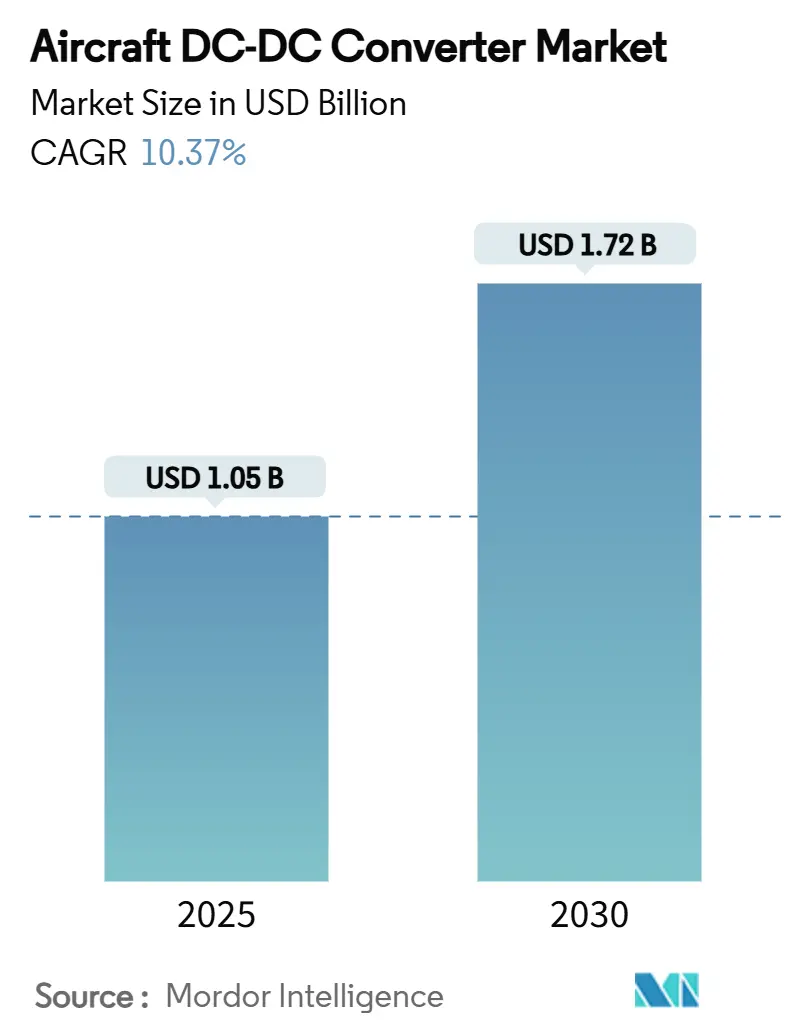

Aircraft DC-DC Converter Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 1.05 Billion |

| Market Size (2030) | USD 1.72 Billion |

| Growth Rate (2025 - 2030) | 10.37% CAGR |

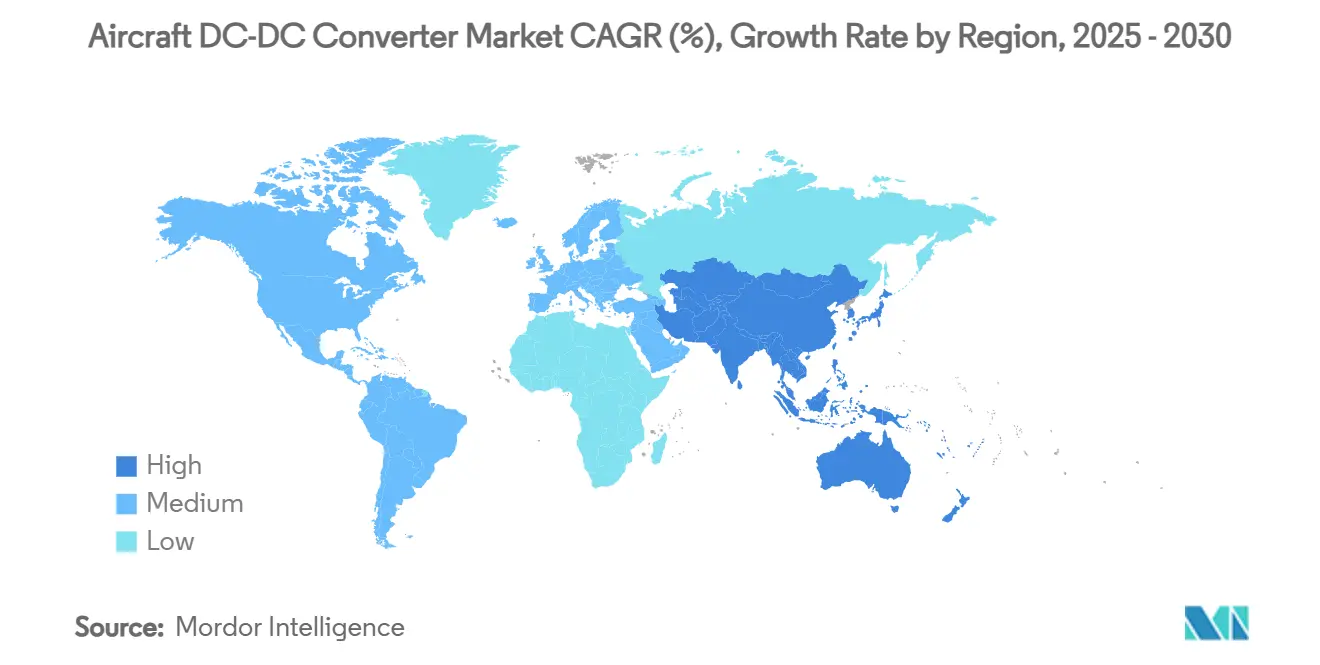

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft DC-DC Converter Market Analysis by Mordor Intelligence

The aircraft DC-DC converter market size stands at USD 1.05 billion in 2025 and is projected to reach USD 1.72 billion by 2030, translating into a 10.37% CAGR over the forecast period. Strong demand stems from the aviation sector’s shift to more-electric architectures, wide-bandgap (SiC/GaN) semiconductor adoption, and surging production of next-generation commercial and military platforms. Power-dense converters are becoming central to cabin systems, flight controls, and emerging hybrid-electric propulsion, while urban-air-mobility programs create new volume opportunities. Incumbent Tier-1 suppliers leverage deep certification know-how to protect installed bases, yet modular converter specialists capture share with lighter, easily serviceable units. On the regulatory front, net-zero mandates accelerate electrification, but DO-160 / CS-ETSO compliance and fragile semiconductor supply chains temper the growth pace.

Key Report Takeaways

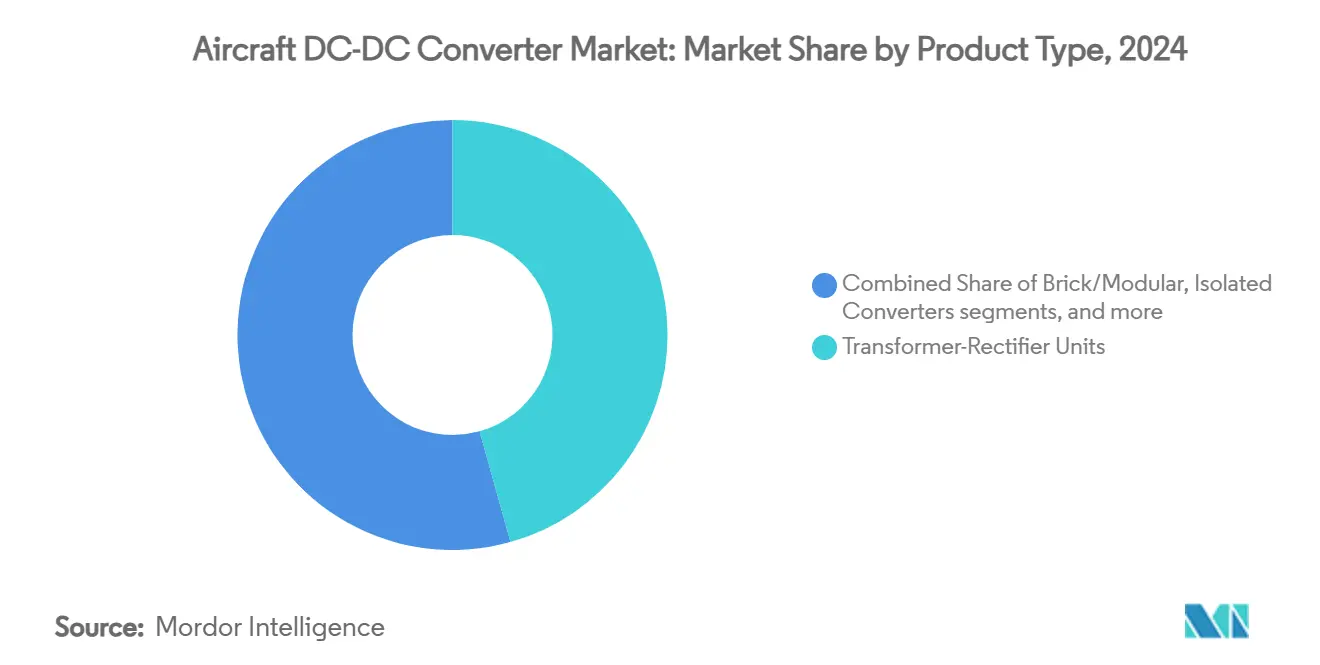

- By product type, transformer-rectifier units held 45.65% revenue share in 2024; modular/brick converters are forecasted to expand at a 12.45% CAGR through 2030.

- By output power, the 250 W to 1 kW segment commanded 37.24% of the aircraft DC-DC converter market size in 2024, whereas units above 5 kW are projected to grow at a 11.65% CAGR.

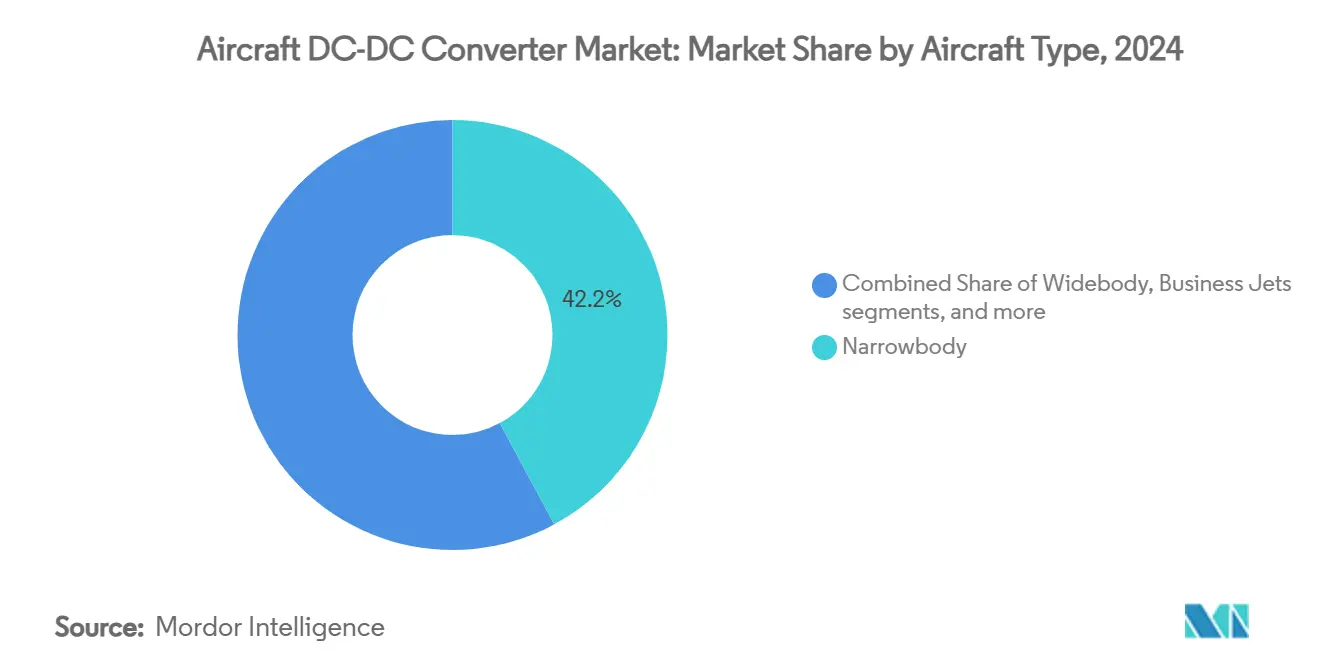

- By aircraft type, narrowbody aircraft led with 42.15% aircraft DC-DC converter market share in 2024, while UAV platforms are advancing at a 15.32% CAGR to 2030.

- By platform, commercial aviation dominated with a 56.24% share of the aircraft DC-DC Converter market size in 2024; eVTOL applications record the highest projected CAGR at 15.35% through 2030.

- North America accounted for 36.44% of revenue in 2024; Asia-Pacific is the fastest-growing region, with a 10.47% CAGR.

Global Aircraft DC-DC Converter Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrification shift toward more-electric and all-electric aircraft | +2.8% | North America and Europe | Medium term (2-4 years) |

| Soaring production of narrowbody/widebody jets and freighters | +2.1% | Global | Short term (≤ 2 years) |

| Rapid eVTOL and UAV prototyping demanding high-density converters | +1.9% | North America and Europe | Long term (≥ 4 years) |

| SiC/GaN devices enabling greater than 98 % efficiency and 540 V DC buses | +1.7% | Global | Medium term (2-4 years) |

| Airline drive for weight, fuel-burn and maintenance cost reduction | +1.5% | Global, with strongest impact in North America and Europe | Short term (≤ 2 years) |

| Open-systems architectures in defense (MOSA) standardizing modules | +1.2% | North America and Europe, expanding to allied nations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Electrification shift toward More-Electric and All-Electric Aircraft

Airframers are redesigning power architectures so that hydraulics and pneumatics give way to electrically driven subsystems, cutting fluid-borne maintenance tasks and emissions in a single step. On B787s, the bleed-less architecture lowers fuel burn because engines no longer extract compressed air for cabin pressurization or anti-ice functions. The Airbus–MTU fuel-cell program highlights how propulsion moves to high-voltage DC distribution.[1]Airbus, “Airbus and MTU Advance Hydrogen Fuel Cell Technology,” airbus.com Converter makers, therefore, confront new reliability tests covering 540 V buses, common-mode noise, and bidirectional energy flow between batteries, turbogenerators, and fuel cells. Tier-1s have responded by ring-fencing budgets—Collins alone moved USD 3 billion into electrified-systems R&D, signaling long-term commitment to the technology pivot

Soaring Production of Narrowbody/Widebody Jets and Freighters

Boeing projects 43,975 deliveries through 2043, the bulk being single-aisle aircraft that standardize on modular 28 V and 540 V rails, multiplying converter demand across avionics, galleys, and actuators.[2]Boeing, “Boeing Forecasts Demand for Nearly 44,000 New Airplanes Through 2043,” boeing.com Airbus, COMAC, and Embraer maintain similar ramp-up schedules, requiring suppliers to double surface-mount capacity to stay even. Widebody jets layer on additional converter sockets because high-power cabin systems migrate to electric loads. Freighter conversions also retrofit legacy airframes, opening aftermarket volume for drop-in bricks. According to McKinsey, accelerated build rates have already pushed aerospace procurement into “code red,” as OEMs scramble for electronic parts, test slots, and qualified labor.

Rapid eVTOL and UAV Prototyping

Over 60 OEMs seek certification for piloted eVTOL designs, each requiring converters with power densities above 19 kW/kg and 10-9 reliability targets.[3]eVTOL News, “AAM Progress and Challenges,” evtol.news Honeywell’s USD 1 billion agreement with Vertical Aerospace exemplifies how legacy avionics players partner with startups to integrate flight-critical power systems. Military HALE UAVs similarly boost demand for tablet-sized Vicor DCM converters that deliver 96% efficiency while doubling on-board bus power. As authorities target the UAE passenger service by 2026 and FAA approval by 2027, production orders should follow prototypes. Honeywell’s USD 1 billion partnership with Vertical Aerospace shows how incumbent avionics vendors seize propulsion-power opportunities while startups supply battery packs and flight software. Military HALE drones add complementary volume: Vicor’s tablet-sized 11 kW DC-DC module delivers 96% efficiency and doubles internal bus power without payload penalties. Prototyping cycles run 9-12 months, so converter suppliers that can iterate firmware and mechanical footprints quickly lock in final-design sockets. Successful programs then translate prototypes into fleet orders, lifting cumulative converter shipments through the 2030s.

SiC/GaN Devices Enabling Greater than 98% Efficiency and 540 V DC Buses

Wide-bandgap switches slash switching losses 70% versus silicon, so converters reach 99% peak efficiency and shrink passives for double-digit weight savings. Automotive EV demand has driven wafer output sharply higher, lowering SiC unit cost and creating supply economies that aerospace can tap within five years. Higher switching frequencies allow 540 V architectures, which use thinner copper and lighten wiring harnesses by up to 30 kg on a single-aisle jet. Designers also gain thermal headroom because cooler devices tolerate higher altitude ambient temperatures. Companies that master SiC qualification and cosmic-ray reliability screening secure first-mover advantage in flight-critical applications.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent DO-160/CS-ETSO certification timelines | −1.4% | Global | Medium term (2-4 years) |

| Supply-chain fragility for wide-bandgap semiconductors | −1.1% | North America and Europe | Short term (≤ 2 years) |

| Thermal-management challenges at high altitude and vibration loads | -0.9% | Global, with emphasis on military and high-performance applications | Medium term (2-4 years) |

| High upfront cost vs. legacy linear supplies | -0.8% | Global, with stronger impact in cost-sensitive markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent DO-160 / CS-ETSO Certification Timelines

RTCA DO-160 testing covers 23 environmental conditions, including lightning strikes and high-intensity radiated fields, extending new converter programs by up to 24 months. Boeing 777-9 special conditions require continued avionics operation after primary-power loss, forcing redundant converter channels and heavier wiring. eVTOL projects face bespoke powered-lift rules that regulators are still drafting, creating moving-target requirements and re-test costs. Certification labs have limited chamber capacity, so queue times lengthen during commercial-aircraft ramp-ups. These hurdles raise engineering budgets and favor incumbents with in-house test facilities, slowing smaller entrants’ market entry.

Supply-Chain Fragility for Wide-Bandgap Semiconductors

China controls 98% of gallium, making GaN wafers vulnerable to export curbs that could ripple through global aerospace lines within weeks. Five firms hold most SiC wafer capacity, and an unplanned outage at one fab in 2024 pushed lead times past 60 weeks for select die sizes. Automotive OEMs often outbid aerospace buyers, concentrating risk during demand spikes. The US Defense Production Act now funds domestic GaN tooling, but commercial output will lag until 2027. To hedge, aerospace primes carry months of inventory, tying up working capital and raising finished-goods prices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: TRU Dominance Faces Modular Disruption

Transformer-rectifier units amassed 45.65% revenue in 2024, thanks to decades of reliability in converting 115 V AC generator output to 28 V DC for avionics. Modular/brick converters exhibit a 12.45% CAGR as airlines favor lighter line-replaceable units that simplify maintenance. Astronics’ solid-state CorePower suite removes bulky transformers, trimming wiring weight and improving fault isolation. Retrofit programs present another opportunity as legacy fleets swap aging TRUs for drop-in high-efficiency bricks, boosting the aircraft DC-DC converter market.

Fleet operators also trial non-isolated bricks on 540 V buses, while isolated topologies stay essential for galvanic separation in flight-safety circuits. MOSA guidelines in defense programs amplify demand for interoperable modules across airframes, encouraging suppliers to standardize footprints and digital-control interfaces. With eVTOL prototypes prioritizing grams saved, modular bricks should keep eroding TRU share and broaden the aircraft DC-DC converter market footprint.

By Output Power: Mid-Range Leadership Amid High-Power Growth

Converters rated 250 W to 1 kW delivered 37.24% revenue in 2024 as they power core avionics, cabin lighting, and data systems. Growth tilts to greater than 5 kW units at an 11.65% CAGR because electrified propulsion, galley induction cookers, and directed-energy payloads require megawatt-class distribution. Honeywell’s 250 kW generator program highlights how future aircraft will embed high-density power modules yet retain compact envelopes.[4]Honeywell, “250 kW Generator,” honeywell.com

The less than 250 W band supplies UAV payloads and seat-back electronics, where efficiency extends endurance or reduces battery mass. 1 to 5 kW converters remain relevant for bleed-less environmental-control packs and flight-control actuators. Suppliers that span the range with scalable digital controllers are well-positioned as fleet electrification deepens, underpinning steady expansion of the aircraft DC-DC converter market.

By Aircraft Type: Narrowbody Strength Versus UAV Innovation

Narrowbody jets accounted for 42.15% revenue in 2024, leveraging rapid A320neo and B737 MAX production. Standardized electrical architectures simplify converter sourcing and create predictable demand streams. Widebodies require triple-redundant power channels for mission-critical loads, lifting per-aircraft content. Business jets seek whisper-quiet cabin systems, prompting a premium on low-EMI converters.

UAV demand, growing at 15.32% CAGR, stems from HALE and Group 3 tactical drones, where Vicor’s tablet-sized 11 kW supply showcases high-power density. Rotorcraft and regional jets round out demand with vibration-tolerant designs. This diversity sustains volume and buffers the aircraft DC-DC converter industry against commercial-cycle swings.

By Platform: Commercial Aviation Versus eVTOL Emergence

Commercial aviation dominated 56.24% of 2024 revenue as airlines retrofit cabins and ramp new-build deliveries. Mature certification pathways and large installed fleets create stable sales for line-fit and aftermarket converters. Military programs contribute premium margins because units must survive −55 °C start-ups, 70,000 ft pressure cycles, and combat-grade EMI.

Urban-air-mobility converters, projected at 15.35% CAGR, demand unmatched power-to-weight ratios for multirotor propulsion. Honeywell’s VX4 supply agreement illustrates how avionics majors secure early design wins in this nascent arena. A successful type of certification will cement recurring spares revenue and increase the aircraft DC-DC converter market size over the long term.

Geography Analysis

North America generated 36.44% of 2024 revenue, supported by Boeing, Lockheed Martin, and a mature MRO ecosystem. The F-35 Enhanced Power and Cooling System doubles onboard electrical capacity, raising converter content per aircraft. US CHIPS Act investments in SiC foundries aim to mitigate Asia dependency. Mexico’s cost-competitive parts machining and Canada’s avionics clusters reinforce regional supply resilience.

Asia-Pacific is the fastest-growing territory at 10.47% CAGR. COMAC’s C919 and Airbus’ Tianjin line drive local sourcing and invite South Korean and Indian suppliers to step in. India’s 100% FDI policy underpins new converter facilities near Bengaluru, aligned with “China+1” risk-diversification strategies. Japan’s semiconductor renaissance and Korea–US tech alliance strengthen regional SiC wafer availability.

Europe retains heft through Airbus and a stringent green aviation policy. Safran’s Equipment & Defense division grew 17.7% on robust electrical system demand.[5]Safran, “Full-Year 2024 Results,” safran-group.com EU Clean Aviation’s SWITCH project, led by Collins, funds high-voltage distribution prototypes critical to future hybrid-electric narrowbodies. Brexit-related customs friction persists, yet the UK maintains power-electronics excellence around Farnborough, ensuring European converter supply continuity and steady growth for the aircraft DC-DC converter market.

Competitive Landscape

The market is moderately concentrated. Collins Aerospace, Honeywell, and Safran combine broad certification portfolios with global support networks that deter switching. They invest in SiC inverters, solid-state contactors, and model-based safety analysis to refresh product lines. In 2024, Honeywell spent USD 1.9 billion buying CAES, extending radiation-hardened power modules for defense satellites and Advanced Air Mobility. Bel Fuse’s USD 320 million Enercon purchase doubled its aerospace share to 31%, adding rugged converters for harsh-environment platforms.

Specialists like Vicor and Crane Aerospace focus on ultra-dense bricks and MIL-STD-qualified designs that slot into UAVs and missiles. Astronics targets airline retrofits with drop-in solid-state TRU replacements. New entrants exploit white-space around eVTOL propulsion and high-voltage battery management, yet they face steep DO-160 barriers and long qualification cycles that favor partnerships with incumbents.

Technology differentiation increasingly hinges on digital control, wide-bandgap efficiency, and modularity. Suppliers that can validate 99% efficient SiC converters while ensuring 20-year component availability will gain an advantage. Conversely, those dependent on single-region fabs risk schedule slips and must diversify wafer sourcing to safeguard aircraft DC-DC converter market share.

Aircraft DC-DC Converter Industry Leaders

Collins Aerospace (RTX Corporation)

Honeywell International Inc.

Safran SA

Astronics Corporation

AMETEK Programmable Power Inc. (AMETEK Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: RTX’s Collins Aerospace completed EPACS for F-35, doubling cooling headroom for advanced sensors.

- November 2024: AeroVironment bought BlueHalo in a USD 4.1 billion all-stock deal, expanding the demand for unmanned systems and power electronics.

- October 2024: Collins Aerospace finished high-voltage power-distribution prototypes under the EU SWITCH project.

- April 2024: Safran Electrical & Power introduced GENeUSCONNECT, a new line of high-power electrical harnesses for next-generation all-electric and hybrid aircraft systems. The harnesses operate at up to 800 volts DC and are engineered to manage partial discharge phenomena at altitude.

Global Aircraft DC-DC Converter Market Report Scope

| Isolated DC-DC Converters |

| Non-isolated DC-DC Converters |

| Transformer-Rectifier Units Upgraded to DC-DC |

| Brick/Modular Converters |

| Less than 250 W |

| 250 W to 1 kW |

| 1 to 5 kW |

| Greater than 5 kW |

| Narrowbody |

| Widebody |

| Regional Jets |

| Piston and Turboprop |

| Business Jets |

| Rotorcraft |

| Unmanned Aerial Vehicle (UAV) |

| Commercial Aviation |

| Military Aviation |

| Urban Air Mobility/eVTOL |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Product Type | Isolated DC-DC Converters | ||

| Non-isolated DC-DC Converters | |||

| Transformer-Rectifier Units Upgraded to DC-DC | |||

| Brick/Modular Converters | |||

| By Output Power | Less than 250 W | ||

| 250 W to 1 kW | |||

| 1 to 5 kW | |||

| Greater than 5 kW | |||

| By Aircraft Type | Narrowbody | ||

| Widebody | |||

| Regional Jets | |||

| Piston and Turboprop | |||

| Business Jets | |||

| Rotorcraft | |||

| Unmanned Aerial Vehicle (UAV) | |||

| By Platform | Commercial Aviation | ||

| Military Aviation | |||

| Urban Air Mobility/eVTOL | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the Aircraft DC-DC Converter market?

The market is valued at USD 1.05 billion in 2025 and is forecasted to reach USD 1.72 billion by 2030, reflecting a 10.37% CAGR.

Which region leads the Aircraft DC-DC Converter market?

North America holds the largest share at 36.44% in 2024, thanks to its robust aerospace manufacturing and defense programs.

What segment is growing fastest by platform?

Urban-air-mobility/eVTOL platforms show the highest growth, recording a 15.35% CAGR for the 2025-2030 period.

Why are SiC and GaN devices important for aircraft converters?

Wide-bandgap semiconductors provide up to 99% efficiency and enable 540 V DC buses, reducing weight and improving power density.

What are the main restraints to market growth?

Lengthy DO-160 / CS-ETSO certification cycles and concentrated gallium and SiC supply chains limit speed to market for new designs.

Which aircraft platforms will create the fastest incremental demand?

Urban-air-mobility/eVTOL aircraft and high-altitude UAVs are set to grow the quickest, requiring multi-kilowatt bricks with extreme power-density and reliability metrics.

Page last updated on: