Aircraft Electrical Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 26.09 Billion |

| Market Size (2031) | USD 37.07 Billion |

| Growth Rate (2026 - 2031) | 7.28% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

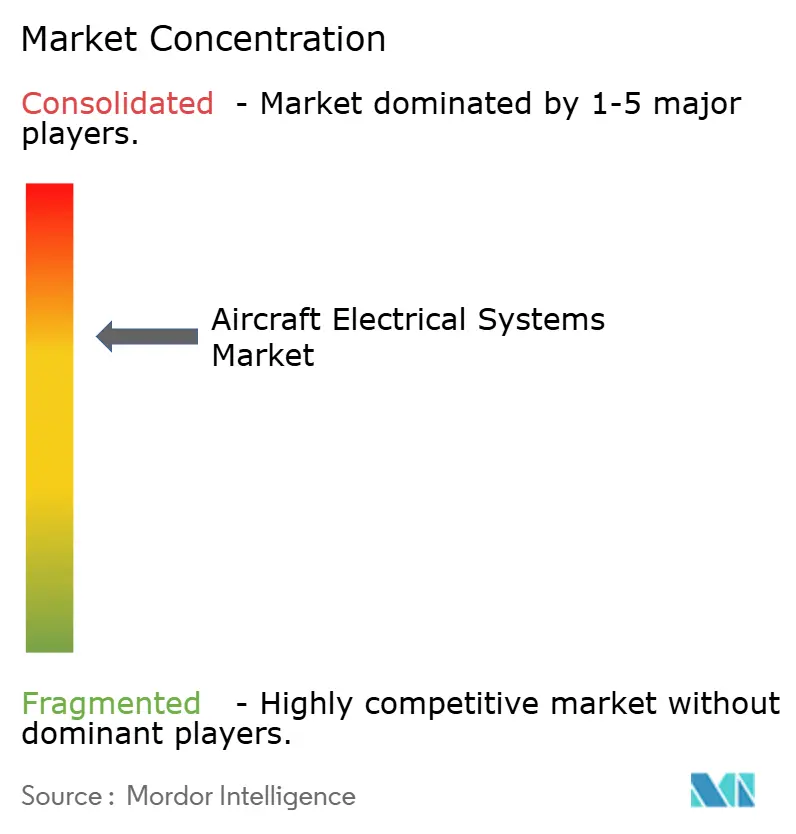

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Electrical Systems Market Analysis by Mordor Intelligence

The aircraft electrical systems market size is expected to grow from USD 23.13 billion in 2025 to USD 26.09 billion in 2026 and is forecasted to reach USD 37.07 billion by 2031 at a 7.28% CAGR over 2026-2031. This growth stems from airline and OEM preferences for More-Electric Aircraft (MEA) designs, which replace pneumatic and hydraulic subsystems with electrically powered equivalents, thereby lowering fuel burn and maintenance demands. Robust commercial backlogs at Airbus SE, The Boeing Company, and COMAC, accompanied by rising widebody retrofits for higher cabin power budgets, secure steady demand across power-generation, distribution, conversion, and energy storage hardware. The continued adoption of 270-volt-plus direct current distribution reduces copper weight by up to 40% while encouraging suppliers to shift toward silicon-carbide (SiC) semiconductors, which are rated for junction temperatures exceeding 200 °C. Hybrid-electric propulsion demonstrators validate high-power starter-generators, and rapid eVTOL prototyping accelerates certification activity for next-generation batteries, converters, and power-distribution software. Collectively, these trends ensure that the aircraft electrical systems market maintains a balanced mix of OEM linefit and aftermarket retrofit opportunities through the early 2030s.

Key Report Takeaways

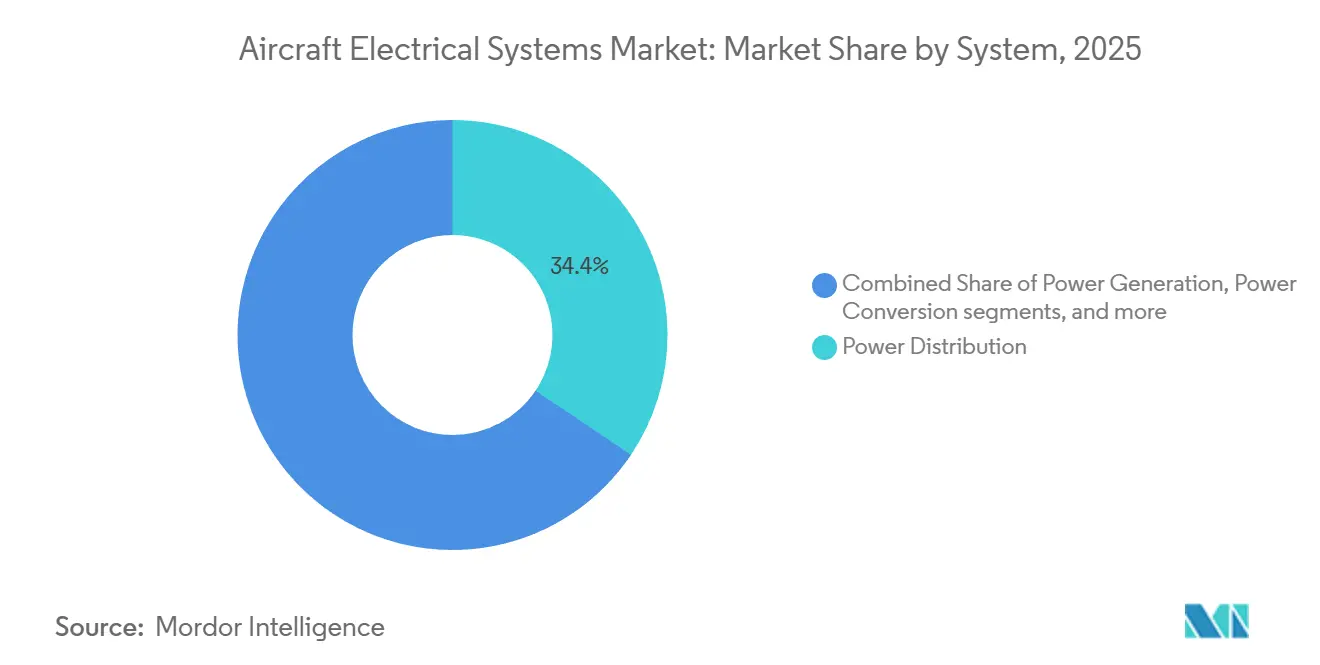

- By system, power distribution led with a 34.41% revenue share in 2025, while energy storage is forecasted to post a 9.44% CAGR through 2031.

- By component, generators and starter-generators held a 23.22% share in 2025, whereas battery packs and battery management systems are projected to expand at an 8.24% CAGR through 2031.

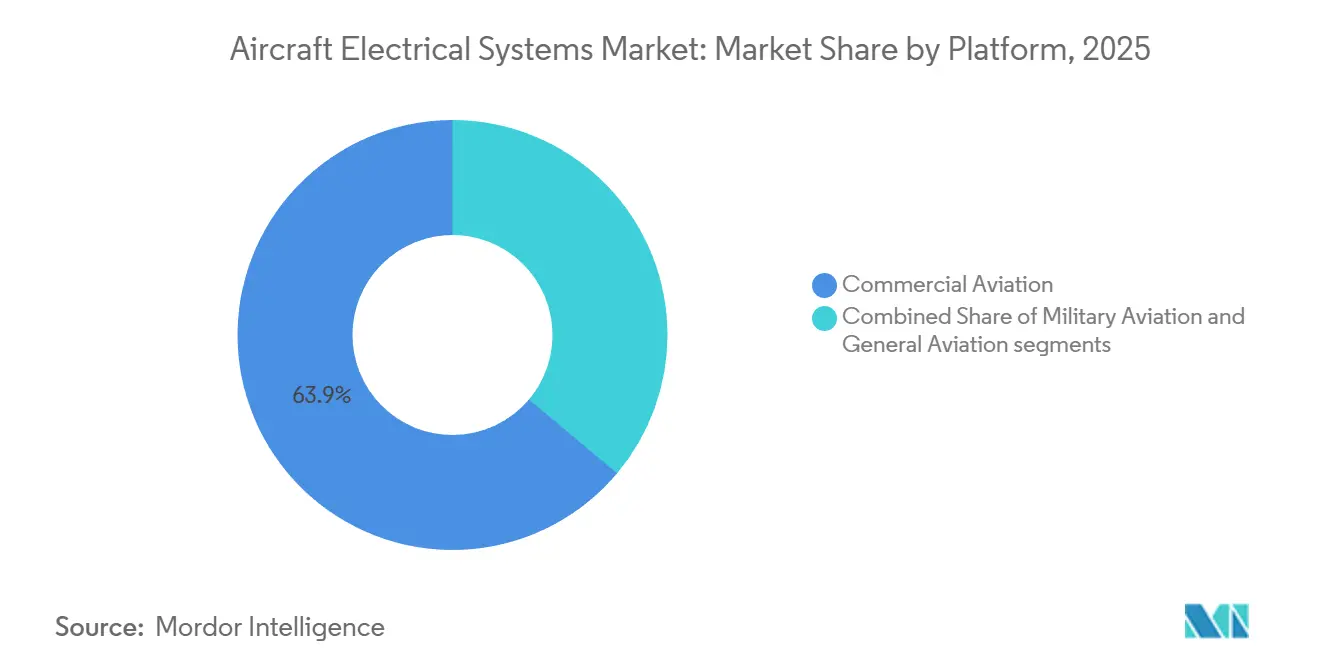

- By platform, commercial aviation accounted for a 63.87% share in 2025, and general aviation is expected to grow at a 9.12% CAGR through 2031.

- By application, power generation management captured a 29.12% share in 2025, while cabin system electrification is expected to increase at an 8.56% CAGR through 2031.

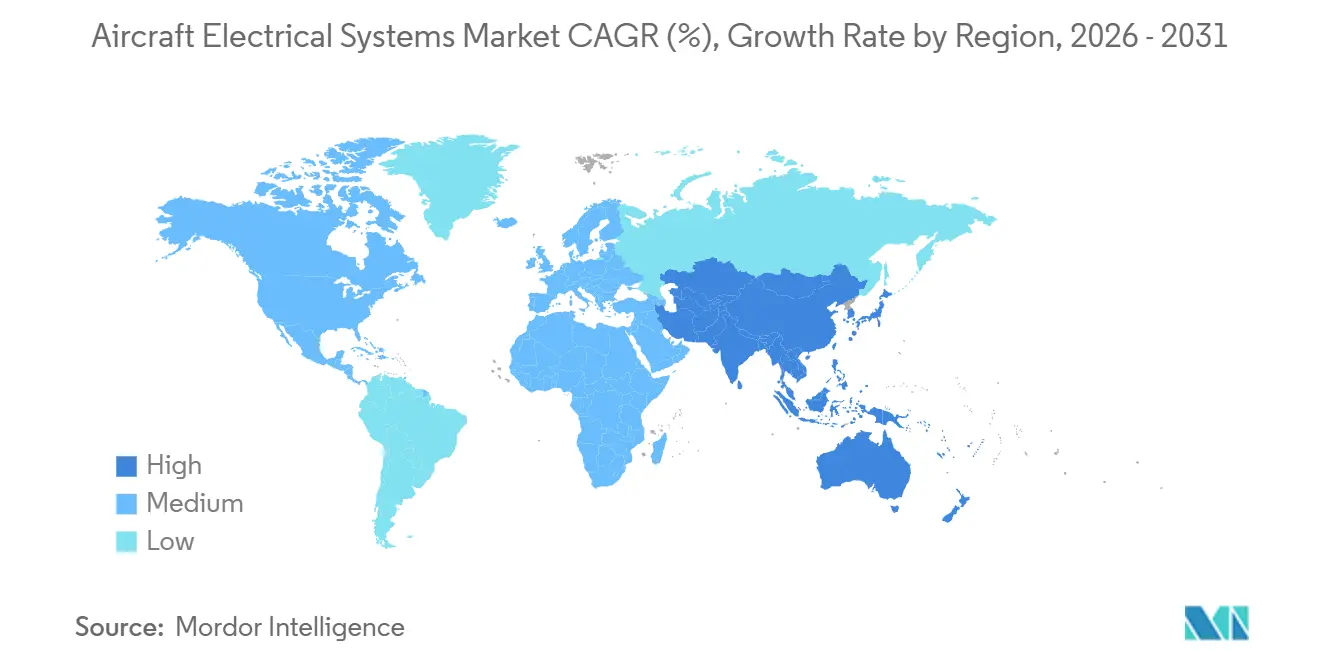

- By geography, North America commanded a 42.22% share in 2025, and the Asia-Pacific region is projected to register the fastest CAGR of 8.01% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Aircraft Electrical Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing adoption of More-Electric Aircraft (MEA) architectures to reduce mechanical complexity and improve efficiency | +2.1% | Global, concentrated in North America and Europe | Medium term (2–4 years) |

| Rising aircraft production volumes and sustained order backlogs driving demand for advanced electrical systems | +1.8% | Global, led by Asia-Pacific and North America | Short term (≤ 2 years) |

| Implementation of high-voltage direct current (HVDC) distribution systems to support next-generation power architectures | +1.5% | North America and Europe, early adoption in Asia-Pacific | Long term (≥ 4 years) |

| Growing need for lightweight and compact electrical systems tailored to unmanned aerial platforms | +0.9% | North America and Middle East, expanding to Asia-Pacific | Medium term (2–4 years) |

| Silicon-carbide (SiC) power electronics enable higher temperature limits | +0.7% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Retrofit-driven upgrades focused on cabin electrification, including in-seat power and galley modernization | +0.6% | Global, concentrated in mature aviation markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Adoption of MEA Architecture

Airlines favor MEA layouts because eliminating engine-bleed air for pressurization and ice protection trims fuel burn by 3-5% on twin-aisle routes across each twenty-year airframe lifecycle. The B787 and A350 paved the way, and the next step targets electromechanical primary flight-control actuators that remove centralized hydraulics altogether. Collins Aerospace’s HECATE program validated a 500-kilowatt hybrid-electric system in 2024, proving that distributed electric motors can assist turbofans during climb and regenerate power during descent.[1]Collins Aerospace, “HECATE Hybrid-Electric Propulsion,” collinsaerospace.com Such architectures require starter-generators exceeding 250 kVA and solid-state power controllers utilizing SiC MOSFETs that can operate at temperatures exceeding 200 °C. Although MEA retrofits increase capital costs by 15-20% over conventional upgrades, they deliver net lifecycle savings by mitigating hydraulic-fluid contamination risk. Compliance with SAE AS50881 on insulation and bend radii ensures that high-voltage harnesses remain compatible with legacy structures.

Rising Aircraft Production Volume and Existing Aircraft Production Backlog

Airbus closed 2024 with 8,658 aircraft on order, equivalent to approximately eleven years of production, guaranteeing recurring demand for generators, power-distribution units, and 180 kilometers of wiring per narrowbody airframe. Boeing plans to increase B737 MAX production to 38 jets per month in 2024 and aims to reach 42 by mid-2026, with each aircraft requiring 15-20 power-distribution modules. COMAC aims to deliver 150 C919s per year by 2028, adding to Asia-Pacific electrical-system demand on an already tight global supply base. India’s Tata-Airbus C295 line in Vadodara features military-grade power-generation capabilities that meet MIL-STD-704F specifications. Although semiconductor packaging bottlenecks lengthen lead times, OEMs now dual-source generator housings and SiC devices to prevent delays in final assembly.

Implementation of HVDC Distribution Systems

Migrating from 115-volt AC to 270-volt DC or higher buses cuts copper mass by up to 40% because lower current minimizes cross-sectional area. Lockheed Martin’s F-35 already employs a 270-volt DC primary bus feeding avionics and directed-energy prototypes without voltage sag. Trials by Airbus and Rolls-Royce using superconducting DC cables cooled by liquid hydrogen have achieved a power density of over 20 kW/kg, although hurdles related to cryogenic certification persist. SiC solid-state circuit breakers can clear faults in 10 µs, yet they cost three times as much as legacy contactors. RTCA DO-160G requires HVDC gear to tolerate 600 A lightning transients, adding weight for filtering networks. Retrofits into legacy airframes mandate electromagnetic-interference recertification under FAA AC 20-158, extending programs by up to a year.

Growing Need for Lightweight and Compact Electrical Systems for Unmanned Aerial Platforms

General Atomics' MQ-9B integrates electric actuators for flight control and sensor gimbals, eliminating hydraulic pumps and trimming empty weight by up to 50 kg. Northrop Grumman's RQ-4 Global Hawk uses a high-resolution radar powered by a 270-volt DC bus that delivers 15 kW, relying on generators with a capacity of more than 5 kW/kg. Battery-electric UAVs under NASA projects reach 300 Wh/kg cell energy, yet AC 20-184 thermal-runaway containment drops pack-level density to roughly 220 Wh/kg. Part 135 cargo drone rules require redundant power channels and load-shedding logic, increasing electrical complexity by 25-30% compared to manned aircraft. Micro-D connectors reduce harness mass by 15-20%, but increase the risk of contact resistance, which engineers address by using gold plating. The Department of Defense's (DoD's) MOSA initiative favors standardized electrical interfaces; however, legacy UAVs lack sufficient bus bandwidth for true plug-and-play upgrades.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Challenges in managing heat and wiring complexity as system voltage levels increase | -1.2% | Global, acute in high-power military and widebody platforms | Short term (≤ 2 years) |

| High certification costs associated with advanced aerospace battery technologies | -0.8% | North America and Europe, regulatory influence spreading to Asia-Pacific | Medium term (2-4 years) |

| Limited availability of qualified semiconductors meeting aerospace-grade performance and reliability standards | -0.7% | Global, with supply chain concentration in Asia-Pacific | Short term (≤ 2 years) |

| Delays in regulatory approvals for software-driven power distribution units due to cybersecurity concerns | -0.5% | Primarily North America and Europe, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Challenges in managing heat and wiring complexity as system voltage levels increase

HVDC buses above 270 volts create localized hotspots where SiC devices dissipate 2-3 W per ampere, requiring robust heat sinks that add up to 12 kg per kilowatt of managed power. Liquid-cooling loops enhance thermal performance but introduce leak risks and duplicate pumps to maintain single-failure tolerance in accordance with FAA Part 25 rules.[2]Federal Aviation Administration, “AC 20-184 Lithium Battery Installation Guidance,” faa.gov Thicker cross-linked polyethylene insulation for HVDC wiring increases the bundle diameter by 20-25%, complicating routing through spars that were initially sized for 115-volt cabling. High-frequency switching noise necessitates the use of shielded twisted pairs and ferrite filters, resulting in an additional 3-5 kg per electrical bay.[3]RTCA, “DO-160G Environmental Conditions,” rtca.org Graphene-enhanced interface pads improve heat transfer but degrade under vibration and must be replaced every 5,000 flight hours, thereby increasing the life-cycle cost. Arc-fault interrupters, as specified in SAE AS5692, prevent wiring fires; however, false trips still disrupt dispatch reliability at rates unacceptable to high-utilization carriers.

High certification costs associated with advanced aerospace battery technologies

FAA AC 20-184 requires lithium-ion (Li-ion) designs to demonstrate thermal-runaway containment at 300 °C, resulting in USD 2-4 million test campaigns per battery model. EASA's CS-ETSO layers vibration and 40-G crash-pulse tests, requiring reinforced housings that reduce gravimetric energy density by up to 20%. Each chemistry tweak restarts qualification and can delay program entry by 18 months, eroding first-mover advantage in the aircraft electrical systems market. DO-178C Level A software development for battery management systems adds USD 0.5-0.8 million per module. The EU Battery Directive's recyclability mandates tack on USD 50-100 per kWh, squeezing margins on price-sensitive regional platforms. Collectively, these hurdles slow the widespread adoption of batteries despite their clear operational benefits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System: Energy Storage Drives Electrification Transition

Energy storage systems are expected to grow at a 9.44% CAGR through 2031, the fastest rate among system categories in the aircraft electrical systems market. The acceleration comes from eVTOL entrants such as Joby’s air taxi and Lilium’s electric jet, both of which are transitioning from prototype to production with large Li-ion packs that comply with AC 20-184 containment rules. Power distribution retained a 34.41% share in 2025, reflecting an installed base of fault-tolerant buses on narrowbody and widebody fleets. Growth moderates as retrofit opportunities on legacy aircraft taper, yet the aircraft electrical systems market size attached to power distribution remains significant for spares and upgrades.

Power generation modules, including constant-frequency and variable-frequency generators, continue to serve baseline loads but are being displaced by hybrid architectures that leverage battery packs during taxi. Power conversion units enable voltage translation between HVDC primary buses and 28-volt secondary avionics rails, with aerospace-qualified converters now achieving 95% efficiency at a power density of 1 kW/in³.[4]Vicor, “High-Density DC-DC Converters,” vicorpower.com Bidirectional converters that recuperate energy during descent support distributed-propulsion concepts being tested on NASA’s X-57 and Airbus’s E-Fan X. As certification frameworks under SAE ARP4754B mature, energy storage and power conversion segments look set for sustained share gains within the aircraft electrical systems market.

By Component: Battery Management Systems Lead Innovation

Battery packs and BMS are forecast to expand at an 8.24% CAGR, driven by eVTOL certification milestones and hybrid-electric demonstrators that demand high-reliability energy storage. Generators and starter-generators maintained a 23.22% share in 2025, underpinned by replacement demand in aging turbofan fleets. Yet growth plateaus as airlines favor auxiliary battery units that power ground operations and reduce fuel burn.

Power distribution units, including SiC solid-state contactors, integrate prognostic health monitoring that predicts wear 500 hours ahead of failure. Converters provide bidirectional power flow for regenerative modes, and aluminum wiring reduces harness mass by 30% while maintaining conductivity via copper-clad terminations. Connectors rated for 50,000 mating cycles ensure reliability on high-frequency test vehicles, and DO-326A cyber-secure firmware is standard in power-distribution software. Together, these trends reinforce component diversification inside the aircraft electrical systems market.

By Platform: General Aviation Embraces Electrification

Commercial aviation commanded a 63.87% share in 2025 as narrowbody production volumes stayed robust at Airbus and Boeing. Widebody programs contribute significantly to the electrical content per airframe, with each B777X set to consume USD 4-6 million in electrical systems. General aviation, encompassing business jets, turboprops, and the rapidly emerging eVTOL cohort, is forecasted to grow at a 9.12% CAGR through 2031, the fastest among platforms within the aircraft electrical systems market.

Business jet retrofits include in-seat power, high-speed connectivity, and induction-heat galleys, with each package costing USD 0.5-1.2 million and increasing cabin electrical loads. Helicopter conversions to electromechanical tail-rotor control reduce hydraulic maintenance and align with the safety expectations of urban air mobility. Military platforms utilize 270-volt DC buses for radar and electronic warfare payloads, transferring technology expertise back to civil programs. The rising demand for advanced power electronics across various platforms is expected to enlarge the aircraft electrical systems market size over the forecast period.

By Application: Cabin Electrification Accelerates Growth

Power generation management accounted for 29.12% of revenue in 2025, covering generator-control units and load-sharing logic that balance the output of multiple generators. Cabin system electrification, however, is expected to achieve the highest application-level growth at an 8.56% CAGR as airlines update their cabins with USB-C charging, 4K displays, and induction-heated galleys. Each narrowbody retrofit can add 10-15 kW of continuous cabin load, driving demand for upgraded generators and power-distribution modules.

Flight control and operation systems are shifting toward electromechanical actuators that halve maintenance intervals by eliminating the need for hydraulic fluids. Electrically driven compressors in environmental control systems reduce fuel burn by up to 5% on long-haul aircraft, although a higher capital cost remains a hurdle. Cargo-handling upgrades in freighters include adding 50 kW generators to power conveyors and hoists, thereby expanding the aircraft electrical systems market share for supplemental power packages. Across various applications, software-mediated load shedding helps manage escalating peak loads without oversizing the generator, thereby reducing costs.

Geography Analysis

Asia-Pacific is poised to post an 8.01% CAGR through 2031, the highest regional rate in the aircraft electrical systems market, supported by COMAC’s C919 ramp, Airbus’s Tianjin A320 line, and India’s Tata-Airbus C295 program. North America retained a 42.22% share in 2025, leveraging Boeing’s Everett and Renton centers, Lockheed Martin’s F-35 facility, and a dense Tier-1 ecosystem across Seattle, Wichita, and Phoenix. Europe benefits from Airbus hubs in Hamburg and Toulouse, and sees consistent demand for retrofits of its widebody fleets.

Middle East carriers operate young, widebody heavy fleets, purchasing high-power cabin connectivity upgrades that boost regional electrical system revenues. South America remains modest, anchored by Embraer’s E2 line, but aftermarket retrofits on older ERJ-145 fleets add steady pull. Africa’s market is small yet growing, as Ethiopian Airlines modernizes its mixed fleets to comply with ICAO Annex 6 electrical safety mandates. As OEM offsets and localized manufacturing spread across Asia and the Middle East, geographic diversification strengthens global supply chain resilience within the aircraft electrical systems market.

Competitive Landscape

The aircraft electrical systems market exhibits moderate consolidation, with the top five suppliers accounting for over 50% of the global revenue. Honeywell International Inc., RTX Corporation, Safran SA, General Electric Company, and Thales Group actively engage in mergers and acquisitions (M&A) to address capability gaps. Honeywell’s CAES takeover extends its RF-shielding and electromagnetic compatibility expertise, while Thales Group absorbs Cobham Aerospace Communications to expand its cockpit connectivity capabilities.

Technology differentiation orbits around power density, HVDC integration, and cyber-resilience. Major players channel R&D dollars into silicon-carbide devices that sustain 200 °C junctions, thus reducing cooling mass. Smaller firms position themselves in niche eVTOL subsystems, often partnering with incumbents to navigate the complexity of certification. The regulatory environment reinforces incumbency, as extensive compliance track records are prerequisites for type certificate amendments.

Technological differentiation centers on silicon-carbide power electronics, where Wolfspeed and Infineon supply MOSFETs that raise operating temperature limits and cut heat-sink mass 30%. Patent filings for solid-state circuit breakers and bidirectional converters increased by 35% between 2023 and 2025, indicating supplier confidence in HVDC adoption for the next commercial single-aisle. Consolidation continues, as illustrated by Parker-Hannifin’s 2022 acquisition of Meggitt, which merges hydraulic and electrical actuation. Meanwhile, Tier-2 suppliers in the Asia-Pacific region are expanding their wiring-harness capacities, although AS9100 audits are extending qualification cycles, thereby maintaining their incumbent advantage within the aircraft electrical systems market.

Aircraft Electrical Systems Industry Leaders

RTX Corporation

Honeywell International Inc.

General Electric Company

Thales Group

Safran SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Safran Electrical & Power (Safran SA) and Saft (TotalEnergies) introduced a modular high-voltage Li-ion battery for next-generation electric aviation, supporting flexible installation and longer endurance.

- May 2025: Vertical Aerospace and Honeywell International Inc. deepened cooperation on the VX4 eVTOL, integrating Anthem Flight Deck and compact fly-by-wire controls to deliver at least 150 aircraft by 2030.

- April 2025: RTX’s Collins Aerospace signed a four-year extension of its cabin interior parts distribution agreement with Satair, which covers the global distribution of cabin interior electrical parts.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the aircraft electrical systems market as the value of on-board networks that generate, distribute, convert, and store electrical power on fixed-wing and rotary platforms across commercial, military, and general aviation fleets. The model covers original equipment and retrofit hardware, together with software that manages these subsystems.

Scope exclusion: standalone avionics, cabin entertainment boxes, and ground power units are excluded to avoid double counting.

Segmentation Overview

- By System

- Power Generation

- Power Distribution

- Power Conversion

- Energy Storage

- By Component

- Generators and Starter-Generators

- Power Distribution Units

- Converters

- Battery Packs and Battery Management System (BMS)

- Wiring and Cables

- Connectors and Contactors

- Power-distribution Software

- By Platform

- Commercial Aviation

- Narrowbody

- Widebody

- Regional Jets

- Freighters

- Military Aviation

- Combat Aircraft

- Transport Aircraft

- Unmanned Aerial Vehicles (UAVs)

- Trainer Aircraft

- General Aviation

- Business Jets

- Helicopters

- Electric Vertical Take-Off and Landing (eVTOL)/Advanced Air Mobility (AAM)

- Commercial Aviation

- By Application

- Power Generation Management

- Flight Control and Operation

- Cabin System

- Configuration Management

- Air Pressurization and Conditioning

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- France

- Germany

- Italy

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed airline engineering managers, military program officers, maintenance providers, and tier-one system integrators across North America, Europe, and Asia-Pacific. Their insights clarified typical replacement cycles, battery adoption hurdles, and average selling price progressions, which we then reconciled with desk findings.

Desk Research

We began with open datasets issued by air-safety regulators such as the FAA, EASA, and ICAO, which offer production, fleet, and flight-hour statistics across aircraft categories. Trade groups like IATA and the Aerospace Industries Association publish annual aircraft delivery guides that help us profile platform mix. Patent abstracts accessed through Questel reveal technology migration toward more-electric architectures, while customs dashboards from Volza trace import values for generators, distribution panels, and lithium batteries. Company 10-Ks and investor decks supplement pricing and share shifts. This list is illustrative, and numerous additional sources fed our evidence base.

Mordor analysts also tapped paid repositories, D&B Hoovers for OEM revenue splits and Aviation Week for program backlogs, providing granular cross-checks on unit shipments and retrofit demand.

Market-Sizing & Forecasting

A single top-down build draws on fleet counts, flight hours, and rated electrical content per platform, then reconciles with selective bottom-up supplier roll-ups to adjust anomalies. Key variables include average kVA installed per new aircraft, retrofit penetration rates, lithium-ion pack cost curves, regulatory mandates on bleed-less systems, and platform production schedules. We forecast through 2030 using multivariate regression tied to deliveries, fuel-price trends, and defense procurement plans. Gaps in bottom-up inputs are bridged by channel checks and normalized against historical price erosion curves.

Data Validation & Update Cycle

Outputs pass a two-step analyst peer review, variance thresholds trigger re-runs, and modeled totals are benchmarked against independent traffic and procurement indicators before sign-off. Reports refresh every year, with interim revisions when material events emerge, so clients receive an up-to-date baseline.

Why Mordor's Aircraft Electrical Systems Baseline Inspires Confidence

Published market figures often differ because studies frame system boundaries, inflation treatments, and forecast cadences in distinct ways.

Key gap drivers include whether energy-storage software is counted, the year in which lithium battery cost parity is assumed, and how retrofit activity is allocated between platforms. Mordor's scope aligns with OEM bill-of-materials and uses 2024 constant dollars, while some publishers mix current and nominal values or apply aggressive electrification take-up curves.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 23.13 B (2025) | Mordor Intelligence | - |

| USD 22.00 B (2024) | Global Consultancy A | Excludes aftermarket retrofits and applies older ASPs |

| USD 26.60 B (2024) | Regional Consultancy B | Counts wiring harnesses and cabin infotainment power units |

| USD 41.70 B (2025) | Trade Journal C | Uses aggressive more-electric adoption rate and nominal dollars |

The comparison shows that when scope creep or optimistic uptake is removed, Mordor's balanced approach, anchored to verified fleet data and moderated adoption curves, offers executives a dependable decision baseline.

Key Questions Answered in the Report

What is the projected value of the aircraft electrical systems market in 2031?

The aircraft electrical systems market is forecasted to reach USD 37.07 billion by 2031, growing at a 7.28% CAGR.

Which geographic region is expected to grow fastest through 2031?

Asia-Pacific is projected to post an 8.01% CAGR, the highest among all regions.

Which system segment shows the highest growth potential?

Energy storage systems are expected to expand at a 9.44% CAGR as eVTOL and hybrid-electric programs mature.

How dominant are incumbents in the competitive landscape?

The top five suppliers hold more than 50% share, reflecting moderate concentration but ongoing space for new entrants.

What certification challenge most affects battery adoption?

Compliance with FAA AC 20-184 thermal-runaway containment tests adds USD 2-4 million per battery design and can delay programs 12-18 months.

Which application area is projected to grow quickest?

Cabin system electrification leads with an 8.56% CAGR, driven by in-seat power, high-definition IFE, and induction-galley retrofits.

Page last updated on: