Market Overview

| Study Period | 2019 - 2031 |

|---|---|

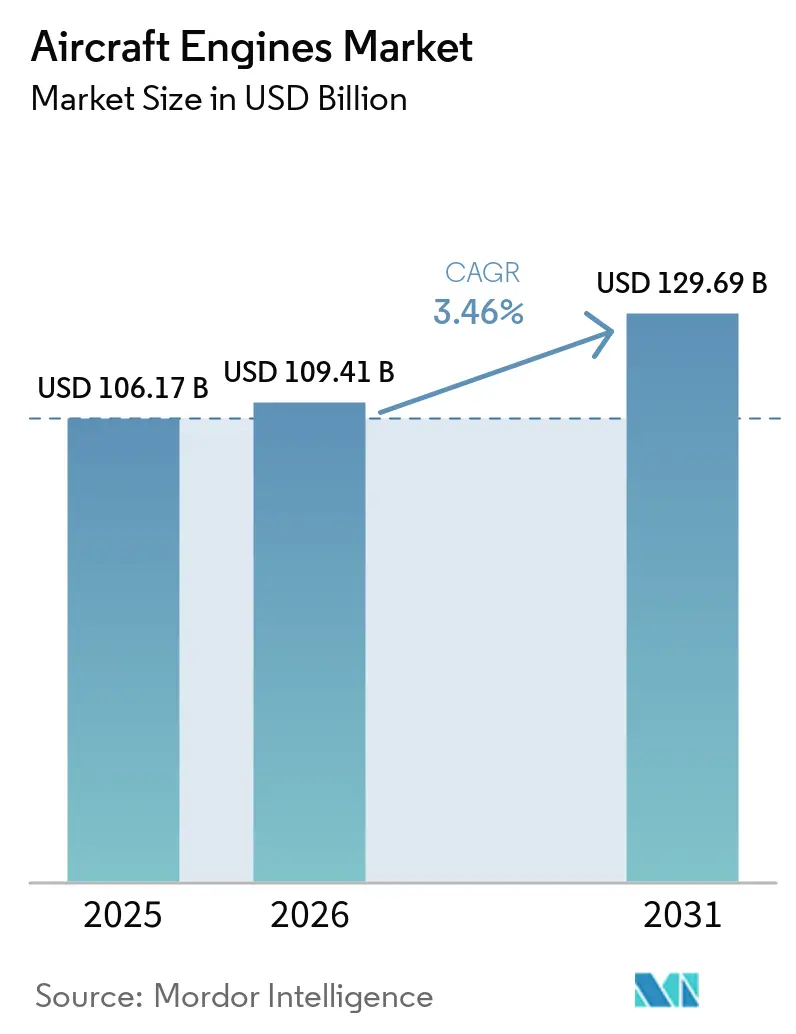

| Market Size (2026) | USD 109.41 Billion |

| Market Size (2031) | USD 129.69 Billion |

| Growth Rate (2026 - 2031) | 3.46% CAGR |

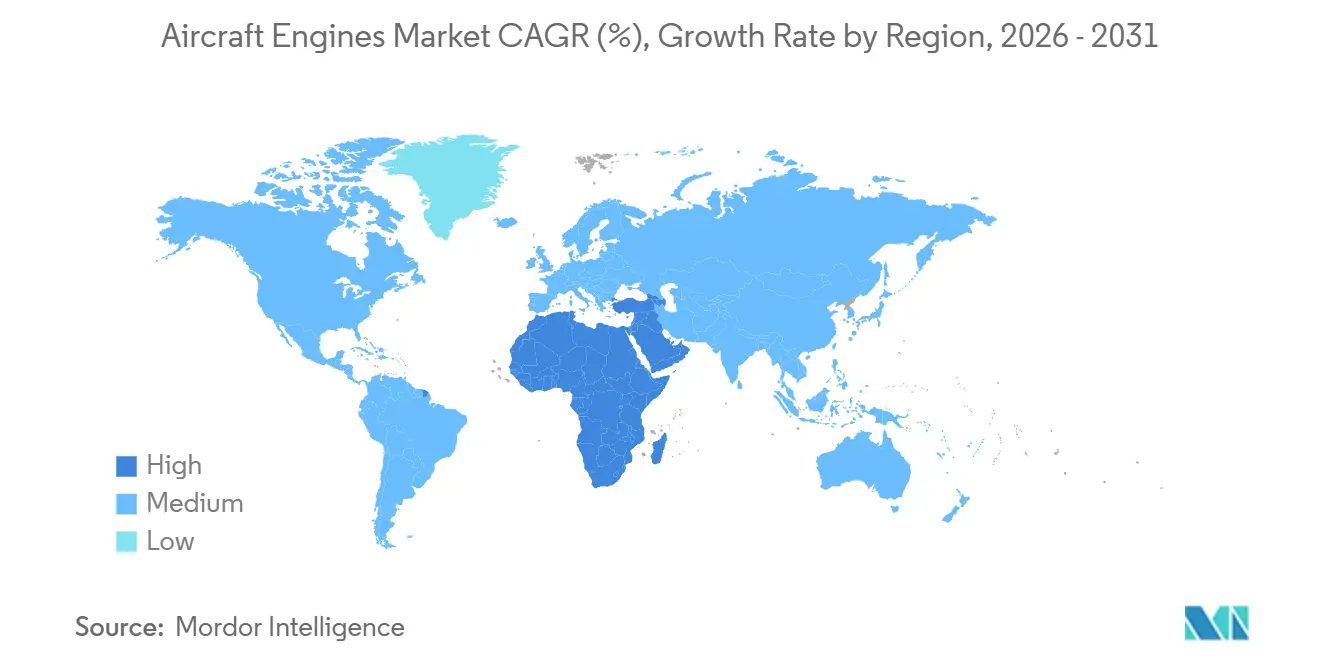

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Engines Market Analysis by Mordor Intelligence

The aircraft engines market size is expected to grow from USD 106.17 billion in 2025 to USD 109.41 billion in 2026 and is forecasted to reach USD 129.69 billion by 2031 at a 3.46% CAGR over 2026-2031. Current growth is supported by rising narrowbody production, a high-thrust widebody replacement cycle, and military re-engagement, yet tempered by persistent groundings of the Pratt & Whitney PW1100G. OEMs are prioritizing the readiness of sustainable aviation fuel (SAF), investing in hydrogen-combustion demonstrators, and expanding geared-turbofan capacity. Independent MRO networks are expanding their capabilities by adding engine bays and predictive-maintenance tools, which compress aftermarket margins. Regionally, Asia-Pacific continues to generate one-third of engine revenue. At the same time, the Middle East is showing the quickest expansion, driven by hot-and-high operations and record twin-aisle orders. The overall realignment of supply and demand positions the aircraft engine market for steady, margin-focused growth amid tightening regulatory and sustainability requirements.

Key Report Takeaways

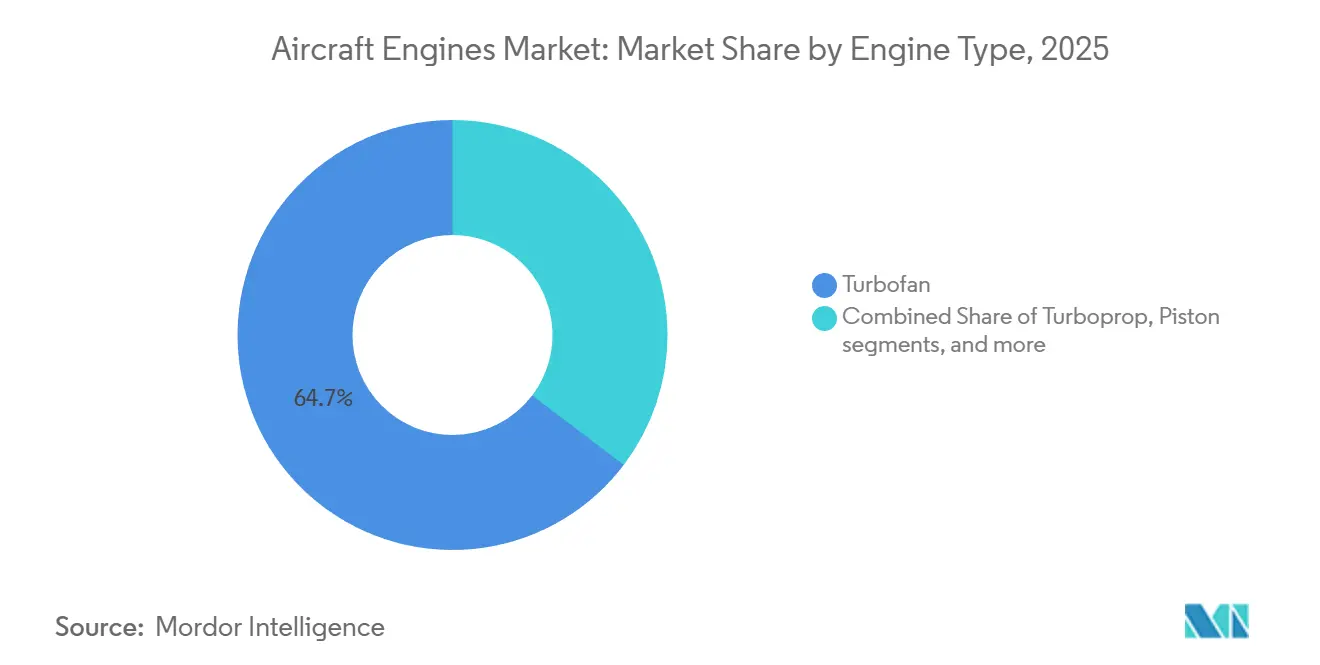

- By engine type, turbofan configurations led the aircraft engines market with a 64.67% share in 2025; hybrid-electric propulsion is forecasted to expand at a 7.17% CAGR through 2031.

- By aircraft type, commercial narrowbodies accounted for 43.12% of the aircraft engines market size in 2025, while advanced air mobility vehicles are anticipated to grow at a rate of 8.64% through 2031.

- By technology, geared-turbofan platforms commanded 36.06% of 2025 revenue; adaptive-cycle engines are projected to register a 9.15% CAGR over the forecast horizon.

- By thrust class, the 25,001–50,000 lbf bracket held 39.33% of the aircraft engines market share in 2025; engines exceeding 50,000 lbf are estimated to rise at a 6.78% CAGR through 2031.

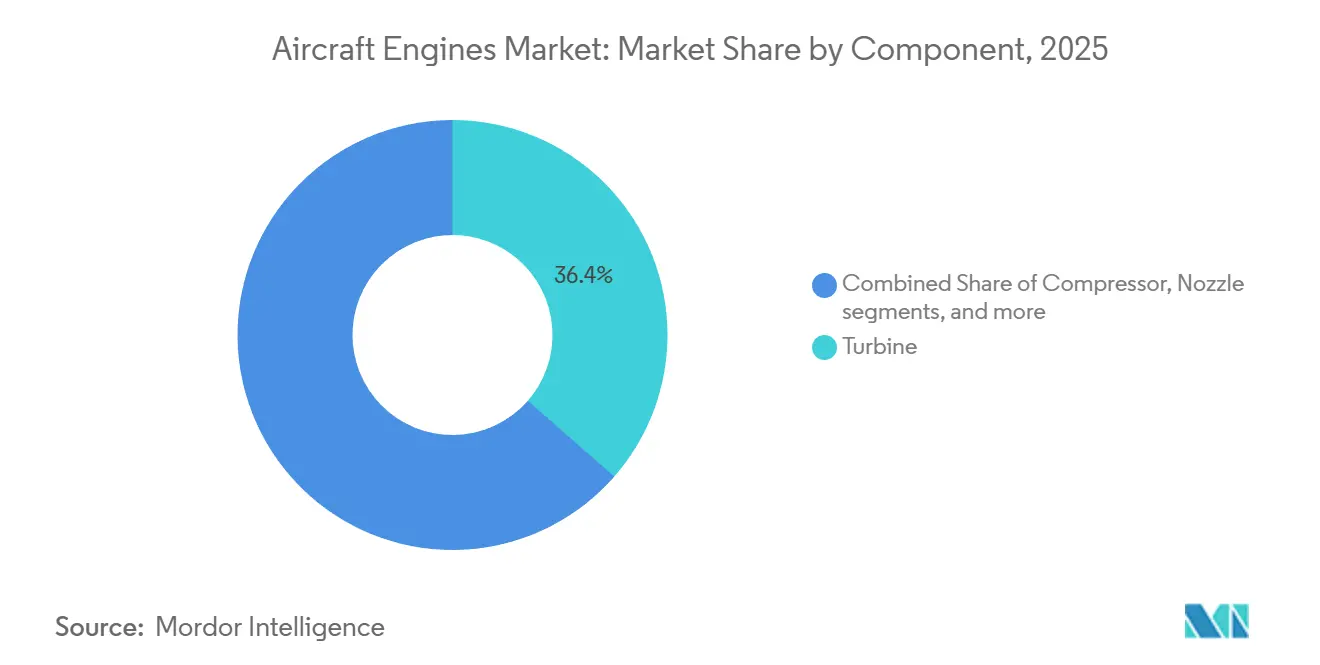

- By component, turbine modules represented 36.43% of 2025 revenue, whereas gearbox systems are poised for a 5.46% CAGR to 2031.

- By end-user, OEM factory-fit deliveries accounted for 54.17% of the aircraft engines market size in 2025; the replacement and aftermarket segment is expected to grow at 4.89% over the same period.

- By geography, the Asia-Pacific region held 33.19% of the 2025 revenue, while the Middle East is expected to grow at a 6.38% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Aircraft Engines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Twin-aisle production ramp-up post supply-chain recovery | +0.8% | North America, Europe | Medium term (2-4 years) |

| Fleet-wide shift toward LEAP and GTF engines in fast-growing Asian carriers | +1.2% | Asia-Pacific, Middle East | Short term (≤ 2 years) |

| NATO transport and tanker fleet modernization programs | +0.4% | North America, Europe | Long term (≥ 4 years) |

| Helicopter fleet renewal for offshore energy operations | +0.3% | Offshore regions worldwide | Medium term (2-4 years) |

| EU mandates for 100% SAF-ready engines in new type certificates | +0.5% | Europe, global OEM compliance | Short term (≤ 2 years) |

| Leasing-driven expansion of African regional-jet operators | +0.2% | Africa, South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Twin-Aisle Production Ramp-Up Post Supply-Chain Recovery

Boeing and Airbus exited 2025 with production rates still below their pre-pandemic peaks, yet both plan to increase monthly output between 2026 and 2028. Lessors reported double-digit leasing rate increases for widebody aircraft, signaling a premium for high-thrust engines that power the B787, A350, and forthcoming freighter variants. OEMs are recalibrating their capacity to balance the thin-margin, narrowbody volume with lucrative widebody aftermarket prospects. Engine suppliers now face allocation decisions that influence shop-visit cascades over 25-year service lives. The resulting production ramp reshapes demand timing across turbine, nozzle, and gearbox value streams.

Fleet-Wide Shift Toward LEAP and GTF Engines in Fast-Growing Asian Carriers

Asia-Pacific carriers placed more than 1,200 narrowbody orders in 2024–2025, with Air India and VietJet Aviation alone accounting for two-thirds of the volume. GE Aerospace expects LEAP deliveries to exceed 1,688 units in 2026, with 40% of these units entering Asian fleets. Pratt & Whitney’s revised powder-metallurgy process aims to restore PW1100G availability by 2027. Airline fleet planners now weigh operational risk more heavily than nominal fuel-burn deltas when selecting engines. The competitive edge remains with CFM in the near term; however, improved PW1100G reliability could rebalance the share during mid-period retrofits.

NATO Transport and Tanker Fleet Modernization Programs Boosting Military Engine Demand

Denmark and Sweden joined NATO’s MRTT consortium in 2025, increasing the aggregate orders to 12 aircraft for delivery in 2028–2029, each equipped with dual Trent 700 or V2500 powerplants.[1]NATO, “Multi-Role Tanker Transport Program Expansion,” nato.int Concurrently, the US Air Force funds GE’s XA102 and Pratt & Whitney’s XA103 adaptive-cycle demonstrators that promise 25% fuel-burn savings over legacy F135s. A successful NGAP transition would exceed 1,000 deliveries in the 2030s, creating a counter-cyclical revenue stream for engine OEMs. European ministries place incremental orders for the C-130J and A400M, further stabilizing defense demand. Military propulsion, therefore, decouples from civil cycles and underpins long-term engineering investment.

Helicopter Fleet Renewal for Offshore Energy Operations Raising Turboshaft Deliveries

Offshore wind expansion above 100 GW by 2030 drives requirements for new AW189 and H175 helicopters that rely on Safran Makila and Pratt & Whitney Canada PT6T powerplants. Operators demand higher power-to-weight ratios and improved single-engine-inoperative performance, in line with revised EASA Part 29 standards.[2]EASA, “Updated Part-29 Rotorcraft Standards,” easa.europa.eu Overhaul cycles are shortened in salt-spray environments, thereby elevating demand for replacement parts. OEMs respond with digital twin tools that predict hot-section deterioration. As oil-and-gas platform servicing rebounds, turboshaft deliveries enjoy a stable niche within the broader aircraft engine market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Slow standardization of hydrogen-combustion engine architectures | -0.6% | Global, concentrated in Europe and North America R&D hubs | Long term (≥ 4 years) |

| High-temperature durability issues in hot-and-high Middle-East operations | -0.4% | Middle East primary, secondary effects in South Asia and North Africa | Short term (≤ 2 years) |

| Margin pressure from independent MRO capacity growth | -0.5% | Global, most acute in North America and Europe | Medium term (2-4 years) |

| Supply chain constraints for advanced materials and components | -0.5% | Global, concentrated in North America and Europe manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Slow Standardization of Hydrogen-Combustion Engine Architectures

Competing liquid and gaseous hydrogen storage concepts lack harmonized certification frameworks, delaying scalable investment. Airbus ZEROe explores cryogenic tanks, while CFM RISE tests hydrogen combustors secondary to SAF priorities. The absence of ICAO guidance forces OEMs to fund bespoke compliance pathways, which in turn inflate program risk. Rolls-Royce and Pratt & Whitney conduct bench tests but defer launch decisions pending clarity on infrastructure. Without aligned standards, the aircraft engines market faces development cost uncertainty that moderates near-term momentum for hydrogen.

Margin Pressure from Independent MRO Capacity Growth

StandardAero, AAR, and Collins Aerospace added more than 50 engine bays in 2025, raising the third-party share of CFM56 and V2500 shop visits above 40%. OEM gross margins compress as line-replaceable-unit pricing faces competitive benchmarks. Regulatory directives require OEMs to share technical data, thereby limiting the exclusivity shields.[3]FAA, “Airworthiness Directives and Repair Data Policy,” faa.gov Airlines welcome lower overhaul invoices but assume increased oversight duties in the supply chain. The profitability reset places greater emphasis on long-term service agreements that bundle digital analytics and parts pools.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Engine Type: Hybrid-Electric Gains Traction

Turbofans accounted for 64.67% of 2025 revenue, underpinning medium- and long-haul activity across both civil and defense fleets. Hybrid-electric units, although currently at sub-5% market share, are projected to secure the fastest 7.17% CAGR as certification efforts progress. Early eVTOL approvals highlight regulatory receptiveness, and lightweight battery advances extend short-range payload. Turboprops maintain relevance for regional mobility, yet incremental efficiency gains lag those of geared turbofans. Turboshaft demand climbs with offshore helicopter cycles, while piston engines gradually cede share to turboprop retrofits. Geared accessory modules appearing on Rolls-Royce Pearl variants illustrate convergence between traditional and hybrid architectures. These shifts collectively diversify the aircraft engine market without displacing the primacy of turbofans.

End-user financing reflects the same pattern. Leasing firms backstop eVTOL programs, spreading risk across diversified portfolios. Supply chains reposition around high-cycle electric motors and power electronics, aligning with automotive-grade manufacturing. OEMs leverage modular designs that allow combustion core upgrades within hybrid-electric envelopes. For suppliers, gearbox lubrication and thermal management remain priority R&D targets, supporting the segment’s outperformance within the broader aircraft engines market.

By Aircraft Type: AAM Vehicles Lead Growth

Commercial narrowbodies represented 43.12% of 2025 revenue, supported by B737 MAX and A320neo deliveries; however, advanced air mobility (AAM) vehicles showed the highest 8.64% CAGR. Joby and Archer approvals validate urban-route economics and attract cargo innovators focused on time-critical logistics. Widebody output recovers more slowly, constrained by fuselage and engine supply bottlenecks. Military cargo and tanker modernization outpaces fighter production in the near term, stabilizing turbofan line utilization. Business-jet orders concentrate at the ultra-long-range end of the spectrum, where Pearl and Passport engines deliver cabin altitude and speed metrics valued by fractional-ownership clients. UAV propulsion growth continues steadily within ISR and strike platforms. Cross-segment interplay widens aftermarket complexity, prompting MROs to specialize by thrust class and mission type.

AAM vehicle integration accelerates the electrification of subsystems, feeding demand for high-power-density generators that couple with small gas turbines. In parallel, widebody cargo conversions sustain production lines for high-thrust engines. Airlines diversify fleet compositions to hedge against range-specific recovery trajectories. The aircraft engines market, therefore, balances mature volume drivers with emergent growth niches.

By Technology: Adaptive-Cycle Engines Emerge

Geared-turbofan designs held 36.06% of 2025 revenue, delivering double-digit fuel-burn gains and lower noise signatures. Adaptive-cycle engines, however, show the steepest 9.15% CAGR outlook as the timelines for sixth-generation fighters crystallize. Variable-bypass capability meets stealth cruise and trans-supersonic dash requirements, ensuring defense procurement support. Conventional turbofan and turboprop systems still underpin existing fleets but face incremental rather than step-change efficiency improvements. Contra-rotating open-rotors promise a 20% lower fuel burn, yet they await acoustic validation and new airframe designs. Hybrid-electric modules slide into auxiliary power roles ahead of primary propulsion adoption. Technology fragmentation compels OEMs to run parallel development tracks, straining R&D budgets but expanding future option value across the aircraft engines market.

Certification bodies adapt guidance for variable-cycle testing and digital twin validation, compressing timeline uncertainty. Supplier ecosystems are evolving toward additive manufacturing for complex, adaptive-cycle components. As demonstrators transition to low-rate initial production (LRIP), economies of scale remain limited, but long-term military contracts underwrite financial viability.

By Thrust Class: High-Thrust Engines Outpace Market

The 25,001 to 50,000 lbf category accounted for 39.33% of 2025 revenue; however, engines above 50,000 lbf are projected to expand at 6.78% through 2031, nearly twice the market average. Cargo conversions and rising long-haul passenger yields drive demand for the B777X and A350-1000, which in turn anchor GE9X and Trent XWB production lines. Regional jet and small narrowbody classes grow in line with the overall aircraft engines market, while sub-10,000 lbf segments face pilot and insurance headwinds. OEMs adjust capacity for single-piece fan-blisk machining and composite case curing to meet high-thrust schedules. Supply-chain localization initiatives in Japan and the UK diversify risk and hedge currency exposure. Rising thrust ratings push material science toward ceramic-matrix composites and next-generation thermal barrier coatings.

Operational stress in hot-and-high airports magnifies high-thrust spare-engine pools. Airlines accept higher capital costs in exchange for reliable thrust margins under extreme ambient conditions. Enhanced durability programs bundled into long-term service agreements illustrate OEM efforts to preserve lifecycle economics.

By Component: Gearbox Systems Accelerate

Turbine assemblies accounted for 36.43% of component revenue in 2025, reflecting complex super-alloy content and high replacement rates. Gearboxes, although accounting for a smaller share, are forecasted to have a 5.46% CAGR as geared-turbofan penetration widens. MTU Aero Engines invested USD 220 million in advanced machining at its Munich plant to meet its commitments for PW1000G gearbox output.[4]MTU Aero Engines, “Gearbox Component Facility Expansion,” mtu.de Enhanced lubrication and thermal designs extend the mean time between overhauls and improve propulsive efficiency. Compressor modules grow in tandem with overall engine production, whereas fan and nozzle components enjoy more extended service lives, moderating their growth rate. Digital part-tracking mandates from regulators are accelerating blockchain adoption among tier-two suppliers. Overall, component stratification drives targeted capital expenditure rather than linear scaling, aligning with the focus of the aircraft engines market on margin protection.

By End-User: Aftermarket Gains Momentum

OEM factory-fit engines comprised 54.17% of 2025 revenue, but the replacement and aftermarket segment is expected to rise 4.89% annually through 2031. CFM disclosed more than 1,000 LEAP performance restorations in 2025, underpinning USD 2 billion in service revenue. Independent MROs now command over 40% of CFM56 shop visits, up from 25% in 2020, applying price pressure on OEM proprietary networks. Airlines leverage competitive quotes to reduce cost per engine flight hour by up to 15%. Regulatory agencies compel OEMs to license repair procedures, further opening the field to third-party overhaul houses. Digital twins and predictive analytics become differentiators rather than optional add-ons. The aftermarket, therefore, evolves into a volume-driven, data-enabled arena within the aircraft engines market.

Geography Analysis

Asia-Pacific retained a 33.19% share in 2025, supported by China’s fleet growth and India’s manufacturing expansions. The Middle East, however, is expected to experience a 6.38% CAGR due to significant twin-aisle commitments and short maintenance cycles resulting from extreme ambient temperatures. North America benefits from B737 MAX volume and NGAP funding. Europe confronts supply-chain constraints and GTF groundings, softening its trajectory. South America and Africa use operating leases to modernize fleets, spreading capital risk while accessing efficiency gains. Local MRO infrastructure investment in Lagos, Nairobi, and Addis Ababa anchors regional capability growth. Indigenous engine programs in China and India are progressing but remain several years away from displacing imported power plants at scale. Geographic diversification thus supports resilience across the overall aircraft engine market.

Competitive Landscape

The aircraft engines market remains oligopolistic. Honeywell International, Inc., RTX Corporation, GE Aerospace, Rolls-Royce Holdings plc, and Safran SA together generated more than 80% of 2025 revenue. CFM expects LEAP deliveries to exceed 1,688 units in 2026 and plans to reach 2,100 by 2028 through a EUR 300 million (USD 349.92 million) capacity expansion in France. Pratt & Whitney launched upgraded PW1100G production, which removes powder-metal defects and funds a USD 7 billion retrofit effort. Rolls-Royce secured a USD 1.2 billion Trent 7000 order from Delta Air Lines that includes a 15-year TotalCare agreement.[5]Rolls-Royce, “Trent 7000 Contract with Delta,” rolls-royce.com GE-Safran-Airbus collaborations on hydrogen-combustion demonstrators highlight long-term strategic bets beyond conventional turbofans.

Independent MROs expand as the chief disruptors. StandardAero alone added 20 engine bays in 2025, pairing capacity with predictive analytics to undercut OEM service pricing. Data-access disputes arise as regulators push for open access to repair information, while striking a balance between safety oversight and market competition. In defense, GE and Pratt & Whitney contend for NGAP adoption, with the winner securing a production run exceeding 1,000 engines. Chinese and Russian programs aim for self-reliance yet endure performance gaps that delay Western substitution. Taken together, competitive intensity remains elevated, with sustainability, digital services, and defense programs dictating strategic positioning in the aircraft engines market.

Aircraft Engines Industry Leaders

Safran SA

General Electric Company

RTX Corporation

Honeywell International, Inc.

Rolls-Royce Holdings plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Wizz Air finalized negotiations to power its incoming A320neo fleet with Pratt & Whitney GTF engines.

- June 2025: GE Aerospace partnered with Kratos Defense to expand small-engine offerings for affordable unmanned systems.

- May 2025: Qatar Airways ordered more than 400 GE9X and GEnx engines, underpinning its forthcoming deliveries of the B777X and B787.

- February 2025: GE Catalyst turboprop secured FAA type certification after demonstrating 18% fuel-burn improvement over peer engines.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, we define the aircraft engine market as the value of all newly built powerplants installed on fixed- and rotary-wing airframes across commercial, military, and general-aviation fleets; auxiliary power units, used engines, and stand-alone aftermarket parts are out of scope.

Scope Exclusion: After-sale MRO, leased spare engines, and APUs are intentionally excluded to prevent double counting.

Segmentation Overview

- By Engine Type

- Turbofan

- Turboprop

- Turboshaft

- Piston

- Hybrid-Electric

- By Aircraft Type

- Commercial Aviation

- Narrowbody Aircraft

- Widebody Aircraft

- Regional Aircraft

- Military Aviation

- Combat Aircraft

- Non-combat Aircraft

- General Aviation

- Business Jets

- Helicopters

- Turboprop Aircraft

- Piston Engine Aircraft

- Unmanned Aerial Vehicles (UAVs)

- Advanced Air Mobility Vehicles (AAM)

- Commercial Aviation

- By Technology

- Conventional Turbofan/Turboprop

- Geared Turbofan (GTF)

- Contra-Rotating Open Rotor

- Adaptive-Cycle Engines

- Hybrid-Electric Propulsion

- By Thrust Class

- Less than 10,000

- 10,001 to 25,000

- 25,001 to 50,000

- Greater than 50,000

- By Component

- Compressor

- Turbine

- Nozzle

- Gearbox

- Other Components (Fan, Combustor,FADEC and Control Electronics, etc.)

- By End-User

- OEM Factory-Fit

- Replacement/Aftermarket

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- France

- Germany

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

We then interviewed aircraft leasing managers, propulsion-system engineers, airline technical-buying heads, and defense acquisition planners across North America, Europe, Asia-Pacific, and the Middle East. These conversations clarified real-world engine lead times, typical pricing brackets, service-life assumptions, and the speed at which hybrid-electric demonstrators may graduate to type certification.

Desk Research

Our analysts first assembled publicly available data from tier-1 authorities such as ICAO traffic statistics, FAA and EASA fleet registers, UN Comtrade HS-8411 trade codes, and Eurostat production indices. We layered these with insights from aviation trade bodies (IATA, AIA) and financial disclosures lodged with the SEC or equivalent regulators. Paid datasets, including Aviation Week orderbook intelligence, Airframer program trackers, and D&B Hoovers company revenues, helped complete delivery pipelines and OEM share splits. The sources cited here are illustrative; many additional publications and databases were consulted during evidence gathering.

Market-Sizing & Forecasting

The base year value emerges from a top-down build using global delivery tallies and fleet retirement schedules, which are then stress-tested with selective bottom-up supplier roll-ups and sampled average selling prices. Key variables, including annual passenger RPK growth, fleet modernization rates, thrust-class mix shifts, SAF blend mandates, and defense procurement outlays, feed a multivariate-regression model; ARIMA smoothing handles short-term shocks. Where bottom-up gaps appear (e.g. classified military volumes), we interpolate using region-specific engine-to-airframe ratios vetted by experts.

Data Validation & Update Cycle

Outputs undergo four-eye analyst review, variance checks against historical margins, and anomaly reconciliation with external indicators before sign-off. We refresh each model annually and trigger interim updates after material events such as major OEM guidance changes or geopolitically driven order spikes.

Why Our Aircraft Engine Baseline Is the Soundest Decision Anchor

Published estimates differ because firms adopt dissimilar scopes, currency bases, and refresh cadences. Some fold in overhaul revenues or legacy spare sales; others convert currencies at spot rather than average rates.

Key gap drivers include inclusion of aftermarket MRO, divergent engine-price curves, and varying assumptions on narrow-body delivery recovery versus wide-body lag. Mordor reports only factory-fresh units and applies a blended ASP ladder that is re-benchmarked each quarter, which curbs overstatement when inflation spikes.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 106.17 bn (2025) | Mordor Intelligence | - |

| USD 63.93 bn (2024) | Global Consultancy A | Excludes military engines and uses delivery counts without price rebasing |

| USD 153.69 bn (2024) | Industry Research B | Adds aftermarket MRO plus APUs and applies list prices |

| USD 75.10 bn (2023) | Research Publisher C | Mixes calendar and fiscal years; partial currency conversion at year-end spot rates |

The comparison shows that figures can swing widely when spare-parts revenue or differing price books creep in. By isolating new-build engines, employing audited delivery data, and updating variables yearly, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can readily trace and replicate.

Key Questions Answered in the Report

How large is the aircraft engine space today and what growth is expected by 2031?

The aircraft engines market reached USD 109.41 billion in 2026 and is projected to rise to USD 129.69 billion by 2031, reflecting a 3.46% CAGR.

Which propulsion technologies are set to expand the fastest over the next five years?

Adaptive-cycle engines lead with a 9.15% CAGR to 2031 in the defense pipeline, followed by hybrid-electric systems at 7.17%.

What is driving the surge in high-thrust engine demand above 50,000 lbf?

Accelerated B777X and A350-1000 orders for long-haul passenger and cargo services, combined with widebody freighter conversions, push this segment toward a 6.78% CAGR.

How do ReFuelEU rules affect upcoming engine certifications?

All new type certificates issued after 2025 must prove full compatibility with 100% sustainable aviation fuel, forcing combustor and fuel-system redesign across every thrust class.

Why are Middle Eastern operators prompting extra maintenance activity?

Ambient temperatures above 50°C in hubs such as Dubai shorten turbine-blade life by roughly 15%, increasing shop-visit frequency and spare-engine pools.

Where can airlines realize the greatest cost savings on overhauls?

Independent MROs now handle more than 40% of CFM56 shop visits, offering overhaul invoices 10-15% lower than OEM networks while expanding capacity in all regions.

Page last updated on: