Dried Soup Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 6.81 Billion |

| Market Size (2031) | USD 7.33 Billion |

| Growth Rate (2026 - 2031) | 1.49% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

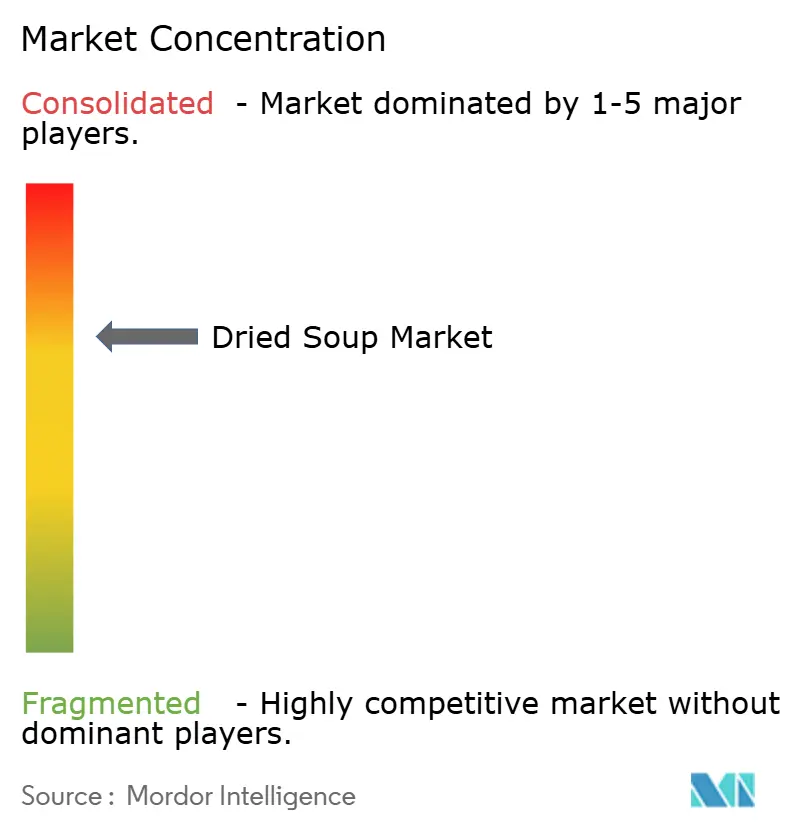

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Dried Soup Market Analysis by Mordor Intelligence

The dried soup market size is expected to grow from USD 6.71 billion in 2025 to USD 6.81 billion in 2026 and is forecast to reach USD 7.33 billion by 2031 at 1.49% CAGR over 2026-2031. This muted growth pattern signals a mature category in which legacy brands contend with consumers who now scrutinize price, nutrition, and ingredient transparency as strongly as they once prioritized convenience. Authenticity narratives, plant-forward formulations, and digital-first retail experiences are recasting the value of categories, forcing incumbents to justify their shelf space through differentiated propositions. In parallel, urbanization drives higher demand for portable meals. However, increased consumer interest in cooking and improved availability of fresh food have reduced the consumption of packaged food products. The market competition has shifted beyond traditional concentration metrics, as niche companies build customer retention through targeted brand positioning and direct-to-consumer distribution models.

Key Report Takeaways

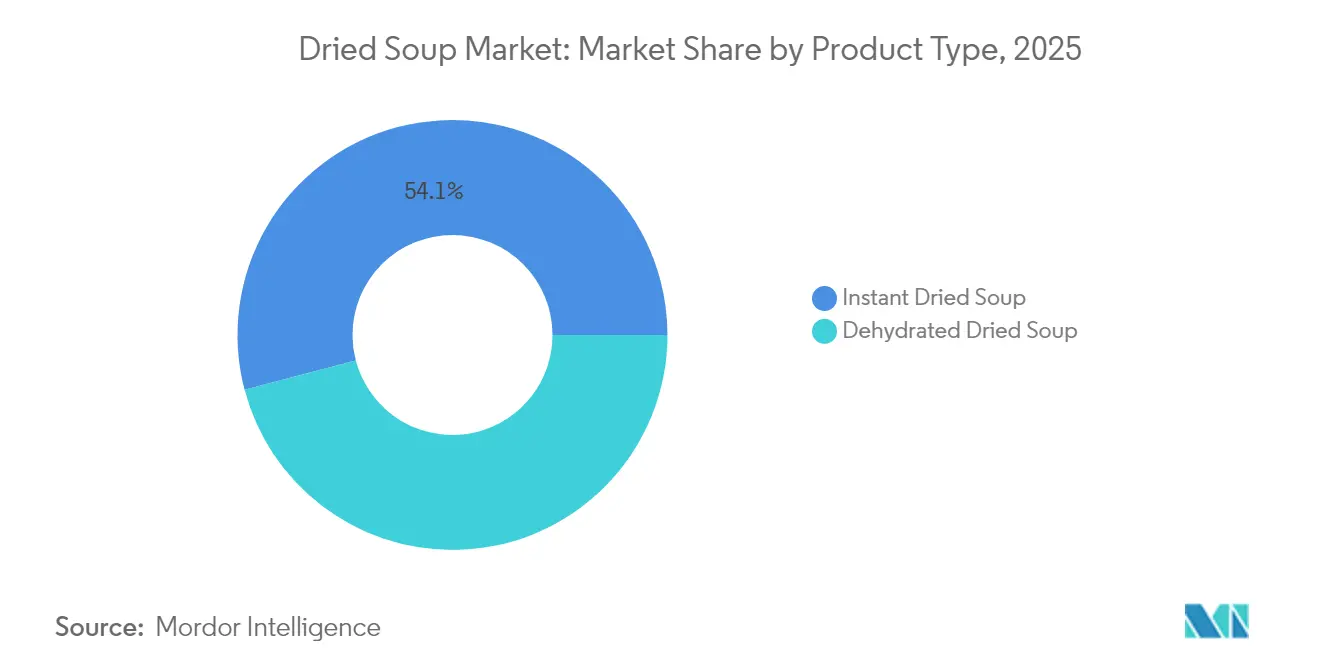

- By product type, instant variants held 54.10% of the dried soup market share in 2025 and are projected to expand at a 1.78% CAGR between 2026-2031.

- By category, vegetarian formulations accounted for 51.30% of the dried soup market size in 2025 and are poised for a 1.96% CAGR growth through 2031.

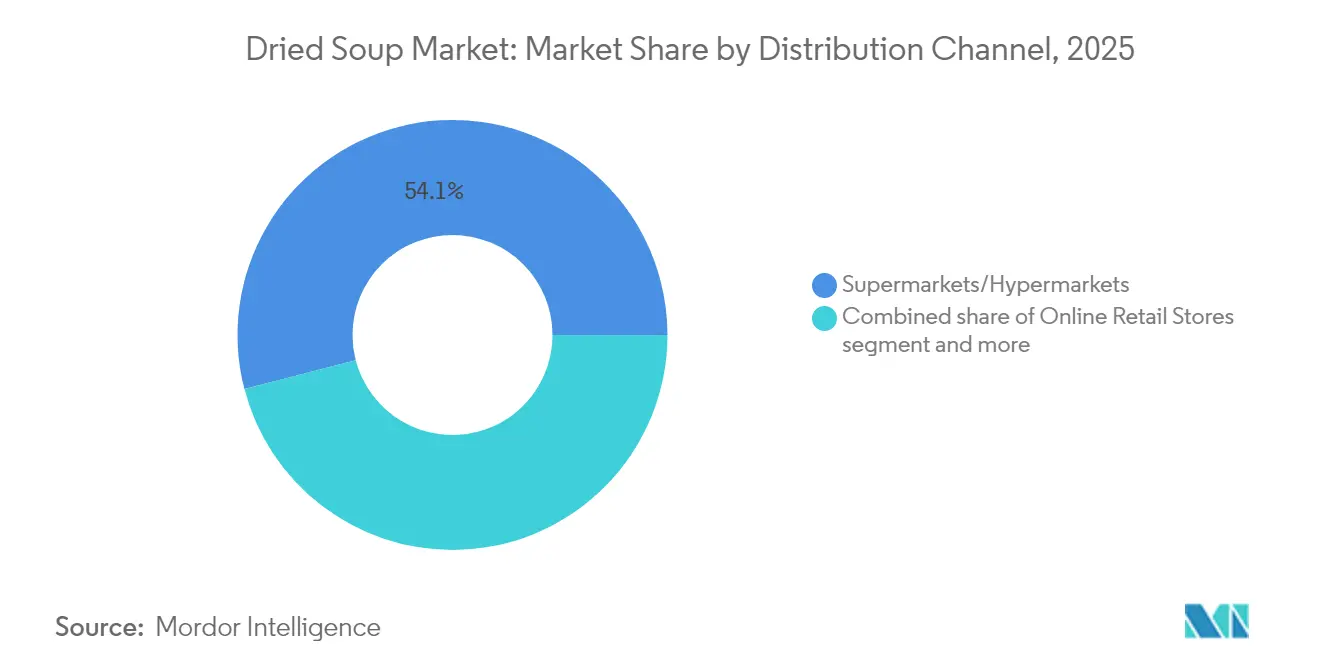

- By distribution channel, supermarkets/hypermarkets commanded 54.05% revenue in 2025, while online retail is set to record the fastest 2.55% CAGR to 2031.

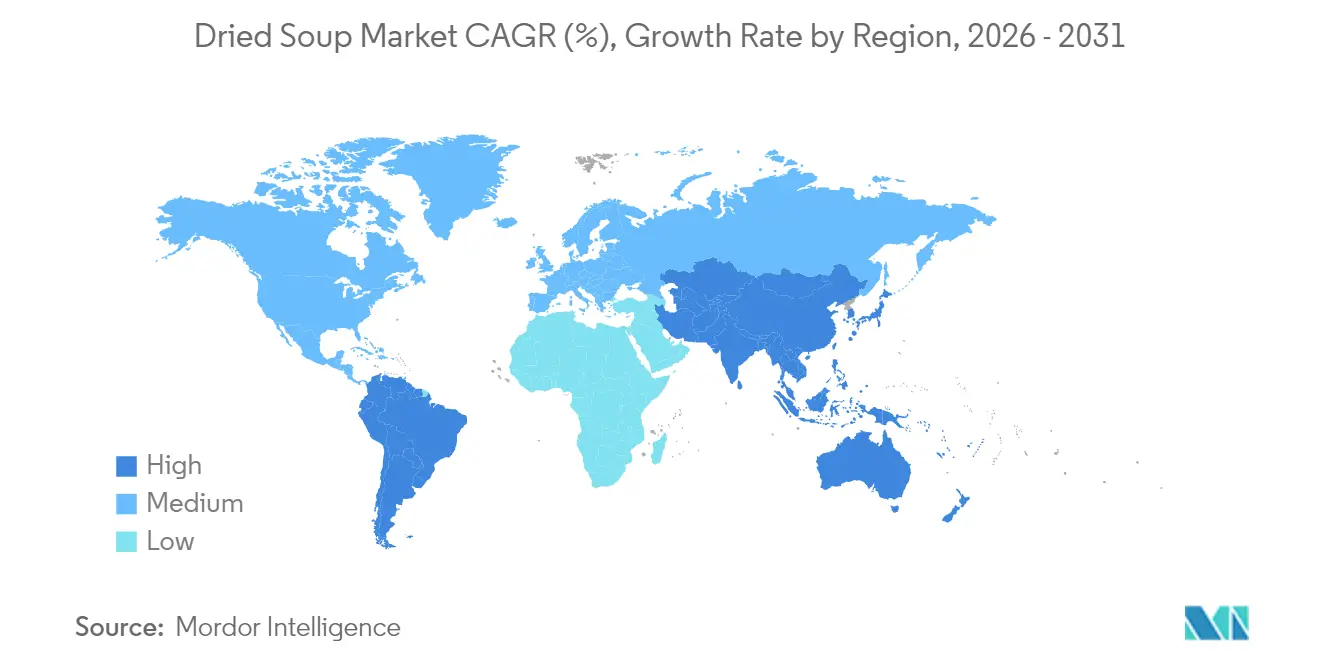

- By geography, Asia-Pacific captured 33.20% of global revenue in 2025 and is forecast to lead with a 2.82% CAGR over the next five years.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Dried Soup Market*

| Driver | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising popularity of vegan and plant-based soups | +0.5% | Global, with Asia-Pacific and North America leading | Medium term (2-4 years) |

| Premiumization and gourmet soups | +0.3% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Sustainable and eco-friendly packaging | +0.4% | Europe leading, Global adoption | Medium term (2-4 years) |

| Long shelf life and portability | +0.2% | Global, particularly emerging markets | Short term (≤ 2 years) |

| Influence of social media and influencers | +0.1% | Global, strongest in Asia-Pacific and North America | Short term (≤ 2 years) |

| Demand for quick and easy meal solutions | +0.2% | Global, urban centers priority | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising popularity of vegan and plant-based soups

Plant-based formulations are expanding the market as manufacturers develop alternatives that meet consumer demand for ethical and health-conscious products. According to the International Food Information Council data from 2024, 3% of the United States population consumed plant-based food exclusively, while 55% incorporated it for health benefits [1]Source: International Food and Information Council, "2024 IFIC Food & Health Survey", foodinsight.org. The trend has evolved beyond simple ingredient substitution to transform the entire value chain, establishing plant-based soups as premium products. The combination of health, environmental, and ethical factors drives demand growth across various demographic segments. Manufacturers are expanding their product portfolios to include innovative plant-based ingredients, diverse flavor profiles, and enhanced nutritional content to capture a broader consumer base. This expansion strategy encompasses new product development, improved distribution channels, and targeted marketing campaigns to increase market penetration.

Premiumization and gourmet soups

Premium positioning enables manufacturers to maintain profitability through differentiated offerings that command higher prices, helping offset commodity price volatility and margin pressure. This strategy is particularly effective in developed markets where consumers increasingly view food as a lifestyle choice rather than basic sustenance. Products featuring gourmet ingredients, organic certifications, and specialized recipes create meaningful differentiation from private label competitors. The incorporation of premium ingredients and innovative formulations allows manufacturers to establish unique value propositions that resonate with quality-conscious consumers. Manufacturers are investing in research and development to create sophisticated product variants that justify premium pricing. As commodity inflation continues to affect standard product margins, manufacturers are strategically shifting their portfolios toward premium offerings to preserve and enhance profitability in competitive market conditions. This transition requires careful market analysis, consumer insight integration, and strategic pricing decisions to ensure the successful implementation of premium positioning strategies.

Sustainable and eco-friendly packaging

Packaging innovation drives competitive differentiation as regulatory pressure and consumer awareness converge to demand environmental responsibility throughout the value chain. Sysco's packaging innovation contest in 2024 highlighted biodegradable solutions, including Cargill's beef packaging, Superior Foods' bio bags, and PA x PulPac's dry molded fiber containers, demonstrating industry-wide commitment to sustainable materials. The foodservice sector's embrace of sustainable packaging creates downstream pressure on consumer packaged goods manufacturers to adopt similar materials to maintain supply chain compatibility. European markets lead adoption due to stringent regulatory frameworks, but global implementation accelerates as cost differentials narrow and consumer preferences shift toward environmentally responsible brands. Sustainable packaging initiatives extend beyond material substitution to encompass entire lifecycle assessments that optimize transportation efficiency and end-of-life disposal options. The integration of sustainability metrics into corporate reporting frameworks creates accountability mechanisms that drive continuous improvement in packaging environmental performance.

Long shelf life and portability

The long-term storage capability of dried soups establishes them as fundamental inventory items, ensuring food availability and operational efficiency during supply chain interruptions. Technological advances in dehydration and preservation extend product viability while maintaining flavor integrity, enabling manufacturers to reduce food waste throughout the distribution chain. Portability features particularly resonate with urban consumers who prioritize convenience and space efficiency in compact living environments where storage optimization becomes critical. The combination of extended shelf life and compact packaging creates value propositions that appeal to emergency preparedness markets, outdoor recreation segments, and international shipping applications where traditional fresh alternatives prove impractical. Supply chain resilience considerations following recent global disruptions reinforce consumer preference for products that provide meal security without compromising nutritional quality.

Restraints Impact Analysis of Dried Soup Market*

| Restraint | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer preference for fresh and homemade alternatives | -0.3% | Global, strongest in developed markets | Long term (≥ 4 years) |

| Negative perceptions regarding healthiness | -0.2% | North America and Europe primarily | Medium term (2-4 years) |

| Production efficiency challenges | -0.2% | Global, acute in emerging markets | Medium term (2-4 years) |

| Supply chain disruptions | -0.1% | Global, with regional concentration risks | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Consumer preference for fresh and homemade alternatives

Health consciousness and culinary engagement drive consumer migration toward fresh ingredients and home preparation methods that provide greater control over nutritional content and flavor customization. Pandemic-induced cooking skill development created lasting behavioral changes as consumers discovered satisfaction in meal preparation and ingredient sourcing that extends beyond convenience considerations. Social media platforms amplify fresh cooking trends through recipe sharing and cooking demonstrations that position homemade alternatives as achievable and desirable lifestyle choices. The availability of fresh ingredients through improved supply chains and online grocery delivery reduces barriers to home cooking that previously favored processed alternatives. Economic considerations increasingly favor fresh ingredients as commodity price inflation affects packaged goods more severely than basic agricultural products, creating cost advantages for home preparation.

Negative perceptions regarding healthiness

Consumers increasingly view processed foods negatively due to their artificial additives, high sodium levels, and limited nutritional value, which contradict current health and wellness preferences. The perception of processed foods as unhealthy has led to a shift in consumer behavior, with many actively seeking alternatives that align with their wellness goals. Manufacturers face heightened regulatory oversight, requiring product reformulations to reduce sodium, artificial preservatives, and flavor enhancers. These regulatory changes aim to address public health concerns and align with evolving consumer preferences for healthier options. The clean label movement's demand for ingredient transparency and simpler formulations challenges traditional dried soup production methods, forcing manufacturers to reconsider their production processes and ingredient sourcing. The need to reformulate products and adjust marketing strategies to address health concerns requires significant investment in research, development, and new manufacturing processes. However, price sensitivity in these categories may limit potential returns, creating a challenging balance between meeting consumer demands and maintaining profitability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Dried Soup Market Segment Analysis

By Product Type:

Instant Variants Lead Through Convenience InnovationInstant dried soup holds a 54.10% market share in 2025 and is projected to grow at a 1.78% CAGR through 2031. This growth stems from improved flavor preservation technology and simplified preparation methods that attract time-pressed consumers. The instant segment's market leadership reflects consumers' preference for convenience over traditional cooking, especially in urban areas where limited kitchen space and time favor quick meal solutions. Dehydrated dried soup variants make up the remaining market share, positioning themselves as premium options with enhanced flavor profiles and visible ingredients for consumers who can dedicate more time to preparation.

Improved manufacturing processes in instant soup production reduce costs while maintaining profit margins across distribution channels. The segment's growth aligns with increasing global urbanization, which drives consistent demand for convenient meal options among working professionals and single-person households. Product development in the instant segment now emphasizes organic certification, plant-based options, and unique flavors to distinguish products from standard offerings and support premium pricing. For instance, in October 2023, the Atlante company launched a range of instant legume cup soups, available in different flavors such as curry, picante, and Mediterranean. The products are vegan-friendly and rich in protein.

By Category:

Plant-Based Momentum Drives Vegetarian LeadershipVegetarian soup formulations command 51.30% market share in 2025 and project the fastest growth at 1.96% CAGR through 2031, reflecting global dietary shifts that extend beyond ethical considerations to encompass health and environmental sustainability priorities. According to the Food Frontier 2024 survey on dietary behaviors in Australia, health improvement emerged as the dominant driver, with 60% of vegetarian diet participants selecting health benefits as their primary motivation. Environmental factors influenced 33% of respondents, while ethical considerations drove 26% of participants . The category's leadership position demonstrates successful manufacturer adaptation to changing consumer preferences through expanded plant-based protein options and enhanced flavor profiles that satisfy both vegetarian and flexitarian consumers. Non-vegetarian variants maintain a significant market presence through premium positioning and protein-forward formulations that appeal to fitness-conscious demographics seeking convenient post-workout nutrition solutions.

The vegetarian soup segment demonstrates lower input costs as plant-based proteins exhibit reduced price fluctuations compared to animal proteins, maintaining profit margins during commodity price increases. Research and development in vegetarian soups incorporates functional components, including probiotics, superfoods, and adaptogens, establishing these products as health and wellness offerings rather than convenience items. Plant-based formulation manufacturing enables operational efficiency through consistent raw material procurement and uniform production methods across multiple geographic regions.

By Distribution Channel:

Digital Migration Accelerates Despite Traditional DominanceOnline retail stores emerge as the fastest-growing distribution channel at 2.55% CAGR through 2031, despite supermarkets and hypermarkets maintaining 54.05% market share in 2025, reflecting pandemic-accelerated digital adoption that creates new competitive dynamics in food retail. South Korea's food e-commerce growth of 12% year-over-year in 2023, accounting for 30% of total e-commerce sales, demonstrates the channel's expansion potential in developed markets with robust digital infrastructure, according to USDA data from 2023.

The digital channel's growth benefits smaller brands that lack extensive physical retail footprints but excel in direct-to-consumer engagement and targeted marketing strategies. Convenience and grocery stores capture a moderate market share through location advantages and impulse purchasing opportunities that favor grab-and-go consumption occasions. Traditional retail channels face margin pressure from online competitors while adapting to changing consumer shopping patterns that prioritize convenience and product variety over physical store experiences.

Geography Analysis

APAC Dried Soup Market

Asia-Pacific's 33.20% market share in 2025, combined with 2.82% CAGR growth through 2031, positions the region as the primary driver of dried soup market expansion, fueled by rapid urbanization and evolving dietary preferences that favor convenience without abandoning traditional flavor profiles. The region's demographic transition toward dual-income households and extended commuting times creates sustained demand for quick meal solutions that maintain nutritional value and cultural authenticity. According to data from the Ministry of Internal Affairs and Communications for 2024, there were 13 million dual-income households in Japan . Rising health consciousness across the region increasingly favors products with clean labels and functional ingredients that align with traditional wellness philosophies while providing modern convenience benefits.

North America and Europe Dried Soup Market

North American and European markets demonstrate mature consumption patterns with moderate growth rates that reflect established market penetration and increasing competition from fresh alternatives and insurgent brands challenging traditional players. European markets lead sustainability initiatives through regulatory frameworks that drive packaging innovation and ingredient sourcing transparency, creating competitive advantages for brands that successfully integrate environmental responsibility into value propositions. The region's focus on premium positioning and artisanal quality enables margin expansion despite volume pressures from health-conscious consumers migrating toward fresh preparation methods.

South America and MEA Dried Soup Market

Emerging markets in South America, the Middle East, and Africa present significant growth opportunities driven by urbanization, rising disposable income, and infrastructure development that support modern retail distribution channels. These regions benefit from lower market penetration rates that create expansion potential for both international brands and local manufacturers who understand cultural preferences and price sensitivity requirements. Economic development patterns in these markets favor convenience products as lifestyle changes reduce available cooking time while increasing exposure to global food trends through digital media and international travel. Supply chain development and local manufacturing capabilities become critical success factors for capturing growth in emerging markets, where import costs and currency volatility can significantly impact product accessibility and pricing competitiveness.

Regulatory Landscape

Global dried soup manufacturers operate under a layered framework that combines national food-safety rules with widely referenced international standards for additives, contaminants, and labeling. In November 2025, the FAO/WHO Codex Alimentarius Commission (CAC48) updated the General Standard for Contaminants and Toxins in Food and Feed (CXS 193-1995) by adopting new maximum levels for lead in dried culinary herbs (2.0 mg/kg), a relevant input category for herb and seasoning-heavy soup mixes that trade across borders.

In the European Union, Regulation (EU) No 1169/2011 continues to shape labeling and ingredient transparency, including requirements related to primary-ingredient origin when it differs from the stated origin of the food. Additive compliance is also an active watch area for dry soup formulations that use hydrocolloids and stabilizers: Regulation (EU) 2026/196, adopted on 28 January 2026, amended usage specifications for common thickeners such as locust bean gum (E 410), guar gum (E 412), and xanthan gum (E 415), prompting specification and supplier-documentation updates for products sold in the EU. Alongside regulatory requirements, audit expectations are evolving as well, with FSSC 22000 releasing Version 7 in May 2026, supporting stricter, GFSI-benchmarked food-safety management expectations across global supply chains.

Value Chain Analysis

The dried soup value chain starts with agricultural inputs (vegetables, herbs, spices, pulses, and animal-derived ingredients for non-vegetarian variants), followed by preprocessing, dehydration or freeze-drying, milling/blending, and co-packing into pouches, sachets, cups, or multi-serve formats. The dehydration node is a high-energy conversion step where throughput, fuel reliability, and dryer or condenser constraints can become structural bottlenecks, tightening availability of core ingredients such as dehydrated vegetables and herb blends and amplifying conversion-cost volatility.

Quality and compliance risks concentrate at farm sourcing and dehydration/milling, because issues such as microbial load, color, and key sensory attributes often cannot be corrected after drying. Downstream, brands and manufacturers rely on a mix of direct retail supply, distributors, and e-commerce; partnerships are also used to bridge capability gaps and accelerate scale. For example, in March 2025, Purition began manufacturing instant soups for Soul Kitchen to help scale production and support expansion into retail and foodservice, while Nature Foods Company Limited (NFC) moved I.SOUP into export-led distribution through exclusive agreements in July 2025 for Australia (Sunny Trading) and Japan (THAK), underscoring how distributor relationships can unlock new markets for shelf-stable soup mixes.

Competitive Landscape

The dried soup market demonstrates moderate consolidation, with major companies including Campbell's, Unilever, and Nestlé commanding substantial market share through their established brands, extensive distribution networks, and product innovation capabilities. However, recent consumer behavior shifts reveal a growing preference for smaller, authentic brands that challenge traditional market leaders through direct-to-consumer strategies and premium positioning that resonates with health-conscious demographics.

The competitive landscape increasingly favors companies that integrate sustainability initiatives, digital marketing capabilities, and product innovation to differentiate offerings in an increasingly commoditized category. Strategic patterns across the industry focus on premiumization, sustainability integration, and digital transformation as manufacturers respond to changing consumer expectations and margin pressures from commodity inflation.

Merger and acquisition activity remains elevated as companies seek to acquire capabilities in plant-based formulations, sustainable packaging, and direct-to-consumer distribution channels that enhance competitive positioning. White-space opportunities emerge in functional food segments, ethnic flavor profiles, and premium organic formulations, where consumer willingness to pay higher prices creates margin expansion potential for innovative brands that execute differentiation strategies.

Dried Soup Industry Leaders

-

Campbell Soup Company

-

Nestlé S.A.

-

Unilever Plc

-

Ajinomoto Co. Ltd.

-

The Kraft Heinz Company

- *Disclaimer: Major Players sorted in no particular order

Dried Soup Market Companies Covered in this Report

- The Campbell Soup Company

- Unilever PLC

- Nestlé S.A.

- The Kraft Heinz Company

- Premier Foods Group Ltd

- Ottogi Co., Ltd.

- General Mills Inc.

- Conagra Brands Inc.

- Baxters Food Group Ltd

- Ajinomoto Co., Inc.

- Hain Celestial Group

- B&G Foods Holding Corp.

- Nissin Foods Holdings Co.

- Tata Consumer Products Limited

- Pacific Foods of Oregon

- Maruchan Inc.

- Bonduelle S.A.

- Ainsley Harriott Food Company Limited

- Funk Foods Private Limited (Simplify Foods)

- Kettle & Fire Inc.

Market Opportunities and Future Outlook

Product whitespace is forming around premium, clean-label instant soups that use freeze-drying or other advanced drying approaches to improve rehydration, ingredient integrity, and perceived freshness, aligning with consumer scrutiny of nutrition and ingredient transparency in a mature category. This shift has tangible supply-side reinforcement: Van Drunen Farms completed a USD 50 million expansion of its Illinois freeze-drying facility in January 2025, doubling capacity for organic fruit and vegetable processing, which can improve access to higher-quality dried inclusions used in vegetable-forward and vegetarian soup mixes.

Geographic opportunity is tied to Asia-Pacific scale and ingredient ecosystems, where instant formats and local flavor alignment support volume growth, and where large ingredient platforms are adding capacity. In January 2026, Aviko commenced expansion works at its potato dehydration site in Gansu province, China, increasing the production footprint for dried potato ingredients serving Asian markets, which are relevant for potato-based soup mixes and thickening systems. Another opportunity track links sustainability to input sourcing through surplus valorization models: the Sopa Project at Mercado Mayorista Lo Valledor processes about 1.5 to 2 tons of surplus vegetables per month into dehydrated soup products, highlighting a replicable pathway for brands and manufacturers to build sustainability claims while securing alternative vegetable inputs.

Recent Industry Developments in Dried Soup Market

- June 2026: The Campbell's Company launched a gluten-free condensed chicken noodle soup in collaboration with Banza, using chickpea pasta. The partnership targets shoppers seeking familiar comfort flavors with allergen- and diet-aligned formulations, raising competitive pressure on incumbents to reformulate mainstream lines for specific dietary needs.

- April 2026: Sumitomo Corporation of Americas announced a national retail partnership to debut premium freeze-dried instant soups at Target stores nationwide starting May 2026. The move expands mass-market access for freeze-dried formats and tightens competition for shelf space with traditional dehydrated soup mixes.

- March 2025: Purition entered a strategic partnership with Soul Kitchen under which Purition assumed manufacturing for Soul Kitchen's instant soups. By pairing manufacturing scale with a premium brand proposition, the collaboration strengthens supply reliability and enables wider expansion across retail and foodservice channels.

Dried Soup Market Report Scope and Research Methodology

Market Definition and Coverage

For this methodology, the dried soup market includes finished, shelf-stable soup products sold in dry form that are meant to be reconstituted with water before consumption, and are counted at the manufacturer level in value terms.

Scope exclusions: We exclude canned, chilled, and frozen soups, and we also exclude broader meal kits or noodle bowl categories that are not sold as dried soup mixes.

Segments Covered in This Report

-

By Product Type

- Instant Dried Soup

- Dehydrated Dried Soup

-

By Category

- Vegetarian Soup

- Non-Vegetarian Soup

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience/Grocery Stores

- Online Retail Stores

- Other Distribution Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set clear market boundaries and to build practical inputs that can be defended during validation. We reviewed public sources such as USDA and ERS food category statistics, US Census and Bureau of Labor Statistics price series, UN Comtrade trade flows for dried prepared foods, and FAO food supply indicators to understand demand direction and price movement.

Alongside this, we referenced company annual reports, investor presentations, and press releases to understand product positioning and distribution shifts. Where needed, paid subscriptions were used only for company financials and news screening, patent searches for dehydration and packaging improvements, and selective shipment level import and export views to sanity-check trade-heavy regions. These examples are not exhaustive, and many other public sources were also reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and surveys were completed with a mix of packaged food manufacturers, ingredient and dehydration solution suppliers, distributors, and retail or foodservice aligned stakeholders. The discussions were spread across major consumption regions so that pricing logic, channel mix, and product form assumptions could be adjusted when local realities differed. We also used these inputs to fill gaps on private company activity, promotional intensity, and typical pack size patterns that are rarely consistent in public reporting.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 12% | APAC: 39% |

| Mid tier: 45% | Functional/Unit leaders: 29% | EMEA: 35% |

| Smaller Players: 21% | Managers: 59% | Americas: 26% |

Market-Sizing & Forecasting

Sizing started with a top-down reconstruction where packaged soup demand signals were translated into dried soup value using region-level consumption direction, shelf-stable mix penetration, and manufacturer level price points. To keep the model grounded, the totals were then checked with selective bottom-up approximations, such as sampling brand and private label pack prices, mapping them to typical volumes, and testing the implied revenues against supplier and channel feedback.

A few inputs that mattered most in the model were average selling price progression by pack format, the share shift between pouches and cups, household convenience trends that change purchase frequency, retail versus foodservice mix, and region-specific inflation effects on packaged foods. When bottom-up visibility was weak for smaller markets, we used proxy indicators like trade intensity, modern retail presence, and expert-validated penetration ranges, and then narrowed them during review.

For forecasting, scenario analysis was used with a base case guided by expert consensus, and it was supported by time series smoothing on prices to avoid overreacting to one-off spikes. The final path was set only after the assumptions created a coherent story across volume, pricing, and channel evolution.

Data Validation & Update Cycle

Validation is done in layers so that a single data point does not steer the output too strongly. We compare the model to independent signals such as trade movement, packaged food pricing direction, and visible portfolio changes, and then investigate any region that looks out of line with the known demand picture.

Before sign-off, the work goes through internal analyst reviews that check arithmetic, definitions, and year-to-year continuity, followed by re-contact triggers when a key assumption seems to be drifting from market reality. Reports are refreshed annually, and material events can lead to interim adjustments. Right before delivery, a final pass is done so clients receive the most current view available.

Mordor Intelligence's Dried Soup Market Estimate Compared With Other Published Estimates

Published dried soup numbers often differ because firms do not always count the same product set, sales level, or pricing basis, and they also choose different current years for their headline value. Differences can also come from how strongly a model leans on broad packaged food totals versus category-specific checks.

In this study, the biggest gap drivers were whether instant cup formats are grouped with wider noodle meal bowls, whether values are captured at manufacturer ex-factory or at retail selling price, and whether currency and inflation are handled in constant dollars or nominal dollars. A tighter link between pack-format mix, region demand signals, and validated ASP movement reduces the risk of overstating value in regions where pricing is volatile.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.81 B (2026) | |

| Industry Data Publisher A | USD 9.49 B (2024) | Uses an earlier base year and appears to report a broader dried soups bucket that leans on revenue reporting by pack types and channels, which can also reflect later-stage pricing in some markets. |

| Global Consultancy B | USD 2.70 B (2026) | Uses a narrower definition focused on commercially traded dried soup products with a long-horizon growth build, which can undercount mainstream retail dried soup mixes and treat adjacent shelf-stable meal formats differently. |

The spread across these figures mostly reflects scope and price-point choices rather than simple math differences. When cup and pouch mixes are counted only as finished dried soup that is sold at the manufacturer level and held in constant-dollar terms, the estimate stays closer to repeatable demand and price variables, which is the approach applied by Mordor Intelligence.

Key Questions Answered in the Report

What is the current size of the dried soup market?

The market stands at USD 6.81 billion in 2026 and is projected to reach USD 7.33 billion by 2031, growing at a 1.49% CAGR over 2026-2031.

Which product segment leads the dried soup market?

Instant variants hold the top position with 54.10% in 2025 revenue and will continue expanding at a 1.78% CAGR through 2031.

Why are vegetarian soups outperforming other categories?

Vegetarian lines benefit from plant-based dietary adoption, sustainability concerns, and cost stability, resulting in a 1.96% CAGR and more than half of category sales.

How significant is e-commerce for dried soup sales?

Online retail is the fastest-growing channel, advancing at 2.55% CAGR as consumers embrace convenience, subscription models, and wider assortment.

Page last updated on: