry condition for utility-adjacent and industrial work. Nigerian Electricity Management Services Agency (NEMSA)’s tighter inspection focus and the certification-before-commissioning environment should support gradual consolidation toward certified assemblers over time. That does not remove fragmentation, but it does raise the barrier between basic assembly shops and players that can serve the more technical end of the Nigeria distribution boards market.

Nigeria Distribution Boards Industry Leaders

Schneider Electric SE

ABB Ltd.

Siemens AG

Eaton Corporation plc

CHINT Group

- *Disclaimer: Major Players sorted in no particular order

Geopolitical Scenarios and Their Impact on the Nigeria Distribution Boards Market

Import Dependence and Supply-Side Cost Pressure

Nigeria's reliance on imported inputs continues to restrain the Nigeria distribution boards market because local panel builders still depend on foreign-sourced breakers, busbars, terminals, and sheet steel for a large share of production. The pressure is visible in the broader manufacturing base, where the raw material import bill reached NGN 3.53 trillion in H1 2025, and more than 70% of manufacturing inputs remained externally sourced. Currency volatility has added to that burden, with manufacturers reporting FX losses of NGN 1.62 trillion in 2024, which reduced pricing flexibility and increased working capital strain across assembly operations. Although the naira appreciated to NGN 1,416.52 per USD in January 2026, cost relief remains limited because imported components still shape both lead times and final board pricing across much of the supply chain. Compliance requirements are also becoming stricter as standards alignment and certification oversight deepen, which improves quality control but can slow procurement and commissioning for installations that depend on imported electrical materials. As a result, this restraint is acting less as a demand shock and more as a drag on margins, delivery schedules, and project execution across the Nigeria distribution boards market.

Recent Industry Developments

- April 2025: FGN Power Company signed a USD 328.8 million Engineering, Procurement, Construction, and Finance (EPC&F) contract with China Machinery Engineering Corporation (CMEC) for rehabilitation and construction of 330 kV and 132 kV transmission lines under Phase I of the Presidential Power Initiative. Two of five priority substations are expected to be completed by end-2026, each requiring matched MDB procurement at the distribution side.

- February 2025: International Finance Corporation (IFC) announced an equity investment of up to USD 50 million in Lagos Free Zone to support the development of Nigeria's first deepsea port-based private special economic zone, including industrial facilities and logistics infrastructure. The associated construction pipeline represents a direct pipeline for low voltage panel boards Lagos-centred industrial demand.

Nigeria Distribution Boards Market Report Scope

A distribution board, also known as a panelboard, breaker panel, or electric panel, is a component of an electricity supply system that distributes electrical power into subsidiary circuits while providing protective fuses or circuit breakers. The distribution board market involves the production, distribution, and sale of these panels, serving residential, commercial, industrial, and utility sectors, from small consumer units in homes to large switchboards in industrial facilities.

The Nigeria Distribution Boards Market is segmented into type, technology, mounting type, end-user, and geography. By type, the market is segmented into main distribution boards, sub-main distribution boards, and final distribution boards. By technology, the market is segmented into conventional boards and smart/IoT-enabled boards. By mounting type, the market is segmented into wall-mounted and floor/free-standing boards. By end-user, the market is segmented into utilities, industrial, commercial, and residential sectors. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Main Distribution Boards (MDB) |

| Sub-Main Distribution Boards (SMDB) |

| Final Distribution Boards (FDB) |

| Conventional Boards |

| Smart/IoT-enabled Boards |

| Wall-Mounted |

| Floor/Free-Standing |

| Utilities |

| Industrial |

| Commercial |

| Residential |

| By Type | Main Distribution Boards (MDB) |

| Sub-Main Distribution Boards (SMDB) | |

| Final Distribution Boards (FDB) | |

| By Technology | Conventional Boards |

| Smart/IoT-enabled Boards | |

| By Mounting Type | Wall-Mounted |

| Floor/Free-Standing | |

| By End-User | Utilities |

| Industrial | |

| Commercial | |

| Residential |

Key Questions Answered in the Report

What is the 2031 outlook for distribution boards in Nigeria?

The Nigeria Distribution Boards Market size is expected to grow from USD 40.26 million in 2025 to USD 43.71 million in 2026 and is forecast to reach USD 63.45 million by 2031 at 7.74% CAGR over 2026-2031. to 2031.

Which product type leads current demand in Nigeria?

Final Distribution Boards lead current demand, with 46.8% of market value in 2025, mainly because every new residential unit needs a compliant final board.

Which technology is growing fastest in this space?

Smart or IoT-enabled boards are growing the fastest, with an 11.6% CAGR through 2031, supported by metering programs, utility upgrades, and captive-power installations.

Why is Lagos so important for board demand?

Lagos combines the country's strongest commercial activity, state-level electricity market rollout, industrial expansion, and the largest local assembly base, which makes it both a demand center and a supply hub.

Which end-user group is expanding the quickest?

Utilities are expanding the quickest, with a 9.3% CAGR through 2031, driven by rehabilitation contracts, feeder upgrades, and new state-led electricity infrastructure.

What is the main cost risk for suppliers and assemblers?

The biggest cost risk remains import dependence. Imported inputs still dominate critical components, so currency volatility and compliance-related shipment costs continue to affect pricing and margins.

Page last updated on: