AI In Population Health Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 16.76 Billion |

| Market Size (2031) | USD 46.51 Billion |

| Growth Rate (2026 - 2031) | 22.64% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Population Health Management Market Analysis by Mordor Intelligence

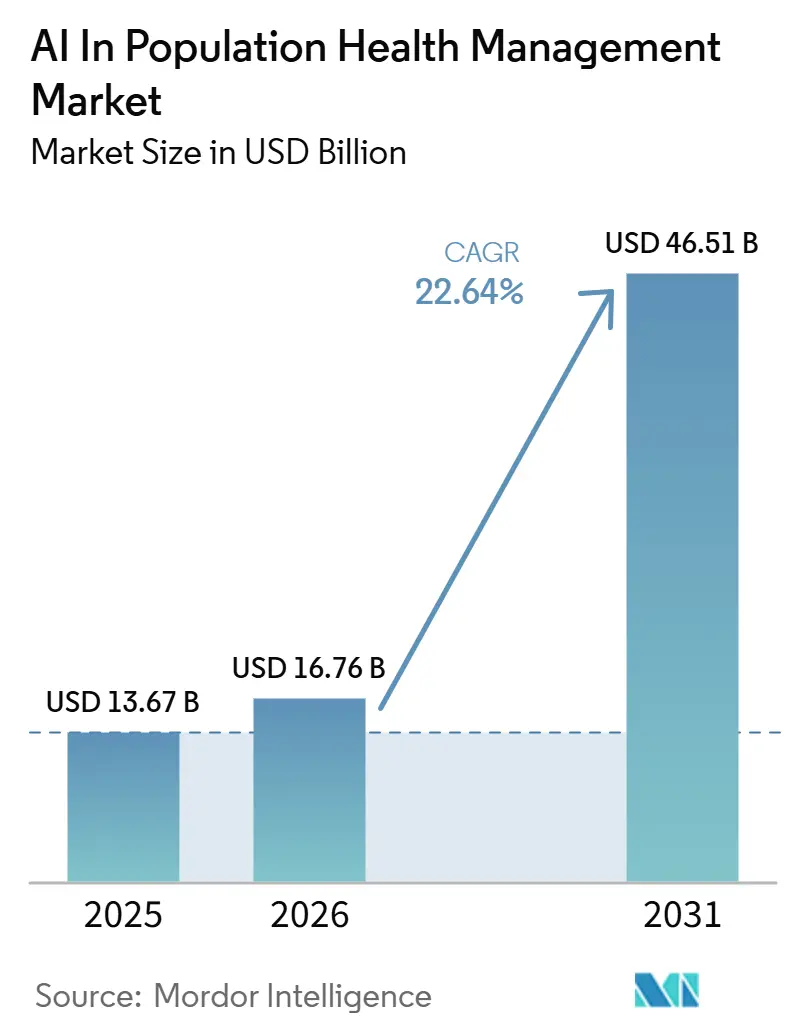

The AI In Population Health Management Market size is expected to increase from USD 13.67 billion in 2025 to USD 16.76 billion in 2026 and reach USD 46.51 billion by 2031, growing at a CAGR of 22.64% over 2026-2031.

The AI in population health management market is moving into a more durable growth phase because care financing, care coordination, and provider accountability are now being reset around measurable outcomes rather than service volume. This shift is making longitudinal analytics, risk identification, and automated care-gap tracking more central to how providers and payers manage attributed populations. CMS now brings mandatory bundled payment participation to selected geographies through TEAM in 2026, which expands value-based obligations beyond the group of organizations that had voluntarily entered earlier models. ACO REACH also showed average savings of USD 930 per beneficiary against fee-for-service benchmarks, which gives health systems and payers a clearer financial basis for AI-led population oversight. As a result, competition in the AI in population health management market is centered on platforms that can connect claims, clinical, and patient engagement data, while the strongest opportunities remain tied to automation that helps organizations manage larger panels with tighter margins.

Key Report Takeaways

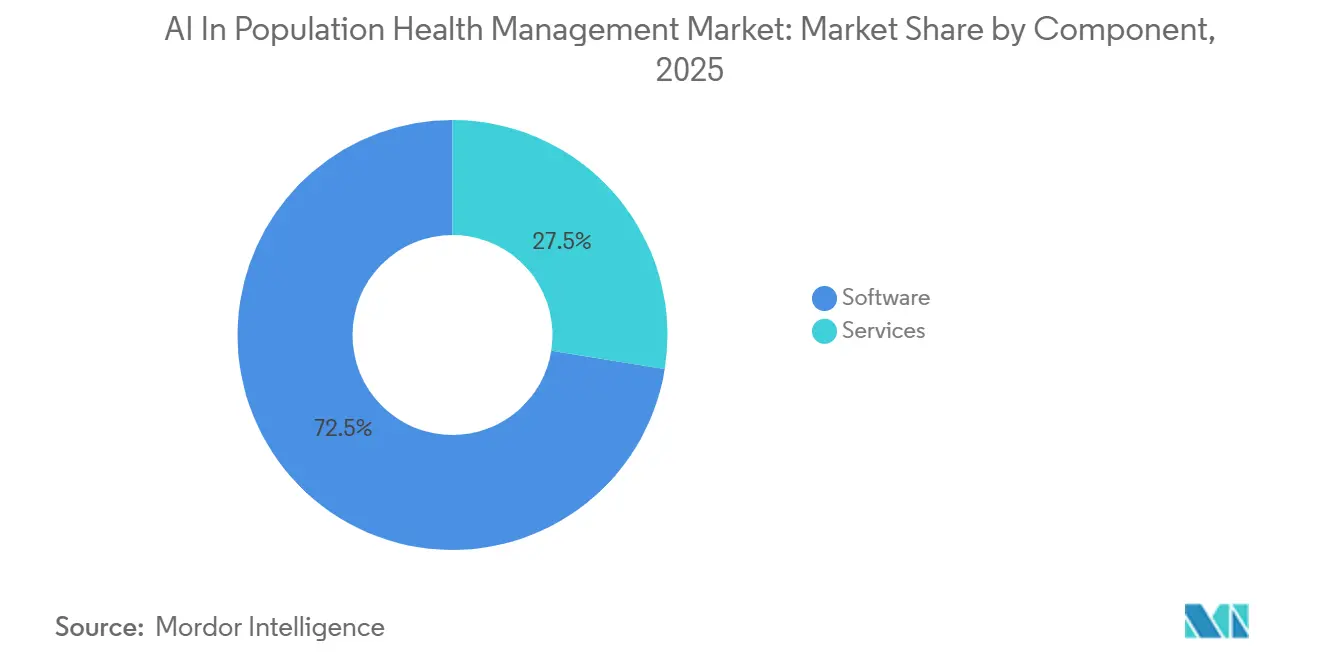

- By component, software held 72.48% share in 2025, while services is projected to grow at 22.97% CAGR through 2031.

- By deployment mode, cloud-based deployment held 56.27% share in 2025, while on-premises deployment is projected to grow at 23.56% CAGR through 2031.

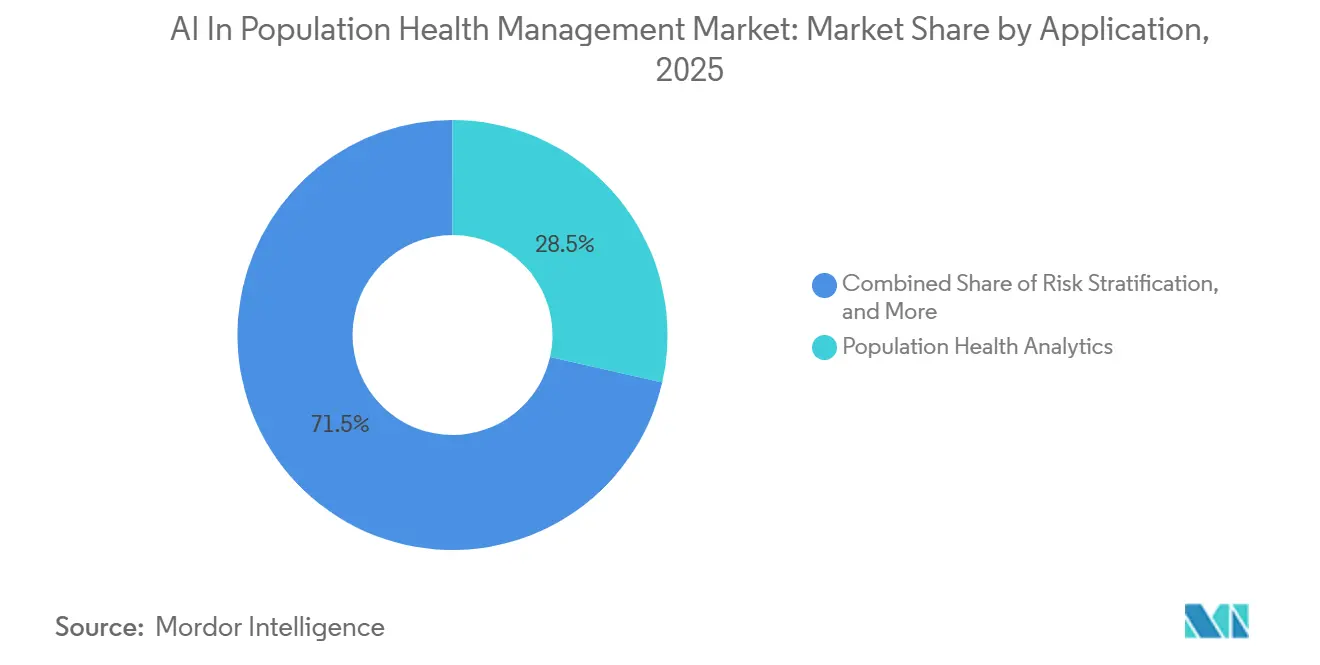

- By application, population health analytics accounted for 28.54% share in 2025, while risk stratification is projected to advance at 24.85% CAGR through 2031.

- By end user, healthcare providers held 53.19% share in 2025, while healthcare payers are projected to grow at 23.92% CAGR through 2031.

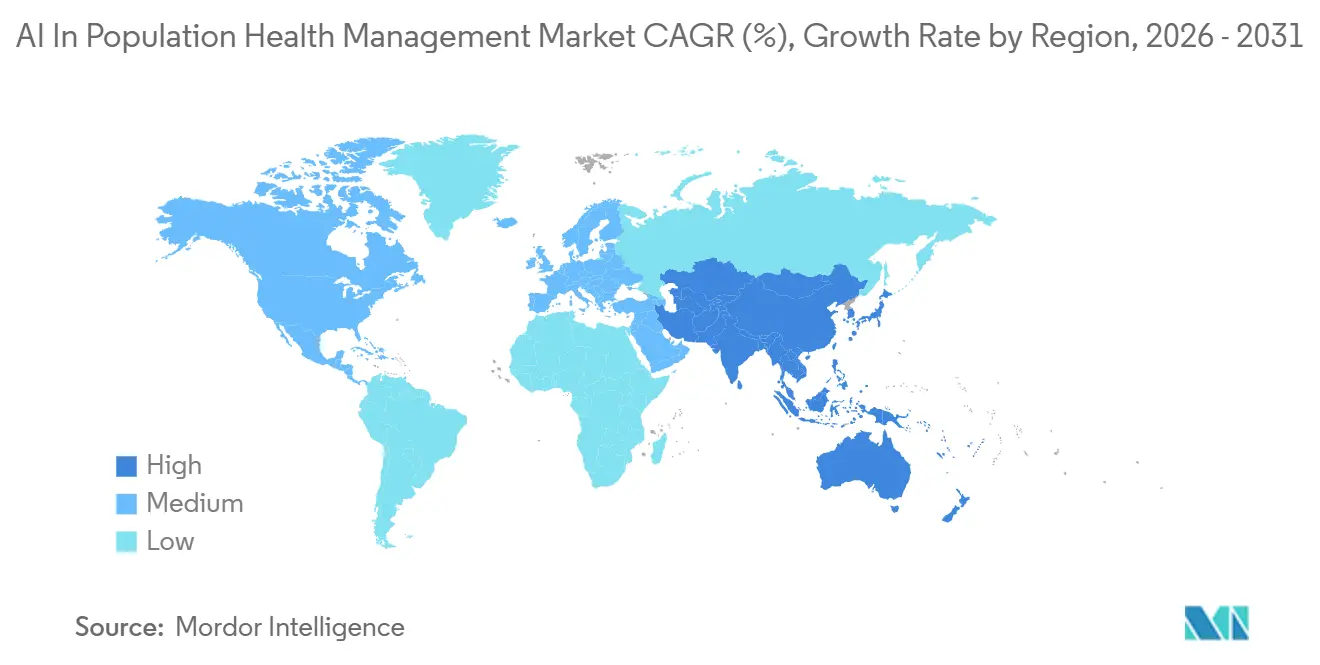

- By geography, North America led with 38.47% revenue share in 2025, and Asia-Pacific is forecast to register a 24.93% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Population Health Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift Toward Value-Based Reimbursement | +4.1% | North America, Western Europe | Short term (≤ 2 years) |

| Rising Chronic-Disease Burden | +4.5% | Global, with acceleration in APAC and MENA | Long term (≥ 4 years) |

| AI-Driven Risk Stratification and Care-Gap Closure | +5.2% | Global, mature in North America, fast-growing in APAC | Short term (≤ 2 years) |

| Cloud-Native Healthcare Data Platforms | +3.6% | North America, EU, Australia | Medium term (2-4 years) |

| Medicaid and Public-Health Data Modernization | +2.0% | United States, expanding to select APAC public health systems | Medium term (2-4 years) |

| Primary-Care Workforce Shortages Favor Panel Automation | +3.1% | Global, acute in UK, Japan, US | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shift Toward Value-Based Reimbursement

The AI in population health management market is gaining direct support from payment reform because value-based care now creates an operating need for continuous performance measurement rather than a discretionary analytics project. TEAM is active in 2026 as a mandatory bundled payment model in selected geographies. That change moves value-based accountability from an optional program into a daily requirement for many provider organizations.[1]“Artificial Intelligence as a Catalyst for Value-Based Health Insurance in the United States: Narrative Review and Policy Perspective,” This matters because mandatory models reach health systems that had stayed outside earlier pilots, including organizations that were slower to fund analytics, workflow automation, or care management tools. The AI in the population health management market, therefore, benefits from a broader demand base, since providers now need better forecasting, attribution management, and utilization control to protect margins under risk-based contracts. ACO REACH savings of USD 930 per beneficiary also make the return on better population oversight easier to defend in capital planning and board discussions. As specialty-focused value-based models move closer to wider use from 2027 onward, population-level AI will increasingly function as a revenue protection tool as much as a clinical support layer.

Rising Chronic-Disease Burden

The AI in the population health management market is also expanding because chronic disease is creating a larger and more complex base of patients who need continuous monitoring, prioritization, and intervention over the years, rather than isolated visits. Global diabetes prevalence reached 588.7 million in 2024, and that burden is being compounded by cardiovascular disease, obesity, and multimorbidity across many health systems.[2]“Medisolv Expands AI Capabilities for Value-Based Care with Acquisition of Lilac Software,” In China, chronic diseases accounted for more than 80% of deaths and over 70% of total disease burden, while prevalence among people aged 60 and above reached 81.1%.[3]“Empowering Chronic Disease Management with Smart Healthcare in China: A Policy Effectiveness Evaluation by PMC Index Model,” These conditions are pushing the AI in the population health management market toward models that can combine long time horizons, multiple conditions, and care patterns that span providers and settings. They are also making single-institution datasets less sufficient, which supports the shift toward federated learning and multi-institution data collaboration for chronic disease modeling. In primary care Medicaid settings, proactive AI-enabled chronic disease management programs reported 22.9% fewer all-cause acute events and 48.3% fewer ambulatory care-sensitive hospitalizations, which strengthens the case for payer-side and provider-side investment in AI in the population health management market.[4]Sanjay Basu, Pablo Bermudez-Canete, Tannen Christopher Hall, and Pranav Rajpurkar, “Optimizing AI Solutions for Population Health in Primary Care,”

AI-Driven Risk Stratification and Care-Gap Closure

The AI in the population health management market is being pulled forward by demand for better risk stratification, but the focus is shifting from raw prediction accuracy toward reliability across underserved populations. Research published in 2026 showed that healthcare access disparities weakened EHR reliability for 73% of examined conditions among patients with cost-constrained care, which directly affects model inputs and increases the risk of missed high-risk cases. That finding changes vendor priorities because health systems and payers now need models that can remain useful even when historical records are incomplete, delayed, or uneven across groups. Arcadia responded by launching its AI Factory development platform in 2026 and by integrating Surescripts' first-fill abandonment data in October 2025 to help close medication-adherence care gaps faster. A Cambridge foundation model trained on 23 million UK primary care patients, SurvivEHR, also showed stronger long-horizon prediction for patients with multiple long-term conditions by modeling competing risks together. The AI in population health management market is therefore moving toward models that connect disease progression, adherence behavior, and multi-condition trajectories rather than treating each risk pathway in isolation.

Primary-Care Workforce Shortages Favor Panel Automation

The AI in the population health management market is also benefiting from workforce pressure because care teams increasingly need automation that can manage outreach, reminders, and prioritization without waiting for direct physician initiation. This is shifting adoption away from simple documentation support and toward panel automation tools that can carry a larger share of routine coordination work. Lumeris has positioned Tom as an agentic platform that engages patients through text and voice using EHR and claims data, which reflects this move toward scalable non-visit care management. The AI in the population health management market gains from that change because organizations can justify investment on staffing grounds as well as quality and utilization grounds. In the UK, AI triage tools showed the ability to reduce administrative time by up to 43 minutes per staff member per day, and an NHS pilot reported a 30% reduction in missed appointments over 6 months. Those results show that automation demand in the AI in population health management market is spreading beyond North America and is increasingly tied to capacity management in frontline care.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy and Cybersecurity Risks | -1.8% | Global, acute in North America and EU | Short term (≤ 2 years) |

| High Implementation and Legacy Integration Costs | -1.5% | Global, particularly acute in mid-size provider organizations | Medium term (2-4 years) |

| Unclear AI Reimbursement and Liability Frameworks | -2.2% | United States, with emerging EU analogue under AI Act | Medium term (2-4 years) |

| Model Bias and Drift from Fragmented Longitudinal Data | -1.6% | Global, most pronounced in APAC and safety-net provider settings | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Unclear AI Reimbursement and Liability Frameworks

The AI in the population health management market still faces a meaningful brake because reimbursement policy has not fully caught up with software-led clinical support and population-level decision systems. Health Affairs noted in 2026 that Medicare payment methodology was not built for software-based AI services, which leaves many tools squeezed into older benefit categories and creates uncertain payment treatment. When buyers cannot see a stable reimbursement path, they become more selective about deploying tools that improve outcomes but may not generate a direct and near-term billing mechanism. That hesitation affects contracting, implementation speed, and internal ownership because finance teams, legal teams, and clinical leaders often judge the same product through different risk lenses. The AI in population health management market is especially exposed, where vendors are asking providers to fund tools that may reduce future utilization, even when the long-term clinical value is strong. Until policy gives clearer signals on reimbursement treatment and responsibility for AI-assisted decisions, adoption will continue to move faster in administrative and operational use cases than in tools that sit closer to formal benefit design or medical necessity decisions.

Model Bias and Drift from Fragmented Longitudinal Data

The AI in the population health management market is also constrained by uneven data quality because fragmented longitudinal records can weaken both fairness and durability in deployed models. A 2025 systematic review covering 129 studies found poorer AI performance for women, racial minorities, patients with public insurance, and geographically underrepresented groups, with diabetic retinopathy screening sensitivity ranging from 51.0% to 85.9% across ethnic subgroups. This problem does not end with initial bias because model drift can remain hidden when training data and real-world deployment data come from different care access environments. Research in 2026 showed that adding patient self-reported health data improved prediction for low-access patients and identified future diabetes cases that EHR-only models missed. That result suggests the AI in the population health management market cannot rely on larger EHR datasets alone when the underlying record still reflects uneven access and incomplete encounters. Vendors and buyers will therefore need multimodal data pipelines, stronger monitoring, and more deliberate recalibration if they want risk stratification tools to remain clinically credible across diverse populations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominance Reflects Platform-First Procurement

Software held 72.48% share in 2025, which means the buying center of AI in population health management market is still concentrated around durable platforms rather than short-term consulting work. This pattern fits a platform-first procurement model because providers and payers want one operating environment that can support risk identification, outreach, contract analytics, and utilization management together. The AI in the population health management market has therefore favored vendors that can embed AI directly into software modules rather than leaving intelligence outside the core application stack. That dynamic reduces the role of episodic advisory work at the earliest stage of adoption, since the initial value now depends more on what the installed platform can do every day.

Services are still the fastest-growing component at 22.97% CAGR over 2026-2031, which shows that implementation work remains important even when software owns the larger revenue base. Growth in services comes from managed support, deployment expertise, and change management for organizations that do not have internal data science or integration teams. The AI in population health management market still carries meaningful service demand because legacy EHR environments, fragmented claims feeds, and provider workflow differences make deployment harder than software demonstrations often suggest. Compliance expectations around predictive decision-support interventions also expand the need for documentation, validation, and governance support across live installations. Within the AI in population health management industry, that leaves the component mix looking stable at the top line, but more service intensive below the surface as buyers move from pilot use into scaled operations.

By Deployment Mode: Cloud Builds the Foundation While On-Premises Accelerates

Cloud-based deployment held 56.27% share in 2025, which confirms that the AI in population health management market still relies heavily on scalable environments that can handle multi-source ingestion and near real-time analytics. Cloud adoption fits population health workloads because those workloads depend on continuous data refresh, broad interoperability, and frequent model updates across large attributed populations. The model also supports faster expansion across use cases because organizations can add risk scoring, care-gap logic, and engagement tools without rebuilding the entire data foundation. In practical terms, cloud remains the easiest path for many buyers who need to combine payer data, provider data, pharmacy data, and outreach activity in one view. That is why the current revenue base in the AI in population health management market continues to lean toward cloud, even as privacy and sovereignty debates become more visible.

On-premises deployment is the fastest-growing mode at 23.56% CAGR over 2026-2031, which shows that data control is becoming a more important buying factor in regulated settings. The AI in population health management market size for on-premises and tightly controlled local environments is rising where buyers want stronger oversight of model training, sensitive patient records, and data movement across borders. China’s NHSA stated in 2026 that AI models for the Personal Medical Insurance Cloud should train internally without data leaving the platform, which illustrates why sovereign or tightly bounded architectures are gaining support. The AI in population health management market is therefore not moving toward one universal hosting model, because many organizations now want cloud flexibility and local control at the same time. Hybrid deployment has become the practical compromise for many mid-market health systems that want the economics of cloud while still meeting residency and privacy expectations.

By Application: Risk Stratification Leads Growth, Analytics Anchors the Market

Population health analytics held the largest application share at 28.54% in 2025, which shows that the AI in population health management market still starts with a broad measurement layer before it narrows into specific interventions. Analytics remains the anchor because providers and payers need a common view of utilization, quality, attribution, and cost before they can direct care management or member engagement effectively. That makes this category the base infrastructure for many other use cases, especially when buyers are still standardizing data models and governance. Risk stratification is the fastest-growing application at 24.85% CAGR over 2026-2031, which reflects the move from retrospective reporting toward forward-looking prioritization inside daily workflows. The AI in population health management market size for risk stratification is therefore expanding faster than mature reporting categories, because buyers increasingly want the system to decide who should be contacted, reviewed, or escalated next.

Care management and coordination are also moving higher in the AI in population health management market as agentic tools take on more outreach and follow-up tasks that once depended on manual nurse or case manager effort. Patient engagement platforms are becoming more multilingual and more voice enabled, which matters when organizations are trying to close equity gaps across populations with different access patterns and communication preferences. The user-supplied evidence also points to a broader application mix, with public health surveillance and pharmaceutical real-world evidence included in the other category as secondary data use frameworks open more access pathways. The European Health Data Space regulation entered into force in March 2025, which supports this wider use of linked health data across approved purposes. A Stanford-led 2025 study found that proactive AI outreach improved colorectal cancer screening engagement among Spanish-speaking patients versus conventional outreach teams, which shows how the AI in population health management market is turning patient engagement from a convenience feature into a targeted access tool.

By End User: Providers Set the Volume, Payers Define the Margin

Healthcare providers held 53.19% share in 2025, which shows that the AI in population health management market still draws most of its installed base from the organizations that hold the deepest clinical data and carry the most direct care delivery accountability. Providers sit closest to the workflows that population health tools are trying to influence, including referrals, follow-up visits, outreach timing, care plans, and quality documentation. They also face direct operational pressure when mandatory value-based models require better utilization control and better attribution performance. The AI in population health management market keeps leaning toward provider demand because hospitals, physician groups, and integrated systems have the widest immediate need to connect clinical decision making with financial accountability. ACO REACH savings of USD 930 per beneficiary reinforce that provider-side adoption is not only a technology decision, but also a margin management decision in risk-bearing care models.

Healthcare payers are the fastest-growing end-user group at 23.92% CAGR over 2026-2031, and that shows how quickly member engagement, risk adjustment, utilization management, and contract performance are converging. The AI in population health management market is becoming more attractive to payers because they can use the same data environment to support care navigation, payment integrity, and network performance. Government agencies and public health organizations also represent a growing part of demand, even if their revenue contribution remains smaller than that of providers and payers. ASTHO reported in 2026 that 14% of state and territorial health offices were already using AI for disease surveillance and predictive modeling, while CDC demonstrations showed more than 5,500 labor hours saved in grant-data analysis. Within the AI in population health management industry, that wider mix of end users suggests the strongest vendors will be those that can serve provider, payer, and public sector workflows without rebuilding the platform for each buyer type.

Geography Analysis

North America held 38.47% of AI in population health management market share in 2025, which keeps the region at the center of current commercial activity. The United States remains the main proving ground because TEAM, ACO REACH, and the Ambulatory Specialty Model place value-based accountability and performance measurement at the center of care financing. That policy stack gives the AI in population health management market a stronger demand signal than in most other regions, since providers and payers have clearer reasons to track cost, quality, utilization, and attributed outcomes in one system. North America also benefits from mature payer-provider contracting structures and a broad installed EHR infrastructure, which makes population-level analytics easier to operationalize. These conditions keep the AI in population health management market commercially strongest in North America, even as growth begins to broaden more sharply outside the region.

Europe is more fragmented, but the region is becoming more organized as data governance, AI oversight, and secondary data access rules move into a clearer framework. Germany’s opt-out electronic patient file covered all 73 million statutory insured people from January 2025 and began feeding the national Research Data Center from July 2025 under formal oversight, which gives the region a stronger longitudinal data base than before. France committed EUR 110 million, around USD 119 million, through France 2030 for health data warehouses and launched a national AI and health data strategy in July 2025 focused on population-level monitoring and digital twin modeling. The UK’s NHS reform agenda is also pushing faster AI use in primary care, especially where capacity pressure and missed appointments are already affecting access. At the same time, European medical leadership has warned that slow validation and governance processes could leave scale advantages to U.S. and Chinese technology firms, which explains why procurement intent is rising even where deployment still lags.

Asia-Pacific is the fastest-growing region, with AI in population health management market size in the region projected to expand at 24.93% CAGR over 2026-2031. China is the clearest scale story inside that growth, because the 15th Five-Year Plan for 2026-2030 treats AI healthcare as a strategic priority, and domestic releases had reached nearly 300 medical large models by May 2025 while county-level remote imaging services had already handled more than 68 million cases. China’s NHSA also launched the Personal Medical Insurance Cloud pilot in February 2026 to build dynamic health profiles across the full care lifecycle for 1.33 billion insured people. The AI in population health management market is therefore likely to find some of its longest runway in Asia-Pacific, where public system modernization, chronic disease pressure, and national-scale data platforms can all support broader deployment over time.

Competitive Landscape

The AI in population health management market is moderately concentrated at the top, with Epic, Optum, Oracle Health, and Innovaccer holding strong visibility across software, analytics, and value-based care workflows. A second group that includes Health Catalyst, Arcadia, Cotiviti, Lightbeam, and ZeOmega continues to compete through narrower vertical focus, workflow depth, and interoperability strength. The field is not consolidated enough for one product architecture to dominate every buyer type, because provider workflows, payer priorities, and public health needs still differ in meaningful ways. That means the AI in population health management market rewards breadth, but only when that breadth is paired with usable workflow design and reliable data integration. Installed relationships also matter, since vendors with established EHR, care management, or payer analytics positions can extend into adjacent population health functions more easily than new entrants.

Mergers and acquisitions remain a defining competitive move in the AI in population health management market because buyers want fewer disconnected tools and broader operational coverage from a smaller vendor set. Cotiviti completed its acquisition of Edifecs in March 2025, which strengthened its interoperability position and gave it a wider base for data exchange and analytics workflows. Medisolv expanded further in 2026 by acquiring Lilac Software in March and Health Elements AI in April, using those deals to deepen value-based care analytics and AI-led clinical data abstraction. Medisolv said its Health Elements AI transaction extends population health analytics coverage to more than 140 million patient records across over 1,800 healthcare organizations, which shows how scale and workflow coverage are now being bought as much as built. These moves show that the AI in population health management market is shifting from point solutions toward fuller operating platforms that can connect measurement, quality action, and care management execution.

AI In Population Health Management Industry Leaders

athenahealth

Epic Systems

Lumeris, Inc.

Oracle Health, Inc.

Koninklijke Philips N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Rialtic and Exponential AI announced a strategic merger to create a unified platform covering the full claim lifecycle, including population-level prior authorization, real-time decision intelligence, and quality processes for both payer and provider markets. The deal accelerates payer-side AI in population health management workflows for US health plans.

- May 2026: IKS Health acquired ARAI Solutions, integrating proprietary biomedical knowledge graphs and a central reasoning engine into its full-stack AI platform to advance autonomous clinical coding, care gap identification, and precision medicine for population-level use cases.

- April 2026: Medisolv acquired Health Elements AI, adding AI-first clinical data abstraction with a reported 96% accuracy rate for clinical registry quality reporting, expanding Medisolv's population health analytics coverage to over 140 million patient records across more than 1,800 healthcare organizations.

Global AI In Population Health Management Market Report Scope

As per the scope of the report, AI in population health management refers to the application of artificial intelligence technologies to analyze health data across defined patient populations, enabling healthcare organizations to identify high-risk individuals, predict disease trends, and improve preventive care. AI-powered population health management platforms integrate clinical, claims, social, and behavioral data to support risk stratification, care coordination, resource optimization, and personalized interventions. These solutions help improve health outcomes while reducing healthcare costs and enhancing value-based care delivery.

The AI in population health management is segmented by component, deployment mode, application, end user, and geography. By component, the market is segmented into software and services. By deployment mode, the market is segmented into cloud-based, on-premises, and hybrid. By application, the market is segmented into population health analytics, patient engagement, risk stratification, care management & coordination, financial & network performance analytics, and others. By end user, the market is segmented into healthcare providers, healthcare payers, accountable care organizations, and others. The geography segment is further divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market size and forecasts in value (USD) for the above segments.

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Population Health Analytics |

| Patient Engagement |

| Risk Stratification |

| Care Management & Coordination |

| Financial & Network Performance Analytics |

| Others |

| Healthcare Providers |

| Healthcare Payers |

| Accountable Care Organizations |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By Application | Population Health Analytics | |

| Patient Engagement | ||

| Risk Stratification | ||

| Care Management & Coordination | ||

| Financial & Network Performance Analytics | ||

| Others | ||

| By End User | Healthcare Providers | |

| Healthcare Payers | ||

| Accountable Care Organizations | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving growth in AI in population health management?

Growth is being driven by value-based reimbursement, rising chronic disease burden, stronger risk stratification needs, and workforce pressure, with the market projected to grow from USD 16.76 billion in 2026 to USD 46.51 billion by 2031.

Which segment leads by component?

Software led with 72.48% share in 2025 because buyers are prioritizing durable analytics and workflow platforms over one-time service engagements.

Which application is growing the fastest?

Risk stratification is the fastest-growing application, with a projected 24.85% CAGR through 2031, as buyers move from retrospective reporting to real-time prioritization.

Why do payers matter more now in this space?

Healthcare payers are the fastest-growing end user at 23.92% CAGR because they are using AI for member engagement, utilization management, and risk-adjusted contract performance.

Which region is growing the fastest?

Asia-Pacific is the fastest-growing region at 24.93% CAGR, supported by large public data platforms, chronic disease pressure, and national AI healthcare programs.

What is the biggest challenge for adoption?

Unclear reimbursement and liability rules remain a major hurdle because many AI tools still sit inside payment structures that were not designed for software-based clinical and population-level services.

Page last updated on: