Aircraft Fuel Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 11.09 Billion |

| Market Size (2031) | USD 13.81 Billion |

| Growth Rate (2026 - 2031) | 4.47% CAGR |

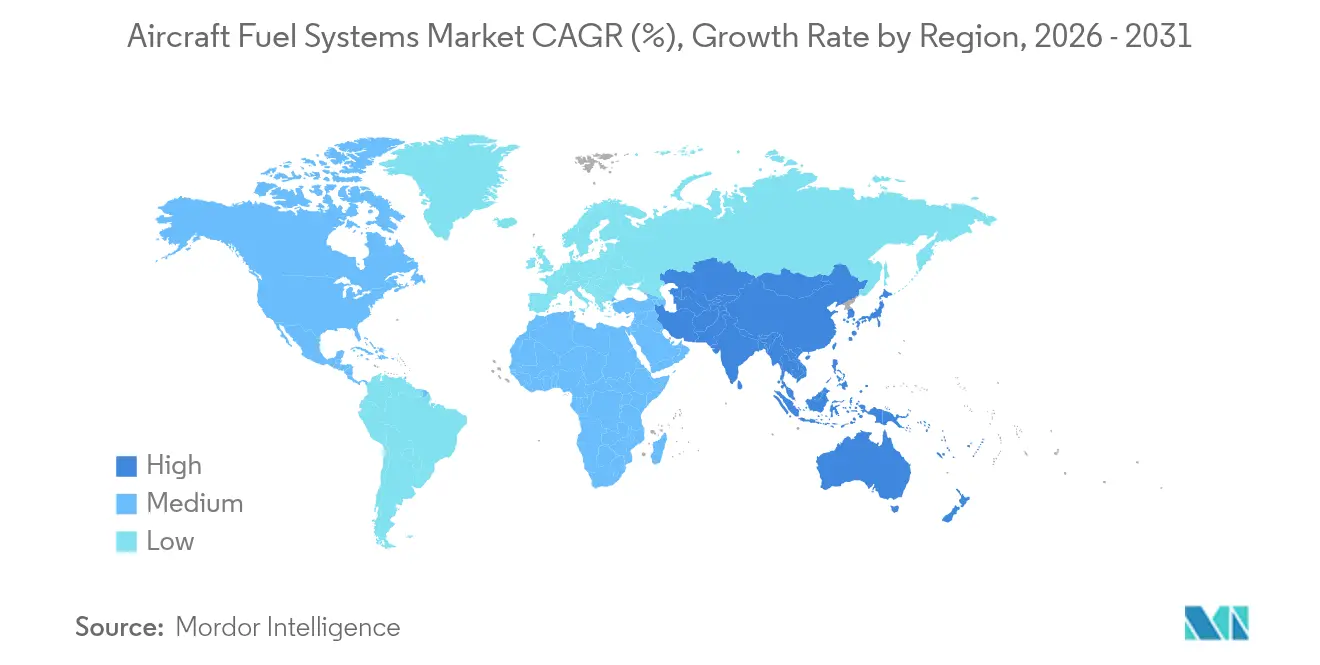

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Fuel Systems Market Analysis by Mordor Intelligence

The aircraft fuel systems market size is expected to grow from USD 10.62 billion in 2025 to USD 11.09 billion in 2026 and is forecast to reach USD 13.81 billion by 2031 at 4.47% CAGR over 2026-2031. Heightened aircraft production schedules, autonomy-driven refueling programs, and digital retrofits reinforce demand even as raw-material shortages challenge supply continuity. Airbus alone handed over 51 aircraft in May 2025, led by the A321neo and A321XLR, underscoring a rebound in single-aisle deliveries that depend on advanced fuel-saving architectures. Parallel momentum stems from a USD 898 million US Navy order covering three MQ-25 Stingray unmanned tankers, inauguring autonomous aerial refueling at sea. North American incumbents such as Parker Hannifin recorded 12% aerospace revenue growth to USD 1.6 billion in Q3 2025, signalling healthy aftermarket pull-through. Asia-Pacific provides the fastest regional lift, posting a 5.78% CAGR on the back of airport infrastructure expansion and rising defence budgets. Regulatory insistence on nitrogen-inerting and shifting toward sustainable aviation fuels (SAF) further stimulates technology upgrades, offsetting certification cost pressures and titanium supply disruptions that persist across civil and military value chains.

Key Report Takeaways

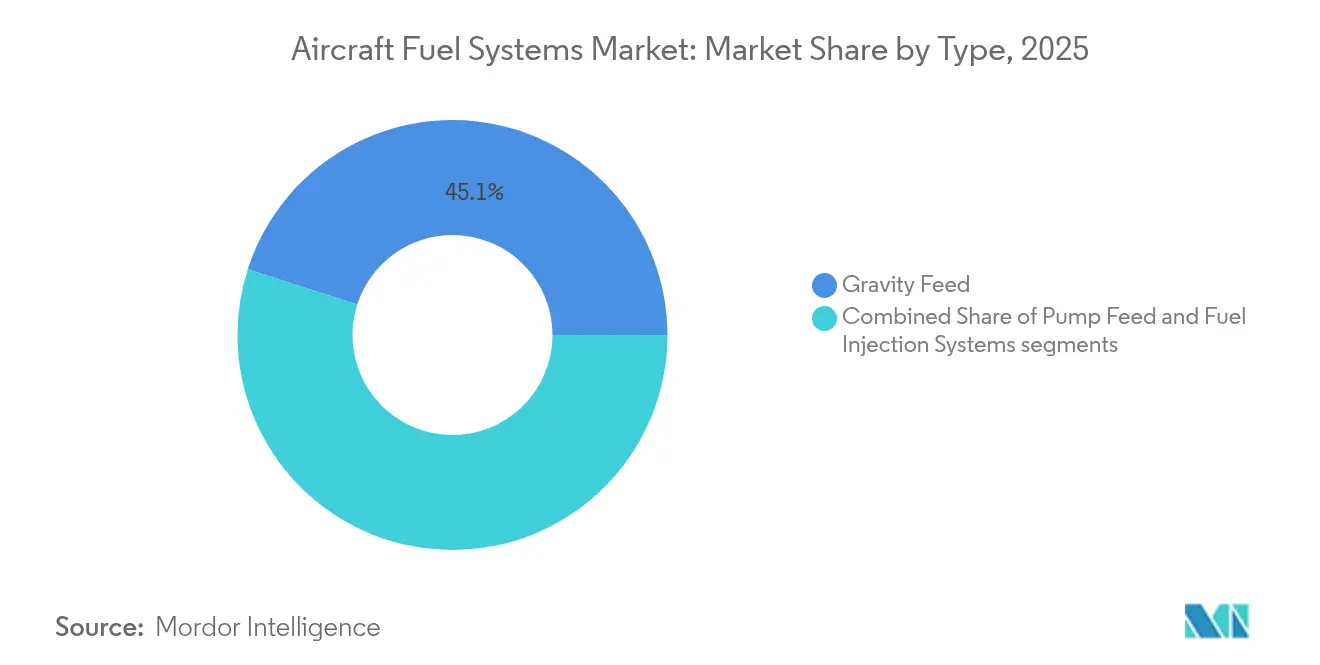

- By type, gravity feed accounted for 45.05% of the aircraft fuel systems market size in 2025, whereas the fuel injection systems segment is projected to climb at a 6.07% CAGR.

- By technology, conventional mechanical systems retained 39.45% of the aircraft fuel systems market share in 2025, while smart/connected systems are advancing at a 6.61% CAGR to 2031.

- By component, fuel tanks dominated, with a 36.15% share of the aircraft fuel systems market in 2025; inerting systems represent the fastest-growing component, with a 5.55% CAGR.

- By aircraft class, commercial aircraft controlled 59.62% revenue share in 2025; unmanned aerial vehicles are expanding at a 7.55% CAGR during 2026-2031.

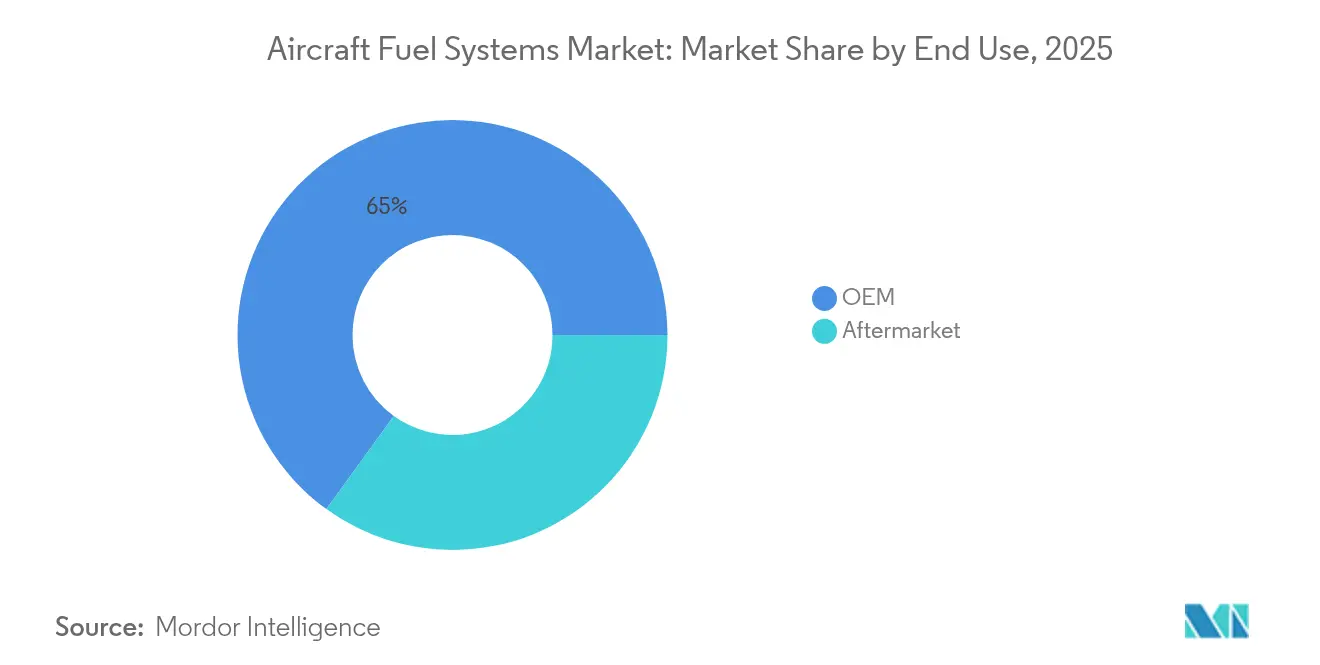

- By end use, OEM sales accounted for 65.02% of the aircraft fuel systems market size in 2025, whereas the aftermarket segment is projected to climb at a 6.28% CAGR.

- Regionally, North America held 41.98% of the aircraft fuel systems market share in 2025, yet Asia-Pacific is forecasted to post the highest 5.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aircraft Fuel Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging global commercial aircraft deliveries | +1.2% | Global (APAC and North America concentration) | Medium term (2-4 years) |

| Expansion of military aerial-refueling programs | +0.8% | North America, Europe, APAC defense corridors | Long term (≥ 4 years) |

| Rapid fleet modernization toward fuel-efficient platforms | +1.0% | Global, led by North America and Europe | Medium term (2-4 years) |

| Rising UAV procurement across civil and defense sectors | +0.6% | Global, early adoption in North America and Europe | Short term (≤ 2 years) |

| Predictive analytics integration for real-time fuel-system health | +0.4% | North America, Europe, advanced APAC markets | Short term (≤ 2 years) |

| Mandatory retrofit of nitrogen-inerting systems for safety | +0.3% | Global (FAA and EASA-driven) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Global Commercial Aircraft Deliveries

Airframers are elevating output to meet airline refurbishment cycles. Airbus aims for 820 deliveries in 2025 and prioritizes long-range single-aisle models that utilise multiple centre- and auxiliary-tank arrangements to achieve up to 4,700 NM range. Boeing’s concurrent production of F-15EX fighters sustains fuel pump and valve demand for combat platforms.[1]Boeing Company, “F-15EX Production Status,” boeing.com Component suppliers, therefore, face enlarged call-offs for precision pumps, probes, and transfer valves while MRO providers register faster consumable replacement cycles as utilization returns to pre-pandemic flight hours.

Expansion of Military Aerial-Refueling Programs

The MQ-25 Stingray marks the first carrier-based unmanned tanker capable of transferring 15,000 lb of fuel beyond 500 NM, pushing requirements for fault-tolerant flow metering and autonomous shut-off logic. The USAF’s KC-46A Pegasus expansion and allied European acquisitions reinforce multi-point refuelling demand, each necessitating high-capacity boost pumps and actively damped boom-actuation manifolds.

Rapid Fleet Modernization Toward Fuel-Efficient Platforms

Airlines are retiring older twin-aisles in favour of lighter airframes and blended-wing-body prototypes purporting 50% fuel savings, such as the JetZero demonstrator backed by Collins Aerospace and Pratt & Whitney. Innovative layouts require distributed tank clusters and smart balancing algorithms to safeguard the centre-of-gravity during cruise and descent.

Predictive Analytics Integration for Real-Time Fuel-System Health

Honeywell’s Connected Maintenance cuts up to 50% of unscheduled removals through sensor-driven algorithms that flag pump cavitation or valve stiction before line removal.[2]Honeywell Aerospace, “Connected Maintenance Performance,” honeywell.com GE Aerospace’s Maintenance Insight provides live dashboards that map fleet fuel burn and leakage trends, enabling operators to save 3-5% on fuel costs.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High certification and qualification costs for new fuel technologies | −0.7% | Global (highest in North America and Europe) | Medium term (2-4 years) |

| Aviation-grade titanium and elastomer supply bottlenecks | −0.9% | Global (acute in North America and Europe) | Short term (≤ 2 years) |

| Fuel-price volatility curbing airline capital expenditure | −0.5% | Global (regional variation with hedging) | Short term (≤ 2 years) |

| Cyber-security risks in digital gauging and control networks | −0.3% | North America, Europe, advanced APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Certification and Qualification Costs for New Fuel Technologies

Novel hydrogen or SAF-ready fuel systems routinely require multi-year test campaigns and FAA certification plans. The agency’s December 2024 Hydrogen Roadmap highlights data gaps that could cost manufacturers tens of millions in qualification expenditure. Small suppliers face disproportionate burdens that slow market entry and limit price competition.

Aviation-Grade Titanium and Elastomer Supply Bottlenecks

Document-fraud revelations involving titanium billets for large civil programs prompted heightened traceability audits, delaying raw-material deliveries and raising per-unit costs for pumps and manifolds that rely on Ti-6-4 forgings. Elastomer seals also remain capacity-constrained due to chem-spec qualification hurdles, extending lead times across the aircraft fuel systems market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Gravity Feed Dominance Faces Digital Disruption

Gravity-feed architectures retained 45.05% of the aircraft fuel systems market share in 2025, underscoring their cost-effective appeal for general aviation and selected military fleets. Within the same period, the aircraft fuel systems market size for fuel-injection platforms advanced at a 6.07% CAGR, the fastest among all types, as operators embraced FADEC-compatible hardware that can trim fuel burn by about 15% through real-time mixture optimization. Pump-feed solutions continued to serve the performance middle ground, supporting airframes that require positive pressure delivery without the full digital overlay.

Suppliers are embedding machine-learning logic into next-gen injectors to predict flow requirements and balance tanks autonomously, turning the fuel circuit into a sensor-rich data source. Safran’s FADEC 4 illustrates the leap, delivering 10 times greater processing power than earlier units while elevating overall efficiency. As IoT connectivity spreads across flight decks, traditional gravity systems face competitive pressure from injection assemblies that promise tighter consumption control, predictive health monitoring, and lower lifecycle cost, accelerating the technology shift within the broader aircraft fuel systems market.

By Component: Inserting Systems Lead Safety Evolution

Fuel tanks held the largest 36.15% revenue share in 2025. Nonetheless, inerting assemblies—spanning nitrogen generators, membranes, and distribution plumbing—advanced at a 5.55% CAGR on the back of mandatory retrofit programs. The aircraft fuel systems market size for inerting solutions stood near USD 1.86 billion in 2026 and is on track to exceed USD 2.48 billion by decade-end. Operators accept higher capital costs in exchange for flammability-exposure compliance and insurance benefits.

Variable-speed electric pumps and smart motor-operated valves augment safety by harmonising tank pressures during inert gas injection. Coupled with embedded oxygen sensors, these systems notify crews or maintenance teams when purity drifts outside thresholds, reinforcing the aircraft fuel systems market's emphasis on real-time data visibility.

By Aircraft Class: UAVs Reshape Market Dynamics

Commercial airliners contributed 59.62% of 2025 revenue, mirroring fleet size dominance. Yet UAV platforms, posting 7.55% CAGR, redefine requirements: autonomous endurance flights necessitate micro-mass flow controllers and scalable bladder tanks manufactured from carbon thermoplastics. The aircraft fuel systems market share of UAVs is projected to double by 2031 as defence ministries procure high-payload tankers and civil operators deploy large cargo drones.

Military jets similarly progress through spiral upgrades, incorporating crash-resistant conformal tanks that extend range without external pods. Rotorcraft programs follow suit, focusing on seal integrity and suction performance under negative-g events.

By End Use: Aftermarket Gains Momentum

Due to new build deliveries, OEM channels kept a 65.02% share in 2025. Yet the aftermarket tallies a faster 6.28% growth trajectory, fuelled by ageing narrow-body fleets and extended heavy-check intervals. Airlines embrace condition-based replacement, triggering component demand peaks outside traditional D-check cycles.

Global MRO providers invest in dedicated fuel accessory cells and contamination-test benches, capturing margin from proprietary overhaul kits supplied by original designers. As predictive maintenance penetrates, data subscription services form an ancillary revenue stream within the aircraft fuel systems market.

By Technology: Smart Systems Transform Operations

Smart or connected solutions, marrying IoT gateways with health-monitoring logic, already illustrate a 6.61% CAGR. Although conventional mechanical builds maintain a 39.45% revenue share, forward orders increasingly specify digital-ready options compatible with airline e-logbook platforms. On-wing software updates extend functionality without hardware swaps, highlighting recurring-license potential inside the aircraft fuel systems industry.

FADEC-integrated electric systems gain traction on next-generation turbofans, exploiting variable-frequency power networks to modulate pump speeds and lower parasitic draw.

Geography Analysis

Asia-Pacific’s aviation services outlay will rise from USD 52 billion in 2025 to USD 129 billion in 2043, implying compound 4.81% growth and a proportional uptick in fuel system spares. Maintenance spend alone accelerates at 5.0% yearly, creating space for predictive analytics licensors and specialty seal manufacturers. China’s civil expansion partners with indigenous wide-body programs, pushing the localization of titanium tank fittings. India’s SAF push underlines the need for dual-fuel-compatible seals by 2030, while Singapore’s early 1% SAF blending rule from 2026 makes it a live testbed for filter adaptability.

North America’s 41.98% market share derives from entrenched OEM and MRO ecosystems across Kansas, Washington, and Georgia. The USAF continues to order the F-15EX and KC-46A, locking in steady valve, pump, and hose procurements through 2030. FAA flammability mandates further generate retrofit workscopes for nitrogen generation and monitoring lines.

Europe maintains primacy in environmental regulation. The ReFuelEU Aviation Act begins with 2% SAF by 2025 and scales to 70% by 2050, compelling filter-housing redesigns for bio-derived fuels with higher solvency. Airbus’ partnership with TotalEnergies targets 1.5 million t annual SAF output by 2030, underpinning nozzle, gasket, and seal demand that can withstand novel fuel chemistries.

Regulatory Landscape

Aircraft fuel-system design and retrofit activity is anchored in fuel-tank safety and pressure-fueling requirements under FAA rules, including 14 CFR 25.981 (fuel tank ignition prevention) and 14 CFR 25.979 (pressure fueling systems). In January 2026, the FAA advanced continued oversight of fuel-tank flammability reduction means through a Federal Register notice on renewing an information-collection program, keeping design approval holders focused on ongoing reliability documentation and compliance reporting tied to in-service performance.

In Europe, EASA continues tightening safety and retrofit expectations through certification specifications and rulemaking materials for fuel-tank safety. EASA CS-26 Issue 5 (effective 22 December 2024) reinforces crash-resistant fuel system requirements for rotorcraft. Separately, US trade-policy actions added a near-term compliance and sourcing variable for imported aerospace parts: a White House Section 232 proclamation dated July 9, 2026 directed negotiations covering commercial aircraft, jet engines, and parts within a 180-day window, creating a planning horizon where suppliers reassess import exposure even without immediate new tariffs.

Value Chain Analysis

The value chain runs from raw materials and specialty processes (aerospace-grade alloys, elastomers, precision castings and forgings) to subcomponent manufacturing (pumps, valves and manifolds, gauges and sensors, filters, inerting modules). It then moves through system integration with engines and airframes, followed by distribution into OEM installation channels and global MRO.

Tier suppliers such as Parker Hannifin, Eaton, Safran, Woodward, and Honeywell typically deliver certified assemblies with traceability, testing, and documentation that align to fuel-tank safety requirements, while airframers and engine OEMs set configuration control and qualification plans. Supply continuity and repair throughput also drive downstream availability: in July 2024, RTX (Pratt & Whitney) highlighted structural casting shortages that constrained production ramp-up, and this constraint propagated into accessory and fuel-system build schedules through shared foundry and machining capacity. At the operator end, IATA estimated airline costs from aerospace supply-chain bottlenecks exceeded USD 11 billion in 2025, reflecting delivery delays, surplus inventory holding, and higher operating costs from keeping older aircraft in service, which lifts demand for overhaul capability, spares staging, and certified replacement parts across the fuel-system aftermarket.

Competitive Landscape

The aircraft fuel systems market features a moderately concentrated profile where the top five suppliers account for roughly 55-60% of revenue. Parker Hannifin’s aerospace bookings reached USD 7.3 billion by Q3 2025, buoyed by Airbus single-aisle demand and F-35 spares. Safran recorded EUR 7.26 billion (USD 8.51 billion) Q1 2025 revenue, with a 25.1% jump in civil-engine spare-parts turnover that confirms aftermarket resilience.

Strategic realignment continues: Woodward agreed to acquire Safran’s electromechanical actuation unit, broadening its fuel-control heritage just as the GE Aviation-Woodward joint venture scales integrated fuel systems for wide-body engines. Honeywell leverages Connected Maintenance to reduce unscheduled events by 30-50%, translating digital leadership into long-term service agreements.

Emerging opportunities cluster around hydrogen storage, autonomous UAV refuelling, and high-blend SAF lines where incumbent IP positions are less fortified. GKN Aerospace’s participation in the ICEFlight cryogenic hydrogen project signals early moves toward fuel-cell architectures that could reshape competitive hierarchies.[5]GKN Aerospace, “ICEFlight Hydrogen Collaboration,” gknaerospace.com

Aircraft Fuel Systems Industry Leaders

Eaton Corporation plc

Parker-Hannifin Corporation

Safran SA

Woodward, Inc.

Crane Aerospace & Electronics (Crane Company)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The clearest whitespace is readiness and sustainment for aerial-refueling fleets, alongside expanding repair and logistics capability for fuel accessories, where faster turnaround and certified repair content support recurring demand. In June 2026, the US Air Force awarded USD 471 million across 28 companies (including Honeywell, Collins Aerospace, Crane Aerospace and Electronics, and Eaton) to improve KC-46 Pegasus readiness through component repair and logistics. This reinforces the opportunity for repairable fuel-system content and supply-chain services around a high-utilization tanker platform.

Technology-driven opportunity centers on smart sensing, fuel compatibility, and next-energy carrier architectures. Suppliers are pushing sensor-rich monitoring approaches, including MEMS and optical concepts for fuel-system health monitoring that target HIRF resilience and fit within composite structures, aligning with the broader shift toward smart/connected fuel systems. Policy-driven fuel transitions also create engineering work for seals, hoses, filters, and gauging calibration that can tolerate higher SAF blends, including the EU ReFuelEU Aviation mandate beginning with 2% SAF in 2025. Longer-horizon R&D programs around cryogenic liquid hydrogen and methane-based concepts, including NASA-led ecosystem studies, expand the design space for thermal management, boil-off mitigation, and new distribution architectures.

Recent Industry Developments

- July 2026: The White House issued a Section 232 proclamation covering commercial aircraft, jet engines, and related parts, directing the Secretary of Commerce and USTR to pursue agreements with foreign trading partners within 180 days. The action did not impose immediate new tariffs, but it formalized a negotiation window that can influence sourcing strategy and inventory positioning for US-bound fuel-system components and materials.

- September 2025: Eaton was selected by Bell Textron to design, develop, and certify an aerial refueling retractable probe for the US Army MV-75 Future Long Range Assault Aircraft (FLRAA). The win expands Eaton's content on a next-generation military platform where refueling hardware, valves, and control integration are program-critical and carry long production tails.

- April 2024: Parker Aerospace joined the HyFIVE consortium backed by the Aerospace Technology Institute (ATI) to advance liquid hydrogen fuel system development and supply-chain readiness for zero-emission aviation. Participation aligns Parker with early-stage cryogenic fuel handling and distribution requirements that reshape pumps, valves, sensing, and materials choices versus conventional Jet-A fuel systems.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the equipment and assemblies used on aircraft to store aviation fuel, measure it, and safely move it from tanks to engines and the auxiliary power unit during operation, including control and conditioning elements.

Scope exclusions: ground refueling and fueling infrastructure (such as airport refuel trucks, hydrant networks, and fuel storage depots) are not counted.

Segmentation Overview

- By Type

- Gravity Feed

- Pump Feed

- Fuel Injection Systems

- By Component

- Fuel Tanks

- Fuel Pumps

- Valves and Manifolds

- Gauges and Sensors

- Inerting Systems

- Fuel Filters

- By Aircraft Class

- Commercial Aircraft

- Narrowbody Aircraft

- Widebody Aircraft

- Regional Aircraft

- Military Aircraft

- Combat Aircraft

- Non-Combat Aircraft

- Helicopters

- General Aviation Aircraft

- Business Jets

- Turboprop Aircraft

- Piston Aircraft

- Helicopters

- Unmanned Aerial Vehicles (UAVs)

- Commercial Aircraft

- By End Use

- OEM

- Aftermarket

- By Technology

- Conventional Mechanical Systems

- FADEC-Integrated Electric Systems

- Inerting-Enabled Systems

- Smart/Connected Fuel Systems

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- Egypt

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundary and to anchor the model to real aircraft activity signals. We relied on public aviation and trade statistics such as ICAO air transport data, IATA passenger and cargo updates, FAA and EASA airworthiness and safety publications, and civil aircraft registry and fleet data released by national regulators.

To keep assumptions realistic, we also reviewed sources such as SEC filings and investor presentations from listed suppliers, aerospace association releases, and reputable press coverage of aircraft deliveries, retrofit programs, and production rate changes. Where needed, our analysts used paid subscriptions for company financials and news, and also for patent databases and global tenders to understand technology direction and long-cycle contracts. These examples are illustrative only, and many other sources were also checked to collect, validate, and clarify data points.

Primary Interviews and Surveys

Primary work focused on cross-checking how demand is formed across new aircraft builds and the replacement cycle, and then stress-testing pricing and content assumptions at the subsystem level. We spoke with a mix of airframe and subsystem stakeholders, maintenance and repair participants, and industry specialists across APAC, EMEA, and the Americas, so gaps from desk inputs could be closed and key parameters could be confirmed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 14% | APAC: 41% |

| Mid tier: 55% | Functional/Unit leaders: 27% | EMEA: 34% |

| Smaller Players: 17% | Managers: 59% | Americas: 25% |

Market-Sizing & Forecasting

For the core sizing, a top-down and bottom-up model pairing was used, where aircraft production, deliveries, and active fleet levels by aircraft type are translated into fuel system demand using typical content per aircraft and replacement intensity over maintenance cycles. Once the demand pool was formed, it was converted to revenue using system-level and key component-level pricing ranges, which were then normalized to a single currency and year.

To make sure the totals are not drifting, we also corroborated outputs using selective bottom-up approximations such as sampled supplier revenue exposure to fuel systems, channel checks on spares volumes, and a few ASP times unit build-ups for high-value modules. Inputs that mattered most in this market included annual aircraft deliveries and production rate changes, in-service fleet size and utilization, typical fuel system architecture shifts (including inerting and electronic control content), overhaul intervals that influence replacement demand, and inflation and material cost pass-through that affects ASP progression.

Forecasting relied mainly on scenario analysis, because aircraft build rates and aftermarket timing can change quickly after events such as order deferrals, certification actions, or defense procurement swings. We kept the forward view consistent by tying each scenario to expected delivery ramps, fleet growth, and maintenance activity discussed by experts, and then applying moderated price progression to avoid over-stating revenue uplift when volumes are soft. Where bottom-up signals were incomplete for smaller platforms, gaps were handled through proxy ratios based on comparable aircraft classes and then rechecked during interviews.

Data Validation & Update Cycle

Checks were applied at several levels so outputs stay explainable and stable. Our team compared results against independent aviation signals like delivery counts, fleet utilization direction, and aftermarket activity cues, and then looked for unusual jumps by region or aircraft class that could be caused by a wrong assumption or a timing mismatch.

When variances appeared, sources were revisited and experts were re-contacted to confirm whether the change was real or model-driven. Before sign-off, another analyst reviewed key inputs, conversions, and growth logic so math and scope are consistent across the full time series. Reports are refreshed annually, and interim updates are made when material events occur, followed by a final pre-delivery review so clients receive the latest view.

Mordor Intelligence's Aircraft Fuel Systems Market Sizing Compared With Other Published Estimates

Published market sizes for aircraft fuel systems do not always line up because each publisher makes its own choices on what is included, how pricing is treated, and which year is used as the anchor for forecasts. Differences also come from how new-build demand is blended with spares and replacements, which can shift totals even when the same aircraft activity trend is referenced.

The table points to a spread that is mostly explained by scope and rate assumptions. Some estimates appear to apply faster ASP escalation across the full system, or to include adjacent fuel-related equipment that sits outside onboard fuel management, while others may lean on more aggressive production ramp scenarios without enough checks against fleet and maintenance signals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 10.62 B (2025) | |

| Global Consultancy A | USD 9.53 B (2024) | Uses a different base year and may classify a broader set of aircraft hardware as part of fuel systems, which changes the starting value before growth is applied. |

| Industry Portal B | USD 10.31 B (2025) | Shows a higher long-range total, which can result from assuming faster delivery ramps and stronger price progression, and it is less clear how new-build demand is separated from replacement cycles. |

The table shows that even close 2025 starting points can lead to very different long-term totals. Under Mordor Intelligence's scope, revenue is counted only for onboard fuel storage, transfer, metering, indication, and control content, while ground refueling infrastructure is excluded. With this structure, the sizing stays traceable to aircraft deliveries, fleet utilization, and maintenance-driven replacement timing, and the same steps can be rerun when those inputs change.

Key Questions Answered in the Report

What is the growth outlook for the aircraft fuel systems market by 2031?

The aircraft fuel systems market is projected to rise from USD 11.09 billion in 2026 to USD 13.81 billion in 2031, reflecting a 4.47% CAGR over 2026-2031.

Which region is expanding the fastest?

Asia-Pacific is forecasted to post a 5.55% CAGR, driven by large commercial fleet additions and growing defence budgets.

How significant is the aftermarket compared with OEM deliveries?

OEM sales still lead with 65.02% revenue share in 2025, yet the aftermarket is growing faster at 6.28% CAGR thanks to predictive maintenance and life-extension programs.

What technology segment shows the highest growth?

Smart/connected fuel systems lead with a 6.61% CAGR as airlines adopt data-rich solutions for predictive health monitoring.

Why are nitrogen-inerting systems gaining traction?

FAA flammability rules require operators to limit tank exposure, prompting a retrofit wave that positions inerting assemblies as the fastest-growing component category at 5.55% CAGR.

How will UAV adoption influence future demand?

UAV fuel systems exhibit a 7.55% CAGR because autonomy and long-endurance missions demand lightweight, highly automated tanks and flow-control hardware.

Page last updated on: