Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

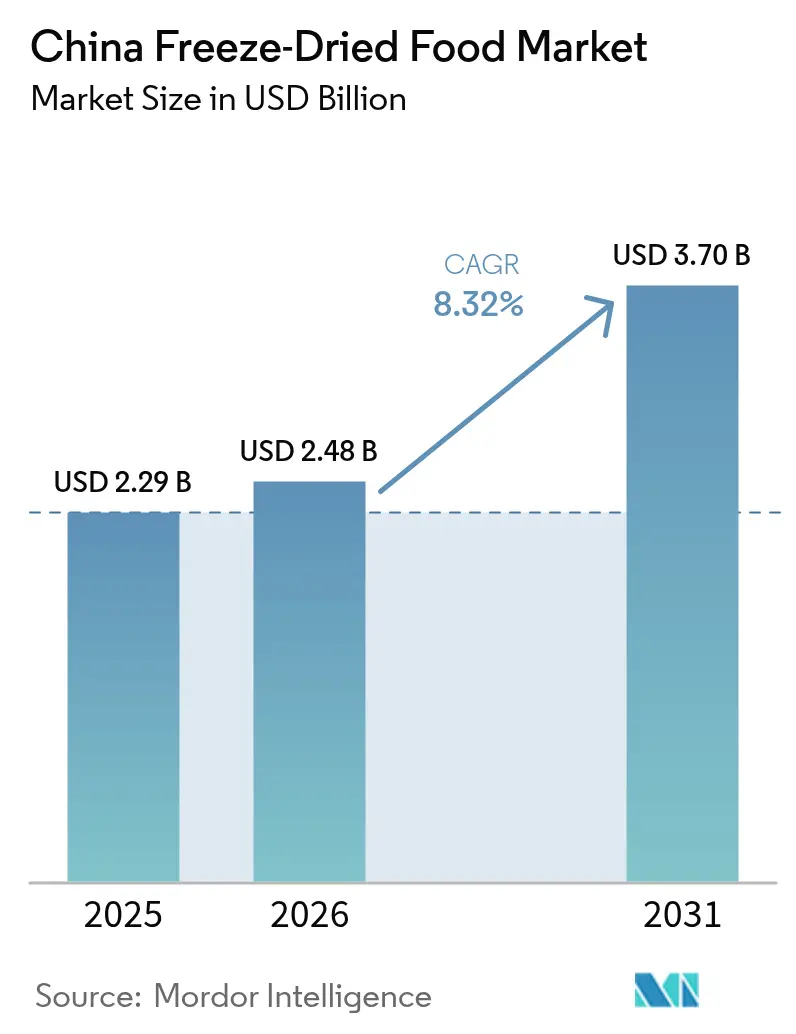

| Base Year Market Size (2025) | USD 2.29 Billion |

| Market Size (2026) | USD 2.48 Billion |

| Market Size (2031) | USD 3.7 Billion |

| Growth Rate (2026 - 2031) | 8.32% CAGR |

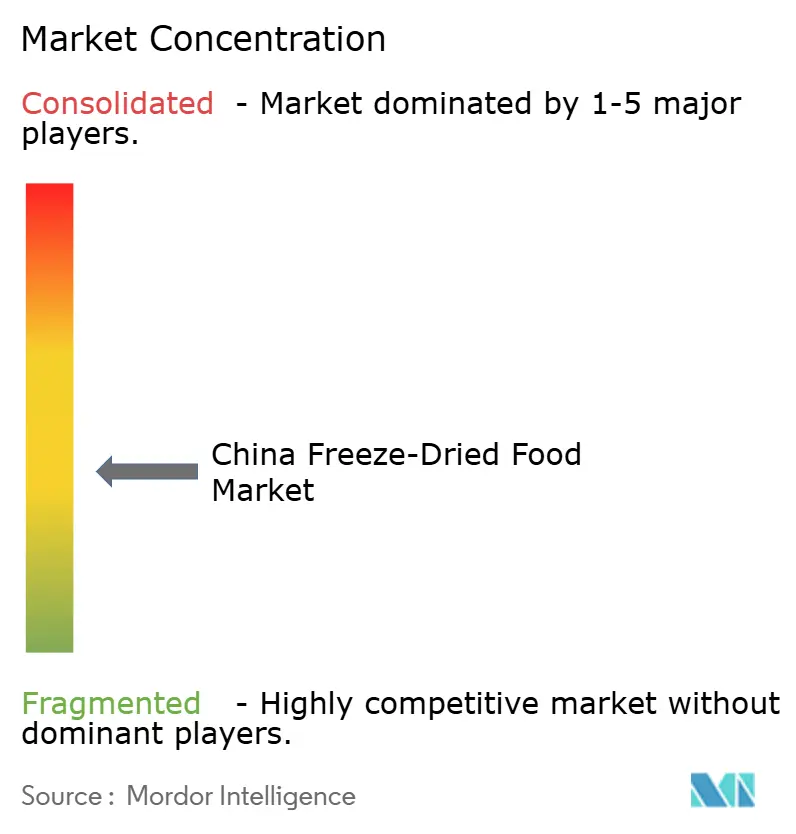

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Freeze-Dried Food Market Analysis by Mordor Intelligence

The China freeze-dried food market size was valued at USD 2.29 billion in 2025 and estimated to grow from USD 2.48 billion in 2026 to reach USD 3.7 billion by 2031, at a CAGR of 8.32% during the forecast period (2026-2031). Capacity additions in Gansu, Henan, and Shaanxi are closing cost gaps with coastal exporters, while the State Council’s draft “Freeze-dried Food General Rules” promises unified standards that should lower compliance overheads for small and mid-sized plants. Supermarkets, hypermarkets, and convenience stores still account for the majority of offline sales; however, live-streaming sessions on Douyin and Xiaohongshu are transforming single-ingredient snack packs into impulse buys and drawing tier-2 consumers into premium price tiers. Equipment makers are benefiting from 30% R&D subsidies under the 14th Five-Year Plan, driving innovations such as alternating cold-trap systems that reduce energy use by 40% per kilogram and cut payback periods. Against this favorable backdrop, headline risks remain: capital-intensive vacuum chambers, volatile power tariffs, fragmented raw-material supply, and a lingering “space food” stigma in lower-income cities.

Key Report Takeaways

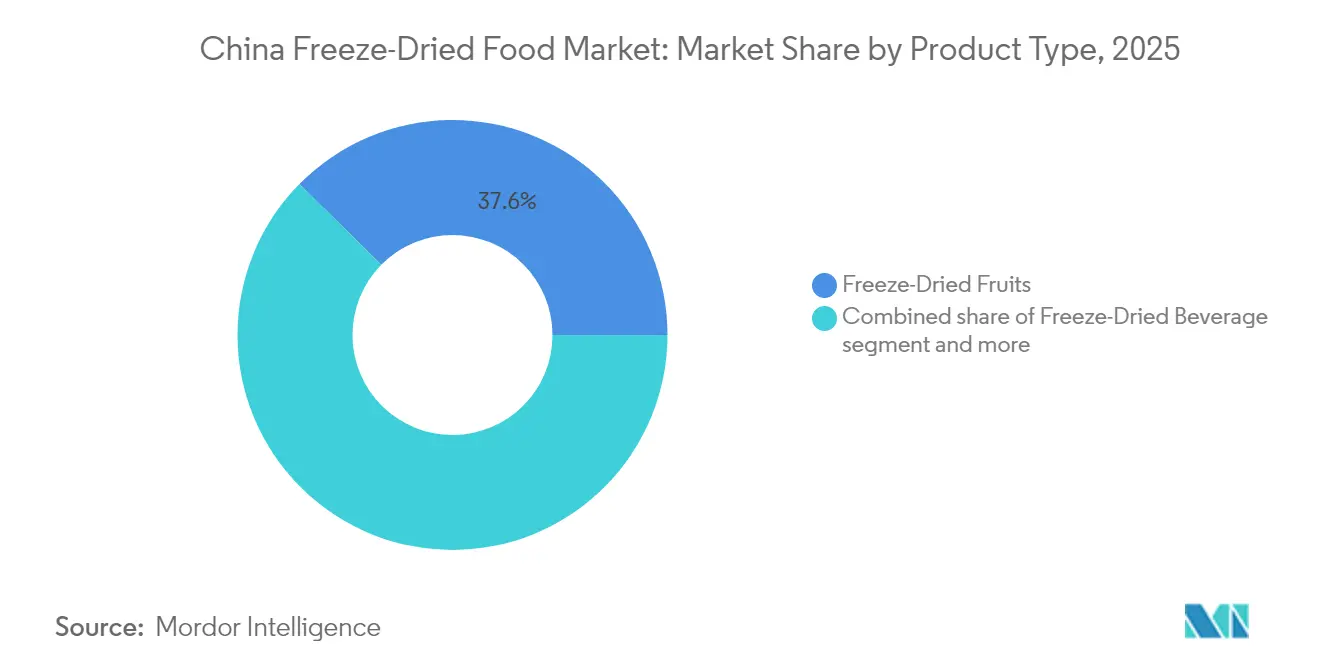

- By product type, freeze-dried fruits captured 37.62% of China's freeze-dried food market share in 2025, while beverages are projected to post the fastest 10.05% CAGR through 2031.

- By nature, conventional lines held an 83.05% share of the China freeze-dried food market size in 2025, but the organic tier is advancing at an 11.32% CAGR, driven by clean-label premiums.

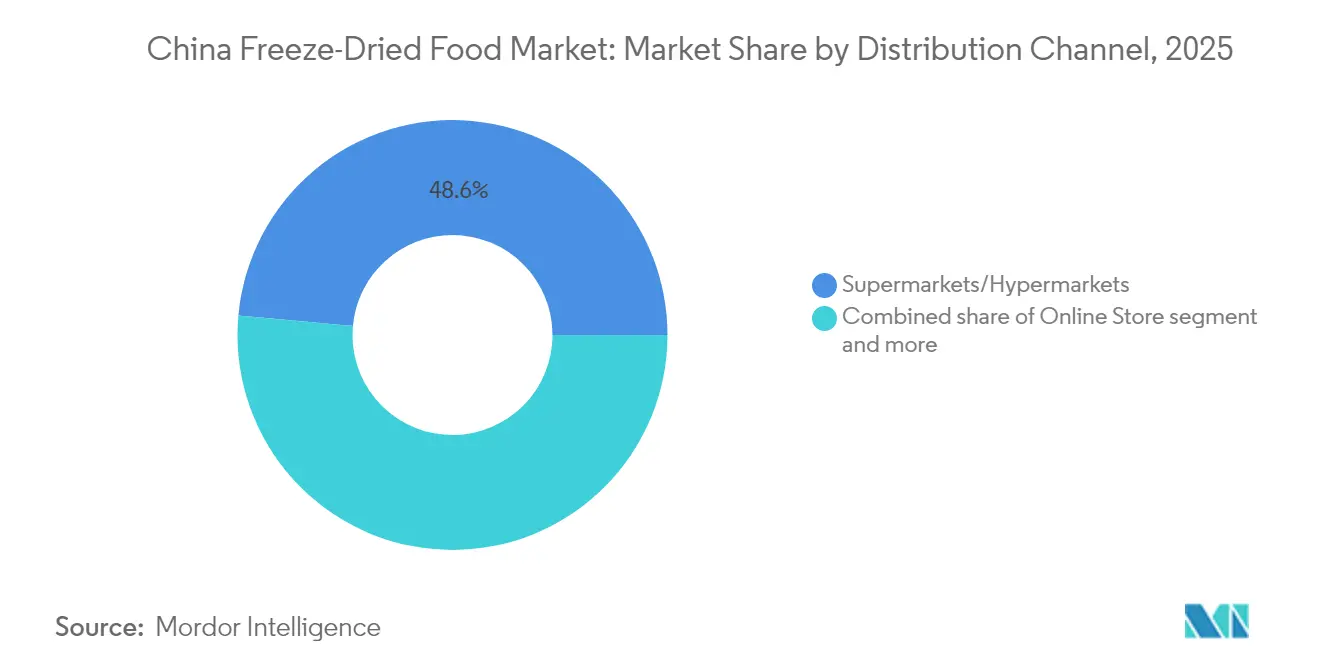

- By distribution channel, supermarkets and hypermarkets accounted for 48.55% of sales in 2025, whereas online stores are projected to grow at a 10.89% CAGR to 2031, as live-streaming expands its reach beyond tier-1 cities.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Freeze-Dried Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for natural, clean-label snacks | +2.1% | National, with premium demand concentrated in Beijing, Shanghai, Guangzhou, Shenzhen | Medium term (2-4 years) |

| Rapid penetration of freeze-drying capacity in inland provinces | +1.8% | Gansu, Shaanxi, Henan, Sichuan, Heilongjiang | Short term (≤ 2 years) |

| Government incentives for agri-processing in rural revitalization zones | +1.5% | National, with early gains in Tianshui (Gansu), Shangqiu (Henan), Guyuan (Ningxia) | Long term (≥ 4 years) |

| Social media influence boosting market growth | +1.3% | National, strongest in tier-1 and tier-2 cities with high Douyin/Xiaohongshu penetration | Short term (≤ 2 years) |

| Rise in infant and toddler freeze-dried snacks | +0.9% | National, with early adoption in coastal urban centers | Medium term (2-4 years) |

| Culinary and foodservice innovation | +0.7% | National, with pilot adoption in premium hotel chains and QSR formats | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Natural, Clean-Label Snacks

Urban Chinese consumers are increasingly scrutinizing ingredient lists, with 57% reviewing nutrition labels before purchase (USDA, 2024). This trend is driving demand for freeze-dried products that list single ingredients, such as “100% strawberry” or “pure mango,” which are free from preservatives, colorants, and added sugars. The organic segment is growing, as consumers are willing to pay 30–50% premiums for certified products, despite labeling distrust and limited availability outside tier-1 cities. Chocolate manufacturers are incorporating freeze-dried fruits into “Chocolate+” formulations to reduce cocoa costs while enhancing visual appeal and taste, reflecting cross-category demand beyond standalone snacks. Compliance with GB 10770-2025, effective March 2026, which enforces stricter limits on additives and contaminants in infant complementary foods, is further accelerating reformulation toward the inclusion of freeze-dried fruit and vegetables that meet clean-label standards without compromising shelf life (USDA)[1]Source: United States Department of Agriculture Foreign Agricultural Service, “China: Food Processing Ingredients Annual,” fas.usda.gov.

Rapid Penetration of Freeze-Drying Capacity in Inland Provinces

Provincial governments in Gansu, Shaanxi, Henan, and Heilongjiang offered targeted subsidies and tax incentives in 2024-2025 to attract freeze-drying equipment manufacturers and processors, leveraging lower land and labor costs compared with coastal regions. Tianshui City (Gansu) allocated RMB 25.7 million (approximately USD 3.5 million) in subsidies, stimulating RMB 65 million (approximately USD 9 million) in private investment and supporting the development of 3,468 cold-chain facilities with a capacity of 1.14 million tons since 2020 (USDA). In April 2025, Jiangsu BoLaiKe supplied industrial freeze-dryers to a Shaanxi pet food enterprise, highlighting its focus on serving inland processors in both domestic and export markets. Guyuan (Ningxia) cultivates over 500,000 mu of cold-climate vegetables, producing 2 million tonnes annually, with 18 geographic-indication products exported to Malaysia and Saudi Arabia. Proximity to raw materials reduces logistics costs by 12-18% for co-located freeze-dried producers. Regional specialization, with Heilongjiang focusing on vegetables and Henan on fruits, enhances supply-chain efficiency and product consistency (USDA).

Government Incentives for Agri-Processing in Rural Revitalization Zones

China’s 2024–2027 rural revitalization plan promotes value-added agri-processing, with 31 provinces issuing supportive measures (USDA). The 14th Five-Year Plan prioritizes freeze-drying equipment, offering R&D subsidies of over 30% for energy-efficient technologies. Zhejiang Tongking’s alternating cold-trap system reduces energy consumption by 24% per trap and 40% per kilogram, resulting in an annual savings of approximately RMB 110,000 (USD 15,200) at 5,000 hours, benefiting processors with thin margins. The draft "Freeze-dried Food General Rules" (Nov 2024) will harmonize standards and labeling nationwide, lowering compliance costs and enabling smaller processors to reach national distribution[2]Source: China–Africa SPS Cooperation Information Platform, “Draft Freeze-dried Food General Rules,” chinaafricasps.org. The clarity is expected to attract foreign investment and joint ventures for localized supply chains in prepared meals and infant nutrition.

Social Media Influence Boosting Market Growth

Live-streaming generated USD 514 billion in gross merchandise value in 2024, and freeze-dried snacks benefit from demonstrations that dramatize rehydration and texture in seconds, as per the USDA Foreign Agricultural Service. JD.com and Tmall now run self-operated cold-chain warehouses that place inventory within 48 hours of tier-2 and tier-3 addresses, allowing hosts to promise next-day delivery. Conversion rates run 20-30% higher in tier-1 cities, but influencer-led education is narrowing the gap in lower-income zones. Convenience chains such as Sinopec Easy Joy Coffee amplify visibility by stocking single-serve sachets at petrol stations, merging digital impulse with offline availability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Geographic Relevance |

|---|---|---|---|

| High capex and energy costs of vacuum freeze-dryers | -1.4% | National, with acute impact on tier-2 and tier-3 processors lacking subsidy access | Short term (≤ 2 years) |

| Fragmented raw-material supply chain quality issues | -1.1% | National, particularly inland provinces with nascent cold-chain infrastructure | Medium term (2-4 years) |

| Consumer perception as "Artificial" or "Space Food" | -0.8% | Tier-3 and tier-4 cities with lower exposure to premium food trends | Long term (≥ 4 years) |

| Competition from alternatives | -0.6% | National, with strongest pressure in prepared-meal and snack categories | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capex and Energy Costs of Vacuum Freeze-Dryers

Industrial vacuum freeze-dryers range from USD 10,000 for entry-level units to USD 350,000 for large-scale automated systems, creating a capital barrier for smaller processors without subsidized financing (USDA). Energy use during sublimation, typically 40-70°C at 5-50 Pa for 10-15 hours per batch, can account for 30-40% of operating costs, especially in provinces lacking preferential electricity rates. Zhejiang Tongking’s alternating cold-trap system cuts energy consumption by 40% per kilogram, but adoption is largely limited to processors with technical expertise and capital to retrofit existing lines. Subsidies exceeding 30% under the 14th Five-Year Plan benefit processors in Gansu and Shaanxi, while those in provinces without incentives face payback periods of 4-6 years, discouraging investment and reinforcing regional capacity disparities.

Fragmented Raw-Material Supply Chain Quality Issues

China’s agricultural sector remains fragmented, with smallholder farms supplying inconsistent grades of fruits, vegetables, and meats, complicating batch-to-batch quality control for freeze-dried processors. By Q3 2024, cold-storage capacity reached 66.945 million tonnes, but inland provinces lack sufficient refrigerated logistics to preserve peak freshness (USDA). Food safety enforcement is intensifying: in Q1 2024, the Supreme People’s Procuratorate filed 5,126 public-interest lawsuits, 4,235 of which involved agricultural products, highlighting the pressures of traceability and testing on processors sourcing from multiple suppliers (Mérieux NutriSciences)[3]Source: Mérieux NutriSciences China, “Market News April 2024,” merieuxnutrisciences.com.cn. A national eight-month crackdown launched in March 2024 targeted illegal practices in livestock and poultry, prompting stricter supplier audits and third-party testing for freeze-dried meat and seafood producers. Consumer distrust in organic certification, stemming from past labeling scandals, limits the willingness to pay premiums above 50%, thereby constraining the revenue potential for certified supply chains. The draft "Freeze-dried Food General Rules" (November 2024) will mandate enhanced origin documentation and microbial testing, accelerating upstream consolidation while raising near-term compliance costs (China–Africa SPS Cooperation Information Platform).

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fruits Dominate, Beverages Accelerate

Freeze-dried fruits dominated the largest slice of the China freeze-dried food market in 2025, accounting for 37.62%, thanks to eye-catching strawberry and mango slices that shine in livestream demos. Instant coffee and tea lines, while starting from a smaller base, are on track for a 10.05% CAGR through 2031, helped by office culture and capsule systems in convenience stores. The China freeze-dried food market size for beverages could therefore double by mid-decade, attracting both global brands and local startups. Vegetables, meat, dairy, and prepared meals round out the basket, supplying foodservice and pet-food channels that prize ease of storage. Product innovation now ranges from freeze-dried wontons for quick-service restaurants to heat-stable chocolate for warm-chain distribution, hinting at broader culinary applications ahead.

A second growth layer stems from inland specialization: Henan and Gansu concentrate on strawberry and apple feeds, while Heilongjiang focuses on carrots and mushrooms, shortening farm-to-factory legs by up to 18%. This clustering supports quality consistency that livestream hosts can showcase with close-up texture shots, further widening consumer acceptance. Meanwhile, pet-food demand is at the premium end, and processors are securing supply by co-investing in freeze-dryer fleets near livestock bases. Overall, diversified demand across snacks, beverages, pet, and prepared meals steadies utilization rates and limits over-reliance on any single product line.

By Nature: Conventional Still Leads, Organic Scales Up

Conventional SKUs captured 83.05% of sales in 2025 thanks to price points aligned with supermarket shoppers, and they remain the default in mass-market gift boxes sold during Lunar New Year. Yet the organic tier is growing at a 11.32% CAGR, faster than any other attribute, as label-conscious millennials pay a premium for pesticide-free claims. China freeze-dried food industry players are responding with QR-code farm videos, on-pack audit certificates, and live-stream tours that demystify supply chains. The China freeze-dried food market size for organic snacks remains small, but rising urban incomes suggest potential headroom as trust infrastructure strengthens.

A critical bottleneck is certification credibility: past scandals have dampened the willingness to pay premiums over 50%. Regulators are tightening audits, and public-interest lawsuits on food safety keep pressure high. Processors that invest early in traceable upstream partnerships are poised to win shelf space once GB 10770-2025 raises the bar on infant food additives. Over time, organic penetration is likely to exceed today’s 16% volume share, nudging conventional players toward incremental pesticide-residue tests to defend relevance.

By Distribution Channel: Online Races Ahead of Brick-and-Mortar

Supermarkets and hypermarkets still hold the largest share at 48.55%, supported by in-store sampling tables that allow shoppers to taste crispy fruit slices. Yet online stores are racing ahead at an 10.89% CAGR, powered by live-stream flash sales where hosts demonstrate instant rehydration. The Chinese freeze-dried food market benefits from JD.com and Tmall's cold-chain hubs, which guarantee 48-hour delivery to inland households, expanding beyond the coastal comfort zone. Convenience chains such as Sinopec Easy Joy Coffee offer on-the-go sachets, providing a physical touchpoint that reinforces digital exposure.

Hybrid retail models are emerging: Freshippo blends app ordering with 30-minute pickup, and stores stock up to 1,500 freeze-dried SKUs. Private-label brands exploit platform algorithms, bidding on “pure mango” keywords to surface during primetime streams. Meanwhile, specialty health-food shops cater to organic lines that require educated staff to explain traceability. Distribution diversity, therefore, spreads risk and ensures that supply shocks in any one channel do not derail overall growth.

Geography Analysis

China's freeze-dried food market activity is split between coastal export hubs and inland subsidy zones, creating a complementary two-track system that stabilizes national output. Inland provinces such as Gansu and Henan utilized subsidy packages worth tens of millions of renminbi to establish more than 3,000 cold-chain sites and attract processors closer to orchards and vegetable plots. These moves trimmed raw-material costs by 15-25% and reduced transit-damage claims, as fruits now reach chambers within hours of harvest. Guyuan in Ningxia exemplifies the model, nurturing 2 million tonnes of cold-climate vegetables annually and funneling them into nearby freeze-dryers that serve both domestic and Gulf markets.

Coastal provinces continue to dominate export volume; Shandong alone shipped 2,044 containers of freeze-dried fruit to North America in the 12 months ending May 2025, reflecting a logistics advantage in port proximity. Fujian and Zhejiang leverage deep-water harbors to ship fresh pineapple and mushroom chips onto reefer vessels bound for ASEAN and Japan. The coastal cluster also houses multinational R&D centers that pilot new textures before rolling them inland for cost-optimized scaling. Energy-saving retrofits, such as Zhejiang Tongking’s alternating cold-trap systems, often debut in Zhejiang plants before wider rollout, illustrating a technology cascade from coast to hinterland.

Tier-1 cities, Beijing, Shanghai, Guangzhou, Shenzhen, command premium demand; 68% of 18-35-year-olds there express willingness to trial freeze-dried snacks on health grounds. They also anchor live-stream ecosystems that broadcast nationwide, making them trend incubators. Tier-2 and tier-3 cities represent the fastest incremental gains as cross-border e-commerce cuts delivery times, while price-sensitive tier-4 towns still equate freeze-dry with astronaut rations. Over time, demographic shifts and improving logistics should narrow perception gaps, boosting per-capita uptake across inland counties.

Competitive Landscape

The Chinese freeze-dried food market is moderately concentrated, meaning the top five players hold sizeable yet non-dominant influence, leaving room for regional upstarts. Fujian Lixing runs more than 29 lines in an 80,000 m² plant and leads innovation with quick-rehydration wontons that target hotel buffets. Chaucer Foods’ Qingdao arm exported over 10 million kg to North America in the past year, underscoring China’s cost competitiveness in fruit inputs. Kerry Group, after acquiring Greatang, now cross-sells taste systems into its local freeze-dry portfolio, reinforcing flavor customization for infant and beverage clients.

Strategically, incumbents are pushing inland to secure subsidies and raw material clusters, while private-label brands are leveraging e-commerce algorithms to win millennial baskets. Energy efficiency is a differentiator; plants that retrofit alternating cold traps cut unit costs and can underprice rivals without sacrificing margin. Technology partnerships with equipment vendors accelerate adoption: Zhejiang Tongking’s 40% energy-saving modules are now integrated into lines at both Fujian Lixing and Anyang General Foods, demonstrating a rising standard for operational excellence.

Emerging disruptors include pet-food specialists leveraging single-ingredient positioning and livestream-native snack labels that sell directly through Douyin without traditional distributors. Patents like Qingdao Anxin Zhiguo’s heat-stable chocolate broaden possible categories and set higher bars for R&D agility. Overall, the race is tilting toward brands that combine cost-efficient inland production, flavor systems tailored to local palates, and digital-first storytelling that resonates with health-seeking shoppers.

China Freeze-Dried Food Industry Leaders

Tianjin Sai Yu Food Co., Ltd.

Anyang General Foods Co. Ltd

Fujian Lixing Foods Co. Ltd

Chaucer Foods Ltd (China ops.)

Kerry Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Jiangsu BoLaiKe dispatched industrial freeze-dryers to a Shaanxi pet food enterprise, marking capacity expansion in inland provinces targeting the high-margin pet food segment.

- June 2024: Qingdao Anxin Zhiguo filed a patent, CN118160802A, describing freeze-dried chocolate with embedded oil and water cores that maintain thermal stability up to 70°C, opening confectionery applications previously constrained by cold-chain requirements.

China Freeze-Dried Food Market Report Scope

Freeze drying is a method of preserving food, which involves freezing the food, removing almost all the moisture in a vacuum chamber, and finally sealing the food in an airtight container. Freeze-dried foods can be easily transported at normal temperatures, stored for a long period, and consumed with a minimum of preparation. China freeze-dried food market is segmented by product type and end user. Based on product type, the market is segmented into freeze-dried fruits, freeze-dried vegetables and herbs, freeze-dried tea and coffee, freeze-dried dairy products, freeze-dried meat and seafood, and other freeze-dried food. Also, the market is segmented based on the end-users into food service, processed food manufacturers, retail, and institutions. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

By Product Type

| Freeze-Dried Fruits | Strawberry |

| Raspberry | |

| Pineapple | |

| Apple | |

| Mango | |

| Other Fruits | |

| Freeze-Dried Vegetables | Pea |

| Corn | |

| Carrot | |

| Potato | |

| Mushroom | |

| Other Vegetables | |

| Freeze-Dried Meat and Seafood | |

| Freeze-Dried Dairy Products | |

| Freeze-Dried Beverages (Instant Coffee, Tea) | |

| Prepared Meals | |

| Pet Foods |

By Nature

| Conventional |

| Organic |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Stores |

| Other Distribution Channels |

| By Product Type | Freeze-Dried Fruits | Strawberry |

| Raspberry | ||

| Pineapple | ||

| Apple | ||

| Mango | ||

| Other Fruits | ||

| Freeze-Dried Vegetables | Pea | |

| Corn | ||

| Carrot | ||

| Potato | ||

| Mushroom | ||

| Other Vegetables | ||

| Freeze-Dried Meat and Seafood | ||

| Freeze-Dried Dairy Products | ||

| Freeze-Dried Beverages (Instant Coffee, Tea) | ||

| Prepared Meals | ||

| Pet Foods | ||

| By Nature | Conventional | |

| Organic | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Stores | ||

| Other Distribution Channels | ||

Key Questions Answered in the Report

How fast is demand growing for freeze-dried snacks in China?

Retail sales are projected to rise at an 8.32% CAGR through 2031, lifted by clean-label preferences and rapid online adoption.

Which product line is expanding quickest?

Freeze-dried beverages, mainly instant coffee and tea, are forecast to post a 10.05% CAGR between 2026 and 2031.

What share do conventional products hold today?

Conventional SKUs account for 83.05% of current sales, but organic lines are steadily gaining ground.

Why are inland provinces attracting new plants?

Subsidies, lower land costs, and proximity to farms cut raw-material expenses by up to 25% and shorten payback times on equipment.

Which sales channel is growing the fastest?

Online stores, buoyed by live-stream commerce and enhanced cold-chain logistics, are expanding at 10.89% CAGR to 2031.

Page last updated on: