Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 64.46 Billion |

| Market Size (2031) | USD 86.07 Billion |

| Growth Rate (2026 - 2031) | 5.96% CAGR |

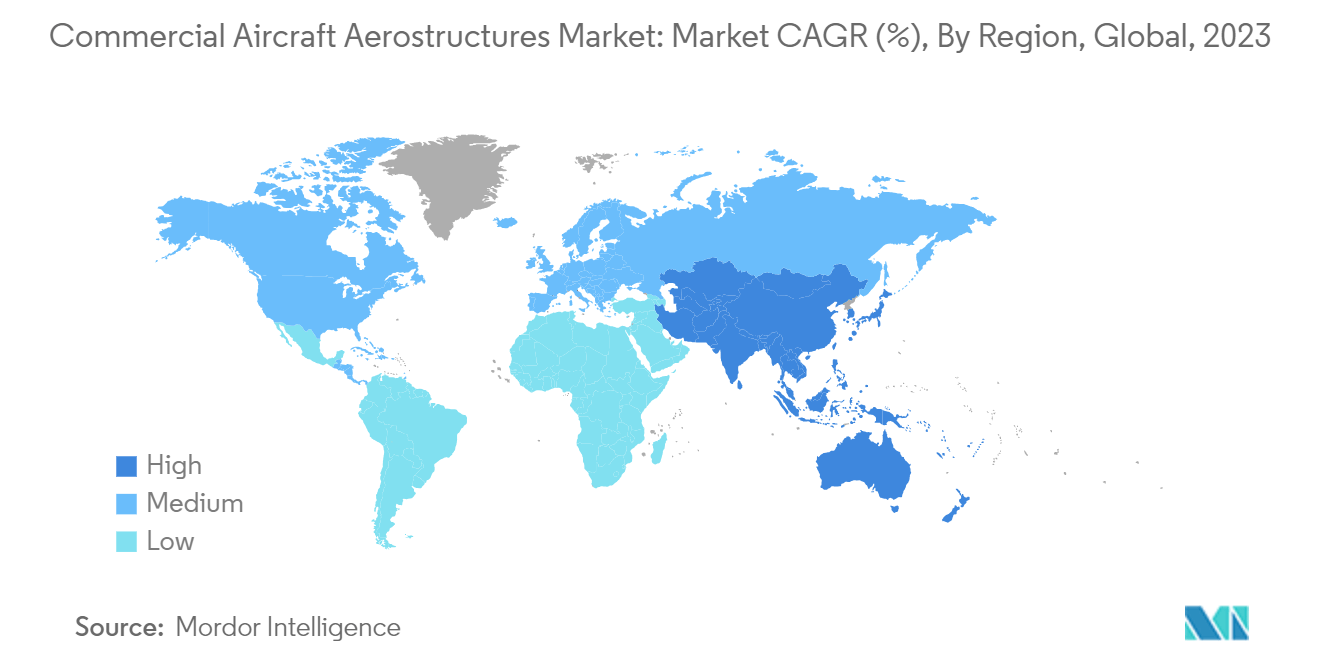

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

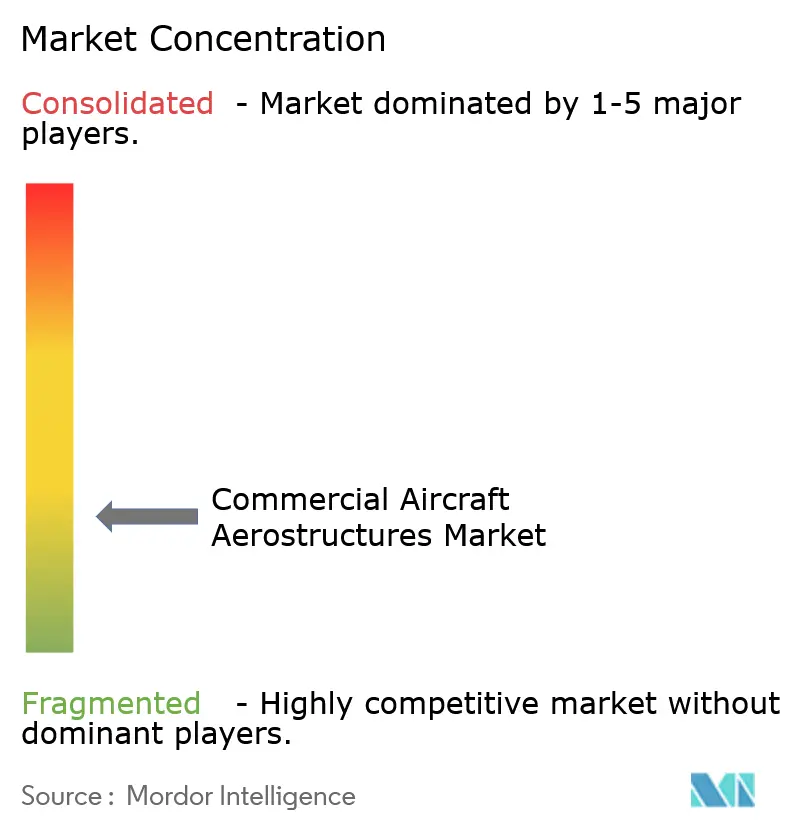

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Commercial Aircraft Aerostructures Market Analysis by Mordor Intelligence

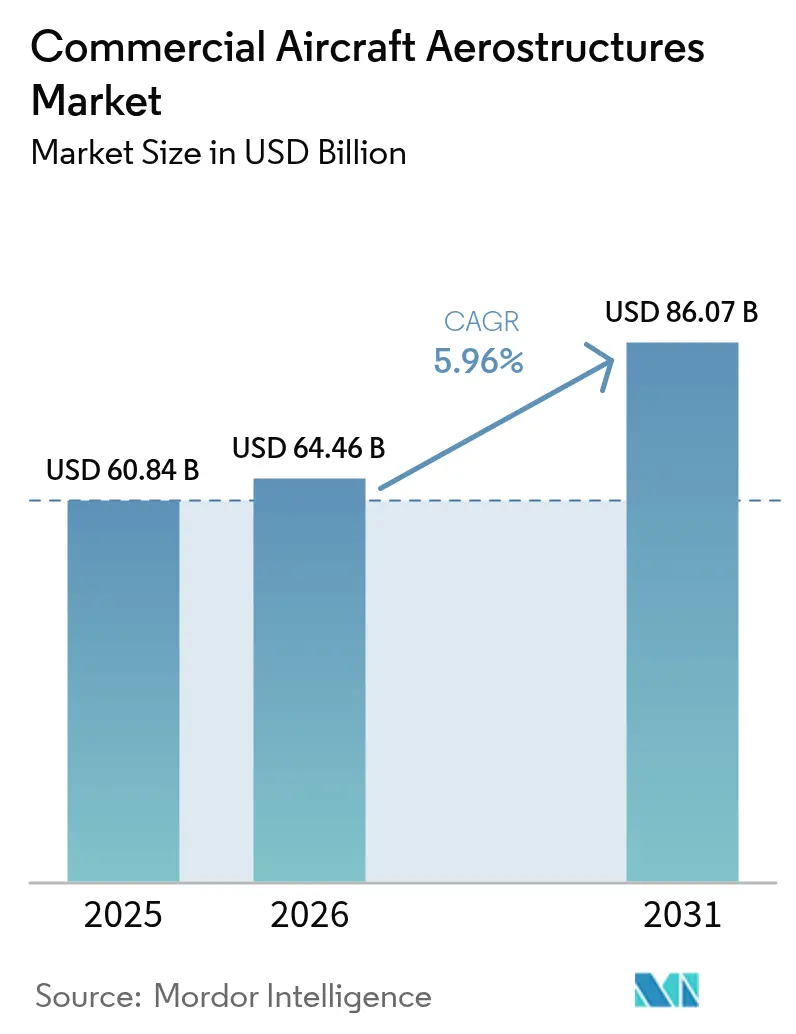

The Commercial Aircraft Aerostructures Market size market is expected to grow from USD 60.84 billion in 2025 to USD 64.46 billion in 2026 and is forecast to reach USD 86.07 billion by 2031 at 5.96% CAGR over 2026-2031.

The main driver for growth in the aircraft aerostructure market is increasing deliveries of commercial aircraft all over the world. The commercial aviation industry saw a significant increase in the number of new aircraft deployed. It is helping to support growth in the global aerostructure market as passengers have become more flexible over recent years. The use of composites and other advanced materials in aerostructures led to radical design changes in aircraft design. Their inherent high strength-to-weight ratio resulted in significant weight savings, thereby enhancing the fuel efficiency of the aircraft.

The market's growth is also due to an increase in tourism at the domestic and international levels, together with strict government rules on air safety.

However, the remuneration scope of the aeronautic sector is hindered by volatility in raw material prices. Technological innovations in the field, growing research & development investments in the aviation industry, and rising efforts of market players to develop advanced product ranges are adding traction to the industry expansion. Emerging technologies such as additive manufacturing and Automated Fiber Placement (AFP) techniques enhance the scope of integrating advanced materials into complex component designs while reducing the aircraft's turnaround time (TAT).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Commercial Aircraft Aerostructures Market Trends and Insights

OEMs Segment to Dominate Market Share During the Forecast Period

The significant increase in global passenger traffic drove airline operators to initiate procurement drives and place firm orders for new-generation aircraft. In 2022, Airbus delivered 676 commercial aircraft, while Boeing delivered 480. Aircraft OEMs are continuously honing their supply chain to reduce the backlog of orders and ensure on-time delivery to the airlines. Several new orders were placed during 2022, which encouraged associated aerostructure manufacturers and integrators alike to enhance their production capabilities. For instance, in June 2023, Indigo (India) ordered 500 Airbus A320neo family planes at the Paris Air Show.

Similarly, Air India (India) signed purchase agreements for 250 Airbus aircraft and 220 new Boeing jets worth USD 70 billion. Air India's orders include 70 widebody planes, comprising 34 A350-1000s and six A350-900s from Airbus, 20 B787 Dreamliners, and 10 B777Xs from Boeing. It also includes 140 Airbus A320neo, 70 Airbus A321neo, and 190 Boeing B737 MAX narrowbody aircraft. The airline also signed options to buy an additional 70 planes from Boeing, including 50 B737 MAXs and 20 B787 Dreamliners. Such procurement orders would drive the business prospects of the market players during the forecast period.

Asia-Pacific to Witness Highest Growth During the Forecast Period

The robust economic growth, coupled with favorable population and demographic profiles of the populace in developing countries, especially in the Asia-Pacific region, is driving the air passenger traffic in the region. It resulted in a steady increase in the demand for aircraft originating from Asia-Pacific. By 2025, China is forecasted to become the world's largest aviation market in terms of air traffic. India is forecasted to develop into the world's third-largest aviation market, while other countries, such as Indonesia and Thailand, are forecasted to enter the top 10 global markets.

The aviation manufacturing infrastructure is further supported by lower production costs, driving major aircraft OEMs to establish manufacturing hubs in the region. For instance, Airbus entrenched industrial partnerships with more than 600 firms in 15 countries in the region to ensure the supply of parts for Airbus aircraft. South Korea's KAL Aerospace and Korea Aerospace Industries (KAI) are key suppliers for Airbus and produce aerostructures, including parts of the A350 XWB fuselage, wing, cargo door, and landing gear, and the Sharklet wingtip device for the A320 and A330neo aircraft.

Moreover, in April 2023, Airbus is working to expand production of its best-selling A320 single-aisle jet and bolster sales in China. Airbus planned to build a second assembly line at its factory in China, and Beijing approved the old order for 160 aircraft.

Competitive Landscape

The commercial aircraft aerostructures market is fragmented and is witnessing the emergence of new market players that provide full lifecycle support, ranging from conceptual design, testing, and regulatory compliance certification. Since an aerostructure is required to withstand extreme operating conditions, the aerostructure materials are subjected to extensive testing to analyze and determine their performance parameters. Leading market players such as Elbit Systems Ltd., RUAG Group, Airbus SE, FACC AG, and Singapore Technologies Engineering Ltd. combine customer-specific design processes with their extensive metallic and composite structures knowledge, value engineering techniques, and design automation expertise to design cost-effective next-generation aerostructures.

Furthermore, the aerostructure designers are required to conduct manufacturing non-conformance, stress justifications, and design office dispositions after signatory approvals from concerned authorities. Such regulations may expose the market players to financial risks owing to the high R&D expenditure divested towards designing advanced materials for aerostructure construction. For instance, in April 2023, Leonardo S.p.A (Italy) entered into a partnership with Cisco Technology to develop joint technology projects. The partnership aims to develop joint products and solutions as a green transition to secure logistics and transportation solutions.

Similarly, in June 2021, Magellan Aerospace (UK) signed an agreement with Airbus to extend the contract to supply titanium and aluminum structural wing components. The components are supplied from Magellan's manufacturing units located throughout India and Europe.

Commercial Aircraft Aerostructures Industry Leaders

FACC AG

Elbit Systems Ltd.

RUAG Group

Airbus SE

Singapore Technologies Engineering Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

OEM production ramp initiatives and continued order backlogs keep demand centered on high-rate aerostructures output, but supply-chain constraints have created room for Tier-1 and materials suppliers to add qualified capacity and support more stable lead times. In 2026, Airbus expanded aerostructure-related capability across the Americas, including MX$646.7 million invested to grow its Queretaro, Mexico operations (supporting items such as aircraft doors) and the Kinston, North Carolina site, which operates as a composite Center of Excellence for A350 wing spars and fuselage panels after being integrated into the Airbus network in December 2025. Airbus and Boeing using Antonov An-124 charters in mid-2026 to move critical parts also points to logistics-driven bottlenecks that increase the value of regionalized production and resilient supplier footprints.

Process and material roadmaps are creating additional entry points in automated composites and next-generation bonding solutions aimed at higher build rates and repeatable quality. The Airbus-led HEMERA project (Nov 2025 to Jan 2029) focuses on validating high-rate manufacturing methods for thermoset CFRP fuselage panels, targeting production rates above 70 aircraft per month, which strengthens investment cases for automation, tooling, and inspection around large composite structures. Materials-side expansions reinforce this direction: Syensqo broke ground in July 2026 on an expansion in Havre de Grace, Maryland to add more than 30% capacity for structural adhesives and surfacing products, while SeAH Superalloy Technologies outlined a new Temple, Texas nickel-based superalloy facility with 6,000-ton annual capacity planned for the second half of 2026, supporting access to critical feedstocks used across major airframe programs.

Recent Industry Developments

- May 2026: FACC AG announced a EUR 350 million investment program through 2030, including a planned EUR 120 million high-tech plant in St. Martin im Innkreis, Austria, to expand aerostructures manufacturing capability. The program focuses on scaling industrial capacity and automation to support higher build rates across major aircraft platforms.

- April 2026: ST Engineering reported new contracts secured in 1Q 2026 totaling SGD 4.8 billion, including SGD 1.7 billion attributed to its commercial aerospace segment covering aerostructures and MRO activities. The commercial aerospace intake indicates continued demand for integrated build-and-support offerings as operators and lessors manage fleet availability and modification cycles.

- April 2024: Airbus formalized the launch of the HEMERA project, an Airbus-led initiative running from Nov 2025 to Jan 2029 to develop and validate high-rate manufacturing processes for CFRP fuselage panels. The program supports industrialization of large composite aerostructures, with emphasis on repeatable quality and cycle-time reduction for higher production rates.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of structural airframe parts and assemblies used in commercial aircraft, including major sections such as wings, fuselage structures, empennage, and nacelle related structures. Values are captured across OEM supply and replacement demand where applicable, and are expressed in nominal USD.

Scope exclusions: Military aircraft, space platforms, and non-structural onboard systems (such as avionics, propulsion hardware, and cabin electronics) are not counted in this sizing.

Segmentation Overview

- Material

- Alloys

- Composites

- Metals

- End-user

- OEMs

- Aftermarket

- Geography

- North America

- United States

- Canada

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle-East and Africa

- United Arab Emirates

- Saudi Arabia

- Turkey

- South Africa

- Rest of Middle-East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the boundaries and to build the starting data series that a sizing model needs. We relied on public aviation production and fleet indicators and official trade statistics, such as ICAO air transport indicators, IATA traffic releases, the US Bureau of Transportation Statistics for passenger and fleet context, and UN Comtrade for aircraft parts import-export patterns. Supporting context was also taken from airworthiness and program signals published by regulators such as the FAA and EASA, plus peer-reviewed aerospace manufacturing journals on materials adoption and processing trends.

On the supply side, we reviewed annual reports, investor presentations, and earnings transcripts to understand aerostructure revenue exposure, contract timing, and program mix. A paid subscription for aircraft and aerospace databases was used to cross-check aircraft deliveries, backlog direction, and platform-level production plans. These sources are not exhaustive, and other public documents and datasets were also used for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary interviews and structured surveys were used to test the desk assumptions and to close gaps around pricing movement, outsourcing intensity, and the split between new-build demand and replacement demand. We spoke with aerostructure manufacturers, material and process specialists, airline and MRO facing stakeholders, and program-level experts across APAC, EMEA, and the Americas, so regional build rates and cost dynamics were not averaged too early.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 19% | APAC: 42% |

| Mid tier: 40% | Functional/Unit leaders: 25% | EMEA: 37% |

| Smaller Players: 22% | Managers: 56% | Americas: 21% |

Market-Sizing & Forecasting

The core sizing starts from a top-down build that reconstructs aerostructure demand from commercial aircraft production and in-service activity. Aircraft delivery and build-rate trajectories were mapped by major commercial categories, and then translated into aerostructure value using structure content factors and program-level outsourcing assumptions. Where replacement demand drives the market, the in-service fleet and heavy-check cadence were used as practical anchors, so the model did not rely only on new aircraft output.

To keep the totals realistic, selective bottom-up approximations were used as checks, such as sampled supplier revenue exposure to commercial aerostructures, channel checks on contract coverage, and a limited ASP-times-volume approach on high value structures. Key inputs tracked (illustrative) include commercial aircraft deliveries and backlog direction, ramp-up timing by airframe programs, composite versus metallic structure share shifts, labor and raw-material cost pass-through expectations, and the share of work retained in-house by airframe OEMs versus outsourced tiers. Forecasting was completed using scenario analysis supported by a simple multivariate regression overlay, where the main drivers were traffic recovery, build rates, and pricing progression, followed by adjustments based on expert consensus. When a bottom-up check lacked visibility for smaller suppliers, we bridged the gap using observed concentration patterns and program mix, then ran a reasonableness check against aircraft-level demand signals.

Data Validation & Update Cycle

Validation was done through several practical checks so one dataset did not dominate the outcome. Model outputs were compared with independent signals like delivery totals, fleet in-service growth, and public guidance on production ramps, and then outliers were reviewed until the drivers were clear. Where interview feedback pointed to a mismatch, the input that caused it was revisited first, followed by a re-run of the scenario set before any final changes were accepted.

A multi-step internal review is completed before sign-off, and clarifying calls are triggered when a key assumption moves, such as a major program rate change or a material cost swing. Reports are refreshed annually, and interim updates are made when material events occur. Before delivery, an analyst performs a fresh pass on the most time sensitive indicators so clients receive the latest updated view.

Mordor Intelligence's Commercial Aircraft Aerostructures Market Sizing Compared With Other Published Estimates

Published market sizes for commercial aircraft aerostructures often do not match because each publisher makes slightly different choices on what counts as an aerostructure, how aftermarket value is treated, and which year and currency assumptions are locked in. Differences also show up when production ramps are smoothed differently across the forecast window.

The biggest gaps usually come from refresh cadence and pricing mechanics. Some estimates keep older exchange rates and do not re-normalize ASP progression when raw-material and labor pass-through changes, which can widen the value even if aircraft deliveries look similar. In our work, the model is re-checked against updated delivery and backlog signals and then re-stated with current USD timing and program-level ASP logic, a refresh step that explains part of the spread seen versus other numbers, including the figure reported by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 64.46 B (2026) | |

| Aerospace Intelligence Publisher A | USD 67.00 B (2024) | Uses a broader aerostructures framing and can mix civil and military activity and modifications, which shifts the demand pool away from commercial-only production and spares timing. |

| Global Research Outlet B | USD 85.47 B (2024) | Often applies wider component and application boundaries with more aggressive ASP escalation and less transparent linkage to aircraft build rates, which can inflate value even without matching delivery trajectories. |

When placed side by side, the spread is mainly explained by scope boundaries and how quickly assumptions are refreshed for currency timing and price movement. By keeping the demand build tied to commercial aircraft output and fleet-linked replacement signals, and then validating with supplier exposure checks, we end up with a number that is easier to trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

How big is the Commercial Aircraft Aerostructures Market?

The Commercial Aircraft Aerostructures Market size is expected to reach USD 64.46 billion in 2026 and grow at a CAGR of 5.96% to reach USD 86.07 billion by 2031.

What is the current Commercial Aircraft Aerostructures Market size?

In 2026, the Commercial Aircraft Aerostructures Market size is expected to reach USD 64.46 billion.

Who are the key players in Commercial Aircraft Aerostructures Market?

FACC AG, Elbit Systems Ltd., RUAG Group, Airbus SE and Singapore Technologies Engineering Ltd. are the major companies operating in the Commercial Aircraft Aerostructures Market.

Which is the fastest growing region in Commercial Aircraft Aerostructures Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Commercial Aircraft Aerostructures Market?

In 2025, the North America accounts for the largest market share in Commercial Aircraft Aerostructures Market.

What years does this Commercial Aircraft Aerostructures Market cover, and what was the market size in 2024?

In 2024, the Commercial Aircraft Aerostructures Market size was estimated at USD 57.17 billion. The report covers the Commercial Aircraft Aerostructures Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Commercial Aircraft Aerostructures Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: