Aircraft Water And Waste Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

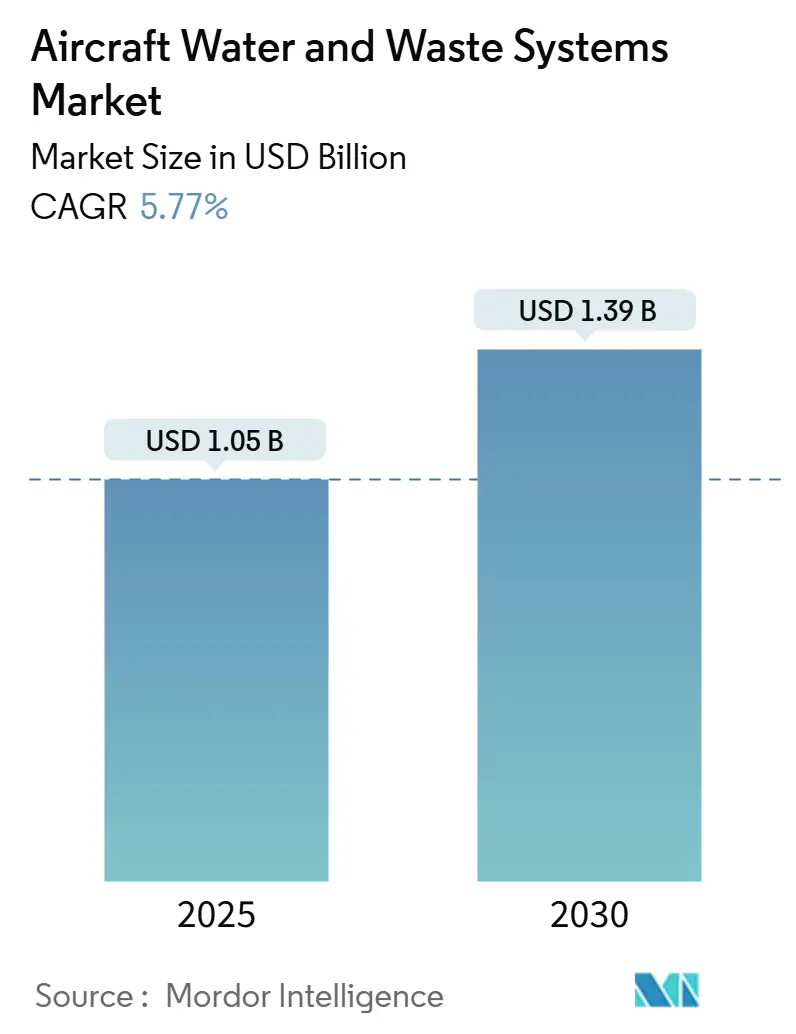

| Market Size (2025) | USD 1.05 Billion |

| Market Size (2030) | USD 1.39 Billion |

| Growth Rate (2025 - 2030) | 5.77% CAGR |

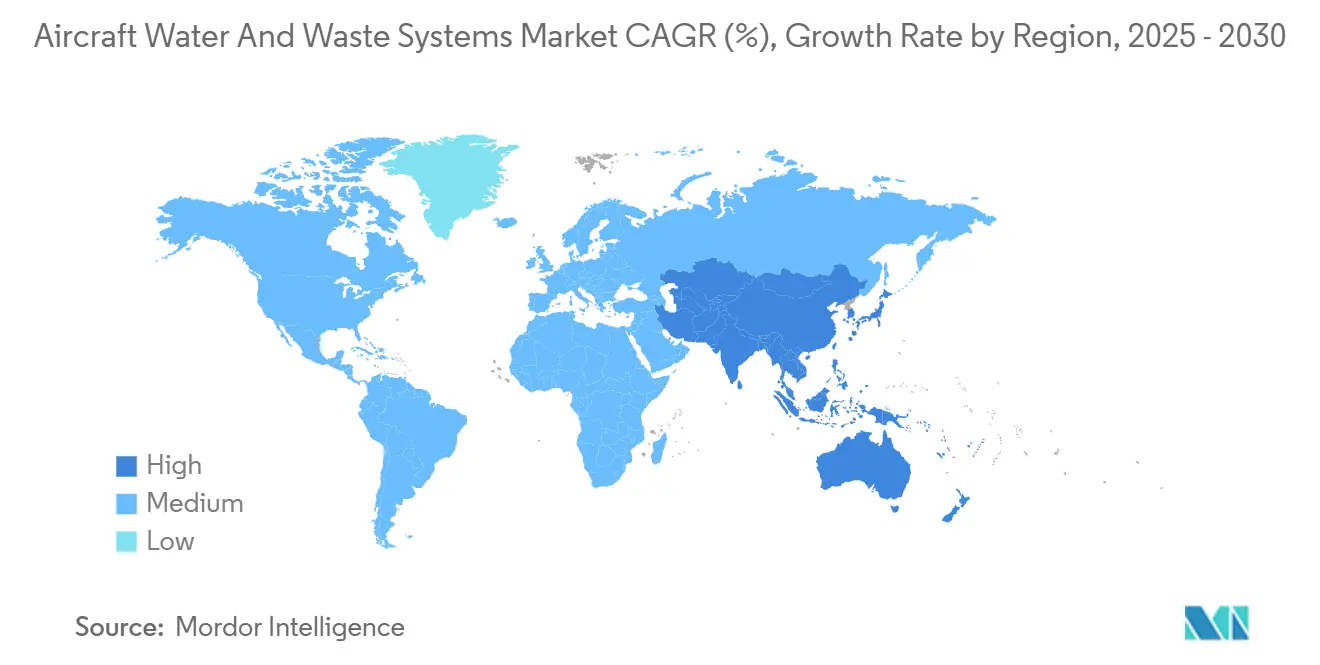

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Water And Waste Systems Market Analysis by Mordor Intelligence

The aircraft water and waste systems market size was valued at USD 1.05 billion in 2025 and is forecasted to reach USD 1.39 billion by 2030, advancing at a 5.77% CAGR. Demand tracks the airline sector’s rebound, with Boeing projecting deliveries of almost 44,000 commercial jets through 2043, three-quarters of them single-aisle platforms, thereby expanding the installed base that requires reliable potable-water, vacuum-waste, and disinfection solutions.[1]Source: Boeing Communications, “Boeing Forecasts Demand for Nearly 44,000 New Airplanes Through 2043,” boeing.mediaroom.com Regulatory tightening around the US Environmental Protection Agency’s Aircraft Drinking Water Rule and new PFAS limits compel carriers to modernize aging tanks, lines, and sensors to remain compliant. Sustainability imperatives add another layer of momentum: grey-water loops and lightweight composite tanks offer measurable fuel-burn and CO2 savings that fit within corporate net-zero roadmaps. On the competitive side, moderate consolidation persists; JAMCO retains half the global wide-body lavatory share, yet retrofit specialists and technology newcomers are gaining ground where airlines require faster delivery cycles and cabin densification drives compact-lavatory adoption.

Key Report Takeaways

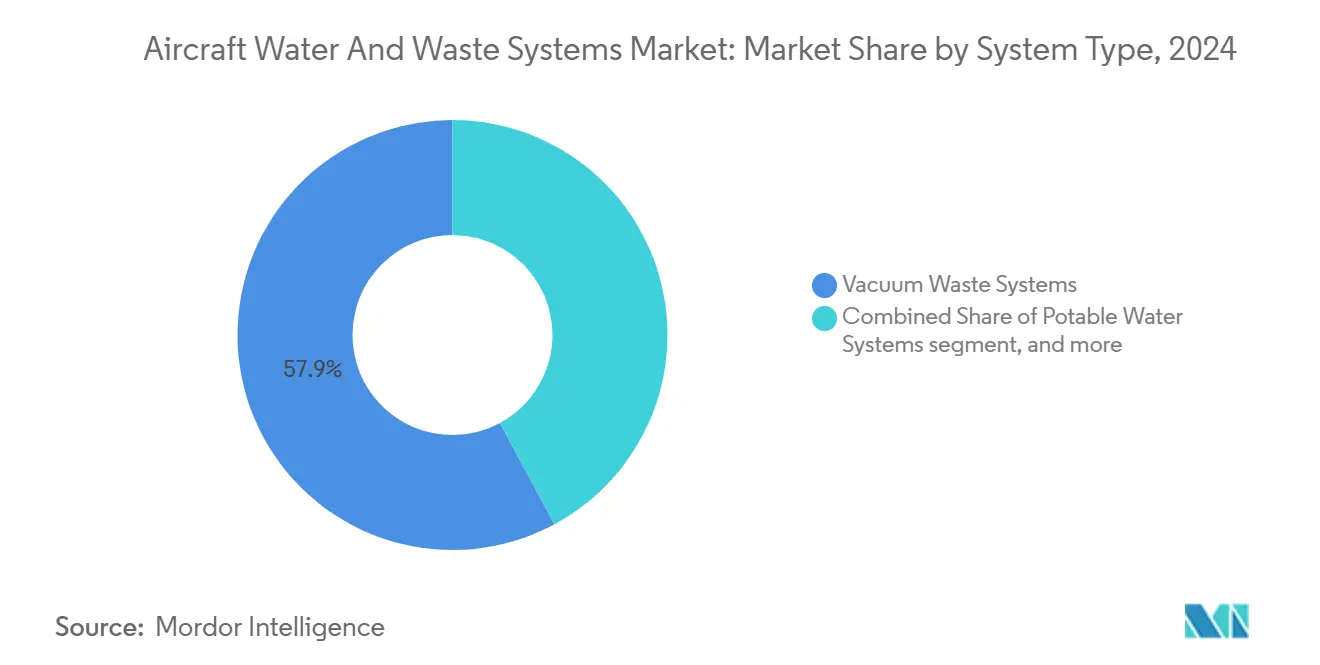

- By system type, vacuum waste units held 57.87% revenue in 2024, while grey-water reuse equipment is projected to post a 10.40% CAGR to 2030.

- By aircraft type, narrowbody platforms accounted for 49.70% of the aircraft water and waste systems market share in 2024; business jets are expected to expand at 8.34% CAGR through 2030.

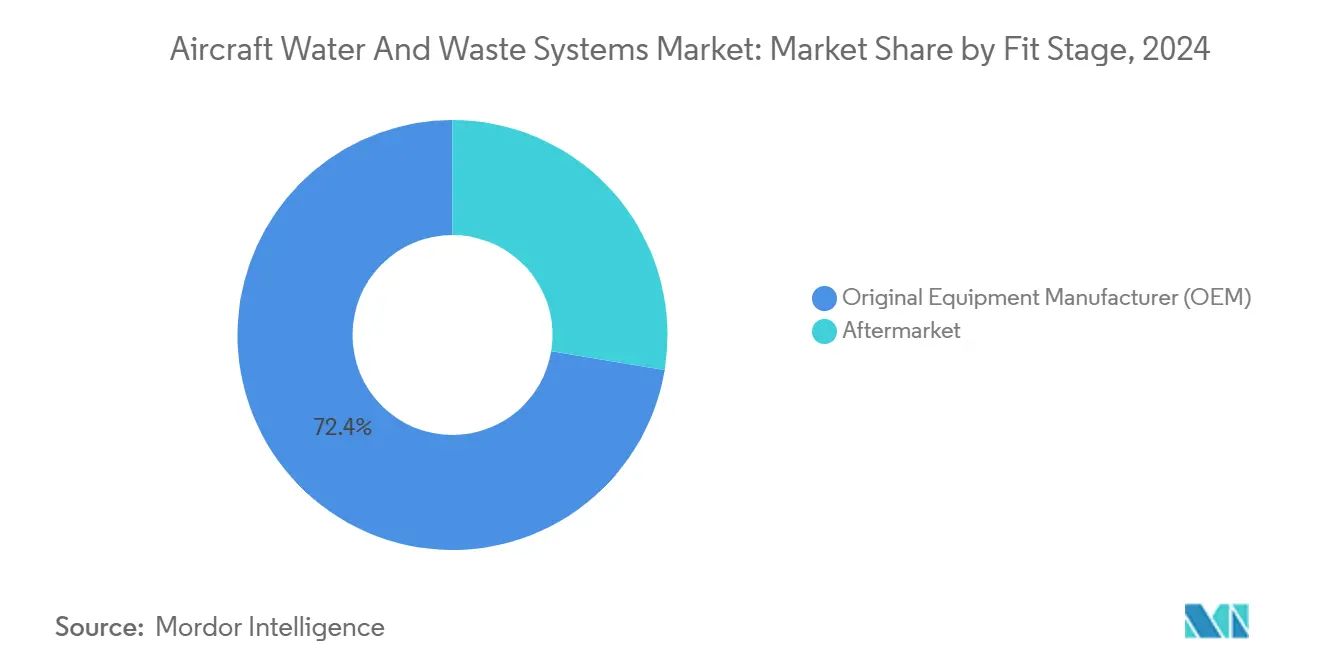

- By the fit stage, OEM installations represented 67.31% of the aircraft water and waste systems market size in 2024; aftermarket retrofits are forecasted to advance at a 9.24% CAGR to 2030.

- By end user, commercial and cargo airlines captured 72.40% of 2024 revenue, whereas VIP and business aviation led growth at 8.57% CAGR to 2030.

- By geography, North America dominated with 37.70% of 2024 revenue; Asia-Pacific shows the fastest trajectory, with a 6.89% CAGR toward 2030.

Global Aircraft Water And Waste Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-pandemic rebound in commercial aircraft deliveries | +1.2% | Global, with strongest impact in Asia-Pacific and North America | Medium term (2-4 years) |

| Stricter potable-water and lavatory-leak regulations | +0.8% | North America and EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Lightweight composite tanks and smart-sensor upgrades | +0.6% | Global, led by North America and Europe | Medium term (2-4 years) |

| Airlines’ cabin-retrofit wave for passenger experience | +0.7% | Global, with premium focus in North America and Europe | Short term (≤ 2 years) |

| Grey-water reuse loops for fuel-burn reduction | +0.9% | Global, driven by sustainability mandates in EU and North America | Medium term (2-4 years) |

| On-board ozone/UV disinfection retrofits | +0.5% | Global, accelerated adoption in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Post-pandemic rebound in commercial aircraft deliveries

Boeing’s long-term forecast underscores sustained jet demand as traffic has exceeded 2019 levels in every region, prompting airlines to lock in fleet-growth slots despite near-term delivery delays caused by parts shortages. Airbus trimmed its 2024 handover target to 770 units because of cabin-equipment bottlenecks, prolonging retrofit windows for incumbent fleets.[2]Source: Airbus Newsroom, “Airbus Provides 2024 Guidance Update,” airbus.com The single-aisle backlog, representing 76% of global orders, standardizes potable-water line diameters and vacuum pressures, lowering unit costs for component suppliers. Asia-Pacific carriers have 4,430 jets on order and request lighter, more efficient tanks to unlock mission range on secondary routes. System vendors therefore enjoy a dual-channel opportunity: line-fit volumes tied to new builds and a retrofit surge as operators keep older aircraft flying while production slots remain scarce.

Stricter potable-water and lavatory-leak regulations

The EPA now requires coliform sampling plans and PFAS testing that extend to every US-registered aircraft serving at least 25 passengers daily, with full PFAS compliance mandatory by April 2029. Airlines must also replace AFFF firefighting foam with fluorine-free alternatives under FAA rules, adding complexity to maintenance schedules. European agencies are developing parallel potable-water protocols, potentially forcing global carriers to certify dual-spec hardware. Large network airlines absorb the compliance burden through centralized engineering teams, whereas regional operators often outsource line checks, raising demand for turnkey water-system service packages. OEMs are pre-certifying new tanks and hoses to the tighter standards, and retrofit kits are bundled with sampling valves and smart-sensor ports that reduce manual labor.

Lightweight composite tanks and smart-sensor upgrades

Type-V composite pressure vessels lower empty weight by up to 20% versus aluminum liners, freeing payload or trimming fuel burn on long sectors. Ultrasonic level gauges in these tanks enable continuous capacity read-outs without intrusive probes, allowing crews to upload only the required water mass for each flight. Yet supply-chain fragility persists: resin shortages lengthen lead times, and geopolitical disruptions have cut titanium supply by 12% over five years, elevating bill-of-material costs. Airlines counter by signing multi-year spares contracts while system integrators diversify material sourcing across North America and Asia. Therefore, the shift to advanced composites delivers efficiency gains but necessitates careful inventory planning.

Grey-water reuse loops for fuel-burn reduction

Diehl Aviation’s ECO system channels hand-wash water to toilet flush reservoirs, eliminating 250 liters of unnecessary potable load on each B787 sector and saving nearly 90 tons of CO2 annually per aircraft. Airlines such as Iberia report shorter return-on-investment periods because reduced uplift directly translates into fuel savings on four-hour stage lengths. Grey-water units combine anaerobic filtration with UV disinfection to meet potable-reuse guidelines without harmful by-products. Early adopters show reliability comparable to legacy systems once maintenance crews receive targeted training. Certification hurdles remain, yet the business case aligns with corporate ESG targets, accelerating fleet-wide rollouts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High maintenance cost of vacuum waste lines | −0.4% | Global, particularly affecting cost-sensitive carriers | Long term (≥ 4 years) |

| Composite-material supply-chain bottlenecks | −0.6% | Global, with acute impact in North America and Europe | Medium term (2-4 years) |

| PFAS and micro-contaminant water-quality rules | −0.3% | North America and EU, with regulatory spillover to Asia-Pacific | Long term (≥ 4 years) |

| Cabin densification crowding lavatory footprint | −0.2% | Global, driven by low-cost carrier expansion | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High maintenance cost of vacuum waste lines

Vacuum waste systems rely on pumps, ejectors, and sensors, requiring specialist tooling and frequent gasket replacement to prevent odor and blockage. Airlines budget extra labor hours for line-flush procedures mandated under the Aircraft Drinking Water Rule, inflating maintenance overhead. Component downtime can cause operational delays and passenger dissatisfaction, especially on high-utilization narrowbody fleets. Cost-sensitive operators may delay upgrades or select hybrid solutions, slowing replacement cycles.

Composite-material supply-chain bottlenecks

Aerospace manufacturers report longer lead times for carbon fiber, epoxy resins, and honeycomb cores, raising unit costs for water tanks and service panels.[3]Source: Boston Consulting Group Analysts, “Fixing Aerospace’s Supply Chain for Casting and Forging,” bcg.com Titanium forgings used in waste-line couplings face geopolitical exposure to Russian and Ukrainian supply sources, pressing OEMs to stockpile raw material at elevated prices. Workforce shortages in composite lay-up and autoclave operations further limit capacity. These constraints hinder short-term volume expansion even as the long-term demand outlook remains positive.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: Vacuum Waste Leads, Grey-Water Scales

Vacuum waste platforms dominated the aircraft water and waste systems market in 2024, with a 57.87% share, reflecting airline confidence in proven suction-flush reliability across altitude and temperature ranges. Grey-water reuse solutions are projected to deliver a 10.40% CAGR because carriers can cut uplifted potable weight without compromising hygiene standards. The aircraft water and waste systems market size tied to disinfection modules is forecast to climb steadily as UV emitters migrate from widebody galleys into single-aisle lavatories, aided by falling diode prices.

Manufacturers increasingly market integrated suites that bundle vacuum pumps, composite tanks, and UV disinfectors within a unified control architecture, reducing wiring count and maintenance access time. Smart-sensor nodes feed fleet-health dashboards, allowing predictive part replacement that avoids on-wing faults. Suppliers investing in data analytics partnerships with airlines gain recurring revenue from software licenses and hardware sales.

By Aircraft Type: Narrow-Body Core, Business-Jet Upside

Narrowbody jets commanded a 49.70% market share in 2024, anchored by high flight frequencies across domestic networks prioritizing quick-turn lavatory reliability. In contrast, business jets will expand at an 8.34% CAGR through bespoke cabin renovations integrating bidet functions, touch-free faucets, and antimicrobial surface coatings—features now expected by high-net-worth travelers. The aircraft water and waste systems market share for widebodies remains stable, supported by ultra-long-haul routes where larger tanks and redundant pumps are mission-critical.

OEM selection patterns highlight shifting priorities: JAMCO supplies every B787 lavatory, yet Gulfstream’s G700 leverages Collins Aerospace’s advanced nuclease-coated sinks to reassure passengers on intercontinental missions. Regional-jet programs, including the D328eco turboprop, embed fuel-cell-ready water heaters to align with future hydrogen propulsion pathways.

By Fit Stage: OEM Volume Versus Aftermarket Agility

Line-fit installations captured 67.31% of 2024 revenue, showing airlines still prefer factory-integrated plumbing that protects warranty coverage and optimizes weight distribution. Retrofit momentum, however, will outpace OEM growth at 9.24% CAGR as operators extend airframe life past original economic thresholds while updating systems to meet stricter water-quality rules. The aircraft water and waste systems market size for retrofits jumps whenever regulators publish new sampling protocols, because carriers must modify even relatively young fleets.

Aftermarket players tout fast-track supplemental type certificates that install modular lavatories during C-checks, cutting downtime to less than seven days. Service bulletins increasingly pair water-system upgrades with cabin densification, allowing airlines to generate incremental seat revenue that offsets retrofit cost within a single financial year.

By End User: Commercial Airlines Dominate, VIP Aviation Accelerates

Commercial and cargo carriers held 72.40% of 2024 demand, benefiting from a fleet scale that standardizes part numbers and drives volume discounts at purchase negotiations. VIP and business aviation, while representing a smaller installed base, will post an 8.57% CAGR as operators pursue luxury amenity packages that emphasize health-centric features such as reverse-osmosis purification and aroma-infused washrooms. MRO firms capitalize by offering white-glove refurbishment programs, synchronizing interior redesign and system overhauls.

The segment split underscores divergent priorities: network airlines chase the lowest life-cycle cost per available seat kilometer, whereas charter operators value exclusivity and brand prestige. Yet both customer groups converge on digital monitoring tools that feed operational dashboards, signaling that data-driven maintenance will become the industry standard across all tiers.

Geography Analysis

North America contributed 37.70% of 2024 revenue due to strict EPA oversight, expansive MRO footprints, and incumbency advantages for Collins Aerospace, Diehl Aviation, and Astronics. Carriers such as Delta retrofit single-aisle fleets with compact lavatories that maintain accessibility compliance while freeing extra seat rows, supporting revenue optimization efforts.

Asia-Pacific is the fastest-growing region at 6.89% CAGR through 2030. Its 4,430-unit order backlog steers local suppliers to co-locate manufacturing sites in Indonesia, India, and China, reducing logistics cost and easing import-duty exposure. Government initiatives—from India’s UDAN connectivity scheme to China’s carbon-neutral airport goals reinforce the adoption of lightweight tanks and grey-water loops that cut fuel burn on high-frequency short hops.

Europe remains a technology incubator, with Airbus pushing cabin-retrofit programs emphasizing recyclable composite lavatories and low-flow fixtures to align with Fit for 55 emissions targets. The region’s carriers are early adopters of ultraviolet-C disinfection modules, a trend supported by the Water Research Foundation’s endorsement of UV/chlorine advanced oxidation for potable reuse. Brexit-related certification divergence still introduces complexity for UK operators sourcing parts from EU vendors, but mutual-recognition talks ease the paperwork burden.

Competitive Landscape

The aircraft water and waste systems market shows moderate concentration. Collins Aerospace leverages its nacelle and interiors portfolio to supply advanced lavatories to Boeing and Airbus single-aisle lines. At the same time, Diehl Aviation positions integrated grey-water reuse loops as a differentiator tied to fuel-efficiency KPIs.

Strategic collaborations intensify competitive dynamics. RTX agreed to furnish power units and nacelles for JetZero’s blended-wing demonstrator, potentially unlocking new system-architecture paradigms that will ripple into cabin-plumbing designs. JAMCO and Japan Aerospace Exploration Agency unveiled a “Metamorphic” lavatory that converts two adjacent units into an accessible enclosure without sacrificing seat count, addressing regulatory and inclusivity pressures simultaneously.

Supply-chain constraints shape strategic behavior; OEMs diversify resin and titanium sourcing, while tier-one suppliers acquire smaller composites shops to secure capacity. Digital-service models gain traction, with predictive analytics subscriptions providing recurring revenue that partially insulates companies from the cyclicality of aircraft deliveries.

Aircraft Water And Waste Systems Industry Leaders

RTX Corporation

Safran SA

Diehl Stiftung & Co. KG

JAMCO Corporation

AeroControlex Group Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Diehl Aviation initiated the construction of a new production facility in Craiova, Romania, to expand its manufacturing footprint. The facility will produce components for commercial passenger aircraft, ensuring reliable deliveries to meet rising production rates and addressing the growing demand in the aviation sector.

- April 2024: JAMCO and JAXA introduced an accessible “Metamorphic” lavatory prototype for single-aisle cabins.

Global Aircraft Water And Waste Systems Market Report Scope

| Potable Water Systems |

| Vacuum Waste Systems |

| Grey-Water Reuse Units |

| Disinfection Modules (UV/Ozone) |

| Narrowbody Aircraft |

| Widebody Aircraft |

| Regional Jets |

| Business Jets |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| Commercial and Cargo Airlines |

| MRO Service Providers |

| VIP/Business Aviation |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By System Type | Potable Water Systems | ||

| Vacuum Waste Systems | |||

| Grey-Water Reuse Units | |||

| Disinfection Modules (UV/Ozone) | |||

| By Aircraft Type | Narrowbody Aircraft | ||

| Widebody Aircraft | |||

| Regional Jets | |||

| Business Jets | |||

| By Fit Stage | Original Equipment Manufacturer (OEM) | ||

| Aftermarket | |||

| By End User | Commercial and Cargo Airlines | ||

| MRO Service Providers | |||

| VIP/Business Aviation | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the aircraft band clamp market in 2025?

The aircraft water and waste systems market size stands at USD 1.05 billion in 2025.

What is the forecast CAGR for these systems through 2030?

Industry revenue is projected to expand at a 5.77% CAGR over 2025-2030.

Which system type is growing the fastest?

Grey-water reuse equipment leads growth with a 10.40% CAGR forecast to 2030.

Which region offers the highest growth opportunity?

Asia-Pacific shows the strongest outlook at a 6.89% CAGR thanks to its 4,430-unit aircraft backlog.

What is driving retrofit demand?

Stricter EPA potable-water rules and cabin densification programs are prompting carriers to upgrade existing fleets.

Who holds the leading share in lavatory manufacturing?

JAMCO Corporation supplies roughly 50% of widebody lavatories, chiefly for B787 and other twin-aisle models.

Page last updated on: