Aircraft Engine Compressor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

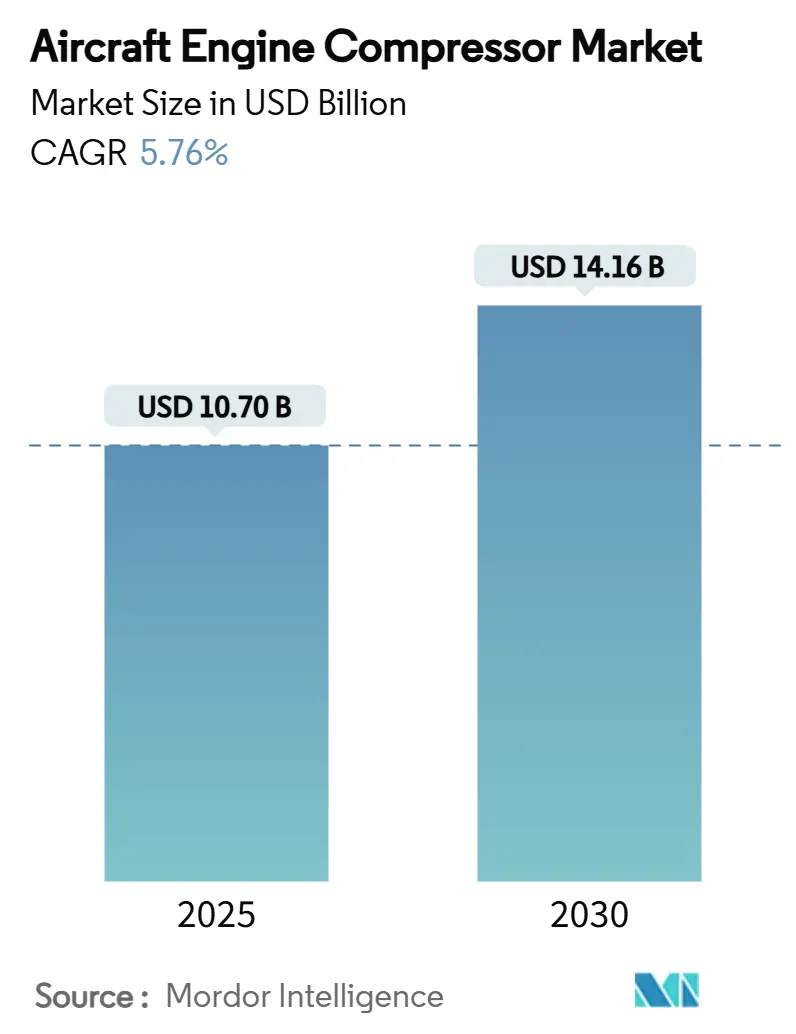

| Market Size (2025) | USD 10.70 Billion |

| Market Size (2030) | USD 14.16 Billion |

| Growth Rate (2025 - 2030) | 5.76% CAGR |

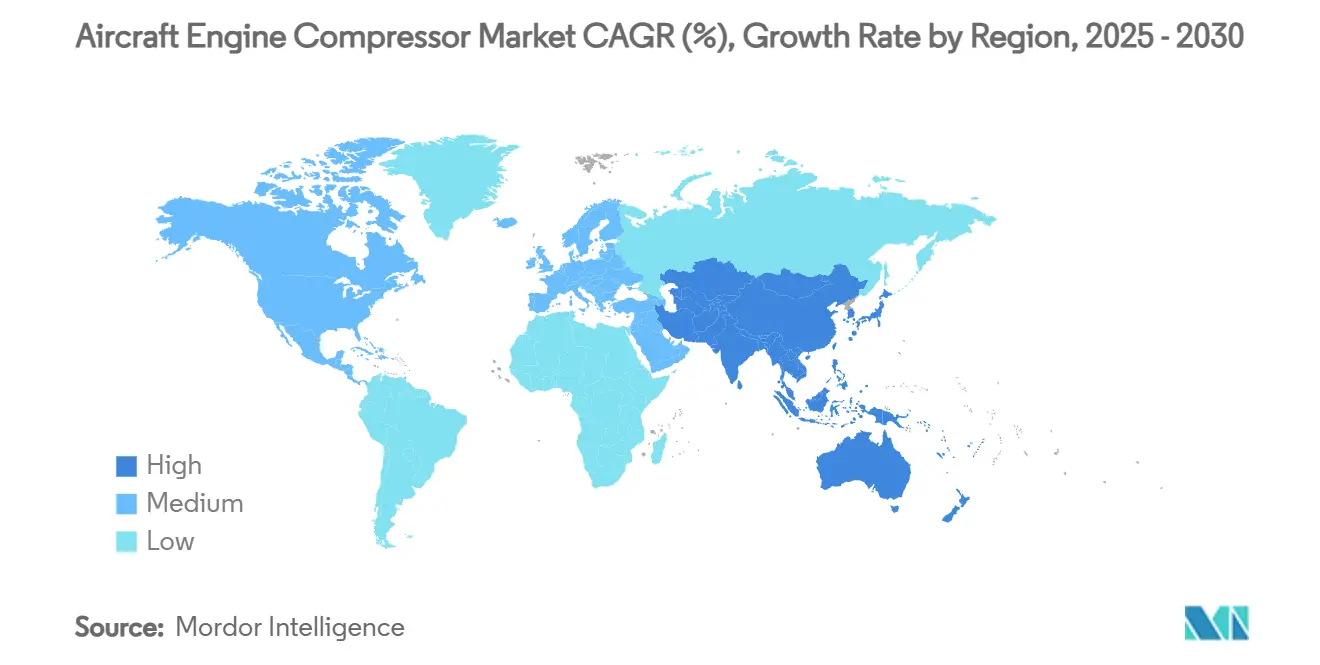

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

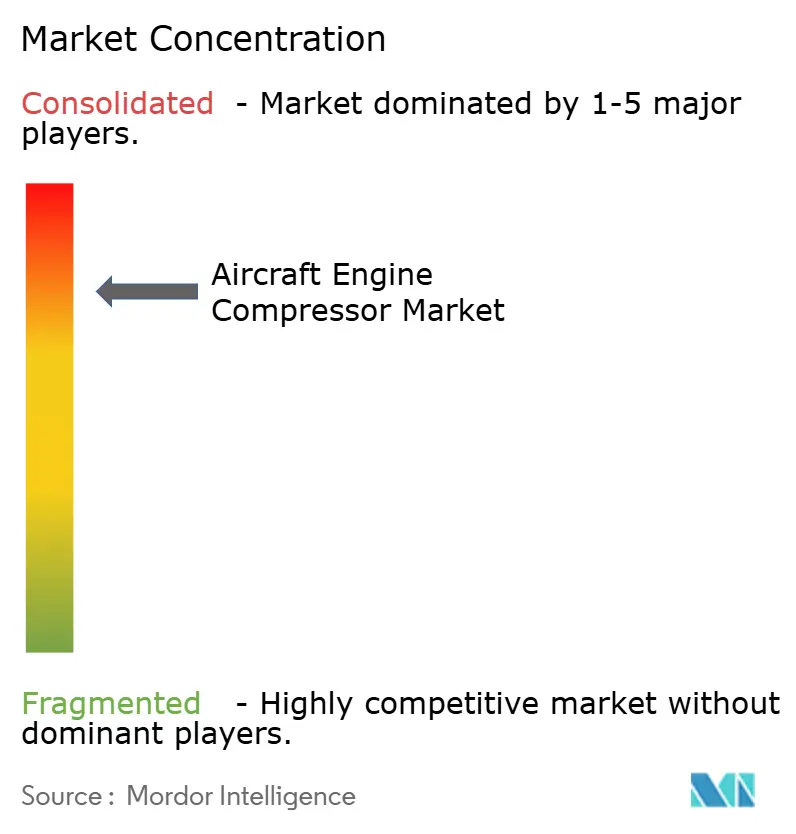

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Engine Compressor Market Analysis by Mordor Intelligence

The aircraft engine compressor market was valued at USD 10.7 billion in 2025 and is projected to reach USD 14.16 billion by 2030, growing at a 5.76% CAGR. Robust replacement demand for fuel-efficient single-aisle jets, sizeable defense propulsion programs, and steady recovery in long-haul travel jointly underpin this sustained growth path. The increasing reliance on high-bypass axial-flow architectures, the swift adoption of ceramic-matrix composites, and the broader use of additive repairs collectively tighten the value chain around advanced compressor stages. Strategic focus on titanium supply diversification mitigates raw material risk, while the rising uptake of sustainable aviation fuel accelerates the need for fouling-resistant designs. Together, these forces reinforce the long-term attractiveness of the aircraft engine compressor market.

Key Report Takeaways

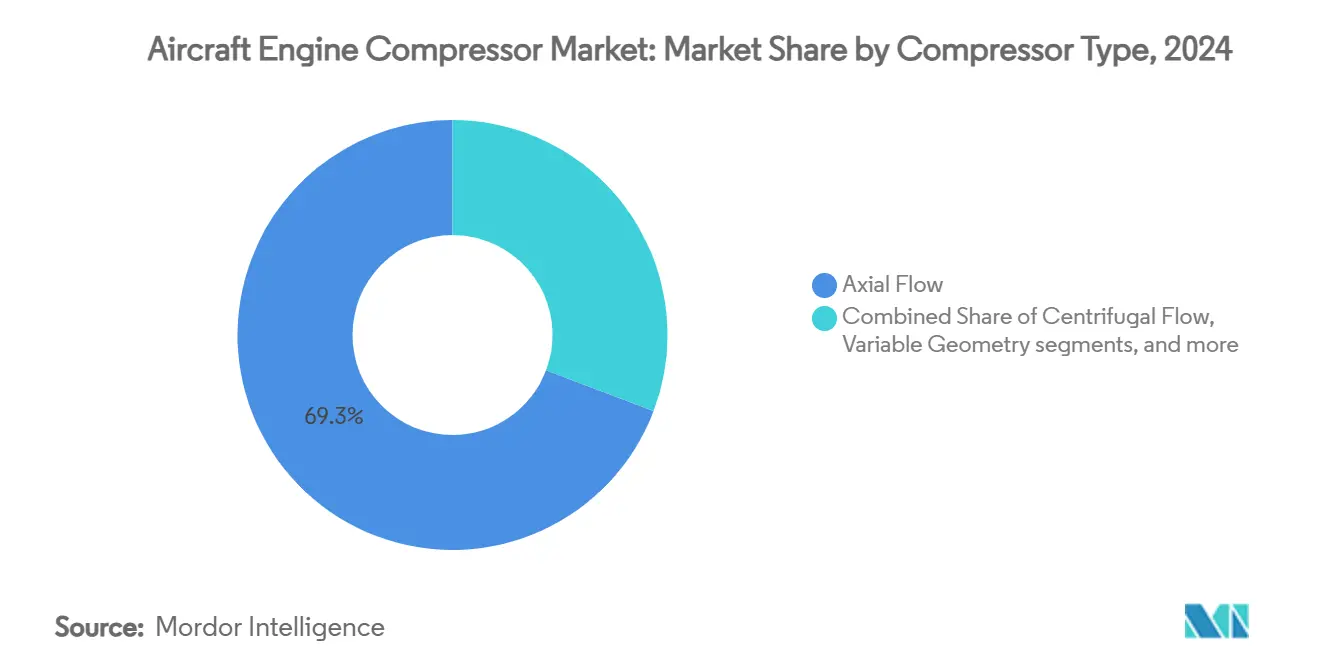

- By compressor type, axial-flow systems led the aircraft engine compressor market, accounting for 69.25% of the market share in 2024. In contrast, variable-geometry compressors are projected to advance at an 8.23% CAGR through 2030.

- By engine type, turbofan engines accounted for a 63.65% share of the aircraft engine compressor market size in 2024, while turboshaft engines are expected to post the fastest growth rate of 9.38% from 2024 to 2030.

- By material, titanium alloys dominated with a 55.31% share in 2024; composite materials are anticipated to register the highest CAGR of 7.21% between 2025 and 2030.

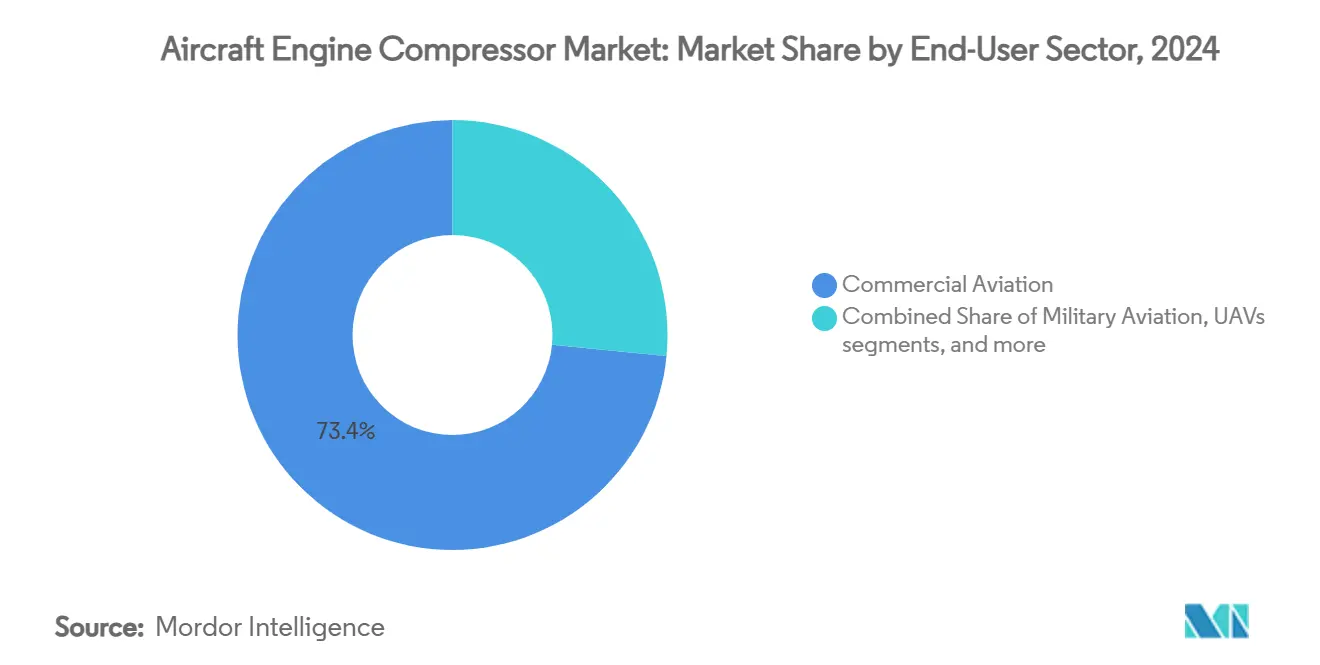

- By end-user sector, commercial aviation captured 73.44% of the aircraft engine compressor market in 2024, and unmanned aerial vehicles (UAVs) are forecasted to expand at a 10.85% CAGR through 2030.

- By stage count, multi-stage (3 to 5) configurations held a 60.21% share of the aircraft engine compressor market in 2024, and high-stage (greater than 5) designs are projected to advance at a 6.22% CAGR through 2030.

- By geography, North America accounted for a 41.24% share of the aircraft engine compressor market in 2024, while the Asia-Pacific is projected to record the fastest CAGR of 6.75% from 2025 to 2030.

Global Aircraft Engine Compressor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising deliveries of fuel-efficient narrowbody aircraft | +1.8% | Global, concentrated in North America and Asia-Pacific | Medium term (2-4 years) |

| Stringent emission and noise regulations pushing compressor upgrades | +1.2% | Global, led by Europe and North America regulatory frameworks | Long term (≥ 4 years) |

| Growing defense procurement of next-gen fighter engines | +0.9% | North America, Europe, Asia-Pacific defense markets | Medium term (2-4 years) |

| Increase in global air-passenger traffic and fleet renewal | +0.8% | Global, highest growth in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Emergence of additive-manufactured blisks enabling cost-effective MRO | +0.7% | Global, early adoption in developed markets | Short term (≤ 2 years) |

| Demand for high-temperature titanium-matrix composites boosting redesign | +0.6% | Global, concentrated in advanced manufacturing regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Deliveries of Fuel-Efficient Narrowbody Aircraft

Boeing projects 33,380 single-aisle deliveries between 2024 and 2043, which is equal to 76% of the total new-aircraft demand.[1]Boeing, “Boeing Forecasts Demand for Nearly 44,000 New Airplanes Through 2043,” boeing.com Each delivery carries an advanced axial-flow core that pushes bypass ratios above 10:1, directly lifting unit demand within the aircraft engine compressor market. The CFM LEAP backlog exceeds 10,000 engines, and more than 3,300 LEAP-powered aircraft are already flying commercial routes, demonstrating the conversion of orders into installed engines. Airlines focus on replacing ageing fleets rather than expanding absolute seat counts, locking in multi-year orders for efficient compressor architectures. Elevated jet-fuel prices sustain the economic case for 15-20% burn cuts compared with retiring engines. Consequently, narrowbody renewal remains the most significant growth lever through 2030 for the aircraft engine compressor market.

Stringent Emission and Noise Regulations Pushing Compressor Upgrades

ICAO’s global CO2 rule, effective in 2031, mandates a 10% reduction in fuel burn relative to today’s baselines, with European regulators targeting a 35% improvement by 2050.[2]European Commission, “Commission Welcomes ICAO Agreement on New Aircraft Standards,” europa.eu Complementary noise caps require a 6 dB reduction for post-2028 type certificates, reshaping acoustic design priorities at the compressor-blade level. EPA Part 1031 particulate limits intensify the need for cleaner, more stable combustion chambers, which depend on finely tuned pressure ratios and efficient airflow. OEMs respond by integrating variable-stator systems and composite acoustic liners that jointly lift pressure while dampening tonal peaks. Successful compliance positions compliant engines for global sales; failure risks type-certificate blocks in core markets. Environmental policy, therefore, exerts a structural, long-term pull on the adoption of advanced compressors inside the aircraft engine compressor market.

Growing Defense Procurement of Next-Generation Fighter Engines

The US Air Force committed USD 3.5 billion to adaptive-cycle demonstrators from GE Aerospace and Pratt & Whitney, a sizable vote of confidence in variable-geometry compressor technology.[3]GE Aerospace, “Meet the Super Material Helping GE’s Adaptive-Cycle Engine Deliver Transformational Performance,” geaerospace.com Prototype XA102/XA103 cores feature actuated stators that vary bypass ratios on demand, offering 35% range gains for sixth-generation fighters. NATO studies add hybrid-electric and hydrogen options, further broadening compressor-design requirement sets. Defense ministries in Europe and the Asia-Pacific region replicate spending patterns as they refresh their fleets, spurring demand for high-pressure, multistage compressors that can throttle seamlessly across supersonic and loiter regimes. Military budgets, therefore, provide a stable second pillar beneath the aircraft engine compressor market.

Emergence of Additive-Manufactured Blisks Enabling Cost-Effective MRO

Pratt & Whitney’s directed-energy deposition cuts geared-turbofan repair turnaround by 60%, underscoring additive’s role in compressor life-cycle economics. GE’s USD 200 million Alabama CMC campus establishes a vertically integrated supply line for silicon-carbide compressor parts. Additive techniques yield complex internal cooling channels and near-net-shape blisks that shed previous buy-to-fly material waste. Rapid certification progress lowers entry barriers for mid-tier MRO houses, expanding the aftermarket footprint of the aircraft engine compressor market. Early adopters in North America and Europe validate cost curves, encouraging broader global diffusion within two years.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in aerospace titanium and nickel supply chains | −1.4% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Extended lead-times in aerospace qualification processes | −1.0% | Global, notable for new entrants | Medium term (2-4 years) |

| Compressor fouling from sustainable-aviation-fuel contaminants | −0.9% | Global, rising with SAF uptake | Medium term (2-4 years) |

| Competitive threat from electrified propulsion in short-haul aircraft | −0.8% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Aerospace Titanium and Nickel Supply Chains

Geopolitical disruptions in Eastern Europe curtailed legacy titanium flows, forcing OEMs to pivot toward Japanese, Kazakh, and Saudi sponge suppliers.[4]US Geological Survey, “Titanium in 3rd Quarter 2024,” usgs.gov Spot prices climbed, while aerospace-grade billet availability tightened, resulting in lengthened forging queues for compressor disks. Parallel shortages in vacuum-melt nickel alloys created a dual metal dependency risk. OEMs respond by dual-sourcing, holding larger safety stocks, and qualifying alternative foundries; however, near-term delays persist. Higher raw-material costs feed through to unit compressor pricing, tempering top-line expansion in the aircraft engine compressor market until 2027.

Competitive Threat from Electrified Propulsion in Short-Haul Aircraft

Megawatt-class hybrid-electric demonstrators, developed under the NASA-GE collaboration, aim to achieve single-aisle entry by the early 2030s. ZeroAvia’s hydrogen-electric backlog nears 2,000 engines across major carriers, signalling a commercial appetite for compressor-free architectures. Energy-density gaps still preclude long-haul substitution, yet regional turboprop and commuter segments could see progressive displacement. Compressor manufacturers must, therefore, hedge their risks via hybrid cores, bleed-less auxiliaries, or new service revenue streams. Over the long term, electrification poses a measurable but containable threat to the aircraft engine compressor market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Compressor Type: Axial-Flow Systems Sustain Leadership

Axial-flow compressors held a 69.25% market share in the aircraft engine compressor market in 2024, underscoring their central role in high-bypass commercial turbofan engines.[5]Baker Hughes, “Axial Compressors with High Airflow Efficiency,” bakerhughes.com Their ability to stack multiple stages while keeping the frontal area low enables OEMs to achieve pressure ratios above 40:1 without compromising nacelle drag, which directly translates into lower block fuel for airlines. The segment’s growth will be paced by incremental blade-aerodynamic refinements, wider adoption of ceramic-matrix composite shrouds, and a push toward automated blisk milling that trims production lead times. Although starting from a small base, variable-geometry compressors are poised to expand at an 8.23% CAGR through 2030 as adaptive-cycle demonstrators transition into sixth-generation fighter programs, thereby increasing the average value per shipped unit. Centrifugal and mixed-flow designs will continue to serve the auxiliary-power and regional-jet niches, yet their single-stage limitations cap the attainable pressure ratios, limiting share gains.

Market dynamics favor sustained investment in axial-flow aerodynamic research while encouraging selective bets on variable-stator actuation for military and high-altitude UAV cores. OEMs already model unsteady flow interactions at sub-millimeter scales to minimise end-wall losses, and early tests of 3D-printed inlet guide vanes indicate double-digit efficiency jumps in surge margins. As these gains reach production, the aircraft engine compressor market size attached to axial-flow platforms is set to widen its absolute revenue gap over rival architectures. At the same time, the maturing supply chain for electrically actuated stator rings will lower cost barriers, allowing variable-geometry concepts to leak into premium business-jet programs by the late decade. Compressor-type segmentation will increasingly revolve around a two-horse race between high-volume axial cores and high-growth, high-margin variable-geometry variants.

By Engine Type: Turbofan Dominance Meets Turboshaft Momentum

Turbofan engines commanded a 63.65% market share of the aircraft engine compressor market in 2024, thanks to the expansive single-aisle backlog and the widebody replacement wave expected to crest after 2027. Each LEAP, PW1100G-JM, or Trent XWB delivery locks in a multistage high-pressure compressor assembly worth several hundred thousand dollars, creating a resilient installed base for aftermarket spares. Even so, turboshaft engines are projected to grow at a 9.38% CAGR through 2030, driven by global helicopter recapitalization and the emerging advanced air-mobility segment. GE’s T901, for example, delivers 1,000 additional shaft horsepower within the Black Hawk’s original envelope, illustrating how material upgrades and additive passages can stretch legacy platforms. The turbojet and turboprop families will remain important for business-jet, trainer, and regional applications, but neither presents the same aggregate dollar opportunity.

Therefore, compressor suppliers must serve two divergent demand curves: high-volume civil turbofans that prize cost per stage, and lower-run turboshaft programs that prioritise power density and thermal margin. Turbofan backlogs continue to rise: Boeing forecasts 33,000 single-aisle deliveries over 20 years, solidifying a steady turbine-core pull that underpins the aircraft engine compressor market share in commercial aviation. Conversely, military and parapublic rotorcraft fleets require engines that can accommodate hybrid-electric assist or sustainable aviation fuel blends, driving the need for custom compressor redesigns with higher surge buffers. Suppliers can stabilise revenue streams against cyclic swings in either end-market by balancing recurring civil volumes with defense-driven margin upside. Over the forecast window, engine-type diversification will remain a critical hedge while the technology frontier steadily migrates toward adaptive-cycle and hybrid architectures.

By Material: Titanium Alloys Lead, Composites Rise

Titanium alloys accounted for 55.31% of the aircraft engine compressor market share in 2024, owing to their unmatched strength-to-weight ratio and corrosion resistance at compressor-stage temperatures. Yet geopolitical supply shocks have exposed a strategic vulnerability, prompting OEMs to second-source sponges from Japan, Kazakhstan, and Saudi Arabia while qualifying lower-buy-to-fly additive feeds for blisks. On the growth side, ceramic-matrix composites (CMCs) lead with a 7.21% CAGR forecast as they raise allowable compressor-exit temperatures by 200-300°F, unlocking higher overall pressure ratios without proportional cooling-flow penalties. CFRP cases and outlet guide vanes are also scaling, with automated fibre placement now producing 28,000 fan and compressor blades per year for the LEAP program. Nickel-base superalloys and stainless steels round out the material mix, primarily in high-stress disks and cost-sensitive light-turbine models.

The shift toward CMCs and advanced polymers materially alters the value chain, drawing in chemical-vapor-infiltration experts and thermal-barrier-coating specialists who were previously confined to turbine hot sections. GE’s USD 200 million Alabama CMC hub embodies this pivot by colocating fiber prepreg, weaving, and final machining under one roof, compressing lead times by 50%. As production ramps, composite learning curves should narrow the cost delta versus wrought titanium, expanding addressable penetration beyond flagship wide-body cores into next-generation single-aisles and UAV engines. At the same time, titanium demand will hold firm for integrally bladed rotors and low-pressure sections where CMC brittleness remains a constraint. By 2030, hybrid metal-composite stage stacks are expected to become mainstream, providing material suppliers and forging houses with new opportunities for collaboration across the aircraft engine compressor market.

By End-User Sector: Commercial Aviation Still Rules as UAVs Surge

Commercial aviation generated 73.44% of 2024 compressor revenues as global passenger traffic surpassed pre-pandemic peaks and carriers pursued aggressive fleet renewal strategies. Every LEAP or PW1100G-JM entering service contributes decades of MRO demand, reinforcing a high-margin aftermarket tied to flight-hour contracts. Meanwhile, UAV platforms are forecasted to log a 10.85% CAGR, fuelled by defence investments in loyal-wingman concepts and civilian logistics ventures. GE and Kratos’s collaboration on compact turbofan families exemplifies the drive to cut acquisition cost below USD 2 million per engine without sacrificing thrust-to-weight ratios. Military fixed- and rotary-wing fleets are expected to offer a steady mid-single-digit CAGR as sixth-generation fighter prototypes and special-operations rotorcraft enter low-rate production.

The business jet and general aviation segments remain sensitive to macroeconomic cycles yet continue to adopt bleed-less environmental-control systems, which demand tighter compressor tolerance bands, indirectly boosting spares consumption per flight hour. Across sectors, sustainable aviation fuel mandates are consistent: all operators must manage fouling risks, which raises demand for filtration retrofits and short-interval borescope inspections. For suppliers, the aircraft engine compressor market size is increasingly split between high-volume, moderate-growth airline cores and fast-rising, small-thrust UAV engines that reward rapid design-to-production cycles. Diversifying service offerings, from power-by-the-hour for airlines to parts-availability guarantees for drone fleets, will be crucial to monetize each sector’s distinct operating profile.

By Stage Count: Multi-Stage Configurations Dominate, High-Stage Gains Pace

In 2024, multi-stage assemblies, ranging from 3 to 5 stages, dominated the aircraft engine compressor market, securing a notable 60.21% share. These assemblies strike an optimal balance between performance and manufacturability, making them the preferred choice for narrowbody and regional applications. These layouts yield pressure ratios in the low to mid-30s, providing ample bleed air for cabin pressurization while maintaining an acceptable weight. Yet demand for pressure ratios above 50:1 is driving a 6.22% CAGR in designs with more than 5 stages, particularly within the GE9X, Rolls-Royce UltraFan, and military adaptive-cycle demonstrators. Each additional stage adds machining hours and inspection nodes, increasing the bill of materials value and generating incremental revenue per delivered compressor. Single-stage units will remain limited to APUs and microturbines, where simplicity and quick-start capability take precedence over absolute efficiency.

Advances in precision electro-chemical machining and robotic airfoil polishing now permit tighter tip-clearance control, enabling designers to stack additional stages without incurring prohibitive leakage penalties. Additive manufacturing further assists by embedding serpentine cooling passages within stator walls, keeping metal temperatures in check as overall pressure climbs. Over time, OEMs are likely to converge on split-spool architectures that combine a compact, three-stage, low-pressure unit with an eight-stage, high-pressure core, thereby satisfying both cruise efficiency and transient response targets. As such, as hybrids proliferate, the aircraft engine compressor market share held by high-stage configurations will increase, even if multi-stage assemblies continue to retain dominant shipment volumes. Suppliers that master high-stage airflow modelling and automated blisk finishing will be best placed to capture this emerging premium tier.

Geography Analysis

North America retained a 41.24% stake in 2024, driven by USD 800 billion-plus US defense appropriations and established OEM footprints. GE Aerospace will invest nearly USD 1 billion in additional US manufacturing capacity in 2025, scaling the LEAP and T901 lines to meet rising domestic and foreign military sales demand. Canada fosters hybrid-electric R&D through targeted grants, while Mexico’s new Querétaro LEAP shop plans to overhaul 350 engines annually by 2030.

Asia-Pacific posts the fastest 6.75% CAGR to 2030, led by over 1,000 COMAC C919 orders and India’s Production-Linked Incentive scheme that draws component investment from GE, Safran, and Airbus. Japan’s IHI maintains 70% of the local jet-engine share, and South Korea-based tier-II suppliers benefit from “China+1” sourcing shifts. Collectively, these factors enhance the region’s position in the aircraft engine compressor market.

Europe sustains mid-single-digit growth through technology leadership and unified regulations. The European Commission’s ICAO alignment anchors fuel-efficiency goals, while the Safran–MTU EURA venture readies a next-generation turboshaft for 2040 service. The Middle East and Africa are poised to benefit from the launch of new airlines and titanium-sponge expansion projects in Saudi Arabia, thereby assuming a progressively larger role in compressor supply chains.

Competitive Landscape

The aircraft engine compressor market remains highly concentrated, with GE Aerospace, RTX Corporation, Rolls-Royce, and Safran accounting for the majority of deliveries and aftermarket billings. GE’s USD 1 billion global MRO expansion and Safran’s EUR 1 billion (USD 1.2 billion) LEAP network build-out underline the premium on life-cycle support.

Strategic collaborations shape competitive posture. GE and Kratos co-develop low-cost UAV engines, while RTX integrates PW2040 cores into JetZero’s blended-wing demonstrator, illustrating diversification into emerging propulsion niches. Technology racepoints include adaptive-cycle compressors, high-temperature CMCs, and fully additive blisks.

Supply-chain resilience now differentiates winners. Leading players dual-source titanium, on-shore CMC production, and localise machining to offset geopolitical shocks. New entrants, such as Bharat Forge and PBS Aerospace, target the UAV and light-jet sub-segments, but scale economies and certification hurdles preserve the incumbent's advantage. Overall, rivalry intensity supports continuous innovation, keeping barriers high for latecomers in the aircraft engine compressor market.

Aircraft Engine Compressor Industry Leaders

General Electric Company

RTX Corporation

Rolls-Royce plc

Safran SA

MTU Aero Engines AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: GE Aerospace and Kratos expanded their teaming agreement to advance propulsion technologies for affordable unmanned systems and collaborative combat aircraft.

- March 2025: RTX’s Pratt & Whitney and Collins Aerospace partnered with JetZero on engine integration for a blended-wing-body demonstrator using PW2040 cores.

- February 2025: The US Air Force completed detailed design reviews of adaptive-cycle engine prototypes from GE Aerospace and Pratt & Whitney under the NGAP program.

- January 2025: GE Aerospace secured an order for 210 T700 turboshaft engines for military helicopter fleets.

Global Aircraft Engine Compressor Market Report Scope

| Axial Flow |

| Centrifugal Flow |

| Axial-Centrifugal (Mixed) |

| Variable Geometry |

| Turbofan Engines |

| Turbojet Engines |

| Turboprop Engines |

| Turboshaft Engines |

| Titanium Alloys |

| Nickel-Based Superalloys |

| Composite Materials (CFRP/TMCs) |

| Stainless and Other Steels |

| Commercial Aviation |

| Military Aviation |

| Business and General Aviation |

| Unmanned Aerial Vehicles (UAVs) |

| Single-Stage |

| Multi-Stage (3 to 5) |

| High-Stage (Greater than 5) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| Compressor Type | Axial Flow | ||

| Centrifugal Flow | |||

| Axial-Centrifugal (Mixed) | |||

| Variable Geometry | |||

| Engine Type | Turbofan Engines | ||

| Turbojet Engines | |||

| Turboprop Engines | |||

| Turboshaft Engines | |||

| Material | Titanium Alloys | ||

| Nickel-Based Superalloys | |||

| Composite Materials (CFRP/TMCs) | |||

| Stainless and Other Steels | |||

| End-User Sector | Commercial Aviation | ||

| Military Aviation | |||

| Business and General Aviation | |||

| Unmanned Aerial Vehicles (UAVs) | |||

| Stage Count | Single-Stage | ||

| Multi-Stage (3 to 5) | |||

| High-Stage (Greater than 5) | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the aircraft engine compressor market?

The aircraft engine compressor market size reached USD 10.7 billion in 2025 and is projected to grow to USD 14.16 billion by 2030, reflecting a 5.76% CAGR.

Which compressor type holds the largest market share?

Axial-flow compressors led with 69.25% share in 2024, driven by their use in high-bypass turbofan engines.

Which region is growing the fastest?

Asia-Pacific is forecasted to post the quickest 6.75% CAGR from 2025-2030, supported by COMAC C919 orders and India’s manufacturing push.

Why are adaptive-cycle engines important for future growth?

Adaptive-cycle cores use variable-geometry compressors to deliver 35% range gains for next-generation fighters, opening a new high-value defense segment.

How will electrified propulsion affect compressor demand?

Hybrid-electric and hydrogen-fuel-cell systems could displace compressors in some short-haul aircraft after 2030, though long-haul and military platforms will still rely on gas-turbine compressors.

Which materials are gaining traction in compressor manufacture?

Ceramic-matrix composites are expanding at a 7.21% CAGR because they withstand higher temperatures while lowering weight versus traditional metal alloys.

Page last updated on: