Aircraft Electrification Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

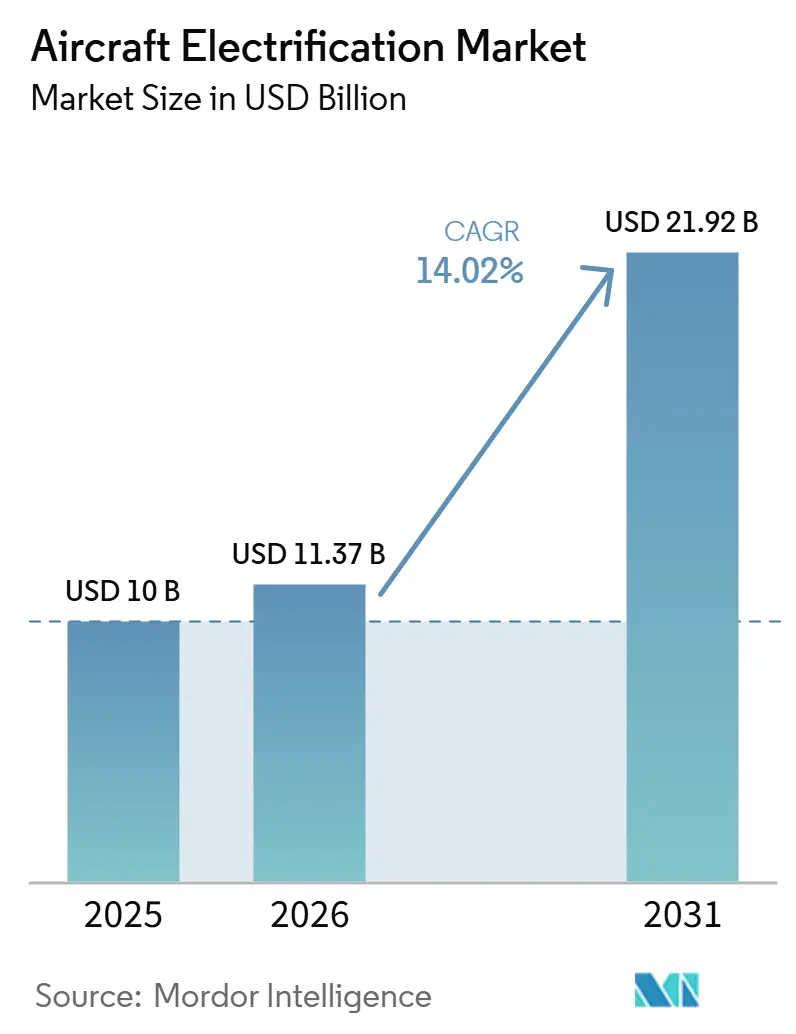

| Market Size (2026) | USD 11.37 Billion |

| Market Size (2031) | USD 21.92 Billion |

| Growth Rate (2026 - 2031) | 14.02% CAGR |

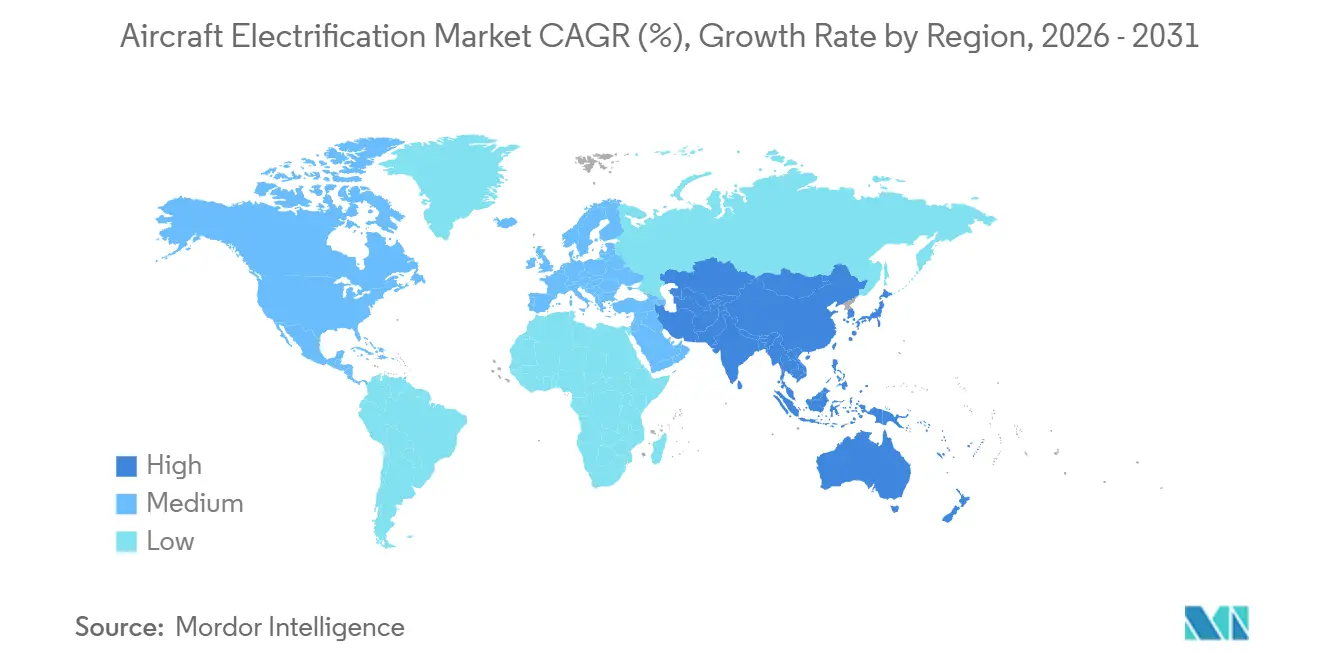

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

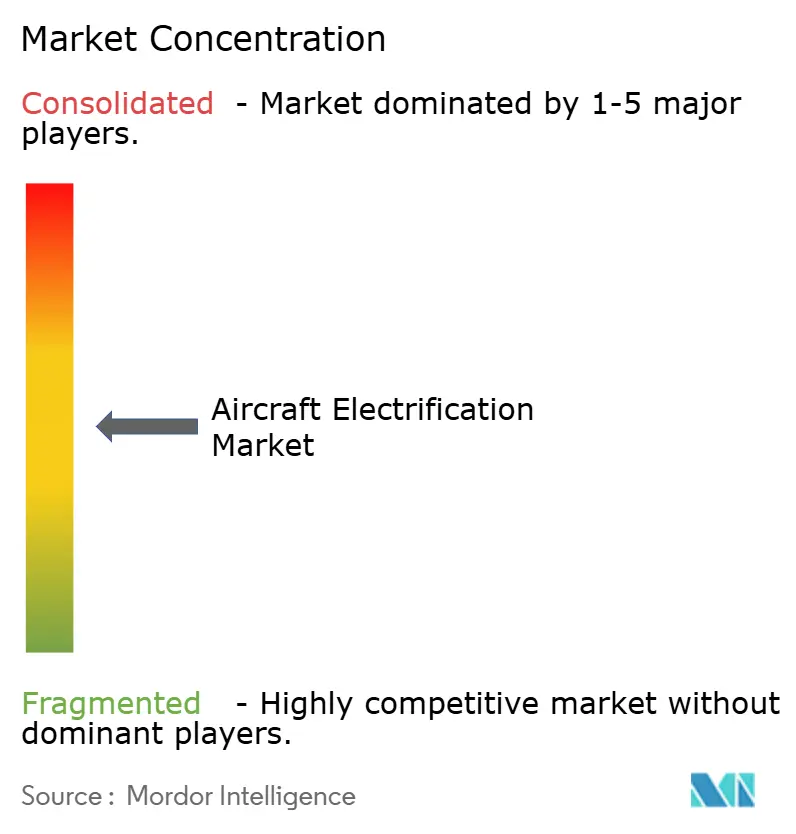

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Electrification Market Analysis by Mordor Intelligence

The aircraft electrification market size is expected to grow from USD 10.00 billion in 2025 to USD 11.37 billion in 2026, and is forecast to reach USD 21.92 billion by 2031, at a 14.02% CAGR over 2026-2031. The aircraft electrification market is expanding as airlines face firmer emissions rules and stronger pressure to lower operating emissions over long asset lives. The aircraft electrification market is moving first toward more-electric and hybrid-electric systems because these approaches better align with existing certification paths and fleet renewal cycles than full aircraft replacement. Defense programs and urban air mobility projects add demand less tied to fuel prices, giving the aircraft electrification market a broader growth base than commercial aviation alone. Competition is forming around large subsystem suppliers with deep certification experience and smaller developers that focus on propulsion, charging, and energy storage niches in the aircraft electrification market. Funding conditions remain tighter for pure-play developers, but public co-funding, infrastructure work, and steady progress in batteries and power electronics still create room for new supplier roles and long-cycle partnerships across the aircraft electrification market.

Key Report Takeaways

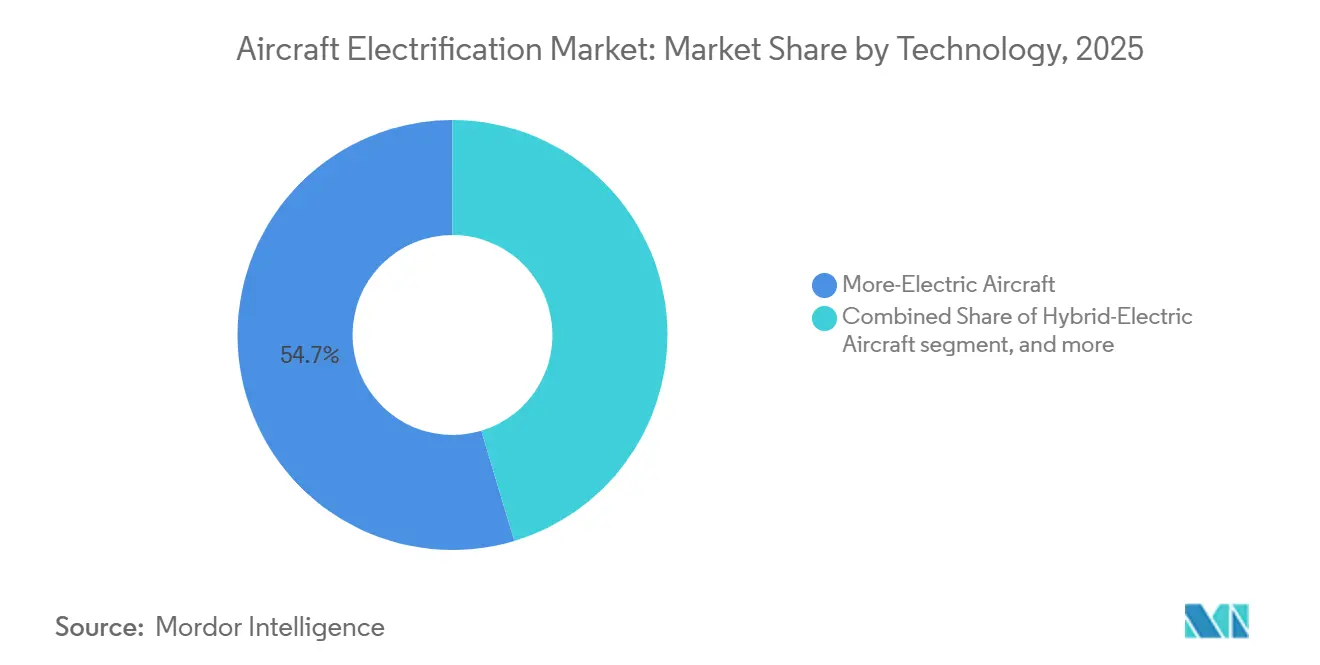

- By technology, more-electric aircraft held 54.65% share in 2025, while fully electric aircraft are projected to expand at a 19.86% CAGR through 2031.

- By platform, commercial aviation held 46.75% share in 2025, while advanced air mobility is projected to expand at a 23.90% CAGR through 2031.

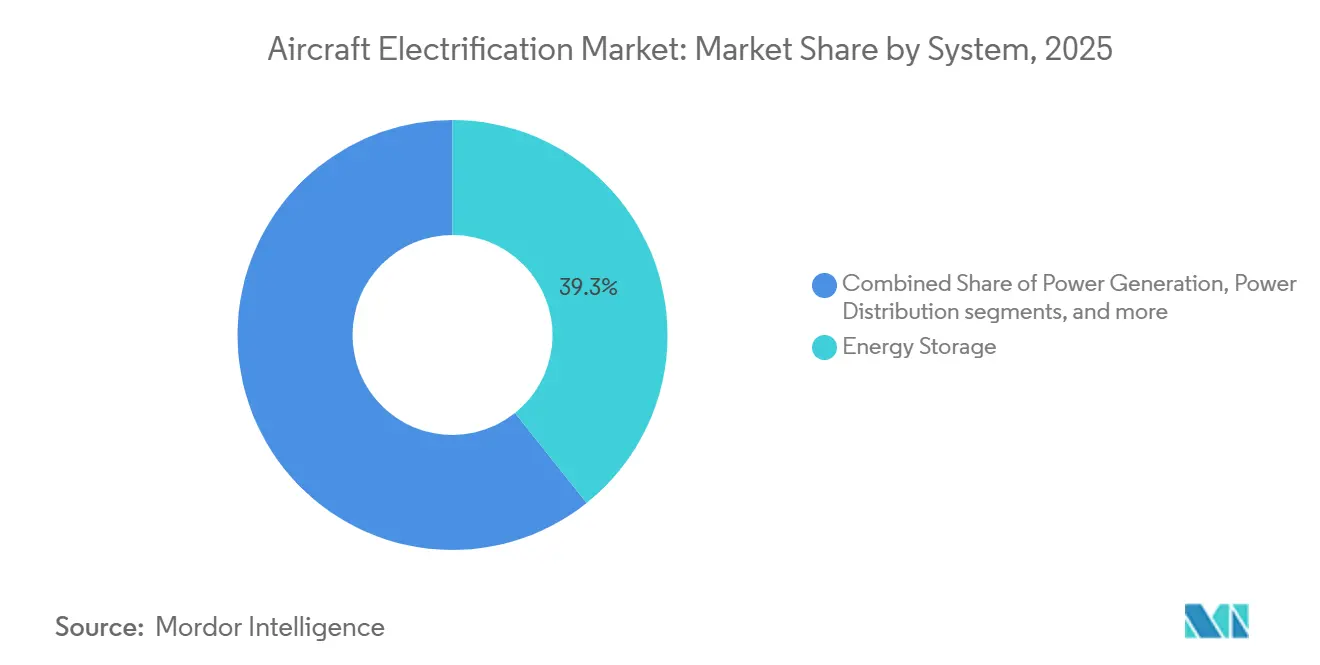

- By system, energy storage held 39.26% share in 2025, while power conversion is projected to expand at a 19.91% CAGR through 2031.

- By power class, the 500 to less than 1,000 kW segment held a 44.98% share in 2025, while the less than 100 kW segment is projected to expand at a 20.37% CAGR through 2031.

- By geography, North America held 39.38% share in 2025, while the Asia-Pacific is projected to expand at an 18.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Aircraft Electrification Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Airline-fleet net-zero mandates accelerate e-propulsion | +2.50% | Global, with Europe and North America leading compliance timelines | Short term (≤ 2 years) |

| Solid-state and Li-metal packs surpassing 450 Wh/kg | +1.80% | Global, especially US, Europe, and Asia-Pacific research clusters | Medium term (2-4 years) |

| Vertiport build-outs unlock urban air-mobility corridors | +1.50% | Middle East, Asia-Pacific, and North America | Medium term (2-4 years) |

| Power-semiconductor (SiC/GaN) cost curve halves by 2028 | +1.50% | Global, with Japan, Europe, and the US as key supply corridors | Short term (≤ 2 years) |

| Military demand for low-acoustic ISR drones | +1.20% | North America and Europe | Short term (≤ 2 years) |

| Slot-constrained regional hubs push less than 500 nm electric legs | +1.20% | Europe and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Airline Fleet Net-zero Mandates Accelerate E-propulsion

Airline net-zero commitments are turning environmental targets into near-term planning assumptions for the aircraft electrification market. IATA member airlines are committed to net-zero carbon emissions from operations by 2050, and that commitment now shapes long-range fleet decisions across major carriers.[1]International Air Transport Association, “Fly Net Zero, Commitment to Net-Zero Carbon Emissions by 2050,” International Air Transport Association, iata.org In Europe, policy-setting is becoming less forgiving as aviation operators enter a tougher carbon-cost environment in 2026, raising the value of lower-emission propulsion pathways. The Destination 2050 roadmap, updated in February 2025, also places readiness for electric and hydrogen aircraft alongside the need for infrastructure co-investment, thereby supporting longer program visibility for the aircraft electrification market. This matters most in high-frequency short-haul networks because those routes feel carbon costs sooner and can absorb hybrid-electric use cases earlier than long-haul fleets. The result is that electrification is moving from a technical option to a renewal criterion inside airline planning cycles.

Solid-state and Li-metal Packs Surpass 450 Wh/kg

Battery progress is improving the performance ceiling that supports the aircraft electrification market, even if the path remains selective by aircraft size and mission. A 2025 review in Applied Energy states that pack-level densities of 350 Wh/kg to 400 Wh/kg by 2035 are needed to make hybrid-electric commuter aircraft viable.[2]Javier De Souza et al., “Battery Technology for Sustainable Aviation, A Review of Current Trends and Future Prospects,” Applied Energy, sciencedirect.com That threshold matters because it moves the discussion away from basic feasibility and toward which regional missions can become commercially practical first. The user-supplied material also points to 2026 test activity in solid-state and lithium-metal systems, which supports the view that the technology curve is improving faster than earlier aviation roadmaps assumed. An automotive scale is also likely to help with cell sourcing, as pilot production programs outside aerospace can lower manufacturing costs before aviation-specific volumes become meaningful. This leaves the aircraft electrification market with a clearer medium-term route in commuter aircraft, eVTOL platforms, and other short-range designs where battery weight can be managed.

Vertiport Build-outs Unlock Urban Air-mobility Corridors

Physical infrastructure is becoming a direct enabler of revenue timing in the aircraft electrification market. In April 2026, Dubai’s Roads and Transport Authority and Skyports Infrastructure completed the world’s first commercial vertiport near Dubai International Airport, with a facility designed for up to 42,000 annual aircraft movements. That milestone matters because infrastructure approvals establish practical operating frameworks for charging, passenger handling, and airspace coordination, not just for parking aircraft. Each completed site also provides regulators and operators with a working precedent that can shorten subsequent rollout cycles in other cities. This is especially relevant for advanced air mobility, where certification progress must align with usable ground networks before commercial service can scale. As a result, vertiport work functions as market creation rather than simple capacity addition inside the aircraft electrification market.

Military Demand for Low-acoustic ISR Drones

Defense demand is providing the aircraft electrification market with an important second growth channel beyond civil airline economics. The military case is driven by quiet surveillance, lower thermal signatures, and mission flexibility, which makes hybrid-electric and electric systems valuable even when fuel savings are not the main objective. In practice, that pushes development toward better motor efficiency, tighter battery management, and improved inverter performance because acoustic performance matters at the mission level. The same supply chain can then serve commercial applications, especially in UAVs and smaller aircraft, where dual-use components move more easily across end markets. This effect is important because defense budgets can support validation work during periods when private venture capital becomes less patient. It also means the aircraft electrification market benefits from a technical baseline shaped by defense-grade reliability standards.

Restraints Impact Analysis of Aircraft Electrification Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Battery energy gap vs. Jet-A (More than 30× lower) | -2.50% | Global, with the highest effect on narrowbody and widebody aircraft | Long term (≥ 4 years) |

| Sparse MW-class charging at secondary airports | -1.20% | Global, especially secondary airports in South America, the Middle East and Africa, and parts of Europe | Medium term (2-4 years) |

| Rare-earth magnet supply-chain volatility | -1.00% | Global, with the US and Europe more exposed to external supply concentration | Short term (≤ 2 years) |

| Investor pullback post-SPAC stalls late-stage OEMs | -0.90% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Battery Energy Gap vs. Jet-A (More than 30x Lower)

The energy density gap remains the main structural limit on how far the aircraft electrification market can move toward full-electric flight by 2031. NASA work cited in the user-supplied draft shows that current battery chemistry does not support all-electric operation for larger commercial aircraft, including the 150-passenger class. The problem is not whether batteries are improving, but whether they are improving fast enough to offset the mass and volume penalties that arise as mission range and passenger count increase. That keeps the near-term commercial path centered on hybrid-electric architectures and smaller fully electric aircraft rather than broad replacement of narrowbody fleets. It also narrows the strongest near-term opportunities in the aircraft electrification market to UAVs, eVTOLs, and short regional platforms. Until battery chemistry closes more of that gap, the addressable market for full electrification will remain selective.

Sparse MW-class Charging at Secondary Airports

Airport charging infrastructure is a separate bottleneck that can slow the aircraft electrification market, even as aircraft technology continues to advance. A 2026 US GAO report states that only 47 US airports had identified charging stations for electric aircraft in airport plans as of December 2025. Regional electric aircraft also require high-power turnaround capability, and the user-supplied material notes that a 30-seat aircraft with a 1 MWh battery would need a 1.5-2 MW charging connection for a 30-minute turnaround. That requirement exceeds the current grid capacity of many secondary airports, especially the very airfields that are the most natural early deployment points for short electric routes. The challenge is therefore not only the availability of hardware but also who pays for utility upgrades and how quickly those upgrades can be permitted. This leaves the aircraft electrification market dependent on airport grants, utility coordination, and consortium-style funding in the first phase of regional deployment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Aircraft Electrification Market Segment Analysis

By Technology:

Incremental to Fully ElectricMore-electric aircraft held 54.65% of the aircraft electrification market share in 2025, indicating that the market still favors lower-risk adoption paths over abrupt platform changes. These aircraft use electrified actuation, environmental control, and onboard power distribution across current narrowbody and widebody fleets, so they fit existing production programs more easily than new propulsion concepts. That installed-base advantage keeps more-electric aircraft at the center of revenue generation across the aircraft electrification market through the forecast period. Hybrid-electric aircraft remain smaller today, but they are strategically important because they bridge current battery limits and the emissions needs of short regional missions. GE Aerospace completed the first integrated ground test of a megawatt-class hybrid-electric engine system in June 2026, which shows that the hybrid pathway is moving from concept work toward flight-ready validation.[3]GE Aerospace, “GE Aerospace Completes Ground Test of Megawatt-Class Hybrid Electric Engine System,” GE Aerospace, geaerospace.com

Fully electric aircraft are the fastest-growing technology segment, with a projected 19.86% CAGR from 2026 to 2031, because the first workable use cases sit in smaller aircraft, UAVs, and eVTOL designs. The regulatory landscape is also becoming more clearly defined for the aircraft electrification market, especially in the sub-19-seat category, which aligns with current commercial activity. The Federal Register (FAR) published final special conditions for ZeroAvia’s ZA601 600 kW electric engine in March 2026, marking a practical step in establishing certification precedent for future electric propulsion programs. ZeroAvia’s order pipeline of more than 3,000 preorders also suggests that long-term supplier positions are already being contested before full volume commercialization begins.

By Platform:

Commercial still Rules, Advanced Air Mobility SurgesCommercial aviation accounted for 46.75% of the aircraft electrification market in 2025 because large fleet operators and major OEM production lines adopt more-electric systems faster than any other platform group. The segment benefits from the widespread adoption of electrified subsystems that do not require an immediate shift to full-electric propulsion, thereby keeping adoption tied to current aircraft programs and retrofit paths. It also gains support from the rule finalized in July 2025, because lighter and training-oriented aircraft categories can now move through a broader certification path for electric designs. This makes business and general aviation an important bridge between prototype activity and recurring delivery volume in the aircraft electrification market. Military aircraft and UAVs remain commercially relevant because they sustain demand for electric motors, batteries, power conversion, and low-signature mission systems outside airline purchasing cycles.

Advanced air mobility is the fastest-growing platform segment, with a 23.90% CAGR through 2031, as aircraft certification, charging readiness, and city-level operating plans advance in tandem across several regions. The aircraft electrification industry is especially visible here because platform design, software, charging, infrastructure, and operating approval all need to mature in parallel. Dubai’s commercial vertiport completion in April 2026 is a clear example of this alignment, since the facility was designed to support Joby Aviation’s future air taxi operations near a major airport. The same pattern is appearing beyond a single geography, with new testing and supply chain activity in India, China, Japan, and the Middle East. That gives the aircraft electrification market a platform category where commercial timing is now linked as much to infrastructure rollout as to aircraft readiness.

By System:

Batteries Rule Spend, Power Electronics AccelerateEnergy storage accounted for 39.26% of the aircraft electrification market size in 2025, reflecting the central role of batteries, fuel cells, and energy management architectures across every aircraft concept now in development. This segment leads because no electric or hybrid design can progress without workable storage performance, so investment tends to cluster here before it spreads across the rest of the system stack. The aircraft electrification market also depends more heavily on energy storage than many adjacent aerospace technology themes because battery performance directly shapes range, payload, turnaround time, and economics. Power distribution and power generation remain major contributors as aircraft move toward high-voltage architectures and more integrated electrical loads. Airbus’s LEIA program, which runs from December 2025 to 2027 and targets TRL 5 for a hybrid-electric non-propulsive energy architecture, shows how leading OEMs are developing generation and distribution together rather than as isolated modules.

Power conversion is the fastest-growing system segment, with a 19.91% CAGR from 2026 to 2031, as efficient inverters and converters become a core performance lever across the aircraft electrification market. A 2025 paper in IEEE Transactions on Power Electronics described flight-tested silicon carbide propulsion drive systems for hybrid-electric aerospace applications, supporting the move toward higher-power-density conversion systems. This system category matters because better conversion efficiency lowers thermal management pressure and improves the value of every kilowatt stored or generated onboard. It also gives established suppliers a strong foothold because certification depth, semiconductor relationships, and system integration capability are hard to replicate quickly. That is why power conversion is emerging as one of the most contested parts of the aircraft electrification market.

By Power Class:

Dual-Track EvolutionThe 500 to less than 1,000 kW power class accounted for 44.98% of the aircraft electrification market in 2025, reflecting the near-term fit between current battery capabilities and regional hybrid-electric aircraft concepts. This range aligns with turboprop hybrid conversions, advanced rotorcraft work, and megawatt-class demonstrators that target future commuter and regional missions. It also sits close to the practical center of near-term commercial viability because the aircraft are large enough to create meaningful value but still small enough to manage current energy density limits. The 100 to less than 500 kW class supports smaller commuter platforms and some advanced eVTOL configurations, while the greater than 1,000 kW class is still dominated by test and validation activity. GE Aerospace’s 2026 ground test milestone supports that reading, as very high-power propulsion is still undergoing staged validation before routine commercial deployment.

The less than 100 kW class is the fastest-growing power segment, with a projected 20.37% CAGR through 2031, because lightweight UAVs and early eVTOL designs can reach useful commercial milestones faster than larger aircraft. The aircraft electrification industry is most dynamic in this band because new entrants can iterate on hardware and software faster than large commercial programs can. magniX launched the MagniAIR 175 kW electric engine in April 2026 for general aviation, and while that rating sits above the sub-100 kW threshold, it still signals how adjacent lower-power designs are maturing into product families. Customer behavior also differs by band, with tactical UAV and startup-led purchases shaping the lower end while airlines and defense OEMs dominate procurement in the mid-range. That split keeps the aircraft electrification market segmented not only by power level, but also by buying cycle, certification speed, and capital profile.

Geography Analysis

North America retained 38.98% revenue in 2025, underpinned by the FAA’s early issuance of special-conditions airworthiness standards for eVTOLs and hybrid regional transports. US state incentives cover battery-module plants in Connecticut and Washington, strengthening domestic supply resilience. Canada’s Sustainable Aviation Technology program co-funds hydrogen-combustion demonstrations that share component commonality with hybrid-electric architectures, further anchoring regional supply networks.

Europe codifies a complementary ruleset through EASA, creating mutual-recognition pathways with the FAA to shorten certification cycles. France funnels EUR 100 million (USD 117.69 million) into nine zero-carbon aircraft projects under the France 2030 banner, expanding the talent pool for megawatt-motor design. The UK’s Future of Flight plan targets routine eVTOL service by 2028, unlocking city-center vertiport tenders and supporting the broader aircraft electrification market across the continent.

Asia-Pacific posts the fastest growth, at an 18.28% CAGR through 2031, driven by economies of scale in battery manufacturing and urbanization. CATL leverages automotive-sector tooling to fast-track aviation-grade cell production, while Japanese chipmakers supply gallium-nitride (GaN) wafers critical for 1 MHz inverter switching. Australian and New Zealand test ranges facilitate early flight trials with lower air-traffic congestion, shaving certification time for regional air-taxi models. Despite regulatory lags, manufacturing cost advantages, and policy enthusiasm around electric mobility, the region is a pivotal node within the aircraft electrification market value chain.

Competitive Landscape

The aircraft electrification market shows medium concentration, with Honeywell Aerospace Inc., Safran SA, Airbus SE, Rolls-Royce Holdings plc, and RTX Corporation holding strong positions in power generation, power distribution, and energy storage subsystems. These companies benefit from certification depth, installed relationships with OEMs, and better access to government-backed development programs than their smaller peers usually have. The aircraft electrification market is therefore not evenly fragmented across the value chain, as subsystems with high safety and integration requirements are already concentrated among large aerospace groups. GKN Aerospace, Thales, BAE Systems, and Moog also remain important because they support actuation, conversion electronics, and energy management areas that scale with more-electric aircraft adoption. This structure gives incumbents a durable advantage in the revenue-heavy parts of the market, even while startups shape much of the technology direction.

Several strategic moves in 2025 and 2026 show how competition is being built through partnerships, production capacity, and certification progress. GE Aerospace completed the first integrated ground test of its megawatt-class hybrid-electric engine system in June 2026, which strengthens its position in larger hybrid propulsion architectures. Honeywell signed a USD 500 million multi-year framework agreement with the US Department of Defense (DoD) in March 2026 to expand production capacity for navigation systems, actuators, and power systems for more-electric and hybrid aircraft. ZeroAvia advanced its regulatory position when the FAA published final special conditions for the ZA601 electric engine in March 2026, giving the company a tangible certification milestone in the propulsion race. Those moves show that the advantage in the aircraft electrification market is being built through proof points that are hard for late entrants to replicate quickly.

Pure-play developers still matter because they move faster on new propulsion concepts, small-aircraft applications, and specialized infrastructure niches. The aircraft electrification market depends on them for experimentation in hydrogen-electric systems, eVTOL operations, charging hardware, and software-led energy management. Yet the funding environment is tighter than it was during the earlier SPAC cycle, which gives large incumbents more room to expand through co-funded programs and supplier capture. This creates a mixed structure in which startups drive design ambition while established aerospace groups retain a stronger position in manufacturing scale, certification, and program continuity. The clearest white-space areas remain MW-class charging, aviation-grade solid-state cell supply, and hybrid energy management software, as demand is outpacing the current qualified supplier base.

Aircraft Electrification Industry Leaders

Safran SA

RTX Corporation

Airbus SE

Honeywell Aerospace Inc.

Rolls-Royce Holdings plc

- *Disclaimer: Major Players sorted in no particular order

Aircraft Electrification Market Companies Covered in this Report

- Honeywell Aerospace Inc.

- Safran SA

- General Electric Company

- Rolls-Royce Holdings plc

- RTX Corporation

- Airbus SE

- Ampaire Inc.

- ZeroAvia, Inc.

- Wright Electric Inc.

- magniX USA, Inc.

- GKN Aerospace Services Limited

- Thales Group

- BAE Systems plc

- Astronics Corporation

- Moog Inc.

- EaglePicher Technologies, LLC

- Crane Company

Recent Industry Developments in Aircraft Electrification Market

- June 2026: GE Aerospace completed ground testing of a megawatt-class hybrid-electric engine system developed with NASA, clearing the way for flight trials of a propulsion technology widely regarded as a potential pathway to lower-emission commercial aviation.

- July 2025: Electra partnered with the US Army through a USD 1.90 million Small Business Innovation Research (SBIR) contract to advance hybrid-electric powertrain and propulsion systems (HEPPS). This collaboration focuses on enhancing fuel efficiency, extending range, and enabling new mission capabilities for current and future Army aircraft by leveraging Electra’s expertise.

- May 2025: Vertical Aerospace and Honeywell expanded their partnership to bring the VX4 eVTOL to market. Under a USD 1 billion contract, they target at least 150 aircraft deliveries by 2030.

- March 2025: RTX’s Pratt & Whitney and Collins Aerospace joined JetZero to supply systems for a blended-wing-body demonstrator powered by PW2040 engines aimed at 50% fuel-burn reduction.

Global Aircraft Electrification Market Report Scope

Aircraft electrification refers to the replacement of traditional mechanical, hydraulic, and pneumatic aircraft systems with electrical alternatives. It ranges from partially electric systems to fully electrified propulsion, to reduce emissions, improve fuel efficiency, and minimize maintenance costs in the aviation sector.

The aircraft electrification market is segmented by technology, platform, system, power class, and geography. By technology, the market is segmented into more-electric, hybrid-electric, and fully electric aircraft. By platform, the market is segmented into commercial, military, unmanned aerial vehicles (UAVs), and advanced air mobility. By system, the market is segmented into power generation, power distribution, power conversion, and energy storage. By power class, the market is segmented into less than 100 kW, 100 to less than 500 kW, 500 to less than 1,000 kW, and greater than 1,000 kW. The report also covers the market sizes and forecasts for the aircraft electrification market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

Segmentation Overview

| More-Electric Aircraft |

| Hybrid-Electric Aircraft |

| Fully Electric Aircraft |

| Commercial | Narrowbody |

| Widebody | |

| Regional Jets | |

| Business Jets and General Aviation Aircraft | |

| Commercial Helicopters | |

| Military | Fighter Jets |

| Transport Aircraft | |

| Special Mission Aircraft | |

| Military Helicopters | |

| Unmanned Aerial Vehicles (UAVs) | |

| Advanced Air Mobility |

| Power Generation |

| Power Distribution |

| Power Conversion |

| Energy Storage |

| Less than 100 kW |

| 100 to Less than 500 kW |

| 500 to Less than 1,000 kW |

| Greater than 1,000 kW |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Technology | More-Electric Aircraft | ||

| Hybrid-Electric Aircraft | |||

| Fully Electric Aircraft | |||

| By Platform | Commercial | Narrowbody | |

| Widebody | |||

| Regional Jets | |||

| Business Jets and General Aviation Aircraft | |||

| Commercial Helicopters | |||

| Military | Fighter Jets | ||

| Transport Aircraft | |||

| Special Mission Aircraft | |||

| Military Helicopters | |||

| Unmanned Aerial Vehicles (UAVs) | |||

| Advanced Air Mobility | |||

| By System | Power Generation | ||

| Power Distribution | |||

| Power Conversion | |||

| Energy Storage | |||

| By Power Class | Less than 100 kW | ||

| 100 to Less than 500 kW | |||

| 500 to Less than 1,000 kW | |||

| Greater than 1,000 kW | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2031 outlook for aircraft electrification?

The aircraft electrification market is forecast to reach USD 21.92 billion by 2031 from USD 11.37 billion in 2026, at a 14.02% CAGR over 2026-2031.

Which technology segment leads current demand?

More-electric aircraft led in 2025 with 54.65% share because they fit existing aircraft programs and avoid the certification burden of fully new propulsion architectures.

Which platform is growing the fastest through 2031?

Advanced air mobility is the fastest-growing platform, with a projected 23.90% CAGR through 2031 as eVTOL certification and vertiport development progress together.

Why is full-electric adoption still limited in larger aircraft?

Battery energy density remains far below jet fuel, which keeps full-electric use focused on smaller aircraft, UAVs, and short regional missions in the current forecast window.

Which region is leading current revenue and which is growing the fastest?

North America held the largest share in 2025 at 39.38%, while Asia-Pacific is projected to expand the fastest at an 18.28% CAGR through 2031.

Where are the strongest competitive opportunities emerging?

The clearest openings are in MW-class charging, aviation-grade solid-state battery supply, and hybrid energy management software, where demand is rising faster than the qualified supplier base.

Page last updated on: