Healthcare Wearable Robots Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.62 Billion |

| Market Size (2031) | USD 5.94 Billion |

| Growth Rate (2026 - 2031) | 10.41% CAGR |

| Fastest Growing Market | North America |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Wearable Robots Market Analysis by Mordor Intelligence

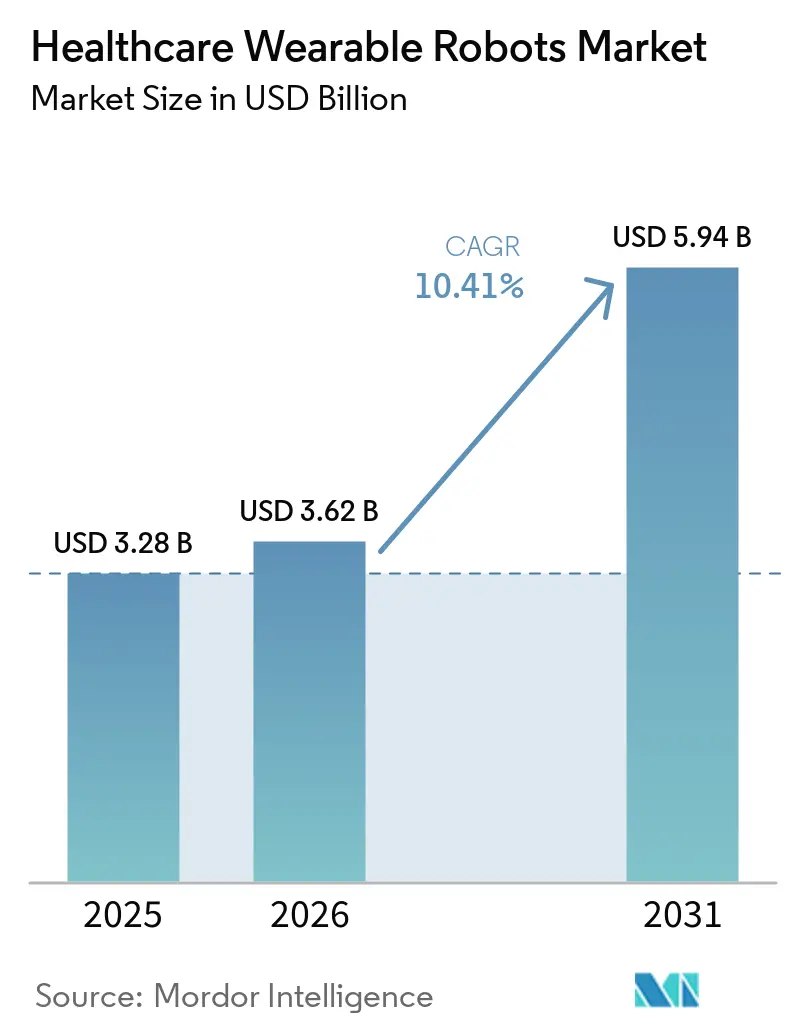

The Healthcare Wearable Robots Market size is projected to expand from USD 3.28 billion in 2025 and USD 3.62 billion in 2026 to USD 5.94 billion by 2031, registering a CAGR of 10.41% between 2026 to 2031.

Heightened reimbursement coverage in the United States, Japan, and Germany is reshaping demand more quickly than incremental hardware upgrades because payers now treat exoskeleton‐assisted therapy as a substitute for long-term institutional care [1]Centers for Medicare & Medicaid Services, “Medicare Coverage of Exoskeleton-Assisted Therapy,” cms.gov. FDA 510(k) clearances for three next-generation systems between 2024 and 2025 compressed the traditional 18- to 24-month regulatory lag to well under one year, accelerating time to revenue for new entrants. Soft-exosuit breakthroughs that cut donning time from 15 minutes to under 3 minutes are widening the addressable home-care segment and bringing first-mover advantage to vendors able to combine textile actuation, cloud telemetry, and low price points. On the demand side, global stroke incidence climbed to 12.2 million cases in 2024 and is projected to reach 15.3 million by 2030, while the 60-plus population will swell from 1.4 billion in 2024 to 2.1 billion by the end of the decade, creating a structural tailwind that decouples growth from short-term capital-spending cycles.

Key Report Takeaways

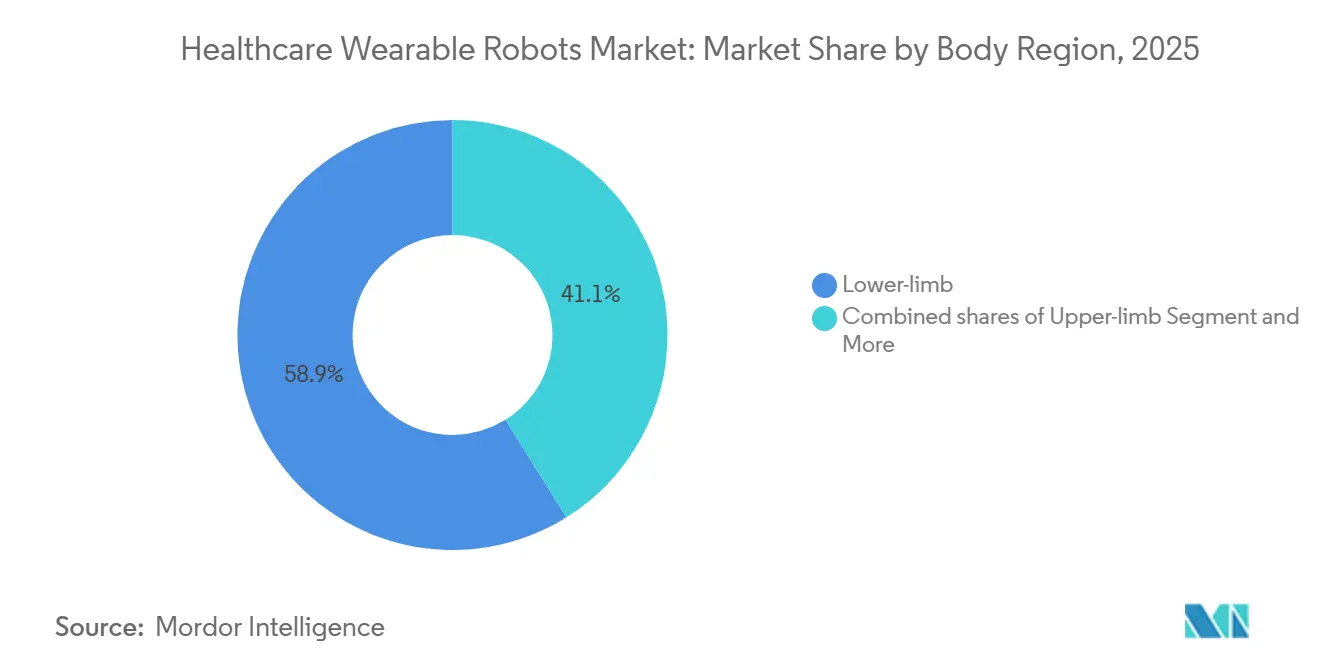

- By body region, lower-limb exoskeletons led with 58.9% of healthcare wearable robots market share in 2025, yet Upper-limb systems are projected to advance at a 10.96% CAGR through 2031.

- By frame type, rigid designs accounted for 58.96% of the healthcare wearable robots market size in 2025, yet soft exosuits are expanding at an 11.13% CAGR between 2026 and 2031, outpacing all other frame types.

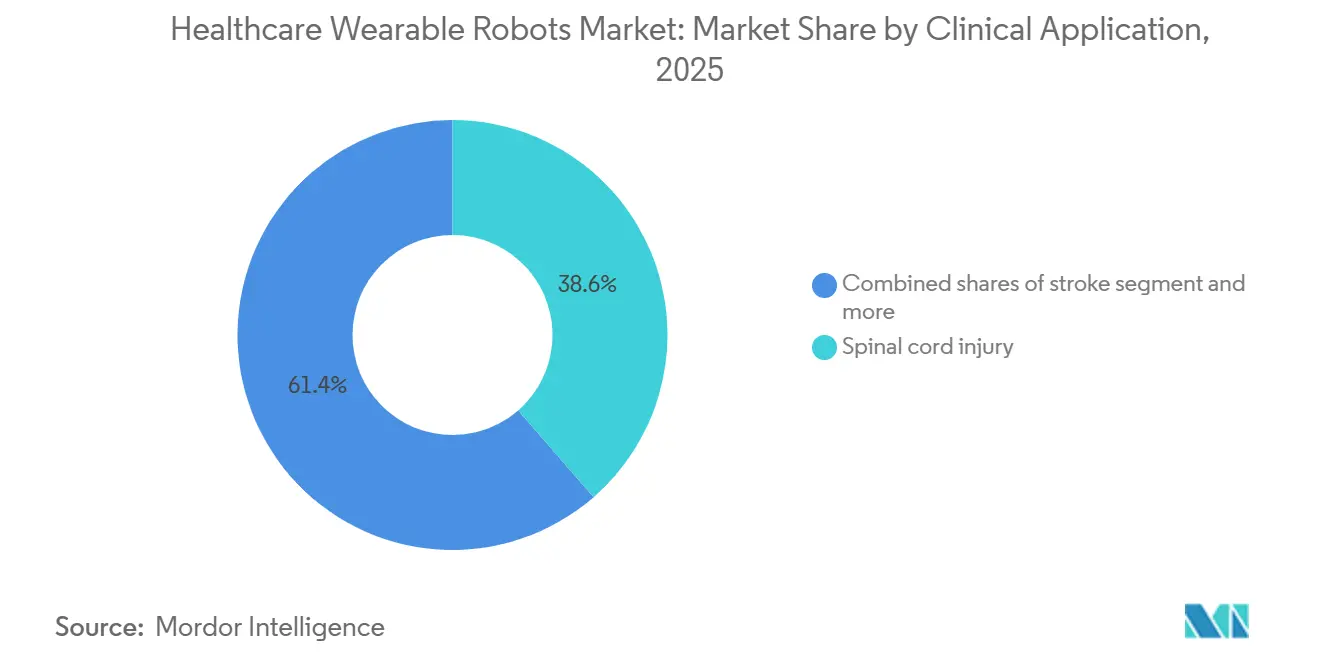

- By clinical application, spinal cord injury maintained 38.6% revenue share in 2025, while stroke rehabilitation is rising at a 10.87% CAGR to 2031.

- By end user, hospitals retained 43.12% share in 2025; home-care deployments are climbing at a 10.75% CAGR through 2031.

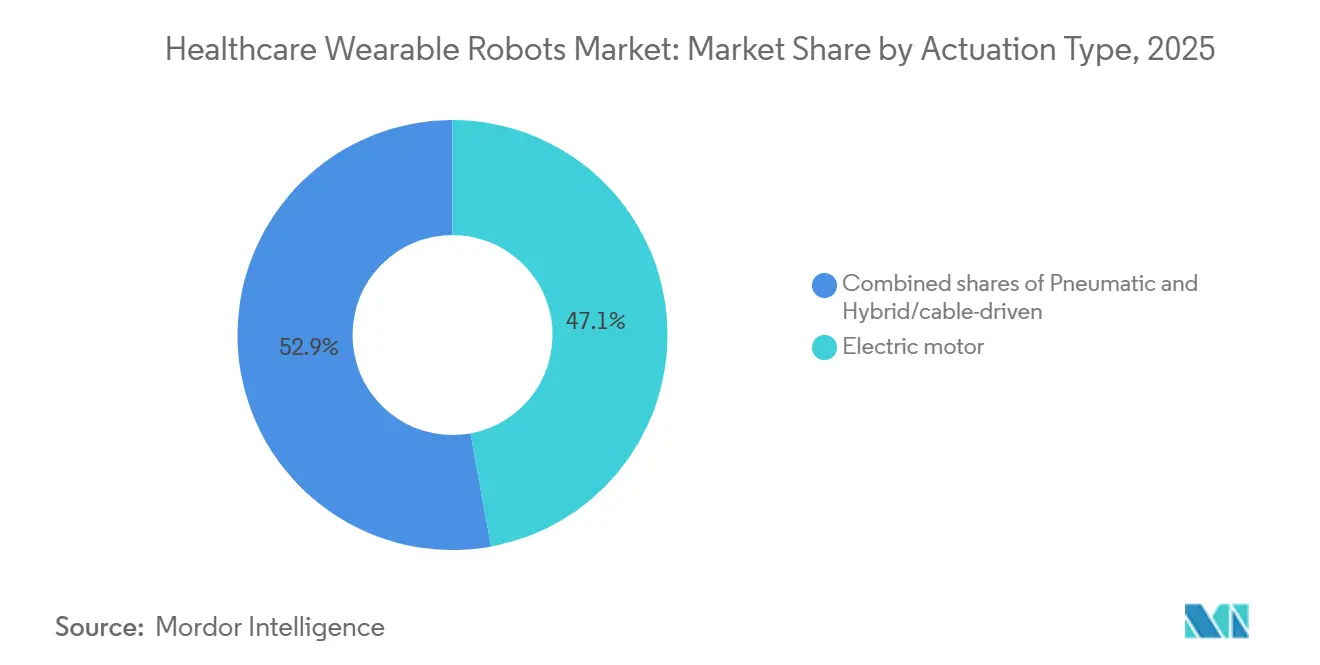

- By actuation, electric motors commanded 47.13% of the healthcare wearable robots market share in 2025 and are growing at a 10.83% CAGR, thanks to batteries reaching 250 Wh/kg energy density.

- By geography, North America accounted for 41.60% of 2025 revenue and is on track to expand at a 10.81% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Healthcare Wearable Robots Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging-related neuro-musculoskeletal impairment prevalence | +2.1% | Global; strongest in Japan, Europe, North America | Long term (≥ 4 years) |

| Expanding regulatory clearances and clinical indications | +1.8% | FDA, EU MDR, PMDA, NMPA markets | Medium term (2-4 years) |

| Strengthening clinical evidence for functional recovery & ADL gains | +1.6% | Global early adopters | Medium term (2-4 years) |

| Emerging reimbursement pathways and coverage pilots | +2.3% | United States, Japan, Germany | Short term (≤ 2 years) |

| Miniaturized soft exosuits enabling home use and continuous therapy | +1.5% | North America, Europe, Japan, urban APAC | Medium term (2-4 years) |

| Tele-rehab integration and outcomes-linked contracting | +1.2% | United States, U.K., Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging-Related Neuro-Musculoskeletal Impairment Prevalence

The World Health Organization recorded 1.71 billion people living with neuro-musculoskeletal disorders in 2024, a 12% rise since 2019. Japan subsidizes exoskeleton costs for elder-care facilities, spurring 400 CYBERDYNE HAL deployments by December 2024 [2]Ministry of Health, Labour and Welfare Japan, “Elder-Care Subsidy Program,” mhlw.go.jp. Germany followed suit in 2024 when statutory insurance began covering robotic gait therapy, driving Ottobock C-Brace orders up significantly year over year. Prevalence climbs non-linearly after age 75, concentrating demand in super-aged societies such as Japan, Italy, and Germany. Because U.S. skilled-nursing care costs USD 80,000–120,000 annually, a USD 100,000 exoskeleton has a 1.2-year payback, locking in long-run demand even if device prices soften.

Expanding Regulatory Clearances and Clinical Indications

The FDA granted 510(k) clearances to CYBERDYNE’s HAL small model, ReWalk 7, and Wandercraft’s Atalante X between May 2024 and October 2025, showing the agency’s growing comfort with exoskeleton safety profiles. CYBERDYNE’s May 2024 clearance added pediatric and rare-disease indications, expanding the treatable addressable population. CE-mark approvals after the tougher EU MDR rules prove that robust clinical files can still move through Europe in roughly 18 months [3]European Commission, “Medical Device Regulation,” eur-lex.europa.eu. China sliced its approval timeline to 18 months in 2024, allowing local vendors to win share across Asia before Western incumbents secure registration. Each successive approval supplies post-market data that shortens review cycles for follow-on submissions, reinforcing the positive loop.

Strengthening Clinical Evidence for Functional Recovery & ADL Gains

A 2024 meta-analysis of 18 RCTs with 1,240 participants found that exoskeleton therapy improved walking speed by 0.17 m/s and boosted Berg Balance scores by 6.56 points compared with manual physiotherapy. ReWalk demonstrated that the majority of spinal-cord-injury users achieved independent standing within 12 weeks, cutting the length of stay in rehabilitation by 7 days and saving USD 14,000 per admission. Ekso GT users finished inpatient rehab faster in a 2025 study, accelerating patient turnover for hospitals. Tele-rehab pilots at the U.S. Department of Veterans Affairs trimmed in-clinic visits, proving that cloud data streams can safeguard outcomes while easing staffing burdens. These findings help insurers write coverage policies that hinge on objective gait metrics rather than subjective quality-of-life surveys.

Emerging Reimbursement Pathways and Coverage Pilots

CMS reclassified powered exoskeletons as “braces” in January 2024, lifting Medicare coverage to 80% and finalizing a USD 91,032 lump-sum payment three months later. Ekso Bionics received its first Medicare reimbursement in August 2024, triggering a flood of claims from U.S. rehabilitation hospitals. UnitedHealthcare extended Medicare Advantage coverage to ReWalk 7 in November 2025; Aetna launched a 200-patient stroke pilot the following month. Japan’s national plan now finances the majority of HAL sessions, and Germany added robotic gait therapy to its benefits catalog in 2024, giving Europe a second major jurisdiction that reimburses after the United States. Because the majority of U.S. rehab hospitals cited “no payer coverage” as the primary adoption barrier in a 2024 APTA survey, these policies could deliver a step change in near-term unit volumes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High device, service, and training costs | −1.9% | Global; acute in India, Southeast Asia, Latin America | Short term (≤ 2 years) |

| Safety, supervision, and liability constraints in real-world use | −1.3% | North America, Europe, Japan | Medium term (2-4 years) |

| Lack of standardized outcomes hindering broad reimbursement | −0.8% | United States, Europe, emerging markets | Medium term (2-4 years) |

| Precision component supply constraints | −1.1% | Global bottle-necks in Japan, Taiwan, China | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Device, Service, and Training Costs

Exoskeleton price tags span USD 70,000–150,000, while annual service contracts add USD 8,000–12,000, pushing the five-year total cost of ownership to as much as USD 180,000. The majority of U.S. rehab hospitals flagged sticker shock as the top hurdle in a 2024 APTA poll, and 41% cited 40-hour therapist training requirements. Leasing eases capex pressure; CYBERDYNE’s 2024 pact with Mitsubishi UFJ Lease prices HAL access at JPY 150,000 (USD 1,000) per month, a model now mirrored by ReWalk and Wandercraft. In India, locally assembled devices sell for USD 30,000–50,000, yet adoption lags because out-of-pocket costs exceed average household income for the majority of candidates. Medicare’s 80% coverage erases most financial friction in the United States, but only 30% of European private insurers reimbursed exoskeleton therapy as of 2024, prolonging payback horizons.

Safety, Supervision, and Liability Constraints in Real-World Use

Liability insurers boosted premiums for U.S. clinics offering exoskeleton therapy after a handful of minor falls in 2024. FDA labeling still mandates therapist supervision for ReWalk 7 and Wandercraft Atalante X, limiting unsupervised home use. Japan’s caregiver shortfall—projected at 690,000 workers by 2025—reduces staff available for monitored sessions, prompting facilities to confine exoskeleton therapy to well-staffed morning shifts. EU MDR now requires annual real-world safety updates, adding roughly USD 500,000 in compliance expense for large installed bases. Early data suggest soft exosuits carry lower fall rates: Daiya’s six-month geriatric pilot logged zero adverse events among 100 users, implying textile frames may relax supervision rules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Body Region: Upper-Limb Gains Traction in Stroke Recovery

Lower-limb systems accounted for 58.9% of the healthcare wearable robots market share in 2025, owing to their entrenched use in spinal cord injury rehabilitation. The healthcare wearable robots market size for upper-limb devices is projected to expand at a 10.96% CAGR through 2031, as evidence mounts that robotic arm therapy increases Fugl-Meyer scores by 12 points in eight weeks. Trunk and full-body variants meet a separate need for postural stability for elderly users, and Honda placed 50 Walking Assist devices in Japanese care homes in 2024.

While lower-limb therapy delivers milestone gains up to community ambulation, upper-limb platforms continue adding value by tackling fine-motor recovery, extending the revenue window per patient. Pediatric indications opened by CYBERDYNE’s small HAL clearances enlarge the addressable base, especially for cerebral palsy. Hospitals now procure mixed portfolios to align device geometry with diagnosis, and vendors that master modular architectures can address multiple body regions without redesigning core electronics.

By Frame Type: Soft Exosuits Accelerate as Home Use Expands

Rigid architectures held 58.96% of 2025 revenue because their 40 Nm knee torque accommodates users with complete motor loss. However, the healthcare wearable robots market size for soft exosuits is tracking an 11.13% CAGR as pneumatic muscles and Bowden cables slash frame weight significantly and enable 8-hour wear periods.

Functionally, rigid frames remain the gold standard for inpatient SCI therapy, yet soft exosuits dominate home-care adoption where comfort and fast donning beat raw power. Ottobock’s hybrid Paexo proves the segments will blend: its 25 Nm output bridges the gap and drew 28% higher 2024 orders from European rehab centers. ISO 13482 certification is becoming a marketing prerequisite, and soft-exuit makers that clear the bar early will ride accelerated direct-to-consumer channels.

By Clinical Application: Stroke Rehabilitation Outpaces SCI

Spinal cord injury still represented 38.6% of the 2025 value, yet stroke-specific platforms are growing 10.87% annually on the back of expanding Medicare Advantage and private-payer pilots. The healthcare wearable robots market share advantage may flip by 2029 because the stroke population dwarfs annual SCI incidence 24-to-1.

Manufacturers are tailoring firmware for asymmetric gait patterns common in stroke, while MS and pediatric models sit in earlier commercialization stages, awaiting larger RCTs. Orthopedic post-surgical rehab shows white-space potential, with Mayo Clinic pilots proving three-day length-of-stay reductions that finance device leases inside a single quarter.

By End User: Home-Care Surges as Miniaturization Removes Supervision Barrier

Hospitals owned 43.12% of 2025 revenue because they absorb purchase costs and marshal trained staff. Yet the healthcare wearable robots market size allocated to home-care solutions is climbing at 10.75% annually, as VA pilots showed higher adherence with in-home ReWalk Personal units.

Rehab centers hold a significant share, serving as the bridge from acute care to the living room. Leasing and subscription models lower patient upfront spend, and remote-monitoring dashboards now integrate seamlessly with outpatient EMR systems, collapsing traditional site-of-service barriers.

By Actuation Type: Electric Motors Dominate as Battery Density Improves

Electric motors delivered 47.13% of the healthcare wearable robots market share in 2025, with lithium-polymer cells at 250 Wh/kg enabling 10-hour shifts without recharging. The electric motor is expected to grow with 10.83% CAGR through 2031,

Hybrid cable-driven architectures blend motor precision with remote actuation to save limb weight. Vendors that vertically integrate battery, motor, and controller lines shorten supply chains and secure margin headroom when raw-material prices spike.

Geography Analysis

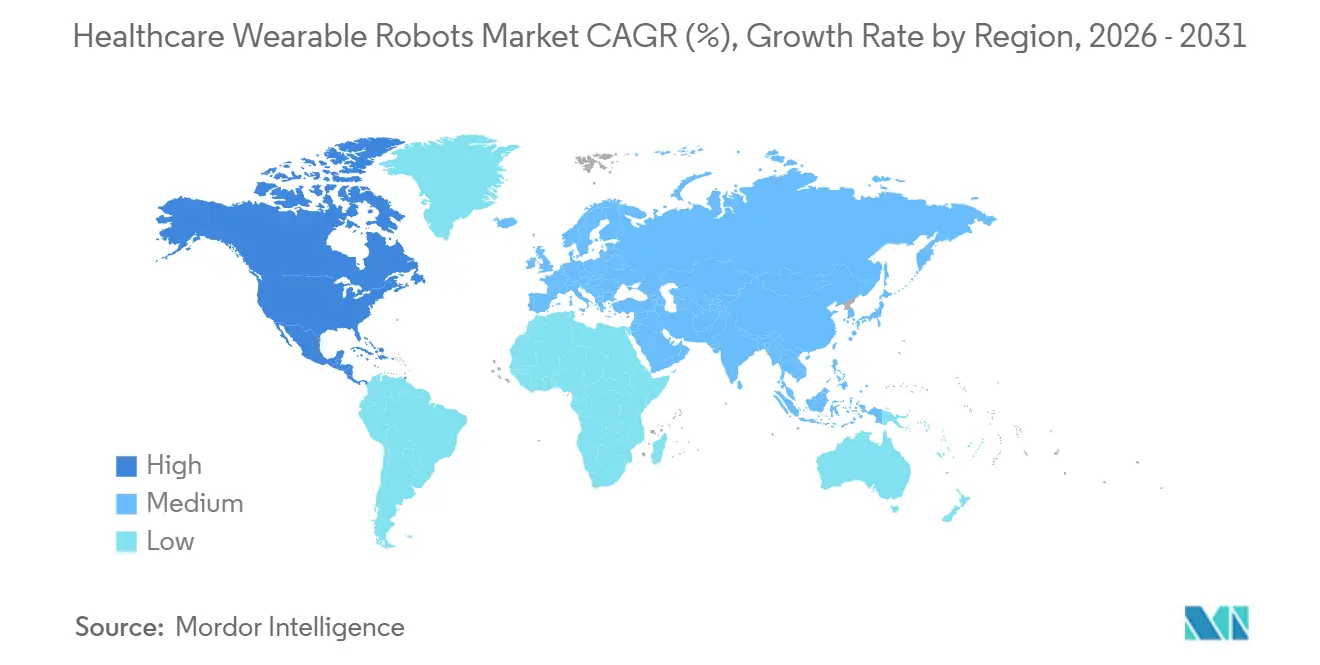

North America generated 41.6% of 2025 sales and is advancing at a 10.81% CAGR because CMS’s lump-sum payment slashed out-of-pocket costs from USD 100,000 to roughly USD 20,000 for Medicare beneficiaries. The Veterans Affairs program placed 500 units for home therapy in 2024, and 340 U.S. hospitals now offer robotic gait services, up from 200 in 2022. Canada and Mexico launched provincial and federal pilots in 2024-2025, signaling continent-wide momentum for reimbursement.

Europe held a significant share of 2025 revenue and is rising at a notable CAGR despite heterogeneous payer policies. Germany’s 2024 green light for robotic gait therapy lifted Ottobock orders significantly, while CYBERDYNE and ReWalk both navigated the stricter EU MDR to secure CE marks. U.K. tele-rehab pilots achieved better completion rates, but the lack of French reimbursement and fragmented Southern European funding are restraining broader penetration.

Asia-Pacific is expected to register significant growth over the forecasted period. Japan’s super-aged demographics and subsidy scheme drove 400 HAL installs by late 2024. China cut approval times in half and backed local manufacturing with a USD 2 billion fund, allowing Angel Robotics and Fourier Intelligence to notably undercut Western pricing. Australia’s NDIS and South Korea’s stroke pilots widen Oceania access, while India remains price-constrained until a national payer plan materializes.

The Middle East & Africa and South America accounted for a modest share of 2025 consumption and posted notable growth. The UAE and South Africa launched limited pilots, but widespread uptake hinges on private insurance participation and philanthropic grants, as public budgets remain focused on primary care.

Competitive Landscape

Moderate concentration defines the healthcare wearable robots market: the top five suppliers command the majority of global revenue. Lifeward’s ReWalk 7 won both FDA and CE clearances in 2025, adding cloud analytics that strengthen pay-for-performance contracts. Ekso Bionics’ Parker Hannifin alliance shortens custom-actuator lead times to four weeks, a defensible edge amid supply-chain volatility.

Fourier Intelligence amassed USD 100 million in Series C funding in March 2024 and shipped 2,000 units, leveraging China’s cost base to price significantly below Western incumbents. CYBERDYNE’s leasing pact with Mitsubishi UFJ Lease democratizes access for smaller Japanese clinics at USD 1,000 per month. Wandercraft cut U.S. delivery cycles from six months to eight weeks by opening a domestic factory, a decisive factor for hospitals with annual budgeting windows.

Technology moats are coalescing around battery life, sub-3-minute donning, AI-driven gait prediction, and tele-rehab dashboards. Chinese new entrants with vertically integrated component lines threaten a price war that could compress gross margins 5-10 points unless incumbents double down on reimbursable clinical evidence and premium service bundles.

Healthcare Wearable Robots Industry Leaders

Lifeward Ltd

Ekso Bionics Holdings, Inc.

Fourier Intelligence Co., Ltd.

Cyberdyne Inc.

Wandercraft SAS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: At the Hannover Messe trade fair, 'SUITX by Ottobock' showcased its enhanced business unit. Alongside its exoskeleton portfolio, it provides scalable digital ergonomics solutions integrating hardware, sensors, and AI-driven analyses.

- December 2025: German Bionic expanded its Exia line with vest designs tailored for female anatomy, improving long-term wearability.

- March 2025: Lifeward gained FDA clearance for ReWalk 7 featuring real-time cloud telemetry

Global Healthcare Wearable Robots Market Report Scope

As per the scope of the report, healthcare wearable robots are advanced assistive devices designed to be worn on the body to enhance, supplement, or replace limb motor functions that have been affected by aging, injury, or neurological conditions like stroke and ALS.

The healthcare wearable robots’ market is segmented by body region, frame type, clinical applications, end users, actuation type, and geography. By body region, the market is segmented into lower-limb, upper-limb, and trunk/full-body. By frame type, the market is segmented into rigid exoskeletons and soft exosuits. By clinical applications, the market is segmented into stroke, spinal cord injury, multiple sclerosis, cerebral palsy & pediatrics, orthopedic & post-surgical rehab, and elderly mobility assistance. By end users, the market is segmented into hospitals, rehabilitation centers, and home care. By actuation type, the market is segmented into electric motor, pneumatic, and hybrid/cable-driven.

Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Lower-limb |

| Upper-limb |

| Trunk/Full-body |

| Rigid exoskeletons |

| Soft exosuits |

| Stroke |

| Spinal cord injury |

| Multiple sclerosis |

| Cerebral palsy & pediatrics |

| Orthopedic & post-surgical rehab |

| Elderly mobility assistance |

| Hospitals |

| Rehabilitation centers |

| Homecare |

| Electric motor |

| Pneumatic |

| Hybrid/cable-driven |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Body Region | Lower-limb | |

| Upper-limb | ||

| Trunk/Full-body | ||

| By Frame Type | Rigid exoskeletons | |

| Soft exosuits | ||

| By Clinical Application | Stroke | |

| Spinal cord injury | ||

| Multiple sclerosis | ||

| Cerebral palsy & pediatrics | ||

| Orthopedic & post-surgical rehab | ||

| Elderly mobility assistance | ||

| By End User | Hospitals | |

| Rehabilitation centers | ||

| Homecare | ||

| By Actuation Type | Electric motor | |

| Pneumatic | ||

| Hybrid/cable-driven | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the healthcare wearable robots market expected to grow through 2031?

The sector is projected to advance at a 10.41% CAGR from 2026 to 2031 on the back of expanding reimbursement and demographic pressure

Which region currently leads in exoskeleton revenue?

North America accounts for 41.6% of global sales due to Medicare’s lump-sum payment and 340 U.S. hospital deployments.

What will be the market size of Healthcare Wearable Robots Market in 2031?

Stroke rehabilitation devices are rising at a 10.87% CAGR as private insurers begin to reimburse robotic gait training.

Are soft exosuits replacing rigid frames?

The Healthcare Wearable Robots Market size is projected to expand from USD 3.28 billion in 2025 and USD 3.62 billion in 2026 to USD 5.94 billion by 2031, registering a CAGR of 10.41% between 2026 to 2031.

How much can a hospital expect to pay for a single exoskeleton?

List prices range USD 70,000–150,000, with annual service contracts adding USD 8,000–12,000 over a five-year lifespan.

Page last updated on: