Aircraft Electric Motors Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

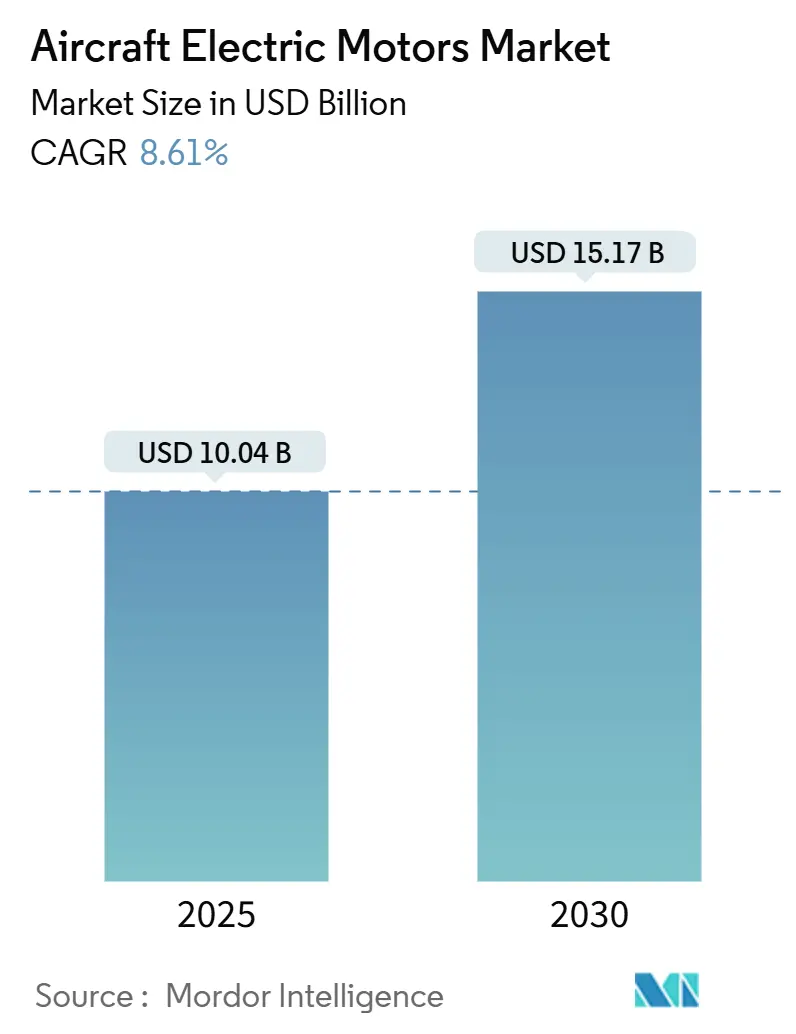

| Market Size (2025) | USD 10.04 Billion |

| Market Size (2030) | USD 15.17 Billion |

| Growth Rate (2025 - 2030) | 8.61% CAGR |

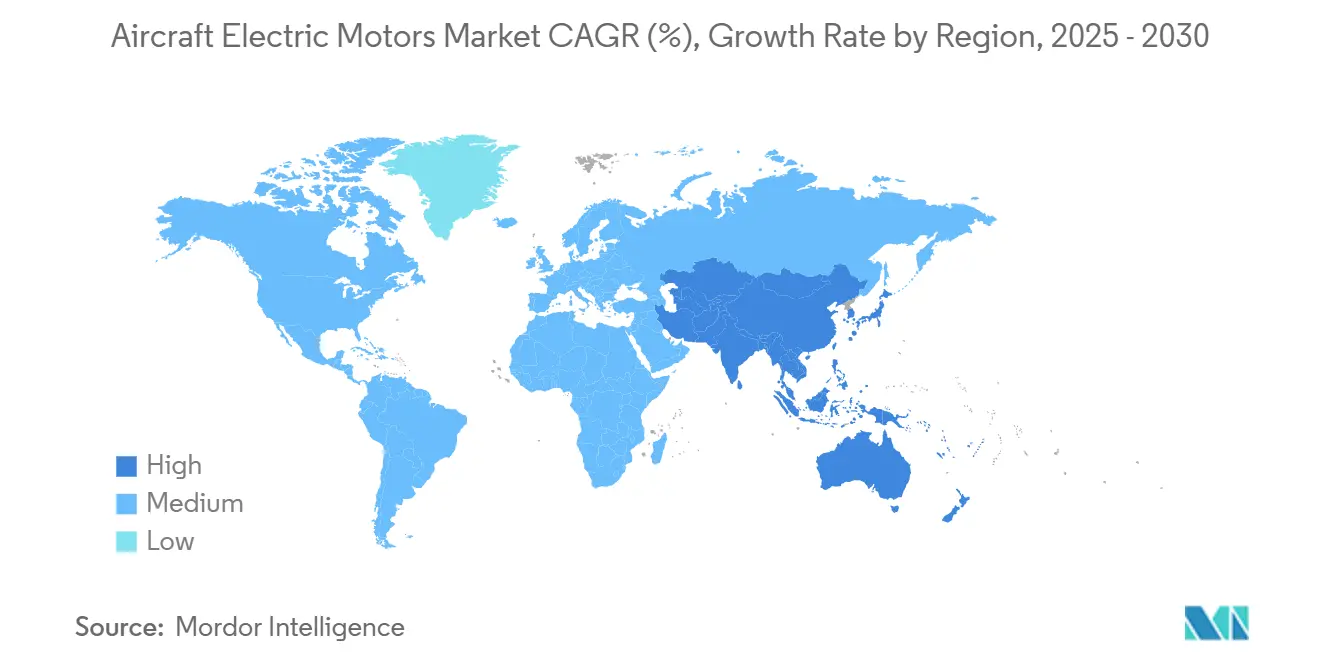

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Electric Motors Market Analysis by Mordor Intelligence

The aircraft electric motors market size reached USD 10.04 billion in 2025 and is forecasted to advance to USD 15.17 billion by 2030, translating into an 8.61% CAGR over the period. Growth is propelled by commercial and military programs that replace hydraulic and pneumatic subsystems with high-efficiency electric alternatives, tighter global CO₂ and noise mandates that reward zero-emission propulsion, and record venture funding for urban air mobility projects. Established airframers accelerate more-electric aircraft road maps, while defense ministries embed electric actuation into next-generation rotorcraft and unmanned systems. In parallel, power-dense axial-flux and superconducting motor architectures migrate from automotive and research labs to flight hardware, driving fresh supplier rivalry across the aircraft electric motors market.[1]Source: European Union Aviation Safety Agency, “Technology and Design | EASA Eco,” easa.europa.eu North America’s defense budgets and Europe’s climate policies shape early adoption, but Asia-Pacific’s resurgent airline traffic and UAV build-out deliver the steepest regional growth. Supply-chain vulnerabilities around rare-earth magnets and battery energy density ceilings temper the otherwise robust expansion outlook.

Key Report Takeaways

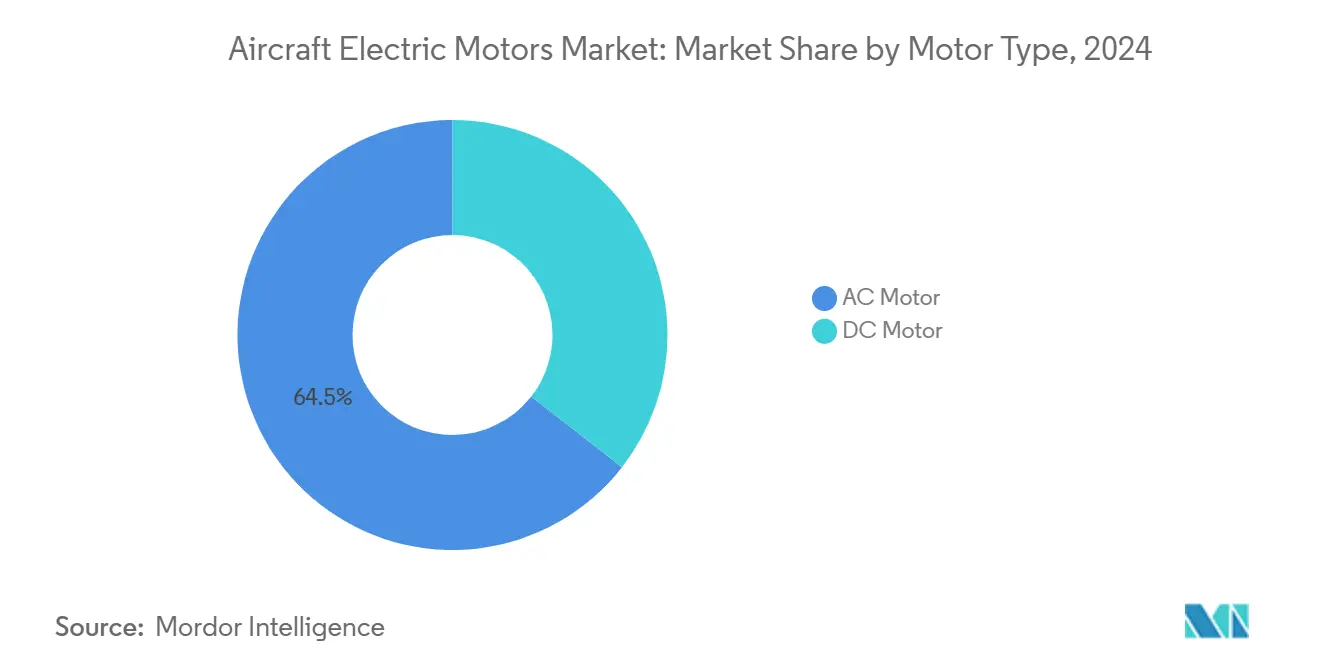

- By motor type, AC machines had a 64.45% share in 2024, yet DC architectures will expand at a 10.67% CAGR due to eVTOL and UAV adoption.

- By aircraft type, fixed-wing platforms commanded 64.78% of the aircraft electric motors market share in 2024, while advanced air mobility is projected to accelerate at a 14.54% CAGR through 2030.

- By output power, the 10 to 200 kW band represented 57.91% of the aircraft electric motors market size in 2024, while motors above 200 kW are forecasted to climb at a 10.75% CAGR through 2030

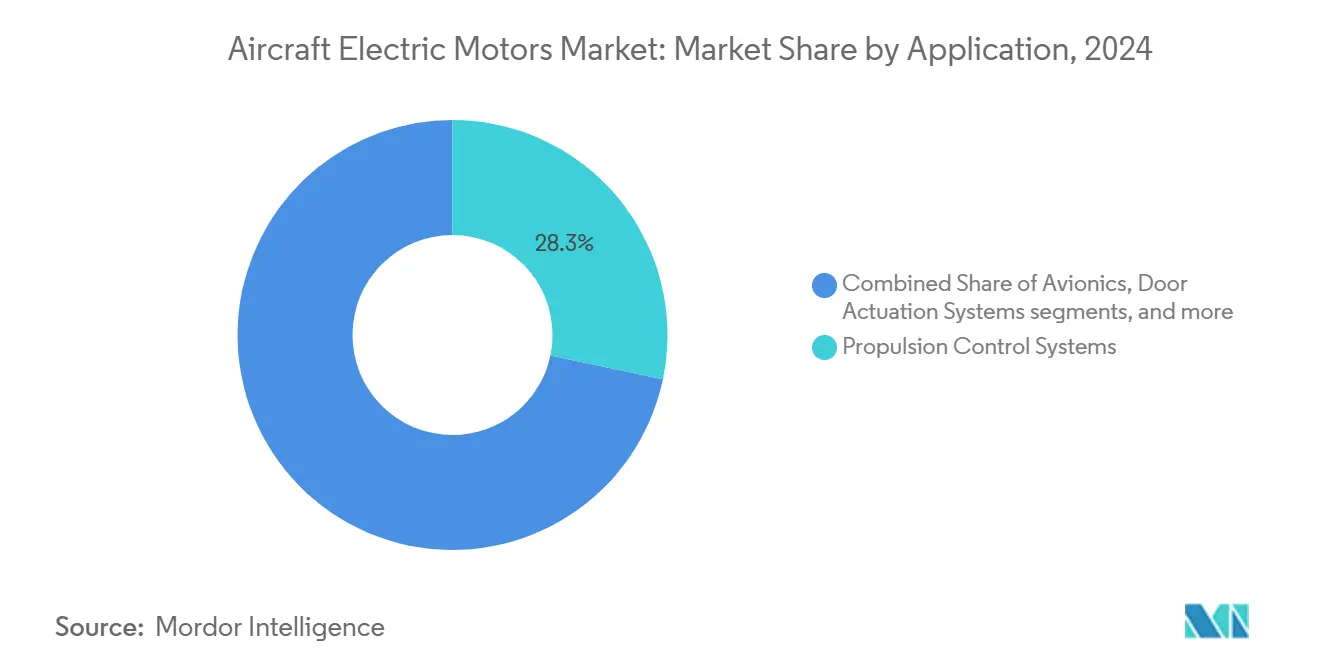

- By application, propulsion control systems led with 28.30% revenue share in 2024, whereas avionics systems are set to post the fastest 9.78% CAGR to 2030.

- By end-use, OEM installations dominated with 67.91% share in 2024, whereas aftermarket integrations will log a 9.65% CAGR as retrofit programs gain regulatory traction.

- By geography, North America retained a 38.78% share in 2024, yet Asia-Pacific is expected to outpace all other regions with a 9.98% CAGR through 2030.

Global Aircraft Electric Motors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for more-electric and all-electric (MEA/AEA) architectures | +2.1% | Global, with North America and Europe leading adoption | Medium term (2-4 years) |

| Rapid UAV and eVTOL fleet expansion | +1.8% | Global, concentrated in North America, Europe, and Asia-Pacific urban centers | Short term (≤ 2 years) |

| Tighter CO₂/NOx limits and airport noise caps | +1.4% | Global, with strictest enforcement in Europe and North America | Long term (≥ 4 years) |

| OEM shift to integrated starter-generator architectures | +1.2% | Global, led by commercial aviation in North America and Europe | Medium term (2-4 years) |

| Surplus axial-flux production capacity migrating from EV to aviation | +0.9% | Global, with capacity concentration in Europe and Asia-Pacific | Short term (≤ 2 years) |

| Falling rare-earth magnet intensity per kW via topology innovation | +0.7% | Global, with R&D centers in North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Demand for more-electric and all-electric (MEA/AEA) architectures

Airframers continue to migrate critical subsystems from bleed-air and hydraulics to distributed electric architectures that promise higher efficiency, reduced maintenance, and lower emissions. The B787 shows the blueprint for replacing pneumatic ice protection and cabin pressurization packs with high-voltage electric machines, trimming fuel burn by 30%, and cutting carbon by more than 20%. Military programs follow suit: the US Army’s FLRAA selects a Safran high-voltage starter-generator to satisfy escalating onboard power loads.[2]Source: Safran Group, “Safran Selected by Bell to Provide Electrical Power Generation,” safran-group.com Start-ups like Eviation pair fully electric propulsion with next-generation batteries to address regional routes, proving commercial appetite for zero-emission service. As these architectures proliferate, the aircraft electric motors market benefits from a rising content-per-aircraft metric, increasing revenue, and unit shipments.

Rapid UAV and eVTOL Fleet Expansion

Urban air mobility has moved from concept to pre-commercial testing, backed by harmonized FAA-EASA guidance that assigns four certification tiers tied to payload and passenger count. Archer and Joby cumulatively surpassed 100 full-scale flight tests, while Joby broke ground on high-rate production lines in California. Defense customers simultaneously ramp electric UAV acquisitions for ISR and logistics missions that value low acoustic signatures and simplified support footprints. The surge of platforms requiring high torque at low RPM favors axial-flux and brushless DC machines, accelerating unit demand across the aircraft electric motors market and pressuring supply chains to deliver aviation-grade reliability at automotive-like volumes.

Tighter CO₂ / NOx Limits and Airport Noise Caps

ICAO’s 2031 entry-into-service rule mandates at least 10% fuel-burn improvement and 6 dB cumulative noise reduction for new aircraft. The FAA’s 2024 particulate matter rule builds on that baseline by replacing legacy smoke number metrics with a direct NVPM standard that gas-turbine engines struggle to meet. Community-driven curfews at major hubs intensify compliance pressure, particularly for helicopters and emerging eVTOL services. Electric motors inherently emit zero local pollutants and generate substantially less noise, allowing operators to satisfy regulatory thresholds without costly engine retrofits. Compliance requirements, therefore, convert into direct revenue expansion for the aircraft electric motors market as airlines and OEMs adopt electric solutions to preserve route authority.

OEM Shift to Integrated Starter-Generator Architectures

Combining engine start, power generation, and boost functions within a single electric machine reduces weight, part count, and lifecycle costs. Safran’s starter-generator for Bell’s FLRAA delivers 350 kW continuous output while withstanding harsh rotorcraft vibration environments. GE Aerospace pursues similar multifunctionality by embedding motor-generators inside a modified turbofan under a NASA contract, aiming for 5% fuel-burn reduction on single-aisles. Integrated units require advanced thermal paths and power electronics, spurring joint development programs between motor specialists and inverter suppliers. As certification efforts mature, integrated starter-generators will replace standalone accessories, expanding penetration of the aircraft electric motors market across both new-build and retrofit fleets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Battery gravimetric-energy plateau | -1.9% | Global, with particular impact on long-range applications | Long term (≥ 4 years) |

| Qualification and certification bottlenecks (DO-160, DO-178C) | -1.4% | Global, with regulatory complexity highest in North America and Europe | Medium term (2-4 years) |

| Supply-chain exposure to Nd-Fe-B price shocks | -1.1% | Global, with highest impact in regions dependent on Chinese rare-earth processing | Short term (≤ 2 years) |

| Thermal runaway risk in high-altitude pressurized installations | -0.8% | Global, with particular concern for commercial aviation and high-altitude UAV operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Battery Gravimetric-Energy Plateau

State-of-the-art lithium-ion (Li-ion) packs hover near 350 Wh/kg, yet regional airliners need at least 800 Wh/kg to match today’s payload-range profiles. Incremental chemistry gains of 5–8% annually inch the needle but fail to bridge the gap before 2030, constraining pure-electric designs to short-haul or training roles. Solid-state prototypes promise step-changes, yet manufacturing scale and aviation safety validation remain unresolved. The mass penalty forces OEMs toward hybrid architectures that still rely on conventional fuel, reducing immediate demand potential for high-power standalone electric motors and capping near-term growth of the aircraft electric motors market.

Qualification and Certification Bottlenecks (DO-160, DO-178C)

Electric motor installations face extended compliance cycles because legacy standards focus on turbine engines. FAA special conditions applied to BETA Technologies’ H500A demonstrate the intensity of line-by-line hazard analyses for novel propulsion.[3]Source: Federal Aviation Administration, “Special Conditions: BETA Technologies Model H500A,” federalregister.gov Software-heavy motor controllers trigger additional DO-178C scrutiny, stretching development by two to three years and elevating start-up burn-rate pressures. Certification delays therefore defer revenue recognition across the aircraft electric motors market and can deter risk-averse investors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Motor Type: AC Dominance Faces Rising DC Adoption

AC machines retained the lion’s share by servicing legacy three-phase aircraft buses and critical constant-speed actuation duties. At 64.45% in 2024, their hold on the aircraft electric motors market size underscores decades of field reliability and mature repair networks. Brushless synchronous and induction variants deliver precise torque curves essential for primary flight controls and environmental systems that demand unwavering performance in hot-high and cold-soak extremes. Yet the accelerating pivot toward battery-centric powertrains in eVTOL and high-end UAV fleets ignites fresh interest in direct-current ecosystems.

The DC segment, registering a double-digit 10.67% CAGR, benefits from simplified wiring, native battery compatibility, and easier speed modulation through electronic commutation. Pioneers such as Safran’s ENGINeUS™ series demonstrate scalable modules reaching 850 VDC, while H3X’s ultra-compact units hit 12 kW/kg continuous output. As dual-conversion inverters blur AC-DC boundaries, suppliers that master both families secure competitive flexibility, reinforcing the long-term resilience of the aircraft electric motors market. Three-line redundancy, fault-tolerant windings, and hermetic cooling are universal differentiators across both current types.

By Output Power: Mid-Range Motors Anchor, Megawatt Class Ascends

Power bands between 10 and 200 kW fulfill the bulk of auxiliary propulsion, rotorcraft, and regional aircraft demands, translating into a 57.91% share of the aircraft electric motors market size in 2024. Proven thermal paths, off-the-shelf inverters, and standardized voltage interfaces streamline integration across multiple airframer programs. These units cover starter-generator roles, anti-ice fans, and propulsive lift systems in distributed arrangements.

The above 200 kW machines, though smaller in installed base, command the steepest 10.75% CAGR as air-framers pursue hybrid-electric narrowbodies and cargo drones. Honeywell’s 1 MW turbogenerator couples turbine efficiency with electric flexibility, anchoring propulsion for nine-to-nineteen-seat concepts. Immersion-oil impinging cooling removes concentrated heat flux, unlocking megawatt scalability without violating aviation-grade mass budgets. As thermal limits recede, these high-power segments broaden the aircraft electric motors market, sparking new supplier alliances around power electronics, cryogenic wire, and magnetic alloys.

By Application: Propulsion Leads, Avionics Surge

Starter-generators, electric compressors, and traction motors for distributed propulsion yielded 28.30% of 2024 revenues as OEMs advanced from auxiliary electrification to thrust-class applications. High-cycle durability and confined nacelle environments elevate power-density and thermal-rejection thresholds, prompting investment in axial-flux rotors and silicon-carbide inverters. These attributes ensure propulsion remains the cornerstone of the aircraft electric motors market, although ancillary systems rapidly close the gap.

Avionics records the briskest 9.78% CAGR, mirroring the industry-wide passage to fly-by-wire, which jettisons hydraulic plumbing in favor of electrically driven ball screws and rotary actuators. Multilane voting logic and health-monitoring firmware grant fail-operational integrity, while compact motor-gearbox cartridges ease wing-box packaging. As certification confidence rises, airlines will retrofit trailing-edge flaps and rudder systems, further diversifying revenue streams and heightening resilience within the aircraft electric motors industry.

By Aircraft Type: Fixed-Wing Holds Ground, AAM Accelerates

Commercial single-aisle and twin-aisle jets remain the largest users, absorbing a 64.78% share, reflecting fleet-scale replacement cycles and sustainability retrofits required under tightening emissions caps. Power-hungry galleys, pressurization packs, and anti-ice devices migrate to electric drives, steadily increasing content per frame across the aircraft electric motors market. Parallel defense acquisition funnels for tankers, ISR platforms, and stealth bombers guarantee a persistent baseline even during civil demand swings.

Advanced Air Mobility, however, rises as the runaway growth champion, tracking a 14.54% CAGR to 2030. Battery-fed distributed propulsion architectures enable vertical lift without complex transmissions, allowing start-ups to reimagine air-space integration for point-to-point urban travel. Rotorcraft and long-endurance drone classes also gain traction, capitalizing on electric torque for low-noise hover and efficient loiter missions. As certification milestones fall, these emerging vertical markets challenge fixed-wing dominance and inject fresh product-mix complexity into the aircraft electric motors market.

By End-Use: OEM Integration Dominates, Aftermarket Awakens

Airframe manufacturers captured 67.91% of spending in 2024 as clean-sheet designs baked electric propulsion into baseline requirements. Close collaboration between OEMs, Tier-1 integrators, and motor specialists streamlines certification and creates proprietary supply chains. Early inclusion allows structural optimization around motor mass distribution, cooling channels, and wire runs, reinforcing OEM influence over the aircraft electric motors market.

Retrofit momentum intensifies; MROs eye electric actuation kits to replace aging hydraulic packs on legacy fleets, targeting fuel-burn savings and lower maintenance costs. CAE’s conversion of trainer aircraft and Woodward’s acquisition of Safran’s actuation arm foreshadow an aftermarket race projected to log a 9.65% CAGR. As fleets age, the line-fit/retrofit balance will equalize, forcing suppliers to service dual lifecycle channels and fortify spares logistics.

Geography Analysis

North America held 38.78% of 2024 revenue, underpinned by USD 886 billion in US defense funding, NASA hybrid-electric demonstrators, and venture-backed eVTOL leaders that collectively accelerate technology readiness. California’s Silicon Valley clusters funnel capital and talent into propulsion laboratories, while longstanding aerospace hubs across Washington and Connecticut ensure scale manufacturing. Regulatory clarity from the FAA on special-class electric engines further cements first-mover advantages, drawing global airframers to certify on US soil and reinforcing regional weight in the aircraft electric motors market.

Asia-Pacific registers the fastest 9.98% CAGR due to China’s combined civil-military procurement of electric UAVs, Japan’s high-precision motor metallurgy, and South Korea’s breakthrough carbon-nanotube conductors that promise magnet-free designs. Rising middle-class travel, airport infrastructure expansion, and governmental green-aviation subsidies converge to lift local demand. India’s “Make in India” aerospace initiative and Australia’s mining-drone deployments further diversify regional contribution, collectively enlarging the aircraft electric motors market and challenging the traditional West-centric order.

Europe remains an influential pillar through Airbus, Rolls-Royce, and Safran, each pouring billions into superconducting and hydrogen-electric demonstrators aligned with the EU’s 2050 net-zero commitment. EASA’s harmonized eVTOL rule-set and national R&D grants propel a pipeline of certification campaigns. Stringent carbon taxes and airport slot incentives make electric retrofits financially attractive, sustaining healthy demand amid macroeconomic headwinds. Altogether, geographic dynamics ensure a balanced yet competitive growth canvas for the aircraft electric motors market over the forecast horizon.

Competitive Landscape

The aircraft electric motors market remains moderately fragmented, with key players such as Moog Inc., Safran SA, and Meggitt PLC holding significant positions in the market. Collins earmarked USD 3 billion for electrification, and Safran secured the first EASA-approved flight motor, feats that amplify brand credibility among risk-averse OEMs. Their certification muscle and aftermarket footprint grant pricing leverage; nonetheless, disruptive entrants seize ground by out-innovating on power density and cost.

H3X’s 12 kW/kg continuous metric, YASA’s 550 kW lightweight marvel, and Evolito’s dual-rotor axial-flux modules reset engineering baselines, appealing to eVTOL builders who value kilogram-for-kilowatt supremacy. Partnerships proliferate: Honeywell teams with Regal Rexnord on eVTOL drive-train kits, and Vertical Aerospace locks Honeywell as prime motor-controller supplier. Intellectual-property battles loom around superconducting stators and carbon-nanotube windings, shaping future competitive fences.

Market shake-out will likely hinge on sustained capital access, supply-chain resilience for rare-earth substitutes, and navigating multi-jurisdictional certification. Firms that combine scalable manufacturing, field-data feedback loops, and system-level optimization stand poised to consolidate share as the aircraft electric motors market matures into a high-stakes, innovation-driven arena.

Aircraft Electric Motors Industry Leaders

Moog Inc.

AMETEK Inc.

Woodward, Inc.

Meggitt PLC (Parker Hannifin Corporation)

Safran

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: The US Army awarded Electra a USD 1.9 million Small Business Innovation Research (SBIR) contract to advance hybrid-electric powertrain, power, and propulsion systems (HEPPS). This partnership will explore the operational benefits of hybrid-electric propulsion, including reduced fuel demand, extended range, and enhanced mission capabilities for current and future aircraft.

- June 2025: Unusual Machines Inc. signed a definitive agreement to acquire Rotor Lab Pty Ltd, an Australian company specializing in electric motors and propulsion systems for unmanned aerial systems (UAS). The USD 7 million all-equity deal (including a USD 3 million earnout) will strengthen UMAC’s commercial and defense drone market position.

Global Aircraft Electric Motors Market Report Scope

| AC Motor | Induction Motors |

| Synchronous Motors | |

| DC Motor | Brushed DC Motors |

| Brushless DC Motors | |

| Stepper Motors |

| Up to 10 kW |

| 10 to 200 kW |

| Above 200 kW |

| Propulsion Control Systems |

| Environmental Control Systems |

| Avionics Systems |

| Door Actuation Systems |

| Landing Gear and Braking Systems |

| Others |

| Fixed-Wing Aircraft | Commercial | Narrowbody |

| Widebody | ||

| Regional Jets | ||

| Business Jets | ||

| Piston and Turboprop | ||

| Military | Fighter Jets | |

| Transport Aircraft | ||

| Special-Mission Aircraft | ||

| Rotorcraft | Civil Helicopters | |

| Military Helicopters | ||

| Unmanned Aerial Vehicles (UAVs) | ||

| Advanced Air Mobility (AAM) | ||

| Original Equipment Manufacturer |

| Aftermarket/MRO |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Motor Type | AC Motor | Induction Motors | |

| Synchronous Motors | |||

| DC Motor | Brushed DC Motors | ||

| Brushless DC Motors | |||

| Stepper Motors | |||

| By Output Power | Up to 10 kW | ||

| 10 to 200 kW | |||

| Above 200 kW | |||

| By Application | Propulsion Control Systems | ||

| Environmental Control Systems | |||

| Avionics Systems | |||

| Door Actuation Systems | |||

| Landing Gear and Braking Systems | |||

| Others | |||

| By Aircraft Type | Fixed-Wing Aircraft | Commercial | Narrowbody |

| Widebody | |||

| Regional Jets | |||

| Business Jets | |||

| Piston and Turboprop | |||

| Military | Fighter Jets | ||

| Transport Aircraft | |||

| Special-Mission Aircraft | |||

| Rotorcraft | Civil Helicopters | ||

| Military Helicopters | |||

| Unmanned Aerial Vehicles (UAVs) | |||

| Advanced Air Mobility (AAM) | |||

| By End-Use | Original Equipment Manufacturer | ||

| Aftermarket/MRO | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the aircraft electric motors market in 2030?

The aircraft electric motors market size reached USD 10.04 billion in 2025 and is forecasted to advance to USD 15.17 billion by 2030, translating into an 8.61% CAGR.

Which application will grow fastest through 2030?

Avionics systems are expected to post the highest 9.78% CAGR as fly-by-wire becomes standard.

Why are axial-flux motors gaining traction?

They offer exceptional power-to-weight ratios, with recent records such as 550 kW at 13 kg, suiting eVTOL and hybrid aircraft needs.

How will rare-earth supply risks influence suppliers?

They encourage adoption of wound-field or rare-earth-lean designs and could shift sourcing toward regions outside China by 2027.

Which region shows the strongest growth outlook?

Asia-Pacific leads with a projected 9.98% CAGR, driven by rising airline demand and UAV proliferation.

What certification hurdles face electric propulsion developers?

Extended DO-160 and DO-178C compliance cycles add two to three years to programs, increasing cost and time to market.

Page last updated on: