Aircraft Landing Gear Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

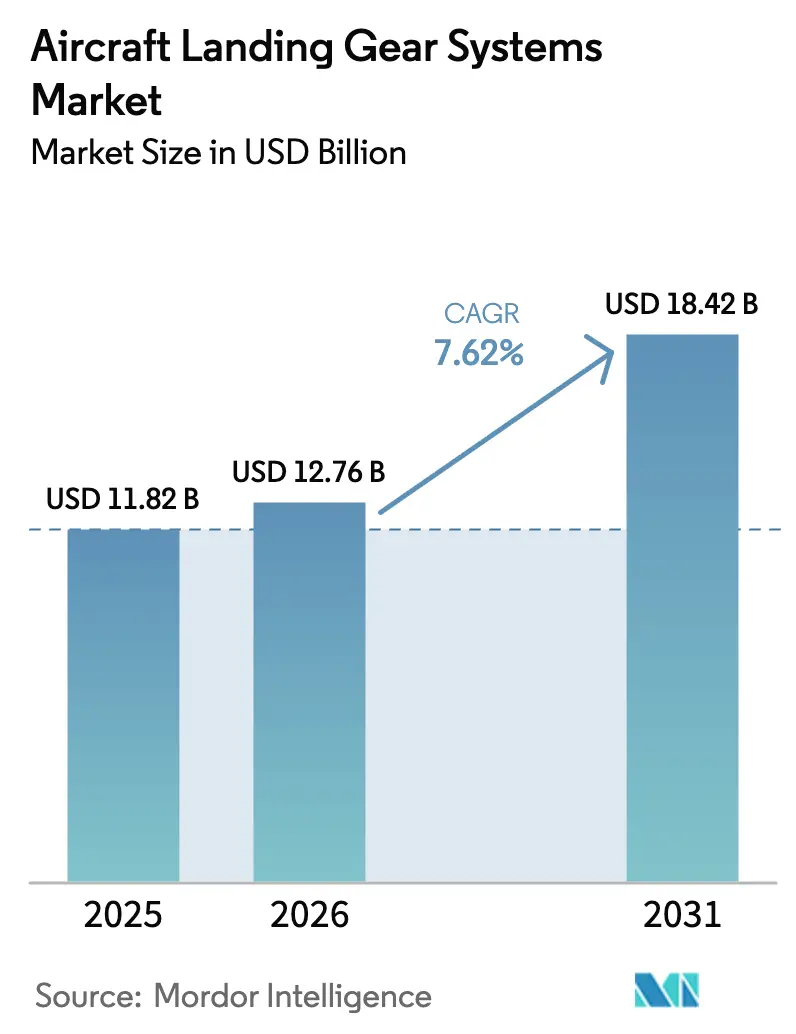

| Market Size (2026) | USD 12.76 Billion |

| Market Size (2031) | USD 18.42 Billion |

| Growth Rate (2026 - 2031) | 7.62% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Landing Gear Systems Market Analysis by Mordor Intelligence

The aircraft landing gear systems market size is expected to grow from USD 11.82 billion in 2025 to USD 12.76 billion in 2026 and is forecasted to reach USD 18.42 billion by 2031 at a 7.62% CAGR over 2026-2031. Composite struts, electromechanical actuation, and sensor-rich assemblies are transitioning from prototypes to high-rate production, providing suppliers with a path to premium pricing on narrow-body and military platforms. Demand is amplified by a production backlog exceeding 17,000 commercial jets, with Airbus and Boeing targeting a combined 1,200 single-aisle deliveries in 2026, each shipset valued at USD 1.5 million to USD 2.0 million. Defense programs add resiliency: F-35, F-15EX, and tanker replacements require ruggedized gear that tolerates rough-field operations and stealth-driven packaging constraints. Urban air mobility (UAM) platforms from Joby and Archer are expected to enter low-rate production in 2026, creating a niche for additive-manufactured titanium components that reduce lead times from 12 months to six weeks. Finally, digital-twin maintenance platforms, led by Safran, Collins, and Honeywell, reduce unscheduled removals by 25% and reshape aftermarket economics toward condition-based overhaul models.

Key Report Takeaways

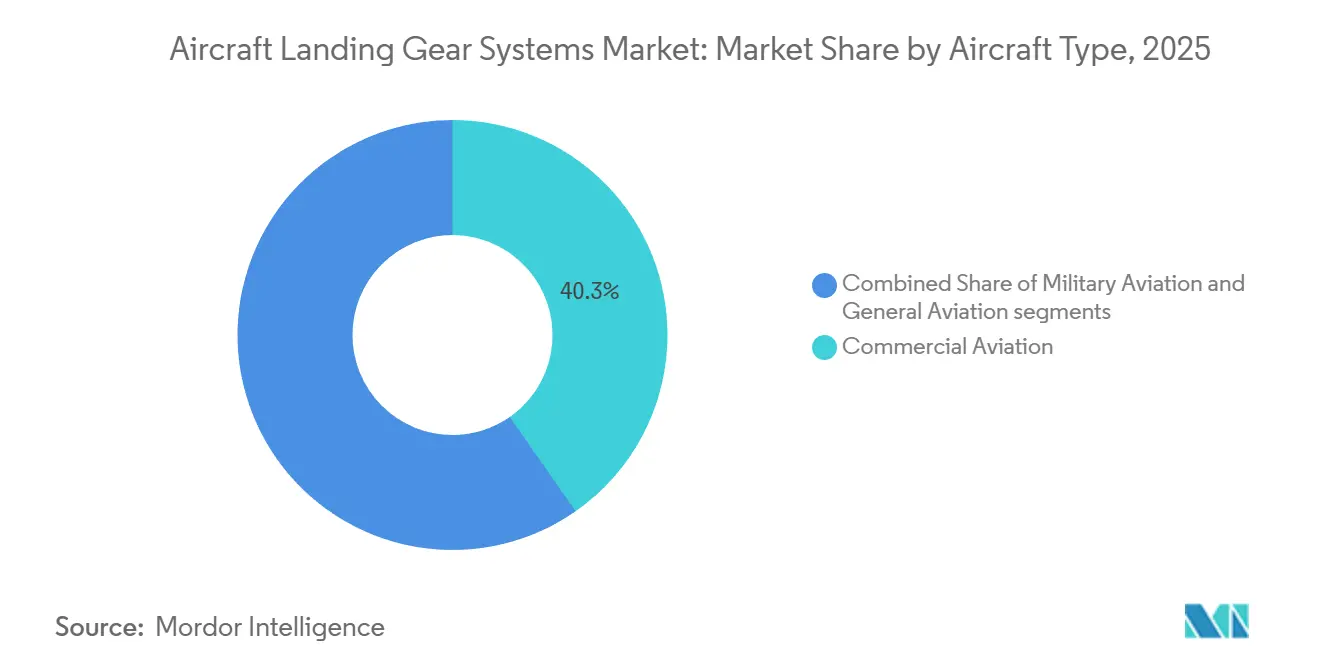

- By aircraft type, commercial aviation held 40.21% of the aircraft landing gear systems market share in 2025, while military aviation recorded the fastest growth at an 11.56% CAGR through 2031.

- By gear position, main assemblies commanded a 72.78% revenue share in 2025 and are projected to expand at a 10.43% CAGR through 2031.

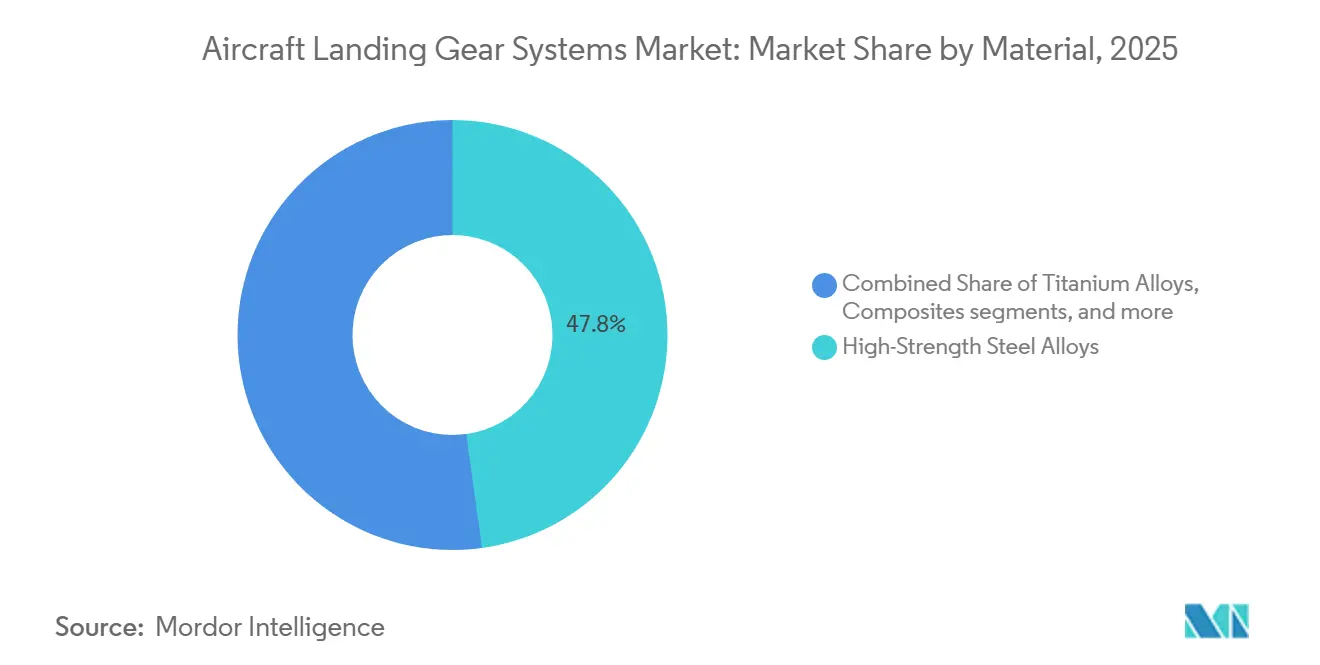

- By material, composites accounted for 13.76% of the aircraft landing gear systems market size in 2025 and are set to grow at a 13.76% CAGR between 2026 and 2031.

- By end user, OEM channels captured 63.65% revenue share in 2025, whereas the aftermarket segment is projected to post an 8.78% CAGR to 2031.

- By subsystems, the structural system commanded 43.67% of the aircraft landing gear systems market size in 2025, while actuation systems are growing at a 11.56% CAGR through 2031.

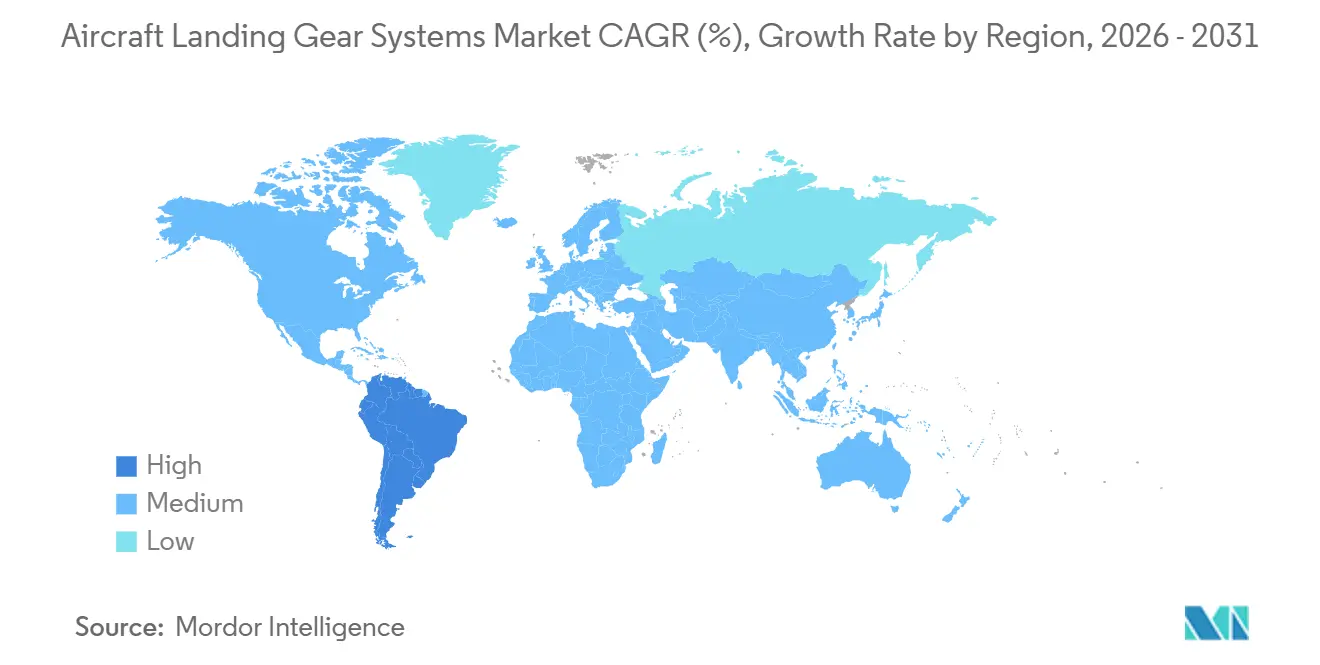

- By geography, Asia-Pacific led with a 34.56% share in 2025; South America is forecasted to register the highest 14.29% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Aircraft Landing Gear Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commercial aircraft production ramp-ups post-2025 | +2.10% | Global; concentrated in APAC and North America | Short term (≤ 2 years) |

| Lightweight-materials demand surge | +1.80% | Global; APAC; North America | Medium term (2–4 years) |

| OEM push for electric/hydraulic-free eBrake systems | +1.20% | North America & Europe; spillover to APAC | Long term (≥ 4 years) |

| Digital twin-enabled predictive maintenance | +1.00% | Global; early adoption in North America and Europe | Medium term (2–4 years) |

| MRO outsourcing and exchange-service adoption | +0.90% | Global; mature markets in North America and Europe | Medium term (2–4 years) |

| Urban air mobility (eVTOL/air-taxi) landing-gear volumes | +0.70% | North America; Europe; select APAC cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Commercial Aircraft Production Ramp-ups Post-2025

Airbus and Boeing aim for a combined 1,200 narrowbody deliveries in 2026, underpinned by firm orders from IndiGo, Southwest, and United Airlines. Each aircraft embeds landing-gear systems priced between USD 1.5 million and USD 2.0 million, locking in multi-year visibility. China’s COMAC C919 program is expected to add localized demand, with Liebherr delivering 100 shipsets by September 2024. However, titanium shortfalls and fuselage-quality defects at key Tier-1 suppliers trimmed Airbus’s 2025 target by 10 units, illustrating the fragility of the supply chain that cascades to gear makers.

Lightweight-materials Demand Surge

Airframers target 25% to 30% weight cuts in landing-gear assemblies to meet ICAO’s 2% annual carbon-intensity mandate. Cranfield University demonstrated a 30% mass saving when carbon-fiber struts replaced steel baselines during 50,000-cycle fatigue tests. Mitsubishi Heavy Industries applied resin-transfer molding to torque links and drag braces, resulting in a 20% reduction in recurring costs. Although titanium alloys cost four times more than steel, lifecycle fuel savings of USD 200,000 per widebody justify the premium. The shift strains supply chains because sanctions have removed Russian titanium sponge, forcing the qualification of Japanese and Kazakh alternatives that require an 18-month lead time.

OEM Push for Electric/hydraulic-free eBrake Systems

The B787 introduced electromechanical brakes in 2011, but fleet-wide adoption did not occur until Clean Aviation’s electric nose-gear trials delivered 15% weight and 20% maintenance savings in 2024. Airbus intends to retrofit eBrakes on A320neo derivatives entering service in 2027, while Boeing has a similar roadmap for the B737 MAX. Eliminating hydraulic pumps removes 50 pounds of fluid and plumbing, enhances dispatch reliability, and shifts value toward suppliers with power-electronics expertise. Eaton and Safran formed a USD 50 million joint venture to industrialize electric actuators by 2027.[1]“Eaton-Safran Electric Landing Gear JV,” Eaton Corporation, eaton.com

Digital Twin-Enabled Predictive Maintenance

Safran’s LifePulse, Collins’ Predictive Suite, and Honeywell Forge stream wheel speed, brake temperature, and strut strain data into cloud models that predict failures 30-60 days in advance. Early adopter airlines cut unscheduled removals by 25% and lengthened overhaul intervals by 15%. The practice fragments the aftermarket because carriers with in-house analytics bypass third-party shops, negotiating direct-repair agreements that reduce out-of-service time below 72 hours. Regulators have yet to harmonize data-validation standards, creating compliance gaps between FAA and EASA rules.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Titanium and composite supply-chain bottlenecks | -1.3% | Global; acute in Europe and North America | Short term (≤ 2 years) |

| Regulatory certification delays for novel architectures | -0.9% | Global; concentrated in North America and Europe | Medium term (2–4 years) |

| High capex and eight-to-ten-year overhaul costs | -0.6% | Global; more pronounced in emerging markets | Long term (≥ 4 years) |

| OEM–airline power-by-the-hour dominance squeezing independents | -0.5% | North America and Europe; spillover to APAC | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Titanium and Composite Supply-chain Bottlenecks

Sanctions removed 30% of global aerospace-grade titanium sponge, driving alloy prices from USD 35/kg in 2021 to USD 50/kg in 2024. Landing-gear shipsets for widebodies now cost USD 150,000 to USD 250,000 more, cutting OEM margins by up to 300 basis points. Composite output is also constrained: resin shortages linked to petrochemical outages have delayed Airbus A350 deliveries. At the same time, autoclave capacity caps CFRP strut output at 1,200 units per year, which is below industry demand. Only 12 forging houses own 40,000-ton presses, so any surge beyond 1,200 narrowbody units risks allocation shortages.

Regulatory Certification Delays for Novel Architectures

FAA and EASA mandate 1,500–2,000 flight-test hours for new landing-gear designs, and any failure restarts the clock, delaying revenue by 12–18 months and adding USD 20 million–USD 40 million in engineering costs. Clean Aviation’s eNLG demo remains in approval queues despite validated weight savings. Archer’s eVTOL slipped from 2025 to late 2026 after regulators demanded extra high-sink-rate tests. Divergent maintenance rules add complexity: The FAA allows condition-based overhaul, while the EASA still enforces calendar-based triggers, forcing airlines to manage dual maintenance programs.[2] “Special Condition for VTOL Aircraft,” European Union Aviation Safety Agency, easa.europa.eu

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Commercial Aircraft Dominate, Military Accelerates

Military programs posted an 11.56% CAGR to 2031, fueled by the F-35, F-15EX, and unmanned combat platforms requiring stealth-compatible gear that retracts flush with the fuselage.[3]“F-35 Lightning II Program,” Lockheed Martin, lockheedmartin.com The aircraft landing gear systems market size for combat fleets is projected to increase through 2031, driven by multi-decade sustainment budgets that schedule overhauls every 2,000 flight hours. Non-combat tankers and transports adopt civil-derivative gear to curb cost, yet still face 30% price uplifts for rough-field operation kits. Across Asia, Japan, India, and South Korea are inducting indigenous fighters that specify local content in landing-gear assemblies, diversifying the supplier map.

Commercial aviation remains the revenue anchor with a 40.21% share in 2025. Narrowbodies represent 75% of deliveries, averaging three daily cycles that accelerate brake wear and feed the aftermarket. Widebodies carry triple the mass per shipset, yet they grow in mid-single digits, because airlines prioritize fleet commonality over long-haul expansion. Regional jets and turboprops serve secondary-city routes in Latin America and Southeast Asia, necessitating reinforced gear for short, hot-and-high runways, which increases unit prices by USD 100,000 per aircraft.

By Gear Position: Main Gear Holds Mass, Nose Gear Innovates

Main landing-gear assemblies held a 72.78% revenue share in 2025 and are expected to advance at a 10.43% CAGR through 2031, as twin-aisle and heavy-lift military programs recover. A B777X main gear tips the scales at 12,000 pounds and sells for USD 2.5 million to USD 3.0 million, reflecting the use of six-wheel bogies and titanium forgings certified for 500,000-pound loads. Carbon-ceramic brake discs, costing USD 40,000-USD 60,000 each, require replacement every 2,500 landings, securing lucrative aftermarket streams that outstrip original equipment revenue by three-to-one across a 25-year life.

Nose gear's 27.22% share belies its strategic role in steering and anti-skid sensing. Clean Aviation's eNLG prototype reduced weight by 50 pounds by switching to electromechanical steering, thereby extending maintenance intervals to 12,000 hours. Composite struts are viable on narrow-body nose gear because loads represent only 15% of the aircraft's weight. However, eVTOL designs invert load maps, placing 60% of the load on the aft axles during ground operations, which requires adaptive dampers priced at nearly USD 100,000 per shipset.

By Material: Steels Still Rule, Composites Surge

High-strength steel alloys still account for 47.81% of 2025 shipments thanks to fatigue strength and cost advantages. Yet composites are set to expand at a 13.76% CAGR, as Airbus plans to use CFRP nose struts for the A320neo in 2027, delivering a 200-pound savings and a USD 40,000 annual fuel benefit. Hybrid architectures pair CFRP beams with steel torque links, striking a balance between weight and crashworthiness. Titanium maintains a roughly 30% share of the widebody and military primary gear market because it withstands salt-spray corrosion and absorbs high energy, although supply risks and 18-month lead times put pressure on margins.

Aluminum alloys retreat to general aviation niches where low load and cost sensitivity dominate. Additive-manufactured titanium struts, certified aboard Triumph-supplied F-15EX gear, cut material waste by 70% yet await volume scaling until regulators finalize batch-consistency rules.

By End User: OEM Share Solid, Aftermarket Momentum Builds

OEM channels accounted for 63.65% of 2025 revenue, aligning with the surging narrowbody output. Nevertheless, the aftermarket segment is gaining at an 8.78% CAGR. Fleet age averages 11 years; once aircraft cross 12–15 years, landing-gear overhauls climb from USD 400,000 to USD 600,000, lifting shop-visit income. Power-by-the-hour contracts now capture 40% of narrowbody aftermarket spending, shifting risk from airlines to OEMs while compressing margins for independent shops that cannot finance exchange pools. Data-rich predictive maintenance reduces MRO frequency but increases the value of each visit through more comprehensive refurbishment scopes.

By Sub-Systems: Electrification Drives Actuation Growth

Actuation systems are expanding at an 11.56% CAGR through 2031, the fastest pace among sub-systems. They are projected to surpass USD 2 billion in revenue by the end of the period, steadily lifting their contribution to the overall aircraft landing gear systems market size. The shift is propelled by electromechanical actuators that eliminate 50 pounds of hydraulic fluid per aircraft, extend inspection intervals from 8,000 to 12,000 flight hours, and deliver 15% weight savings validated by Clean Aviation’s electric-nose-gear trials completed in 2024.[4]“Electric Nose Landing Gear Project,” Clean Aviation, clean-aviation.eu FAA Advisory Circular 25-7D, issued the same year, codified certification criteria for electric actuation, unlocking wider adoption across the A320neo and B737 MAX families, which were scheduled for entry into service in 2027. Eaton and Safran formed a USD 50 million R&D joint venture in February 2024 to commercialize electric landing-gear actuators, aiming to capture a 20% share of the actuation-system aircraft landing gear systems market by 2031.

Structural systems retained the highest 43.67% revenue share in 2025, anchored in load-bearing components such as struts, torque links, drag braces, and axles, which account for more than half of the manufacturing cost due to titanium forgings and composite layups designed to absorb 500,000-pound vertical loads. Only 12 forging houses worldwide possess 40,000-ton presses needed for main-strut production, creating an 18-month lead-time bottleneck that concentrates pricing power among a handful of suppliers serving Safran, Collins, and Liebherr. Composite adoption remains limited to lower-weight regional jets and business aircraft due to fatigue-cycle exposure, with more than 50,000 takeoff–landing events over 20 years, which still favors steel and titanium on larger models.

Geography Analysis

The Asia-Pacific region owned 34.56% of the 2025 revenue, led by China and India. COMAC plans 150 C919 deliveries per year from 2028, and India’s 970-unit order pipeline will add USD 3.5 billion in landing-gear demand this decade. Regional connectivity initiatives under UDAN stimulate turboprop replacements, which require rough-field kits that cost 20% more than baseline systems. Japan supplies titanium forgings and composite struts for the B787 and A350 programs, maintaining high domestic plant utilization despite flat demand from local airlines.

South America is projected to deliver the fastest growth, with a 14.29% CAGR through 2031, primarily driven by Embraer’s E2 family and government subsidies for underserved routes. Brazil’s carriers are replacing their aging E1 jets with E2 variants, which feature composite torque links that extend overhaul intervals to 12,000 cycles. Chile, Peru, and Colombia invest in high-altitude airport upgrades that require reinforced gear, lifting per-unit value by up to 30%.

North America and Europe account for half of the global revenue, growing at mid-single digits. A 3,000-unit narrowbody backlog sustains OEM demand, yet supply constraints shift revenue into the aftermarket. EASA now allows condition-based maintenance for sensor-equipped assemblies, enabling Lufthansa and Air France-KLM to extend overhaul spacing, whereas the FAA retains a mixed approach. Middle East fleets are young and widebody-heavy, supporting premium gear sales but limited overhaul activity. Africa remains a nascent market; Ethiopian Airlines dominates capacity, and ruggedized kits for unpaved runways offer a small but strategic foothold.

Competitive Landscape

Safran SA, Collins Aerospace (RTX Corporation), and Liebherr Group control a significant portion of the global sales market. Safran manages over 1,000 exchange shipsets, promising a 24-hour turnaround that independents cannot match without a USD 300 million inventory. Collins cross-sells avionics and actuation, lowering integration costs and locking OEMs into bundled contracts. Liebherr secured a sole-source position on China’s C919 through a joint venture in Changsha, ensuring compliance with local content requirements.

White-space opportunities cluster around UAM and additive manufacturing. GKN and GE Additive supply 3D-printed titanium struts for Joby’s air taxi, cutting lead times from 12 months to six weeks. Independent MROs face shrinking margins, yet retrofit kits, such as carbon-ceramic brakes for 737NG fleets, offer a USD 700 million addressable niche. Data analytics firms like Uptake partner with regional shops to offer vendor-agnostic predictive maintenance, challenging OEM platforms.

Aircraft Landing Gear Systems Industry Leaders

Safran SA

Honeywell International Inc.

Collins Aerospace (RTX Corporation)

Liebherr Group

Héroux-Devtek Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Collins Aerospace and Emirates extended their long-term agreement to strengthen MRO support for the A380 main landing gear. The collaboration includes increased overhaul capacity through global MRO centers and on-site training to support uninterrupted fleet operations.

- October 2025: Southwest Research Institute has secured a seven-year, USD 9.90 million contract from the US Air Force under the Comprehensive Landing Gear Integrity Program. The contract aims to predict the lifespan of F-16 landing gear components and enhance maintenance practices.

- July 2025: Air Industries Group was awarded a USD 5.4 million contract by the US Air Force to provide landing gear steering collar components for B-52 aircraft. Deliveries are planned to commence in late 2026 and continue through the third quarter of 2027.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the aircraft landing gear systems market as the revenue earned from newly manufactured main and nose gear assemblies, together with their actuators, steering, braking, and structural sub-systems, installed on fixed-wing and rotary-wing aircraft across commercial, military, and general aviation segments.

We exclude retrofits carried out when older aircraft are converted for cargo or other specialty roles to keep double counting out of the baseline.

Segmentation Overview

- By Aircraft Type

- Commercial Aviation

- Narrowbody Aircraft

- Widebody Aircraft

- Regional Aircraft

- Military Aviation

- Combat Aircraft

- Non-Combat Aircraft

- Helicopters

- General Aviation

- Business Jets

- Turboprop Aircraft

- Piston Aircraft

- Helicopters

- Commercial Aviation

- By Gear Position

- Nose Landing Gear

- Main/Undercarriage Landing Gear

- By Material

- High-Strength Steel Alloys

- Titanium Alloys

- Composites (CFRP/GFRP)

- Aluminum Alloys

- By End User

- Original Equipment Manufacturer (OEM)

- Maintenance, Repair, and Overhaul (MRO)

- By Subsystem

- Actuation System

- Steering System

- Braking System

- Structural System

- Other Sub-Systems

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- France

- Germany

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Egypt

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed airline engineering heads, global MRO planners, defense procurement officers, and tier-one gear engineers across North America, Europe, Asia-Pacific, and the Middle East. Their guidance refined utilization rates, aftermarket mix, and composite penetration assumptions that underpin Mordor's model.

Desk Research

We began by compiling fleet and traffic statistics from public sources such as FAA Form 41 data, Eurocontrol registers, ICAO aircraft databanks, and the World Air Forces inventory. We then matched these with OEM delivery tallies and program notes found in SEC 10-K filings and EASA Type Certificate Data Sheets. Trade flows under HS-8803 codes from UN Comtrade, material-cost indices published by the U.S. Bureau of Labor Statistics, Questel patent trends on composite struts, and select records inside D&B Hoovers and Dow Jones Factiva added price, technology, and company context. This list is illustrative; many other repositories supported data collection, validation, and clarification.

Market-Sizing & Forecasting

A top-down build starts with annual aircraft deliveries, active fleet counts, and average bill-of-materials values. We then corroborate totals with sampled OEM contract disclosures, regional MRO invoices, and channel checks to adjust for price tiers and platform mix. Key variables include flight-hour growth, scheduled retirements, titanium and carbon-fiber cost indices, defense budget outlooks, and composite share in main-gear beams. Multivariate regression, informed by GDP-weighted passenger-kilometer forecasts and expert consensus, projects demand to 2030. Where bottom-up gaps appear, we apply region-specific unit-price factors drawn from primary interviews.

Data Validation & Update Cycle

Outputs undergo variance screens against historic ratios, aftermarket billings, and airline capex signals. Anomalies are reviewed by senior analysts before sign-off. Reports refresh each year, with interim updates triggered when OEM production rates, regulations, or macro shocks materially shift the baseline.

Why Our Aircraft Landing Gear Systems Baseline Earns Trust

Published estimates often diverge because providers pick different component scopes, currency bases, and refresh cadences.

By anchoring results to reconciled delivery counts, verified trade data, and on-ground interviews, Mordor Intelligence offers a balanced midpoint decision-makers can rely on.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 11.82 B (2025) | Mordor Intelligence | - |

| USD 13.02 B (2024) | Global Consultancy A | Captures full wheel-and-brake aftermarket and applies one blended price across all aircraft platforms |

| USD 6.84 B (2024) | Industry Association B | Omits military rotorcraft and values sales at prior-year exchange rates |

Takeaway: Results swing widely when scope widens or narrows; our disciplined variables, annual refresh, and dual-path validation deliver the most transparent, repeatable baseline for strategic planning.

Key Questions Answered in the Report

What is the 2026 size of the aircraft landing gear systems market and its expected CAGR through 2031?

The aircraft landing gear systems market size is USD 12.76 billion in 2026 and is projected to reach USD 18.42 billion by 2031, reflecting a 7.62% CAGR over the forecast period.

Which sub-system category is forecast to expand the quickest by 2031?

Actuation systems lead with an 11.56% CAGR thanks to rapid adoption of electromechanical actuators.

Why are electromechanical actuators overtaking hydraulic units?

They remove 50 pounds of fluid, cut maintenance intervals from 8,000 to 12,000 flight hours, and deliver 15% weight savings validated in 2024 trials.

Which region is expected to log the highest growth to 2031?

South America posts a 14.29% CAGR, outperforming all other geographies on the back of Embraer E2 deliveries and regional-connectivity programs.

How do composite materials influence landing-gear weight and upkeep costs?

Carbon-fiber struts trim up to 30% mass and can lower lifetime fuel burn by roughly USD 200,000 per widebody while extending overhaul intervals.

Who currently controls the largest share of global revenue?

Safran Landing Systems, Collins Aerospace, and Liebherr together account for a significant share of global revenue.

In what way does predictive maintenance reduce unscheduled removals?

Sensor-rich digital twins warn of failures 30–60 days early, allowing airlines to cut unexpected gear removals by around 25%.

Page last updated on: