Aircraft Communication Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

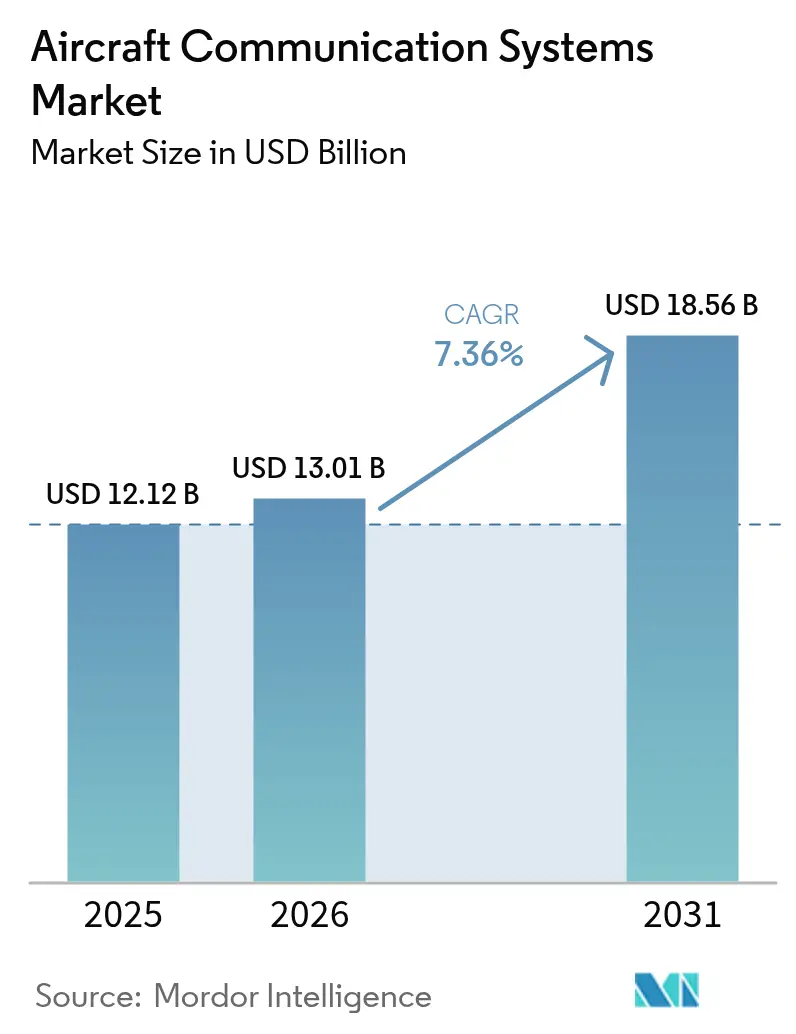

| Market Size (2026) | USD 13.01 Billion |

| Market Size (2031) | USD 18.56 Billion |

| Growth Rate (2026 - 2031) | 7.36% CAGR |

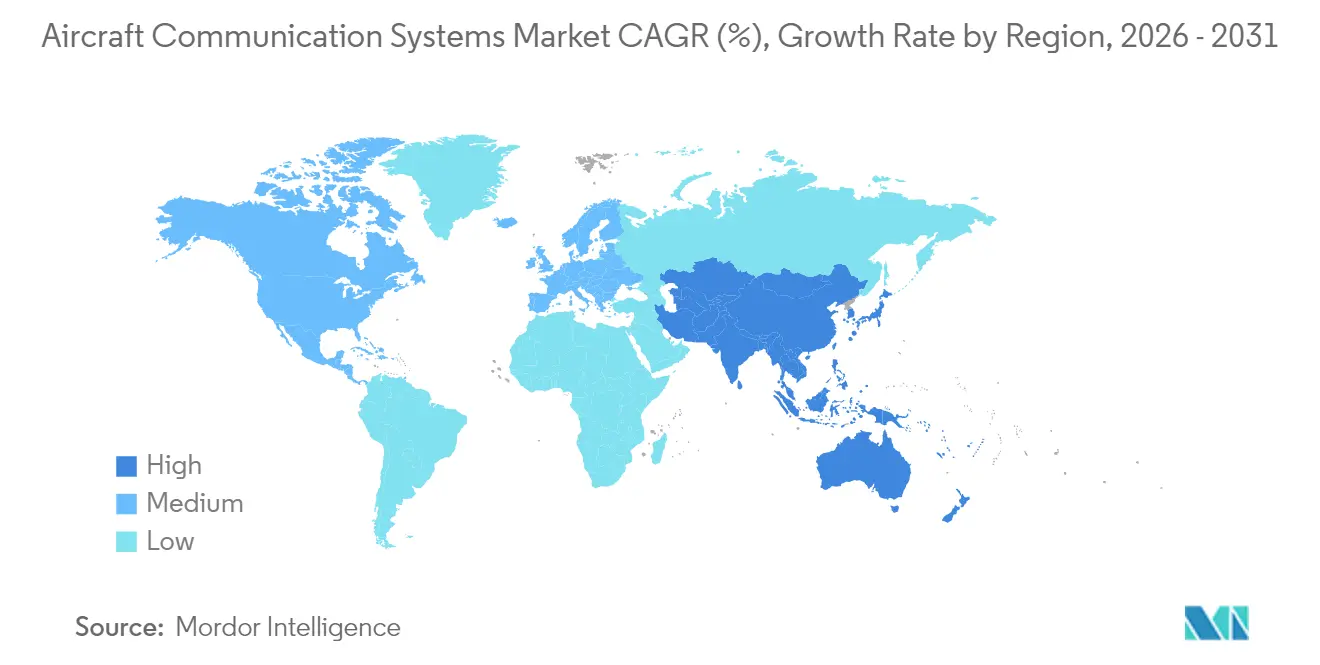

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Communication Systems Market Analysis by Mordor Intelligence

The aircraft communication systems market size is expected to grow from USD 12.12 billion in 2025 to USD 13.01 billion in 2026 and is forecast to reach USD 18.56 billion by 2031 at 7.36% CAGR over 2026-2031. The main growth catalyst is increasing demand for uninterrupted, secure, and multi-orbit connectivity across commercial, defense, and emerging urban-air-mobility fleets. Airlines are re-positioning connectivity from a cost center to a revenue service, while defense programs continue to upgrade tactical datalinks and satellite terminals for contested environments. Rapid digitalization of cockpit avionics, regulatory mandates such as CPDLC and ADS-B Out, and AI-driven spectrum management are stimulating investment across all aircraft classes. Consolidation among connectivity suppliers—seen in Gogo’s Satcom Direct purchase—and sustained fleet growth in Asia-Pacific further reinforce momentum for the aircraft communication systems market.

Key Report Takeaways

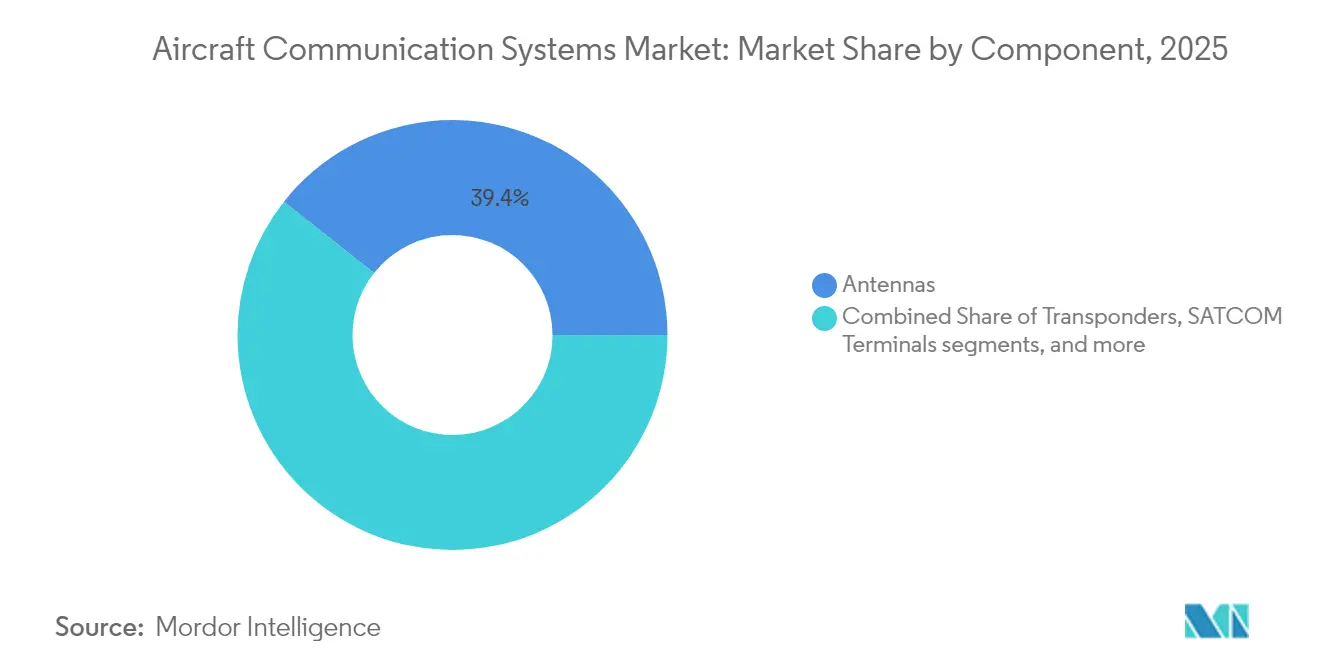

- By component, antennas led with 39.35% of the aircraft communication systems market share in 2025, whereas displays and processors are forecasted to expand at a 9.49% CAGR to 2031.

- By aircraft type, commercial aviation held 53.10% revenue share in 2025; urban-air-mobility platforms are projected to register the fastest 11.28% CAGR through 2031.

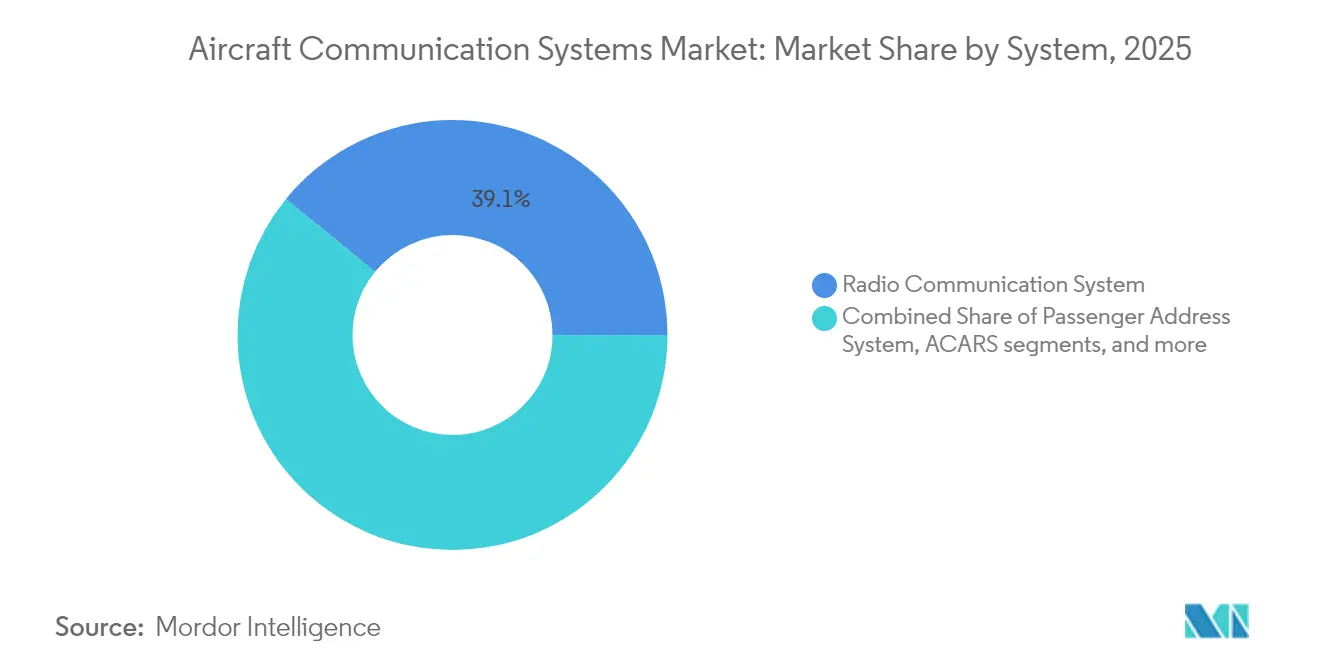

- By system, radio communication accounted for 39.10% share of the aircraft communication systems market size in 2025, while ACARS is advancing at an 8.18% CAGR.

- By connectivity technology, SATCOM commanded a 40.30% share of the aircraft communication systems market size in 2025, and 5G air-to-ground solutions are set to grow at a 7.62% CAGR.

- By geography, North America contributed a 35.50% share in 2025, whereas Asia-Pacific is the fastest-growing region, with an 8.29% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aircraft Communication Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| SATCOM-enabled in-flight connectivity surge | +1.2% | North America and Europe, spreading globally | Medium term (2-4 years) |

| Mandatory ADS-B Out and CPDLC compliance timelines | +0.8% | US and Europe leadership, global adoption | Short term (≤ 2 years) |

| Expansion of APAC narrowbody aircraft fleet | +1.0% | Asia-Pacific core, MEA spill-over | Long term (≥ 4 years) |

| Military fleet retrofit programs for secure comms | +0.9% | North America and Europe, allied nations | Medium term (2-4 years) |

| Software-defined radio integration across avionics | +0.7% | Global early military uptake | Long term (≥ 4 years) |

| AI-driven cognitive radios for dynamic spectrum use | +0.6% | North America and Europe pilot sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

SATCOM-enabled in-flight connectivity surge

Airlines are transitioning to multi-orbit architectures that combine LEO, MEO, and GEO capacity to eliminate latency gaps while preserving global reach. Delta Air Lines selected a Hughes multi-orbit solution for more than 400 aircraft, reflecting a paradigm shift toward viewing broadband connectivity as strategic infrastructure. ThinKom’s Ka2517 antennas have logged 17 million flight hours with 98% availability across 1,550 aircraft, proving interoperability and reliability.[1]ThinKom Solutions, “Ka2517 Antenna Flight Hours Milestone,” thinkom.com These service upgrades underpin revenue-sharing business models that encourage fleet-wide adoption of high-throughput links, reinforcing top-line growth for the aircraft communication systems market.

Mandatory ADS-B Out and CPDLC compliance timelines

ADS-B Out and domestic CPDLC are now required across US airspace, compelling airlines to retrofit VDL Mode 2 radios and communication management units. Parallel European mandates extend to autonomous distress tracking for aircraft above 27,000 kg from January 2025.[2] International Civil Aviation Organization, “Global Aeronautical Distress and Safety System Requirements,” icao.int Honeywell’s PM-CPDLC Supplemental Type Certificate offers a ready pathway to compliance using VHF Data Link radios and CMUs. Compulsory timelines accelerate near-term adoption cycles, lifting the demand for aircraft communication systems.

Expansion of APAC narrowbody aircraft fleet

Airbus forecasts Asia-Pacific’s aircraft services market to jump from USD 52 billion in 2025 to USD 129 billion by 2043, supported by roughly 19,500 new deliveries.[3]Airbus, “Global Services Forecast 2025–2043,” airbus.com As low-cost carriers grow, weight- and power-efficient antennas, processors, and VHF/SATCOM hybrids are prioritized. Chinese 5G air-to-ground trials and India’s secure radio roll-outs further elevate regional demand, translating into the fastest aircraft communication systems market growth rate.

Military fleet retrofit programs for secure communications

L3Harris’s USD 999 million contract for MIDS JTRS terminals underscores ongoing Link-16 upgrades, including concurrent-multiple-reception for higher data fidelity. Northrop Grumman’s USD 3.5 billion TACAMO program introduces next-generation strategic communication aircraft with Collins Very Low Frequency systems. Continuous retrofit funding sustains medium-term momentum, adding resilience to the aircraft communication systems market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Certification and DO-178/DO-254 cost burden | -0.9% | Stricter in North America and Europe | Medium term (2-4 years) |

| Cyber-vulnerabilities in IP-based avionics networks | -0.7% | Global, defense-focused concern | Short term (≤ 2 years) |

| RF spectrum congestion and interference risk | -0.6% | Dense urban regions worldwide | Long term (≥ 4 years) |

| Semiconductor supply shortages for RF chipsets | -0.8% | Global, niche aviation parts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Certification and DO-178/DO-254 cost burden

DO-178C and DO-254 verification costs rise sharply for multi-core and AI-enabled avionics. Collins Aerospace’s Mosarc architecture—recently cleared by the FAA—shows a 75% processing uplift without proportional certification costs, yet overall expense remains a headwind. Smaller OEMs face resource constraints, partially tempering the aircraft communication systems market in the medium term.

Cyber-vulnerabilities in IP-based avionics networks

The US GAO urges the FAA to bolster cybersecurity oversight of connected flight decks, citing new attack surfaces introduced by IP links.[4]US Government Accountability Office, “Aviation Cybersecurity: FAA Should Strengthen Oversight,” gao.gov Honeywell and the European Space Agency are developing quantum-key-distribution satellites to secure data paths. Elevated risk perceptions slow adoption of open-architecture communication suites, marginally reducing near-term growth for the aircraft communication systems market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Antennas hold the lead while processing power accelerates

Antennas captured 39.35% of the aircraft communication systems market share in 2025, led by electronically steered arrays designed for multi-orbit satellites. Satcom Direct's Plane Simple Ka-band ESA exemplifies a high-gain, low-profile design favored on long-haul fleets. The displays and processors category is forecasted to grow at a 9.49% CAGR through 2031, underpinned by Collins Aerospace's FAA-certified multi-core chips that lift cockpit computing capacity by 75%. The aircraft communication systems market size for displays and processors is on a steeper trajectory than legacy hardware. Transponders maintain steady demand as late-adopters meet ADS-B mandates, while communication management units (CMUs) gain from CPDLC roll-outs. Military counter-measure radios and SWaP-optimized SDR modules round out component demand, extending the breadth of the aircraft communication systems market.

A historical look shows hardware-centric growth, which has given way to software-defined functionality. Thales' FlytX tactile display reduces size and power by 30% and supports incremental certification, illustrating how modularity reshapes upgrade cycles. As modular avionics proliferate, procurement volumes migrate from fixed antennas toward processing platforms, keeping lifecycle revenues balanced across the aircraft communication systems market.

By Aircraft Type: Commercial fleets dominate as eVTOL ramps up

Commercial jets generated 53.10% of 2025 revenue as airlines prioritized broadband connectivity and regulatory compliance. Boeing’s plan to acquire Spirit AeroSystems signals greater vertical control of avionics integration, which should streamline communication-system fit-outs across narrowbody production lines. Urban-air-mobility (UAM) programs are projected to post an 11.28% CAGR, the fastest in the aircraft communication systems market, driven by Honeywell’s Anthem flight deck on Vertical Aerospace’s VX4. Military aircraft funding remains significant, illustrated by the E-130J TACAMO and Link-16 modernization contracts. Business aviation adds incremental volume through long-range cabin SATCOM upgrades, such as Bombardier’s multi-year agreement with Honeywell. Regional jets sustain demand across the expanding APAC fleet, while unmanned systems integrate advanced SDRs and AI processors, deepening tactical use cases within the aircraft communication systems market.

By System: Radio communication’s lead narrows as ACARS modernizes

Traditional VHF/HF voice radio still accounts for 39.10% of 2025 revenue, but capacity limits and rising data needs are steering growth toward IP-enabled messaging. ACARS over IP is the fastest-growing system at 8.18% CAGR, with airlines exploiting broadband links to lower HF charges and improve dispatch efficiency. The aircraft communication systems market size for ACARS solutions will expand in line with air-ground digitization initiatives. Interphone, digital audio, and tactical datalink systems also benefit from SDR roadmaps that enable multi-waveform support in a single LRU. The shift from circuit-switched to packet-based architectures underpins a steady reallocation of spending within the aircraft communication systems market.

By Connectivity Technology: SATCOM maintains scale while 5G ATG gains pace

SATCOM retained a 40.30% share of the aircraft communication systems market size in 2025 across L, Ku, and Ka bands. Viasat’s Amara platform layers dual-beam connectivity across LEO, MEO, and GEO orbits for 2028 entry, signaling continued SATCOM primacy. However, 5G air-to-ground networks are forecasted to grow at 7.62% CAGR, especially in regions where high-density terrestrial towers can service narrow-body fleets cost-effectively. VHF data link remains foundational for ATC voice backup, while tactical waveforms such as Link-16 and Protected Tactical Waveform expand defense usage. Hybrid architectures that switch between ATG and satellite links based on cost and latency optimize total cost of ownership, elevating technology diversity across the aircraft communication systems market.

Geography Analysis

North America retained 35.50% of 2025 revenue thanks to FAA modernization programs and sustained military spending. The FAA’s telecommunication infrastructure overhaul across 4,600 ATC facilities continues, providing a robust domestic market for radios, datalinks, and spectrum-management upgrades. US defense contracts—including a USD 269 million BACN task order—reinforce procurement visibility through 2027.

Asia-Pacific is the fastest-growing region, increasing at an 8.29% CAGR through 2031. Aircraft communication systems market investments mirror rising fleets in China, India, and Southeast Asia. China Telecom is piloting nationwide 5G air-to-ground coverage with fewer than 1,000 towers, while India is fitting Vayulink secure radio networks onto its expanding fighter inventory. Regional carriers like Thai Airways have adopted SES multi-orbit connectivity, highlighting commercial pull for advanced SATCOM.

Europe maintains a solid position owing to stringent regulatory leadership. ICAO’s updated future air navigation standards mandate cyber-resilient data exchange, spurring adoption of encrypted link management. Thales and Spire Global are deploying 100+ satellites to deliver space-based ADS-B surveillance, slated for 2027 service entry. Airbus HBCplus offers integrated multi-orbit terminals that reduce drag and fuel burn, underlining OEM-level influence on the aircraft communication systems market.

South America, the Middle East, and Africa contribute moderate but growing demand, leveraged by fleet renewals and strategic defense projects. Owing to sparse terrestrial infrastructure, hybrid ATG/SATCOM solutions appeal in these geographies, sustaining a globally diversified growth pattern for the aircraft communication systems market.

Regulatory Landscape

The regulatory environment for aircraft communication systems is anchored by mandated surveillance and datalink performance requirements, and by tighter spectrum coexistence rules. In the United States and Europe, ADS-B Out and controller-pilot datalink communications (CPDLC) compliance continues to drive demand for certified VHF data link radios, communication management units, and interoperable avionics, while FAA DataComm program updates reinforce operational formats and equipage consistency. In April 2024, EASA released Issue 5 of CS-ACNS, updating certification specifications and acceptable means of compliance for airborne communications, navigation, and surveillance equipment, which affects how OEMs and integrators qualify radios, datalinks, and associated avionics functions.

Spectrum protection and interference tolerance requirements are also shaping product roadmaps and certification work. In January 2026, the FAA published a proposed rule to require radio altimeters to meet minimum performance requirements for interference tolerance in the Upper C-band (3.98-4.2 GHz), strengthening the safety case for integrated avionics architectures and increasing verification activities around RF coexistence. Internationally, ITU published Recommendation M.2176-0 in February 2026, setting technical characteristics and protection criteria for ICAO-standardized VDL Mode 2 systems in the 136-137 MHz band. RTCA and EUROCAE alignment through joint standards such as DO-262G/ED-243D (September 2025) supports globally synchronized minimum operational performance expectations for satellite and datalink-related avionics.

Value Chain Analysis

The value chain spans RF and digital semiconductors, antennas and SATCOM terminals, radios and communication management units, and embedded software that must clear airworthiness and cybersecurity assurance. Upstream contributors include chipset and RF front-end suppliers, antenna and terminal manufacturers, and specialized avionics software developers operating under DO-178C/DO-254 constraints. Midstream system integration is concentrated among Tier-1s that package LRUs, racks, and wiring into certifiable aircraft configurations. Downstream, airframers, MROs, and licensed modifiers execute line-fit and retrofit installations through STCs, supported by connectivity service providers and defense prime contractors that manage network services, keys, and sustainment.

Procurement and fulfillment are being shaped by defense modernization programs and supply chain risk management. For example, Airbus Defence and Space contracted Thales for the AVIATOR 700S safety satcom system for the A400M (June 2025), and L3Harris was selected as a subcontractor to provide assured communications for the U.S. Air Force E-4C fleet under the SAOC program (December 2025). In both cases, certified components flow through a prime-led integration and long-term support pipeline. Semiconductor constraints and tariff exposure remain bottlenecks for RF components, driving dual-sourcing and higher safety stocks. They also reinforce the use of modular, software-defined architectures that reduce recertification friction when parts change or new capabilities are inserted.

Competitive Landscape

The aircraft communication systems market is moderately concentrated. Honeywell’s USD 1.9 billion acquisition of CAES adds 2,200 RF engineers and electronic warfare capabilities, bridging antenna design and secure communication payloads. Gogo’s USD 375 million purchase of Satcom Direct consolidates business-aviation connectivity, targeting USD 890 million combined revenue and 24% EBITDA margins. Raytheon’s Collins Aerospace division differentiates on certified multi-core processing power, opening new revenue in avionics computing.

Defense-focused suppliers such as L3Harris extend Navy programs while experimenting with LEO Link-16 satellites to harden tactical networks. Peraton Labs showcases AI-based spectrum tools that could disrupt conventional fixed-frequency planning. Across commercial, business, and emerging UAM sectors, competition centers on integrating multi-orbit links, certifying SDR architectures, and securing semiconductor supply.

Supply-chain resilience is now a competitive metric. OEMs and Tier-1s diversify chip fabrication partners and maintain higher safety stocks to navigate RF component shortages. Collectively, these moves indicate an industry seeking agility while addressing the increasingly complex requirements of the aircraft communication systems market.

Aircraft Communication Systems Industry Leaders

Honeywell International Inc.

RTX Corporation

L3Harris Technologies, Inc.

Thales Group

ViaSat Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Multi-orbit connectivity upgrades and the shift toward IP-based aeronautical networking create whitespace for retrofit kits and line-fit solutions that simplify installation while meeting evolving certification and interference constraints. A near-term market signal is the scale of airline connectivity procurement: in July 2026, Frontier Airlines and Indigo Partners selected Starlink for a multi-airline rollout covering more than 1,000 aircraft across Frontier, Wizz Air, Volaris, JetSMART, and Cebu Pacific. This selection supports demand for compatible antennas, terminals, and onboard network integration across large narrowbody fleets. In business aviation, certification-driven retrofit activity is reflected in July 2026, when Gogo Galileo HDX gained FAA/EASA certification for Gulfstream G650/G650ER and other platforms, expanding the addressable installed base for electronically steered antennas and related satcom avionics.

Security and resiliency requirements are also creating adjacent opportunity areas within the airborne communications scope, particularly where GNSS and RF threats influence avionics architecture decisions. In July 2026, Iridium began selling a GNSS jamming and spoofing prevention chip, aligning with operator and defense interest in hardened PNT and resilient communications that can be integrated into aircraft avionics suites. Regulatory and standards work on spectrum coexistence, including the FAA’s January 2026 proposed radio altimeter interference tolerance rule and CAAC performance standards for 5G AeroMACS equipment (CTSO-2C610, January 2025), further supports demand for upgraded RF front ends, filtering, and certification-ready integration. This is relevant for minimizing downtime during fleet modernization cycles.

Recent Industry Developments

- April 2026: RTX (Collins Aerospace) was selected by Bell Textron to supply five critical systems for the U.S. Army's MV-75 Future Long Range Assault Aircraft (FLRAA). The package strengthens Collins' position as a platform-level integrator where communications and avionics subsystems are designed into a new-production military rotorcraft program. It also supports longer-cycle revenue from qualification, production ramp, and sustainment around mission communications and related avionics.

- December 2025: L3Harris was selected by SNC as a subcontractor to provide assured communications for the U.S. Air Force E-4C fleet under the Survivable Airborne Operations Center (SAOC) program as part of a five-year engineering and manufacturing development contract. The award ties resilient airborne communications to a modernization pathway for strategic command-and-control aircraft. Program-funded development and certification work can translate into follow-on production and support demand for secure terminals, radios, and integration services.

- September 2024: Viasat received a USD 33.6 million contract from the U.S. Air Force Research Laboratory under the Defense Experimentation Using Commercial Space Internet (DEUCSI) program to develop and deliver AESA systems to enhance satcom capabilities for tactical aircraft, including rotary wing platforms. The effort advances electronically steered antenna maturity for contested and mobile operations. Demonstrated performance in defense experimentation programs can accelerate transition into operational kits and broader platform adoption.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenues earned from airborne communication equipment and embedded software that enable voice and data exchange between an aircraft, ground stations, and other aircraft, across civil and defense platforms.

Scope exclusions: We exclude ground-based air traffic control infrastructure and standalone cabin Wi-Fi routers sold only for passenger internet.

Segmentation Overview

- By Component

- Transponders

- SATCOM Terminals

- Antennas

- Displays and Processors

- Communication Management Units

- Other Components

- By Aircraft Type

- Commercial Aircraft

- Narrowbody

- Widebody

- Regional Jets

- Business Jets

- Military Aircraft

- Fighter

- Transport

- Special-mission

- Unmanned Aerial Vehicles (UAVs)

- Urban Air Mobility/eVTOL

- Commercial Aircraft

- By System

- Radio Communication System

- Interphone Communication System

- Passenger Address System

- Digital Radio and Audio Integrating Management System

- Aircraft Communications Addressing and Reporting System (ACARS)

- By Connectivity Technology

- SATCOM (L/Ku/Ka-band)

- VHF/HF Voice

- Air-to-Ground (ATG/5G-ATG)

- Tactical Data Links (Link-16, MADL)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Russia

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the factual base for the model, and to keep assumptions tied to real aviation activity. We relied on public sources such as FAA aircraft registration and activity data, ICAO air transport statistics, EASA publications, and defense and civil procurement notices from official portals. Where trade flows mattered for certain assemblies, customs statistics and aircraft delivery announcements were reviewed to cross-check demand timing.

Along with these, we reviewed annual reports, investor presentations, and product certification and spectrum related updates from official bodies, plus reputable aviation press to validate program ramps and retrofit cycles. In parallel, we used a paid subscription for company financials and news to check revenue mix and identify major contract wins without depending on any single company story. These examples are not exhaustive, and many other public sources were also consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and short surveys with aircraft OEM and Tier suppliers, aftermarket and MRO stakeholders, airline and defense user side teams, and aviation regulators or advisors. Since this is a global market, inputs were checked across Americas, EMEA, and APAC so regional fleet mix, retrofit behavior, and certification timing could be reflected in the final assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 14% | APAC: 46% |

| Mid tier: 48% | Functional/Unit leaders: 33% | EMEA: 34% |

| Smaller Players: 19% | Managers: 53% | Americas: 20% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs the addressable aircraft communication demand pool using fleet and delivery volumes, plus installation and retrofit penetration by aircraft type and mission. Once the demand pool is defined, it is translated into revenue using system level pricing ranges and expected content per aircraft, and then split by region based on fleet distribution and new build activity.

To keep the totals realistic, we corroborate the outcome with selective bottom-up approximations, such as sampled program level supplier roll-ups, channel checks on retrofit kits, and ASP times volume checks for key units like radios, SATCOM terminals, antennas, and communication management units. The model is guided by market fingerprints that can be repeatedly tracked, including commercial aircraft deliveries, defense modernization timelines, retrofit cycles during heavy maintenance checks, certification and mandate driven upgrades, and the mix shift toward connected avionics.

For forecasting, scenario analysis is applied around aircraft production rates, defense budgets, retrofit uptake, and pricing movement, and then these scenarios are aligned to what interviewees see in near term programs and backlog conversion. Where bottom-up inputs are incomplete (for example, fragmented retrofit channels), gaps are handled using penetration ranges anchored to fleet counts and then stress tested against supplier commentary and published program activity.

Data Validation & Update Cycle

Outputs are checked in multiple steps so any odd jumps are caught early. We compare results against independent signals such as fleet growth, aircraft delivery trends, and known upgrade cycles, and then review any variances that do not match the expected pattern by region or aircraft type.

Before sign-off, assumptions and calculations go through an internal peer review, and follow-up calls are triggered when a key input moves materially, such as a major program delay or a new mandate affecting avionics upgrades. The report is refreshed annually, and interim updates are made when major market events occur. Right before delivery, a final analyst pass is completed so clients receive the most current view possible.

Mordor Intelligence's Aircraft Communication Systems Market Size Measured Against Other Published Estimates

Published market values for aircraft communication systems can look far apart even when the topic name sounds the same, because each publisher draws the product boundary differently and also uses different price and volume assumptions. Differences also come from the year selected as the base, the way retrofit demand is counted, and how often the model is refreshed.

Some published figures fold adjacent onboard connectivity and cabin networking hardware into the same total. In Mordor Intelligence, the count stays focused on airborne communication equipment and embedded software used for aircraft to ground and air to air exchange, and it keeps ground ATC infrastructure and standalone cabin Wi-Fi routers out of scope, which changes the final total.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 12.12 B (2025) | |

| Global Consultancy A | USD 18.50 B (2025) | Uses a wider system basket that also includes items like passenger address and interphone systems, and it does not clearly separate cabin networking hardware from mission communication, which inflates the addressable revenue base. |

| Trade Journal B | USD 9.80 B (2024) | Anchors the model to a narrower set of radio communication line items and an earlier base year, and it appears to apply more conservative retrofit penetration and pricing progression, which pulls the total down versus broader definitions. |

The spread in the table is mainly explained by what is counted as a communication system versus an adjacent onboard function, and by how retrofit uptake and pricing are treated by year. By tying the estimate to fleet and delivery indicators, and then cross-checking with program level pricing ranges, our approach stays traceable to clear inputs that can be updated in a repeatable way as aircraft production and upgrade cycles change.

Key Questions Answered in the Report

What is the current size of the aircraft communication systems market?

The market is valued at USD 13.01 billion in 2026 and is expected to reach USD 18.56 billion by 2031, representing a 7.36% CAGR.

Which component segment is growing the fastest?

Displays & processors are forecasted to grow at a 9.49% CAGR through 2031, driven by FAA-certified multi-core processing platforms that boost cockpit computing by 75%.

Why is Asia-Pacific the fastest-growing region?

Fleet expansion, 5G air-to-ground trials and increased defense spending push Asia-Pacific to an 8.29% CAGR, outpacing other regions.

How are regulatory mandates influencing demand?

Mandatory ADS-B Out and CPDLC timelines compel airlines to equip VDL radios and CMUs, accelerating near-term spending on compliant communication solutions.

What technologies are challenging SATCOM’s dominance?

5G air-to-ground networks are the fastest-growing connectivity technology, offering low-latency broadband that complements multi-orbit satellite links.

What is the main cybersecurity concern with modern avionics networks?

IP-based connectivity introduces new attack vectors, prompting initiatives such as quantum-key-distribution satellites and FAA oversight enhancements to secure data paths.

Page last updated on: