Aircraft Cargo Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

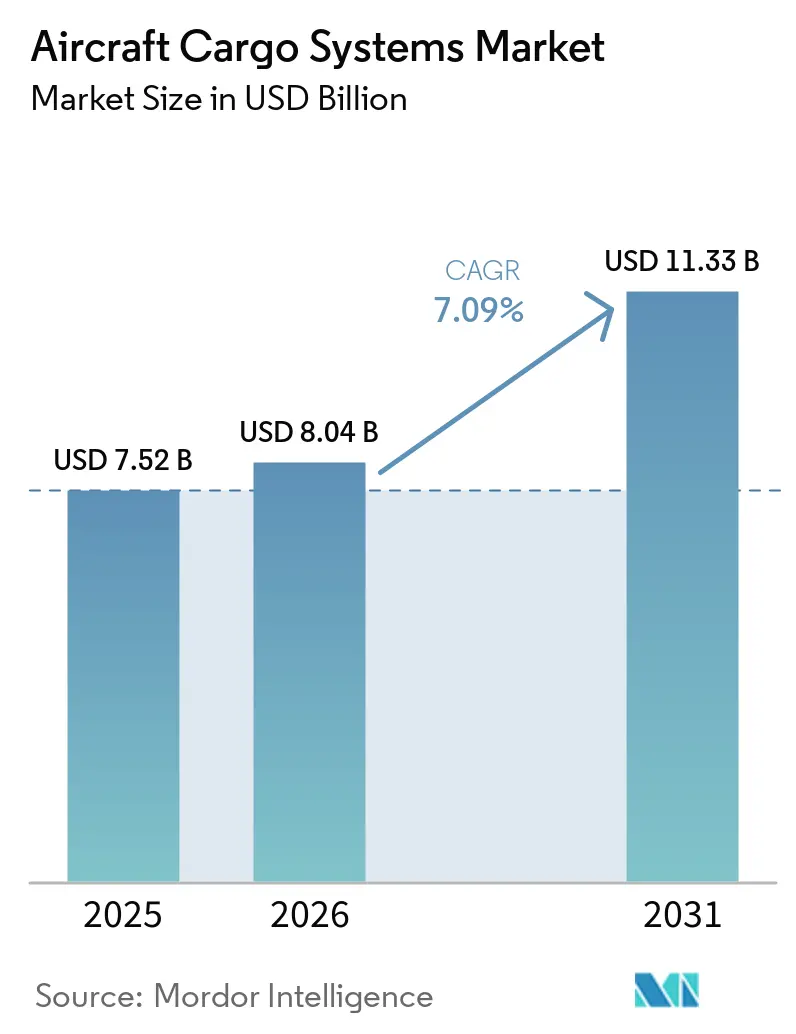

| Market Size (2026) | USD 8.04 Billion |

| Market Size (2031) | USD 11.33 Billion |

| Growth Rate (2026 - 2031) | 7.09% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Cargo Systems Market Analysis by Mordor Intelligence

The aircraft cargo systems market size is expected to grow from USD 7.52 billion in 2025 to USD 8.04 billion in 2026 and is forecasted to reach USD 11.33 billion by 2031 at a 7.09% CAGR over 2026-2031. Global momentum is supported by cross-border e-commerce that demands time-definite logistics, a strong pipeline of passenger-to-freighter conversions, and sustained defense modernization across NATO and Asia-Pacific that prioritizes rapid-deploy airlift. Air cargo demand reached record volumes in 2025, with Asia–Europe lanes leading the recovery as carriers shifted capacity to corridors that absorbed e-commerce flows after changes to de minimis in the United States. Fleet growth prospects remain constructive as freighter conversions supplement limited new-build slots, while next-generation narrowbody and widebody P2F programs align with carriers’ needs to flex capacity with demand. The aircraft cargo systems market also benefits from a steady shift toward lighter electromechanical actuation and software-enabled diagnostics, which reduce maintenance events and support more reliable, on-time performance. These factors together underpin durable system spend across new installations and retrofit programs, even as supply-side constraints delay some aircraft deliveries.

Key Report Takeaways

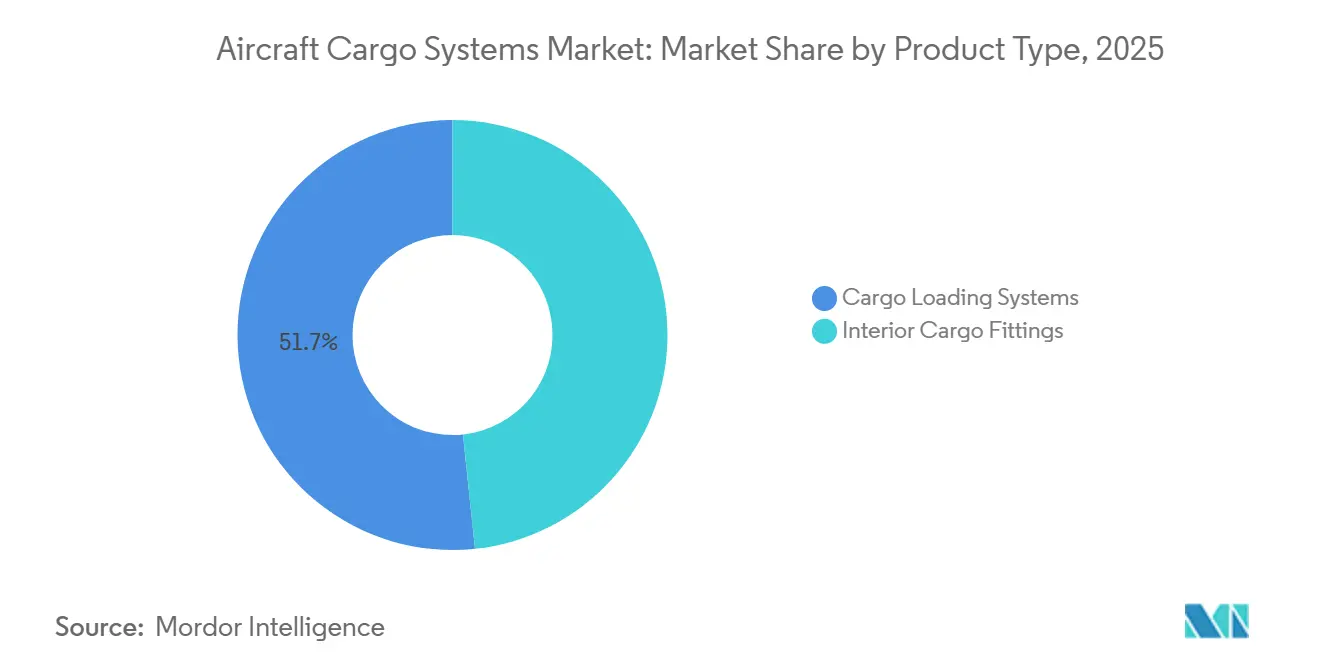

- By product type, cargo loading systems led the aircraft cargo systems market with a 51.67% revenue share in 2025 and are forecasted to grow at a 7.76% CAGR through 2031.

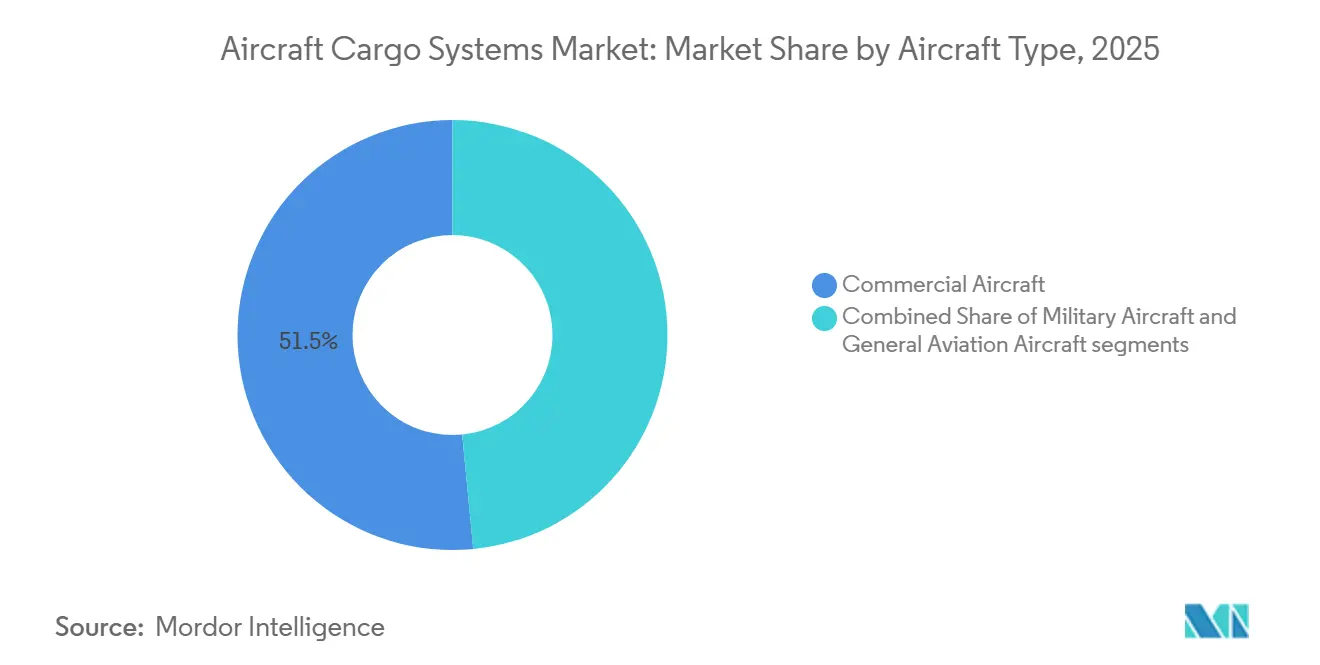

- By aircraft type, commercial aircraft held a 51.54% share of the aircraft cargo systems market in 2025, while military aircraft is projected to expand at the fastest 7.64% CAGR to 2031.

- By end user, the aftermarket segment accounted for 38.48% of 2025 revenue and is set to grow at a 7.28% CAGR through 2031.

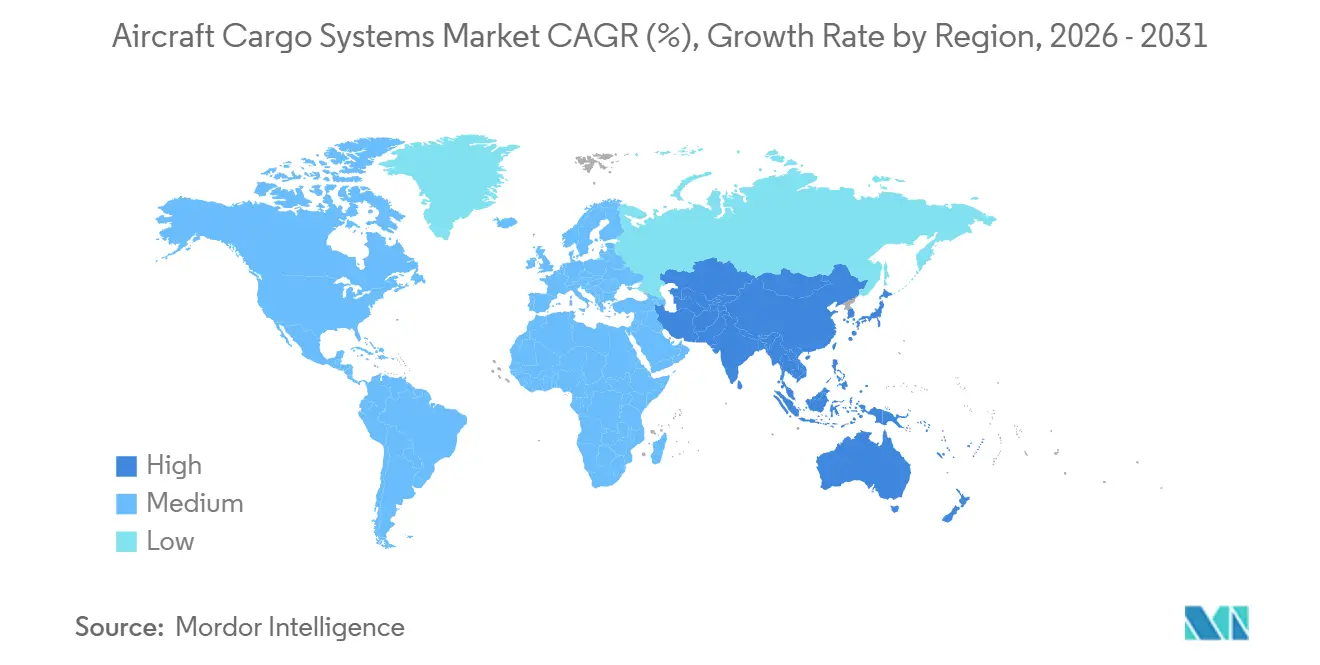

- By geography, North America held a 42.53% share in 2025, while Asia-Pacific is expected to record the fastest CAGR of 7.32% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Aircraft Cargo Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of cross-border e-commerce requiring time-definite air cargo | +2.1% | Global, driven by Asia-Europe and intra-Asia corridors, North America experiencing shifts | Short term (≤ 2 years) |

| Surge in dedicated freighter conversions | +1.2% | Global, with particular strength in North America, Asia-Pacific, and Europe | Medium term (2-4 years) |

| Rising defense spending on rapid-deploy logistics aircraft | +0.9% | North America, Europe, Middle East, Asia-Pacific | Long term (≥ 4 years) |

| OEM shift toward lighter, electric floor-actuated systems | +0.7% | Global, earlier adoption in North America and Europe | Long term (≥ 4 years) |

| AI-enabled predictive maintenance reducing AOG time | +0.6% | Global, led by large carriers in North America, Europe, Middle East | Medium term (2-4 years) |

| Formation of cargo-focused eVTOL/UAV ecosystems | +0.5% | Initial presence in North America, China, Europe, Middle East, expanding to India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Dedicated Freighter Conversions

Conversion activity strengthened in 2025 as airlines sought to cover capacity gaps caused by delays in new-build freighter deliveries into the late 2020s. Operators and integrators pivoted to B737-800BCF and A321P2F programs on narrowbody routes and to B777-300ER-based programs on high-density lanes, concentrating demand for cargo-loading hardware and interior fittings. Regulatory and supply-chain timing remains the gating factor as several large widebody STCs target 2026 decisions and long-lead items stretch conversion calendars. Feedstock economics also tightened as lease extensions reduced the number of aircraft available for part-out, raising airframe prices and requiring closer route-level planning. With widebody production slots constrained and the B777F covering the large freighter role in the near term, conversions are underpinning system retrofits and upgrades across fleets.[1]Grant Holve, “Supply Chain Challenges Limit A350 Production to Six Aircraft Per Month, A350F Deliveries Delayed to 2027,” Forecast International Flight Plan, forecastinternational.com

Growth of Cross-Border E-Commerce Requiring Time-Definite Air Cargo

E-commerce dynamics accelerated air cargo's role as retailers and platforms sought reliable 24–48 hour delivery windows across long-haul corridors. After policy changes in the US reshaped flows from China in mid-2025, capacity and inventory shifted into Europe-bound channels, where carriers reported higher load factors on Asia–Europe lanes. IATA tracked a strong rebound in 2025 cargo traffic on Europe–Asia routes, reflecting airlines' agility in redeploying freighters to demand hotspots. European policy adjustments planned for 2026 on low-value shipments are set to raise compliance emphasis, which supports consolidated air moves that favor speed and traceability. Carriers and airports are extending digital and tracking investments that compress processing timelines, allowing air networks to hold service levels while volumes normalize along new trade lanes.[2]International Air Transport Association, “Global Air Cargo Demand Achieved Record Volume in 2025,” IATA, iata.org

Rising Defense Spending on Rapid-Deploy Logistics Aircraft

Defense budgets in 2026 prioritize resilient airlift and sustainment, supporting recurring demand for cargo systems that increase aircraft availability and mission flexibility. European and North American fleets continue to upgrade platforms such as the A400M and C-130J for tactical and strategic roles, driving the need for standardized pallets, advanced restraint systems, and ruggedized loading hardware. Airlift utilization remains elevated, sustaining maintenance and retrofit cycles for cargo floors, rollers, and fire suppression systems across heavy transports. New procurement in Europe includes additional medium and heavy transports that align with interoperability standards, helping mixed fleets operate from short or semi-prepared runways. These missions require reliable, modular cargo systems that integrate with modern avionics and communications, reinforcing steady demand for both OEM linefit and aftermarket support.[3]John Hill, “Airbus Allude to ‘Uncertainties’ in Future Orders of A400M,” Airforce Technology, airforce-technology.com

OEM Shift Toward Lighter, Electric Floor-Actuated Systems

Airframers and system integrators are moving cargo actuation and restraint components toward lighter electromechanical designs to reduce weight and simplify service. This shift complements broader efficiency targets seen in new-build freighters with lower fuel burn per tonne-kilometer and tighter CO₂ standards. Lightweight composite floors and nets are increasingly paired with electric actuators and digital monitoring to improve reliability and enable predictive maintenance workflows. The approach aligns with planned next-generation widebodies that emphasize improved payload-range economics, encouraging airlines to specify higher-value cargo systems at line fit. Suppliers also link these platforms to diagnostics that feed maintenance scheduling, enabling carriers to keep aircraft on the line longer between interventions.[4]Airbus Communications, “World Freighter Fleet to Grow 45% by 2044,” Airbus, airbus.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile jet-fuel prices compressing airline margins | -1.4% | Global, with sharper impact in Europe and North America | Short term (≤ 2 years) |

| Limited widebody production slots through 2030 | -1.1% | Global, with pronounced effects for Europe and North America | Long term (≥ 4 years) |

| Lengthy certification cycles for new cargo hardware | -0.9% | Global, primarily FAA and EASA jurisdictions | Medium term (2-4 years) |

| High up-front retrofit CAPEX for legacy fleets | -0.6% | Global, with higher impact in Asia-Pacific, Latin America, and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Jet-Fuel Prices Compressing Airline Margins

Jet fuel prices rose sharply through early 2026, putting pressure on airline and freighter operating margins and narrowing the room for discretionary retrofit spending. Route adjustments around conflict zones add miles to many long-haul charts, increasing consumption and reducing effective capacity on key corridors. Regulatory carbon programs and the introduction of sustainable aviation fuel raise carriers' average fuel bills, keeping cost pressure elevated even if spot prices ease from their peaks. IATA has outlined higher compliance and sustainability costs during 2024 and 2025, which remain relevant as more routes fall under the scheme in 2026. These fuel and compliance dynamics prompt carriers to pace capital projects and to prioritize upgrades that deliver faster payback in reliability and turnaround time.

Limited Widebody Production Slots Through 2030

Production delays for new widebody freighters and constrained engine and structural component timelines have limited near-term slot availability. With some large freighter entries pushed out by OEMs, carriers depend on the B777F to serve the highest-payload missions and fill the gap while awaiting next-generation models. Narrowbody ramp constraints and retrofit campaigns for engine fleets further slow delivery normalization, which tightens overall feedstock for conversion. These constraints spill over into the used-aircraft market, elevating pricing for conversion candidates and raising the bar for route economics. Industry tracking showed ambitious ramp targets slipping to the right, with airframers and suppliers prioritizing quality and stability over volume as they rebuild rate confidence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Loading Systems Command Fleet-Wide Mandates

Cargo loading systems captured 51.67% share in 2025 and are projected to grow at 7.76% CAGR through 2031, reflecting fleet-wide priorities to modernize roller tracks, ball mats, and locking mechanisms for standardized ULD handling. This segment benefits from the conversion wave as airlines specify quick-change configurations that compress downtime and support flexible scheduling during demand spikes. Interior cargo fittings at 48.33% share address stringent fire safety and thermal control requirements, particularly in pharmaceutical and high-value shipments. Temperature-controlled modules, liner upgrades, and compliant fire detection support consistent service levels on long-haul missions. Standardization in pallet and container handling reduces ramp time and improves turn performance, which carriers translate into higher aircraft utilization on busy corridors. Digital monitoring and weight-and-balance analytics flow into line operations to improve compliance and reduce manual error in high-velocity hubs.

The aircraft cargo systems market continues to see a progressive shift toward electric actuation and composite components, enabling lighter floors, nets, and cargo doors. Airlines are also introducing RFID and sensor-enabled hardware that feeds maintenance and inventory data into unified control towers. Certification frameworks for cargo compartments and liners drive rolling upgrade cycles, including for B737-800BCF and A321P2F fleets in commercial service. Operators route capital to cargo subsystems that deliver cost savings with faster turns and fewer maintenance events rather than aesthetic cabin upgrades. Interoperability with ground equipment remains a critical selection criterion for carriers operating mixed fleets across multiple hubs. IATA CEIV standards and airworthiness directives shape procurement checklists, which raise the technical bar for linefit and retrofit solutions.

By Aircraft Type: Military Aircraft Surge Outpaces Commercial Aircraft Base

Commercial aircraft captured 51.54% of the aircraft cargo systems market share in 2025. Installed B777F, B767-300BCF, and A330-300P2F fleets to support long-haul lanes with nonstop operations that cut transit times versus multi-leg routings. Conversion activity rebounded in 2025 as integrators filled gaps created by new build delays, positioning converted narrowbodies and widebodies as the economic backbone of regional and trunk networks. Boeing projects the global freighter fleet to reach 3,900 aircraft by 2043, with about two-thirds of those being passenger-to-freighter conversions. Airbus forecasts a 45% rise in the dedicated freighter fleet to 3,420 by 2044, reinforcing long-term cargo system demand. ICAO 2027 CO2 standards are shaping new product choices, and Cathay Cargo has selected the A350F for 2027 deliveries with a lower fuel burn profile that supports premium service economics.

Military aircraft are the fastest-growing segment, with a 7.64% CAGR in the aircraft cargo systems market through 2031. Growth reflects elevated defense outlays and modernization programs that replace aging transports and lift demand for cargo floors, restraint systems, and fire protection, thereby raising mission availability. Interoperable load equipment and standardized pallet systems enable joint operations across allied fleets and support higher tempo logistics across North America, Europe, and the Asia Pacific. General aviation, which includes cargo eVTOL and UAV platforms and regional aircraft, holds the remaining 48.46% share of the aircraft cargo systems market, and AIR’s first production-ready Air One Cargo delivery in December 2025 illustrates focused last-mile use cases where large aircraft cannot land.

By End User: Aftermarket Cycles Intensify as Fleets Age

The aftermarket accounted for 38.48% of 2025 revenue and is projected to post the fastest CAGR of 7.28% through 2031 as carriers extend the life of maturing fleets. Longer time on wing and conversion-driven utilization keep systems under higher cycle stress, which expands demand for cargo floor, roller track, and liner replacements. Predictive maintenance adoption is reshaping scheduling by pushing planned interventions into shoulder seasons and reducing aircraft-on-ground exposure. Operators prioritize parts that deliver availability gains and shorten aircraft turns for those that cycle multiple rotations per day. Heavy-check throughput is elevated, which supports recurring orders for mission-critical cargo components in widebodies and freighters. This dynamic positions integrated suppliers and MROs to capture larger bundles of line-replaceable units within each visit.

OEM linefit installations, at 61.52% in 2025, remain substantial but grow more slowly, given constrained aircraft deliveries through the middle of the decade. New-build freighter programs will normalize in the later forecast years, which supports a higher base level of linefit business for large suppliers. In the near term, many airlines are channeling spend into upgrades that bring older aircraft closer to the performance of newer freighters. This pattern sustains service contracts across commercial and military transports that require periodic refresh cycles for cargo floors, restraints, and fire suppression. As fleets adopt lighter components and digital monitoring, suppliers are bundling hardware and software to provide lifecycle value. These shifts favor suppliers that offer end-to-end solutions and certified retrofit kits for large installed bases across platforms in service.

Geography Analysis

North America led with 42.53% in 2025 as carriers and defense programs sustained high utilization and steady upgrade cycles. The aircraft cargo systems market size in North America reflects consistent investment in system reliability, standardized pallets, and safer cargo compartments on tactical and strategic platforms. Conversion and MRO ecosystems remain strong across the US and Canada, where qualified labor and familiarity with certifications support throughput. Drone and eVTOL pilots continued to expand in 2026 as regulators incrementally opened pathways for beyond-visual-line-of-sight (BVLOS) operations within controlled areas. Commercial freighter networks focused on express and e-commerce lanes, with system upgrades to improve turnaround and reliability. Defense sustainment budgets in the region are broad-based and support floor, restraint, and liner workscopes on transports operating in austere environments.

Asia-Pacific is the fastest-growing region, with a 7.32% CAGR, and benefits from e-commerce scale, conversion capacity, and expanding defense fleets. Converted narrowbodies support dense intra-Asia networks, while larger widebodies handle trunk routes into Europe and the Middle East. Cargo drone adoption advanced with certified platforms entering service in China in 2025, which opened new use cases in urban delivery and remote logistics. Regional MRO and conversion activity continued to grow, extending local capacity to handle package-specific roller and restraint upgrades. Governments and airports focused on digital cargo processes, which accelerated cycle times at major gateways. As carriers add capacity and diversify routes, they specify lighter and smarter cargo systems to balance fuel efficiency with service reliability.

Europe maintains a significant share supported by e-commerce hubs, express integrators, and defense rearmament that reinforces transport aircraft fleets. Major cargo airports invested in automation and digital traceability, which lifted throughput under stricter compliance regimes. Procurement of tactical and strategic airlift, including medium transports, has kept supplier order books active for palletization, restraints, and fire safety systems. Certification complexity across European jurisdictions continues to extend timelines for new systems, which shapes rollout calendars for advanced actuation and monitoring. OEMs remain a focus for airlines planning replacement cycles. Europe’s structure of mixed fleets across consortium programs also sustains steady retrofit demand through the forecast period.

Competitive Landscape

The aircraft cargo systems market is moderately concentrated, with large system integrators and avionics suppliers shaping specifications across the OEM and retrofit channels. Leading suppliers such as Telair International GmbH, Collins Aerospace (RTX Corporation), Safran SA, Ancra International, LLC, and U.S. Cargo Systems deliver cargo loading hardware, restraint systems, actuators, and liner technologies that meet evolving safety and efficiency requirements. The top tier competes on certified product breadth, integration capability, and global support networks that align with airline and airframer programs. Digital enablement and lighter materials are primary levers, as airlines seek measurable gains in turn time, reliability, and weight. With delivery slots for widebodies tight, retrofit roadmaps remain central in 2026 and sustain high utilization across MRO networks. As cargo drones and eVTOLs scale in niche missions, they add adjacent demand for lighter systems and modular loading concepts without displacing core freighter needs in the near term.

Strategic moves from ecosystem players illustrate how demand is translating into platform and system activity. Cathay Cargo's 2025 commitment for A350F aircraft shows the airline's intent to pair lower fuel burn with modern cargo systems at linefit, a choice that aligns with future CO2 compliance and efficiency goals. AIR's late-2025 delivery of a cargo eVTOL unit demonstrated a transition from prototypes to initial commercial deployment for short-range logistics, creating new system requirements at the small-aircraft scale. European transport programs continued to elevate mission readiness and sustainment, which encourages standardized pallets and ruggedized loading equipment across mixed fleets. Suppliers that deliver composite components and electronic controls highlighted performance improvements at major industry events in 2025, focusing on lighter floors, improved health monitoring, and tighter integration. Reliability metrics and availability remain core to airline decision-making, which supports vendors that offer combined hardware and software value. Longer term, winning portfolios will tie linefit options to scalable retrofit kits that maintain high commonality across aircraft generations.

In 2026, the aircraft cargo systems market continues to benefit from durable aftermarket cycles and an improving outlook for new-build freighters. OEMs are pacing production rate increases in line with supplier readiness, which tempers near-term linefit volume but stabilizes long-term plans. Airlines allocate budget to system areas that reduce operating cost per turn and boost on-time performance, while defense customers emphasize ruggedness and interoperability. As more airports and carriers adopt digital cargo processes, integration with tracking and documentation becomes a must-have in new systems. This anchoring of digital features helps carriers manage compliance overhead while improving network planning predictability. The combination of aftermarket strength and gradual new-build normalization forms a balanced outlook through 2031.

Aircraft Cargo Systems Industry Leaders

Ancra International, LLC

Safran SA

U.S. Cargo Systems

Collins Aerospace (RTX Corporation)

Telair International GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: The US Air Force issued a Request for Information (RFI) to identify qualified sources with the expertise, capabilities, facilities, equipment, and experience required to repair the left and right sides of the C-5 Aft Cargo Center Door.

- March 2026: AAR Manufacturing LLC was awarded a USD 159.78 million contract by the US Department of War to repair 463L Legacy Cargo Pallets, as stated by the Air Force Life Cycle Management Center.

- February 2026: Hengqin Winglet Aircraft Technology in China inked a deal with Elbe Flugzeugwerke (EFW) for the conversion of an A330 from passenger to freighter (P2F). EFW, a German firm specializing in freighter conversions and a joint venture between ST Engineering and Airbus, will execute the A330P2F conversion at its partner facility in China. Mid-2026 marks the start of the conversion work, bolstered by technical planning and certification from EFW’s Dresden headquarters in Germany.

Global Aircraft Cargo Systems Market Report Scope

The aircraft cargo systems market encompasses a broad range of applications and end users. It includes cargo systems utilized in both commercial and military aircraft. The study also covers cargo systems designed for loading and installing cargo in fixed-wing and rotary-wing aircraft. Key end users include major commercial airlines, freight forwarders, shippers, government agencies, humanitarian organizations, and military entities.

The aircraft cargo systems market is segmented by product type, aircraft type, end user, and geography. By product type, the market is segmented into cargo loading systems and interior cargo fittings. By aircraft type, it is classified into commercial aircraft, military aircraft, and general aviation aircraft. By end user, the market is segmented into OEM and aftermarket. The report also covers the market sizes and forecasts for the aircraft cargo systems market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Cargo Loading Systems |

| Interior Cargo Fittings |

| Commercial Aircraft | Narrowbody Passenger Aircraft |

| Widebody Passenger Aircraft | |

| Freighter Aircraft | |

| Regional Jets | |

| Military Aircraft | Military Transport/Cargo Aircraft |

| General Aviation Aircraft | Cargo eVTOL and Large UAV |

| OEM |

| Aftermarket |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Product Type | Cargo Loading Systems | ||

| Interior Cargo Fittings | |||

| By Aircraft Type | Commercial Aircraft | Narrowbody Passenger Aircraft | |

| Widebody Passenger Aircraft | |||

| Freighter Aircraft | |||

| Regional Jets | |||

| Military Aircraft | Military Transport/Cargo Aircraft | ||

| General Aviation Aircraft | Cargo eVTOL and Large UAV | ||

| By End User | OEM | ||

| Aftermarket | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2026–2031 CAGR for the Aircraft Cargo Systems Market?

The aircraft cargo systems market is set to grow at a 7.09% CAGR from 2026 to 2031, reaching USD 11.33 billion by 2031 from USD 8.04 billion in 2026.

Which product category leads in the aircraft cargo systems market as of 2025?

Cargo loading systems led with 51.67% revenue share in 2025 and are forecasted to grow at 7.76% CAGR through 2031.

Which aircraft type is expanding fastest in the aircraft cargo systems market?

Military aircraft are projected to post the fastest 7.64% CAGR to 2031, supported by elevated defense outlays and modernization programs.

Which region holds the largest share of the aircraft cargo systems market?

North America led with 42.53% in 2025, supported by strong commercial conversion ecosystems and defense sustainment outlays.

Which region is growing fastest in the aircraft cargo systems market?

Asia-Pacific is projected to be the fastest-growing region at 7.32% CAGR, helped by e-commerce scale, conversions, and certified cargo drone activity.

How are OEM delays affecting the aircraft cargo systems market?

Constrained widebody slots and later entries for next-generation freighters are shifting demand toward conversions and retrofits, sustaining aftermarket momentum during 2026.

Page last updated on: