Commercial Aircraft Battery Management Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

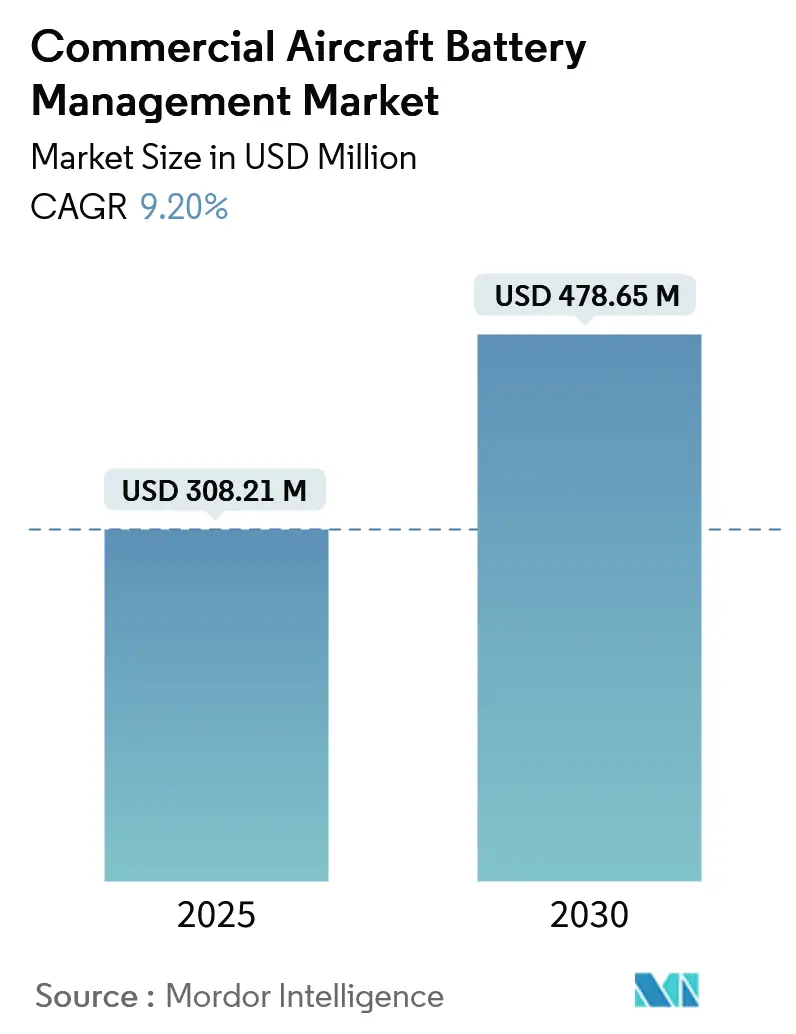

| Market Size (2025) | USD 308.21 Million |

| Market Size (2030) | USD 478.65 Million |

| Growth Rate (2025 - 2030) | 9.20% CAGR |

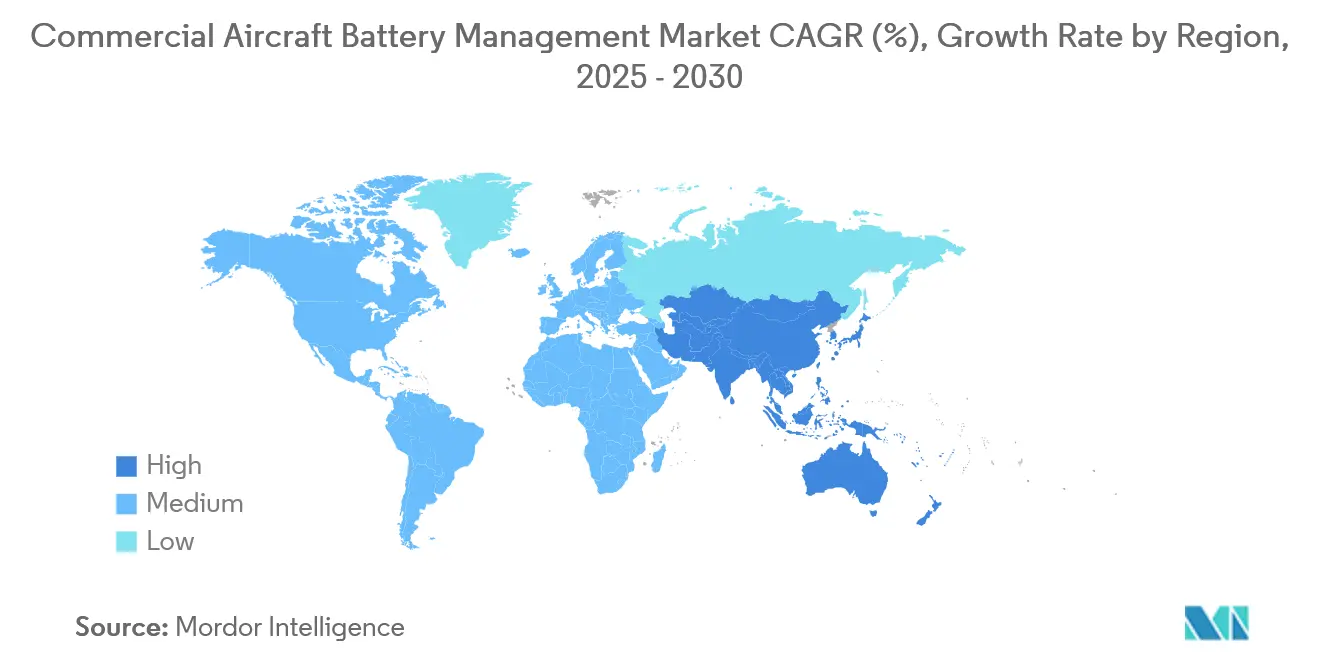

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

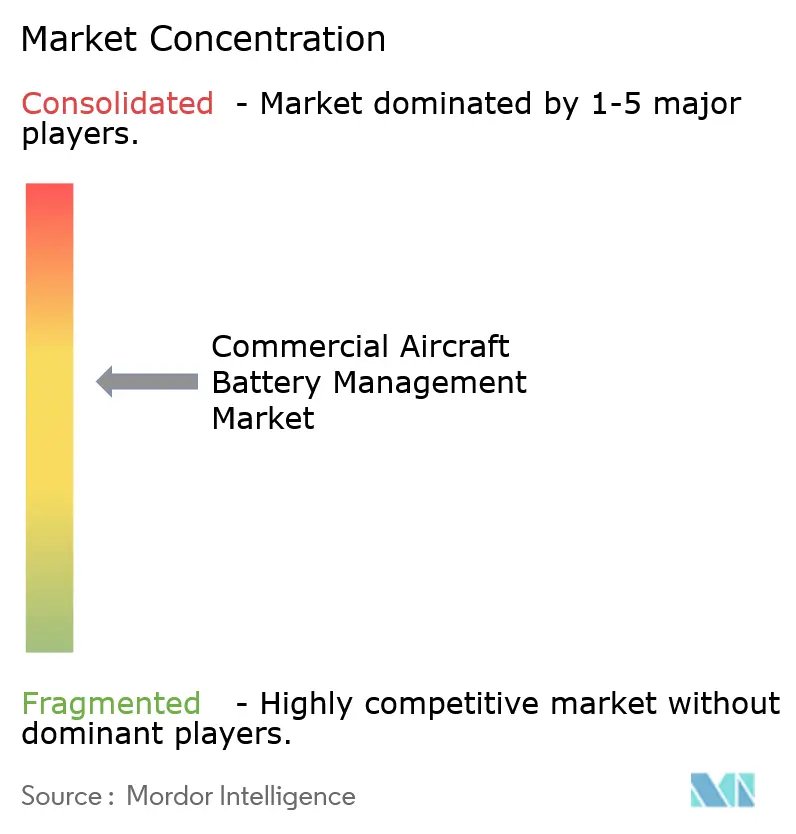

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Commercial Aircraft Battery Management Market Analysis by Mordor Intelligence

The commercial aircraft battery management market size is estimated at USD 308.21 million in 2025 and is projected to reach USD 478.65 million in 2030, advancing at a 9.20% CAGR. Intense regulatory pressure to decarbonize aviation, rapid progress in electric propulsion technologies, and rising investment in advanced air mobility platforms underpin this commercial aircraft battery management system market expansion. Airlines are prioritizing high-voltage lithium-ion and emerging solid-state solutions that enable more-electric architectures, reducing fuel burn and carbon emissions while supporting new eVTOL operating models. Certification activities by the Federal Aviation Administration for BETA Technologies and Archer Aviation, as well as the European Union Aviation Safety Agency’s technology-agnostic rules, remove key barriers. It accelerates the deployment of certified battery management solutions. Incumbent suppliers respond with modular, fault-tolerant designs that integrate AI-based predictive maintenance. At the same time, start-ups pursue high-energy solid-state chemistries to reshape the commercial aircraft battery management system market.

Key Report Takeaways

- By battery type, lithium-ion (Li-ion) captured 62.67% of the commercial aircraft battery management market share in 2024. In contrast, solid-state platforms for advanced air mobility are projected to record the highest CAGR of 18.90% from 2024 to 2030.

- By aircraft type, commercial aviation accounted for 64.52% of the commercial aircraft battery management market size in 2024, while eVTOL and urban air mobility platforms are expected to expand at a 14.67% CAGR through 2030.

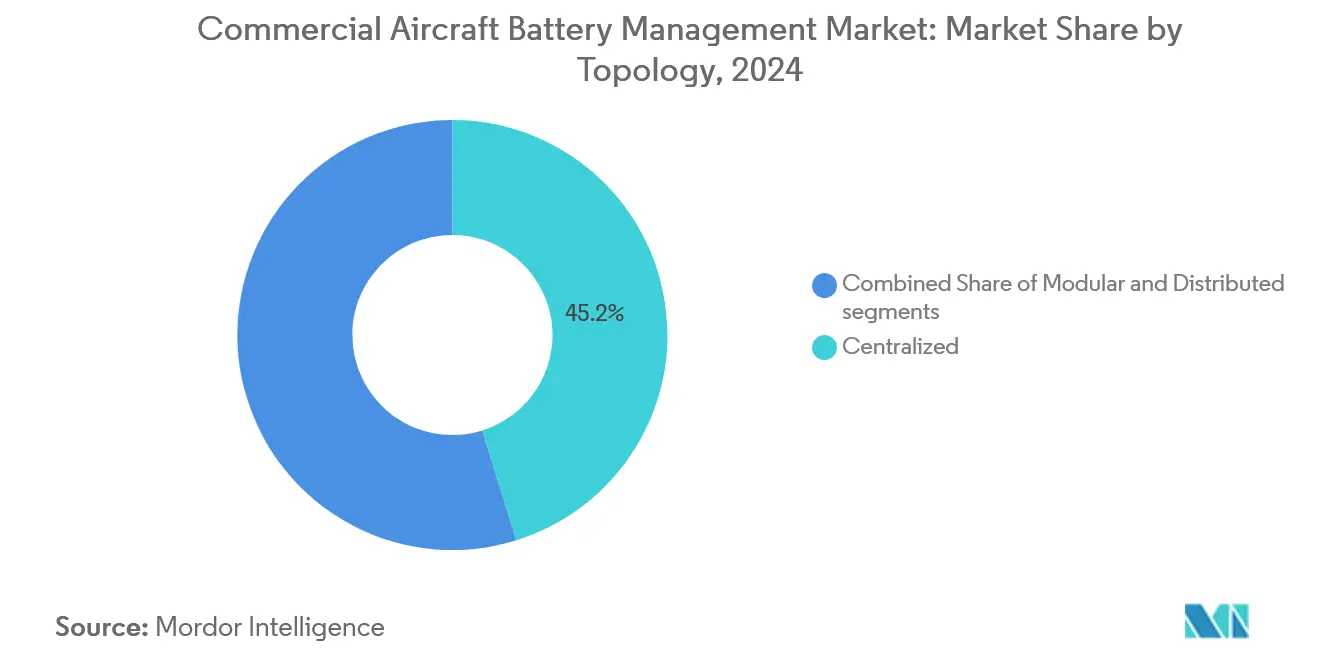

- By topology, centralized architectures led with a 45.19% share in 2024; distributed systems posted the strongest 12.11% CAGR as OEMs seek redundancy and fault isolation.

- By application, power supply management held a 27.34% share of the commercial aircraft battery management system market in 2024. In contrast, safety-monitoring solutions are projected to rise at a 10.22% CAGR through 2030.

- By geography, North America contributed 35.4% 2% revenue in 2024; Asia-Pacific exhibits the quickest 11.71% CAGR due to large-scale Chinese electrified aircraft programs.

Global Commercial Aircraft Battery Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated integration of more-electric and all-electric aircraft platforms | +2.1% | Global, led by North America and Europe | Medium term (2-4 years) |

| Tightening ICAO CO₂ and NOx regulations for post-2028 compliance | +1.8% | Global, impacting international carriers | Long term (≥ 4 years) |

| Global aviation safety rules mandating lithium battery health monitoring | +1.4% | Global, strictest in North America and Europe | Short term (≤ 2 years) |

| Certification pathways for eVTOLs fuelling OEM demand for advanced BMS | +1.6% | North America and Europe, Asia-Pacific following | Medium term (2-4 years) |

| AI-powered predictive maintenance reducing airline operating costs | +1.2% | Global, early adoption in developed markets | Medium term (2-4 years) |

| EM investment in solid-state battery technologies | +0.9% | Global, R&D centered in North America and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Integration of More Electric and All-Electric Aircraft Platforms

Airframe manufacturers integrate megawatt-class electric-propulsion packages such as the Collins Aerospace 1 MW demonstrator for regional jets. This shift elevates power-distribution complexity and stimulates the commercial aircraft battery management system market.[1]Collins Aerospace, “Alternative Power Sources,” collinsaerospace.com Converting hydraulic and pneumatic loads to electrical alternatives cuts fuel use by up to 10% and multiplies the number of high-voltage nodes that must be supervised simultaneously. STEP-Tech turbo-electric trials scale from 100 kW to 1 MW, requiring real-time cell-level telemetry, precise thermal balancing, and cyber-secure communication interfaces. Therefore, the commercial aircraft battery management system market prioritizes high-speed processors, redundant sensing, and modular control units that fit diverse installation envelopes. Fleet operators view these systems as indispensable for demonstrating energy-efficiency gains that enable compliance with upcoming carbon-levy schemes.

Tightening ICAO Emission Regulations on CO₂ and NOx Post-2028 Compliance

The 2028 ICAO limits compel carriers to adopt electric or hybrid drive trains, and that compliance timetable drives immediate procurement of certified energy-storage controls. EASA Opinion establishes type-certification guidelines that treat batteries as propulsion-critical elements, placing additional design-assurance requirements on state-of-charge accuracy, thermal-runaway resilience, and end-of-life detection. Airlines, therefore, demand proof that a commercial aircraft battery management system market solution can furnish continuous emission metrics, optimize charge cycles for minimal carbon intensity, and interface with flight-data-monitoring systems. Developers meeting these criteria gain fast-track approvals and secure early fleet-retrofit contracts that expand the commercial aircraft battery management system market.

Global Aviation Safety Regulations Mandating Enhanced Lithium Battery Health Monitoring

Incidents of in-flight battery thermal events rose 28% in 2024, prompting the FAA to release Advisory Circular 20-184 that tightens test and installation guidance.[2]Federal Aviation Administration, “Advisory Circular 20-184,” faa.gov Regulators also require cockpit annunciation of abnormal cell conditions, pushing vendors to integrate AI-derived health-index algorithms that forecast failure up to five hours before onset. The commercial aircraft battery management system market answers with multilayer diagnostic architectures able to isolate the affected string, execute graceful-degradation modes, and trigger cabin-crew alerts. Adoption accelerates because compliance reduces insurance premiums, lowers unscheduled maintenance, and aligns with continuous-airworthiness mandates.

Certification Pathways for eVTOLs Fueling OEM Demand for Advanced BMS Solutions

EASA’s clearance of H55’s CS-23 propulsion battery pack highlights a repeatable approval route for urban air-mobility designs, unlocking volume demand for specialized control solutions that accommodate rapid-charge and high-C-rate requirements. eVTOL cells must deliver burst currents during vertical climb while withstanding frequent turnaround charging, which magnifies heat generation and cycling stress. Therefore, the commercial aircraft battery management system market invests in distributed topologies with sub-millisecond balancing, fault-tolerant communication layers, and automatic dispatch-readiness reporting. Honeywell’s collaboration with Vertical Aerospace on the VX4 targets a 10⁻⁹ critical-system failure probability, setting a benchmark that the broader commercial aircraft battery management system market now strives to meet.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Certification challenges related to thermal-runaway containment and mitigation | -1.7% | Global, strictest in North America and Europe | Short term (≤ 2 years) |

| Supply-chain vulnerabilities for high-purity lithium compounds | -1.3% | Global, notable in Asia-Pacific | Medium term (2-4 years |

| Cybersecurity exposure in integrated avionics and battery management systems | -0.9% | Global, heightened in defense and commercial sectors | Long term (≥ 4 years) |

| Infrastructure gaps in megawatt-level fast charging at airports | -1.1% | Global, slowest in emerging markets | Long term (≥ 4 years |

| Source: Mordor Intelligence | |||

Certification Challenges Related to Thermal-Runaway Containment and Mitigation

FAA airworthiness directives, such as the 2025 Dassault bulletin on swelling lithium-polymer display batteries, highlight ongoing risks and the burden of retrofit mandates. The trinational EASA-FAA white paper prescribes a three-step approach—initiation, propagation, and containment—that demands exhaustive validation of venting paths, fire-resistant materials, and cell-level isolation. Semi-confined-space tests reveal explosion phases absent in automotive applications, raising barriers for new entrants. Therefore, the commercial aircraft battery management system market incurs elevated R&D and certification costs that can delay product launches.

Supply Chain Vulnerabilities for High-Purity Lithium Compounds and Class-I Salts

Battery-grade lithium requires 99.9% purity, and any sodium, boron, or potassium residuals impair cycle life, yet extraction and refining capacity lag demand. Research indicates that controlled magnesium additions may ease purity constraints, but implementation remains nascent. Trade litigation over separator patents further complicates raw-material sourcing. These factors inflate production expenses across the commercial aircraft battery management system market and increase lead times for new programs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Lithium-Ion Dominance Faces Solid-State Disruption

Lithium-ion (Li-ion) commanded 62.67% of the commercial aircraft battery management market share in 2024, driven by the mature supply chains, proven airworthiness data, and predictable thermal behavior. Solid-state chemistries now enter flight-test phases with energy densities near 500 Wh/kg, a leap that could halve pack mass and improve range. The commercial aircraft battery management system market size for solid-state units is forecast to expand at an 18.90% CAGR as advanced air mobility (AAM) platforms mature.

Transitioning to solid-state cells forces redesign of thermal-regulation loops, fault-detection thresholds, and charging algorithms. OEMs such as CATL and NASA have demonstrated condensed or anodeless prototypes, but scale-up remains a hurdle. Nickel-cadmium retains niche utility for harsh-temperature redundancy, while lead-acid gradually exits mainstream programs. The commercial aircraft battery management system market increasingly values chem-agnostic firmware that can accommodate multiple cell types within standard hardware, preserving airline investment cycles.

By Aircraft Type: Commercial Aviation Leads While eVTOL Transforms Market Dynamics

Commercial airplanes accounted for 64.52% of the commercial aircraft battery management market size in 2024, reflecting the demand for retrofitting narrow-body and wide-body fleets with more electric subsystems, such as galley power and taxi assist. Cargo conversions add momentum by electrifying environmental controls to reduce auxiliary power unit runtime.

eVTOL craft, air taxis, and regional hybrids surge at a 14.67% CAGR, reshaping expectations for cycle life, burst-power tolerance, and ultra-fast charging. Vertical Aerospace and Honeywell aim to certify the VX4 in 2028, demonstrating high-reliability design goals that influence mainstream standards. The commercial aircraft battery management system market now balances legacy retrofit with clean-sheet AAM architectures that demand lighter, smarter, and more modular controllers.

By Topology: Distributed Architectures Challenge Centralized Systems

Centralized designs still led with a 45.19% share in 2024 because single-unit certification is straightforward, and maintenance procedures are familiar to operators. However, distributed configurations grow at 12.11% CAGR as OEMs demand graceful degradation and cell-level isolation. Safran’s GENeUSPACK features multiple smart sub-modules with independent monitoring and power conversion capabilities.[3]Safran Group, “Smart Battery System GENeUSPACK™,” safran-group.com

In distributed layouts, the commercial aircraft battery management system market benefits from improved packaging flexibility, simplified wing or nacelle integration, and lower harness mass. Communication latency and cybersecurity become paramount, so controller boards incorporate deterministic Ethernet and secure boot functions. Modular arrangements, meanwhile, serve retrofit projects by overlaying extra monitoring boards onto existing packs, providing a compromise between complete centralization and fully distributed designs.

By Application: Power Management Dominates While Safety Monitoring Accelerates

Power-supply management held 27.34% of the commercial aircraft battery management system market share in 2024 because every electrified subsystem relies on stable DC-bus control. Energy-storage optimization modules extend pack life through balanced cycling, while flight-control backup solutions ensure fly-by-wire integrity during generator outages.

Safety-monitoring functions advance fastest at 10.22% CAGR as regulators require real-time fault detection, post-event containment, and predictive maintenance integration. Algorithms using impedance spectroscopy and thermal modeling detect precursors of venting with five-hour lead times, and automatic fault isolation reduces incident severity. The commercial aircraft battery management system market is increasingly converging power management, health analytics, and cyber-secure connectivity in single-line-replaceable units.

Geography Analysis

North America contributed 35.42% revenue in 2024 owing to supportive certification guidance, a deep aerospace supply chain, and proactive infrastructure roll-outs such as Beta Technologies’ 46-site charging network. FAA special conditions for BETA Technologies and Archer Aviation offer clear roadmaps that accelerate commercialization. Therefore, the commercial aircraft battery management system market finds its most extensive installed base among US-built narrow-body and AAM prototypes.

Asia-Pacific is the fastest-growing region at an 11.71% CAGR, driven by the CNY 3.5 trillion (USD 0.49 trillion) low-altitude-economy plan and CATL’s 2,000–3,000 km electric airliner program.[4]China Daily, “CATL Electric Plane,” chinadaily.com.cn Japanese and Korean material giants supply advanced electrolytes and separators, giving the region an integrated value chain that supports cost-competitive production. The resulting momentum enlarges the regional commercial aircraft battery management system market, particularly for high-energy solid-state packs.

Europe maintains steady expansion as EASA’s technology-agnostic rules reduce time-to-certification and multinational consortia like Daher-Safran-Collins explore hybrid-electric demonstrators. H55’s CS-23 pack approval underscores regional competency in safety-critical battery design. Ongoing investment in hydrogen-electric hybrids further diversifies demand, ensuring the commercial aircraft battery management system market remains central to Europe’s net-zero-by-2050 aviation objectives.

Competitive Landscape

The commercial aircraft battery management market features moderate concentration. Collins Aerospace (RTX Corporation), BAE Systems plc, and Safran combine long-standing regulator relationships with vertically integrated electronics to anchor their positions. They bundle controllers with power converters, thermal management, and flight-deck tools, creating lock-in around common data architectures. Strategic moves include Safran’s EUR 1.98 billion (USD 2.30 billion) R&D spend on decarbonization technologies in 2024, and Honeywell’s partnership with NXP to embed AI accelerators that cut latency in Anthem-based monitoring systems.

Partnerships proliferate as incumbents fill capability gaps. Honeywell collaborates with Regal Rexnord for electro-mechanical actuation to complement battery packs for eVTOL platforms, while Safran pairs with Saft to boost high-voltage cell integration. These alliances accelerate time-to-market and share certification costs, a significant advantage in the commercial aircraft battery management system market.

Emerging specialists target white-space niches such as solid-state-specific thermal barriers, cyber-secure communication stacks, and machine-learning-based health prognostics. Competitive intensity therefore balances scale advantages of incumbents against the agility of niche developers, sustaining innovation across the commercial aircraft battery management system market.

Commercial Aircraft Battery Management Industry Leaders

Collins Aerospace (RTX Corporation)

BAE Systems plc

Saft Groupe SAS

Safran

Thales Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: BAE Systems signed an agreement with Airbus to provide energy storage systems for Airbus' micro-hybridization demonstration project for commercial aircraft, where BAE Systems will develop, test, and supply energy storage packs for electric aircraft in the megawatt power class, with a 200-kilowatt-hour energy capacity to improve energy efficiency and performance.

- October 2024: GE Aerospace secured a 10-year, multi-million-dollar services agreement with Emirates to support the electrical load management system across the airline's B777 fleet.

Global Commercial Aircraft Battery Management Market Report Scope

| Lithium-Ion |

| Nickel-Cadmium |

| Lead-Acid |

| Others |

| Commercial Aviation | Narrowbody |

| Widebody | |

| Freighters | |

| General Aviation | Business Jets |

| eVTOL/Urban Air Mobility |

| Centralized |

| Modular |

| Distributed |

| Power Supply Management |

| Energy Storage Management |

| Flight Control Systems |

| Safety Monitoring Systems |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Battery Type | Lithium-Ion | ||

| Nickel-Cadmium | |||

| Lead-Acid | |||

| Others | |||

| By Aircraft Type | Commercial Aviation | Narrowbody | |

| Widebody | |||

| Freighters | |||

| General Aviation | Business Jets | ||

| eVTOL/Urban Air Mobility | |||

| By Topology | Centralized | ||

| Modular | |||

| Distributed | |||

| By Application | Power Supply Management | ||

| Energy Storage Management | |||

| Flight Control Systems | |||

| Safety Monitoring Systems | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2025 value of the commercial aircraft battery management market?

The market stands at USD 308.21 million in 2025.

How fast will the commercial aircraft battery management market grow by 2030?

It is forecasted to expand at a 9.20% CAGR, reaching USD 478.65 million.

Which battery chemistry leads the commercial aircraft battery management market?

Lithium-ion remains dominant with 62.67% share in 2024, though solid-state solutions are the fastest-growing.

Why is Asia-Pacific the fastest-growing region for the commercial aircraft battery management market?

Aggressive Chinese electrified-aircraft programs and integrated battery supply chains drive an 11.71% regional CAGR.

What application segment is expanding most quickly?

Safety-monitoring solutions lead growth at a 10.22% CAGR due to stringent thermal-runaway regulations.

How are AI tools changing battery management in aviation?

Predictive analytics platforms detect degradation early, optimize maintenance schedules, and reduce airline operating costs by billions over fleet lifecycles.

Page last updated on: