Aircraft Hydraulic Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

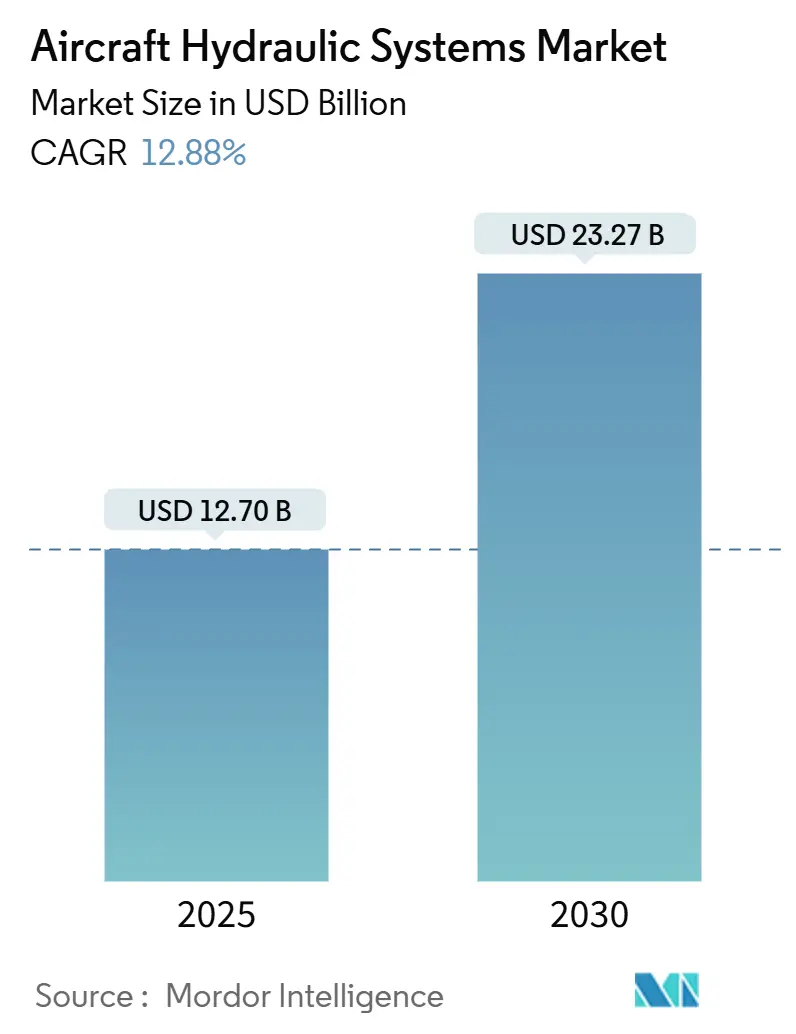

| Market Size (2025) | USD 12.70 Billion |

| Market Size (2030) | USD 23.27 Billion |

| Growth Rate (2025 - 2030) | 12.88% CAGR |

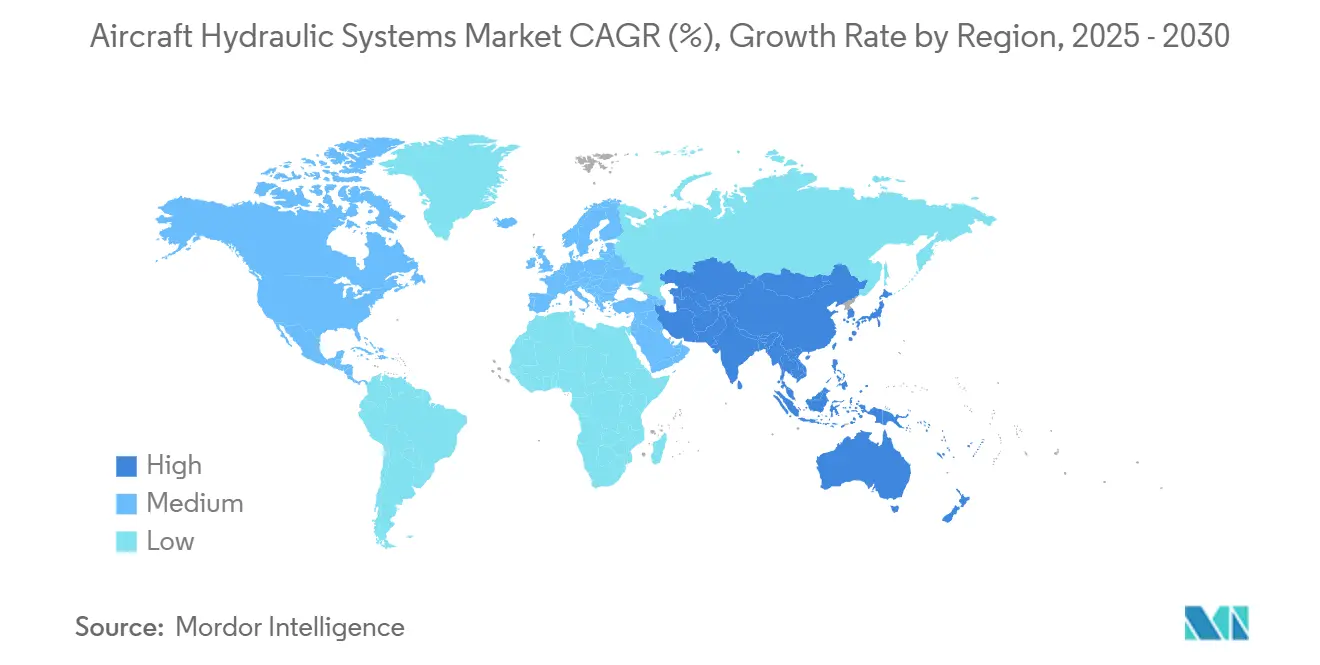

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Hydraulic Systems Market Analysis by Mordor Intelligence

The aircraft hydraulic systems market size reached USD 12.7 billion in 2025 and is forecasted to climb to USD 23.27 billion by 2030, translating into a 12.88% CAGR. Growth stems from accelerated fleet renewals, rapid certification timelines for Advanced Air Mobility (AAM) platforms, and the broader move to 5,000 psi-plus architectures that trim weight without sacrificing power. Long-term demand is further secured by regulatory mandates for fire-resistant phosphate ester fluids and by the hybrid-electric design trend, which preserves hydraulics for high-force functions even as other subsystems migrate to electricity. Asia-Pacific leads expansion on the back of aircraft manufacturing growth in China and India, while North America remains the most significant contributor thanks to entrenched OEM and defense programs. Component-level momentum is strongest in filters as operators lengthen maintenance intervals, and electro-hydrostatic actuators (EHA) are challenging centralized valve-controlled networks across new build designs.

Key Report Takeaways

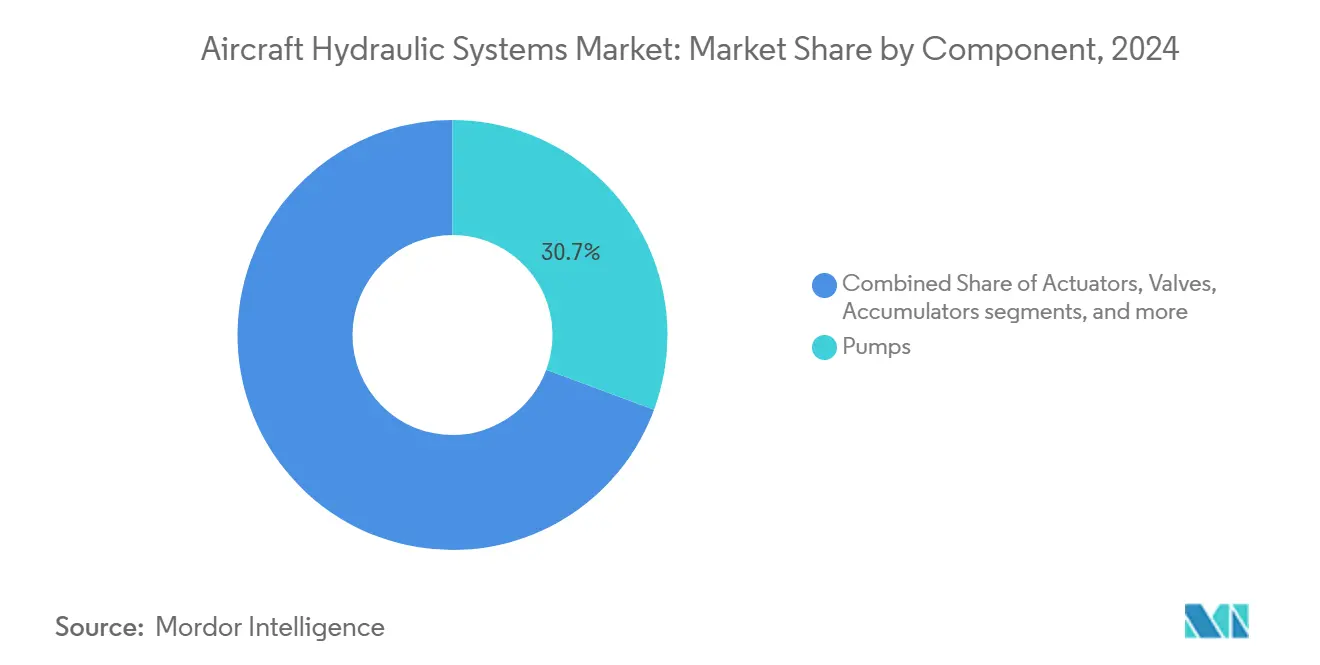

- By component, pumps held 30.65% of the aircraft hydraulic systems market share in 2024, whereas filters are projected to register the fastest 14.01% CAGR through 2030.

- By actuation technology, centralized valve-controlled hydraulics dominated with a 44.24% share in 2024, while the EHA segment is forecasted to advance at a 13.42% CAGR to 2030.

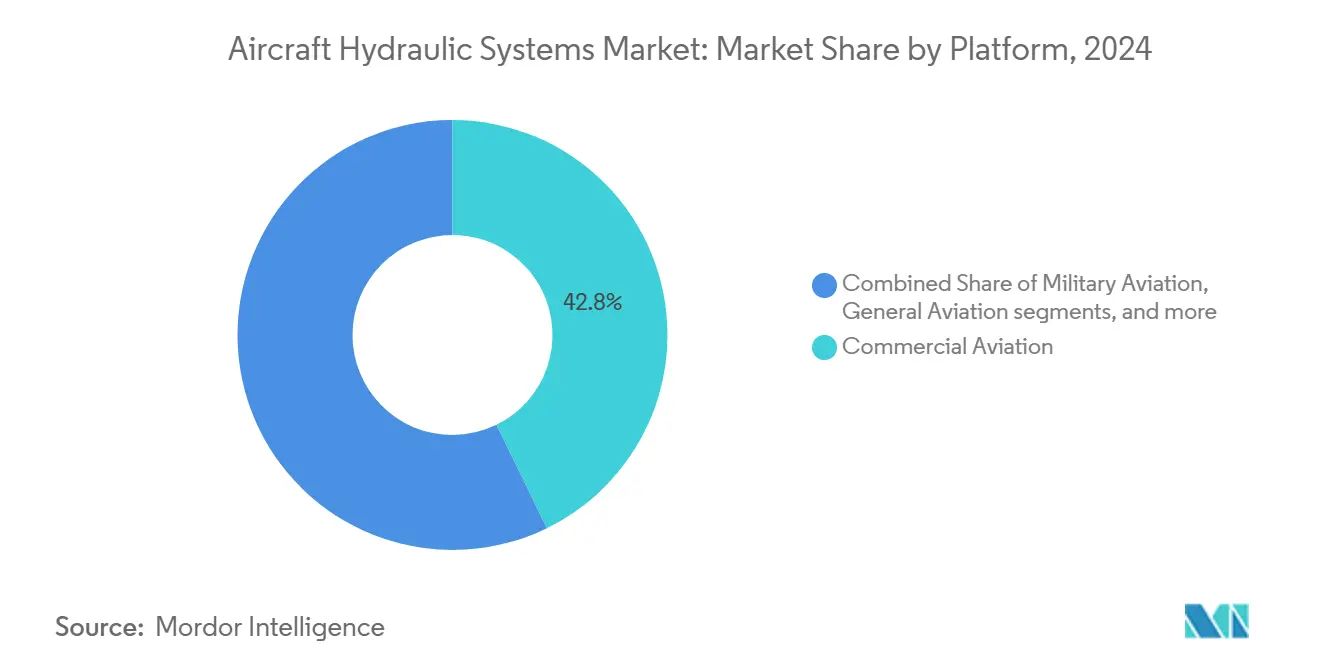

- By platform, commercial aviation led with 42.76% revenue share in 2024; AAM platforms are set to expand at a 13.23% CAGR during the outlook period.

- By fit, linefit installations accounted for 62.67% of the aircraft hydraulic systems market size in 2024, yet retrofit activities are pacing ahead at a 13.78% CAGR.

- By geography, North America retained a 31.75% share in 2024, and Asia-Pacific is projected to grow the fastest at a 14.55% CAGR to 2030.

Global Aircraft Hydraulic Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption of high-pressure hydraulic architectures | +2.3% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| Rising demand for hydraulic systems in eVTOLs and unmanned systems | +1.8% | North America and Asia-Pacific core, expanding to Europe | Short term (≤ 2 years) |

| Pump replacements driven by aging fleet renewal cycles | +1.5% | Global, concentrated in North America and Europe | Long term (≥ 4 years) |

| Increasing use of leak-free, quick-connect coupling technologies | +1.2% | Global, with MRO focus in Asia-Pacific | Medium term (2-4 years) |

| Growing adoption of fire-resistant phosphate-ester hydraulic fluids | +0.9% | Global, regulatory driven in North America and Europe | Short term (≤ 2 years) |

| Advancements in additive manufacturing for hydraulic manifolds | +0.8% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Adoption of High-Pressure Hydraulic Architectures

The shift to 5,000 psi and higher working pressures represents a decisive design change that lets OEMs reduce line diameter and component weight by up to one-third while preserving force capability. Aircraft like the B787 and A350 already demonstrate lower fuel burn attributable partly to these lighter hydraulics, reinforcing airline confidence in the technology.[1]Collins Aerospace, “Hydraulic Systems – Commercial Aviation,” collinsaerospace.com Digital pressure-monitoring units now feed real-time data to flight-control computers, allowing tighter tolerances and boosting dispatch reliability. As military transports seek payload gains and business jets chase range, retrofit kits offering high-pressure hoses, pumps, and accumulators have begun to circulate, enlarging the aftermarket slice of the aircraft hydraulic systems market. Over the medium term, high-pressure plumbing will also serve hybrid-electric architectures that need compact, high-force actuators for primary control surfaces.

Rising Demand for Hydraulic Systems in eVTOLs and Unmanned Systems

Despite electrification hype, prototype eVTOL aircraft rely on hydraulics for fail-safe redundancy, landing-gear operation, and high-authority flight controls. Hybrid layouts—electric primaries backed by hydraulic secondaries—dominate certification test plans as regulators insist on demonstrated safety margins. The projected urban air-taxi volume of 130 million passenger trips by 2029 translates to thousands of shipsets, each requiring micro-pumps, accumulators, and lightweight titanium manifolds. In the unmanned segment, heavy lift drones for logistics and military ISR missions specify hydraulics to handle payload winches and retractable sensor masts in dusty or saline environments. Consequently, AAM and unmanned systems programs act as a fresh growth stream that offsets partial substitution in conventional transport-category airplanes.

Pump Replacements Driven by Aging Fleet Renewal Cycles

Global fleets are flying longer as OEM delivery slots tighten, pushing average aircraft age into the mid-teens and lifting hydraulic-pump failure rates. Airlines that stretched retirements during the 2020-2023 downturn now face successive heavy checks, and pumps account for roughly 10% of total hydraulic maintenance expense. Military operators mirror the trend: legacy C-130, KC-135, and F-16 programs schedule pump swaps during structural upgrades to keep mission-capable rates above 80%. The aftermarket secures a dependable revenue floor for suppliers even as new-build volumes fluctuate, reinforcing the resilience of the aircraft hydraulic systems market.

Increasing Use of Leak-Free, Quick-Connect Coupling Technologies

Quick-connect couplings cut hose change labor by up to 40%, slash fluid spillage, and satisfy stricter environmental guidelines. Self-sealing valves isolate residual pressure, letting technicians disconnect lines without external bladders or drip trays. Because labor shortages challenge global MRO hubs, carriers value the reduced man-hours almost as much as the fluid savings. Fire-resistant phosphate-ester fluids accelerate seal-compatibility development, pushing providers to offer couplings with wider temperature and chemical envelopes. Adoption is fastest in Asia-Pacific maintenance bases that handle high-cycle narrowbody traffic, but retrofit programs are spreading to corporate jets and military rotorcraft.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward more-electric aircraft reducing hydraulic system usage | -1.4% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Extended maintenance intervals lowering hydraulic fluid consumption | -0.8% | Global, concentrated in commercial aviation | Medium term (2-4 years) |

| Regulatory push for PFOS-free hydraulic fluid formulations | -0.6% | North America and Europe, expanding globally | Short term (≤ 2 years) |

| Risk of thermal runaway in actuators during hot-soak conditions | -0.3% | Global, critical in hot-climate operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift Toward More-Electric Aircraft Reducing Hydraulic System Usage

MEAs such as the B787 and A350 showcase the removal of bleed-air-driven hydraulics in de-icing and cabin pressurization, trimming system weight, and maintenance. Electric linear actuators now govern spoilers and stabilizers on several narrowbody programs, signaling a gradual migration path. Yet primary flight controls and landing-gear functions continue to favor hydraulics for their power-density edge, so outright obsolescence is unlikely before the late 2030s.[2]National Aeronautics and Space Administration, “Evaluation of Novel eVTOL Aircraft Automation Concepts,” nasa.gov The result is a slow squeeze rather than a cliff, shaving points off long-range growth but leaving space for high-pressure hybrids.

Extended Maintenance Intervals Lowering Hydraulic Fluid Consumption

Condition-based monitoring coupled with superior filtration lets operators stretch fluid change cycles to 3,000–4,000 hours. While this reduces annual liter demand, it boosts filter cartridge sales and raises specifications for particle-count sensors. Defense fleets in sandy theaters still require shorter intervals, limiting overall impact; nonetheless, the net effect trims fluid revenue within the aircraft hydraulic systems market over the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Pumps Sustain Leadership While Filters Accelerate

Pumps generated 30.65% of 2024 revenue, anchoring the aircraft hydraulic systems market through indispensable power-generation duties. The market size for pumps in aircraft hydraulic systems is projected to increase in parallel with high-pressure conversion programs that mandate new motor-pump assemblies. Electric-motor-driven pumps, already standard on MEAs, now penetrate legacy fleets via retrofit kits that offer fuel savings by decoupling from engine gearboxes. Aftermarket service contracts covering seal swaps and bearing overhauls secure recurring income for Tier-1 suppliers, reinforcing pumps’ centrality despite electrification headwinds.

Though historically viewed as consumables, filters are forecast to outpace all other components at a 14.01% CAGR. Extended service intervals demand nanofiber media capable of trapping sub-5 µm particulates without pressure penalties, elevating average selling prices. Fire-resistant fluid adoption intensifies attention to acid-scavenging additives, leading airlines to procure higher-spec filters during base maintenance. Asian MRO houses increasingly stock multi-layer elements to match growing narrowbody traffic, ensuring filters remain the breakout component story in the aircraft hydraulic systems market.

By Actuation Technology: EHA Gains Traction Against Centralized Hydraulics

Centralized valve-controlled networks still commanded 44.24% revenue in 2024, benefiting from established certification data and mature supply chains. This architecture's aircraft hydraulic systems market share remains solid across single-aisle and regional jets, where operators favor proven maintenance playbooks. However, weight penalties tied to extensive plumbing create incremental fuel costs that airlines track closely, encouraging future programs to consider distributed options.

EHA solutions are advancing at a 13.42% CAGR on the promise of reduced line length, lower fluid volume, and inherent fault isolation. Each unit integrates a mini-pump, reservoir, and servo valve within the actuator body, allowing modular replacement and simplifying aircraft wiring diagrams. Early deployments on military fighters validate performance in high-G environments, and eVTOL prototypes rely almost exclusively on EHA for primary controls. As certification evidence amasses, EHA is poised to claim a larger slice of the aircraft hydraulic systems market across civil and defense programs.

By Platform: AAM Emerges as the Growth Catalyst

Commercial aviation retained a 42.76% leading share in 2024, fueled by narrowbody production ramps and sustained twin-aisle demand for global connectivity. High-pressure system retrofits on widebody fleets underscore the segment’s revenue durability. Nevertheless, orderbook cycles introduce volatility that encourages suppliers to diversify.

AAM vehicles, including lift-plus-cruise and tilt-rotor concepts, are expected to expand at a 13.23% CAGR. Each shipset typically includes multiple compact accumulators, fail-safe landing-gear actuators, and micro-valves sized for distributed electric propulsion layouts. Government incentives for regional air-mobility corridors bolster confidence among Tier-2 firms investing in clean-sheet hydraulic modules. Military and general aviation segments, supported by modernization budgets and business jet demand, grow steadily in parallel, ensuring the aircraft hydraulic systems market maintains a multi-platform balance.

By Fit: Retrofit Activity Accelerates on Aging Fleets

Linefit installations captured 62.67% of the 2024 value, propelled by OEM production lines where hydraulic kits arrive as fully kitted shipsets. Airframe backlog visibility allows suppliers to forecast material requirements accurately and optimize lot sizes.

Retrofit, though smaller, advances at a faster 13.78% CAGR as carriers tackle mid-life checks and performance upgrades. Quick-connect couplings and high-efficiency filters rank among the most popular retrofit items, delivering instant maintenance savings without disruptive airframe modifications. Defense depots also favor retrofit paths to align legacy fleets with NATO standardization updates, keeping demand elevated across the aircraft hydraulic systems industry.

Geography Analysis

North America represented 31.75% of global revenue in 2024, reflecting dense OEM footprints in Washington, Alabama, and Québec, plus robust US Department of Defense orders. The region also hosts the largest concentration of FAA-approved repair stations, guaranteeing a stable aftermarket for pumps, valves, and actuation spares. Electrification research funded by NASA spurs local EHA development, further anchoring the aircraft hydraulic systems market.

Asia-Pacific, forecasted to register a 14.55% CAGR, benefits from fleet-expansion commitments by Chinese and Indian carriers targeting underserved domestic routes. Joint ventures between Western Tier-1s and regional assemblers localize component production, allowing price-competitive bids on narrowbody work packages. Government-backed AAM test corridors in Japan and South Korea add incremental volume for microhydraulic solutions, reinforcing the region’s long-term pull.

Europe maintains momentum via Airbus final-assembly lines in Germany and France, plus multinational defense platforms like the Eurofighter and A400M. Environmental policies accelerate the adoption of leak-free couplings and PFOS-free fluids, pushing average component prices upward. Meanwhile, the Middle East and Africa leverage fleet renewal in Gulf carriers and modernization in North African air forces, whereas South America orders remain steady on regional jet replacements. Together, these dynamics ensure a broad geographic spread for the aircraft hydraulic systems market.

Competitive Landscape

The market features a moderate concentration, with Parker-Hannifin Corporation, Eaton Corporation plc, and Safran SA holding long-standing Type-Certificate credits that deter new entrants. Vertical integration—from pump design to MRO—lets incumbents bundle products with lifetime support agreements, locking in cash-flow visibility. Collins Aerospace recently secured long-term contracts covering high-pressure pumps and EHA shipsets for next-gen programs, underscoring OEM reliance on proven suppliers.[3]Collins Aerospace, “Hydraulic Systems – Commercial Aviation,” collinsaerospace.com

Strategic acquisitions shape the field: Eaton partnered with SIAEC to establish an Asia-Pacific hydraulic-component overhaul center, and Moog increased capital spending to scale additive-manufactured actuator housings. These moves address the proximity and lightweight design demands of airlines and eVTOL developers.

White-space competition revolves around thermal-management integration for hybrid-electric powertrains and predictive maintenance analytics tied to cloud platforms. Smaller firms such as Tactair Fluid Controls and Arkwin Industries differentiate through niche valves and accumulators formatted for tight fuselage bays. As program risk migrates from hardware to software, data integration capabilities will increasingly determine share shifts within the aircraft hydraulic systems market.

Aircraft Hydraulic Systems Industry Leaders

Parker-Hannifin Corporation

Eaton Corporation plc

Moog Inc.

Liebherr Group

Safran SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2023: SIA Engineering Company (SIAEC) and Eaton Corporation formed a joint venture for component maintenance, repair, and overhaul services. The partnership focuses on maintaining Eaton-manufactured aircraft components, specifically airframe, engine, fuel, and hydraulic systems.

- July 2022: Parker Aerospace, a business segment of Parker-Hannifin Corporation, signed a five-year performance-based logistics (PBL) contract with the Defense Logistics Agency and the US Air Force. The agreement covers hydraulic equipment for five Air Force platforms.

Global Aircraft Hydraulic Systems Market Report Scope

| Pumps |

| Actuators |

| Valves |

| Accumulators |

| Hoses, Pipes and Connectors |

| Filters |

| Hydraulic Fluid |

| Centralised Valve-Controlled Hydraulics |

| Electro-Hydrostatic Actuators (EHA) |

| Hydraulic-Powered Electro-Mechanical Hybrid (EHP) |

| Commercial Aviation | Narrowbody |

| Widebody | |

| Regional Jets | |

| Military Aviation | Combat |

| Transport | |

| Special Missions | |

| Helicopters | |

| General Aviation | Business Jets |

| Commercial Helicopters | |

| Unmanned Aerial Systems | Civil and Commercial |

| Defense and Government | |

| Advanced Air Mobility (AAM) | eVTOL |

| Urban Air Mobility (UAM) |

| Linefit |

| Retrofit |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Component | Pumps | ||

| Actuators | |||

| Valves | |||

| Accumulators | |||

| Hoses, Pipes and Connectors | |||

| Filters | |||

| Hydraulic Fluid | |||

| By Actuation Technology | Centralised Valve-Controlled Hydraulics | ||

| Electro-Hydrostatic Actuators (EHA) | |||

| Hydraulic-Powered Electro-Mechanical Hybrid (EHP) | |||

| By Platform | Commercial Aviation | Narrowbody | |

| Widebody | |||

| Regional Jets | |||

| Military Aviation | Combat | ||

| Transport | |||

| Special Missions | |||

| Helicopters | |||

| General Aviation | Business Jets | ||

| Commercial Helicopters | |||

| Unmanned Aerial Systems | Civil and Commercial | ||

| Defense and Government | |||

| Advanced Air Mobility (AAM) | eVTOL | ||

| Urban Air Mobility (UAM) | |||

| By Fit | Linefit | ||

| Retrofit | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the aircraft hydraulic systems market in 2030?

The aircraft hydraulic systems market is expected to reach USD 23.27 billion by 2030 based on a 12.88% CAGR.

Which component category will grow the fastest through 2030?

Filters are forecasted to expand at a 14.01% CAGR due to longer service intervals that require higher-performance contamination control.

How quickly will AAM platforms drive hydraulic demand?

Advanced Air Mobility (AAM) is projected to record a 13.23% CAGR, making it the highest growth platform segment within the forecast period.

Why do high-pressure architectures matter for operators?

Moving from 3,000 psi to 5,000 psi cuts component weight by up to one-third, improving payload and fuel efficiency for both new-build and retrofit aircraft.

Which region offers the strongest growth outlook?

Asia-Pacific leads with a 14.55% CAGR due to expanding commercial fleets and localized manufacturing investments.

Page last updated on: