Aircraft Gearbox Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

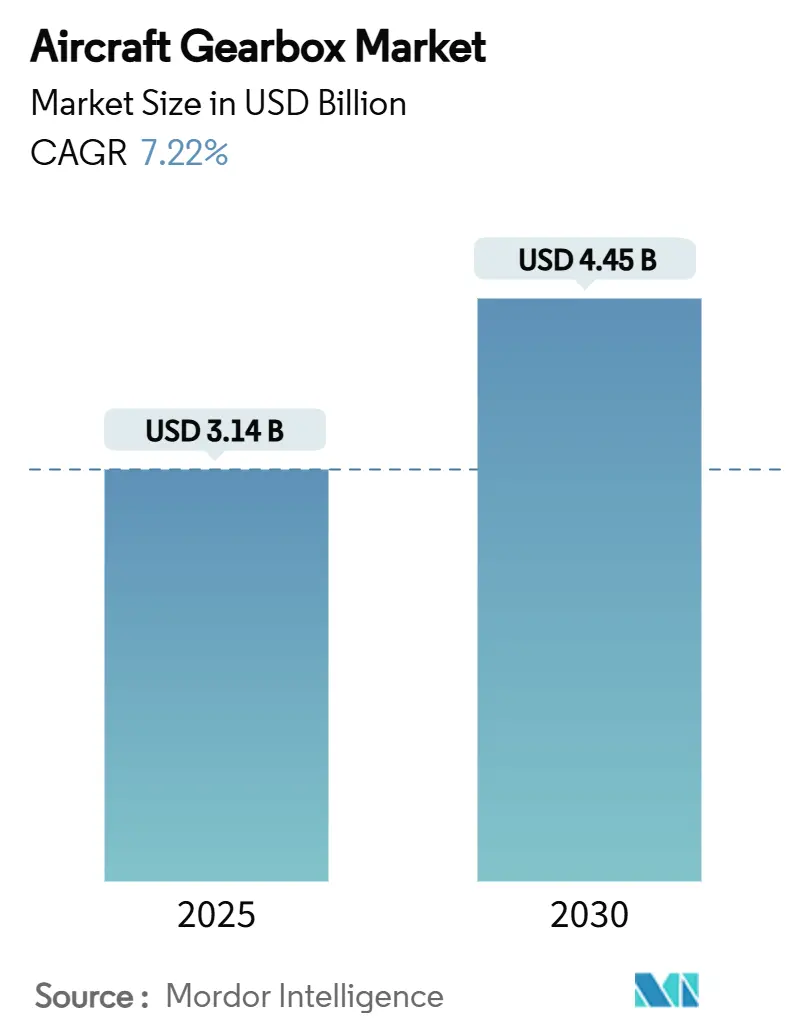

| Market Size (2025) | USD 3.14 Billion |

| Market Size (2030) | USD 4.45 Billion |

| Growth Rate (2025 - 2030) | 7.22% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Gearbox Market Analysis by Mordor Intelligence

The aircraft gearbox market size is USD 3.14 billion in 2025 and is projected to reach USD 4.45 billion by 2030 after growing at a 7.22% CAGR over the forecast period. Substantial order backlogs for next-generation single-aisle jets, the broad deployment of geared-turbofan engines, and early commercial demonstrations of hybrid-electric propulsion systems sustain shipment volumes. Airlines prioritize fuel-efficient propulsion architectures that couple large-diameter fans to high-speed turbines through precision reduction systems, translating into higher gearbox content per aircraft. Meanwhile, additive manufacturing and condition-based monitoring shorten development cycles and lower life-cycle costs for key sub-assemblies. Thermal-management innovations and improved surface treatments also lift the power-to-weight ceiling, opening design space for 1 MW-class electric propulsion demonstrators. These converging forces indicate a decade of solid demand for suppliers that can scale production quality while meeting tougher certification standards.

Key Report Takeaways

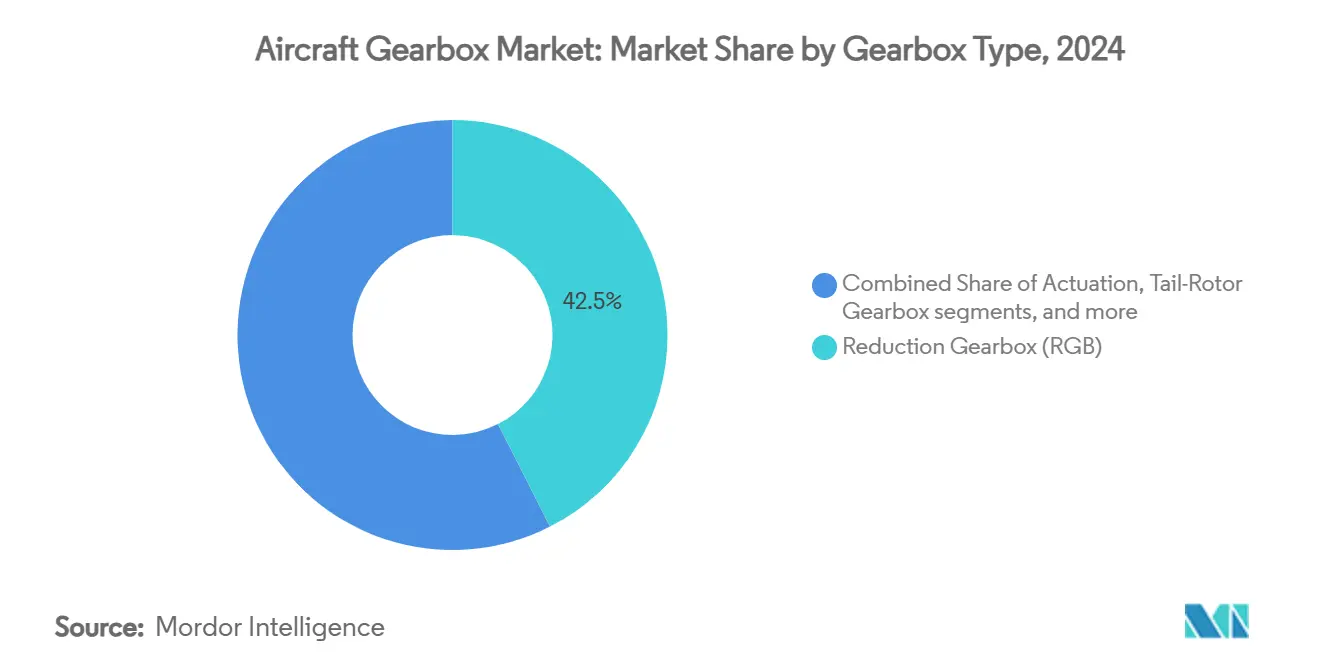

- By gearbox type, reduction gearboxes led with 42.50% revenue share of the aircraft gearbox market in 2024, while tail-rotor gearboxes are forecasted to expand at an 8.77% CAGR through 2030.

- By aircraft type, fixed-wing platforms accounted for 67.87% of the aircraft gearbox market share in 2024; unmanned aerial vehicles are set to grow at a 10.45% CAGR over the same period.

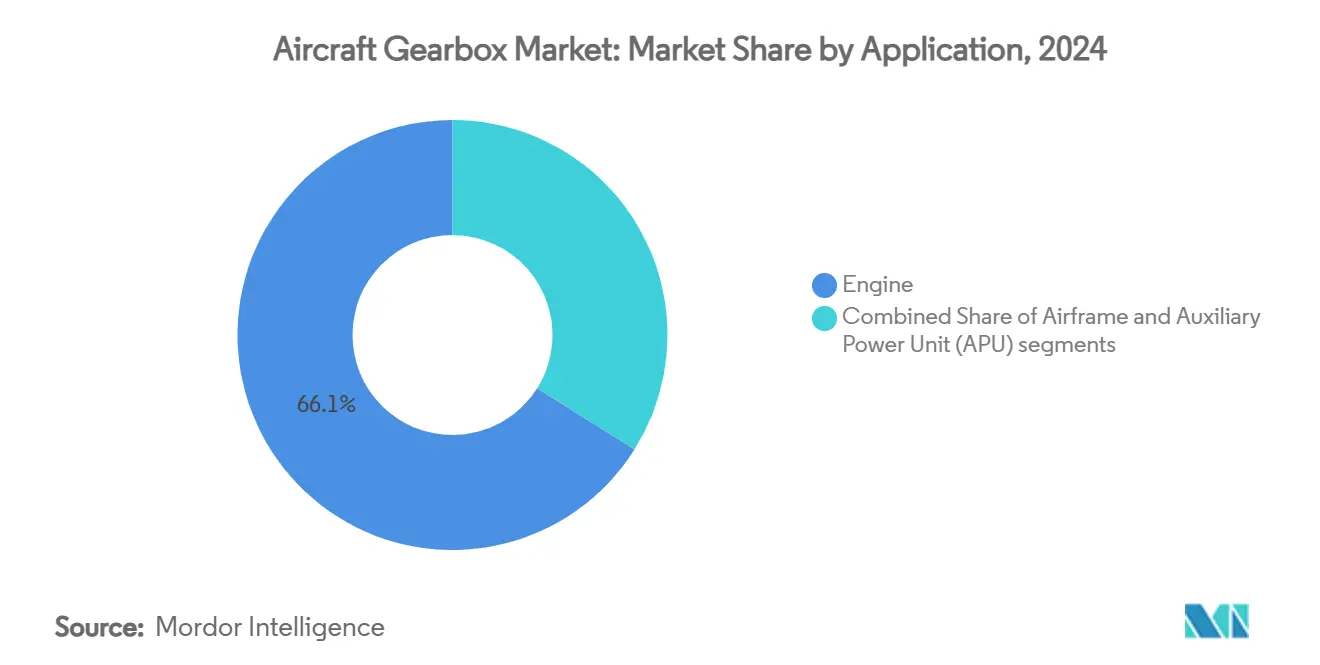

- By application, engine systems commanded 66.14% of the aircraft gearbox market size in 2024; airframe applications are advancing at an 8.10% CAGR to 2030.

- By fit, line-fit installations represented 73.45% of the aircraft gearbox market in 2024, whereas retrofit programs are expected to rise at a 9.20% CAGR over the forecast horizon.

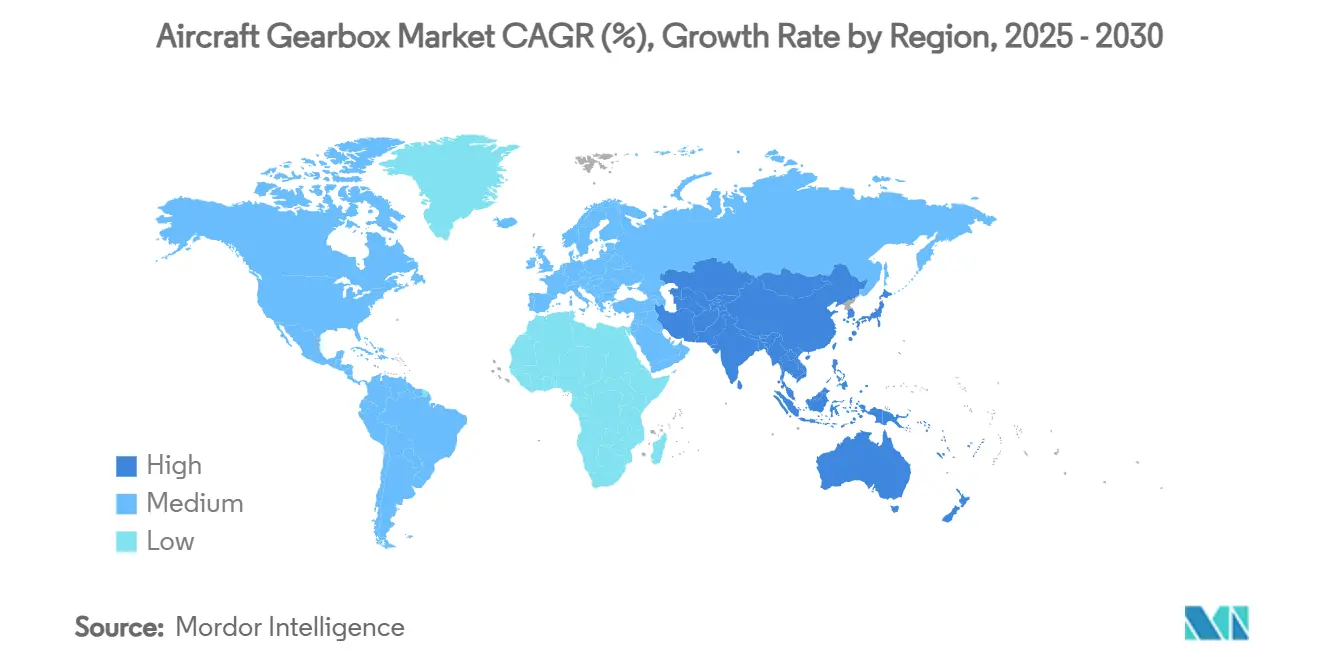

- By geography, North America maintained 37.80% of the aircraft gearbox market in 2024; Asia-Pacific exhibits the fastest regional CAGR at 8.97% through 2030.

Global Aircraft Gearbox Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in geared-turbofan (GTF) engine deliveries | +1.8% | North America and Europe, spreading globally | Medium term (2-4 years) |

| Growing global aircraft production backlog | +1.5% | North America and Asia-Pacific | Long term (≥ 4 years) |

| Shift toward lightweight, fuel-efficient propulsion components | +1.2% | North America and Europe | Long term (≥ 4 years) |

| Adoption of condition-based gearbox health-monitoring systems | +0.9% | Initially North America and Europe | Medium term (2-4 years) |

| Additive manufacturing advances in high-torque gears | +0.7% | North America and Europe, emerging Asia-Pacific | Medium term (2-4 years) |

| Hybrid-electric aircraft requiring high-ratio reduction gearboxes | +0.6% | Early adoption in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise in Geared-Turbofan Engine Deliveries

Airlines continue to migrate toward geared-turbofan (GTF) propulsion because the architecture cuts block fuel burn by up to 20%, trims perceived noise by 75%, and lowers maintenance spend. Pratt & Whitney’s GTF Advantage engine achieved US FAA type certification for the A320neo family in February 2025, adding 4–8% more take-off thrust without sacrificing the baseline fuel-savings profile. MTU Aero Engines, which holds an 18% program share, notes that the global GTF fleet has already saved 7 billion L of fuel and avoided 20 million t of CO₂ emissions.[1]MTU Aero Engines Media Relations, “Pratt & Whitney GTF Engine Family Delivers Environmental Benefits,” mtu.de Each GTF installs a high-ratio reduction gearbox between the fan and low-pressure turbine, boosting unit demand across new deliveries and spares pools. As narrowbody production climbs toward pre-pandemic peaks, the aircraft gearbox market gains a reliable pull-through in OEM and aftermarket channels.

Growing Global Aircraft Production Backlog

Boeing and Airbus have combined backlogs of over 14,800 aircraft, equating to close to 13 years of planned output at current build rates. Such structural order depth insulates gearbox suppliers from short-term traffic volatility and enables multi-year capital planning. Powerplant selections inside the backlog overwhelmingly favor geared turbofan or open-fan concepts, ensuring that reduction gearboxes remain standard hardware over the decade. Sustained production slots underpin sizeable line-fit volumes for actuation, tail-rotor, and auxiliary gearboxes. The visibility created by this backlog allows supply networks to invest in new lines, automate heat-treat operations, and qualify additive processes that raise throughput without compromising airworthiness.

Shift Toward Lightweight, Fuel-Efficient Propulsion Components

Advanced titanium alloys, case-hardened steels, and selective-laser-melted lattices replace legacy castings to cut rotating mass and improve thermal paths. Boeing’s B787 program highlighted how a 20% structural weight reduction can translate into double-digit fuel savings, energizing similar initiatives in propulsion subsystems. Gearboxes now integrate thin-wall housings, topology-optimized bearing carriers, and conformal oil channels to shave kilograms while sustaining higher torque. Safran Transmission Systems confirms that additive-manufactured star-planet carriers are entering flight tests after clearing static strength benchmarks. These weight-focused designs align with airline carbon-reduction pledges and support the aircraft gearbox market’s pivot toward holistic efficiency.

Additive Manufacturing Advances in High-Torque Gears

Powder-bed fusion and directed-energy deposition are enabling gear geometries once deemed unmachinable. Beehive Industries reports cost reductions approaching 50% for small hot-section gears printed from high-strength steels.[2]Source: Beehive Industries, “Small-Scale Engines Made Through Additive Manufacturing,” additivemanufacturing.media In parallel, research into in-situ pulse-current techniques demonstrates enhanced grain refinement that lifts fatigue life in AISI 9310 gear steel, a staple alloy for aerospace drives. These breakthroughs accelerate prototype iteration and simplify part consolidation, helping the aircraft gearbox market cut lead times while sustaining stringent metallurgical integrity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High development and certification costs | -1.4% | North America and Europe | Long term (≥ 4 years) |

| In-service gearbox reliability issues causing fleet groundings | -1.1% | Regions operating large GTF fleets | Short term (≤ 2 years) |

| Supply-chain scarcity of aerospace-grade alloy steels | -0.8% | North America and Europe | Medium term (2-4 years) |

| Thermal-management limits on ultra-high-power gearboxes | -0.6% | Global next-gen programs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Development and Certification Costs

Civil aviation approval protocols often exceed 5 years and can cost over USD 100 million per clean-sheet gearbox, stretching the cash cycles of mid-tier innovators. Digital twin methods and simulation-driven verification cut wind tunnel and rig hours, yet applicants must validate materials, lubrication, and failure-mode analyses under FAA and EASA oversight. The financial hurdle tends to entrench incumbent suppliers with certified product families and mature quality systems.

In-Service Gearbox Reliability Issues Causing Fleet Groundings

Contamination of powdered-metal disks in specific PW1100G assemblies forced Pratt & Whitney to recall more than 1,200 engines, grounding roughly 350 jets worldwide in 2025 and leading to average off-wing times of 360 days for affected carriers.[3]Source: FlightGlobal Newsroom, “JetBlue’s GTF Engines Off-Wing for Average of 360 Days,” flightglobal.comAlthough root causes centered on turbine disks, public perception associated the event with the wider GTF gearbox, prompting airlines to scrutinize advanced drive-train designs more closely and potentially slowing retrofit uptake until durability upgrades are in service.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Gearbox Type: Reduction Systems Drive Efficiency

Reduction gearboxes accounted for 42.50% of the revenue in 2024, underscoring their pivotal role in the geared-turbofan propulsion packages produced by industry giants Airbus, Boeing, and COMAC. This trend highlights the increasing importance of speed-reduction stages in new single-aisle power plants, driven by stringent fuel-efficiency mandates. As the segment is poised to expand alongside the overall output of OEM narrow bodies, it can benefit further from the emerging open-fan architectures. Tail-rotor drives are witnessing the steepest ascent, boasting an impressive 8.77% CAGR, fueled by renewals in heavy-lift and offshore helicopters. Sikorsky’s Phase IV S-92 main gearbox, designed to operate for an additional 30 minutes post oil-pressure loss, exemplifies the reliability-centric design philosophy that resonates deeply with operators.

Across all gearbox classes, suppliers are embracing topology-optimized casings, additively manufactured planet carriers, and high-velocity-oxygen-fuel (HVOF) sprayed tooth coatings that extend wear life. Accessory gearboxes are moving to modular layouts that simplify maintenance and shave cost, while APU gearboxes adopt integrated starters to reduce part count. Developers study compound-planet sets capable of ratios above 20:1 without prohibitive noise or vibration as electrified propulsion grows, signaling a future adjacency for incumbent reduction-gear specialists.

By Aircraft Type: Fixed-Wing Dominance Amid UAV Acceleration

In 2024, fixed-wing programs dominated the market, making up 67.87% of the demand. Their established presence, regular flight cycles, and leading position in global backlogs ensure consistent aftermarket volumes. Meanwhile, unmanned aerial vehicles are on track to grow at a 10.45% CAGR through 2030, buoyed by defense ISR budgets and emerging logistics drone corridors. These airframes utilize compact, high-cycle gearboxes, typically crafted with composite housings and dry-film lubricated spur sets, carving out a unique design niche for specialized suppliers.

Widebody jets form a mature but lucrative pocket where each spare LPT or transfer gearbox commands premium pricing due to high nickel-alloy content and overhaul complexity. Regional jets and business aircraft embrace scaled-down GTF derivatives, importing reduction-driven value propositions. Rotorcraft remain a steady user of split-torque and bevel gear layouts that must handle sudden load surges during autorotation, pushing metallurgists to refine carburizing depths and shot-peen regimes for crack resistance over long overhaul intervals.

By Application: Engine Systems Lead Integration

In 2024, engine-mounted drives commanded a substantial 66.14% of the revenue. This dominance underscores the industry's shift towards high-bypass turbofans, where the reduction gearbox plays a pivotal role in harmonizing low-speed fan aerodynamics with turbine efficiency. Engine-mounted drives continue to lead the market, as every emerging propulsion concept, ranging from open-fan demonstrators to 1 MW turbogenerators, depends on tailored reduction stages.

Airframe installations are catching momentum at an 8.10% CAGR as more-electric architectures embed electro-mechanical actuators across flaps, spoilers, and landing-gear doors. That shift raises overall gearbox count per airframe and favors modular designs that share standard bearing cartridges. Auxiliary-power-unit gearboxes continue to emphasize cold-soak start reliability and easy line-replaceability, particularly for business jets operating from remote strips. Across categories, integrated oil-condition monitoring chips are becoming baseline hardware, feeding real-time viscosity and metallic-particle data back to predictive-maintenance dashboards.

By Fit: Line-Fit Leadership With Retrofit Momentum

Line-fit channels absorbed 73.45% of sales in 2024, as every new airframe requires a complete gearbox suite before leaving the final assembly line. Retrofit activity, while smaller, grows faster at 9.20% CAGR by piggybacking on heavy-maintenance visits where airlines seize fuel-saving or durability upgrades. Modules engineered for drop-in interchangeability minimize aircraft downtime, making retrofit paths attractive for legacy A320ceo and B737NG fleets seeking incremental savings ahead of retirement.

From a supplier standpoint, line-fit programs deliver predictable volume but impose long certification lead times and stiff warranty obligations. Retrofit kits, by contrast, command higher margins and allow tailored service-bulletin bundles, albeit with lumpier demand. Providers that design standard core gear sets adaptable to both channels will be best positioned to capture full-life revenue streams while simplifying inventory

Geography Analysis

North America commanded 37.80% of global revenue in 2024, buoyed by urbanization-driven passenger demand and sizable defense budgets funneling through Boeing rotorcraft and Lockheed Martin platforms. The US also hosts Pratt & Whitney’s GTF overhaul network and Triumph Group’s accessory-drive assembly lines, reinforcing aftermarket stickiness. Approved Model List supplemental-type certificates accelerate retrofit uptake, giving local MROs a head start in deploying additive-manufactured spares.

Asia-Pacific exhibits the fastest expansion at 8.97% CAGR as indigenous programs seek vertical supply-chain autonomy. COMAC’s C919 achieved initial service in 2024 and now relies on domestic factories for second-source gear casings, a shift encouraged by government policy. India plans USD 12 billion in airport infrastructure to lift narrowbody and regional jet orders, and its aerospace offset rules push foreign primes to co-invest in gear machining hubs. Japanese conglomerates continue to channel defense outlays into advanced-drive R&D, while Korean helicopter programs create steady demand for split-torque main-gearbox technology.

Europe maintains a technology-rich ecosystem anchored by Airbus, Safran Transmission Systems, MTU Aero Engines, and Rolls-Royce. The region champions sustainability, channeling EU funding into hydrogen-ready and hybrid-electric demonstrators that rely on high-ratio epicyclic gear trains. Germany’s cluster of precision-forging houses and France’s additive-manufacturing centers provide material and process innovation that feeds the broader aircraft gearbox market. Smaller regions such as the Middle East, South America, and Africa represent emerging growth fronts, particularly for helicopter heavy-maintenance and utility transport retrofits. However, the lack of indigenous manufacturing tempers near-term share gains.

Competitive Landscape

The aircraft gearbox market features moderate consolidation, with the top five suppliers controlling an estimated 68% of revenue. Safran Transmission Systems holds a 30% share of mainline commercial-jet gearboxes and continues to invest in laser-powder-bed fusion for spiral-bevel gears, reducing raw-material scrap rates by 25%. RTX leverages its vertically integrated GTF architecture, aligning gearbox, fan, and turbine upgrades to deliver cumulative 10% durability gains in the Advantage block standard. Rolls-Royce is funneling USD 1.25 billion into Trent family life-cycle upgrades and has launched a single-aisle UltraFan demonstrator aimed at 10% efficiency improvement over contemporary wide-core engines.

Emerging entrants specialize in hybrid-electric architectures or UAV drives. GE Aerospace and Airbus have completed the first phase of a next-generation helicopter propulsion study that targets modular gearboxes for open-rotor layouts. RENK Group, traditionally a land-systems gearbox leader, has earmarked nearly EUR 500 million (USD 584.89 million) in capacity and R&D to exploit surging defense budgets for heavy-lift aircraft and tracked vehicles. Meanwhile, additive-focused niche suppliers are working on rapid-turnaround spares niches, exemplified by Avio Aero’s gearshaft HVOF repair cell that cut TAT from 30 days to one week.

Strategic competition centers on mastering high-temperature material systems, digital-twin certification workflows, and HUMS-enabled service offerings. Suppliers with strong balance sheets and global MRO footprints can underwrite multi-year development while guaranteeing worldwide asset availability, a decisive advantage as fleet managers demand reliability contracts rather than standalone hardware.

Aircraft Gearbox Industry Leaders

Rolls-Royce plc

Safran SA

RTX Corporation

GE Avio S.r.l.

Liebherr-International Deutschland GmbH (Liebherr Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: XTI Aerospace, Inc. selected Triumph Geared Solutions, Formsprag Clutch, and Kamatics Corporation to design, develop, and manufacture the drivetrain system for its innovative TriFan 600 xVTOL aircraft.

- July 2024: Triumph Group's Geared Solutions business secured a contract from GE Aerospace to supply the auxiliary gearbox for the F404 engine. The gearbox may support platforms like the Boeing T7-A Red Hawk.

Global Aircraft Gearbox Market Report Scope

| Reduction Gearbox (RGB) |

| Accessory Gearbox (AGB) |

| Actuation Gearbox |

| Tail-Rotor Gearbox |

| Auxiliary Power Unit (APU) |

| Fixed-Wing Aircraft | Commercial | Narrowbody Aircraft |

| Widebody Aircraft | ||

| Regional Jets | ||

| Business Jets | ||

| Piston and Turboprop Aircraft | ||

| Military | Fighter Jets | |

| Transport Aircraft | ||

| Special-Mission Aircraft | ||

| Rotorcraft | Civil Helicopters | |

| Military Helicopters | ||

| Unmanned Aerial Vehicles (UAVs) | ||

| Engine |

| Airframe |

| Auxiliary Power Unit (APU) |

| Line-fit |

| Retrofit |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Gearbox Type | Reduction Gearbox (RGB) | ||

| Accessory Gearbox (AGB) | |||

| Actuation Gearbox | |||

| Tail-Rotor Gearbox | |||

| Auxiliary Power Unit (APU) | |||

| By Aircraft Type | Fixed-Wing Aircraft | Commercial | Narrowbody Aircraft |

| Widebody Aircraft | |||

| Regional Jets | |||

| Business Jets | |||

| Piston and Turboprop Aircraft | |||

| Military | Fighter Jets | ||

| Transport Aircraft | |||

| Special-Mission Aircraft | |||

| Rotorcraft | Civil Helicopters | ||

| Military Helicopters | |||

| Unmanned Aerial Vehicles (UAVs) | |||

| By Application | Engine | ||

| Airframe | |||

| Auxiliary Power Unit (APU) | |||

| By Fit | Line-fit | ||

| Retrofit | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the aircraft gearbox market?

The aircraft gearbox market size stands at USD 3.14 billion in 2025 and is projected to reach USD 4.45 billion by 2030, reflecting a 7.22% CAGR.

Which gearbox type generates the highest revenue?

Reduction gearboxes dominate, accounting for 42.5% of 2024 revenue thanks to their central role in geared-turbofan propulsion.

Which region is growing fastest?

Asia-Pacific is forecasted to expand at an 8.97% CAGR through 2030, driven by indigenous aircraft programs in China and India.

How are airlines improving gearbox reliability?

Operators are adopting condition-based monitoring systems that track vibration, temperature, and oil debris to predict maintenance needs and reduce unscheduled removals.

What impact do hybrid-electric aircraft have on gearbox demand?

Hybrid-electric concepts require high-ratio, lightweight reduction gearboxes to couple electric motors and propellers, creating a new growth avenue for specialized suppliers.

Page last updated on: