Aircraft Strut Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

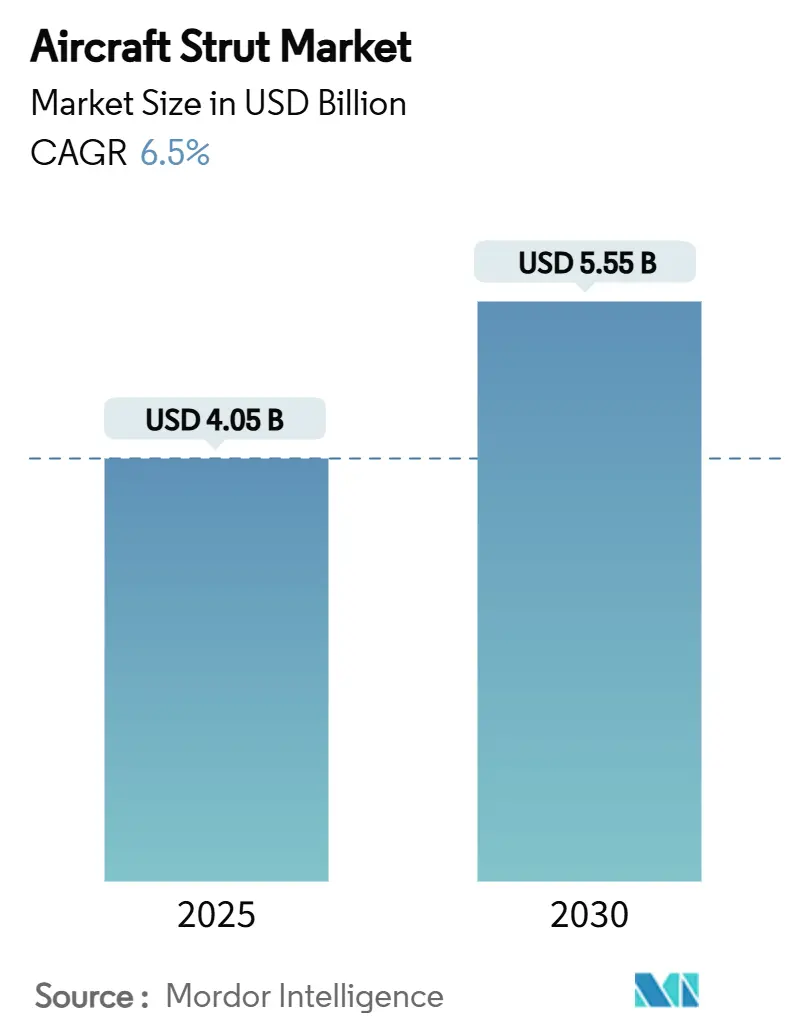

| Market Size (2025) | USD 4.05 Billion |

| Market Size (2030) | USD 5.55 Billion |

| Growth Rate (2025 - 2030) | 6.50% CAGR |

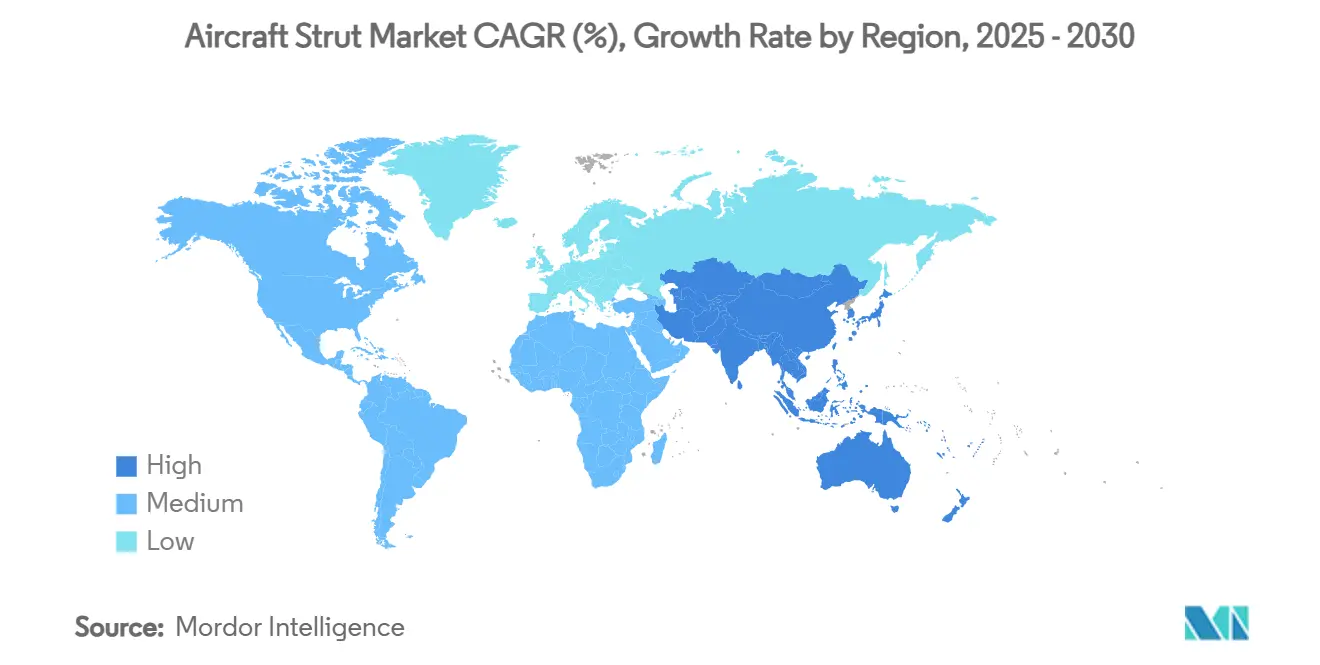

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Strut Market Analysis by Mordor Intelligence

The aircraft strut market size stood at USD 4.05 billion in 2025 and is forecasted to reach USD 5.55 billion by 2030, reflecting a 6.50% CAGR. Rising narrowbody production, expanding defense procurement, and accelerated composite adoption continue to underpin demand across commercial, military, and emerging aviation platforms. The aircraft strut market benefits from record OEM backlogs exceeding 15,700 jets, even as supply-chain pressures prompt greater use of predictive maintenance and component exchange programs. Weight-saving mandates steer manufacturers toward advanced composites that can reduce mass by up to 30% while preserving fatigue life. Meanwhile, Asia-Pacific fleet expansion is reshaping the competitive order as regional MRO spending is projected to triple by 2043. Established suppliers such as Safran, Collins Aerospace, and Liebherr consolidate share through vertically integrated landing-gear capabilities and global overhaul networks, safeguarding their position in an aircraft strut market increasingly focused on lifecycle economics.

Key Report Takeaways

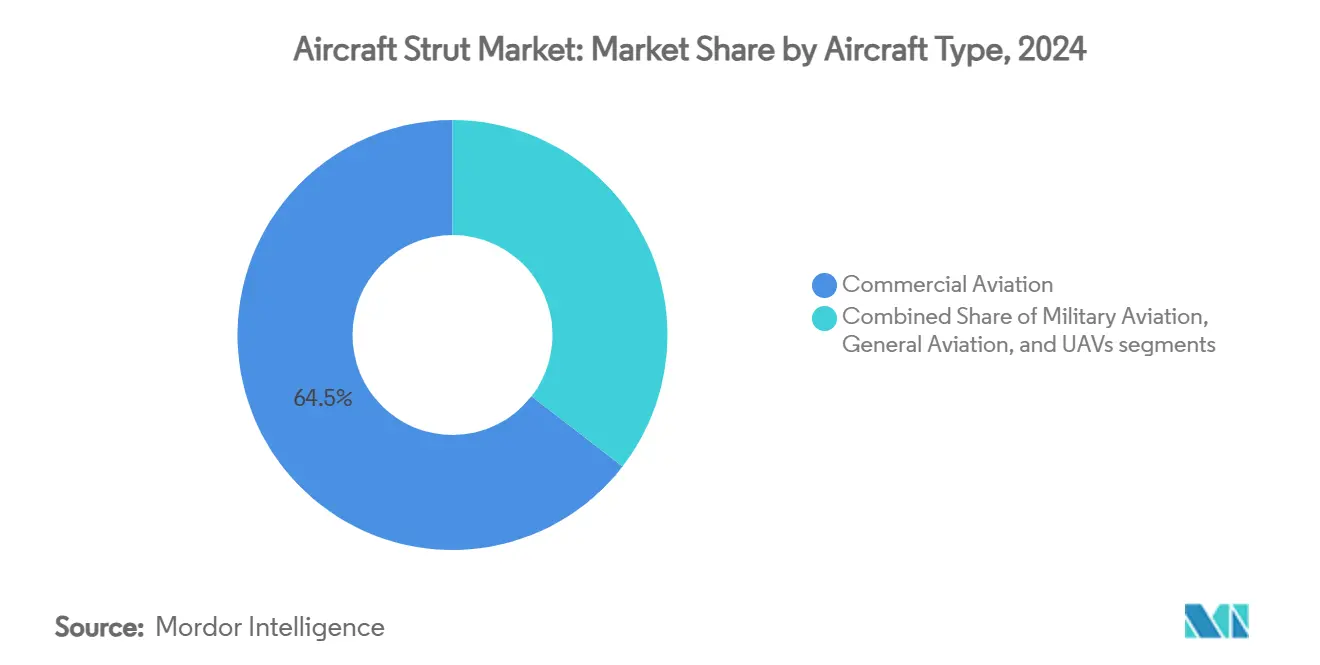

- By aircraft type, commercial aviation led with 64.52% revenue share in 2024; military aviation is projected to register the highest 7.43% CAGR through 2030.

- By strut type, shock absorber/drag struts accounted for 40.25% of the aircraft strut market share in 2024, while main landing gear struts are poised for a 6.23% CAGR to 2030.

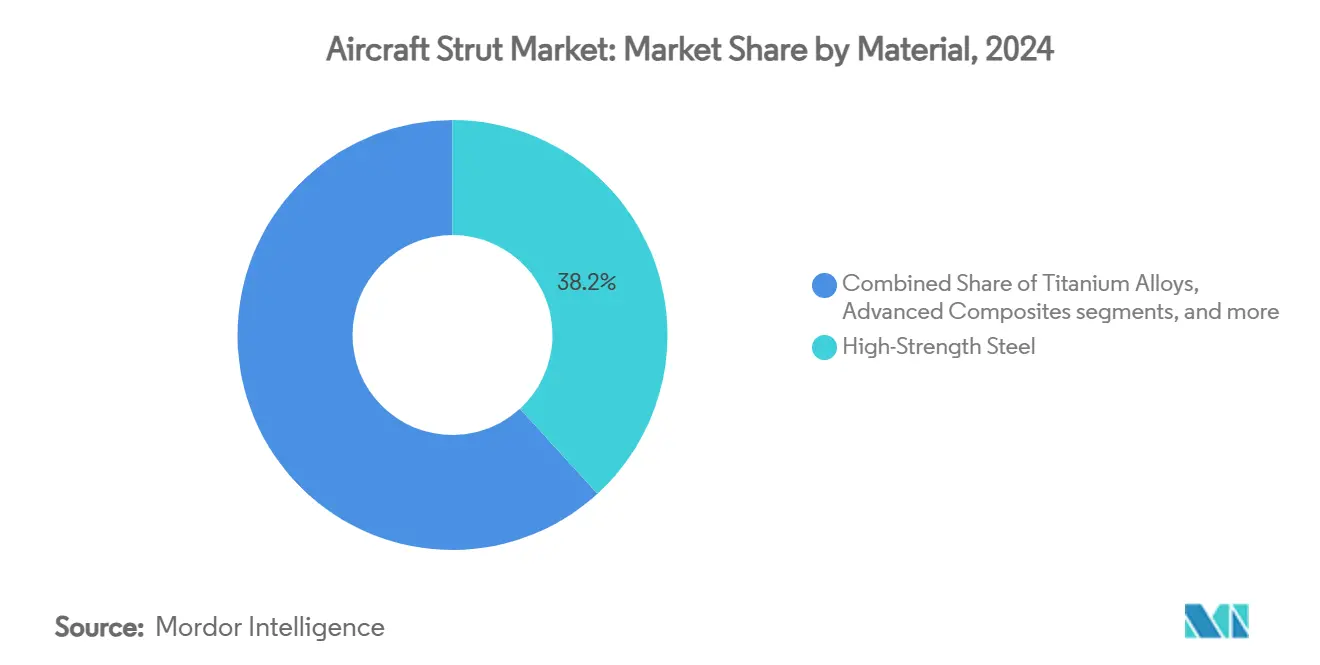

- By material, high-strength steel held a 38.21% share of the 2024 aircraft strut market; advanced composites are forecasted to expand at an 8.29% CAGR between 2025 and 2030.

- By end-user, OEM installations captured a 59.48% share in 2024, whereas the aftermarket/MRO segment is advancing at an 8.27% CAGR through 2030.

- By geography, North America commanded 38.49% of the aircraft strut market in 2024; Asia-Pacific represents the fastest-growing region, with a 6.29% CAGR to 2030.

Global Aircraft Strut Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased narrowbody build rates | +1.2% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Fleetwide aging gear replacement cycle | +1.0% | Global | Long term (≥ 4 years) |

| Defense procurement upswing in landing gear intensive aircraft | +0.8% | Asia-Pacific, Middle East | Medium term (2-4 years) |

| Revival of regional/commuter turboprops | +0.6% | Asia-Pacific, Emerging markets | Long term (≥ 4 years) |

| Lightweight smart-strut R&D tax incentives | +0.4% | North America, Europe | Long term (≥ 4 years) |

| eVTOL certification rules mandating shock-loading tests | +0.3% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increased Narrowbody Build Rates

Airbus delivered 278 aircraft and Boeing delivered 300 by mid-2025, sustaining accelerated A320neo and B737 MAX output despite supply-chain headwinds.[1]ePlane AI, “Boeing and Airbus Aircraft Deliveries in 2025 Compared,” eplaneai.com Each narrow-body requires multiple main, nose, and auxiliary struts, directly elevating aggregate demand across the aircraft strut market. Safran’s reinforced A320 family landing-gear design extends overhaul intervals by more than 20%, aligning component durability with higher fleet utilization. Suppliers are reallocating production capacity toward Airbus programs as Boeing grapples with ramp-up constraints, intensifying competition for precision-machined strut assemblies. Elevated single-aisle output, therefore, remains the single most significant volume catalyst through at least 2028, translating into sustained upside for manufacturers positioned on high-rate platforms.

Fleetwide Aging Gear Replacement Cycle

Deferred retirements and delivery delays are extending airframe service lives, propelling an aftermarket forecast of USD 135 billion by 2034 for maintenance activities that heavily feature landing-gear overhauls. Airlines favor premium strut designs with longer time-on-wing to minimize unplanned removals, encouraging component upgrades that price above legacy equivalents. Safran recorded a 10.8% year-on-year rise in equipment and defense revenue in Q1 2025, driven partly by aftermarket landing-gear sales.[2]Safran Group, “Main and Nose Landing Gears for the Airbus Single-Aisle Aircraft Family,” safran-group.com Predictive analytics embedded within smart struts further improves replacement timing, reinforcing a secular shift toward condition-based maintenance strategies. Consequently, the aircraft strut market secures recurring revenue streams insulated from OEM production cyclicality.

Defense Procurement Upswing in Landing Gear Intensive Aircraft

Asia-Pacific nations are boosting fighter and transport fleets, exemplified by Indonesia’s order for 48 KAAN fifth-generation jets valued at USD 10 billion. Military programs demand rugged struts capable of absorbing high-sink-rate carrier or unprepared-strip landings, generating higher unit-value opportunities versus commercial platforms. Aviation Week estimates USD 63 billion worth of military aircraft competitions over the next decade, with the Middle East and Asia-Pacific accounting for more than 40% of projected awards. The resultant procurement surge bolsters long-term order visibility for specialized strut suppliers adept at meeting stringent defense specifications.

Revival of Regional/Commuter Turboprops

ATR secured 56 orders in 2024 while maintaining a backlog beyond 150 aircraft, signalling a rebound in sub-90-seat turboprop demand. Embraer projects 1,780 turboprop deliveries over the next two decades as emerging economies prioritize short-haul connectivity. Turboprops require robust struts designed for frequent cycles and rough-field operations, adding incremental volume to the aircraft strut market through 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw material price volatility | -0.8% | Global | Short term (≤ 2 years) |

| High certification and testing costs | -0.6% | Developed markets | Medium term (2-4 years) |

| Cyclical airline profitability dampening MRO budgets | -0.4% | Global | Short term (≤ 2 years) |

| Additive manufacturing IP barriers for strut redesigns | -0.3% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility

Steel, aluminum, and titanium prices swung widely in 2024, with titanium alloy costs climbing amid geopolitical supply constraints.[3]Lasting Titanium, “Titanium Price Trends and Influencing Factors in the Second Half of 2024,” lastingtitanium.com Reinstating 25% tariffs on select metals in the United States aggravated input-cost uncertainty for aerospace suppliers. Landing-gear makers respond by carrying higher raw-material inventories, which tie up working capital and raise storage expenses, eroding already thin margins. Hedging on metals futures offers partial relief, but volatile spot prices often diverge from contracted hedge levels, weakening the effectiveness of such strategies. Long-term fixed-price contracts, meanwhile, limit manufacturers’ ability to pass surcharges to OEMs or airlines, compressing profitability and curbing near-term investment in new strut programs within the aircraft strut market. Extended budget uncertainty delays strategic sourcing decisions, creating ripple effects across the landing-gear supply chain.

High Certification and Testing Costs

Regulatory frameworks such as 14 CFR Part 25 Subpart D mandate exhaustive shock-absorption and fatigue testing that can extend development cycles by up to three years and cost several million dollars. Composite or additively manufactured struts must also show material equivalency, escalating compliance outlays for smaller suppliers that lack in-house laboratories. Full-scale drop tests require purpose-built rigs capable of replicating high-sink-rate impacts, and any late-stage design tweak can trigger retesting, further inflating budgets. Manufacturers must fund extensive documentation, including finite-element analysis packages and traceable raw-material records, adding months to program timelines. The resultant financial burden slows innovation diffusion and keeps entry barriers high in the aircraft strut market, particularly for disruptive startups seeking to replace legacy metallic designs. Protracted certification schedules deter venture investment, leaving incumbents with entrenched regulatory know-how to dominate upcoming platform awards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Commercial Dominance with Accelerating Military Orders

Commercial aviation generated 64.52% of 2024 revenue, cementing its status as the core demand pillar for the aircraft strut market. Narrowbody jets contribute the highest unit volume, while widebodies integrate titanium inner-cylinder struts to shave weight and maintenance costs. Though smaller in absolute terms, military aviation is on track for a 7.43% CAGR, buoyed by sustained fighter acquisitions across Asia-Pacific and Middle-Eastern customers that favor rugged landing-gear architectures.

Strut suppliers serving both sectors diversify revenue and hedge cyclicality, positioning the aircraft strut market for balanced growth. Unmanned combat air vehicles (UCAVs) like the XQ-58A now feature retractable gear, opening a budding sub-segment. Airlines’ continuous cycle-driven wear keeps replacement demand high, while defense programs carry thicker margins tied to stringent durability specifications.

By Strut Type: Shock Absorbers Hold Share as Main Gear Surges

Shock absorber/drag struts retained 40.25% of 2024 revenue, reflecting their multiplicity across main and nose assemblies. Yet main landing gear struts are forecasted to grow at 6.23% CAGR, outpacing total aircraft strut market growth as heavier, longer-range aircraft require stronger load-bearing solutions. Two-cylinder main gear designs adopted on widebodies improve load distribution and service intervals, increasing average content per aircraft.

Smart-monitoring sensors embedded in new-generation struts alert operators to pressure or temperature deviations, supporting predictive maintenance adoption across the aircraft strut industry. Enhanced metering-pin hydraulics further optimize damping characteristics, reducing rebound forces and extending tire life.

By Material: Steel Still Dominant while Composite Adoption Accelerates

High-strength steel contributed 38.21% of 2024 revenue because of its mature supply base and predictable behavior under high-load events. Composite materials, however, are forecasted to post an 8.29% CAGR, the fastest in the aircraft strut market, as carbon-fiber reinforced polymers achieve up to 30% mass reduction alongside superior fatigue resistance.

OEMs integrating composites reduce fuel burn and open avenues for smart-sensor embedment during lay-up. Titanium alloys remain the premium choice for extreme strength-to-weight applications, including high-cycle fighter fleets. Suppliers able to balance multipronged material portfolios are expected to capture disproportionate aircraft strut market share gains through 2030.

By End-User: OEM Installations Lead but Aftermarket Gains Momentum

OEM fitments generated 59.48% of 2024 revenue, closely tracking aircraft rollout rates. The aftermarket/MRO channel is set to record 8.27% CAGR as airlines extend fleet lives and seek cost-effective landing-gear exchanges. Boeing’s Landing Gear Exchange Program exemplifies service models that minimize downtime by supplying ready-overhauled ship-sets.

Consolidation is reshaping the MRO landscape; GA Telesis’s USD 51 million purchase of AAR’s landing-gear unit augments repair depth and regional coverage.[4]Cargo Facts, “GA Telesis Acquires AAR’s Landing Gear MRO Business for $51 Million,” cargofacts.com As predictive analytics proliferate, component life is optimized, yet scheduled overhaul frequency remains governed by regulatory cycle limits, anchoring a stable aftermarket for the aircraft strut market.

Geography Analysis

North America dominates the aircraft strut market through sheer production scale and defense outlays. Boeing’s Renton and Charleston lines anchor commercial output, while US government programs such as the F-35 and B-21 Raider sustain high-specification landing-gear demand. Safran’s USD 80 million investment in Querétaro expands LEAP engine component capacity and deepens regional vertical integration. Robust aftermarket infrastructure, including WestJet and Lufthansa Technik’s new Calgary facility for LEAP-1B engines, further cements regional pull for premium strut services.

Asia-Pacific’s aircraft strut market ascends on the back of rising turboprop and narrow-body deliveries. Indonesia’s record fighter purchase and India’s growing ATR fleet exemplify defense and regional air mobility growth drivers. Local supply-chain maturation, especially in titanium sponge production in China, could compress cost bases and redirect export flows. Meanwhile, eVTOL certification pilots in Singapore and Japan will likely spark demand for specialized urban-mobility struts before 2030.

Europe maintains a sizeable share through Airbus’ multination assembly footprint and strong R&D funding lines such as Clean Sky 2. Liebherr-Aerospace allocates more than 17% of revenue to research, securing positions on the B777X main-gear program. The region’s emphasis on sustainability, illustrated by thermoplastic fuselage demonstrators, supports advanced-material penetration that benefits composite-capable strut suppliers.

Competitive Landscape

The aircraft strut market exhibits moderate concentration, with Safran Landing Systems, Collins Aerospace, and Liebherr Group collectively estimated to control over 55% of OEM ship-set awards. Safran logged 16.7% revenue expansion in Q1 2025 on civil-aftermarket strength, simultaneously investing more than EUR 1 billion (USD 1.17 billion) to enlarge its global LEAP MRO network. Collins Aerospace differentiates through composite structural expertise that is capable of delivering 30% weight savings.[5]Collins Aerospace, “Composite Structural Components,” collinsaerospace.com Liebherr continues to win new-generation wide-body contracts by combining electro-hydraulic actuation with predictive-health monitoring.

Market entrants focus on additive manufacturing to cut lead times, yet face IP entanglements and certification costs, reinforcing incumbent advantages. Consolidation remains active; Platinum Equity’s proposed USD 1.35 billion acquisition of Héroux-Devtek exemplifies private-equity interest in niche aerostructure specialists. Strategic partnerships, such as Safran and HAL’s forging collaboration in India, illustrate localization moves intended to secure offset credits and lower logistics risk.

Technology roadmaps converge on smart struts incorporating embedded sensors and advanced surface treatments that lengthen overhaul intervals. Suppliers able to pair material advancements with digital-health capabilities are best placed to expand the aircraft strut market share as airlines and militaries transition toward data-driven maintenance frameworks.

Aircraft Strut Industry Leaders

Safran SA

Collins Aerospace (RTX Corporation)

Liebherr Group

Parker-Hannifin Corporation

Héroux-Devtek Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Dublin Aerospace signed a five-year agreement with EgyptAir Maintenance & Engineering for landing gear overhaul services on B737NG aircraft. Starting in July 2025, the contract builds on their partnership from 2017 and strengthens Dublin Aerospace's position in maintaining EgyptAir's fleet.

- April 2025: Air Industries Group received contracts worth USD 1.5 million to manufacture landing gear components for the US Air Force's B-1B Lancer heavy bomber and F-16 Fighting Falcon combat aircraft.

- March 2025: Liebherr-Aerospace Saline signed an agreement with SkyWest Airlines to provide landing gear overhaul and systems maintenance for a portion of SkyWest's Embraer 175-E1 fleet.

- December 2024: GA Telesis, LLC, signed a multi-year agreement with CommuteAir, a United Express carrier, to repair and overhaul Embraer landing gear systems. The agreement covers CommuteAir's Embraer 145 aircraft fleet, providing landing gear maintenance support and improving operational efficiency.

Global Aircraft Strut Market Report Scope

| Commercial Aviation | Narrowbody |

| Widebody | |

| Regional Jets | |

| Military Aviation | Fighter Jets |

| Transport Aircraft | |

| Rotorcraft | |

| General Aviation | |

| Unmanned Aerial Vehicles (UAVs) |

| Main Landing Gear Struts |

| Nose Landing Gear Struts |

| Tail Gear Struts |

| Shock Absorber/Drag Struts |

| High-Strength Steel |

| 7000-Series Aluminium |

| Titanium Alloys |

| Advanced Composites |

| OEM |

| Aftermarket/MRO |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of South Africa | ||

| By Aircraft Type | Commercial Aviation | Narrowbody | |

| Widebody | |||

| Regional Jets | |||

| Military Aviation | Fighter Jets | ||

| Transport Aircraft | |||

| Rotorcraft | |||

| General Aviation | |||

| Unmanned Aerial Vehicles (UAVs) | |||

| By Strut Type | Main Landing Gear Struts | ||

| Nose Landing Gear Struts | |||

| Tail Gear Struts | |||

| Shock Absorber/Drag Struts | |||

| By Material | High-Strength Steel | ||

| 7000-Series Aluminium | |||

| Titanium Alloys | |||

| Advanced Composites | |||

| By End-User | OEM | ||

| Aftermarket/MRO | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of South Africa | |||

Key Questions Answered in the Report

What is the current size of the aircraft strut market?

The aircraft strut market size reached USD 4.05 billion in 2025 and is projected to climb to USD 5.55 billion by 2030, reflecting a 6.50% CAGR.

Which segment holds the largest Aircraft strut market share?

Commercial aviation leads, generating 64.52% of 2024 revenue thanks to sustained narrow-body production.

Which material segment is growing the fastest?

Advanced composites are expanding at an 8.29% CAGR as OEMs prioritize weight reduction and fuel efficiency.

Why is Asia-Pacific the fastest-growing regional market?

The region’s rapid fleet expansion, rising defense budgets, and burgeoning MRO capacity drive a forecasted 6.29% CAGR through 2030.

How are smart struts influencing maintenance strategies?

Embedded sensors enable condition-based monitoring, reducing unscheduled removals and aligning overhaul timing with true wear patterns.

What factors most threaten near-term growth?

Raw-material price volatility and high certification costs are the principal restraints, subtracting a combined 1.4 percentage points from the forecasted CAGR.

Page last updated on: