Aircraft Actuators Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

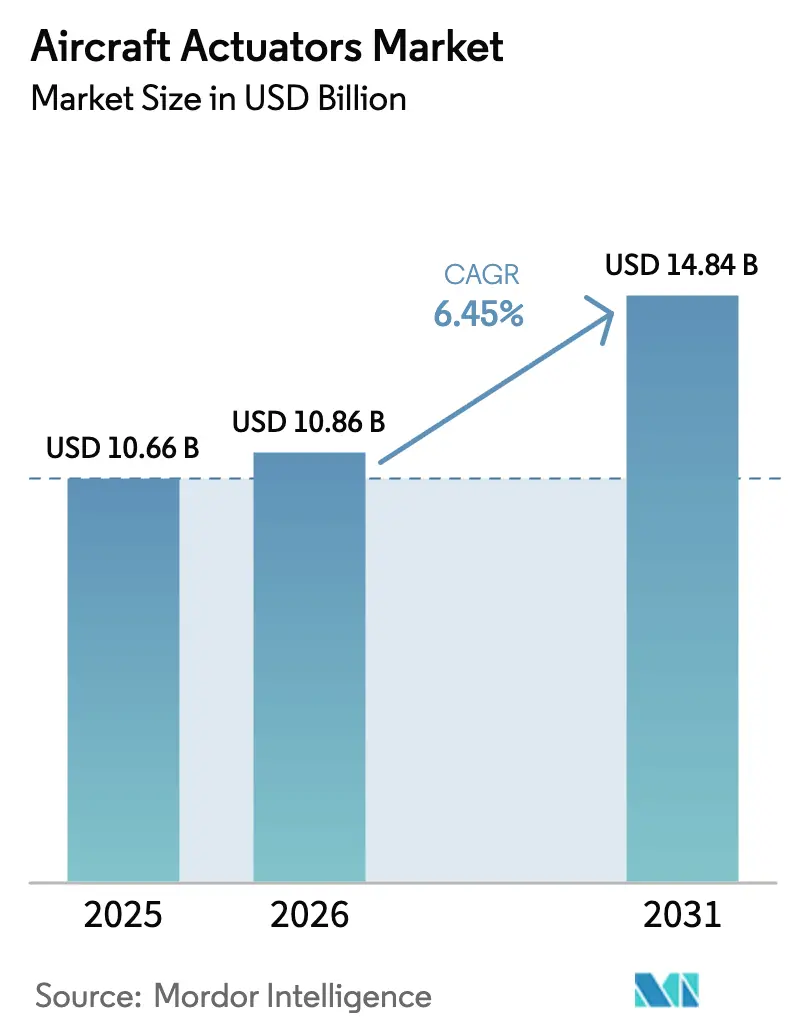

| Market Size (2026) | USD 10.86 Billion |

| Market Size (2031) | USD 14.84 Billion |

| Growth Rate (2026 - 2031) | 6.45% CAGR |

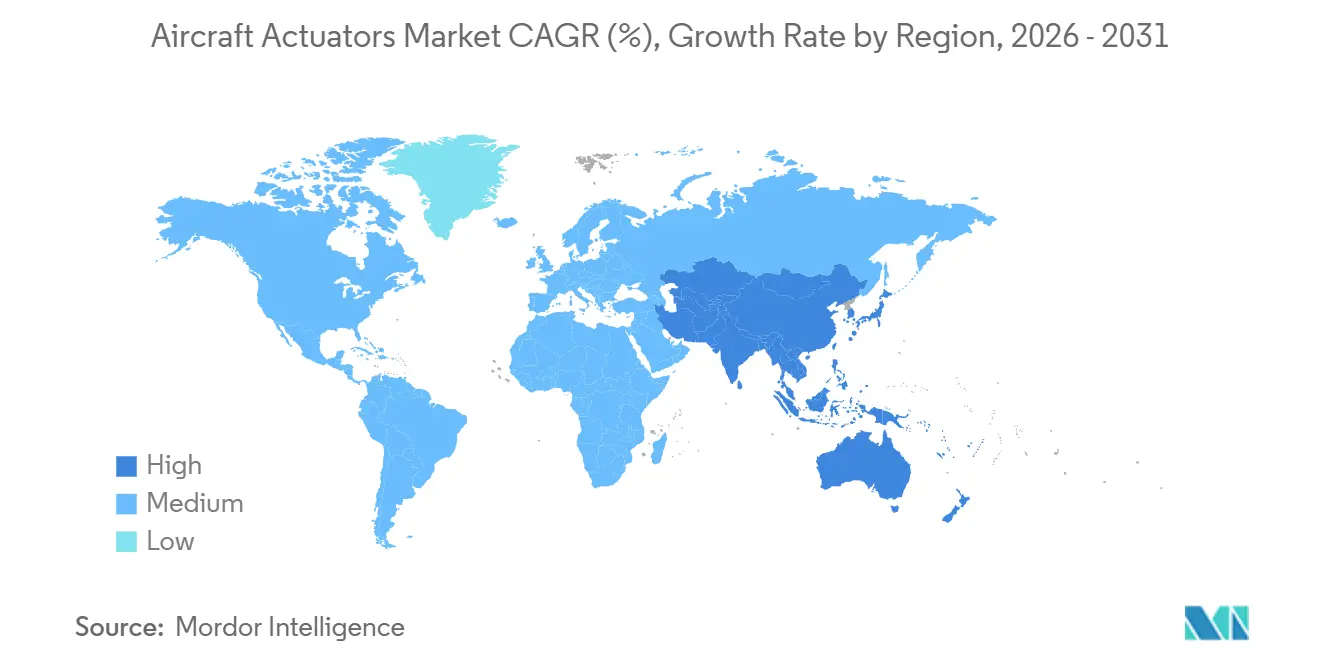

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Actuators Market Analysis by Mordor Intelligence

The aircraft actuators market size is expected to grow from USD 10.66 billion in 2025 to USD 10.86 billion in 2026 and is forecasted to reach USD 14.84 billion by 2031 at a 6.45% CAGR over 2026-2031. Persistent narrowbody backlogs at Airbus and Boeing, the march toward more-electric architectures, and the shift toward predictive-maintenance-ready components are the primary drivers of this expansion. Electromechanical technologies are gaining market share because they eliminate hydraulic leakage, reduce empty weight, and stream health data to operators. Thermal-management hurdles still restrict their role in high-speed primary controls. Airlines remain cautious about complete retrofits, but regulatory moves, such as FAA Advisory Circular 25-19A, have created a compliance path for smart actuators. Meanwhile, sustainability programs around SAF and hydrogen are spawning new design cycles that further expand actuator content per aircraft. On the competitive front, the aircraft actuators market is moderately concentrated, as the top five suppliers leverage digital twin platforms and vertical integration, while niche specialists court eVTOL and UAV programs with ultra-light, electro-hydrostatic designs.

Key Report Takeaways

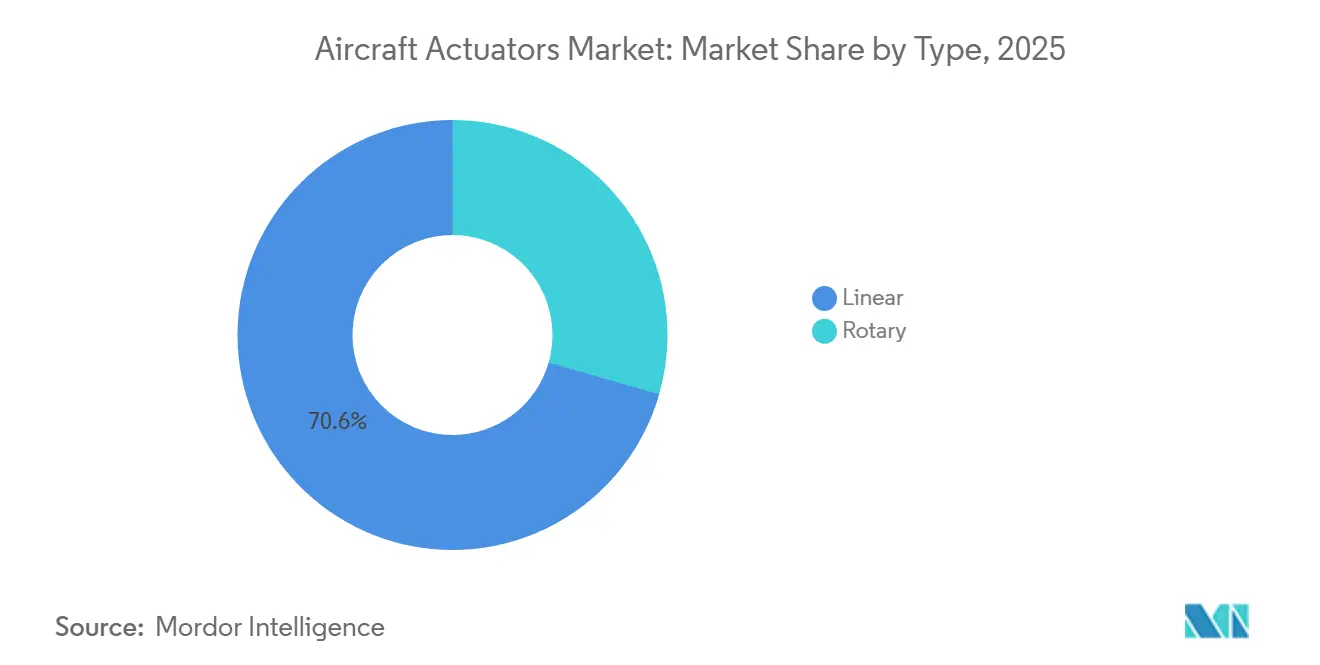

- By type, linear actuators held 70.55% of the aircraft actuators market share in 2025, whereas rotary units are projected to post the fastest 6.90% CAGR through 2031.

- By system, hydraulic actuators retained 44.90% of the revenue in 2025; electrical and electromechanical units are on track for the highest 7.10% CAGR through 2031.

- By application, flight-control surfaces accounted for 47.20% of 2025 revenue, while cabin and seat systems are forecasted to expand at a 7.85% CAGR.

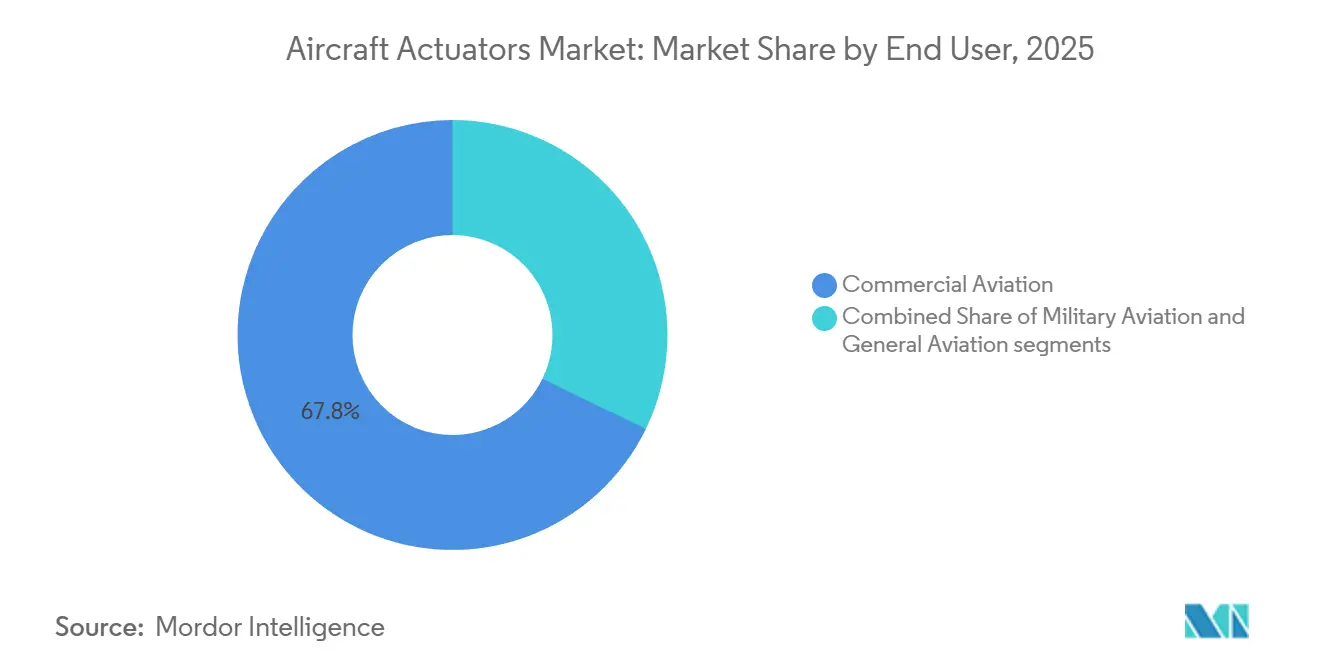

- By end user, commercial aviation led with 67.80% revenue in 2025; military aviation is expected to grow at the fastest rate, with an 8.10% CAGR through 2031.

- By fit, the aftermarket captured 56.90% of the 2025 value, whereas OEM installations are expected to rise at a 6.85% CAGR as production rates recover.

- By geography, North America generated 36.85% of 2025 sales, but Asia-Pacific will deliver the strongest 7.25% CAGR until 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Aircraft Actuators Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in narrowbody production backlog | +1.2% | Global, North America and Europe | Medium term (2–4 years) |

| Increased electrification of secondary flight systems | +0.9% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Rising retrofit demand for health-monitoring smart actuators | +0.7% | Global, early adoption in North America and Europe | Short term (≤ 2 years) |

| More-electric and hybrid-electric aircraft programs | +0.8% | Global, North America & Europe | Long term (≥ 4 years) |

| Light-weight electro-hydrostatic actuator (EHA) adoption in UAVs and eVTOLs | +0.5% | Global, APAC and North America | Medium term (2–4 years) |

| Government support for SAF and hydrogen driving redesign of actuation loads | +0.4% | Global, Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Narrowbody Production Backlog

Airbus and Boeing ended 2024 with a combined backlog exceeding 14,000 single-aisle jets. Each narrowbody requires 80–120 actuators for flight controls, landing gear, thrust reversers, and cabin systems, translating into more than 1 million linefit units through 2031.[1]Source: “Aircraft,” Airbus, airbus.com Production bottlenecks at fuselage and wing suppliers have stretched delivery schedules, forcing operators to keep aging fleets in service longer and elevating aftermarket pulls for health-monitoring linear actuators that can warn of failure 500 flight hours in advance. Asia-Pacific and Middle East low-cost carriers (LCCs), such as IndiGo and Flynas, have collectively ordered nearly 1,000 A320neo family aircraft in 2024 and are contributing to global volume while concentrating new-build deliveries at airports where MRO capacity remains limited. These dynamics elevate the value proposition of predictive maintenance-ready electromechanical systems that can transmit real-time health data over existing ACARS links. Regulatory momentum reinforces the shift; FAA Advisory Circular 25-19A now requires extended-range jets to incorporate actuator health monitoring, nudging both linefit and retrofit buyers toward sensor-rich electromechanical options.[2]Source: “Regulations & Policies,” Federal Aviation Administration, faa.gov

Increased Electrification of Secondary Flight Systems

Airlines are rapidly replacing hydraulic cylinders with electromechanical actuators (EMAs) on spoilers, cabin doors, flap panels, and environmental-control valves because EMAs eliminate leakage risk, weigh less, and reduce scheduled maintenance labor by nearly one-third. Airbus proved the concept when the A321XLR entered Iberia service in 2025, featuring electromechanical units on every cabin door, which reduced empty operating weight by 6% and enhanced cargo payload flexibility on transatlantic routes. NASA’s Electrified Powertrain Flight Demonstration program added technical validation, recording 95% efficiency for electromechanical flight-control units compared with 65% for hydraulics during 2025 sorties over California’s Mojave Desert. Rotary thrust-reverser EMAs from Parker now deploy in less than two seconds, a safety gain that airlines value for rejected-take-off scenarios. Certification cost has been the principal brake on wider adoption. EASA’s 2025 rule revision permits EMAs on primary controls when dual thermal sensors and fully segregated power feeds are present, narrowing the regulatory gap with hydraulics and clearing a smoother runway for the next tranche of electrical upgrades.

Rising Retrofit Demand for Health-Monitoring Smart Actuators

Unscheduled AOG events still cost widebody operators around USD 150,000 per aircraft per day; therefore, carriers are turning to sensor-equipped actuators that stream vibration, temperature, and current-draw data to airline maintenance centers in near real-time. Honeywell’s Forge analytics platform, now resident on more than 2,400 aircraft, merges those telemetry feeds with digital-twin models to predict remaining useful life within a 95% confidence band, trimming spare-parts inventory by 22% and lifting parts-availability assurance to 95%. Lessors and insurers are reinforcing adoption by increasingly rewarding predictive maintenance compliance with lower redelivery penalties, while underwriters offer premium discounts of 3-5% to fleets operating continuous-monitoring regimes. The economics stack up because airlines can convert a lumpy USD 300,000 hardware retrofit into a pay-as-you-fly subscription that aligns expense with flight hours and keeps capital budgets intact. Suppliers also win: recurring software fees smooth quarterly revenue and lift gross margin by eight percentage points compared with traditional spare-parts models.

More-Electric and Hybrid-Electric Aircraft Programs

The A321XLR and all-electric Eviation Alice illustrate complementary pathways toward higher onboard electrification. Airbus fitted its stretched A321 with electromechanical spoilers, cabin-door units, and horizontal-stabilizer trim, removing 180 kg of hydraulic plumbing and unlocking a 4,700-nautical-mile range that bridges mid-continent hubs with secondary European airports. Alice goes further, eliminating hydraulics by pairing Parker EMAs on primary controls with Curtiss-Wright rotary units on the landing gear. While certification was delayed to 2028 after high-altitude thermal tests overheated motor windings, the effort has led to the development of dual-fan cooling solutions and next-generation wire insulation, which are now being evaluated for Boeing's ecoDemonstrator projects. Each new program raises the actuator count, as Alice uses more than 200 per airframe, and demands higher power density, thereby tightening the link between electrical architecture advances and actuator innovation. As sustainable aviation fuel (SAF) and hydrogen propulsion gain traction, these more-electric baselines will become the platform of record rather than niche demonstrators.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent reliability concerns vs. hydraulics in primary flight controls | −0.8% | Global, North America and Europe | Medium term (2–4 years) |

| Thermal management limits for high-power EMAs on supersonic platforms | −0.4% | Global, North America | Long term (≥ 4 years) |

| Rare-earth magnet supply-chain concentration | −0.6% | Global, APAC and Europe | Short term (≤ 2 years) |

| AOG-driven cost pressure in long-life retrofit programs | −0.3% | Global, North America and Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Persistent Reliability Concerns versus Hydraulics in Primary Flight Controls

Hydraulics still dominate elevators, ailerons, and rudders because a Boeing 777 hydraulic unit regularly exceeds 50,000 flight-hour MTBF. In contrast, first-generation EMAs on the Airbus A380 spoiler family averaged only 22,000 hours, opening a lifecycle-cost delta of roughly USD 340,000 per wide-body airframe over 25 years. Electromechanical failure modes, such as motor-winding shorts, power-supply transients, and ball-screw jamming, can drive hard-over scenarios that hydraulics mitigate via passive pressure relief. The FAA Special Airworthiness Information Bulletin CE-24-03 now requires shielded wiring and ferrite filtering within two meters of passenger Wi-Fi to mitigate electromagnetic interference, following 14 uncommanded movement incidents reported in 2024. Airlines such as Delta continue to specify hydraulics on new B737 MAX and A321neo orders to simplify certification, sidestep insurer surcharges, and leverage established MRO networks. Until dual-redundant EMA logic and higher-temperature motor insulation are adopted for civil platforms, hydraulics will remain the default for primary controls.

Thermal Management Limits for High-Power EMAs on Supersonic Platforms

Supersonic platforms face extreme thermal stress: Mach 1.7 cruise drives skin temperatures to 120 °C, and resistive losses add another 85 °C inside actuator motors, enough to demagnetize neodymium and soften aluminum housings. Boom Supersonic, pursuing a 2026 first flight, initially specified Parker EMAs but reverted to hydraulics for elevons after flux density fell 18% during 205 °C soak tests, cutting force output below certification minima. Forced-air cooling would add 2.3 kg per actuator and consume 450 W, negating weight savings; liquid cooling reintroduces leak hazards that EMAs aim to avoid. Research into samarium-cobalt magnets that retain 90% of their flux at 250 °C is at the Technology Readiness Level 4, with commercial volumes unlikely to occur before 2029.[3]Source: “Standards Development,” SAE International, sae.org Military NGAD projects echo the issue, specifying hydraulics on primary controls while reserving EMAs for lower-temperature weapon-bay and inlet-ramp duties.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Linear Actuators Retain Dominance yet Rotary Units Accelerate

Linear units commanded a 70.55% market share of the aircraft actuators market in 2025, driven by the need for long-stroke requirements on landing gear, flaps, and horizontal stabilizers. They will continue to grow at a 6.90% CAGR, thanks to the ramp-up of narrowbody production, although cooling demands for extended ball-screws add design complexity. Rotary actuators, while representing a smaller slice of the aircraft actuators market size today, benefit from 15% better power-to-weight ratios, passive cooling advantages, and regulatory allowances for single-string sensing on secondary systems. That profile suits thrust-reverser cascades, eVTOL tilt-rotors, and UAV pintle-steering, where Moog’s 180 °C-capable EHAs already operate without active cooling. Looking forward, rotary formats will capture incremental share as emerging platforms prize compact footprints and thermal resilience, eroding but not overturning linear supremacy.

A certification asymmetry reinforces the divergence. FAA rules updated in 2024 require dual sensors on linear units used in primary controls, allowing for simpler architectures in rotary devices for secondary applications. This halves validation costs for rotary designs and accelerates entry on weight-sensitive aircraft. Suppliers are sizing the opportunity; Parker-Hannifin’s modular EMA family reuses 70% of parts across both formats, enabling rapid tailoring without retooling. Collins Aerospace’s next-gen rotary EMA for A321XLR thrust reversers shaved deploy time by 19% in cold soak trials, and gains airlines translate directly into runway safety margins.

By System: Electrification Push Chips Away at Hydraulic Incumbency

Hydraulic architectures still account for 44.90% of 2025 revenue, as airlines and regulators trust their 50,000-hour MTBF record on primary surfaces. However, electrical and electromechanical solutions are leading the field with a 7.10% CAGR as more-electric aircraft gain certification. Airbus’ A321XLR validated EMAs on spoilers and horizontal stabilizer trim, carving 180 kg of hydraulic plumbing from the airframe and demonstrating embedded-sensor health monitoring that hydraulics cannot match. Mechanical and pneumatic formats persist in backup and environmental systems. Even here, the weight penalty of central bleed air is steering future programs toward localized electric actuation.

Suppliers blend portfolios accordingly. Parker-Hannifin’s electro-hydrostatic landing-gear package for the A320neo retains hydraulic force density in a self-contained loop, eliminating the need for fleet-wide hydraulic reservoirs and reducing the weight by 85 kg per aircraft. Moog’s defense line adopts a dual-string electrical core with hydraulic lock-pins for primary controls, satisfying military reliability thresholds while nudging systems toward all-electric roadmaps. As reliability data matures and certification agencies become more comfortable with electromechanical redundancy logic, the aircraft actuators market will witness a gradual, irreversible shift toward electrical content in both secondary and, eventually, primary domains.

By Application: Cabin and Seat Systems Deliver the Fastest Upside

Flight control surfaces generated 47.20% of the 2025 value and will continue to dominate gross revenue because safety-critical units carry higher margins and longer qualification cycles. The fastest-growing application is cabin and seat systems, with a 7.85% CAGR, driven by airline efforts to densify premium economy and refresh lie-flat business cabins. Each new seat features six to eight compact EMAs that control recline, leg-rest, and massage functions, transforming the cabin from a hydraulic enclave into a fully electric environment. Those retrofit programs align closely with passenger-experience strategies, allowing airlines to spread capex across seats instead of whole airframes.

Landing gear actuators sit in the mid-pack; electrification is quickening here, too. Safran’s electro-hydrostatic main-gear actuator sliced system weight by 85 kg and won a 250-shipset deal for A320neo deliveries through 2028. Thrust-reverser actuation is transitioning to rotary EMAs, reducing viscosity drag during cold soak and enhancing deployment speed. Environmental and fuel systems, although smaller in revenue, are at the forefront of SAF and hydrogen conversions, driving advancements in seal technology and thermal cycling standards that will eventually permeate mainstream actuation designs.

By End User: Military Outpaces Commercial Growth Trajectory

Commercial operators controlled 67.80% of the 2025 value due to their sheer fleet size, but military programs are expected to expand at an 8.10% CAGR through 2031. The NGAD fighter, F-35 Block 4, and multiple UCAV lines require actuators capable of operating at 180 °C, with a power density of less than 2 kW/kg, and achieving blistering response times of 50 ms. Defense schedules prioritize performance over cost, allowing suppliers to introduce cutting-edge EHAs and high-temperature magnet materials ahead of commercial adoption. Meanwhile, commercial buyers continue to focus on total-cost-of-ownership metrics, favoring retrofit pathways and predictive-maintenance functionality that lock in aftermarket revenue.

General aviation remains a modest and steady contributor as business-jet OEMs migrate to fly-by-wire technology. Gulfstream’s G700 introduced all-EMA secondary controls, trimming maintenance costs by 18% while providing a technical demonstrator for wider commercial adoption. Over the long term, the aircraft actuators industry will benefit from cross-pollination between military high-performance requirements and commercial sustainability mandates.

By Fit: Aftermarket Dominates, but OEM Pull Strengthens

The aftermarket delivered 56.90% of 2025 turnover because actuators undergo multiple replacements over an aircraft’s 25-year life and because smart-sensor retrofits now generate annuity software revenue. Each widebody houses 180-plus units with overhaul cycles ranging from 8,000 to 25,000 flight hours, driving dependable demand. Honeywell’s Forge platform exemplifies the shift to service-oriented models, billing USD 12 per flight hour for actuator health analytics and boosting supplier margins by eight percentage points.

OEM demand rebounds on the back of Airbus and Boeing rate recoveries and the ramp-up of COMAC’s C919. OEM installations are expected to grow at a rate of 6.85% annually through 2031, while fleet growth (3.5% per year) continues to underpin incremental aftermarket demand alongside linefit deliveries (2.8% per year). Lessors’ insistence on OEM-approved components also sustains replacement revenue and cements lock-in for tier-one suppliers.

Geography Analysis

North America contributed 36.85% of 2025 revenue, buoyed by Boeing production hubs in Washington State and USD 842 billion in US defense outlays that funnel actuator demand into F-35 Block 4, NGAD prototypes, and UCAVs. The region also leads in electromechanical adoption; NASA’s Electrified Powertrain flights and the FAA’s health-monitoring mandates have reduced certification friction, stimulating uptake across commercial narrowbody aircraft. A mature installed base of more than 18,000 aircraft drives robust aftermarket turnover, particularly as United Airlines and American Airlines retrofit widebody aircraft with sensor-ready linear actuators to reduce AOG costs. Supply-chain risk, however, looms large because over 90% of neodymium magnets originate from China, amplifying price and lead-time volatility.

Europe remains a steady growth state, anchored by Airbus’ Toulouse and Hamburg lines, as well as defense programs like FCAS and Tempest. The A321XLR’s all-EMA secondary controls shaved 180 kg of hydraulic mass and set a precedent that reverberates through EASA’s certification files. Sustainability policies, such as ReFuelEU, catalyze the retrofitting of fuel-system actuators compatible with higher-lubricity SAF blends. Meanwhile, EASA guidelines, which demand dual-sensor thermal oversight, add USD 45,000 per primary-control EMA, yet accelerate familiarity with smart-actuation setups. Middle East carriers provide another vector; Qatar Airways adopted Safran’s ZEPHYR seats, injecting 8 EMAs per passenger and elevating premium-cabin actuator density.

The Asia-Pacific region is the fastest-growing market, with a projected 7.25% CAGR through 2031. COMAC’s C919 targets 150 deliveries a year by 2028, embedding roughly 110 actuators per aircraft sourced from both local and western brands. India’s Tejas Mk1A and AMCA programs will collectively require millions of actuators across flight controls, weapons bays, and landing gear by 2030, reinforcing the momentum in military aviation. The region has upgraded its overhaul capacity. ST Engineering’s USD 180 million Changi site now cuts actuator turnaround times in half, reducing reliance on North American service centers and intensifying local competition. South America and Africa represent smaller but accelerating bases as Embraer jets and regional carriers add fleets and build indigenous MRO footprints.

Competitive Landscape

The market concentration is moderate, with a few leading players holding significant positions. Key companies include Honeywell, Collins Aerospace (RTX), Parker-Hannifin, Moog, and Safran. These companies secure long-term supply agreements and utilize digital-twin analytics to enhance aftermarket revenue. For instance, Honeywell’s Forge platform predicts actuator wear 500 hours in advance and generates USD 12 per flight hour, shifting profitability toward service offerings. Parker-Hannifin’s modular EMA achieves 70% parts commonality, reducing certification costs by USD 8 million per variant and enabling faster customization across commercial and defense applications.

Smaller challengers, such as Nabtesco, Electromech Technologies, and Curtiss-Wright, are gaining traction in UAV and eVTOL markets by offering lightweight EHAs with power densities exceeding 2 kW/kg. Joby Aviation has adopted vertically integrated actuator designs to meet stringent mass requirements, signaling a potential trend toward OEM-designed systems in the urban air mobility (UAM) segment. Patent activity also highlights emerging areas of competition. For example, Parker filed 14 patents in 2024 related to rare-earth-lean hybrid-reluctance motors, while Collins Aerospace’s HealthAware monitoring service now incorporates machine-learning algorithms, resulting in a 22% reduction in spare-parts inventory.

Regulations are shaping competitive dynamics in the market. The FAA Advisory Circular 25-19A mandates extended-range airframes to include health-monitoring systems, benefiting suppliers with sensor-integrated product portfolios while creating barriers for low-tech entrants. Consolidation trends continue, as evidenced by RTX’s acquisition of a precision motion-control specialist in 2024, which expanded its rotary actuator offerings for thrust-reverser programs, a segment growing at an annual rate of 8%. Looking forward, advancements in rare-earth diversification and high-temperature magnet technologies are expected to redefine sourcing strategies, making materials science a critical factor alongside mechanical innovation in maintaining market share within the aircraft actuators industry.

Aircraft Actuators Industry Leaders

Honeywell International Inc.

Parker-Hannifin Corporation

Moog Inc.

Safran SA

Collins Aerospace (RTX Corporation)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Collins Aerospace announced the expansion of its next-generation electric Thrust Reverser Actuation Systems (elecTRAS) with new facilities in the UK and France. This strategic move underscores the company’s commitment to advancing aircraft electrification, leveraging proven technology with 11 million flight hours on the A350 aircraft.

- January 2025: Air Industries Group secured a contract worth USD 5.9 million to supply flight control assemblies (actuators) for the US Air Force's F-5 and T-38 aircraft. This contract strengthens Air Industries' position in the aerospace supply chain and aligns with defense modernization efforts. It reflects the growing demand for maintaining legacy aircraft, presenting strategic opportunities for manufacturers specializing in precision components to support long-term military readiness and operational efficiency.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the aircraft actuators market as all newly delivered linear and rotary devices, powered by hydraulic, electric, pneumatic, or mechanical energy, that translate cockpit or autonomous commands into motion for flight-control surfaces, landing-gear assemblies, engine inlets and doors, cargo or weapon bay doors, and other utility subsystems on manned and unmanned fixed-wing and rotary-wing aircraft worldwide.

Scope Exclusion: Passenger-seat adjustment mechanisms and ground test rigs sit outside this coverage.

Segmentation Overview

- By Type

- Linear

- Rotary

- By System

- Hydraulic Actuators

- Electrical/Electromechanical Actuators (EMAs)

- Pneumatic Actuators

- Mechanical Actuators

- By Application

- Flight Control Surfaces

- Landing Gear and Braking

- Thrust Reverser Actuation System

- Cabin and Seat Systems

- Environmental and Utility Systems

- Fuel Storage and Distribution System

- By End User

- Commercial Aviation

- Military Aviation

- General Aviation

- By Fit

- Orginial Equipment Manufacturer (OEM)

- Aftermarket

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- France

- Germany

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews and mini-surveys with air-frame engineering leads, Tier-1 actuator suppliers, MRO executives, and regulators across North America, Europe, and Asia helped us confirm production schedules, retrofit intent, price dispersion, and field reliability. As we have learned, a leaked actuator seal can double direct operating costs on a narrow-body within weeks.

Desk Research

Mordor analysts first mapped global fleet growth, production rates, and retirement schedules with open datasets issued by FAA, EASA, IATA, UN Comtrade, SIPRI, and multiple defense procurement portals. They then cross-checked component content in OEM filings, investor decks, and respected trade journals. We anchored average selling prices through contract award notices and pricing cues captured in D&B Hoovers, Dow Jones Factiva, and public tenders before layering currency and raw-material index trends.

Further context on electrification roadmaps, certification cycles, and failure modes was drawn from bodies such as the Aerospace Industries Association, ASTM standards committees, and scholarly articles, giving us clarity on technology substitution timelines. The sources cited illustrate our desk inputs and are not exhaustive; many additional references supported data collection and validation.

Market-Sizing & Forecasting

A top-down build began with yearly aircraft deliveries, in-service fleet hours, and modeled actuator count per platform, which are then multiplied by calibrated ASP bands. Selective supplier roll-ups and channel checks act as bottom-up tests that refine totals. Key variables such as narrow-body backlog burn, electric substitution rate in secondary controls, average flight hours per aircraft, and regional defense procurement budgets feed a multivariate regression, while an ARIMA overlay smooths short-run shocks. Sampled maintenance invoices and retrofit campaign data close any remaining gaps.

Data Validation & Update Cycle

Outputs face variance checks against independent shipment logs, customs flows, and OEM revenue splits, followed by tiered analyst reviews. Only after every anomaly is resolved do we sign off on the model. Reports refresh annually, with interim updates triggered by material events. Before delivery, an analyst performs a fresh pass so clients receive the latest view.

Why Mordor Intelligence's Aircraft Actuators Baseline Commands Confidence

Published estimates often diverge because each firm chooses its own scope, price basis, and refresh rhythm, yet decision-makers need one dependable anchor.

Key gap drivers include whether seat actuation and overhaul services are counted, the aggressiveness of cost-inflation factors, treatment of retrofit labor, and how quickly new electric platforms enter the model. These are areas where Mordor's disciplined scope selection and yearly refresh stand apart.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 10.16 B (2025) | Mordor Intelligence | |

| USD 21.68 B (2024) | Regional Consultancy A | Seats and overhaul services included, ASPs uplifted without OEM discounting |

| USD 8.10 B (2022) | Global Consultancy B | Rotary-wing and retrofit demand omitted, outdated production dataset used |

The comparison shows that Mordor's balanced top-down and bottom-up approach, anchored to transparent variables and an annual review cycle, delivers a market baseline clients can trust for planning and investment decisions.

Key Questions Answered in the Report

What is the projected value of the aircraft actuators market in 2031?

The aircraft actuators market is forecasted to reach USD 14.84 billion by 2031, reflecting a 6.45% CAGR.

Which actuator type currently dominates new deliveries?

Linear units dominate, holding 70.55% market share in 2025 due to long-stroke applications on landing gear and flaps.

Which region will grow fastest over the next five years?

Asia-Pacific is set to advance at a 7.25% CAGR through 2031, propelled by COMAC C919 and Indian defense programs.

Why are airlines adopting smart actuators?

Sensor-embedded actuators enable predictive maintenance that can cut unscheduled events by more than 30% and lower AOG costs.

How are sustainability mandates influencing actuator design?

SAF and hydrogen initiatives require fuel-system actuators with new seal materials and longer strokes, sparking fresh design cycles.

What is the major supply-chain risk for electromechanical actuators (EMAs)?

Dependence on Chinese rare-earth magnets exposes manufacturers to price spikes and delivery delays, prompting research into alternative motor chemistries.

Page last updated on: