Aircraft Fuel Cell Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

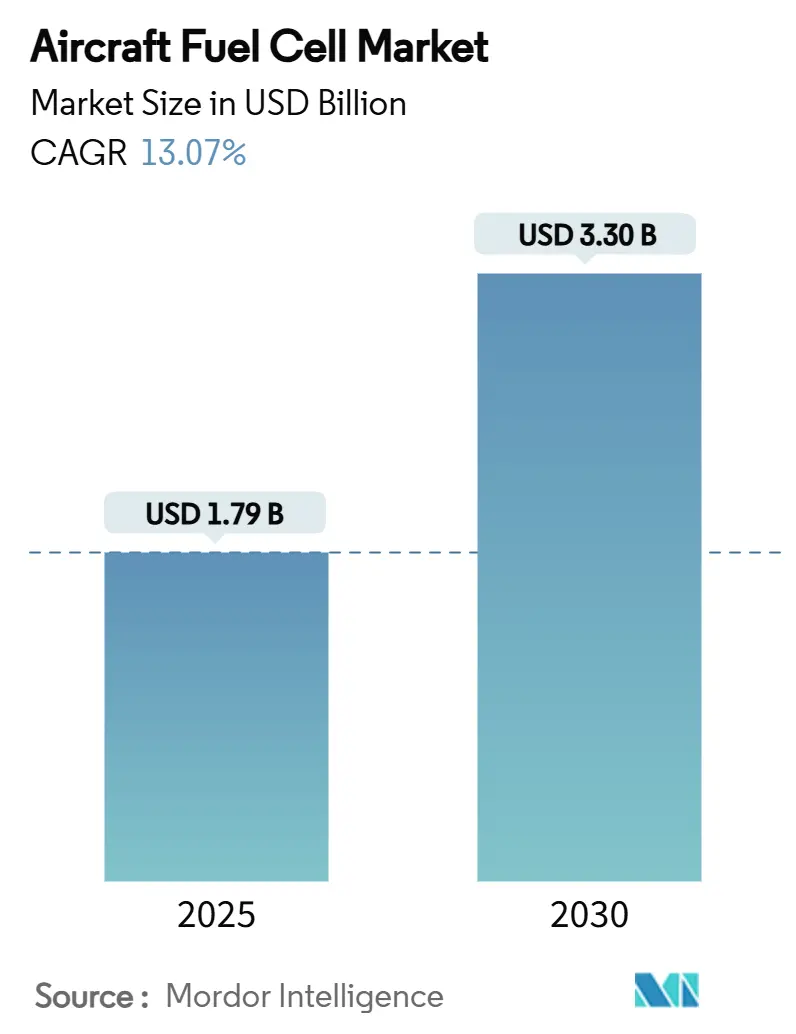

| Market Size (2025) | USD 1.79 Billion |

| Market Size (2030) | USD 3.30 Billion |

| Growth Rate (2025 - 2030) | 13.07% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Fuel Cell Market Analysis by Mordor Intelligence

The aircraft fuel cell market size is estimated at USD 1.79 billion in 2025, and is expected to reach USD 3.30 billion by 2030, advancing at a 13.07% CAGR over the period. Heightened pressure to decarbonize aviation, rising private capital flows into hydrogen-electric programs, and rapid progress in airport refueling infrastructure keep demand for fuel-cell propulsion on a firm upward path. Developers now demonstrate multi-hundred-kilowatt stacks, while certification agencies publish technology-agnostic safety rules that shorten time-to-market. Strategic alliances between airframers and hydrogen specialists are reshaping supply chains, and the first hydrogen-ready commercial routes are penciled in for the second half of the decade. Against this backdrop, the aircraft fuel cell market is shifting from experimental testing toward serial production of propulsion-grade systems.

Key Report Takeaways

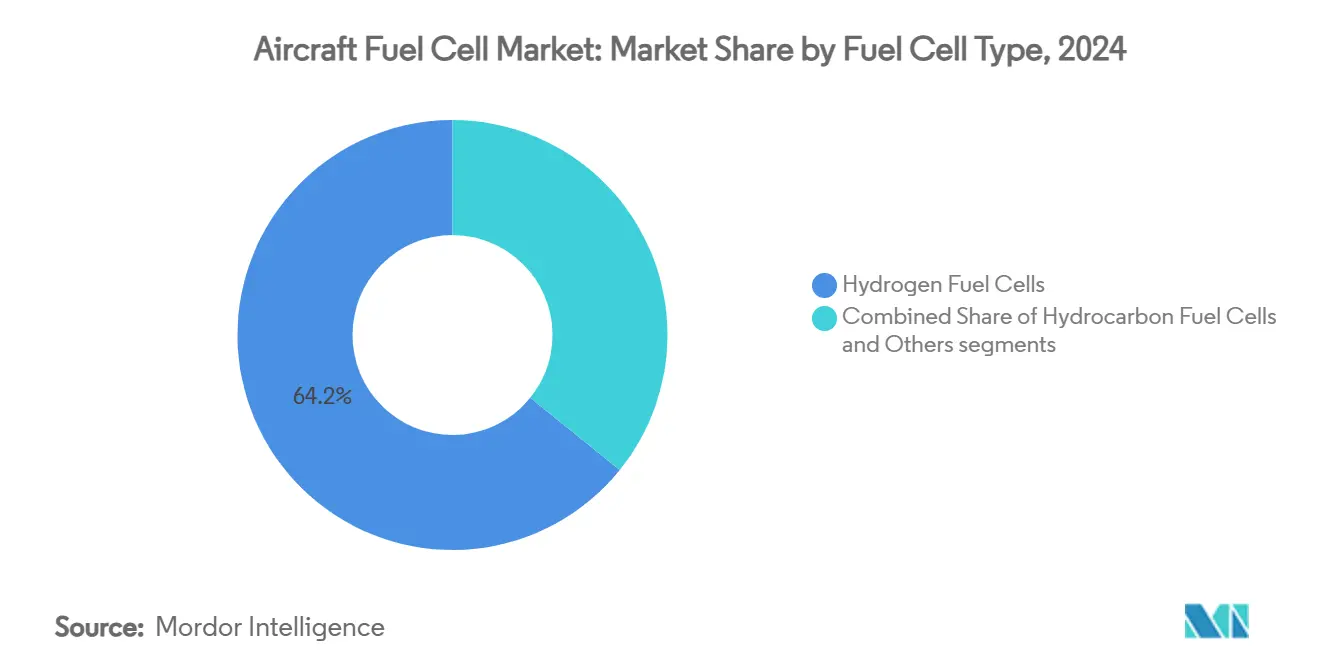

- By fuel-cell type, hydrogen cells captured a 64.20% share of the aircraft fuel cell market size in 2024 and are expanding at a 17.45% CAGR.

- By platform, unmanned aerial systems led with 30.01% of the aircraft fuel cell market share in 2024, while advanced air mobility platforms registered the highest 20.23% CAGR through 2030.

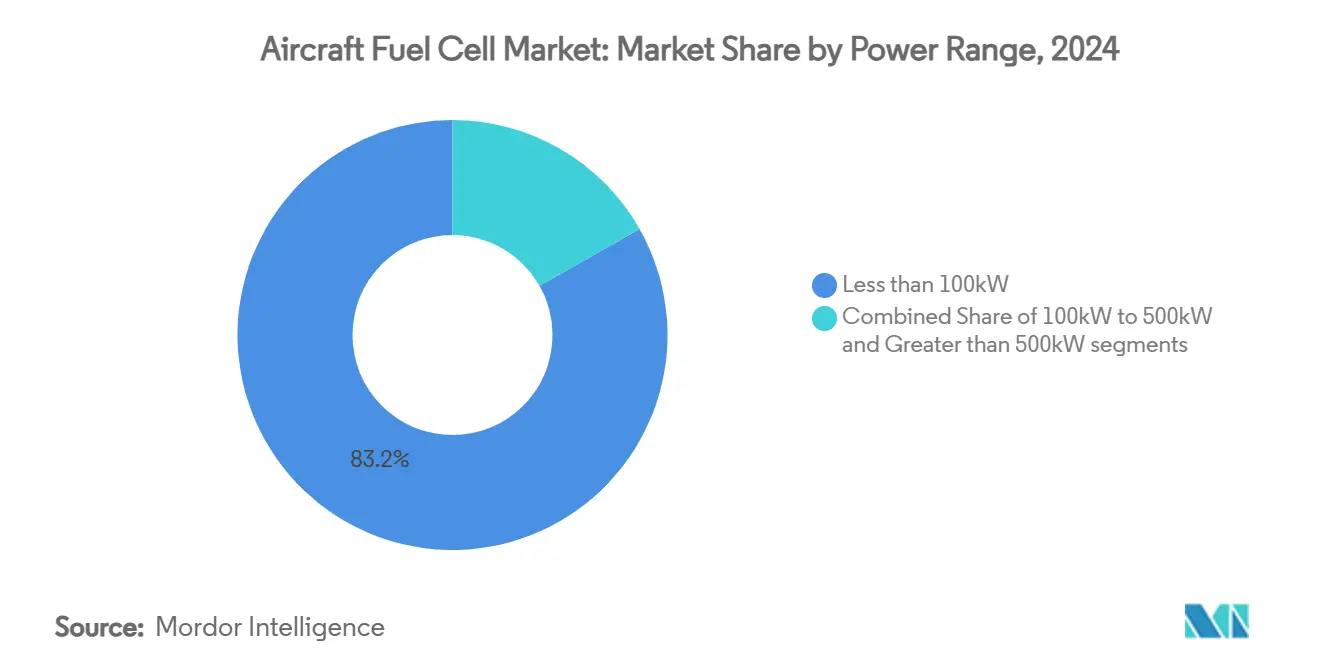

- By power range, systems under 100 kW accounted for 83.21% of the aircraft fuel cell market in 2024; the 100 kW to 500 kW class is growing fastest at an 18.76% CAGR.

- By application, propulsion systems held a 61.77% share of the aircraft fuel cell market in 2024 and will rise at a 21.98% CAGR.

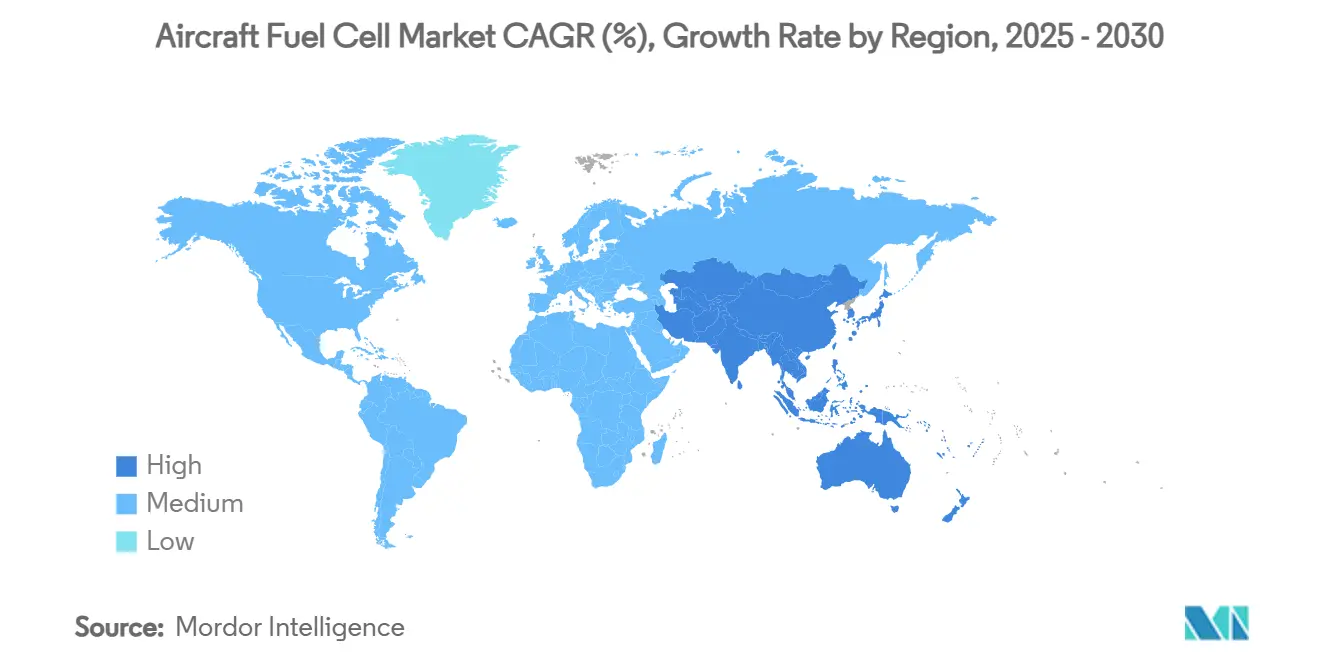

- By geography, North America commanded 31.56% of the aircraft fuel cell market share in 2024, whereas Asia-Pacific delivered the strongest 16.89% CAGR to 2030.

Global Aircraft Fuel Cell Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening global emissions regulations driving zero-emission propulsion solutions | +2.1% | EU and North America | Medium term (2-4 years) |

| Accelerated investment in hydrogen-powered aviation research and development | +1.8% | North America and EU; spill-over Asia-Pacific | Long term (≥ 4 years) |

| Fuel cells preferred over batteries for mid-range aircraft due to weight efficiency | +1.5% | Global | Medium term (2-4 years) |

| Advancements in fuel cell power density and lightweight composite components | +1.3% | Germany, US, Japan | Long term (≥ 4 years) |

| Growing demand for low-acoustic signature propulsion in ISR and cargo UAVs | +0.9% | Global defense markets | Short term (≤ 2 years) |

| Emergence of hydrogen refueling infrastructure at airports supporting aviation use cases | +1.1% | Europe leading | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening Global Emissions Regulations Driving Zero-Emission Propulsion Solutions

The European Union’s ReFuelEU mandate pushes carriers toward 2% sustainable aviation fuel in 2025, scaling up to 63% by mid-century, and positions zero-emission aircraft as an attractive compliance pathway.[1] European Union, “ReFuelEU Aviation Regulation,” europa.eu FAA rule 14 CFR 31.45 formally sets safety requirements for airborne fuel cells, signalling regulator readiness to clear commercial hydrogen flights.[2]Federal Aviation Administration, “14 CFR 31.45—Fuel Cells,” ecfr.gov EASA Opinion 04/2024 further eases adoption by outlining technology-neutral electric and hybrid propulsion certification. Carbon pricing regimes strengthen the business case, and airlines project that meeting long-run climate targets without fuel-cell propulsion will be economically daunting. Collectively, these measures lift demand for hydrogen powertrains and accelerate program launches across the aircraft fuel cell market.

Accelerated Investment in Hydrogen-Powered Aviation Research and Development

Private and public funding for hydrogen aviation reached new highs 2025 as Universal Hydrogen closed a USD 85.5 million round led by strategic carriers and engine OEMs. Government grants such as the EUR 73 million (USD 85.37 million) Dutch package for Conscious Aerospace and German support for the BALIS 2.0 project position Europe as a technology launchpad. NASA’s planned cryogenic hydrogen test complex underlines the US resolve to dominate next-generation propulsion. Capital inflows help niche fuel-cell specialists scale production tooling, win supplemental-type certificates, and bid on whole-aircraft programs. The resulting innovation flywheel keeps the aircraft fuel cell market on a high-growth trajectory and lowers cost barriers for future entrants.

Fuel Cells Preferred Over Batteries for Mid-Range Aircraft Due to Weight Efficiency

Hydrogen systems deliver near-1,500 Wh/kg versus lithium-ion's (Li-ion's) 300–400 Wh/kg, enabling three-to-five-hour missions without payload sacrifice. Flight tests like Joby Aviation's 523-mile hydrogen-electric sortie confirm real-world range benefits. Intelligent Energy's 1.5 kW/kg stack allows quick throttle response critical for flight operations. Manufacturers targeting 9-to-19-seat commuter aircraft state that batteries would exceed the allowable maximum take-off weight, whereas fuel-cell packs fit well within structural margins. Weight advantages therefore tilt product-roadmap decisions toward hydrogen and reinforce scale economies for the aircraft fuel cell market over the forecast horizon.

Advancements in Fuel Cell Power Density and Lightweight Composite Components

H3 Dynamics certified a 400 kW aviation stack in 2025, marking a near-five-fold jump in power from 2023 levels. PowerCell’s low-temperature plates cut cooling loads by 30%, trimming system mass and improving climb performance. Florida State University researchers achieved a 0.62 gravimetric index for cryogenic tanks through carbon-fiber composites—meaning 62% of total system weight is usable hydrogen. Cryomotive’s cryo-compressed concept promises densification advantages that slash refueling downtime. Each breakthrough converges to lift power-to-weight ratios, shrink fuselage integration volumes, and keep the aircraft fuel cell market on track for certification of megawatt-class propulsion within ten years.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of fuel cell stacks and balance-of-plant compared to conventional APUs | -1.9% | Global | Medium term (2-4 years) |

| Limited availability of liquid hydrogen infrastructure at global airports | -1.6% | Global | Long term (≥ 4 years) |

| Regulatory and certification uncertainty for cryogenic hydrogen systems in aviation | -1.2% | Global | Medium term (2-4 years) |

| Complex thermal management requirements at high-altitude operating conditions | -0.8% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Fuel Cell Stacks and Balance-of-Plant Compared to Conventional APUs

Aviation-grade stacks still require precious metal catalysts and tight-tolerance machining, which push capital costs to three to five times traditional APUs. Balance-of-plant items—cryogenic tanks, compressors, and power conditioners—lack commodity supply chains, limiting bulk discounts. Airbus testing on an A330 platform shows that the cost per installed kilowatt remains uncompetitive for high-cycle operators absent volume production. While long-term fuel savings partly offset outlay, airlines face multi-year payback horizons that inhibit procurement decisions. Until gigafactories ramp and platinum loadings decline, cost barriers will temper upside for the aircraft fuel cell market.

Limited Availability of Liquid Hydrogen Infrastructure at Global Airports

Fewer than 50 airports worldwide can handle gaseous hydrogen; even fewer support liquid bunkering. Regional carriers with thin route networks hesitate to order hydrogen aircraft without a guaranteed fuel supply. Building cryogenic storage, vapour-handling lines, and safety systems often exceeds USD 100 million, discouraging smaller hubs. Infrastructure concentration in Europe and North America curtails operational flexibility in emerging markets, creating lost utilization hours. Coordinated multi-stakeholder investment is critical for unlocking the complete aircraft fuel cell market potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fuel Cell Type: Hydrogen Dominates Technology Landscape

Hydrogen systems captured 64.20% of the aircraft fuel cell market in 2024 and will advance at a robust 17.45% CAGR, reflecting superior gravimetric energy density and zero-carbon exhaust. The aircraft fuel cell market size associated with hydrogen units is forecasted to witness more than 2x growth by 2030 as stack durability exceeds 20,000 flight hours and liquid-hydrogen tanks are certified for 30-year lifetimes. In response, OEMs, including Airbus and Universal Hydrogen, continue ground and flight demos that target type certification by 2028.

Hydrocarbon reforming cells, solid-oxide variants, and direct-methanol units retain a niche foothold for operators lacking hydrogen infrastructure. Lockheed Martin’s Stalker UAS leverages solid-oxide technology for long-loiter military missions. Yet as green hydrogen costs slide below USD 2/kg and airport bunkering spreads, most new-build programs pivot toward hydrogen, cementing its strategic primacy within the aircraft fuel cell market.

By Platform Type: UAV Leadership Yields to eVTOL Growth

Unmanned aerial systems held a 30.01% share of the aircraft fuel cell market in 2024, owing to early defense adoption and lower certification hurdles. Advanced air mobility craft are expanding fastest at a 20.23% CAGR, supported by urban-air-mobility demand curves and multi-megawatt stack road maps from developers like H3 Dynamics. The aircraft fuel cell market size servicing eVTOL fleets could overtake UAV spending by 2029 if city-pair routes obtain air traffic approval.

Commercial narrowbody programs remain in concept phase but attract sizable R&D budgets under Airbus’s ZEROe architecture. Military fixed-wing transport and rotorcraft procurements add stable baseline demand, while general aviation conversions provide retrofit opportunities. Overall, platform diversification spreads revenue risk and underpins the long-term resilience of the aircraft fuel cell market.

By Power Range: Small Systems Lead, Mid-Range Accelerates

Sub-100 kW stacks commanded 83.21% of the aircraft fuel cell market share in 2024 because most fielded UAVs and prototype eVTOLs fall inside this envelope. However, systems rated 100 kW to 500 kW post an 18.76% CAGR as regional airliners and cargo drones transition from demonstrators to commercial certification. This band's aircraft fuel cell market size benefits from economies of scale, where stack architecture is modular and can be paralleled for higher power.

Beyond 500 kW, megawatt-class solutions appear in flight-test pipelines; Airbus bench-tested a 1.2 MW installation in early 2025. Though capital-intensive, high-power platforms unlock single-aisle and wide-body segments. Graduated progress across power classes builds a sequential adoption path that keeps the aircraft fuel cell market upward throughout the forecast period.

By Application: Propulsion Systems Drive Market Expansion

Propulsion captured 61.77% of the aircraft fuel cell market share in 2024 and will rise at a 21.98% CAGR, underscoring the pivot from auxiliary to primary power. Once the green hydrogen supply stabilises, airlines view stack-based engines as the most direct route to zero-carbon operations. Correspondingly, the aircraft fuel cell market size linked to propulsion is forecast to triple by 2030 as airlines firm up conditional purchase agreements.

Auxiliary power units (APUs) constitute the initial commercial niche because they sidestep main-engine certainties and can be installed during heavy checks. Secondary uses such as emergency electrical supply and cabin conditioning broaden stack demand but remain secondary revenue streams. Propulsion’s dominance is thus expected to persist for the entire outlook, anchoring growth prospects for the aircraft fuel cell market.

Geography Analysis

North America led the aircraft fuel cell market with a 31.56% share in 2024, buoyed by FAA regulatory clarity, a deep aerospace manufacturing base, and anchor investments from airlines like American Airlines, which conditionally ordered 100 ZeroAvia engines.[3]American Airlines, “Hydrogen-Electric Engine Order,” aa.com Venture capital networks funnel capital to Californian and Washington-state start-ups, while NASA’s proposed cryogenic hydrogen test complex gives US firms preferential access to infrastructure. Canada also contributes first-in-class piloted hydrogen VTOL demos, widening the regional innovation footprint.

Asia-Pacific is the fastest-growing territory, with a 16.89% CAGR through 2030, as Japan, South Korea, and China roll out hydrogen road maps and mandate sustainable aviation fuel blends. Itochu’s strategic investment in ZeroAvia integrates Japanese trading-house logistics expertise with propulsion know-how, smoothing supply-chain bottlenecks.[4] ZeroAvia, “Itochu Investment Announcement,” zeroavia.com Regional electronics and composite manufacturing hubs in Shenzhen and Incheon help localise stack production, reducing unit costs and lifting adoption in commuter aircraft markets.

Europe maintains a commanding innovation and policy role, propelled by stringent emission ceilings and robust public funding. EASA Opinion 04/2024 de-risks certification for non-conventional engines. Projects such as GOLIAT demonstrate liquid-hydrogen servicing at Hamburg and Toulouse airports, paving operational pathways. German government-backed BALIS 2.0 advances high-power stacks toward 2028 readiness, while the Netherlands supports component validation via GKN test rigs. Despite slower aggregate GDP growth, these initiatives keep Europe influential within the aircraft fuel cell market.

Competitive Landscape

The aircraft fuel cell market exhibits moderate fragmentation but is moving toward higher concentration as aerospace majors ink exclusivity agreements with specialist stack makers. Airbus and ElringKlinger operate Aerostack to co-develop megawatt modules, while Boeing partners with Plug Power on cryogenic supply. ZeroAvia secures provisional type-cert for its 600 kW engine, giving it a first-mover edge. Universal Hydrogen focuses on modular tank-in-capsule logistics that ease fleet retrofits.

Three competitive archetypes emerge. First, incumbent airframers acquire minority stakes in fuel-cell labs to lock up IP. Second, pure-play stack companies leverage agile R&D and pursue supplemental-type certificates for retrofit programs. Third, energy companies like ENEOS enter via upstream hydrogen contracts, offering bundled fuel-plus-propulsion packages. Technology differentiation centers on power density, start-up reliability, and integrated thermal management.

Standardization efforts like SAE AIR8466 equalize basic safety requirements, gradually commoditizing hardware interfaces. In response, firms race to secure exclusive airport fuelling concessions or proprietary digital-twin maintenance software. Patent portfolios around liquid-hydrogen tank geometry and catalyst coatings become key defensive moats. Overall, competitive intensity accelerates, yet high capital demands raise entry barriers and push the aircraft fuel cell market toward an oligopoly by 2030.

Aircraft Fuel Cell Industry Leaders

Ballard Power Systems Inc.

ZeroAvia, Inc.

Plug Power Inc.

Intelligent Energy Limited

Airbus SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: GKN Aerospace partnered with Airbus in ICEFlight to trial cryogenic hydrogen systems in the Netherlands.

- June 2025: Airbus and MTU Aero Engines signed a Memorandum of Understanding to develop hydrogen fuel cell propulsion systems for future aircraft jointly. This collaboration combines Airbus' ZEROe initiative with MTU's Flying Fuel Cell concept.

Global Aircraft Fuel Cell Market Report Scope

| Hydrogen Fuel Cells |

| Hydrocarbon Fuel Cells |

| Others |

| Commecial Aviation | Narrowbody |

| Widebody | |

| Regional Jets | |

| Military Aviation | Combat |

| Transport | |

| Special Mission | |

| Helicopters | |

| General Aviation | Business Jets |

| Commercial Helicopters | |

| Piston and Turboprop | |

| Unmanned Aerial Systems | Civil and Commercial |

| Defense and Government | |

| Advance Air Mobility | eVTOL |

| Urban Air Mobility (UAM) |

| Less than 100kW |

| 100kW to 500kW |

| Greater than 500kW |

| Propulsion |

| Auxiliary Power Unit (APU) |

| On-board Electrical Systems |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Fuel Cell Type | Hydrogen Fuel Cells | ||

| Hydrocarbon Fuel Cells | |||

| Others | |||

| By Platform Type | Commecial Aviation | Narrowbody | |

| Widebody | |||

| Regional Jets | |||

| Military Aviation | Combat | ||

| Transport | |||

| Special Mission | |||

| Helicopters | |||

| General Aviation | Business Jets | ||

| Commercial Helicopters | |||

| Piston and Turboprop | |||

| Unmanned Aerial Systems | Civil and Commercial | ||

| Defense and Government | |||

| Advance Air Mobility | eVTOL | ||

| Urban Air Mobility (UAM) | |||

| By Power Range | Less than 100kW | ||

| 100kW to 500kW | |||

| Greater than 500kW | |||

| By Application | Propulsion | ||

| Auxiliary Power Unit (APU) | |||

| On-board Electrical Systems | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value and predicted growth rate of the aircraft fuel cell market?

The aircraft fuel cell market size is USD 1.79 billion in 2025 and is set to climb to USD 3.3 billion by 2030 at a 13.07% CAGR.

Which region dominates aircraft fuel cell adoption today?

North America leads with 31.56% market share in 2024, supported by clear FAA regulations and significant airline commitments.

Why are hydrogen fuel cells preferred over batteries for mid-range aircraft?

Hydrogen systems deliver about 1,500 Wh/kg energy density versus batteries’ 400 Wh/kg, enabling longer range without payload penalties.

What power range segment is expanding the fastest?

The 100 kW to 500 kW class registers an 18.76% CAGR as eVTOL and regional aircraft projects transition from prototypes to certification.

What is the main bottleneck constraining large-scale deployment?

Limited liquid-hydrogen infrastructure at airports remains the chief hurdle, with fewer than 50 locations worldwide equipped for refueling.

Page last updated on: