Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

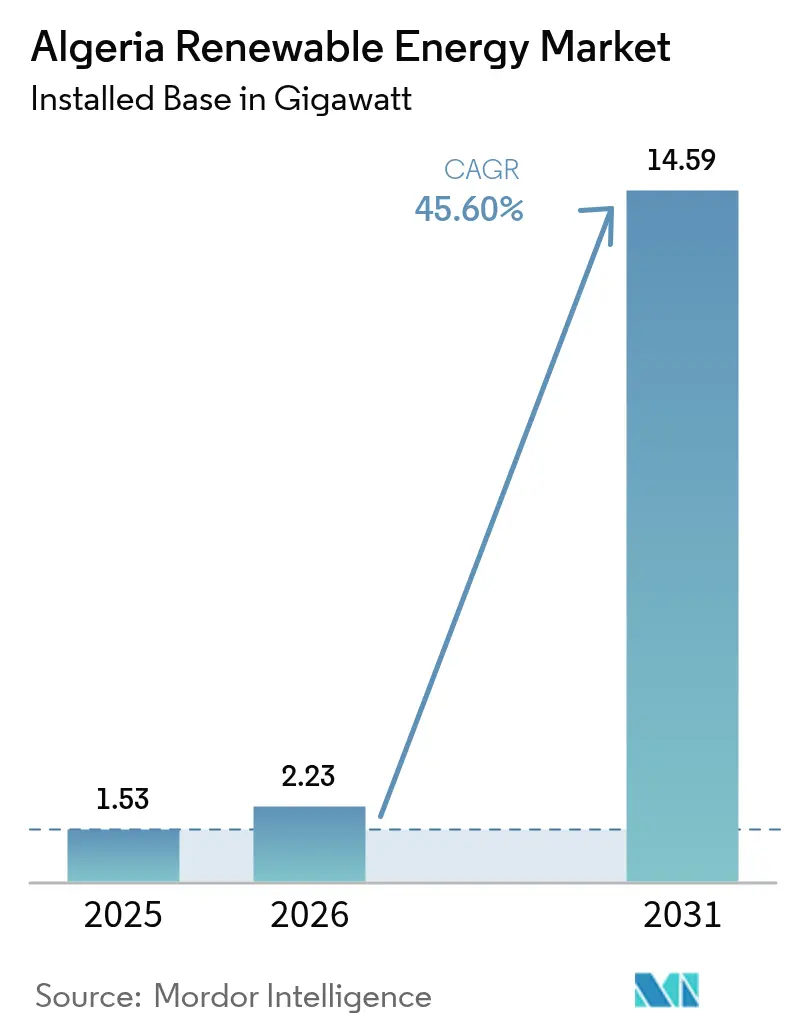

| Base Year Market Size (2025) | 1.53 gigawatt |

| Market Volume (2026) | 2.23 gigawatt |

| Market Volume (2031) | 14.59 gigawatt |

| Growth Rate (2026 - 2031) | 45.60% CAGR |

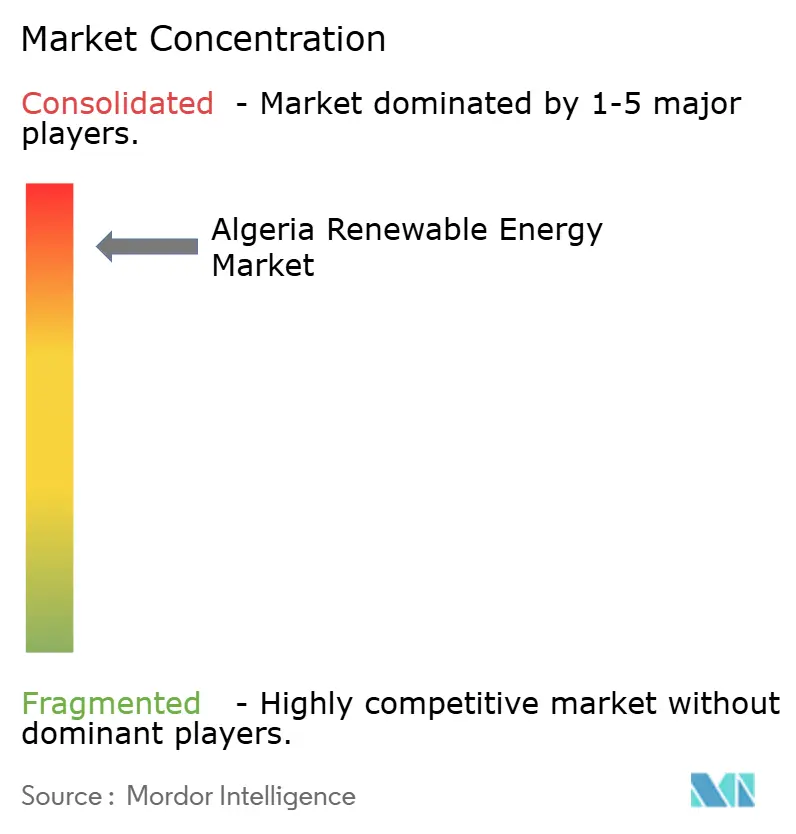

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Algeria Renewable Energy Market Analysis by Mordor Intelligence

Algeria Renewable Energy Market size in 2026 is estimated at 2.23 gigawatt, growing from 2025 value of 1.53 gigawatt with 2031 projections showing 14.59 gigawatt, growing at 45.60% CAGR over 2026-2031.

Ambitious targets in the National Program for the Development of Renewable Energies, the repeal of the 51/49 foreign-ownership rule, and the creation of the Ministry of Energy Transition and Renewable Energies have opened substantial headroom for private and foreign capital. Solar still dominates because Algeria enjoys solar irradiation above 2,200 kWh/m²/yr; however, utility-scale wind, green hydrogen, and hybrid CSP–PV systems are increasingly diversifying the supply mix. Policy refinements, such as streamlined tender rules and Islamic Green Sukuk, lower capital-cost hurdles, while falling LCOE for TOPCon PV and larger turbine classes reduce lifetime generation costs. Finally, Algeria's proximity to Europe, combined with the SoutH₂ Corridor, positions Algeria's renewable energy market as a strategic export platform into hydrogen-hungry EU states.

Key Report Takeaways

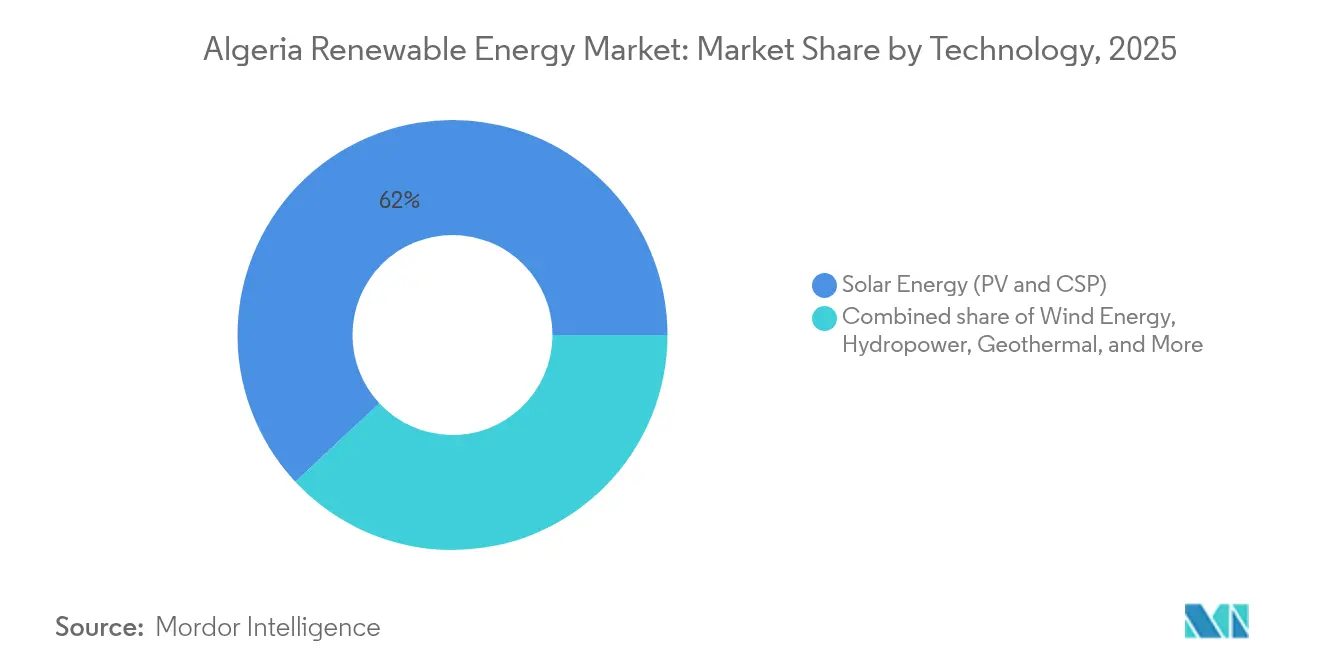

- By technology, solar energy led the Algerian renewable energy market with 61.95% of the market share in 2025; wind energy is projected to expand at a 113.90% CAGR through 2031.

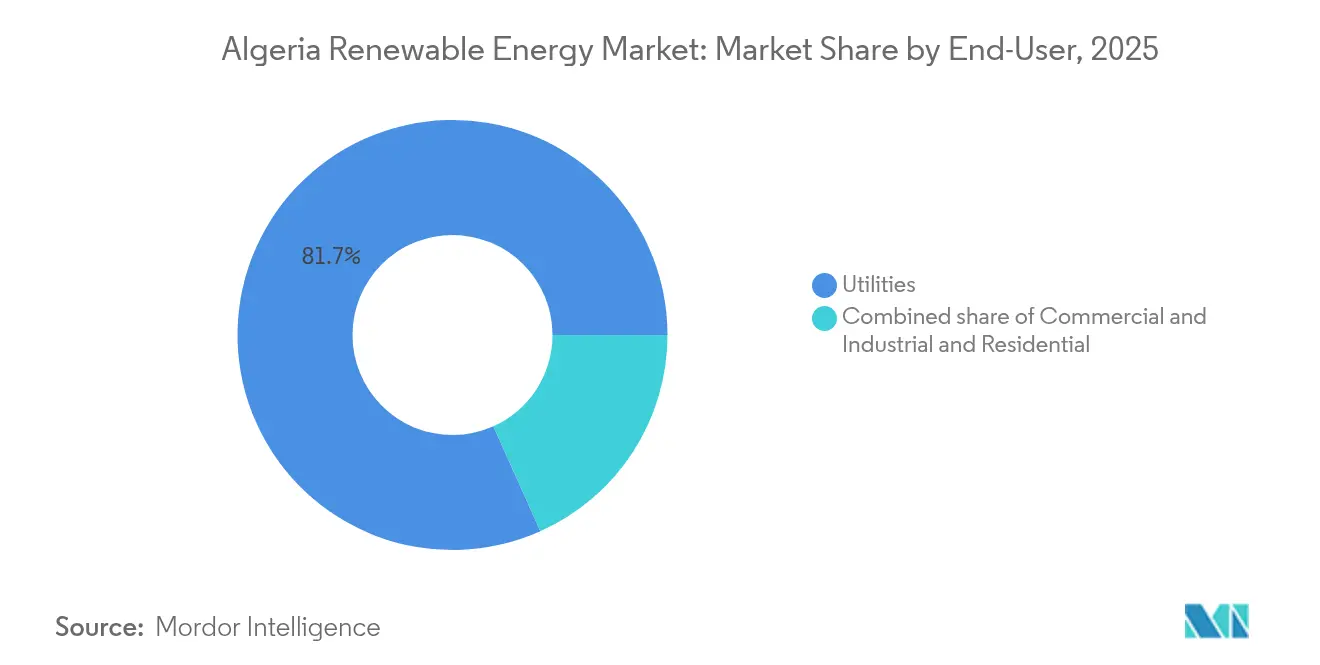

- By end-user, the utilities segment held 81.70% of the Algerian renewable energy market size in 2025, while the residential segment is expected to record the highest forecast CAGR of 52.85% from 2025 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Algeria Renewable Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ambitious 15 GW renewables target | +12.8% | National, Southern provinces lead utility-scale solar | Medium term (2-4 years) |

| Abundant ≥2,200 kWh/m²/yr solar irradiance | +10.5% | Nationwide, strongest in Saharan regions | Long term (≥ 4 years) |

| EU-linked green-hydrogen export corridors | +9.7% | National, export infrastructure in coastal regions | Long term (≥ 4 years) |

| Falling levelised cost of solar PV | +7.2% | Global driver with high local sensitivity | Short term (≤ 2 years) |

| Subsidy reform unlocking IPP participation | +5.8% | National, pilot zones in industrial clusters | Medium term (2-4 years) |

| Islamic Green Sukuk financing innovation | +3.9% | National, spill-over to wider Islamic capital markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ambitious 2030 Target of 15 GW Renewables

Algeria's statutory goal of installing 15,000 MW by 2035 underpins the Algeria renewable energy market, and the interim 2030 milestones push procurement schedules forward. SHAEMS, founded in 2020, coordinates foreign joint ventures and accelerates permitting, yet budget outlays remain under 0.1% of total public spending, leaving a USD 24.8 billion financing gap.[1]GH₂, “Algeria,” gh2.org Capital-market liberalization and the removal of the 51/49 rule address part of this gap, while multi-technology wind additions temper solar-only grid strain and boost the Algeria renewable energy market's CAGR.

Abundant Solar Irradiance Driving Competitive Advantage

Average insolation above 2,200 kWh/m²/yr and more than 3,500 sunshine hours ensure Algeria’s PV capacity factors compete globally. The Algeria renewable energy market, therefore, integrates CSP with thermal storage at sites like Hassi R’Mel to deliver evening power and provide grid inertia.[2]International Energy Forum, “Algeria Powers Ahead …,” ief.org TOPCon modules, such as Astronergy’s 1 GW shipment, further lower LCOE and reduce temperature-related derating. High isolation also reduces renewable hydrogen production costs, aligning with EU off-take needs.

EU-Linked Green Hydrogen Export Corridors

The 3,500-4,000 km SoutH₂ pipeline integrates repurposed natural-gas corridors, trimming CAPEX and speeding deployment. Germany–Algeria task forces harmonize standards and enable predictable revenue streams via long-term hydrogen offtake MoUs. Hydrogen ambitions lock in incremental solar and wind build-out, raising the trajectory of the Algerian renewable energy market size.

Falling Levelized Cost of Solar PV

Module prices fell by 42% between 2020 and 2024, and paired with Algeria’s high irradiation, projects now underbid subsidized gas generation on a per-kWh basis. The 1.5 GW Al Ajban plant achieved financial close with tariffs below USD 0.03/kWh, signaling risk compression. Cheaper PV frees budget for complementary battery storage and grid upgrades.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dominance of state utility delaying PPAs | −6.8% | National, utility-scale segment hardest hit | Medium term (2-4 years) |

| Persistent fossil-fuel price subsidies | −5.2% | National, variable by province | Long term (≥ 4 years) |

| Weak grid in southern and border regions | −4.1% | Remote Saharan and border provinces | Medium term (2-4 years) |

| Dinar convertibility and FX risk | −3.7% | National, foreign-funded projects most exposed | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Dominance of State Utility Delaying PPAs

Sonelgaz’s triple role as offtaker, grid operator, and competitor lengthens PPA negotiations to beyond two years, slowing tender award schedules.[3]Norton Rose Fulbright, “Solar energy in Algeria …,” nortonrosefulbright.com Counterparty credit risk also increases financing costs for IPPs, dampening the CAGR of the Algerian renewable energy market.

Dinar Convertibility & FX Risk for Foreign Investors

Periodic dinar volatility raises debt-service uncertainties for euro- or dollar-denominated loans, compelling lenders to demand higher spreads or political risk coverage. Sukuk and blended-finance structures partly hedge but do not fully offset the FX drag on the Algeria renewable energy industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Wind Energy Acceleration Challenges Solar Dominance

Solar retained a 61.95% share of the Algerian renewable energy market in 2025, contributing 947.8 MW to the country's renewable energy market size, while onshore wind closed the year at only 52 MW. Yet wind capacity is scheduled to jump to 5,010 MW by 2031, posting a 113.90% CAGR that narrows the share gap. Southern CSP projects, such as Hassi R'Mel, integrate three-hour molten-salt storage, proving dispatchability in a region with over 2,200 kWh/m²/yr irradiation.

The shift toward wind stems from complementary generation profiles; strong coastal breezes peak in the late afternoon, smoothing solar-driven midday peaks and limiting curtailment. Turbine OEMs now offer machines with 5+ MW of IEC Class III capacity, suited for low-density Saharan winds, which increases generation per foundation and mitigates logistical constraints. Hybrid PV-wind systems cut substation CAPEX by 12-15%, enhancing total project returns. Hydropower and bioenergy together account for less than 2% of Algeria's renewable energy market, constrained by arid hydrology and limited biomass logistics. However, pilot pumped-storage schemes in Kabylie may unlock time-shifted renewable firming post-2030.

By End-User: Utilities Dominance with Residential Transformation

Utilities accounted for 81.70% of the Algeria renewable energy market size, or 1,250 MW, in 2025, thanks to Sonelgaz-backed procurement rounds. The Algeria renewable energy market share for utilities will erode modestly as distributed systems proliferate; however, capacity additions will still favor utility-scale parks because grid access rules give priority dispatch to plants exceeding 1 MW.

The residential segment, though just 1.92% of the installed base, scales fastest as rooftop kits reach USD 0.65/Wp and payback periods fall below five years without subsidies. Islamic Green Sukuk, denominated in dinars and sold through state banks, finances up to 90% of the capital cost, thereby increasing household adoption. C&I customers, particularly those in the metals, fertilizer, and cement industries, sign direct bilateral PPAs to hedge future carbon-border adjustment costs. Several data centers under construction in Algiers and Oran plan to source 100% of electricity from on-site solar and contracted wind, signaling downstream diversification of the Algeria renewable energy industry.

Geography Analysis

The southern Saharan provinces host more than 70% of Algeria's renewable energy market capacity, as solar irradiation in this region exceeds 2,200 kWh/m²/yr. Ouargla and Adrar lead PV deployment, with the 220 MW Biskra and 80 MW Ouled Djellal plants expected to deliver commercial operation in 2025. High solar output in this region lowers hydrogen production costs at planned ammonia-to-Europe hubs.

Coastal wilayas, Oran, Mostaganem, and Tlemcen, concentrate 90% of wind resource mapping campaigns. Average wind speeds of 7.5 m/s at 100 m hub height justify 5 GW of planned onshore projects that will backfill nocturnal demand and feed the South H₂ export corridor, as per the BMWK. Repurposed subsea pipeline corridors offer pre-existing right-of-way for compressed-hydrogen trunklines, facilitating the integration of coastal wind farms into export value chains.

The High Plateau (Hauts Plateaux) provinces blend 1,900-2,000 kWh/m²/yr solar with rugged topography suitable for micro-wind and pumped storage. Grid limitations curb immediate build-out; yet, a USD 1.9 billion World Bank-backed transmission upgrade will connect these semi-arid zones to the North–South HVDC spine by 2028. Along the eastern borders, small hybrid PV-diesel projects support telecom towers and border-control posts, exemplifying niche off-grid applications.

Regulatory Landscape

Algeria's renewable energy framework is anchored by Law No. 04-09 (2004) on the promotion of renewable energy within sustainable development, alongside the sector operating framework under Law No. 02-01 (2002). The Ministry of Energy and Renewable Energies steers implementation of the national renewable energy program, while CREG (Commission de Regulation de l'Electricite et du Gaz) regulates the electricity and gas markets through licensing, grid-connection oversight, and related approvals, including guarantees of origin for photovoltaic installations. Recent procurement execution has included Sonelgaz signing contracts for 20 solar PV projects totaling 3 GW following tender rounds.

The investment environment has been adjusted to improve bankability and broaden foreign participation, supported by the 2022 Investment Law (Law 22-18) and the removal of foreign ownership restrictions previously capped under the 51/49 rule for renewable projects. At the same time, program implementation is increasingly tied to localization priorities, with policy focus shifting toward local content for infrastructure and components as Algeria scales deployments toward its stated 15 GW renewable capacity objective by 2035.

Competitive Landscape

Algeria’s renewable-energy vendor field remains moderately concentrated. The top five developers, Sonelgaz/SKTM, Masdar, Total Eren, three large Chinese EPC consortia, and Scatec Solar, controlled roughly 65% of the project pipeline MW in 2024.[5]Enerdata, “Algeria Energy Report,” enerdata.net State-backed SHAEMS selectively co-develops flagship sites while simultaneously tendering balance-of-plant packages, which spreads opportunity across mid-tier contractors.

Chinese firms, leveraging vertically integrated supply chains, offer PV EPC quotes 8-12% lower than those of European peers and have secured nine of the last 15 solar lots. European utilities differentiate themselves via premium bankability, advanced grid-forming inverters, and ESG reporting that aligns with EU green taxonomy rules. Wind’s steep 118.7% CAGR is inviting turbine OEM competition between Vestas, Siemens Gamesa, and Goldwind, each proposing local assembly options in Oran by 2027.

Battery storage emerges as a competitive sub-segment. Huawei Digital Power trials a 200 MWh BESS alongside the 300 MW Biskra solar farm, while Fluence advocates containerized blocks for northern substations. Niche Algerian firms, such as Condor Electronics, are pivoting toward BESS integration and rooftop PV retail. The SoutH₂ hydrogen corridor catalyzes new alliances: Cepsa-Sonatrach pursue methanol synthesis, and Eni-Sonatrach studies offshore CO₂ storage to qualify for EU CBAM exemptions.[6]Offshore Energy, “Cepsa and Sonatrach join forces …,” offshore-energy.biz Market entry barriers remain moderate, land acquisition remains centralized, but transparent auctions and removal of ownership caps improve accessibility and diversify the Algeria renewable energy market.

Algeria Renewable Energy Industry Leaders

SKTM Spa (Sonelgaz subsidiary)

Sonelgaz Renewables Holding

Zergoun Green Energy

Total Eren Algérie

Voltalia Algérie SpA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term whitespace is concentrated in utility-scale solar deployment tied to the government's multi-province buildout program, including a 3,200 MW plan across twelve provinces with project blocks commonly ranging from 80 MW to 220 MW. Sonelgaz's 2026 grid additions, including the inauguration of two solar plants adding 400 MW, point to an active delivery pipeline and create opportunities for EPCs, O&M providers, and grid-integration vendors that can execute multi-site programs under a single offtaker. Centralized procurement for large projects also supports more structured contracting and bankable deal structures across the value chain.

Industrial offtake-linked projects form a second opportunity lane where dedicated demand supports solar plus storage integration. The 200 MW Gara Djebilet project in Tindouf, advanced to support power iron ore mining infrastructure and incorporating a battery energy storage system (BESS), reflects growing interest in renewables-plus-storage for reliability in remote and industrial settings. In parallel, local manufacturing and technology upgrades, including domestic module production initiatives referenced in the market context, open space for partnerships that align project pipelines with localization goals, while storage and control systems become more relevant as variable renewables rise on a grid with known constraints in southern and border regions.

Recent Industry Developments

- July 2026: Sonelgaz reported continued execution of its utility-scale solar buildout with the 200 MW Nakhla solar PV plant under construction and slated for commissioning in 2026. The project adds visibility to the near-term capacity pipeline and reinforces Sonelgaz's central role in organizing multi-project delivery across the country.

- February 2025: Zergoun Green Energy initiated a capacity and technology upgrade at its Ouargla facility to produce TOPCon solar modules. This move supports Algeria's localization agenda and improves the domestic supply chain's ability to serve GW-scale PV tenders with higher-efficiency products.

- March 2024: Sonelgaz awarded 20 solar projects totaling 3 GW to local and foreign partners following tender rounds. The award round expanded the bankable project pipeline and increased the addressable market for EPC, balance-of-plant, and grid-connection services tied to utility procurement.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers Algeria's renewable electricity capacity in terms of installed gigawatts, counting grid connected and relevant distributed assets across major renewable technologies and end users.

Scope exclusions: Renewable transport fuels and stand alone renewable heat systems are excluded from this market sizing.

Segmentation Overview

- By Technology

- Solar Energy (PV and CSP)

- Wind Energy (Onshore and Offshore)

- Hydropower (Small, Large, PSH)

- Bioenergy

- Geothermal

- Ocean Energy (Tidal and Wave)

- By End-User

- Utilities

- Commercial and Industrial

- Residential

Data Sources, Market Sizing, and Validation

Desk Research

For desk research, we built the fact base on Algeria's power system and renewable buildout using public statistics and official disclosures. Typical inputs include IEA country power data, IRENA renewable capacity datasets, the World Bank development indicators, and statements from the energy ministry or national utility, which we used to anchor installed capacity by technology over time.

We then stress tested the storyline using procurement announcements, grid connection updates, and public budget statements, plus company filings, investor presentations, and credible press coverage. A paid news and financials subscription was used for timeline checks on major projects, and an import and export shipment-level database was applied selectively to sanity check equipment inflow trends for items such as PV modules and wind components. The examples listed above are not exhaustive, and additional public sources were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary inputs came from interviews and structured surveys with developers, EPC participants, equipment suppliers, grid and policy specialists, and large buyers from utility and C&I cohorts in Algeria. These discussions helped confirm what is commissioned versus only announced, typical lead times, curtailment risk, and practical utilization assumptions, and then we used those inputs to cross-check the desk research signals before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 16% | APAC: 45% |

| Mid tier: 48% | Functional/Unit leaders: 34% | EMEA: 36% |

| Smaller Players: 22% | Managers: 50% | Americas: 19% |

Market-Sizing & Forecasting

Sizing was built using top-down and bottom-up logic, where the top-down layer reconstructs installed renewable capacity by starting from national and international capacity time series and then aligning it with Algeria specific commissioning and retirement patterns. After that, the totals were corroborated through selective bottom-up approximations such as supplier and channel checks, sampled project pipelines, and sanity checks of typical MW blocks by technology.

To keep the model practical, we relied on a small set of fingerprints as key inputs, including annual capacity additions by technology, grid connection and evacuation readiness, tender award volumes versus slippage, local content and import dependency signals, and typical project cycle times that affect when MW actually lands in the base year. Where bottom-up visibility was incomplete for smaller builds, we used conservative adoption ratios that were validated in calls and then rolled into the top-down time series.

Forecasting relied mainly on scenario analysis, because policy execution speed and grid readiness can shift the timing of capacity additions even when targets look stable on paper. We used expert consensus from interviews to set base, slower, and faster commissioning paths, and then translated those paths into yearly GW additions that remain consistent with realistic procurement and construction capacity.

Data Validation & Update Cycle

Validation is done through multiple checks so the final output stays tied to real world buildout signals. Model results are compared against independent markers such as official capacity releases, visible project commissioning milestones, and equipment inflow direction, and then large variances are investigated before sign-off.

We also run consistency checks across years so sudden jumps are explained by identifiable events like major utility scale commissioning or a tender wave landing late. Reports are refreshed annually, and interim updates are made when material events occur such as major policy changes, large project cancellations, or unexpected grid constraints. Before delivery, an analyst performs a fresh pass on the key inputs so clients receive the latest updated view.

Mordor Intelligence's Algeria Renewable Energy Market Sizing Compared With Other Published Estimates

Published market sizes for Algeria renewable energy often do not match because the unit being measured and the counted activity are not the same across sources. Differences also show up when one publisher measures installed capacity, another tracks investments or revenue, and the forecast window is not aligned to the same base year.

Revenue from renewable electricity sales sits outside Mordor Intelligence's scope here, which keeps the estimate tied to installed capacity additions and commissioning timing rather than price and tariff assumptions. The spread also comes from how each study treats projects that are announced but not yet grid connected, how technology coverage is handled (for example, whether small systems are counted), and whether currency conversion and inflation assumptions are embedded in the headline number.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.23 B (2026) | |

| Regional Consultancy A | USD 1.50 B (2024) | This estimate is value based and can include revenue and investment flows, so it moves with tariff levels, financing costs, and currency timing rather than only commissioned GW. |

| Industry Publisher B | USD 15.20 B (2025) | The figure appears to bundle broad spending and development activity across renewables with limited visibility on what is already installed versus still in planning, which can inflate totals when pipelines are counted like commissioned assets. |

The table shows that unit selection and what gets counted as market activity are the main drivers behind the gap. By keeping the model traceable to installed capacity series, commissioning status, and practical timing checks from interviews, the results stay easier to reproduce and to reconcile with what is actually operating on the grid.

Key Questions Answered in the Report

How fast will renewable capacity expand in Algeria by 2031?

Installed capacity is projected to grow from 2.23 gigawatt in 2026 to 14.59 gigawatt by 2031 at a 45.60% CAGR.

Which technology adds the most new capacity?

Onshore wind posts the steepest rise, leaping from 52 MW to 5,010 MW, a 113.90% CAGR that challenges solar dominance.

What role do utilities play in procurement?

Utilities, led by Sonelgaz, still account for 81.70% of capacity but will cede share as residential and C&I segments accelerate.

How will Algeria export green hydrogen to Europe?

The 3,500-4,000 km SoutH₂ Corridor will repurpose gas pipelines, enabling over 1 million t/year of hydrogen exports after 2031.

What financing innovations support rooftop solar?

Islamic Green Sukuk offer dinar-denominated, Sharia-compliant instruments that cover up to 90% of household PV capex.

Which regulatory change most improved foreign investor access?

Article 139 of the 2021 Finance Law removed the 51/49 ownership cap, letting foreign IPPs take majority project stakes.

Page last updated on: