Aircraft Battery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

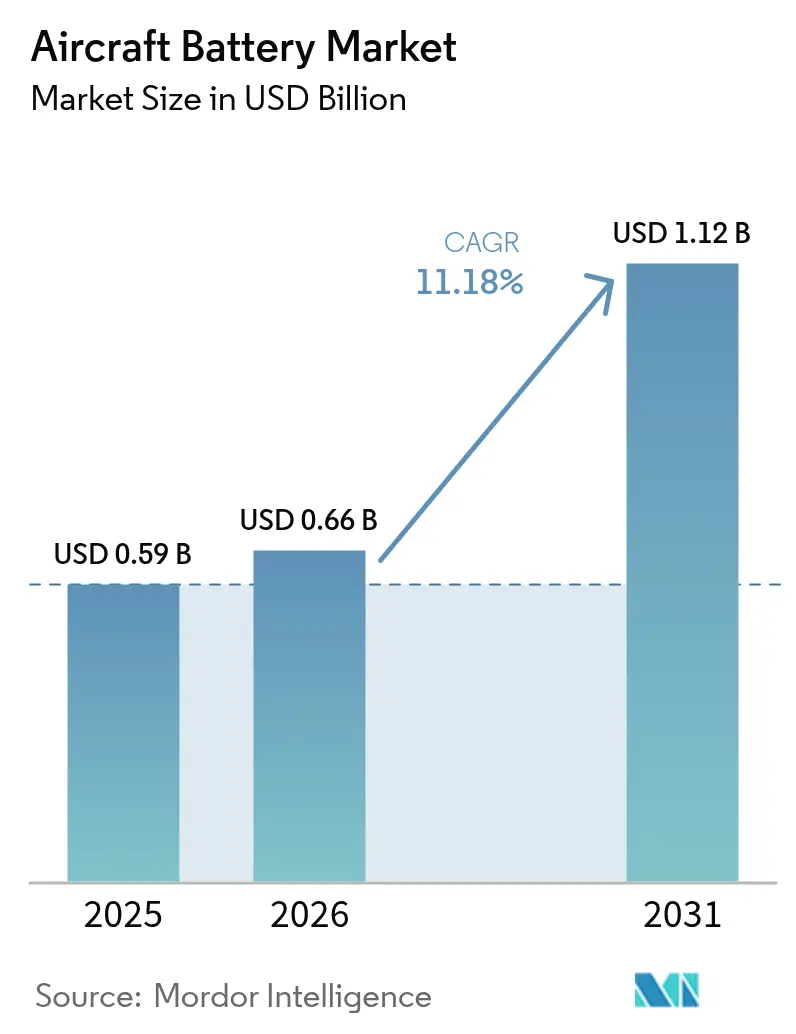

| Market Size (2026) | USD 0.66 Billion |

| Market Size (2031) | USD 1.12 Billion |

| Growth Rate (2026 - 2031) | 11.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Battery Market Analysis by Mordor Intelligence

The aircraft battery market size is expected to grow from USD 0.59 billion in 2025 to USD 0.66 billion in 2026 and is forecast to reach USD 1.12 billion by 2031 at 11.18% CAGR over 2026-2031. Growth rests on airlines and manufacturers moving quickly toward electrified propulsion, regulatory incentives that shorten certification cycles, and sizable venture funding for advanced air-mobility programs. Lithium-based chemistries dominate product strategies, while solid-state and high-rate cells progress from laboratory scale to pilot production. North America retains leadership, yet Asia-Pacific records the strongest growth as China, Japan, and South Korea accelerate low-altitude-economy initiatives. Across platforms, eVTOL and hybrid-electric programs are reshaping supplier relationships, drawing automotive battery leaders into an aviation segment that rewards high energy density and strict safety compliance.

Key Report Takeaways

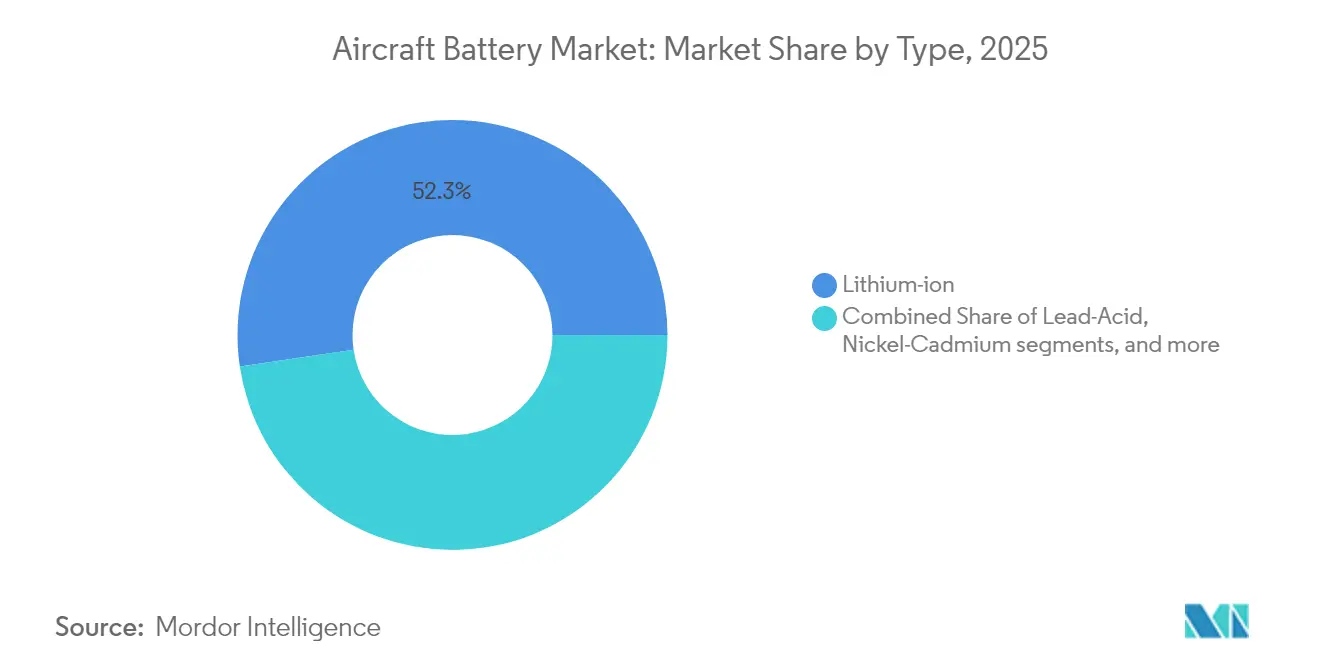

- By battery type, lithium-ion (Li-ion) held 52.34% of the aircraft battery market share in 2025, while lithium-sulfur (Li-S) is projected to expand at a 23.72% CAGR through 2031.

- By application, emergency and backup power systems accounted for 37.85% of the aircraft battery market size in 2025; eVTOL propulsion is poised for a 28.91% CAGR to 2031.

- By aircraft technology, traditional platforms led with a 57.96% revenue share in 2025 in the aircraft battery market, whereas fully electric platforms are forecast to grow at a 29.84% CAGR between 2026 and 2031.

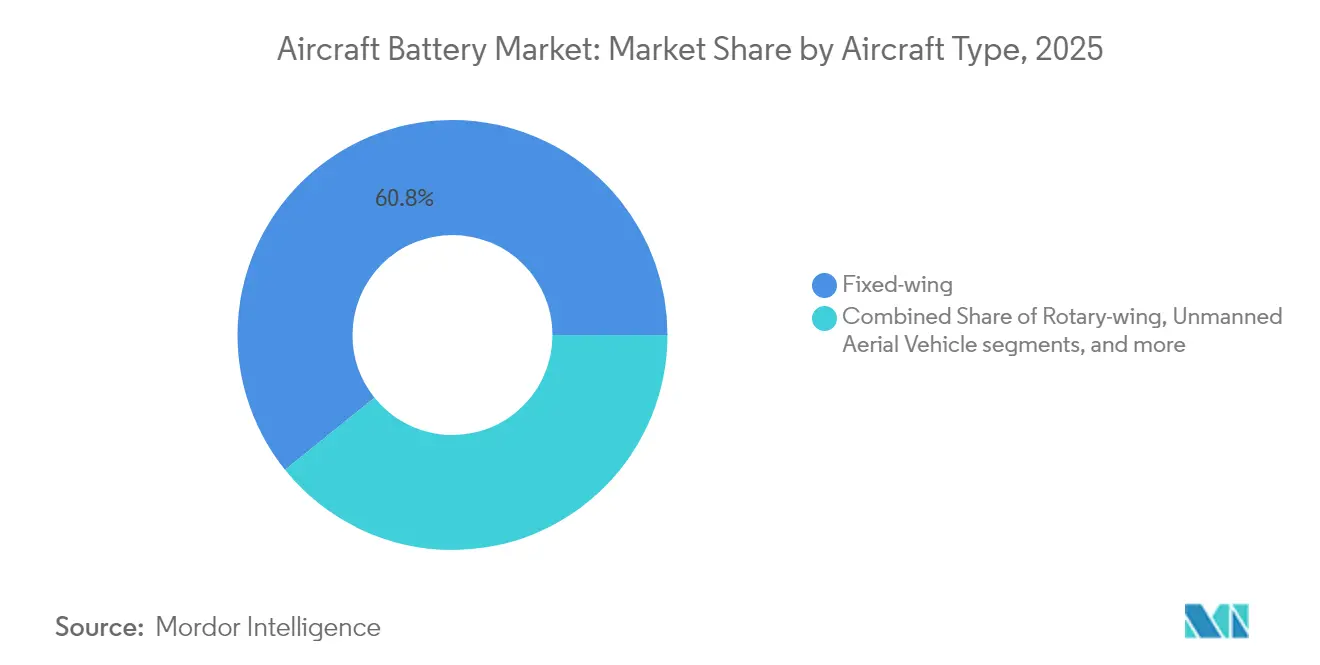

- By aircraft type, fixed-wing aircraft commanded 60.78% of the aircraft battery market share in 2025; the advanced air-mobility segment is set to rise at 29.18% CAGR this decade.

- By power density, batteries below 300 Wh/kg will represent 67.25% of the aircraft battery market in 2025, while cells above 500 Wh/kg will grow at a 26.95% CAGR.

- By end-user, OEM channels captured 61.02% revenue in 2025 in the aircraft battery market; the aftermarket is increasing at 7.61% CAGR on the back of rising replacement cycles.

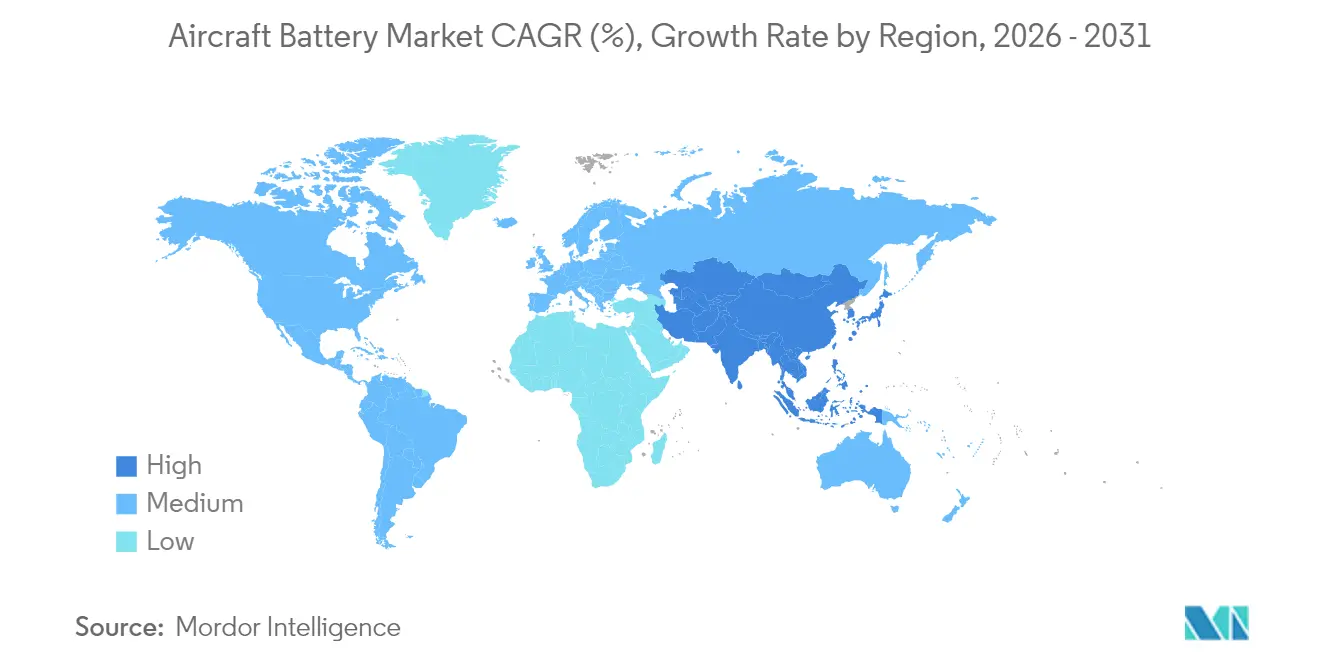

- By geography, North America commanded 30.12% of the aircraft battery market in 2025, while Asia-Pacific will grow at a 9.72% CAGR driven by scale manufacturing and supportive low-altitude-economy policies.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aircraft Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption of More-Electric Aircraft (MEA) architecture in North American narrow-body programs | +2.8% | North America, with spillover to Europe | Medium term (2-4 years) |

| OEM shift to Li-ion batteries for high-load avionics in Asia | +2.1% | Asia-Pacific, particularly China, Japan, and South Korea | Short term (≤ 2 years) |

| Rapid certification pipeline for eVTOL air-taxis in Europe | +2.4% | Europe, North America | Medium term (2-4 years) |

| Military UAV modernization driving high-rate cells in Middle East | +1.6% | Middle East, North America | Short term (≤ 2 years) |

| Government policy support and clean aviation funding | +1.9% | Global, with emphasis on US and EU | Long term (≥ 4 years) |

| Solid-state battery technology breakthroughs | +1.7% | Global, led by Asia-Pacific and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Adoption of More-Electric Aircraft in North American Narrow-Body Programs

North American airframers are redesigning single-aisle jets around electrical subsystems that replace pneumatic architecture, tripling peak loads during take-off and climb in the aircraft battery market. Demonstrators such as RTX’s 1 MW motor aim to cut fuel burn by 30%, aligning with the Clean Aviation initiative that co-funds high-performance battery research. Airlines see lower maintenance costs and carbon compliance value, motivating early retrofits. Battery makers that can validate rapid-charge, high-cycle packs under Federal Aviation Administration (FAA) guidance stand to secure long-term supply contracts.

OEM Shift to Li-ion Batteries for High-Load Avionics in Asia

Chinese, Japanese, and Korean OEMs are phasing out nickel-cadmium units in favor of lithium-ion packs in the aircraft battery market, which study results show reduce supply-chain complexity by 72% and carbon emissions by 75%. Domestic suppliers such as CATL and Gotion High-Tech already reach 500 Wh/kg and 300 Wh/kg, respectively, giving regional manufacturers secure access to advanced chemistries. Competitive pressure intensified when SoftBank reported 350 Wh/kg in all-solid-state prototypes, spurring a regional technology race. The shift will ripple across flight-control computers, radar, and galley systems, cutting weight and freeing space for additional payload.

Rapid Certification Pipeline for eVTOL Air Taxis in Europe

The European Commission’s 2024 regulatory package gives eVTOL makers a structured path to type certification, covering redundant energy-storage requirements and cell-level safety within the aircraft battery market. Harmonization with FAA rules allows battery developers to design once for multiple jurisdictions, lowering unit costs. Firms such as Joby and Archer schedule commercial launches as early as 2026, increasing near-term demand for aviation-grade lithium-ion modules. Venture backing follows regulatory clarity, with new gigafactory announcements in France and Spain targeting aerospace cells.

Military UAV Modernization Driving High-Rate Cells in Middle East

Regional defense ministries prioritize indigenous drone fleets, sparking demand for high-rate discharge cells to sustain rapid climb and long loiter in the aircraft battery market. InoBat’s 2025 launch of a drone-specific battery underscores the commercial opportunity. Israel’s unveiling of a next-generation military battery in 2024 further highlights momentum. Supply-chain security concerns, amplified by export restrictions from China, push Middle Eastern buyers to diversify sources and consider local joint ventures.[1]Center for Strategic and International Studies, “China’s UAV Supply-Chain Restrictions,” csis.org

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Thermal-runaway incidents slowing wide-body adoption | -1.4% | Global, with emphasis on North America and Europe | Medium term (2-4 years) |

| Scarce aerospace-grade Li-S production capacity | -1.1% | Global | Short term (≤ 2 years) |

| Nickel and Cobalt price volatility compressing OEM margins | -0.9% | Global, with highest impact in Asia-Pacific | Medium term (2-4 years) |

| Supply chain vulnerabilities and geopolitical tensions | -1.2% | Global, particularly affecting US-China trade | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Thermal-Runaway Incidents Slowing Wide-Body Adoption

In 2024, the FAA logged 69 lithium-battery smoke or fire events aboard passenger aircraft, reinforcing airline caution on large-format packs. EASA followed by commissioning Fraunhofer’s LOKI-PED tests to quantify cabin and cockpit fire risk, with results due in 2025. Regulators prepare new handling protocols, while research shows that unprotected pouch cells can shatter at crash speeds, making robust housing mandatory. Wide-body programs, therefore, keep legacy battery systems longer, limiting volume growth even as single-aisle and regional platforms electrify.

Scarce Aerospace-Grade Li-S Production Capacity

Lithium-sulfur cells promise 600 Wh/kg energy density, yet only a few pilot lines meet aviation reliability standards. Oxis Energy and partners target quasi-solid-state cells for 2026, but volumes remain small relative to projected aerospace demand. Competing sectors, mainly electric vehicles, absorb 96% of global battery demand growth, tightening raw-material markets, and increasing prices. Until certified production rises, airlines and OEMs curb adoption schedules, moderating the overall aircraft battery market trajectory despite technical potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Lithium-Ion Leads While Lithium-Sulfur Accelerates

Lithium-ion held 52.34% of the aircraft battery market share in 2025, owing to mature supply chains and well-understood performance envelopes. Designers favor its high gravimetric energy for starter-generator duties and growing hybrid-electric thrust demands. Recent capacity enhancements, including silicon-rich anodes, push cycle life past 2,000 deep discharges, lowering total-cost-of-ownership metrics that sway airline procurement. Conversely, nickel-cadmium and lead-acid remain serviceable in hostile environments such as polar routes or rotary-wing missions where low-temperature resilience trumps weight efficiency.

Momentum is shifting toward lithium-sulfur in the aircraft battery market, forecast to compound at 23.72% annually through 2031 as collaborations resolve shuttle-effect durability hurdles. Early flight tests show 20% range gains on light drones, validating performance claims. Sodium-ion solutions under US Navy funding indicate a future niche for thermally stable chemistries in carrier operations.These developments widen the competitive field, encouraging smaller innovators to license cell architectures optimized for aviation’s stringent safety codes.

By Application: Propulsion Surges Ahead of Legacy Emergency Use

Back-up and emergency systems occupied 37.85% of the aircraft battery market size in 2025 because every certified aircraft must power vital radios and fly-by-wire controls during generator loss. Yet the propulsion segment for eVTOL aircraft is outpacing all categories with 28.91% CAGR, to urban-mobility trials across Dubai, Los Angeles, and Singapore. Moore’s law-style cost curves in power electronics amplify the economic case, allowing operators to forecast per-seat-mile costs below regional turboprops for missions under 200 km.

Auxiliary power units (APUs) and avionics packs benefit from lighter lithium-ion formats that cut scheduled maintenance and decrease fuel burn in the aircraft battery market. Advanced battery systems integrated with thermal-management hardware, such as BAE Systems’ 200 kWh pack for a hybrid narrow-body demonstrator, signal a shift toward modular, swappable units. This architectural evolution enables airlines to upgrade chemistries without major airframe modifications, keeping residual values high.

By Aircraft Technology: Transitional Hybrids Bridge Conventional and Full Electric

Traditional architectures still command 57.96% market revenue, reflecting a fleet of more than 25,000 active commercial jets that rely on batteries chiefly for ground starts and emergency functions. OEM retrofits, such as improved lithium-ion shipsets on the B737 MAX, illustrate incremental electrification even within legacy frames. Meanwhile, hybrid-electric concepts blend turbofan efficiency with battery-boosted climb performance, delivering up to 15% fuel savings on routes under 1,500 km.

Though smaller in number, fully electric airframes show the steepest adoption curve with 29.84% projected CAGR as certification frameworks mature. Scaling tests demonstrate endurance of 19.6 hours when batteries pair with hydrogen fuel cells in distributed-propulsion layouts. Once energy densities surpass 500 Wh/kg at production scale, regional point-to-point flights become commercially feasible, reinforcing the aircraft battery market growth narrative.

By Aircraft Type: Fixed-Wing Dominates, AAM Emerges

Fixed-wing models generated 60.78% revenue in 2025, underpinned by commercial single-aisle programs and persistent military trainer demand. Battery suppliers, therefore, prioritize plug-compatible replacements that minimize airline downtime. Rotary-wing applications, including air-ambulance helicopters, remain battery-intensive because of repeated start-stop cycles and hover phases.

The advanced air-mobility segment represents the fastest clip at 29.18% CAGR as city pairs invest in vertiport infrastructure. JSX’s provisional order for up to 82 Electra eSTOL aircraft confirms airline appetite for short-runway solutions that sidestep congested hubs. Uncrewed aerial vehicles add further pull, especially in defense, where high-rate discharge capacity translates directly to extended surveillance endurance.

By Power Density: Medium Range Underpins Today, High Range Powers Tomorrow

Cells below 300 Wh/kg accounted for 67.25% of sales in 2025 in the aircraft battery market because their performance aligns with certification data from decades of operation. Pack costs stay competitive at fleet scale, supporting widespread use across airliner galleys, lighting, and emergency beacons. The medium-range bracket between 100-300 Wh/kg balances temperature stability with reliable cycle life, keeping it the workhorse of both commercial and military fleets.

Growth shifts upward as research roadmaps from NASA and the US Department of Energy target cost parity at 500 Wh/kg by 2030. Cells exceeding that threshold are forecast to grow 26.95% annually, unlocking two-hour electric regional flights and heavy-lift cargo drones. Standards bodies have already drafted test protocols for these higher-energy chemistries, a necessary precondition for fleet deployment.

By End-User: OEM Channel Prevails, Aftermarket Diversifies

OEMs booked 61.02% of shipments in 2025 because batteries form part of the type-certification baseline and require integration with avionics software. Airframers increasingly source cells under long-term agreements to manage traceability and design assurance. The aircraft battery market size for aftermarket services widens as fleets age and airlines demand mid-life performance upgrades.

Repair specialists now re-cell packs with higher-energy chemistry while retaining the original casing, extending the service interval by 40% and reducing hazardous waste volumes. As battery management systems gain software complexity, aftermarket players invest in digital twins that predict state-of-health to individual cell groups, carving a profitable data-services niche and challenging the traditional OEM maintenance monopoly.

Geography Analysis

North America secured 30.12% revenue in 2025 as federal policies such as the Inflation Reduction Act channeled funding into domestic cell production and electric-aircraft demonstration programs. The FAA’s Innovate28 roadmap provides step-by-step integration milestones, allowing airlines to plan fleet renewals around certified electric or hybrid models. Yet material reliance on imported lithium and rare-earths exposes a supply-chain risk that could constrain longer-term expansion.

Asia-Pacific posts the fastest 9.72% CAGR during 2026-2031, propelled by China’s low-altitude economy blueprint and manufacturing scale, which produces roughly 85% of global lithium-ion output. Japanese all-solid-state breakthroughs and Korean cathode expertise reinforce regional self-sufficiency, allowing local OEMs to lock in competitive pricing. India’s aviation upswing and drone-delivery trials add incremental volume, broadening the customer base for regional battery suppliers.

Europe maintains a stronghold built on Airbus, Leonardo, and a dense tier-one supplier network. The EU Battery Regulation mandates recycled-content thresholds and carbon footprint declarations, steering product design toward circular-economy principles. Funding lines from Clean Aviation accelerate hybrid-regional demonstrators, while national energy strategies underwrite gigafactory construction from Scandinavia to Spain. These converging initiatives secure Europe’s relevance in premium-priced sustainable aviation segments.

Competitive Landscape

The aircraft battery market shows medium concentration, with traditional incumbents Saft, EnerSys, and GS Yuasa facing new entrants from the automotive domain. EnerSys deepened its defense position by acquiring Bren-Tronics for USD 208 million, adding portable lithium solutions well suited to UAV ground crews. Automotive-turned-aviation players aim to leverage gigafactory economies of scale but must adapt chemistries to rigorous aviation safety envelopes.

Strategic alliances surge as aerospace primes seek power solutions that match mission profiles. BAE Systems supplies a 200 kWh pack for Airbus’s hybrid narrow-body demonstrator, providing early proof of concept at commercial-aircraft scale. Amprius, wielding silicon-anode cells at 450 Wh/kg, signed a USD 15 million deal to power long-range drones, signaling that niche, high-energy chemistries can win sizeable contracts even before mass-market automotive adoption.

White-space innovation focuses on thermal management systems and battery management software that detect cell-level anomalies in milliseconds, preventing runaway propagation. Suppliers who certify such capabilities earn a premium and lock in multi-year agreements, underpinning durable margins despite rising raw-material costs.

Aircraft Battery Industry Leaders

Saft Groupe SAS

Concorde Battery Corporation

EnerSys

GS Yuasa International Ltd.

EaglePicher Technologies, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: InoBat unveiled a high-rate military-drone battery tailored to desert conditions.

- February 2025: Turkish Aerospace Industries (TUSAŞ) and ASPİLSAN Enerji signed an agreement to manufacture and research aircraft battery cells under the Secretariat of Defence Industries' industrial participation and offset program. This agreement aims to increase domestic production capabilities for aircraft batteries in Türkiye.

- February 2025: Amprius was awarded a USD 15 million contract to supply 450 Wh/kg batteries for an unnamed drone OEM.

- November 2024: Saft introduced lithium-ion packs customized for business jets and helicopters.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the aircraft battery market as revenues generated from main and auxiliary power-unit batteries that store chemical energy and deliver electrical power for engine start, emergency back-up, avionics, and emerging electric-propulsion needs across fixed-wing, rotary, UAV, and advanced air-mobility platforms. The assessment is reported in USD value terms for new batteries, including integrated battery-management and thermal-protection assemblies.

Scope exclusion: standalone ground chargers, airport ground-support power packs, and non-aerospace batteries are not covered.

Segmentation Overview

- By Battery Type

- Lead-Acid

- Nickel-Cadmium (NiCd)

- Lithium-ion (Li-ion)

- Lithium-sulfur (Li-S)

- By Application

- Propulsion

- Auxiliary Power Unit (APU)

- Emergency/Backup

- Avionics and Flight-Control Actuation

- Adavanced Battery System

- By Aircraft Technology

- Traditional

- More-Electric

- Hybrid-Electric

- Fully Electric

- By Aircraft Type

- Fixed-Wing

- Commercial Aviation

- Narrow-body Aircraft

- Wide-Body Aircraft

- Regional Jets

- Business and General Aviation

- Business Jets

- Light Aircraft

- Military Aviation

- Fighter Aircraft

- Transport Aircraft

- Special Mission Aircraft

- Commercial Aviation

- Rotary Wing

- Commercial Helicopters

- Military Helicopters

- Unmanned Aerial Vehicles

- Advanced Air Mobility

- Fixed-Wing

- By Power Density

- Less than 100 Wh/kg

- Between 100-300 Wh/kg

- More than 300 Wh/kg

- By End-User

- Original Equipment Manufacturer (OEM)

- Aftermarket

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts next spoke with battery design engineers, airline MRO managers, eVTOL program leads, and civil-aviation regulators across North America, Europe, and Asia-Pacific. These conversations clarified average replacement cycles, certification bottlenecks, and realistic energy-density road maps, enabling us to refine utilization rates and pricing curves before freezing model assumptions.

Desk Research

We began with broad desk work, drawing on aviation production statistics from the FAA and EASA, civil aircraft shipment data released by IATA, and defense procurement releases from the US DoD and the European Defence Agency. Trade-flow records accessed through UN Comtrade helped us gauge cross-border movement of lithium-ion cells, while patent trends from Questel highlighted chemistry shifts toward lithium-sulfur. Annual reports and 10-Ks from leading airframe and battery makers, press articles archived on Dow Jones Factiva, and weight-reduction studies published in SAE's International Journal of Aerospace further enriched the evidence set. The sources listed are illustrative; many additional public and subscription materials informed our desk analysis.

Market-Sizing & Forecasting

A top-down build starts with annual aircraft deliveries, in-service fleet counts, and penetration ratios of more-electric architectures, which are then converted into demand pools by applying battery string counts and average watt-hour capacities. We corroborate the totals through selective bottom-up checks, sampled OEM list prices multiplied by unit volumes, aftermarket repair logs, and channel feedback, adjusting where variances exceed three percent. Key variables in the model include global aircraft production schedules, eVTOL certification pipeline size, fleet retrofit rates, chemistry mix shifts, average battery cost per kWh, and regional flight-hour growth. Multivariate regression underpins the five-year forecast, with scenario analysis used to test regulatory or energy-density shocks.

Data Validation & Update Cycle

Before sign-off, our team triangulates outputs against independent fuel-burn savings benchmarks and historical replacement ratios, rerunning anomalies through a second analyst review. Reports refresh each year, and we trigger interim revisions when major airframe orders, chemistry breakthroughs, or safety directives materially change volume or price assumptions.

Why Mordor's Aircraft Battery Baseline Commands Confidence for Buyers

Published values often differ because firms pick distinct component mixes, pricing anchors, and refresh cadences. We recognize these gaps up front and explain them so decision-makers can trace each number back to transparent inputs.

Key gap drivers include whether propulsion batteries for eVTOL fleets are counted, how aggressively lithium-sulfur uptake is modeled, the currency conversion month, and the frequency at which OEM list prices are refreshed. Mordor's model aligns scope tightly with airborne batteries only, applies blended ASPs validated quarterly, and updates chemistries every cycle, whereas others may fold in chargers or use static price decks.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.60 B (2025) | Mordor Intelligence | - |

| USD 0.48 B (2024) | Global Consultancy A | Excludes eVTOL propulsion packs and uses 2022 price deck |

| USD 1.61 B (2025) | Industry Journal B | Bundles charger sales and applies uniform 12 percent lithium-sulfur share |

In sum, Mordor's disciplined scope, variable tracking, and annual refresh cadence deliver a balanced, reproducible baseline that planners can rely on when sizing opportunities or benchmarking strategic moves.

Key Questions Answered in the Report

What is the current value of the aircraft battery market?

The aircraft battery market is worth USD 660 million in 2026 and is on track to hit USD 1.12 billion by 2031, reflecting a CAGR of 11.18%.

Which battery chemistry holds the largest market share?

Lithium-ion batteries lead with 52.34% share in 2025 and remain the baseline choice for most commercial and defense aircraft.

Why are eVTOL programs important to battery suppliers?

EVTOL propulsion is growing at a 28.91% CAGR through 2031, creating a high-volume outlet for advanced, high-energy packs that meet stringent aviation safety standards.

Which region is growing the fastest for aircraft batteries?

Asia-Pacific posts the highest projected CAGR at 9.72% between 2026-2031, driven by large-scale manufacturing and supportive low-altitude-economy policies.

How do thermal-runaway incidents affect market growth?

Repeated lithium-battery fire events in wide-body aircraft prompt stricter regulations and slow adoption of newer chemistries, subtracting about 1.7% from the forecast CAGR.

What role do OEMs play compared with the aftermarket?

OEMs control 61.02% of 2025 revenues by integrating certified packs during aircraft production, whereas the aftermarket grows steadily as fleets age and operators seek performance upgrades.

Page last updated on: