AI In Respiratory Monitoring Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.21 Billion |

| Market Size (2031) | USD 2.39 Billion |

| Growth Rate (2026 - 2031) | 14.52% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Respiratory Monitoring Market Analysis by Mordor Intelligence

The AI in respiratory monitoring market is expected to grow from USD 1.08 billion in 2025 to USD 1.21 billion in 2026 and is forecasted to reach USD 2.39 billion by 2031 at 14.52% CAGR over 2026-2031. The AI in respiratory monitoring market is expanding as care delivery shifts from episodic assessment toward continuous monitoring across hospital and home settings. Reimbursement support is strengthening that shift, especially after CMS reduced the respiratory remote therapeutic monitoring transmission threshold to 2 days per 30-day period from January 2026, which improves the billing case for continuous home programs. The AI in respiratory monitoring market is also benefiting from hospital pressure to automate respiratory workflows as allied health staffing gaps remain persistent across many care settings. OECD work published in May 2025 also supports the view that AI-augmented workflows can expand the effective supervisory capacity of respiratory teams, which supports durable institutional demand beyond consumer device cycles. At the same time, the AI in respiratory monitoring market is becoming more selective, because procurement now depends not only on algorithm performance but also on validation depth, interoperability, and post-market governance readiness.

Key Report Takeaways

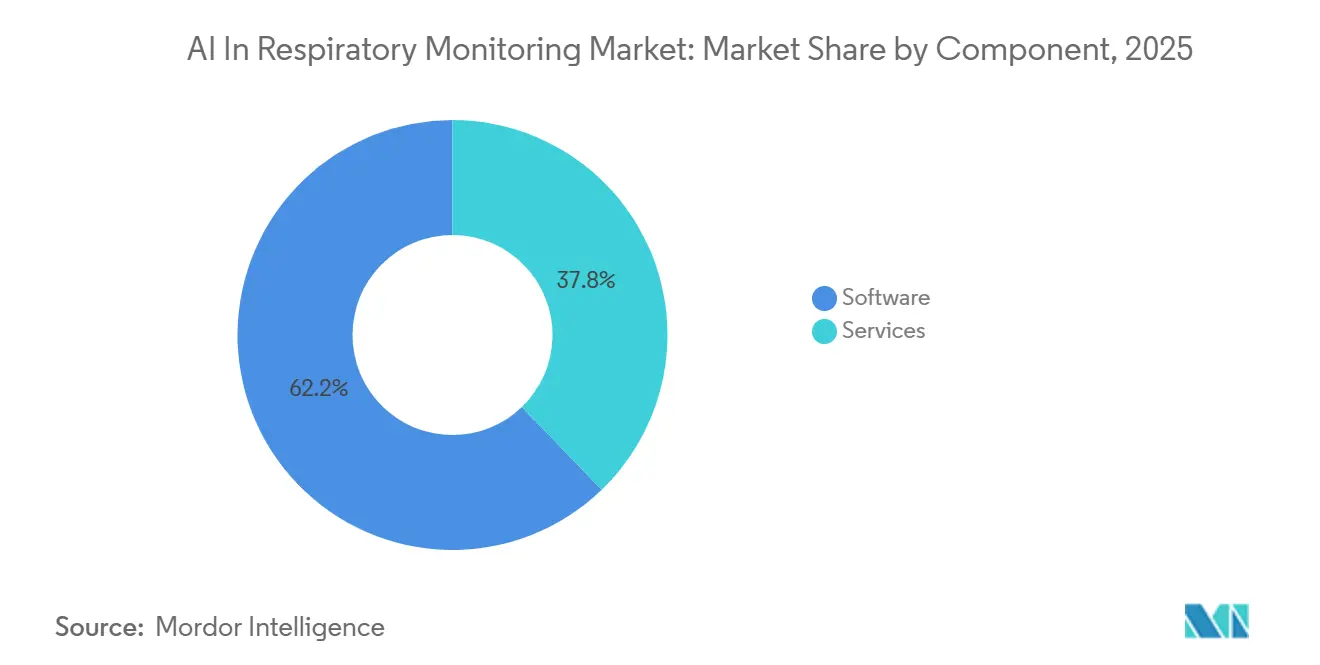

- By component, software held 62.24% revenue share in 2025, while software is projected to have a CAGR at 15.75% through 2031.

- By device type, wearable respiratory monitoring devices commanded 57.63% of the AI in respiratory monitoring market size in 2025, while ventilation and critical care monitoring systems are expected to expand at a 16.90% CAGR through 2031.

- By technology, machine learning and predictive analytics accounted for 53.74% revenue share in 2025, while edge AI and real-time processing are projected to grow at a 15.85% CAGR through 2031.

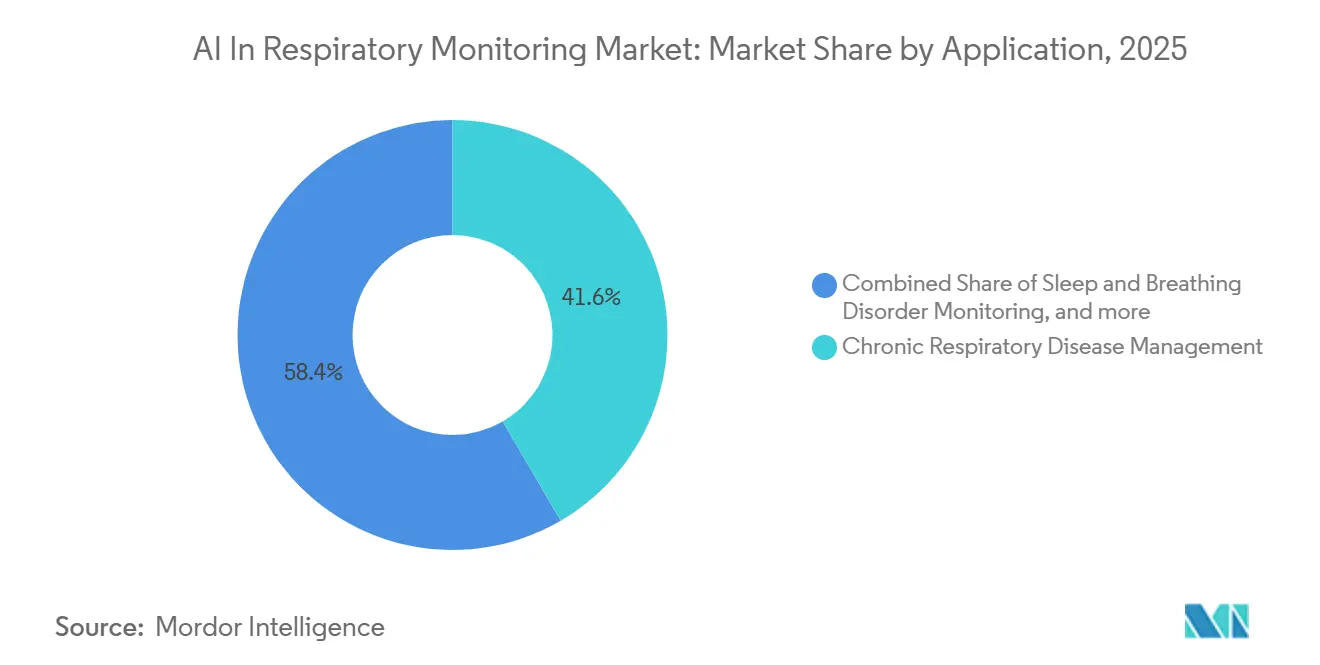

- By application, chronic respiratory disease management captured 41.56% of the AI in respiratory monitoring market size in 2025, while post-acute and home respiratory care is expected to advance at a 16.50% CAGR through 2031.

- By end-user, hospitals and clinics held 43.41% revenue share in 2025, while home care settings posted the fastest projected CAGR at 16.05% through 2031.

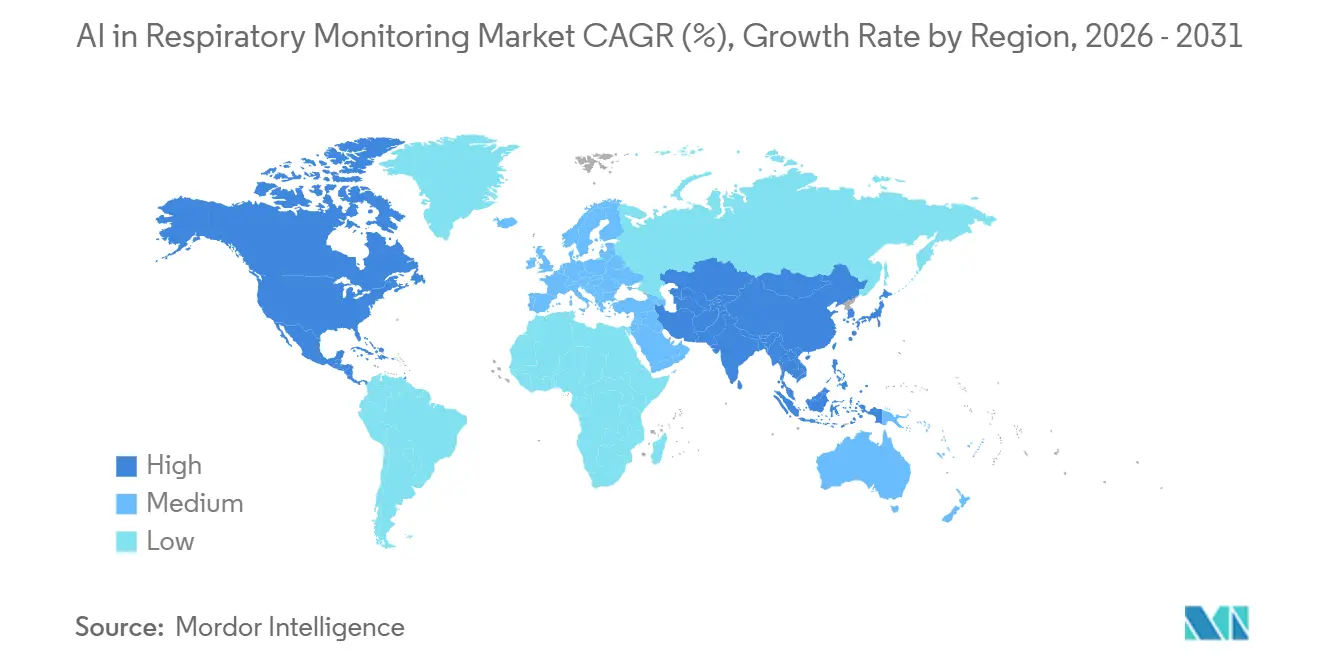

- By geography, North America held 44.37% of the AI in respiratory monitoring market share in 2025, while Asia-Pacific recorded the highest projected CAGR at 17.44% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Respiratory Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Adoption of AI-Enabled Respiratory Wearables | +2.8% | Global, with concentration in North America and Western Europe | Short term (≤ 2 years) |

| Integration of Predictive Analytics into Critical-Care Ventilators | +2.3% | Global, early gains in North America, Germany, and Japan | Medium term (2-4 years) |

| Remote Patient-Monitoring Reimbursement Expansion | +2.0% | North America primary, EU spillover via DiGA and national RPM pilots | Short term (≤ 2 years) |

| Hospital Demand for Workflow Automation to Mitigate Respiratory Therapist Shortages | +1.8% | North America, Australia, and the UK | Medium term (2-4 years) |

| Miniaturization of MEMS Sensors Enabling Continuous At-Home Monitoring | +1.5% | Global, manufacturing scale in East Asia, adoption in North America and APAC | Long term (≥ 4 years) |

| Real-Time Multimodal Data Fusion for Early COPD Exacerbation Alerts | +1.7% | Global, clinical deployment concentrated in North America, the EU, and China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Adoption of AI-Enabled Respiratory Wearables

The AI in respiratory monitoring market is gaining momentum from wearable devices that are moving into regulated and billable care pathways. In August 2025, Respiree received a second FDA 510(k) clearance that expanded its RS001 chest-worn cardiorespiratory wearable from inpatient use into home settings through the connected 1Bio platform.[1]Respiree, “Respiree Secures Second FDA 510(k) Clearance, Expands Cardio-Respiratory Wearable to Home Use via 1Bio Connected Care Platform,” Respiree via BioSpace, biospace.comThat clearance matters because it shows regulatory comfort with continuous wireless streaming outside the hospital, which supports wider use in post-acute respiratory programs. The AI in respiratory monitoring market is also seeing stronger demand for patch and chest-worn formats that reduce friction for longer monitoring periods. This shifts value toward vendors that pair wearables with clinical dashboards, alert logic, and data continuity rather than relying on device sales alone. It also raises the pace of product iteration, because once wearables enter clinical workflows, accuracy, comfort, battery life, and reimbursement fit start to matter at the same time.

Integration of Predictive Analytics into Critical-Care Ventilators

The AI in respiratory monitoring market is also being lifted by predictive analytics that are moving ventilators from alarm response toward active therapy optimization. A prospective real-world evidence study tied to the automated ventilation software package was also listed with a January 2026 update, which shows that validation work is continuing in routine ICU settings.[2]ClinicalTrials.gov Registry, “Comparison of the Prevalence of Asynchronies During Mechanical Ventilation with Manual Versus Automatic Adjustment Using the INTELLISYNC+ Tool, NCT06655805,” ICH GCP, ichgcp.net The practical effect is staffing leverage, because more automation can help one intensivist and a limited respiratory team oversee a larger patient load without lowering surveillance intensity. The AI in respiratory monitoring market therefore benefits not only from clinical utility, but also from workforce economics inside acute care hospitals. Vendors with larger proprietary patient datasets are better positioned here, because procurement committees increasingly want evidence from real-world use rather than only lab performance.

Remote Patient-Monitoring Reimbursement Expansion

The AI in respiratory monitoring market is getting a direct demand boost from reimbursement reform in respiratory remote monitoring. CMS finalized new remote therapeutic monitoring codes for 2026 that allow respiratory device data to be billed with only 2 days of transmission during a 30-day period, which sharply lowers the economic barrier for enrolling patients who do not transmit data consistently every month.[3]Centers for Medicare & Medicaid Services, “Calendar Year (CY) 2026 Medicare Physician Fee Schedule Final Rule (CMS-1832-F),” Centers for Medicare & Medicaid Services, cms.govThat change makes home monitoring programs more commercially viable for COPD, asthma, and sleep-related respiratory care. It also tilts competition toward software-first vendors, because recurring reimbursement now depends on continuous data flow, documentation, and clinician workflow support. The AI in respiratory monitoring market gains from that structural shift because cloud-linked platforms can capture more value than hardware-only offerings. As this model matures, payers and providers are likely to favor solutions that combine physiological monitoring, engagement prompts, and billing-ready reporting in one platform.

Hospital Demand for Workflow Automation to Mitigate Respiratory Therapist Shortages

The AI in respiratory monitoring market is also supported by hospital demand for workflow automation as respiratory staffing remains tight. The American Hospital Association's 2026 workforce scan described persistent allied-health shortages and showed that many health system leaders are adding virtual care and AI-oriented roles to offset bedside pressure. OECD analysis published in May 2025 also noted that AI augmentation can raise the effective supervisory span of health occupations, including respiratory functions, by improving task support and prioritization. That creates a durable procurement pull even when consumer demand weakens, because hospitals are buying labor efficiency as much as monitoring capability. The AI in respiratory monitoring market is therefore increasingly sold on staffing relief, workflow integration, and escalation management instead of only diagnostic accuracy. This favors vendors that can fit alerts into existing clinical systems and reduce manual review burden for overextended care teams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Annotated Datasets for Rare Respiratory Disorders | -1.5% | Global, most acute in developing markets with limited digital health infrastructure | Long term (≥ 4 years) |

| Cyber-Security and HIPAA Concerns Streaming Physiological Data | -1.2% | North America primary, EU secondary, global relevance for IoMT-connected devices | Short term (≤ 2 years) |

| Clinician Skepticism Toward Black Box AI Algorithms | -1.0% | Global, concentrated in academic medical centers and EU markets with high regulatory scrutiny | Medium term (2-4 years) |

| High Integration Costs in Legacy Hospital IT Stacks | -0.8% | Global, most significant in South America, MEA, and Tier 2 and Tier 3 cities in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Annotated Datasets for Rare Respiratory Disorders

The AI in respiratory monitoring market still faces a real data ceiling in rare respiratory disorders where labeled cases remain limited. A 2025 systematic review in Frontiers in Digital Health found strong performance for several AI and machine learning approaches in COPD exacerbation and readmission prediction, but it also noted persistent limits in generalizability when external validation datasets were missing[4]Frontiers Editorial Office, “AI/ML Driven Prediction of COPD Exacerbations and Readmissions, A Systematic Review and Meta-Analysis,” Frontiers in Digital Health, frontiersin.org. This is a structural issue because rarer disorders generate the least training data while often needing the most proactive monitoring. The AI in respiratory monitoring market therefore remains skewed toward common and well-reimbursed conditions such as COPD, OSA, and acute respiratory deterioration. Until multi-institution annotation pipelines improve, niche respiratory applications will continue to face slower adoption and tougher scrutiny from hospital buyers.

Cyber-Security and HIPAA Concerns Streaming Physiological Data

The AI in respiratory monitoring market also faces friction from the security demands attached to continuous physiological data streaming. As respiratory devices become more connected, hospitals increasingly treat cybersecurity as a patient safety and procurement issue rather than only an IT item. That changes the cost structure for vendors, because secure firmware design, device authentication, encryption, and post-market monitoring now have to be built into the product lifecycle from the start. The AI in respiratory monitoring market is especially exposed here because respiratory monitoring often depends on always-on data transfer across home networks, mobile gateways, and hospital systems. Smaller companies can find that burden difficult to absorb when they are also funding validation studies and regulatory submissions. This raises the competitive threshold and gives larger vendors with deeper compliance teams a clearer path to enterprise contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Economics Reshape Market Value Distribution

Software held 62.24% of the AI in respiratory monitoring market share in 2025, and it is also anticipated as the fastest-growing component with a 15.75% CAGR through 2031. The AI in respiratory monitoring market is showing clear value concentration in software because recurring licensing, cloud analytics, and algorithm updates scale more efficiently than physical devices. This dynamic makes revenue streams less dependent on shipment volumes and more dependent on data continuity, model refresh cycles, and clinical workflow adoption. Services remain important, but they mostly support installation, integration, training, and optimization rather than acting as the primary revenue driver. The segment structure therefore reflects how respiratory AI monetizes intelligence layers more effectively than hardware layers.

The AI in respiratory monitoring market also shows that software strength is tied to platform lock-in, not only to innovation speed. Hospitals that already calibrated one vendor's respiratory algorithms against their own patient mix face operational and financial friction when switching platforms. Within the AI in respiratory monitoring industry, this creates a moat for incumbents that can prove reimbursable outcomes such as event prevention and lower readmissions. The result is a software segment where retention economics matter almost as much as technical capability.

By Device Type: Wearables Lead but Critical Care Accelerates

Wearable respiratory monitoring devices held 57.63% of revenue in 2025, while ventilation and critical care monitoring systems are projected to grow at a 16.90% CAGR through 2031. The AI in respiratory monitoring market is seeing wearables lead today because more patients with COPD, OSA, and post-acute respiratory needs are being managed outside hospitals. Smaller, less obtrusive form factors also make longer observation windows easier in both home and ambulatory settings. At the same time, the fastest growth is shifting toward ventilator-linked intelligence where AI software improves weaning support, alarm interpretation, and patient-ventilator synchronization. That growth is being driven by clinical intensity and software upgrade value rather than by unit volume alone.

Devices that transmit respiratory waveforms into analytical platforms carry more strategic value than standalone sensors that only record measurements. Within the AI in respiratory monitoring industry, that trend favors platform vendors that can convert raw waveforms into actionable clinical outputs across many patients at once. It is likely to compress margins for hardware-only manufacturers that do not control analytics, connectivity, or clinical reporting.

By Technology: Machine Learning Leads, Edge AI Accelerates Fastest

Machine learning and predictive analytics accounted for 53.74% of technology revenue in 2025, while edge AI and real-time processing is expected to expand at a 15.85% CAGR through 2031. The AI in respiratory monitoring market still relies most heavily on machine learning because it is already established in COPD exacerbation prediction, ventilator support logic, and sleep-related respiratory screening. A 2025 systematic review in Frontiers in Digital Health found that ensemble and gradient-boosting approaches delivered strong performance in COPD-related prediction tasks, which supports their current leadership in deployment. This installed base gives machine learning a practical advantage, because providers are more comfortable adopting methods with broader validation histories. It also keeps predictive analytics at the center of mainstream respiratory AI procurement.

The AI in respiratory monitoring market is now seeing faster momentum in edge AI because latency, privacy, and connectivity limits are becoming harder to ignore. The AI in respiratory monitoring market therefore stands to benefit as inference moves closer to the patient and reduces dependence on constant cloud access. Deep learning and computer vision still matter, especially in waveform analysis and thoracic imaging, but edge deployment is where technical capability and real-world usability are now converging most visibly.

By Application: Chronic Disease Management Dominates, Home Care Leads Growth

Chronic respiratory disease management held 41.56% of application revenue in 2025, while post-acute and home respiratory care is projected to grow at a 16.50% CAGR through 2031. The AI in respiratory monitoring market is anchored by chronic disease programs because COPD and other long-duration respiratory conditions create recurring need for monitoring, escalation, and adherence support. This segment has a stronger economic case when algorithms can identify deteriorations early and reduce expensive hospital events. Home respiratory care, however, is expanding faster because reimbursement rules, patient preference, and care decentralization now support longer monitoring outside clinical facilities.

The AI in respiratory monitoring market also reveals a tension between clinical and consumer expectations in home care. Within the AI in respiratory monitoring industry, vendors that can turn home data into intervention-ready outputs are in a stronger position than those selling connected hardware alone. Sleep and breathing disorder monitoring remains important, but the highest strategic momentum is moving toward post-acute follow-up and home-centered respiratory management. This is where continuous monitoring, predictive alerts, and payer alignment increasingly meet in the same care pathway.

By End-User: Hospitals Lead, Home Care Settings Gain Ground

Hospitals and clinics captured 43.41% of end-user revenue in 2025, while home care settings are projected to expand at a 16.05% CAGR through 2031. The AI in respiratory monitoring market still draws most of its revenue from hospitals because acute-care volumes, enterprise procurement budgets, and certified clinical workflows remain concentrated there. Hospitals also demand structured interoperability with existing EHR environments, which raises the entry bar for smaller vendors. That requirement favors platforms that can fit into established alert, documentation, and escalation processes without adding new workflow burden. The hospital segment therefore remains the main commercial anchor even as the care setting mix broadens.

The AI in respiratory monitoring market is nevertheless shifting meaningful growth toward home care and distributed provider settings. Long-term care and home healthcare providers have a strong business case for autonomous monitoring because on-site specialist coverage is limited and response speed matters. The AI in respiratory monitoring market is likely to see these end users become more connected over time, with hospitals acting as escalation hubs and home care providers acting as continuous data generators. As that transition develops, vendors that can support both enterprise acute care and lower-touch distributed care models will have a broader path to scale.

Geography Analysis

North America held 44.37% of the AI in respiratory monitoring market share in 2025, which makes it the largest regional revenue base. The AI in respiratory monitoring market is strongest in this region because reimbursement infrastructure, digital workflow maturity, and clinical validation activity are deeper than in other geographies. CMS reinforced that position through the 2026 physician fee schedule updates that lowered the respiratory remote therapeutic monitoring billing threshold to 2 days of transmitted data within a 30-day period. That policy makes home respiratory monitoring more commercially viable and strengthens the software and services layers that sit around connected devices.

Europe remains the second-largest geography in the AI in respiratory monitoring market, with Germany and the UK acting as the main anchor countries. Germany is particularly important because reimbursement routes for digital health applications create a clearer path for software-led respiratory monitoring adoption. The region also benefits from strong hospital engineering standards and established critical care device ecosystems. At the same time, the AI in respiratory monitoring market faces a more demanding compliance path in Europe for clinical AI tools, which raises the burden on validation and documentation for new entrants.

Asia-Pacific is projected to be the fastest-growing geography at a 17.41% CAGR through 2031, which reflects the strongest expansion profile in the AI in respiratory monitoring market. Growth is being driven by China's push toward domestic AI medical devices, Japan's aging population, and India's expanding digital health infrastructure. The region is also benefiting from manufacturing depth in sensors and connected devices, which supports broader rollout of wearable and home-based respiratory systems. This makes Asia-Pacific important not only as a sales region but also as a supply and innovation base. South America and the Middle East and Africa remain smaller in current revenue terms, yet adoption is building in metropolitan tertiary-care centers and digitally advancing health systems.

Competitive Landscape

The AI in respiratory monitoring market shows moderate concentration at the platform level, while remaining fragmented across algorithms, device categories, and care settings. ResMed, Koninklijke Philips, Masimo, GE Healthcare, and Drägerwerk are the clearest large-scale participants. The AI in respiratory monitoring market therefore combines recognizable leaders with a long tail of specialized vendors focused on sleep analysis, imaging, home monitoring, or wearable sensing. That structure keeps competitive pressure active, especially in software layers where differentiation depends on data depth and workflow fit rather than hardware alone.

Strategy in the AI in respiratory monitoring market now centers on 3 recurring themes. The first is dataset-driven validation, because vendors need clinical evidence that supports regulatory review and procurement approval. The second is platform integration, because hospital buyers prefer solutions that fit into existing monitoring and documentation systems. The third is expansion into fast-growth regions and home-centered workflows where greenfield adoption is easier than hospital displacement.

The AI in respiratory monitoring market also has a clear white space between consumer respiratory awareness tools and clinical-grade monitoring systems. Vendors that can bridge wearable data, validated respiratory algorithms, and physician-ready reporting are better positioned than those competing only on sensor form factor. Smaller companies can still win when they move faster in evidence building or focus on under-served niches with strong workflow pain points. The AI in respiratory monitoring market will likely remain moderately concentrated in the near term, because scale helps with compliance, validation, and cybersecurity, but fragmentation will persist where new use cases and specialized algorithms continue to emerge.

AI In Respiratory Monitoring Industry Leaders

Koninklijke Philips N.V.

Medtronic plc

ResMed Inc.

Masimo Corporation

GE Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: China-listed Kefu Medical held a ceremonial rollout of its 10,000th AI respirator C11 at its Changsha facility. The C11, which incorporates an end-cloud collaborative AI architecture and has been recognized by Hunan Province's Ministry of Industry and IT as an official AI terminal product, sold over CNY 1 million in its first 12 hours on JD Health—marking the first credible domestic Chinese challenge to Western premium home-respiratory incumbents.

- March 2026: Lunit Featured in 21 AI Imaging Studies at ECR 2026. Lunit's AI respiratory imaging platform was featured in 21 independent clinical studies at the European Congress of Radiology in Vienna, including research on lung nodule detection version-to-version evaluation in a multicentre study. Thirteen of the 21 studies were selected for oral presentation in the congress's main scientific sessions, providing peer-reviewed validation depth that accelerates EU hospital procurement decisions.

- March 2026: JD Health and Kefu Medical formalized a deep strategic alliance leveraging JD Health's medical AI large model and supply chain capabilities combined with Kefu's respiratory device portfolio, targeting 150% year-over-year sales growth across respiratory oxygen therapy and health monitoring product lines.

Global AI In Respiratory Monitoring Market Report Scope

According to the report’s scope, AI in respiratory monitoring market refers to the use of artificial intelligence technologies to analyze respiratory health data collected from monitoring devices, wearables, ventilators, and connected healthcare systems. These solutions help detect respiratory abnormalities, predict disease progression, enable real-time patient monitoring, and support clinical decision-making for respiratory disorders.

The AI in respiratory monitoring market is segmented into component, device type, technology, application, end-user, and geography. By component, the market is segmented into software and services. By device type, the market is segmented into wearable respiratory monitoring devices, ventilation and critical care monitoring systems, non-invasive monitoring devices, sleep and breathing disorder monitoring devices, and respiratory imaging and advanced diagnostics systems. By technology, the market is segmented into machine learning and predictive analytics, deep learning, computer vision (imaging and waveform analysis), edge AI and real-time processing. By application, the market is segmented into chronic respiratory disease management, sleep and breathing disorder monitoring, critical care and acute respiratory monitoring, fitness and wellness monitoring, and post-acute and home respiratory care. By end-user, the market is segmented into hospitals and clinics, home-care settings, long-term care and home healthcare providers, diagnostic laboratories, and other end-users. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Software |

| Services |

| Wearable Respiratory Monitoring Devices |

| Ventilation and Critical Care Monitoring Systems |

| Non-Invasive Monitoring Devices |

| Sleep and Breathing Disorder Monitoring Devices |

| Respiratory Imaging and Advanced Diagnostics Systems |

| Machine Learning and Predictive Analytics |

| Deep Learning |

| Computer Vision (Imaging and waveform analysis) |

| Edge AI and Real-Time Processing |

| Chronic Respiratory Disease Management |

| Sleep and Breathing Disorder Monitoring |

| Critical Care and Acute Respiratory Monitoring |

| Fitness and Wellness Monitoring |

| Post-Acute and Home Respiratory Care |

| Hospitals and Clinics |

| Home-Care Settings |

| Long-Term Care and Home Healthcare Providers |

| Diagnostic Laboratories |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| By Device Type | Wearable Respiratory Monitoring Devices | |

| Ventilation and Critical Care Monitoring Systems | ||

| Non-Invasive Monitoring Devices | ||

| Sleep and Breathing Disorder Monitoring Devices | ||

| Respiratory Imaging and Advanced Diagnostics Systems | ||

| By Technology | Machine Learning and Predictive Analytics | |

| Deep Learning | ||

| Computer Vision (Imaging and waveform analysis) | ||

| Edge AI and Real-Time Processing | ||

| By Application | Chronic Respiratory Disease Management | |

| Sleep and Breathing Disorder Monitoring | ||

| Critical Care and Acute Respiratory Monitoring | ||

| Fitness and Wellness Monitoring | ||

| Post-Acute and Home Respiratory Care | ||

| By End-User | Hospitals and Clinics | |

| Home-Care Settings | ||

| Long-Term Care and Home Healthcare Providers | ||

| Diagnostic Laboratories | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the expected value of the AI in respiratory monitoring space by 2031?

It is anticipated to reach USD 2.39 billion by 2031, rising from USD 1.21 billion in 2026 at a 14.52% CAGR.

Which component currently generates the most revenue?

Software leads with 62.24% of revenue in 2025, supported by licensing, analytics, and recurring update models.

Which application area is expanding the fastest through 2031?

Post-acute and home respiratory care is the fastest-growing application, with a projected 16.50% CAGR through 2031.

Which region leads today and which region is growing the fastest?

North America leads with 44.37% of 2025 revenue, while Asia-Pacific is expected to grow the fastest at a 17.44% CAGR through 2031.

Page last updated on: