Aircraft Pumps Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

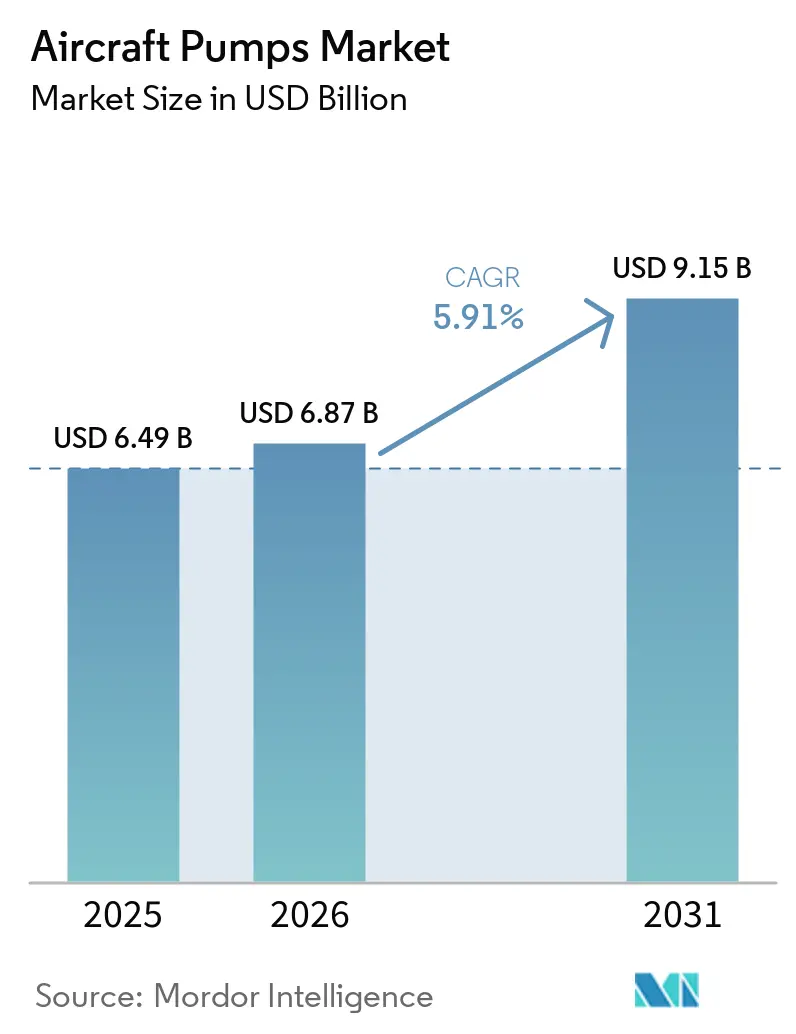

| Market Size (2026) | USD 6.87 Billion |

| Market Size (2031) | USD 9.15 Billion |

| Growth Rate (2026 - 2031) | 5.91% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Pumps Market Analysis by Mordor Intelligence

The aircraft pumps market size is expected to grow from USD 6.49 billion in 2025 to USD 6.87 billion in 2026 and is forecast to reach USD 9.15 billion by 2031 at 5.91% CAGR over 2026-2031. The aircraft pumps market is supported by a steady rise in commercial aircraft production. Airbus delivered 793 aircraft in 2025 and ended the year with an order backlog of 8,754 units, which keeps demand visible across fuel, hydraulic, and lubrication systems for years ahead.[1]Airbus, “Airbus Reports 793 Commercial Aircraft Deliveries in 2025,” Airbus Newsroom, airbus.com The aircraft pumps market is also being shaped by a broader move toward more-electric system layouts, and Liebherr’s work under the FAUST program shows that major suppliers are already building hydraulic power packs that reduce dependence on engine-driven generation. Service opportunities remain important because condition monitoring is improving visibility into pump health, and published work in Sensors and Measurement shows that non-invasive sensing and model-based diagnosis can support more targeted maintenance decisions. The aircraft pumps market also retains strong defense exposure, as fleet upgrades and long service lives continue to support remanufacturing and subsystem replacement, even as new platform deliveries fluctuate. At the same time, high certification burdens and the gradual spread of electromechanical actuation keep the competitive field narrow, which favors suppliers with platform approvals, installed base relationships, and the engineering depth to support new pump architectures.

Key Report Takeaways

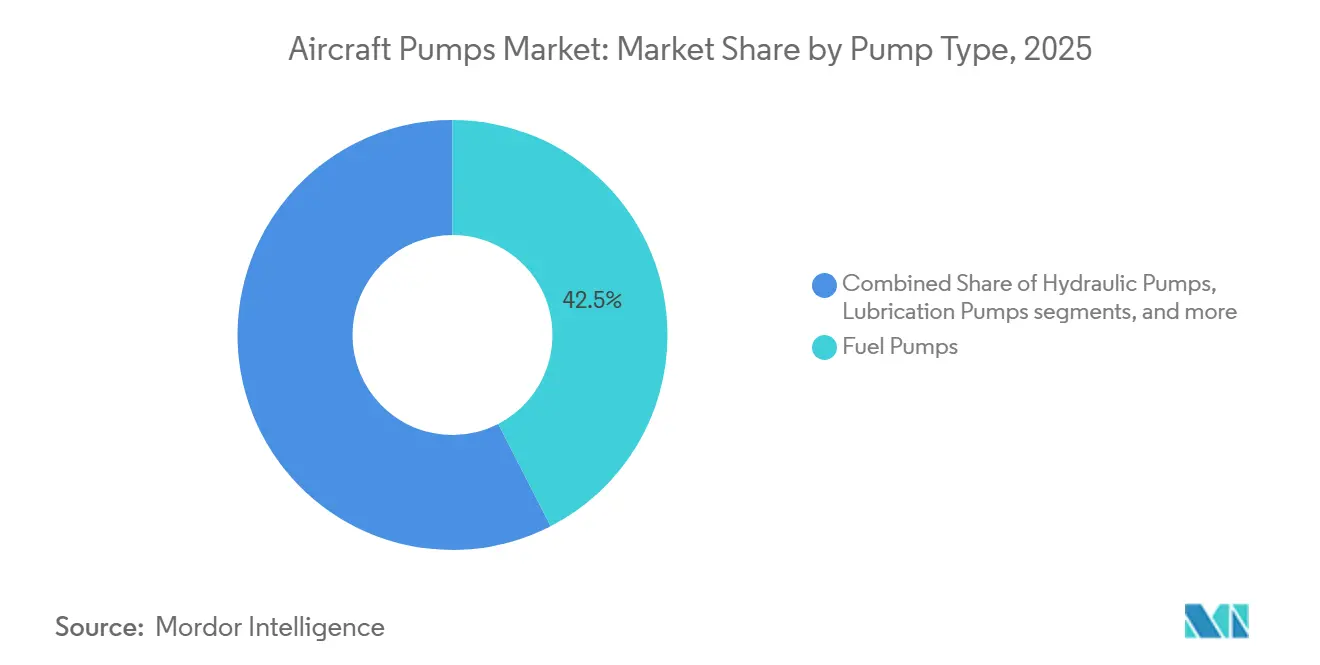

- By pump type, fuel pumps accounted for 42.45% of revenue in 2025, while hydraulic pumps are forecast to register the highest CAGR of 7.75% through 2031.

- By drive mechanism, engine-driven units accounted for 45.35% of revenue in 2025, while electric motor-driven pumps are forecast to expand at an 8.37% CAGR through 2031.

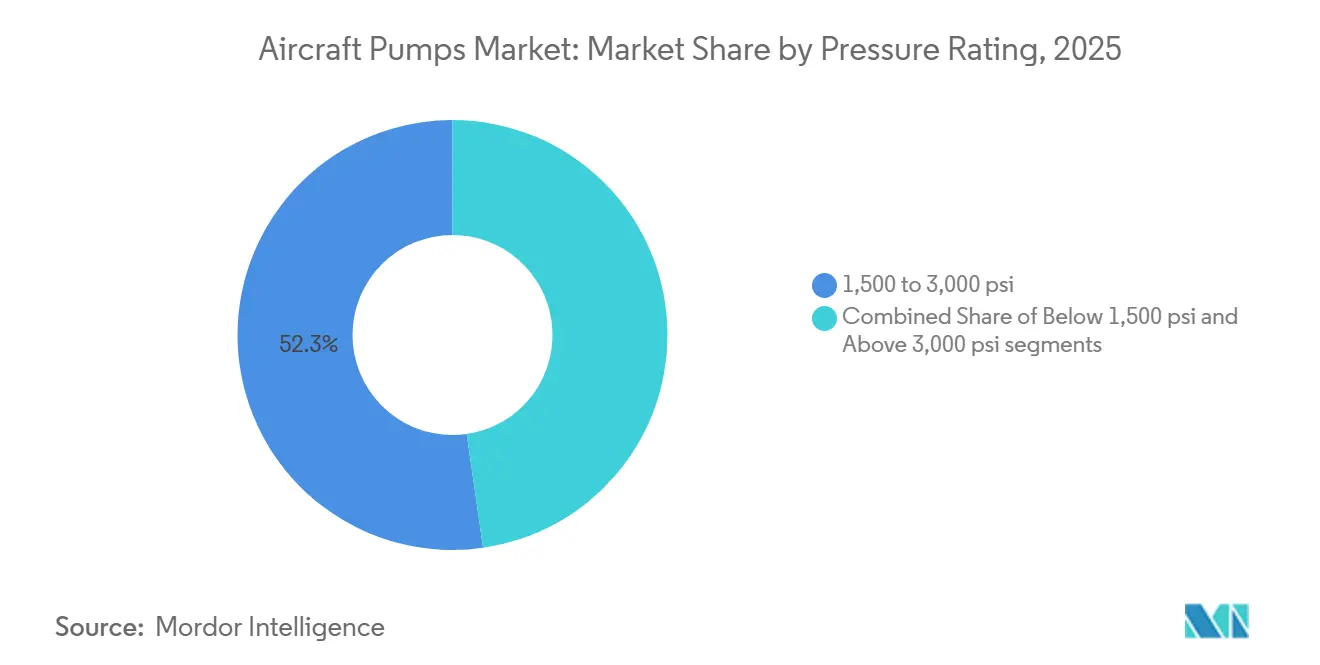

- By pressure rating, the 1,500 to 3,000 psi class represented 52.27% of revenue in 2025, while the above 3,000 psi segment is projected to grow at a 6.61% CAGR through 2031.

- By aircraft type, commercial aviation captured 64.52% of revenue in 2025, while UAVs are projected to post the fastest CAGR at 9.56% through 2031.

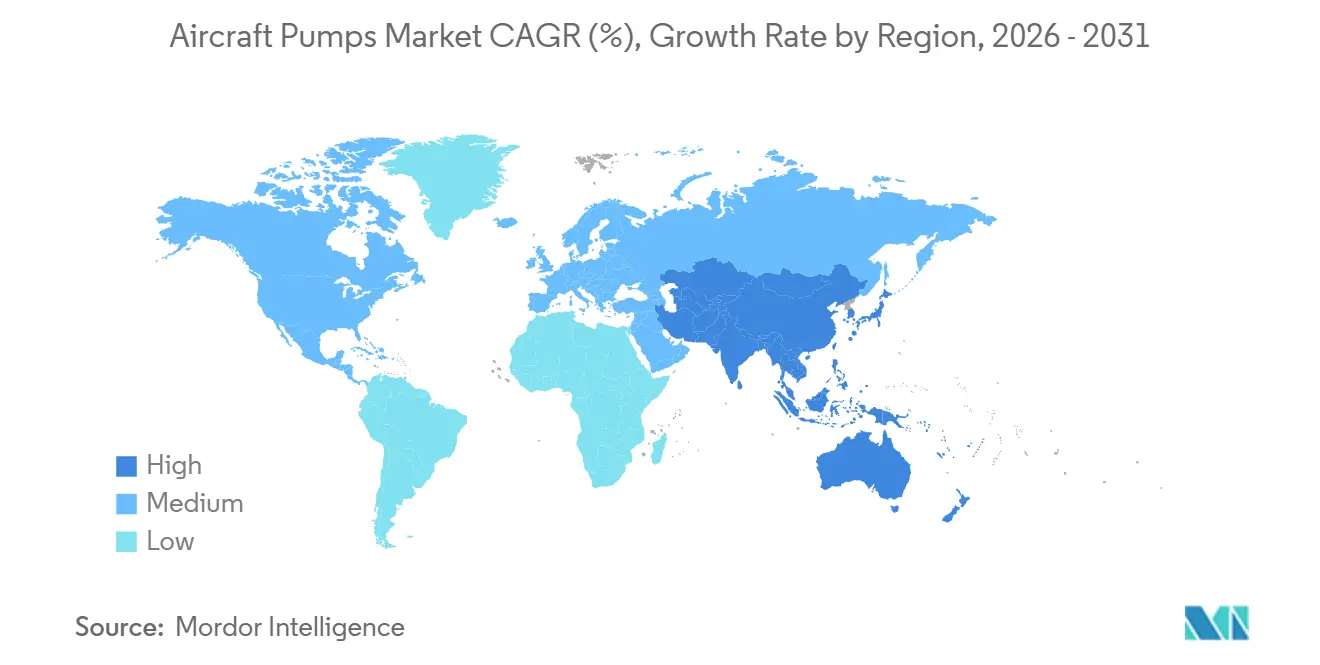

- By geography, North America held 44.68% of the aircraft pumps market in 2025, while Asia-Pacific is forecast to grow at a 6.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Aircraft Pumps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrification of aircraft systems | +1.2% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Surge in commercial aircraft deliveries | +1.5% | Global, concentrated in North America, Europe, and Asia-Pacific | Short term (≤ 2 years) |

| Military fleet modernization | +0.9% | North America, Europe, and Asia-Pacific core | Medium term (2-4 years) |

| Lightweight composite pump designs | +0.7% | Global, early gains in North America and Europe | Long term (≥ 4 years) |

| Predictive maintenance deployment | +0.6% | Global, with early gains in Europe and North America | Medium term (2-4 years) |

| Hydrogen-ready fuel systems | +0.5% | Global, with early gains in Europe and Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Electrification of Aircraft Systems

The aircraft pumps market is being reshaped by a steady shift toward more-electric aircraft layouts, as suppliers now need to support functions that were once closely tied to engine-driven architectures. In this part of the aircraft pumps market, electric motor-driven pumps are gaining ground in auxiliary power, cooling, and secondary hydraulic applications where better control and subsystem independence matter more than the added hardware cost. Liebherr’s work under the FAUST research program is important because it directly targets decoupled hydraulic power generation, demonstrating how the design logic is changing for future short- and medium-haul platforms.[2]Liebherr, “Aviation Research Projects (LuFo VII-1) With Participation of Liebherr-Aerospace Lindenberg GmbH,” Liebherr, liebherr.com The aircraft pumps market also benefits from the fact that electric-drive assemblies can deliver greater value per unit when they combine pumping, control, and local power management into a single package. As this design path matures, the aircraft pumps market is likely to see a mix shift toward higher-value assemblies rather than a simple one-for-one replacement of conventional products.

Surge in Commercial Aircraft Deliveries

The aircraft pumps market continues to draw near-term volume support from commercial fleet expansion, because every new aircraft delivery creates immediate linefit demand and also seeds future maintenance demand. Airbus delivered 793 aircraft to 91 customers in 2025, a 4% increase from the prior year, and its year-end backlog of 8,754 aircraft provides the aircraft pumps market with a visible production base across narrowbody and widebody programs. That backlog matters because fuel, hydraulic, lubrication, and cooling pumps are tied to the aircraft build cycle, yet their revenue stream extends far beyond first installation. The aircraft pumps market also benefits from the operating profile of narrowbody fleets, as repeated short-haul cycles create heavy wear on fluid-handling systems and increase overhaul demand as these aircraft accumulate service hours. This production and usage pattern strengthens both OEM and aftermarket activity, making commercial aviation the clearest volume anchor in the current forecast period. As long as large OEM backlogs continue to convert into deliveries, the aircraft pumps market should retain steady demand visibility, even with some supply chain friction remaining.

Military Fleet Modernization

The aircraft pumps market is also supported by military fleet modernization, because defense operators continue to fund both new platform content and life-extension work on aging fleets. This part of the aircraft pumps market often has longer qualification cycles. Still, it also provides durable revenue because military aircraft remain in service for decades and require repeated subsystem maintenance. Eaton’s selection by Bell Textron for hydraulic power generation and conveyance solutions for the US Army’s Future Long Range Assault Aircraft demonstrates that advanced military programs still rely on specialized hydraulic systems, including components manufactured using additive manufacturing methods to reduce weight and improve internal flow paths.[3]Eaton, “Bell Selects Eaton Hydraulic Technology to Power the U.S. Army’s Future Long Range Assault Aircraft,” Eaton News Release, eaton.com The aircraft pumps market also benefits from the fact that defense customers often prioritize mission readiness over the lowest upfront cost, which supports remanufacturing, replacement inventory, and long-term support agreements. Military demand is not shaped only by aircraft deliveries, because platform upgrades and subsystem changes on in-service fleets can keep pump demand active even when procurement timing shifts, making defense work strategically valuable in the aircraft pumps market, especially for suppliers that already hold approvals and service relationships on major fleets.

Predictive Maintenance Deployment

The aircraft pumps market is beginning to see a change in service economics as pump monitoring becomes more precise and less intrusive. In the aftermarket side of the aircraft pumps market, this matters because operators want fewer unscheduled removals, better overhaul timing, and more useful health data without opening the unit too early. A 2025 study in sensors demonstrated that fiber Bragg grating optical sensors mounted externally on a Rolls-Royce fuel pump could measure strain and vibration up to 2.5 kHz without disassembly, supporting real-time condition monitoring of aircraft pump structures.[4]Edmond Chehura and Stephen W. James et al., “Measurement of Strain and Vibration, at Ambient Conditions, on a Dynamically Pressurised Aircraft Fuel Pump Using Optical Fibre Sensors,” Sensors, mdpi.com A 2026 study in measurement proposed a vibration-sensor-free diagnostic method for aviation piston pumps using the continuous wavelet transform and a vision transformer approach, pointing to another way the aircraft pumps market could reduce the need for additional sensor mass while still improving fault detection. These developments support service models that rely less on fixed overhaul intervals and more on observed conditions, thereby improving asset utilization for airlines and maintenance providers. Over time, the aircraft pumps market may therefore capture more value from analytics-enabled service packages rather than from replacement hardware alone.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electromechanical actuation replacing hydraulics | -0.9% | Global, with early substitution in Europe and North America | Long term (≥ 4 years) |

| High certification and compliance costs | -0.7% | Global, with acute impact in North America and Europe | Medium term (2-4 years) |

| Aerospace-grade supply chain bottlenecks | -0.5% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Raw material price volatility | -0.4% | Global, with concentrated exposure in North America and Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Certification and Compliance Costs

The aircraft pumps market remains difficult for new entrants because certification and ongoing compliance require long test cycles, detailed documentation, and platform-specific quality discipline. This constraint matters across the aircraft pumps market because component suppliers must show repeatable performance under strict airworthiness rules before they can win approved content on commercial or military aircraft. The FAA’s 2025 airworthiness directive for GE Aviation Czech turboprop engines illustrates how regulatory action can trigger inspection, reporting, and maintenance requirements that operators and suppliers must absorb outside normal program planning. Once a supplier has approvals in place, those costs become a barrier that protects incumbents, but the same burden slows new participation and keeps the aircraft pumps market concentrated. The issue is not only the first approval; every configuration change, material change, or process change can create additional work and qualification steps. As a result, the aircraft pumps market often rewards companies with deep regulatory experience and broad installed portfolios rather than firms that compete only on price.

Electromechanical Actuation Replacing Hydraulics

The aircraft pumps market faces a long-term challenge from electromechanical actuation, as some aircraft functions may gradually shift away from centralized hydraulic systems. The risk is uneven across the aircraft pumps market, as replacement pressure is stronger on smaller or newer platforms than on large commercial aircraft with entrenched hydraulic layouts. Liebherr’s more-electric aircraft roadmap still shows a strong role for electro-hydraulic power generation and distributed hydraulic solutions, suggesting that the shift is more likely to reconfigure pump demand than to remove it outright in the medium term. The aircraft pumps market is therefore more exposed in specific applications where electrical actuation can simplify the architecture without creating major thermal or reliability trade-offs. Through 2031, the substitution threat appears real but selective, and the core installed base in the aircraft pumps market is still expected to rely heavily on hydraulic and fuel pumping functions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pump Type: Hydraulic Demand Strengthens Alongside Fuel System Dominance

Fuel pumps accounted for 42.45% of revenue in 2025, giving them the largest position in the segment mix and 42.45% of the global aircraft pumps market share. This position reflects their essential role across propulsion and fuel management functions, and it is reinforced by high-volume narrowbody programs that keep replacement demand active. Airbus delivered 607 aircraft from the A320 family in 2025, which shows why short-cycle commercial operations continue to sustain recurring fuel pump demand across the installed fleet. Research in sensors also showed that aircraft fuel pumps face increasing monitoring needs as pressure and temperature loads increase, supporting the view that this category remains central to both OEM and aftermarket activity in the aircraft pumps market. In practical terms, the aircraft pumps market keeps fuel pumps at the center of fleet reliability because propulsion-related components cannot tolerate extended downtime.

Hydraulic pumps are the fastest-growing segment, with a 7.75% CAGR through 2031, and this part of the aircraft pumps market is expanding as higher-pressure flight control systems and defense upgrades drive demand. The aircraft pumps industry also benefits from the fact that hydraulic content remains deeply embedded in landing gear, braking, actuation, and utility systems across large commercial and military platforms. Eaton’s FLRAA award supports this view because the program includes hydraulic power generation and conveyance content for a next-generation rotorcraft platform. Lubrication pumps continue to track engine output and maintenance demand, while coolant pumps are gaining relevance as thermal management needs rise in more-electric architectures. Other pump categories remain smaller, but they still matter in the aircraft pumps market because cabin, utility, and specialized subsystem functions require qualified components even at lower volume.

By Drive Mechanism: Electric Drive Momentum Builds Against An Entrenched Installed Base

Engine-driven systems accounted for 45.35% of revenue in 2025, making them the leading configuration in the aircraft pumps market, as the installed fleet still relies heavily on centralized hydraulic generation. Their position remains strong because aircraft layouts, maintenance routines, and certification histories have been built around them for decades, which raises switching costs across the aircraft pumps market. Air-driven pumps still support auxiliary and emergency duties on selected platforms, while RAT-driven units remain critical as last-resort hydraulic sources on transport aircraft. Manual pumps are a small category, but they continue to serve general aviation and maintenance use cases where simplicity still matters.

Electric motor-driven pumps are forecast to grow at a 8.37% CAGR through 2031, and this segment represents one of the clearest areas of expansion for the aircraft pumps market within new system architectures. The aircraft pumps market is moving in this direction because distributed power and local control align well with more-electric aircraft goals, especially in subsystems where decoupling from the engine improves flexibility. Liebherr’s FAUST work on high-efficiency power packs directly supports this shift and shows that suppliers are already preparing for aircraft that depend less on engine-linked hydraulic generation. Research in actuators provides technical support by showing how electro-hydrostatic concepts can improve power density and thermal performance, which helps explain why electric-drive pump assemblies are gaining attention in the aircraft pumps market. Even so, the pace of change will vary by platform, and the aircraft pumps market is likely to carry both engine-driven and electric-drive systems in parallel for much of the forecast period.

By Pressure Rating: High-Pressure Platforms Create A Clear Growth Layer

The 1,500 to 3,000 psi class accounted for 52.27% of revenue in 2025, making it the dominant pressure band and the largest share of the aircraft pumps market in installed commercial and military hydraulic systems. This concentration reflects the long service life of aircraft built around conventional hydraulic architectures, where this pressure range remains the standard operating envelope for many critical functions. The aircraft pumps market continues to rely on this class because fleet replacement is gradual, and a large share of in-service aircraft still uses established layouts rather than newly optimized high-pressure systems. The range below 1,500 psi remains relevant for lighter platforms and lower-power applications, where simplicity, lower cost, and easier integration outweigh the performance benefits of higher pressure.

Systems above 3,000 psi are forecast to grow at a 6.61% CAGR through 2031, making this one of the clearest performance-driven pockets in the aircraft pumps market. Higher-pressure designs allow aircraft to extract more force from smaller and lighter packages, which is valuable in military aircraft and advanced transports where weight and space remain tightly constrained. Liebherr’s FAUST program specifically includes miniaturized electro-hydraulic power packs for compact installation zones, which aligns with the demand trend toward more capable high-pressure assemblies. The aircraft pumps industry also sees this shift as a way to protect value even when unit volumes grow more slowly, because higher-pressure systems typically require tighter engineering and qualification control. As a result, the aircraft pumps market is likely to preserve large installed volumes in the mid-pressure range while gradually building a premium growth layer in higher-pressure applications.

By Aircraft Type: UAV Growth Adds A New Demand Curve To A Commercially Led Base

Commercial aviation accounted for 64.52% of revenue in 2025, indicating this segment held the largest share of the aircraft pumps market and remains the core demand base. The aircraft pumps market depends on this category because narrowbody production volume, high daily utilization, and long fleet lives combine to create steady OEM and replacement demand. Airbus’s 2025 delivery mix supports that pattern, since the A320 family alone contributed 607 aircraft and kept linefit demand concentrated in high-cycle commercial platforms. Widebody aircraft add value through higher per-aircraft system content, while military aircraft create a separate layer of demand for rugged, high-performance, and often higher-pressure pump configurations. General aviation remains smaller, yet it still supports the aircraft pumps market through business aviation and utility aircraft that require compact and reliable fluid systems.

UAVs are forecast to grow at a 9.56% CAGR through 2031, which makes them the fastest-rising aircraft class in the aircraft pumps market. This growth reflects expanding use in defense, surveillance, and specialized logistics missions, where endurance and system reliability matter more than low-cost consumer drone design. The Lee Company’s 200 Series radial piston pump for microturbine UAV and tactical missile engines demonstrates that this niche already demands high flow capability, greater than 95% volumetric efficiency, and operation across a wide temperature range from -67°F to 185°F. That performance envelope shows why the aircraft pumps market treats UAVs as a technically distinct segment rather than a small extension of general aviation. Over time, this category may not match commercial aviation in absolute terms. Still, it provides the aircraft pumps market with a useful new growth path with different sizes, weights, and duty-cycle requirements.

Geography Analysis

North America accounted for 44.68% of revenue in 2025, making it the largest region in the aircraft pumps market and the broadest installed base across OEM, defense, and MRO activities. The aircraft pumps market remains strong in North America because the region combines major aircraft programs, deep supplier networks, and established certification capabilities within a single ecosystem. Defense demand adds another layer of stability, and Eaton’s FLRAA role shows that advanced US programs continue to create demand for hydraulic power generation and conveyance systems. The region also benefits from a large aftermarket base, since airlines, military operators, and maintenance providers all depend on approved pump support over long service cycles. That combination keeps North America central to the aircraft pumps market even when production rates or defense timing vary by program.

Europe held the second-largest regional position in 2025, and the aircraft pumps market there is supported by Airbus production activity and a strong base of subsystem suppliers. Airbus’s 2025 delivery performance reinforces Europe’s role in commercial aircraft output, while the company’s large backlog keeps future linefit demand visible for pump suppliers tied to its platform base. Europe is also important to the aircraft pumps market because suppliers are actively preparing for next-generation architectures, and Liebherr’s participation in the FAUST and TiReGo programs shows focused work on decoupled hydraulic power packs and improved material cycles. These efforts matter because they support both near-term production needs and the longer-term redesign of aircraft subsystems toward more-electric, more-material-efficient layouts.

Asia-Pacific is forecast to grow at a 6.23% CAGR through 2031, making it the fastest-growing regional segment and a rising contributor to the aircraft pumps market size. The aircraft pumps market in Asia-Pacific is being lifted by growing commercial fleets, local platform ambitions, and defense procurement across several countries. Japan adds strategic weight because it combines civil and defense demand with interest in hydrogen-related aircraft development, while the wider region benefits from a growing maintenance base as fleet counts rise. South America remains smaller, but its regional contribution is supported by aircraft production and service activity tied to established aerospace programs. The Middle East and Africa also add demand through active military fleets and expanded air transport. However, project timing in this part of the aircraft pumps market is more exposed to budget cycles than in North America or Europe.

Competitive Landscape

The aircraft pumps market is moderately consolidated at the prime supplier level, and Parker-Hannifin Corporation, Eaton Corporation plc, Safran SA, Collins Aerospace (RTX Corporation), and Woodward, Inc. remain the names most closely associated with certified platform content across major aircraft categories. The aircraft pumps market tends to favor these established players because certification, platform integration, quality systems, and long service commitments create high entry barriers that extend well beyond basic component manufacturing. Once a supplier gains approved content, it often remains embedded through replacement, repair, and overhaul work for many years, making installed base access one of the strongest competitive advantages in the aircraft pumps market. That structure limits direct disruption and keeps competition focused on technology shifts, subsystem redesign, and adjacent niches rather than easy replacement of incumbent suppliers.

Leading companies are responding by investing where future aircraft architecture is changing fastest, and that gives the aircraft pumps market a clear innovation track alongside its conventional installed base. Eaton’s role in FLRAA is one example, as it ties hydraulic power generation to a next-generation military aircraft while using additive manufacturing methods that improve design flexibility and reduce weight. Liebherr provides a second example, as its FAUST and TiReGo participation demonstrates strategic work on decoupled electro-hydraulic power packs and improved material use in aerospace components. Airbus adds a third example through its continued work on hydrogen aircraft, which keeps the future fuel system architecture under active evaluation and could eventually reshape specialized pump requirements for new aircraft types.

The next competitive shift in the aircraft pumps market is likely to come from how suppliers position themselves between conventional hydraulic demand and new distributed architectures. Research on actuators suggests that electro-hydrostatic systems can deliver better thermal performance and useful power density, which supports suppliers in designing local hydraulic power for electric drive concepts. Work in sensors and measurement also supports a service-led layer of competition, because better monitoring and diagnosis can help companies differentiate through uptime, analytics, and maintenance planning rather than through hardware alone. The aircraft pumps market, therefore, remains protected by high barriers to entry. Still, it is not static, as value is shifting toward integrated power packs, smarter maintenance, and more specialized pump formats. Suppliers that already hold approvals and engineering depth are in the best position to capture that shift, which is why the aircraft pumps market is likely to stay moderately concentrated through the forecast period.

Aircraft Pumps Industry Leaders

Parker-Hannifin Corporation

Eaton Corporation plc

Safran SA

Collins Aerospace (RTX Corporation)

Woodward, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Liebherr-Aerospace Lindenberg GmbH joined the FAUST and TiReGo research consortia under Germany's LuFo VII-1 program. FAUST targets fully decoupled, electro-hydraulic high-efficiency power packs for next-generation short- and medium-haul aircraft, including miniaturized versions for swept-wing installation spaces. TiReGo targets a closed material-recycling cycle for titanium, a critical pump-casing material, reducing CO₂ emissions without compromising mechanical properties.

- June 2024: SIA Engineering Company Limited and Eaton formed a joint venture, Eaton Aerospace Component Services Asia Sdn Bhd, in Malaysia to deliver MRO services for Eaton-manufactured aircraft fuel and hydraulic system components.

Global Aircraft Pumps Market Report Scope

The aircraft pumps market is witnessing consistent growth driven by increased aircraft production, fleet modernization initiatives, and rising demand for advanced fuel, hydraulic, lubrication, and cooling systems in both commercial and military aviation. The adoption of more-electric aircraft technologies, lightweight pump systems, and high-pressure hydraulic solutions is also contributing to market expansion.

The aircraft pumps market is segmented by pump type, drive mechanism, pressure rating, aircraft type, and geography. By pump type, the market is segmented into fuel pumps, hydraulic pumps, lubrication pumps, coolant pumps, and other specialized pumps. By drive mechanism, it is categorized into engine-driven, electric motor-driven, air-driven, ram-air-turbine (RAT) driven, and manual pumps. By pressure rating, the market is segmented into below 1,500 psi, 1,500 to 3,000 psi, and above 3,000 psi. By aircraft type, the market is segmented into commercial aviation, military aviation, general aviation, and unmanned aerial vehicles (UAVs). The report also covers the market sizes and forecasts for the aircraft pumps market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Fuel Pumps |

| Hydraulic Pumps |

| Lubrication Pumps |

| Coolant Pumps |

| Other Specialized Pumps |

| Engine-Driven |

| Electric Motor-Driven |

| Air-Driven |

| Ram-Air-Turbine (RAT) Driven |

| Manual/Hand Pumps |

| Below 1,500 psi |

| 1,500 to 3,000 psi |

| Above 3,000 psi |

| Commercial Aviation | Narrowbody |

| Widebody | |

| Regional Jets | |

| Military Aviation | Fighter Jets |

| Transport Aircraft | |

| Rotorcraft | |

| General Aviation | |

| Unmanned Aerial Vehicles (UAVs) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Pump Type | Fuel Pumps | ||

| Hydraulic Pumps | |||

| Lubrication Pumps | |||

| Coolant Pumps | |||

| Other Specialized Pumps | |||

| By Drive Mechanism | Engine-Driven | ||

| Electric Motor-Driven | |||

| Air-Driven | |||

| Ram-Air-Turbine (RAT) Driven | |||

| Manual/Hand Pumps | |||

| By Pressure Rating | Below 1,500 psi | ||

| 1,500 to 3,000 psi | |||

| Above 3,000 psi | |||

| By Aircraft Type | Commercial Aviation | Narrowbody | |

| Widebody | |||

| Regional Jets | |||

| Military Aviation | Fighter Jets | ||

| Transport Aircraft | |||

| Rotorcraft | |||

| General Aviation | |||

| Unmanned Aerial Vehicles (UAVs) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2031 outlook for aircraft pumps?

The aircraft pumps market is forecast to reach USD 9.15 billion by 2031 from USD 6.87 billion in 2026, with a 5.91% CAGR over 2026-2031.

Which pump type leads demand in aircraft applications?

Fuel pumps held the largest share at 42.45% in 2025 because they are essential across propulsion and fuel management systems on all major aircraft types.

Which aircraft category is growing fastest for pump demand?

UAVs are expected to post the fastest growth at a 9.56% CAGR through 2031, supported by defense, surveillance, and specialized logistics use.

Why are electric motor-driven pumps gaining traction in aircraft systems?

Electric motor-driven pumps are growing at an 8.37% CAGR because more-electric aircraft layouts need more localized and decoupled power generation.

Which region remains the largest for aircraft pump revenue?

North America led with 44.68% of revenue in 2025 due to its concentration of OEM production, defense programs, and aftermarket support activity.

What is the main long-term risk for hydraulic pump demand?

The main long-term risk is selective replacement by electromechanical actuation in some applications, although large commercial aircraft still rely heavily on hydraulic systems through 2031.

Page last updated on: