Aircraft Environmental Control Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

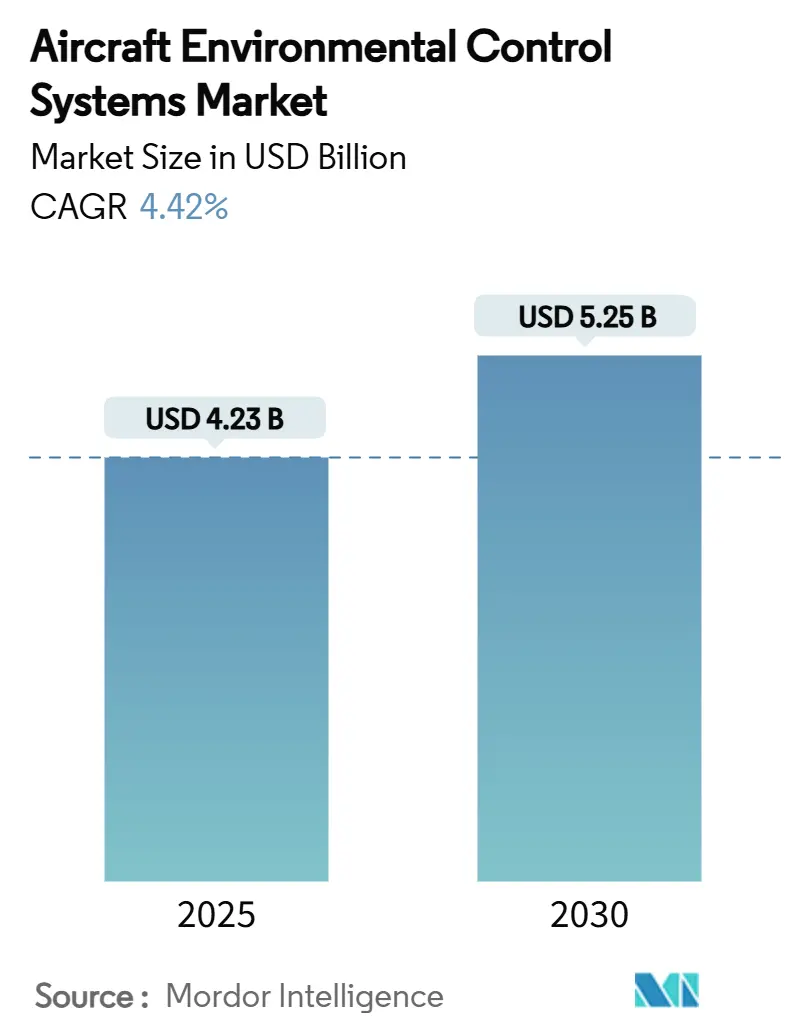

| Market Size (2025) | USD 4.23 Billion |

| Market Size (2030) | USD 5.25 Billion |

| Growth Rate (2025 - 2030) | 4.42% CAGR |

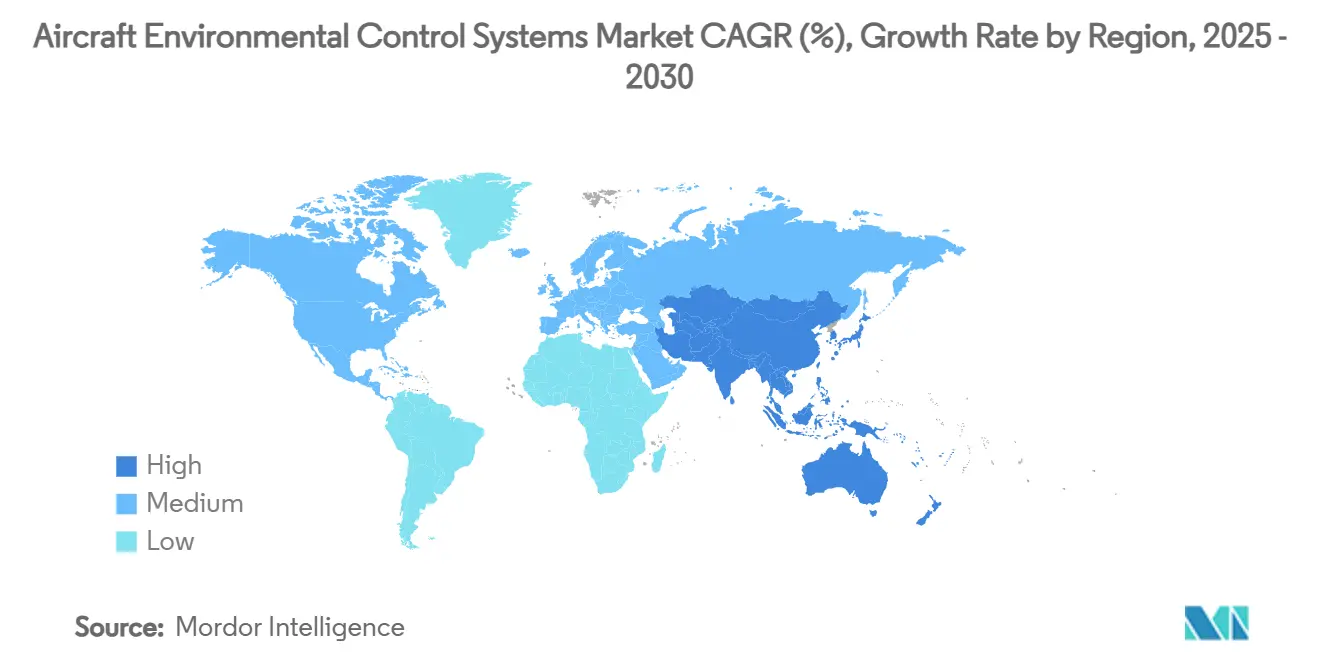

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Environmental Control Systems Market Analysis by Mordor Intelligence

The aircraft environmental control systems market size reached USD 4.23 billion in 2025 and is forecasted to climb to USD 5.25 billion in 2030, reflecting a 4.42% CAGR. This steady expansion comes as airlines refresh fleets, manufacturers shift toward more-electric architectures, and emerging platforms demand compact thermal solutions. Commercial narrowbody deliveries lead near-term volume, while advanced air-mobility prototypes put the spotlight on electric compressors and liquid-cooling loops. Heightened cabin-air-quality rules accelerate filter and sensor innovation, and predictive-maintenance software gains traction as operators look to cut unscheduled ground time. North America preserves the most significant regional slice on the back of defense upgrades and retrofit programs, yet Asia-Pacific records the quickest growth in China’s and India’s fleet trajectories. Competitive intensity rises as incumbents reinforce certification know-how and newcomers chase opportunities in eVTOL and hydrogen testbeds.

Key Report Takeaways

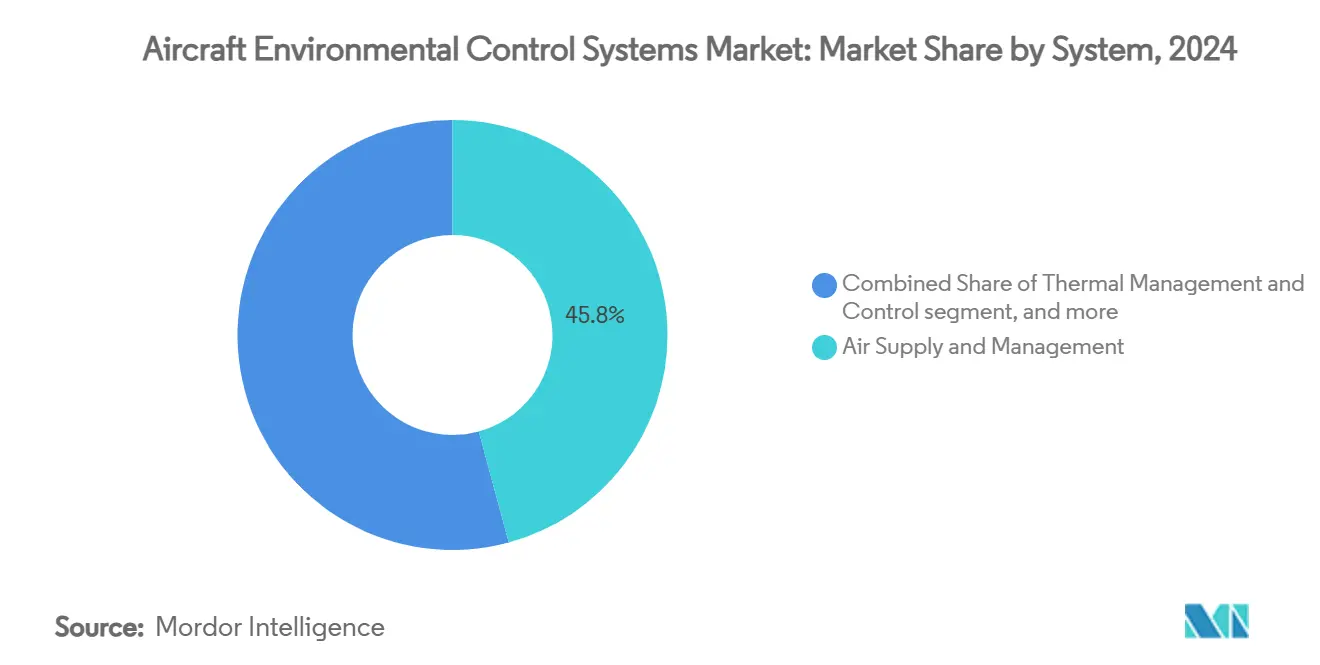

- By system, air supply and management captured 45.78% of the aircraft environmental control systems market share in 2024, while thermal management and control are advancing at a 5.34% CAGR to 2030.

- By platform, fixed-wing aircraft held 73.60% of the aircraft environmental control systems market share in 2024; advanced air mobility is projected to expand at a 12.74% CAGR through 2030.

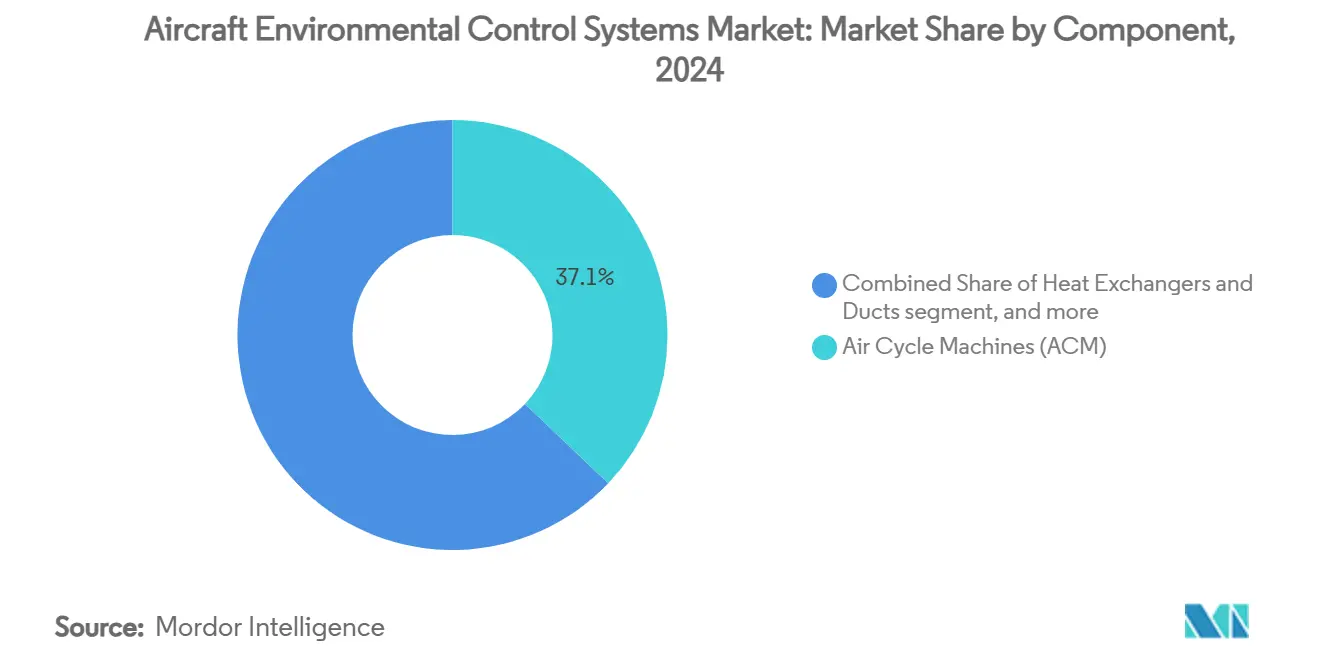

- By component, air-cycle machines held a 37.10% share of the aircraft environmental control systems market in 2024, and control electronics is progressing at a 7.01% CAGR through 2030.

- By end user, OEMs represented 69.50% of the aircraft environmental control systems market share in 2024, while the aftermarket segment is growing at a 5.98% CAGR to 2030.

- By geography, North America led with 37.42% revenue share in 2024, and Asia-Pacific is on course for a 6.45% CAGR through 2030.

Global Aircraft Environmental Control Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating commercial aircraft production | +1.2% | Global with focus on North America and Asia-Pacific | Medium term (2-4 years) |

| Stricter global cabin-air-quality regulations | +0.8% | Global, led by FAA and EASA jurisdictions | Long term (≥ 4 years) |

| Retrofit demand for “more-electric” ECS | +0.9% | North America and Europe, expanding into Asia-Pacific | Medium term (2-4 years) |

| Rising defense aircraft procurement | +0.7% | North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Bleed-less electric ECS enabling zero-emission propulsion | +0.6% | Global, early uptake in developed markets | Long term (≥ 4 years) |

| Predictive-maintenance digital twins for ECS | +0.4% | Global, concentrated around major airline hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating Commercial Aircraft Production

Boeing’s forecast for 44,000 additional jetliners by 2043—three-quarters single-aisle—creates a predictable, multi-decade production skyline that benefits line-fit ECS suppliers.[1]Source: “Boeing Forecasts Demand for Nearly 44,000 New Airplanes Through 2043,” investors.boeing.com Every new narrowbody requires two or three air-cycle packs, a network of heat exchangers, and digital controllers, so even minor rate increases translate into hundreds of extra ship-sets per year. At the same time, supply bottlenecks in engines and structural castings delay retirements, pushing operators to keep ageing A320ceo and B737-NG units longer. That reality has triggered an upswing in retrofit projects that swap older bleed-air packs for lighter vapour-cycle systems that save fuel and improve reliability during end-of-life operation. Embraer’s separate projection for 10,500 regional jets, largely 70-130-seat aircraft, adds another layer of demand where cabin-pressure optimisation directly influences trip economics for short-hop operators.

Stricter Global Cabin-Air-Quality Regulations

Regulators now treat cabin air as a quantified safety parameter rather than a comfort item. The FAA’s 2024 advisory instructs airlines to maintain fresh airflow during extended ground delays, mandating ground-powered ventilation or APU use when main engines are shut down. EASA’s FACTS program parallel maps hundreds of potential cabin contaminants, giving engineers empirical data to design higher-grade filtration and real-time monitoring modules.[2]Source: Federal Aviation Administration, “Management of Passengers During Ground Operations Without Cabin Ventilation,” faa.gov Meeting the long-standing 0.55 lb-per-minute fresh-air rule in 14 CFR 25.831 is no longer sufficient; carriers increasingly specify multi-stage HEPA or catalytic filters that remove ultrafine particulates and VOCs. Lufthansa’s decision to add active-humidity systems in premium cabins underscores a competitive pivot toward well-being features, compelling OEMs to install larger compressors and more intelligent sensors to regulate moisture and air-quality indices automatically.

Retrofit Demand for More-Electric ECS

Bleed-less architecture, first proven on the B787, eliminates thrust-sapping hot-bleed extraction and reduces fuel burn by about 3%, a figure that resonates with airlines facing high fuel-price volatility. Honeywell’s micro vapour-cycle pack advances the concept, delivering a 35% weight cut and 20% efficiency gain, attributes that shorten retrofit payback to only a few years on busy narrowbody routes. Europe’s Clean Sky 2 tests prove that electrically driven compressors combined with ambient-air intake can trim engine thrust loss by up to 8%, a compelling metric for operators juggling payload and range limits. As OEM production slots remain scarce, carriers increasingly opt to upgrade existing fleets, fuelling a parallel aftermarket economy in electric ECS conversion kits and service bulletins.

Rising Defense Aircraft Procurement

Combat platforms have moved from analogue avionics to digital mission systems that dissipate multiple kilowatts of heat, forcing a rethink of legacy pack capacity. Honeywell’s F-35 demonstrator shows an 80 kW cooling capability 2.5x of today’s baseline—highlighting the step-change demanded by radar, electronic-warfare, and laser systems. The U.S. Navy’s award for temperature-critical antenna panels further indicates a spending pattern that values advanced thermal management hardware integrated early in the design spiral. Similar procurement upticks appear in Europe’s FCAS and Japan’s F-X fighter studies, while Asia-Pacific nations add AEW&C and maritime-patrol assets with sizeable onboard electronics suites. Consequently, suppliers able to package high-density liquid loops, NBC filtration, and ruggedized controls are well positioned to capture long-term defence ECS revenues.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High R&D and certification costs | -0.9% | Global, greater pressure on smaller suppliers | Long term (≥ 4 years) |

| Supply-chain constraints for heat-exchangers and compressors | -1.1% | Global with acute stress in Asia-Pacific hubs | Medium term (2-4 years) |

| Labor shortages and engineering expertise loss | -0.7% | North America and Europe; emerging impact in Asia-Pacific | Medium term (2-4 years) |

| Trade barriers affecting compressor imports | -0.5% | Asia-Pacific import-dependent nations; spill-over to EU and NAFTA | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High R&D and Certification Costs

System-safety rules that became mandatory in September 2024 require exhaustive fault-tree analyses and collateral testing, extending development cycles to five or even ten years for complex packs.[3]Source: Federal Register, “System Safety Assessments,” federalregister.gov Collins Aerospace has earmarked USD 1 billion over five years to de-risk next-generation ECS research, a level of spend smaller suppliers cannot match. The burden multiplies for eVTOL applicants, where certification bases blend rotorcraft, fixed-wing, and new “powered-lift” criteria, forcing multiple iterations of environmental testing. As a result, niche innovators often partner with—or are acquired by larger incumbents that already possess Organisation Delegation Authority, reducing competitive diversity and potentially slowing the introduction of disruptive technologies.

Supply-Chain Constraints for Heat-Exchangers and Compressors

Aerospace-grade heat exchangers rely on high-temperature nickel alloys and precision welding talent, which remain in tight supply. Despite shipping 2.5 million units since program inception, Honeywell still battles extended raw-material lead times, prompting dual-source and near-shoring strategies. GE Aerospace’s 10% reduction in 2024 engine deliveries, traced partly to turbine-blade bottlenecks, cascaded into delayed ECS integrations because packs cannot be certified until baseline propulsion tests finish. Boston Consulting Group highlights labour shortages and lost forging expertise as additional choke points, exacerbating schedule and cost pressures downstream. These constraints undercut OEM rate ramp-ups and complicate aftermarket turnaround times, dampening overall ECS market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System: Air Supply Maintains the Core Role while Thermal Innovation Gains Pace

Air-supply and management equipment accounts for 45.78% of the aircraft environmental control systems market size, reflecting its irreplaceable function in pressurization and breathing-air delivery. The segment stays resilient because every commercial or military platform requires a primary air-cycle loop regardless of propulsion type. Still, the thermal-management and control subset posts the fastest 5.34% CAGR as avionics power density multiplies. Liebherr, Safran, and Collins respond with integrated power-and-thermal modules that fuse heat exchange, vapour-cycle, and cabin-pressure tasks into one line-replaceable unit, trimming weight and wiring.

A second growth driver comes from convergence with zero-emission propulsion. Liquid-loop architectures proven in NASA bench tests feed directly into hydrogen-fuel-cell demonstrators, bringing fresh revenue for specialist heat-exchanger makers. Suppliers also adapt catalytic-oxidiser technology to remove VOCs generated at higher cabin humidity targets. As urban-air vehicles certify, scale economics should narrow the cost delta between bleed and electric packs, setting the stage for broader adoption across narrowbody retrofits.

By Platform: Fixed-Wing Holds Share but Advanced Air Mobility Shows Acceleration

Fixed-wing jets preserved 73.60% of the aircraft environmental control systems market share in 2024 because of the large in-service fleet and ongoing NG narrowbody programs. Widebody recovery adds incremental demand as airlines reopen long-haul routes. Defense transports and special-mission variants further cement volume. The 12.74% CAGR in advanced air mobility points to a structural shift. Over 600 eVTOL prototypes are in test phases, each demanding compact packs that function without bleed air, and regulators now issue powered-lift type-rating rules that remove a key uncertainty.

Rotorcraft sustain a stable baseline in EMS, offshore, and parapublic missions where hover requirements induce high thermal loads. However, the segment grows more slowly than the overall aircraft environmental control systems market. Unmanned platforms bring niche opportunities for micro-compressors below 1 kW that can prolong loiter time by stabilising electronics temperatures. As AAM production lines mature after 2028, suppliers able to scale automotive-derived vapour-cycle technologies in aviation-grade configurations will likely gain share.

By Component: Air-Cycle Machines Remain Central as Control Electronics Surge

Air-cycle machines hold 37.10% of the aircraft environmental control systems market and remain the backbone of traditional bleed configurations. Even emerging bleed-less packs often have a miniaturised turbine-expander stage to boost cooling efficiency under low-ambient-pressure cruise. Heat exchangers and ducts follow closely, benefiting from additive-manufactured lattice structures that raise surface area without additional mass.

Control electronics posts a robust 7.01% CAGR as digital architectures proliferate. Honeywell’s tie-up with NXP embeds AI cores inside pack controllers, allowing real-time pattern recognition of impending seal wear. MDPI studies show blockchain frameworks safeguarding in-flight sensor data, paving the way for distributed diagnostics across airline networks. Sensor miniaturisation also drives growth in valves and pressure transducers that communicate wirelessly, cutting harness weight and easing retrofit on older airframes.

By End User: OEM Programs Dominate yet Aftermarket Growth Outpaces

Original-equipment fit accounts for 69.50% of the aircraft environmental control systems market share because every new airframe delivers with a full suite from an approved supplier list. The backlog of narrow-body orders keeps tier-one production lines humming, and design-for-maintainability remains a key differentiator during competitive tender rounds.

The aftermarket segment grows 5.98% per year in response to extended service lives, with many A320ceo and B737-NG jets projected to fly well past 2035. Airlines prioritise predictive-maintenance modules that can integrate seamlessly with existing aircraft-health platforms. Collins Aerospace operates eight global MRO centres that overhaul packs, valves, and sensors with OEM-approved parts, giving it scale economies and just-in-time inventories. Independent shops still capture regional workscopes, but their share shrinks as carriers sign flight-hour agreements bundled with analytics dashboards.

Geography Analysis

North America commands the most significant slice at 37.42% of the aircraft environmental control systems market share, anchored by its mature commercial fleets, extensive MRO infrastructure, and defence modernisation outlays. Boeing and Lockheed Martin source many ECS units locally, reinforcing regional demand. Government funding for sixth-generation fighter demonstrators funnels R&D dollars into high-capacity liquid-cooling modules, keeping suppliers such as Honeywell and Collins ahead in certification pathways.

Asia-Pacific posts the fastest 6.45% CAGR to record fleet expansion in China, India, and fast-growing Southeast Asian carriers. Boeing estimates China’s fleet will jump from 4,345 to 9,740 aircraft by 2043, which alone secures multi-year ECS line-fit volumes. India’s requirement for 2,835 new jets in the same window accelerates demand for adaptable packs that cope with hot-and-high airports. Domestic supply-chain build-outs, such as Diehl Aviation’s new plant announced for Querétaro, support localised heat-exchanger production and reduce import exposure.

Europe remains a technology pacesetter given the Clean-Sky and now Clean-Aviation frameworks that co-fund electric-compressor and alternative-refrigerant projects. Airbus’s concentrated footprint in France, Germany, and Spain sustains steady ECS volumes even as narrow-body ramp-up faces casting bottlenecks. The Middle East leverages major hub airlines that refresh wide-body cabins early, creating retrofit business for humidity and filtration upgrades. Africa grows from a lower base, focusing on pressure-control reliability for high-altitude operations around East African corridors.

Competitive Landscape

The aircraft environmental control systems market shows moderate fragmentation. Four integrated leaders, Honeywell, Liebherr, Safran, and Collins Aerospace, dominate OEM selections through certification depth and global support networks. Each pursues aggressive electrification roadmaps. Collins commits USD 3 billion to electric-architecture projects and fields over 1,000 engineers on power and thermal integration. Honeywell restructures to spin off non-aviation assets by 2026, signalling sharper alignment with flight-critical systems.

Tier-two specialists carve niches in valves, sensors, and compact heat exchangers. The UK antitrust review of Honeywell’s Hymatic purchase highlighted a 30-40% share in aerospace valves, illustrating how component focus can yield defensible positions. Start-ups target urban-air mobility, offering lightweight vapour-cycle modules with automotive supply-chain efficiencies. Their challenge lies in achieving DO-178 and DO-254 compliance at speed. Incumbents answer by launching venture arms to invest in promising concepts, evidenced by Safran’s stake in a hybrid direct air-capture firm that may provide synthetic-fuel inputs and new heat-management use cases.

Service differentiation gains weight as OEMs package predictive analytics and consumables replenishment in fixed-hour contracts. Collins promotes an availability-guaranteed offering that bundles spares, on-wing data collection, and remote diagnostics. Honeywell counters with Forge-enabled dashboards tuned for pack health parameters that aim to cut dispatch delays. Airlines lean toward these integrated options because supply-chain disruptions increase the value of assured part access.

Aircraft Environmental Control Systems Industry Leaders

Honeywell International Inc.

Safran SA

Curtiss-Wright Corporation

Liebherr Group

Collins Aerospace (RTX Corporation)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Honeywell announced that Bell Textron Inc., a Textron Inc. company, selected its 36-150 APU and Honeywell Attune for the US Army's FLRAA. These technologies enhance mission readiness, operational flexibility, and thermal management, aligning with Honeywell's focus on aviation's future and advanced solutions.

- July 2024: Triumph Group, Inc. secured a long-term contract from Deutsche Aircraft to design, manufacture, and support the precooler system for the D328eco regional turboprop aircraft. Pratt and Whitney PS127XT-S engines power the aircraft and can use 100% Sustainable Aviation Fuel (SAF), reducing fuel consumption and carbon emissions by 40%.

Global Aircraft Environmental Control Systems Market Report Scope

| Air Supply and Management |

| Thermal Management and Control |

| Cabin Pressure and Control |

| Fixed-Wing Aircraft | Commercial | Narrowbody |

| Widebody | ||

| Regional Jets | ||

| Business Jets | ||

| Piston and Turboprop | ||

| Military | Fighter Jets | |

| Transport Aircraft | ||

| Special-Mission Aircraft | ||

| Rotorcraft | Civil Helicopters | |

| Military Helicopters | ||

| Unmanned Aerial Vehicles (UAVs) | ||

| Advanced Air Mobility (AAM) | ||

| Air Cycle Machines (ACM) |

| Heat Exchangers and Ducts |

| Valves and Sensors |

| Control Electronics |

| Others (Water Separators, Compressors, Filters) |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By System | Air Supply and Management | ||

| Thermal Management and Control | |||

| Cabin Pressure and Control | |||

| By Platform | Fixed-Wing Aircraft | Commercial | Narrowbody |

| Widebody | |||

| Regional Jets | |||

| Business Jets | |||

| Piston and Turboprop | |||

| Military | Fighter Jets | ||

| Transport Aircraft | |||

| Special-Mission Aircraft | |||

| Rotorcraft | Civil Helicopters | ||

| Military Helicopters | |||

| Unmanned Aerial Vehicles (UAVs) | |||

| Advanced Air Mobility (AAM) | |||

| By Component | Air Cycle Machines (ACM) | ||

| Heat Exchangers and Ducts | |||

| Valves and Sensors | |||

| Control Electronics | |||

| Others (Water Separators, Compressors, Filters) | |||

| By End User | Original Equipment Manufacturer (OEM) | ||

| Aftermarket | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the aircraft environmental control systems market?

The aircraft environmental control systems market size stands at USD 4.23 billion in 2025 and is projected to reach USD 5.25 billion by 2030, reflecting a 4.42% CAGR.

Which system type holds the largest revenue share?

Air-supply and management systems lead with 45.78% share thanks to their critical role in pressurization and ventilation.

Which platform segment is growing the fastest?

Advanced air-mobility aircraft post the highest growth, registering a 12.74% CAGR through 2030.

Why are predictive-maintenance solutions gaining traction?

Airlines connect packs to digital-twin platforms that detect performance drift early, cutting unscheduled ground time and lowering life-cycle costs.

How are stricter air-quality rules influencing ECS design?

Regulations drive the adoption of higher-efficiency filters, active monitoring sensors, and humidification modules that surpass the 14 CFR 25.831 baseline.

Which region will contribute the most incremental demand by 2030?

Asia-Pacific, underpinned by rapid fleet expansion in China and India, is expected to add the greatest number of ECS-equipped aircraft.

Page last updated on: