Aircraft Auxiliary Power Unit Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.19 Billion |

| Market Size (2031) | USD 3.81 Billion |

| Growth Rate (2026 - 2031) | 3.59% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

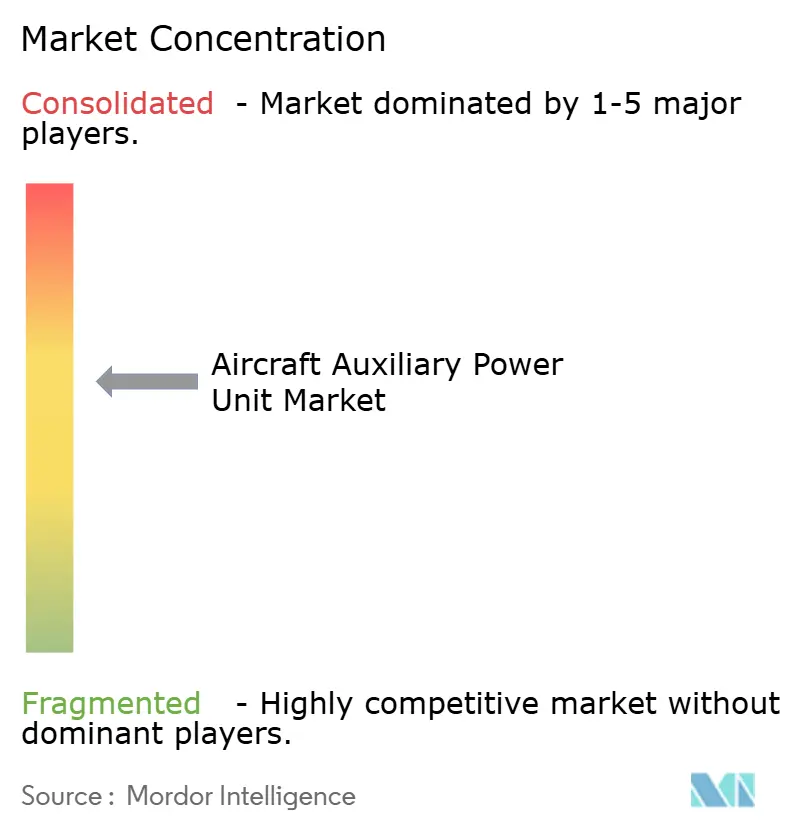

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Auxiliary Power Unit Market Analysis by Mordor Intelligence

The aircraft auxiliary power unit (APU) market size is expected to grow from USD 3.08 billion in 2025 to USD 3.19 billion in 2026 and is forecast to reach USD 3.81 billion by 2031 at 3.59% CAGR over 2026-2031. Moderate expansion stems from airlines shifting toward electrified and hydrogen-ready systems while regulators tighten ground-emissions rules that favor gate-supplied electricity over onboard APUs. Airports enforcing APU-off policies cut ramp emissions up to 50% whenever fixed electrical ground power is available. Commercial airlines command volume through single-aisle deliveries, militaries accelerate technology needs in rotary-wing upgrades, and rising UAV procurement widens demand for micro-rated units. Fuel-cell prototypes gain momentum as Airbus validates hydrogen APUs and Honeywell races to certify 100% sustainable aviation fuel across its conventional line. Meanwhile, supply chain exposure to rare-earth restrictions forces Western OEMs to redesign generators and diversify sourcing.

Key Report Takeaways

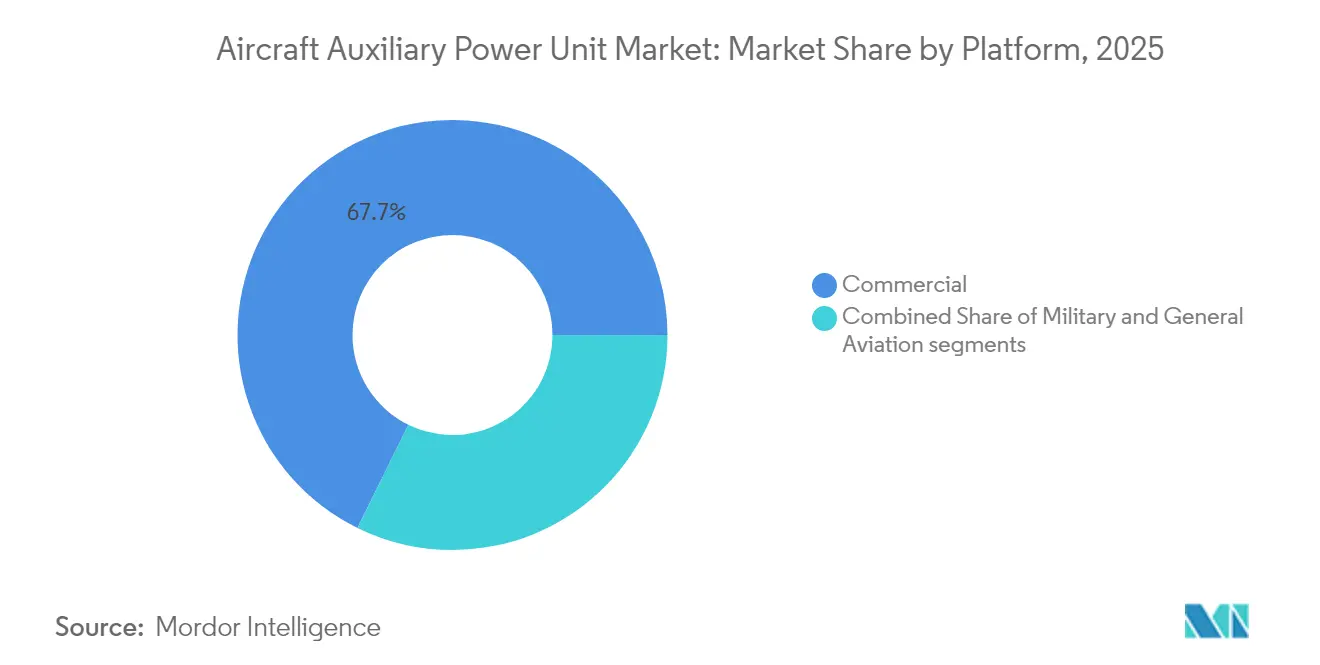

- By platform, commercial aviation led with 67.72% revenue share in 2025, while the military segment is projected to expand at 4.55% CAGR through 2031.

- By aircraft type, fixed-wing platforms accounted for 80.12% of the aircraft auxiliary power unit market share in 2025, and rotary-wing fleets are set to grow at 3.78% CAGR to 2031.

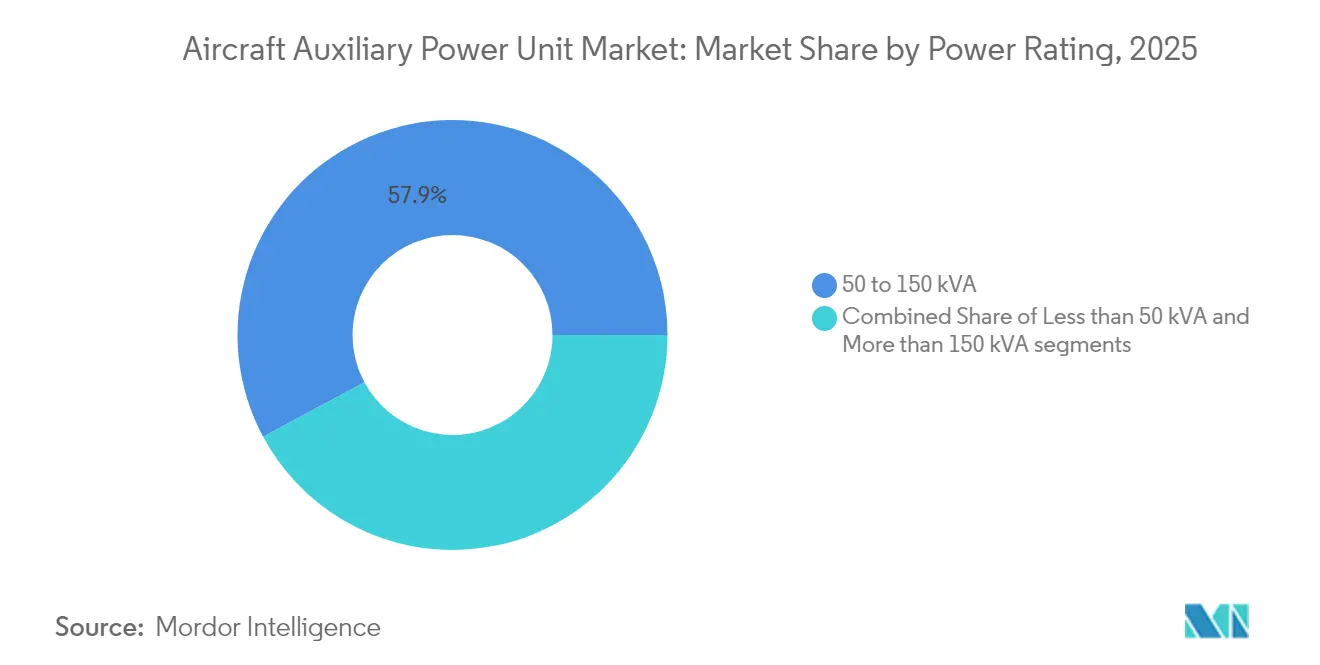

- By power rating, the 50 to 150 kVA class commanded a 57.85% share of the aircraft auxiliary power unit market in 2025, whereas less than 50 kVA units are forecasted to rise at a 5.23% CAGR.

- By technology, conventional turboshaft systems remained dominant, with a 89.62% share in 2025, but fuel-cell solutions are pacing the field at a 6.03% CAGR.

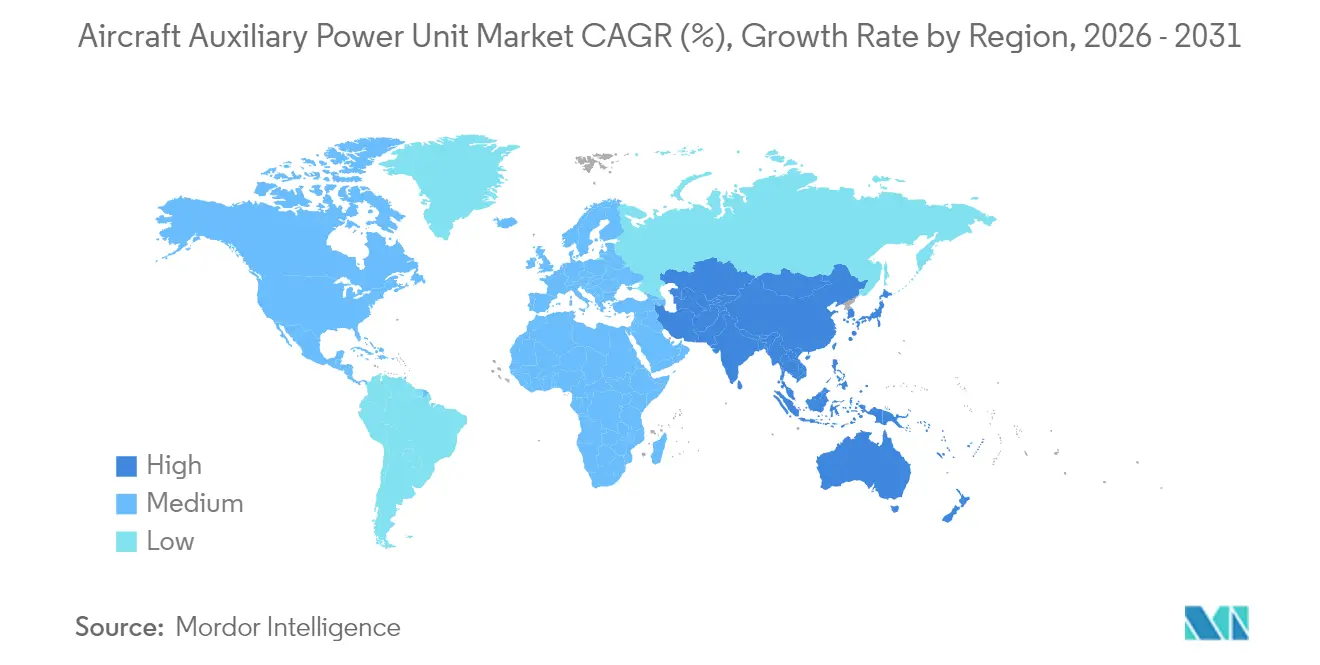

- By region, North America captured 32.35% revenue in 2025 and Asia-Pacific is advancing fastest at 5.22% CAGR on the back of the C919 and Indian fleet expansion programs.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aircraft Auxiliary Power Unit Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased deliveries of next-gen fuel-efficient narrowbody aircraft | +0.8% | North America, Asia-Pacific | Medium term (2–4 years) |

| Rising retrofit activity due to regulatory mandates on APU-off operations | +0.6% | Europe, North America | Short term (≤ 2 years) |

| Expansion of military UAV fleets in high-threat environments | +0.4% | North America, Europe, Middle East | Long term (≥ 4 years) |

| Electrification of ground operations driving adoption of e-APUs | +0.5% | Europe, North America | Medium term (2–4 years) |

| Emergence of commercial spaceplanes creating demand for micro-APUs | +0.2% | North America, Europe | Long term (≥ 4 years) |

| Integration of APUs into hybrid-electric propulsion architectures | +0.3% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increased Deliveries of Next-Gen Fuel-Efficient Narrowbody Aircraft

China’s commercial fleet is expected to double to 9,740 aircraft by 2043, underscoring the sustained demand for APUs optimized for single-aisle operations. Airlines such as Air Arabia selected 131 Honeywell 131-9A units for A320neo aircraft to secure 1-2% fuel savings in High Efficiency Mode.[1]Honeywell, “Air Arabia Selects 131-9A Auxiliary Power Units,” honeywell.com Compact architectures emphasizing rapid starts and minimal thermal loads suit higher-cycle narrowbody schedules. Synergies with LEAP engines enhance dispatch reliability as carriers replace legacy CFM56 fleets. This delivery wave underpins line-fit revenue and a growing spares pipeline for the aircraft auxiliary power unit market.

Rising Retrofit Activity Due to Regulatory APU-Off Mandates

European hubs now enforce electrical ground power use during turnarounds, forcing carriers to upgrade legacy jets with compatible interface kits rather than procure new APUs. Qatar Airways secured the region’s first HGT1700 overhaul capacity to cut compliance costs while extending asset life. Assaia’s ramp-monitoring analytics enable airports to validate APU-off adherence, converting voluntary eco-measures into compulsory upgrades. As a result, aftermarket margins rise even as original-equipment volumes plateau, offering attractive service income for established suppliers.

Expansion of Military UAV Fleets in High-Threat Environments

Allied defense agencies fund micro-APU programs that operate under low thermal and acoustic signatures to support stealth UAV missions. Rheinmetall’s memorandum with Honeywell for tactical vehicle APUs illustrates cross-domain integration of auxiliary power technologies. Safran’s role in the US Army’s Future Long Range Assault Aircraft electrical system demonstrates how demanding battlefield conditions spur innovation, feeding dual-use benefits into commercial designs.

Electrification of Ground Operations Driving Adoption of e-APUs

Collins Aerospace budgeted USD 3 billion for electrification, positioning its battery-based e-APUs as airports lock in zero-emission targets. Battery packs remove ramp emissions and slash noise, though adoption hinges on density improvements and on-stand charging installations. Honeywell’s partnership with Vertical Aerospace proves that lessons from eVTOL propulsion cascade into traditional short-haul aircraft. Although premium pricing remains a hurdle, early adopters signal a viable market niche for high-cycle short-range fleets.

Restraints Impact Analysis*

| Restratin | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price instability of rare-earth materials used in generator components | -0.7% | North America, Europe | Short term (≤ 2 years) |

| Preference for airport ground power units reducing APU operating hours | -0.9% | Europe, North America | Medium term (2–4 years) |

| Lengthy and rigid certification processes for new-energy APU technologies | -0.5% | Global, with stricter requirements in North America and Europe | Long term (≥ 4 years) |

| Thermal management challenges in compact aircraft APU designs | -0.4% | Global, with particular impact on narrowbody and UAV segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Instability of Rare-Earth Materials Used in Generator Components

China’s export curbs on neodymium and dysprosium inflate magnet costs, creating pricing uncertainty for APU permanent-magnet generators. US Air Force analyses list rare-earth dependence among top aerospace supply vulnerabilities, prompting OEMs to explore recycling and ferrite-based designs that may compromise power density. Contract pricing is now indexed to commodity exposure, affecting long-term maintenance agreements and eroding margins across the aircraft auxiliary power unit market.

Preference for Airport Ground Power Units Reducing APU Operating Hours

Gate-supplied 400 Hz electricity delivers up to sixfold energy efficiency compared with onboard APUs. Zurich Airport estimates per-hour savings exceeding CHF 600 when airlines rely on fixed electrical ground power.[2]Zurich Airport, “Ground Power and Pre-Conditioned Air Study,” zurich-airport.com This operating shift trims APU cycles, extends overhaul intervals, and depresses replacement volume. Manufacturers respond with higher-efficiency turboshafts to justify onboard generation in remote gates lacking fixed power, but infrastructure expansion continues to erode long-term demand growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Commercial Dominance Mirrors Global Fleet Growth

The commercial segment generated 67.72% of 2025 revenue and retains the backbone of the aircraft auxiliary power unit market. Line-fit demand matches Airbus and Boeing production ramps, while airlines pursue APU refurbishments instead of replacements to meet emission rules. Military platforms contribute a smaller base today but accelerate at 4.55% CAGR through 2031 as programs such as US rotary-wing modernization specify higher-output electric systems. This defense tailwind supports technology spillovers into civil variants, sustaining value creation across the aircraft auxiliary power unit industry.

Sustained narrowbody deliveries in Asia and North America anchor volume, whereas widebody jets require higher-rated APUs to power galleys and environmental control packs. On the military side, UAVs and transport aircraft adopt micro-and macro-rated solutions, broadening the application matrix. Business jets form a premium niche valuing rapid spool-up and cabin comfort, generating above-average aftermarket yields.

By Aircraft Type: Fixed-Wing Leads but Rotary-Wing Adoption Climbs

Fixed-wing deliveries kept an 80.12% hold on 2025 shipments, reflecting single-aisle production cycles and freighter conversions. Rotary-wing upgrades add 3.78% CAGR, propelled by programs that embed digital avionics and electronic warfare packages requiring a cleaner electrical supply. Helicopter APUs must fit constrained bays and tolerate vibration, driving miniaturized heat exchangers and variable-speed architectures.

Emerging eVTOL prototypes rely on auxiliary generation for backup power and system redundancy, injecting new design criteria. Fixed-wing fuel-cell trials on Airbus A330 demonstrate how long-range platforms may pivot toward alternative energy once certification hurdles are cleared, setting future demand patterns for the aircraft auxiliary power unit market.

By Power Rating: Mid-Range 50–150 kVA Remains the Sweet Spot

The 50 to 150 kVA bracket captured 57.85% of 2025 revenue because it aligns with A320neo, 737 MAX, and C919 power envelopes. These mid-range systems balance output with weight, reinforcing their dominance in the aircraft auxiliary power unit market. Sub-50 kVA solutions are rising at 5.23% CAGR, buoyed by UAV fleets and regional jet growth.

The more than 150 kVA models address widebody and military ISR platforms needing robust power for galleys, radar, and directed-energy payloads. Clean Aviation’s Integrated Cooling for Power Electronics (ICOPE) advances higher power density, potentially realigning cut-points in future product roadmaps. Segment interplay underscores how fleet composition shifts dictate production and overhaul workloads across the aircraft auxiliary power unit industry.

By Technology: Conventional Turboshaft Prevails as Alternatives Take Shape

Conventional designs commanded a 89.62% share in 2025 due to mature support networks and drop-in SAF compatibility. Fuel-cell units show the fastest climb at 6.03% CAGR, spurred by Airbus ground tests validating hydrogen’s operational feasibility. Battery-electric APUs stay niche in weight-sensitive missions but offer zero-emission taxi benefits on short-haul routes.

Honeywell targets 100% SAF certification this decade, prolonging conventional relevance, while Collins and Safran channel investment into electrical architectures positioned for blended-wing demonstrators. Technology roadmaps straddle parallel tracks, reflecting the transitional nature of the aircraft auxiliary power unit market.

Geography Analysis

North America retained a 32.35% share in 2025, anchored by Boeing deliveries and sustained Pentagon spending that underwrite R&D for next-generation solutions. Government stimulus for domestic critical minerals processing also intends to reduce rare-earth exposure. The aircraft auxiliary power unit market size is forecasted to grow steadily as GTF and LEAP fleets mature and enter heavy maintenance cycles.

Asia-Pacific is the fastest riser at 5.22% CAGR through 2031, driven by China’s C919 rollout and India’s forecast for 19,500 new aircraft by 2043. Joint ventures such as Safran–HAL localize parts production, trimming lead times, and aligning with regional offset mandates. Aftermarket revenues will multiply as the regional fleet reaches 129 USD billion service value by 2043, deepening the aircraft auxiliary power unit market footprint.

Europe leverages policy leadership to push low-emission power units under the Clean Aviation umbrella. Hydrogen infrastructure pilots and stringent APU-off enforcement foster innovation in low-NOx combustion and fuel cells. While ground power prevalence tempers unit sales, it pressures suppliers to deliver ultra-efficient products that satisfy airlines facing tight turnaround and environmental compliance.

Competitive Landscape

The marketplace is moderately consolidated, with Honeywell International Inc., Safran SA, Collins Aerospace, and Pratt & Whitney holding long-term supply positions. Honeywell’s proposed spin-off introduces strategic ambiguity around R&D funding, although its existing portfolio spans commercial and defense niches. Safran invests EUR 1 billion (USD 1.17 billion) in global MRO stations to lock in lifecycle revenue, signaling a shift toward service-led profit pools.

Collins Aerospace allocates USD 3 billion to electrification, seeking early leadership in fuel-cell and battery-hybrid architectures. RTX aligns with JetZero on blended-wing demonstrators, ensuring auxiliary system readiness for radically new airframes.[4]RTX, “JetZero Collaboration Announced,” rtx.com Supplier competition now pivots on emissions metrics, lifecycle cost, and digital health monitoring instead of raw power output.

Supply chain resilience emerges as a differentiator. Western OEMs qualify alternate magnet suppliers and invest in recycling to hedge geopolitical risk. Smaller entrants exploit micro-APU niches for UAVs and spaceplanes, fostering targeted innovation but facing certification and capital barriers. Therefore, the aircraft auxiliary power unit market balances incumbents’ scale with specialized challengers’ agility.

Aircraft Auxiliary Power Unit Industry Leaders

Honeywell International Inc.

RTX Corporation

PBS Group a.s.

JSC SPE Aerosila

Safran SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Bell Textron selected Honeywell International, Inc., to provide the 36-150 APUs for the Army's Future Long Range Assault Aircraft (FLRAA). This variant, currently used in Black Hawk and Apache helicopters, will supply secondary electrical and hydraulic power.

- June 2025: Vietjet Air and Honeywell International, Inc. established a five-year maintenance agreement for Honeywell's 331-350 APUs installed on Vietjet Air's fleet of 30 A330 aircraft.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the aircraft auxiliary power unit market as the value generated by factory-built gas-turbine and emerging electric or fuel-cell APUs that supply pneumatic, hydraulic, and electrical power to fixed-wing and rotary-wing aircraft while the main engines are off. Units integrated in commercial transports, regional jets, business jets, helicopters, military aircraft, and larger UAVs are counted at OEM fitment and during first replacement cycles.

Scope exclusion: portable ground power carts, ground power infrastructure, and APUs installed on land vehicles are outside the current scope.

Segmentation Overview

- By Platform

- Commercial

- Narrowbody Aircraft

- Widebody Aircraft

- Regional Jets

- Military

- Combat

- Special Mission

- Transport

- Trainer

- Unmanned Aerial Vehicles (UAVs)

- General Aviation

- Light Aircraft

- Business Jets

- Helicopters

- Commercial

- By Aircraft Type

- Fixed-Wing

- Rotary-Wing

- By Power Rating

- less than 50 kVA

- 50 to 150 kVA

- more than 150 kVA

- By Technology

- Conventional Turboshaft

- Battery-Electric

- Fuel-Cell

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Qatar

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Multiple interviews with airline engineering managers, tier-one APU suppliers, and MRO planners across North America, Europe, and Asia-Pacific clarified utilization hours, replacement intervals, typical transaction prices, and likely adoption timelines for hybrid units. Targeted surveys with regulatory experts added perspective on APU-off mandates and their effect on ground usage. Insights from these conversations filled data gaps and anchored assumptions derived from secondary material.

Desk Research

Mordor analysts assembled baseline data from open-source authorities such as ICAO fleet registers, IATA traffic statistics, FAA and EASA airworthiness directives, and trade association shipment logs. Aircraft OEM order books, airline annual reports, and SEC 10-Ks enriched production, retirement, and MRO trends, which were then validated with press releases and patent filings on next-generation battery-electric APUs. Subscription datasets like Aviation Week and D&B Hoovers supplied program-level delivery schedules and company financials that helped align price bands. Additional context came from UN Comtrade customs codes for turbine components and Volza shipment data tracing spare-part flows. This list is illustrative; many other public and paid sources informed the desk phase.

Market-Sizing & Forecasting

A top-down fleet reconstruction starts with in-service aircraft counts, annual delivery projections, and historical retirement curves, which are multiplied by platform-specific APU penetration and average selling prices to produce the demand pool. Results are cross-checked through selective bottom-up roll-ups of sampled OEM shipments and channel checks. Key drivers in the multivariate forecast include global revenue passenger kilometers, yearly OEM narrow-body deliveries, mean flight hours per aircraft, regulatory penalties on ground emissions, average overhaul interval, and APU price inflation. An ARIMA model, tuned with these variables and expert consensus, projects value through 2030. Where supplier data are sparse, regional MRO spending proxies are used and reconciled to keep aggregate error within an acceptable range.

Data Validation & Update Cycle

Outputs pass two analyst reviews, variance checks versus independent fleet databases, and stress tests under conservative and accelerated delivery scenarios. Models refresh annually; interim updates trigger if OEM guidance, fuel-price swings, or regulation changes move key variables materially.

Why Our Aircraft Auxiliary Power Unit Baseline Stands Up to Scrutiny

Published estimates often diverge because firms choose different platform mixes, price ladders, and refresh cadences.

Key gap drivers include varying treatment of first-overhaul sales, inclusion of portable ground units, dissimilar currency conversions, and whether electric prototypes are counted or kept in a separate future pool. Mordor reports only certified aircraft APUs and applies constant 2025 dollars, while several publishers inflate with aftermarket mark-ups or aggregate adjacent power sources.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.08 B (2025) | Mordor Intelligence | - |

| USD 6.11 B (2025) | Global Consultancy A | mixes ground carts and applies aggressive ASP escalation |

| USD 3.30 B (2023) | Industry Association B | uses pre-COVID fleet base and excludes rotary-wing retrofits |

These comparisons show that Mordor's disciplined scope selection, variable tracking, and annual refresh deliver a balanced, transparent baseline decision-makers can rely on.

Key Questions Answered in the Report

What is the current size of the aircraft auxiliary power unit market?

The market is valued at USD 3.19 billion in 2026 and is projected to reach USD 3.81 billion by 2031, advancing at a CAGR of 3.59%.

Which segment holds the largest aircraft auxiliary power unit market share?

Commercial aviation led with 67.72% revenue share in 2025, driven by narrowbody aircraft deliveries.

Why are fuel-cell APUs gaining traction?

Hydrogen trials on Airbus A330 aircraft demonstrate zero-emission feasibility and support a 6.03% CAGR forecast for fuel-cell units through 2031.

How are regulatory APU-off mandates affecting the market?

Airports enforcing ground-power usage push airlines to retrofit legacy fleets instead of buying new APUs, boosting high-margin aftermarket services.

Which region is growing fastest?

Asia-Pacific is expanding at 5.22% CAGR due to China’s C919 program and India’s long-term fleet growth outlook.

What are the key risks for APU manufacturers?

Dependence on rare-earth materials and rising ground-power adoption reduce run-time hours, pressuring both supply chains and unit replacement demand.

Page last updated on: