AI In Healthcare Quality Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.45 Billion |

| Market Size (2031) | USD 0.97 Billion |

| Growth Rate (2026 - 2031) | 16.47% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Healthcare Quality Management Market Analysis by Mordor Intelligence

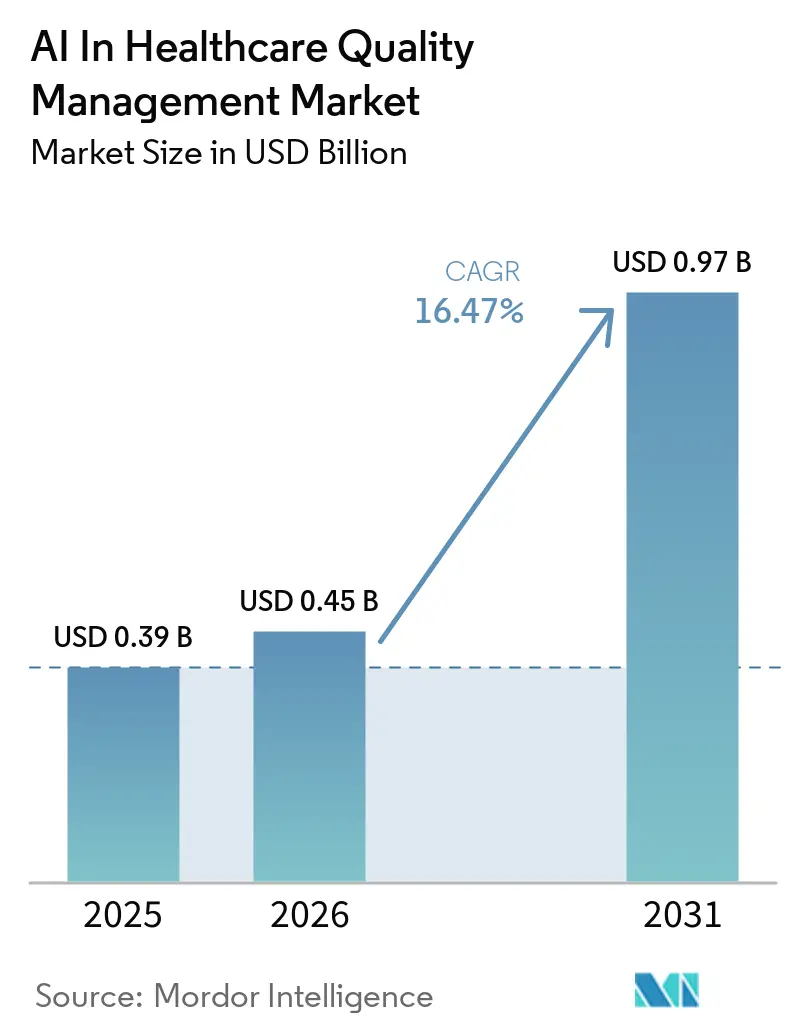

The AI In Healthcare Quality Management Market size is projected to be USD 0.39 billion in 2025, USD 0.45 billion in 2026, and reach USD 0.97 billion by 2031, growing at a CAGR of 16.47% from 2026 to 2031.

Growth in the AI in healthcare quality management market reflects a shift away from rule-based, document-heavy quality systems toward platforms that support automated abstraction, prediction, and root-cause review across regulated healthcare workflows. Federal payment and oversight programs are now pushing providers and life sciences teams to formalize AI quality tracking, especially through the WISeR model and the 2026 Quality Payment Program activity focused on patient safety in AI use. Data scale is also reshaping demand, as large clinical data estates and new multi-omic programs expand the volume and complexity of records that quality teams must review and validate. Published evidence from protocol extraction, trial redesign, and prescreening shows that AI tools are improving accuracy, speed, and workflow economics in ways that support broader enterprise deployment across sponsors and CROs. Vendors with stronger compliance architecture, validated data assets, and implementation capacity are therefore in a better position to capture enterprise demand in the AI in healthcare quality management market.

Key Report Takeaways

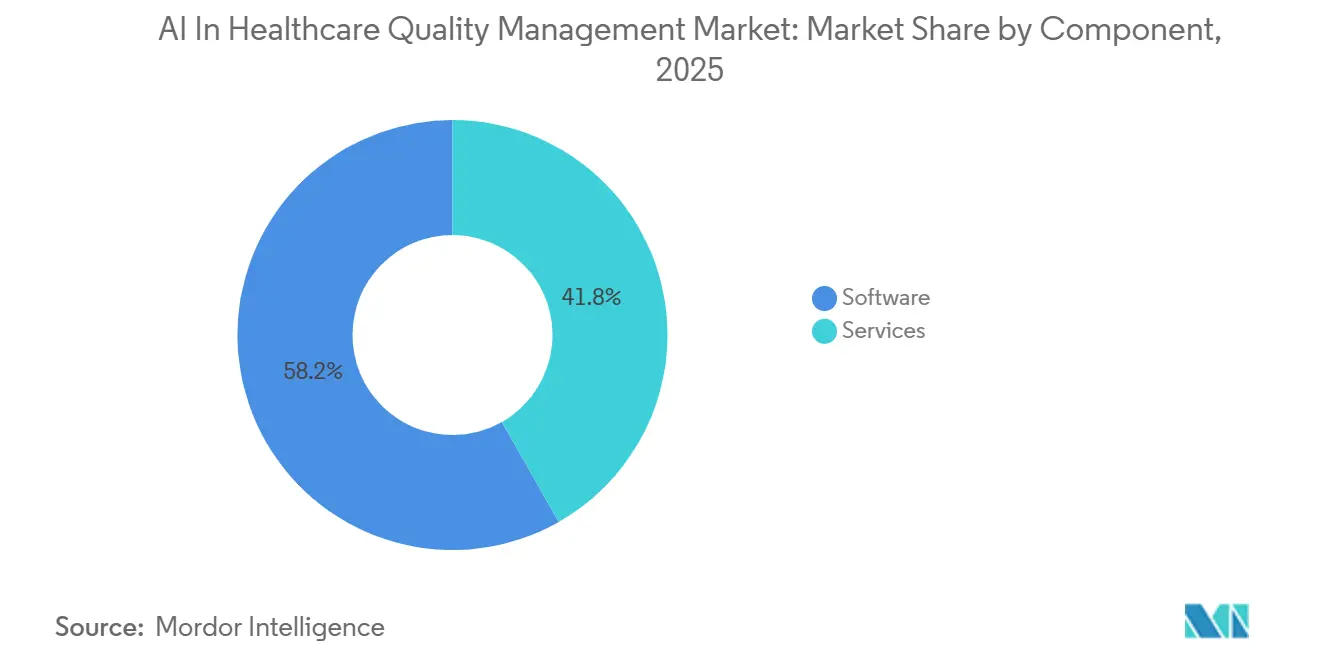

- By component, software held 58.23% of the AI in healthcare quality management market share in 2025, while services are forecast to expand at 17.23% through 2031.

- By application, patient outcome prediction captured 38.54% of the AI in healthcare quality management market size in 2025, while clinical trial optimization is forecast to advance at 16.94% through 2031.

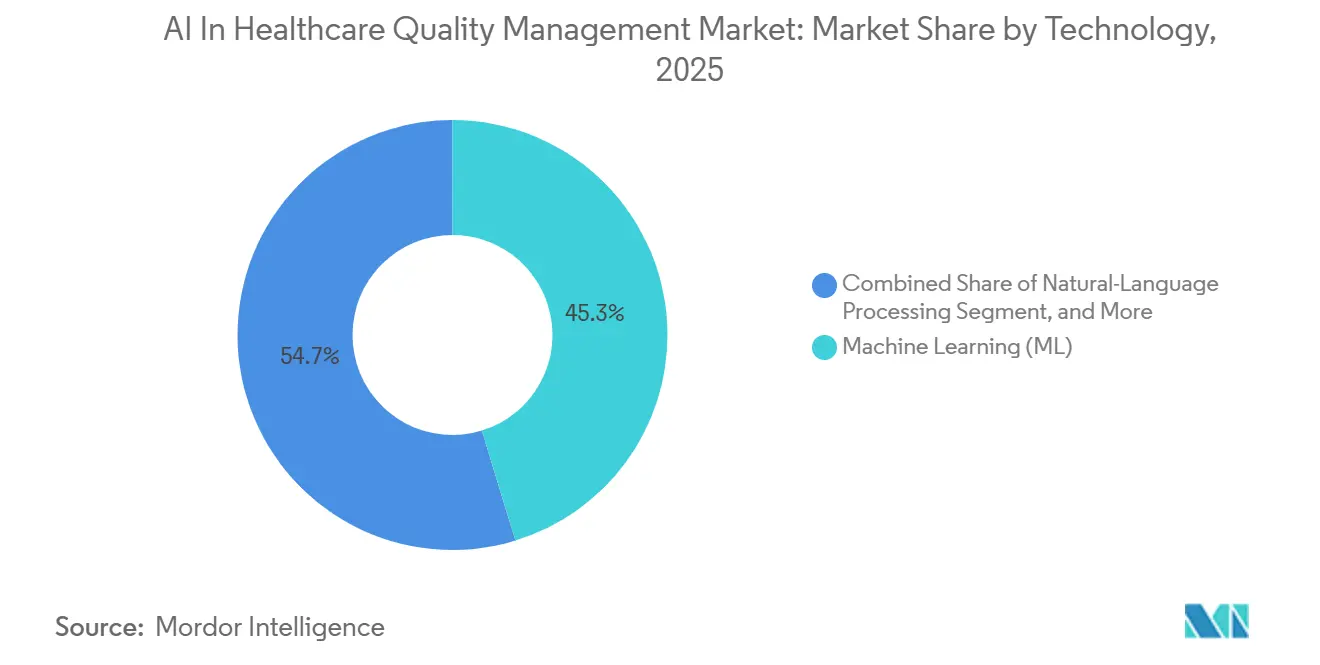

- By technology, machine learning (ML) represented 45.26% of the AI in healthcare quality management market in 2025, while natural language processing is projected to expand at 18.96% through 2031.

- By deployment, cloud deployment held 61.41% of the AI in healthcare quality management market in 2025, while on-premise deployment is expected to grow at 19.23% through 2031.

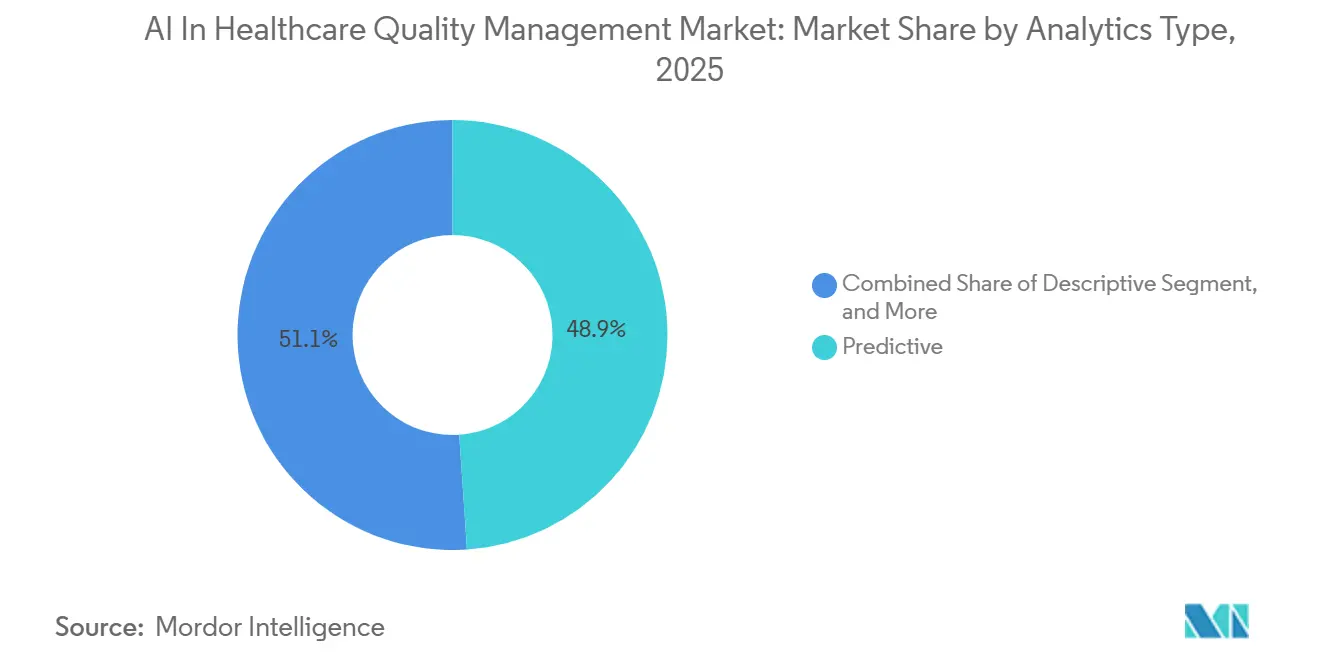

- By analytics type, predictive analytics led with 48.92% of the AI in healthcare quality management market in 2025, while descriptive analytics is forecast to grow at 20.76% through 2031.

- By data source, electronic health records accounted for 43.59% of the AI in healthcare quality management market in 2025, while genomics and multi-omics data are projected to expand at 17.39% through 2031.

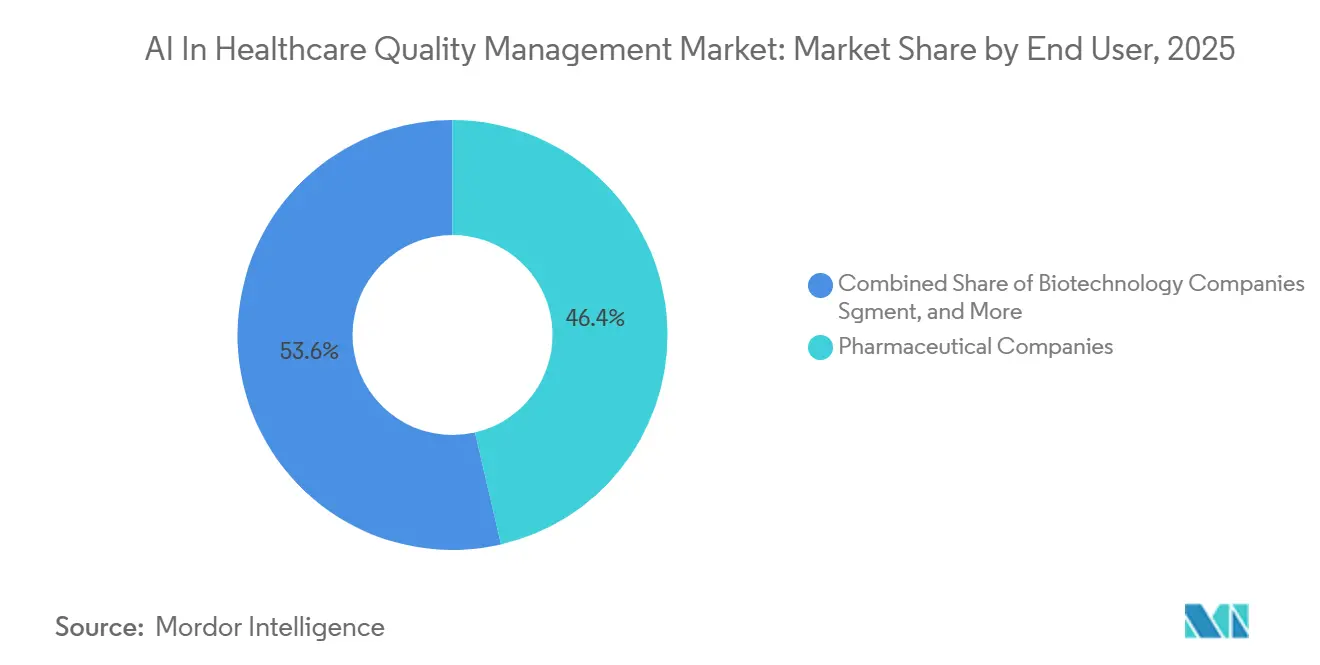

- By end user, pharmaceutical companies held 46.37% of the AI in healthcare quality management market in 2025, while contract research organizations are projected to grow at 20.48% through 2031.

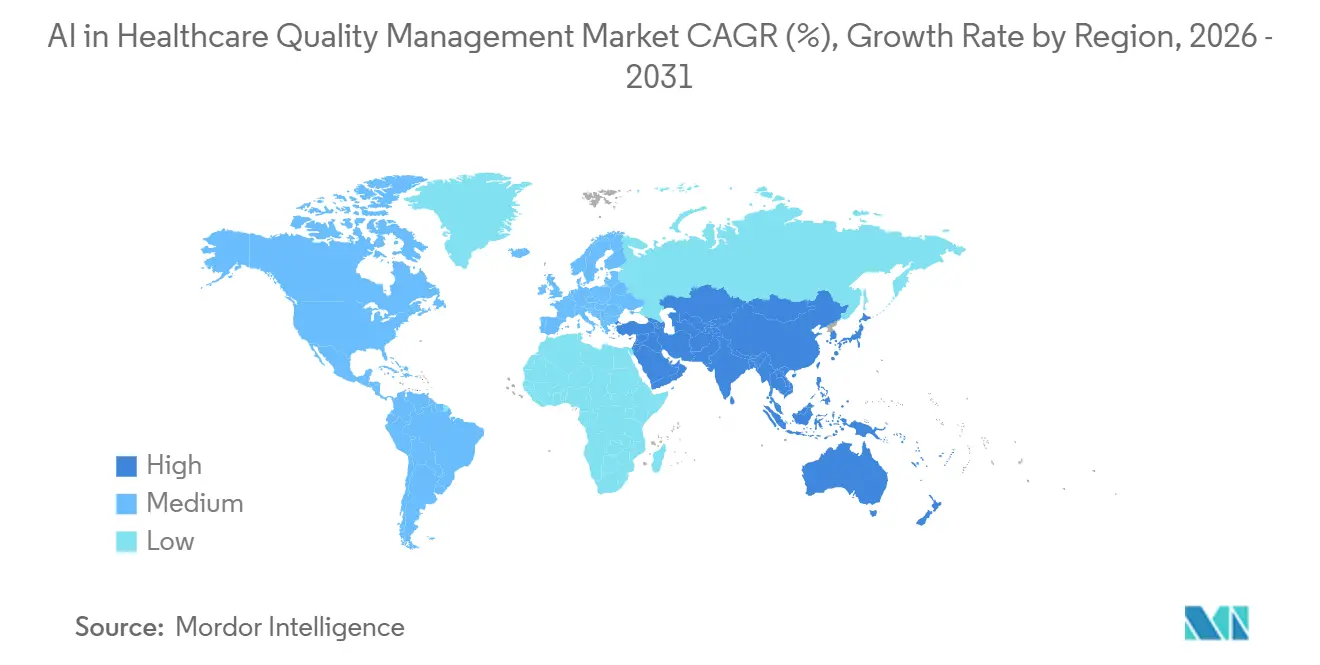

- By geography, North America led with 35.43% revenue share in 2025, and Asia-Pacific is forecast to register a 22.54% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Healthcare Quality Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Mandates and Quality Reporting Regulations | +3.2% | Global, with early gains in North America and the EU | Short term (≤ 2 years) |

| Growing Healthcare Data Volume and Complexity | +2.8% | Global | Medium term (2-4 years) |

| Advancement of AI-Based Predictive and Prescriptive Analytics | +3.5% | North America and the EU core, with spillover to APAC | Medium term (2-4 years) |

| Shift to Value-Based Reimbursement Incentives | +2.4% | North America, with emerging uptake in the EU | Short term (≤ 2 years) |

| Proliferation of Real-World Evidence from Connected Devices | +1.8% | Global, concentrated in North America and APAC | Long term (≥ 4 years) |

| Generative AI Automation of Quality Measure Abstraction | +2.1% | Global, with early gains in North America and Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Mandates & Quality-Reporting Regulations

Federal and cross-border policy actions are now one of the clearest structural drivers for AI in the healthcare quality management market.[1]Centers for Medicare & Medicaid Services, “Calendar Year 2026 Medicare Physician Fee Schedule Final Rule, Quality Payment Program Fact Sheet,” The WISeR model is active from 2026 through 2031 and uses AI and machine learning to process prior authorizations across 6 states, which creates a direct payment-linked use case for algorithmic review workflows.[2]Centers for Medicare & Medicaid Services and ONC, “Medicare Program, Hospital Inpatient Prospective Payment Systems,” CMS also finalized a new 2026 Quality Payment Program improvement activity on patient safety in the use of artificial intelligence, requiring eligible clinicians to document AI-attributable events and mitigation steps in routine care delivery. In parallel, the FDA and EMA issued joint principles in January 2026 that press drug developers toward lifecycle governance, performance monitoring, and human oversight for AI use in regulated development settings. These policy moves favor vendors and users that already have compliance infrastructure in place, and they raise entry barriers for smaller companies in the AI in healthcare quality management market.

Growing Healthcare Data Volume & Complexity

Healthcare data volume has reached a level where manual quality review is no longer workable for many regulated workflows in the AI in healthcare quality management market.[3]Emma Croxford et al., “Development and Validation of the Provider Documentation Summarization Quality Instrument for Large Language Models,” One in 5 patients now has a clinical chart exceeding 206,000 words, which sharply increases the abstraction burden for quality teams and clinical reviewers.[4]Ramtin Babaeipoura, François Charest, and Madison Wright, “AI-Assisted Protocol Information Extraction for Improved Accuracy and Efficiency in Clinical Trial Workflows,” The Mayo Clinic Platform Discover dataset currently includes more than 13.6 million patient records, 3.9 billion imaging records, and 1.25 billion clinical notes, which highlights the scale of data environments now shaping validation and monitoring needs.[5]Sixue Xing et al., “ClinicalReTrial, Clinical Trial Redesign with Self-Evolving Agents,” Complexity is also expanding beyond core EHR data, as Illumina’s Billion Cell Atlas program is set to generate 20 petabytes of single-cell transcriptomic data each year with founding participation from AstraZeneca, Merck, and Eli Lilly. Organizations that can score quality and trace issues across both clinical and omic datasets are likely to hold a stronger position in future drug development and quality operations.

Advancement of AI-Based Predictive & Prescriptive Analytics

Predictive and prescriptive tools are now showing measurable gains on quality-related tasks that matter to pharmaceutical companies and CROs in the AI in healthcare quality management market. A retrieval-augmented protocol extraction system developed by Banting Health AI reached 89% average extraction accuracy across several trial document fields, compared with 62.6% for standalone large language models without retrieval support. The same system reduced extraction time per protocol by 47 minutes, which supports a clearer operating case for automation in document-heavy quality workflows. In trial redesign, the ClinicalReTrial multi-agent system improved 83.3% of the protocols it assessed and lifted mean trial success probability by 5.7% at a cost of USD 0.12 per trial. JPMA also reported in December 2025 that AI can meaningfully support the identification of Critical-to-Quality factors in clinical trials without removing human decision authority, which helps strengthen trust in human-in-the-loop operating models.

Shift to Value-Based Reimbursement Incentives

Value-based reimbursement is turning quality data systems from a compliance cost into a revenue-linked capability for AI in the healthcare quality management market. The TEAM model became mandatory on January 1, 2026, for 5 surgical episode types and uses financial risk adjustment that rewards better prediction and outcome management at the provider level. The Ambulatory Specialty Model will begin in 2027 and applies payment adjustment bands from +9% to -9%, expanding to ±12% by 2031 for 85% of Part B payments tied to targeted specialists. Those payment swings are large enough to justify spending on predictive quality platforms, especially where organizations can model risk earlier and improve documentation quality before claims are finalized. This pressure also supports consolidation, because providers, pharma companies, and CROs increasingly want vendors that can connect quality management with measurable operational and reimbursement outcomes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Implementation and Integration Costs | -2.8% | Global, with stronger pressure in emerging APAC markets and mid-market organizations | Medium term (2-4 years) |

| Data Security, Privacy and HIPAA or GDPR Compliance Hurdles | -2.3% | Global, amplified in the EU and multinational pharma operations | Short term (≤ 2 years) |

| Fragmented Interoperability Standards | -1.9% | Global, most acute in multi-system EHR environments | Medium term (2-4 years) |

| Algorithmic Bias and Clinical Explainability Limitations | -1.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Security, Privacy & HIPAA/GDPR Compliance Hurdles

Security and privacy obligations remain a material restraint on the AI in the healthcare quality management market because they raise both implementation cost and ongoing operating burden. In Europe, GDPR Article 9 treats health information as special category data and requires additional controls, while the European Health Data Space adds new requirements for secondary use in model development. In the United States, stricter expectations around encryption, multi-factor authentication, risk assessment, and governed handling of protected health information are narrowing the room for lightly controlled deployment models. Many off-the-shelf AI tools remain unsuitable for regulated healthcare workflows because buyers need stronger contractual and technical controls than standard consumer-grade offerings provide. This pushes pharma quality teams toward enterprise-scale or tightly managed deployment models, which slows adoption among smaller organizations with fewer compliance resources.

Algorithmic Bias & Clinical Explainability Limitations

Bias and explainability remain durable constraints where AI outputs affect regulatory submissions, patient safety, or core quality decisions in the AI in healthcare quality management market. The FDA’s January 2025 draft guidance requires manufacturers to assess model performance across race, ethnicity, sex, and age subgroups, which increases validation burden as models become more complex. In clinical documentation, AI ambient scribes produced hallucinations in 31% of notes compared with 20% in physician-authored notes, which underscores the need for stronger validation in regulated environments. The joint FDA-EMA principles published in January 2026 also call for lifecycle management and continuous performance assessment across drift events, which extends compliance work far beyond initial deployment. These limits are especially important for knowledge graphs and reinforcement learning approaches, where decision pathways are harder to explain to reviewers and auditors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Infrastructure Anchors Market, Services Pivot to Outcomes

Software accounted for 58.23% of the AI in healthcare quality management market size in 2025, which shows how strongly buyers favor cloud-native quality systems, electronic data capture tools, and AI-enabled workflow layers across pharmaceutical and CRO settings. This lead reflects the preference for integrated platforms over narrow point solutions, because broader systems reduce data handoff issues and support more consistent validation across regulated processes. Modular deployment still matters, but buyers increasingly want modules that sit inside a governed platform rather than tools that operate outside the main quality stack. Roche’s secure AWS deployment for protocol deviation classification illustrates this pattern, since the model sat within a controlled operating environment rather than a lightweight standalone application.

Services, while smaller in 2025, are the fastest-growing component with a 17.23% CAGR through 2031 in the AI in healthcare quality management market. Growth comes from implementation complexity, validation work, governance design, and ongoing model performance review, which many clients cannot staff internally. This service demand is not one-time in nature because models must be updated, revalidated, and monitored as data conditions change over time. The result is a recurring service layer around the software base, which improves vendor stickiness and keeps services tied closely to enterprise account growth in the AI in healthcare quality management market.

By Application: Patient Outcome Prediction Leads, Clinical Trial Optimization Accelerates

Patient outcome prediction held 38.54% of AI in the healthcare quality management market size in 2025, supported by long-running investment in models that flag adverse events, disease progression, and likely response patterns. These use cases are central to quality management because they influence care escalation, monitoring intensity, and documentation completeness across clinical programs. Real-time deterioration surveillance has already shown a 35.6% reduction in in-hospital mortality in randomized settings, which supports ongoing procurement of predictive quality tools. This helps explain why patient outcome prediction remains the largest application area in the AI in healthcare quality management market.

Clinical trial optimization is the fastest-growing application and is projected to grow at 16.94% through 2031, as sponsors try to reduce avoidable amendments, site underperformance, and screening inefficiency. Published evidence shows NLP-assisted prescreening can reach 76.1% chart-level accuracy versus 71.5% for human-only review and can add 10 to 20 patients screened each week in a high-volume cancer center. ConcertAI also reported that AI-driven feasibility validation can shorten overall trial timelines by 10 to 20 months and reduce protocol amendments by 50%. The broader application mix in the AI in healthcare quality management industry is therefore moving from reactive quality checks toward earlier intervention and better protocol design.

By Technology: Machine Learning Holds Share, NLP Reshapes Quality Workflows

Machine learning accounted for 45.26% of the 2025 AI in healthcare quality management market because it remains the core method behind outcome prediction, risk scoring, and deviation classification. Its lead reflects established use in supervised prediction and reinforcement-style optimization tasks that already fit operational quality needs. Machine learning also benefits from a longer validation history than newer generative approaches, which matters in tightly regulated settings. That makes it the most established technology layer within the AI in healthcare quality management market.

Natural language processing is the fastest-growing technology and is projected to expand at 18.96% through 2031 because much of healthcare quality work still sits inside unstructured notes, narratives, and regulatory documents. In pathology report extraction, EHR-derived large language models achieved 99.8% accuracy on structured variables, which shows that text extraction can now support production use in research workflows. Published prescreening work in oncology also showed accuracy gains for NLP-assisted review, which reinforces its value in trial operations and quality abstraction. Computer vision and knowledge graph tools are still early in adoption. Still, they are gaining relevance where quality teams must interpret sequencing outputs and other complex data objects in the AI in healthcare quality management market.

By Deployment: Cloud Leads, On-Premise Paradoxically Accelerates

Cloud deployment held 61.41% of the AI in healthcare quality management market in 2025, reflecting the wider shift toward multi-tenant architectures that support data sharing, benchmarking, and scalable compute. This model is especially useful for large sponsor networks and data-rich research environments where usage can rise quickly across sites and programs. It also aligns with vendors seeking to update models and distribute improvements across broad customer bases without repeated local installations. Those advantages explain why cloud remains the leading deployment model in the AI in healthcare quality management market.

On-premise deployment is still the fastest-growing deployment mode, with a 19.23% CAGR through 2031, because stricter sovereignty and validation needs are preserving demand for controlled local infrastructure. GxP-oriented environments often require stronger audit-trail integrity and tighter data handling control during model training and execution. Many multinational organizations are therefore moving toward dual architectures, using cloud for benchmarking and population analytics while retaining on-premise environments for more sensitive release and validation tasks. ValGenesis’s April 2026 launch of AI-governed validation lifecycle management shows that commercial support for these tightly managed environments is becoming stronger at scale.

By Analytics Type: Predictive Analytics Commands Share, Descriptive Analytics Builds the Foundation

Predictive analytics held the largest share of the 2025 AI in healthcare quality management market at 48.92%, which matches its role in front-loading quality risk detection across drug development and healthcare delivery workflows. Buyers favor predictive tools because they support earlier intervention on safety, protocol, and operational issues before those issues become more costly. This makes predictive analytics central to platforms that aim to shift quality management from retrospective review toward active prevention. Its scale, therefore, reflects both immediate business value and a better fit with the current direction of AI in the healthcare quality management market.

Descriptive analytics is projected to grow fastest at 20.76% through 2031 because many organizations are still building standardized dashboards, reporting layers, and baseline visibility before moving into more advanced optimization. This is especially relevant for smaller biotechs and emerging-market CROs that need cleaner operational foundations before deploying richer prediction tools. The FDA-EMA principles also support phased adoption that starts with lower-risk administrative and descriptive uses before moving deeper into prescriptive quality management. That stepwise path creates a natural upsell motion for vendors as customers mature inside the AI in healthcare quality management market.

By Data Source: EHR Data Anchors the Market, Genomics Emerges as the Growth Layer

Electronic health records accounted for 43.59% of the 2025 AI in healthcare quality management market because they remain the main input for patient outcome prediction, benchmarking, and adverse event review. EHR data is deeply embedded in provider and sponsor workflows, which makes it the most practical starting point for production AI deployment. Strong extraction results from pathology reports, including 99.8% accuracy on structured variables, further support confidence in EHR-centered automation. This anchoring role keeps EHR data at the center of current platform design in the AI in healthcare quality management market.

Genomics and multi-omics data are the fastest-growing data sources, with a 17.39% CAGR through 2031, because target validation and research quality review are becoming more dependent on AI-ready biological datasets. Genomics launched MySTra in October 2025 on the back of more than 20,000 genome-wide association studies, allowing users to complete drug target validation queries in minutes instead of months. Illumina’s Billion Cell Atlas adds another layer by creating a new high-volume source of transcriptomic data that requires AI-native quality scoring and handling. Claims, clinical trial datasets, and other real-world evidence sources remain important, but genomic data is becoming the fastest-expanding growth layer in the AI in healthcare quality management market.

By End User: Pharmaceutical Companies Lead, CROs Accelerate Fastest

Pharmaceutical companies held 46.37% of the AI in healthcare quality management market in 2025 because they carry broad quality obligations across discovery, clinical development, post-marketing surveillance, and manufacturing. They also have clearer return-on-investment visibility than smaller buyers, since quality gains can be spread across large portfolios and multiple functions. Sanofi’s ARTEMIS program, which automates intake and analysis for more than 700,000 adverse event reports annually, achieved a 15% reduction in operational costs after Phase 1 completion in August 2024 and is targeting up to 50% by 2027. That scale advantage keeps pharmaceutical companies in the lead position across the AI in healthcare quality management industry.

Contract research organizations are the fastest-growing end-user group, with a 20.48% CAGR through 2031, as competition shifts toward predictive site quality and faster study execution. PSI CRO’s January 2026 launch of SYNETIC was built on data from more than 500,000 institutions and 3 million study sites, showing how deeply CRO differentiation is now tied to data-driven quality execution. CROs are using these tools to reduce weak site selection, improve enrollment quality, and support more consistent trial delivery across large networks. Biotechnology companies are also adopting AI quickly in focused areas. Still, CROs show the fastest growth path in the AI in healthcare quality management market because quality performance itself is becoming a commercial differentiator.

Geography Analysis

North America held 35.43% of AI in healthcare quality management market size in 2025, which reflects the region’s dense mix of regulatory activity, large healthcare datasets, and strong enterprise buyer presence. The United States remains the center of regional demand because it combines large pharma headquarters, major CRO operations, and health systems with broad digital infrastructure. CMS reimbursement programs and federal AI governance principles continue to create a strong demand signal even when broader IT budgets face pressure. Canada and Mexico remain smaller markets, but both benefit from their role in North American clinical development networks that require more standardized quality processes across sites. Europe follows as the second major regional base in the AI in healthcare quality management market, supported by the EU AI Act, the European Health Data Space, and growing alignment around lifecycle governance for regulated AI use.

Asia-Pacific is the fastest-growing region, with a 22.54% CAGR through 2031, driven by regulatory modernization, strong CRO capacity, and more active collaboration between healthcare and technology players. Japan is a key anchor, where Shionogi and Hitachi launched a generative AI solution in February 2026 that reduced clinical study report preparation time by 50% and clinical trial protocol drafting time by 20%. NTT DATA’s April 2026 collaboration with Chugai Pharmaceutical also shortened draft preparation for Interview Forms by 1 to 2 months, showing that pharmacovigilance and regulatory quality workflows are moving quickly toward automation. China and India add scale through high-volume clinical trial execution, and work from Beijing University Cancer Hospital showed that an AI-enabled QC platform flagged 19.9% of 2023 study reports for quality intervention across 211 studies.

The Middle East and Africa and South America remain smaller in the AI in healthcare quality management market, but both regions show a positive direction of travel. GCC countries are investing in broader AI healthcare infrastructure, which creates early openings for quality management platforms that can scale without heavy local buildout. Brazil and Argentina remain the largest South American country markets in the current regional mix, while South Africa serves as an important base within sub-Saharan Africa. Across both regions, cloud-based SaaS models are better placed than local on-premise approaches because data infrastructure and specialized IT capability remain uneven outside major urban centers.

Competitive Landscape

The AI in healthcare quality management market remains moderately concentrated at the enterprise level, but it is still fragmented across mid-market and specialty use cases. Large vendors such as Oracle Health, Optum, Epic-linked ecosystems, and Cognizant benefit from existing relationships, larger implementation teams, and the ability to invest in governance at scale. Competitive positioning is increasingly shaped by 3 factors, proprietary data access, multimodal AI capability, and the depth of regulatory prevalidation that can shorten customer deployment cycles. That means scale alone is not enough, because buyers also want evidence that models can operate in governed settings without creating validation delays. This mix supports moderate concentration in enterprise accounts while leaving room for specialists that own narrow but valuable datasets or workflow advantages in the AI in healthcare quality management market.

Oracle Health strengthened its position in May 2026 when Oracle obtained ISO/IEC 42001:2023 certification across Oracle Health, Oracle Life Sciences, and Oracle Cloud Infrastructure AI management systems. That move matters because enterprise buyers increasingly view formal AI management certification as a practical signal of readiness for regulated deployment. Tempus AI has taken a different route by expanding multi-year collaborations with drug developers, including Gilead, around de-identified multimodal oncology data, analytics, and R&D support. Parexel’s collaboration with Palantir shows another path, where the focus is less on disease-specific models and more on validated process automation and faster clinical data delivery across trial operations.

Mid-market competition is more dispersed, with vendors differentiating through implementation speed, workflow fit, and narrower domain expertise. ValGenesis is positioning around governed validation lifecycle management for GxP environments, while ConcertAI is pushing agentic trial optimization tied to faster execution and fewer amendments. Optum’s AI marketplace initiative also shows that platform owners are trying to widen their ecosystem reach rather than rely only on internally built applications. Overall competition in the AI in healthcare quality management market is likely to favor vendors that combine trusted data access, governed deployment, and measurable workflow impact rather than those that offer general-purpose AI without sector-specific quality controls.

AI In Healthcare Quality Management Industry Leaders

IBM Watson Health

Cognizant

Epic Systems

Oracle Health

Optum

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Oracle America, Inc. obtained ISO/IEC 42001:2023 certification for its AI Management Systems across Oracle Health, Oracle Life Sciences (including Clinical Suite and Argus), and Oracle Cloud Infrastructure, establishing a formal governance benchmark for regulated AI deployment in pharma quality management.

- April 2026: Tempus AI announced an expanded, multi-year strategic collaboration with Gilead Sciences to advance Gilead's oncology R&D pipeline using Tempus' de-identified multimodal data, Lens platform, and analytical services; Q1 2026 revenue reached USD 348.1 million, up 36.1% year-on-year.

- April 2026: ValGenesis launched the next generation of VAL, an AI-governed validation lifecycle platform for life sciences, promising up to 80% reduction in validation time and at least 50% greater efficiency versus conventional digital validation for GxP-regulated environments.

Global AI In Healthcare Quality Management Market Report Scope

As per the scope of the report, AI in healthcare quality management refers to the application of artificial intelligence tools to improve clinical and operational quality outcomes. It integrates predictive analytics, machine learning, and natural language processing into quality dashboards, risk scoring, and patient outcome monitoring. The goal is to enhance compliance, reduce errors, and optimize care delivery by automating quality measurement and continuous improvement processes.

The AI in healthcare quality management market is segmented by component, application, technology, deployment, analytics type, data source, end user, and geography. By component, the market is segmented into software and services. By application, the market is segmented into drug discovery & development, clinical-trial optimization, patient-outcome prediction, quality-measure benchmarking, adverse-event detection & RCA, and others. By technology, the market is segmented into machine learning, natural-language processing (NLP), computer vision, knowledge Graphs & Reasoning, and others. By deployment, the market is segmented into on-premise and cloud. By analytics type, the market is segmented into descriptive, predictive, and prescriptive. By data source, the market is segmented into electronic health records (EHR), genomics / multi-omics, clinical-trial & RWE datasets, claims & billing, and others. By end user, the market is segmented into pharmaceutical companies, biotechnology companies, contract research organizations (CROs), and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and market trends for 17 countries across major regions worldwide. The report offers market value (in USD) for the above segments.

| Software |

| Services |

| Drug Discovery & Development |

| Clinical Trial Optimisation |

| Patient Outcome Prediction |

| Quality Measure Benchmarking |

| Adverse Event Detection & RCA |

| Others |

| Machine Learning |

| Natural-Language Processing (NLP) |

| Computer Vision |

| Knowledge Graphs & Reasoning |

| Others |

| On-premise |

| Cloud |

| Descriptive |

| Predictive |

| Prescriptive |

| Electronic Health Records (EHR) |

| Genomics / Multi-omics |

| Clinical-Trial & RWE datasets |

| Claims & Billing |

| Others |

| Pharmaceutical Companies |

| Biotechnology Companies |

| Contract Research Organizations (CROs) |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of MEA | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| By Application | Drug Discovery & Development | |

| Clinical Trial Optimisation | ||

| Patient Outcome Prediction | ||

| Quality Measure Benchmarking | ||

| Adverse Event Detection & RCA | ||

| Others | ||

| By Technology | Machine Learning | |

| Natural-Language Processing (NLP) | ||

| Computer Vision | ||

| Knowledge Graphs & Reasoning | ||

| Others | ||

| By Deployment | On-premise | |

| Cloud | ||

| By Analytics Type | Descriptive | |

| Predictive | ||

| Prescriptive | ||

| By Data Source | Electronic Health Records (EHR) | |

| Genomics / Multi-omics | ||

| Clinical-Trial & RWE datasets | ||

| Claims & Billing | ||

| Others | ||

| By End User | Pharmaceutical Companies | |

| Biotechnology Companies | ||

| Contract Research Organizations (CROs) | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of MEA | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the expected value of the AI in healthcare quality management market by 2031?

The AI in healthcare quality management market is forecast to reach USD 0.97 billion by 2031, rising from USD 0.45 billion in 2026 at a 16.47% CAGR over 2026-2031.

What is driving adoption of AI in healthcare quality management solutions?

The main drivers are stronger regulatory oversight, larger and more complex healthcare datasets, better predictive and prescriptive analytics, and payment models that reward better quality and outcomes.

Which component leads current spending in this field?

Software leads current spending with 58.23% share in 2025, reflecting demand for integrated quality management platforms and AI-enabled workflow systems.

Which end users are growing fastest?

Contract research organizations are growing fastest with a projected 20.48% CAGR through 2031, as they use AI to improve site selection, enrollment quality, and trial execution.

Which region is expanding fastest?

Asia-Pacific is the fastest-growing region with a 22.54% CAGR through 2031, supported by regulatory modernization and active deployment in Japan, China, and India.

What technologies are shaping workflow change the most?

Machine learning still holds the largest technology share at 45.26%, while natural language processing is growing fastest at 19.23% because quality work remains heavily dependent on unstructured text.

Page last updated on: