AI In Medication Reconciliation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.03 Billion |

| Market Size (2031) | USD 5.31 Billion |

| Growth Rate (2026 - 2031) | 21.16% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Medication Reconciliation Market Analysis by Mordor Intelligence

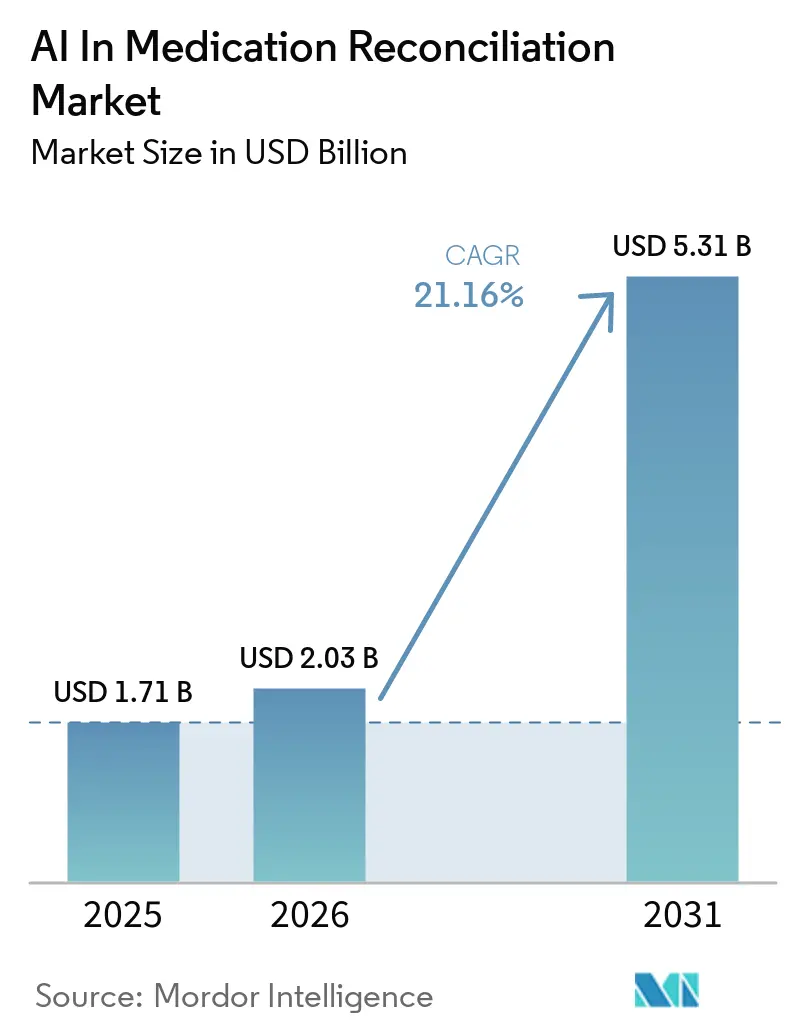

The AI In Medication Reconciliation Market size is expected to increase from USD 1.71 billion in 2025 to USD 2.03 billion in 2026 and reach USD 5.31 billion by 2031, growing at a CAGR of 21.16% over 2026-2031.

The AI in medication reconciliation market is expanding because manual reconciliation still breaks down when patients move between hospital, ambulatory, pharmacy, and post-acute settings, and that leaves medication lists incomplete, delayed, or inconsistent. Medication errors cost USD 42 billion each year worldwide, and poor communication at care transitions remains a major source of hospital-related errors, which keeps this category tied closely to quality, safety, and payment pressure. CMS continues to link clinical information reconciliation to certified EHR use under its Promoting Interoperability framework, so the AI in medication reconciliation market is being pushed by compliance as much as by workflow demand. Clinical evidence also keeps the issue visible, with 88% of post-discharge adults in one 2025 study showing at least 1 discrepancy and older critically ill patients with unintentional discrepancies facing a higher risk of emergency department revisits after discharge. Competition remains fragmented, and new specialists are narrowing feature gaps with established networks and broader care platform vendors, which is likely to keep product improvement fast and pricing discipline tight over the forecast period.

Key Report Takeaways

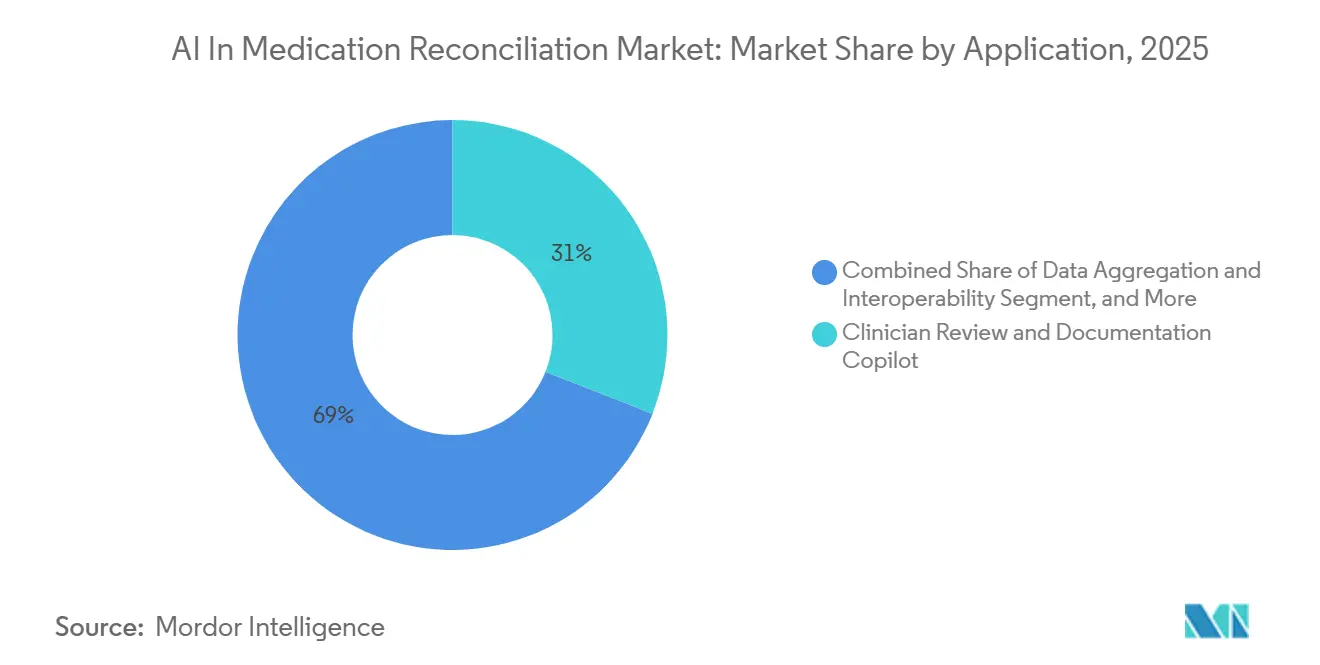

- By application, clinician review and documentation copilot led with 30.95% revenue share in 2025, while data aggregation and interoperability are forecast to expand at 23.51% CAGR through 2031.

- By deployment model, cloud-based platforms held 40.41% share in 2025, while hybrid recorded the highest projected CAGR at 22.07% through 2031.

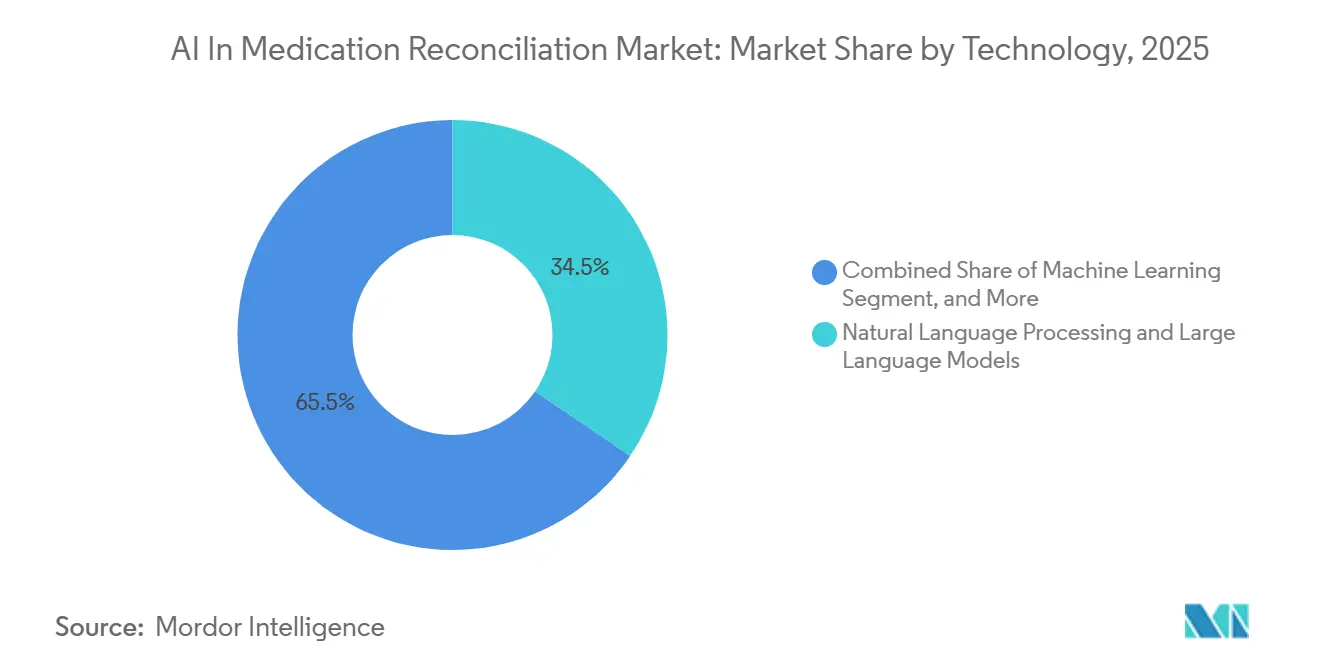

- By technology, NLP and LLMs accounted for 34.53% share in 2025, while ML and Predictive Analytics are advancing at a 21.72% CAGR through 2031.

- By end user, hospitals and health systems held 27.68% share in 2025, while Ambulatory Provider Networks and ACOs are growing fastest at 22.71% CAGR through 2031.

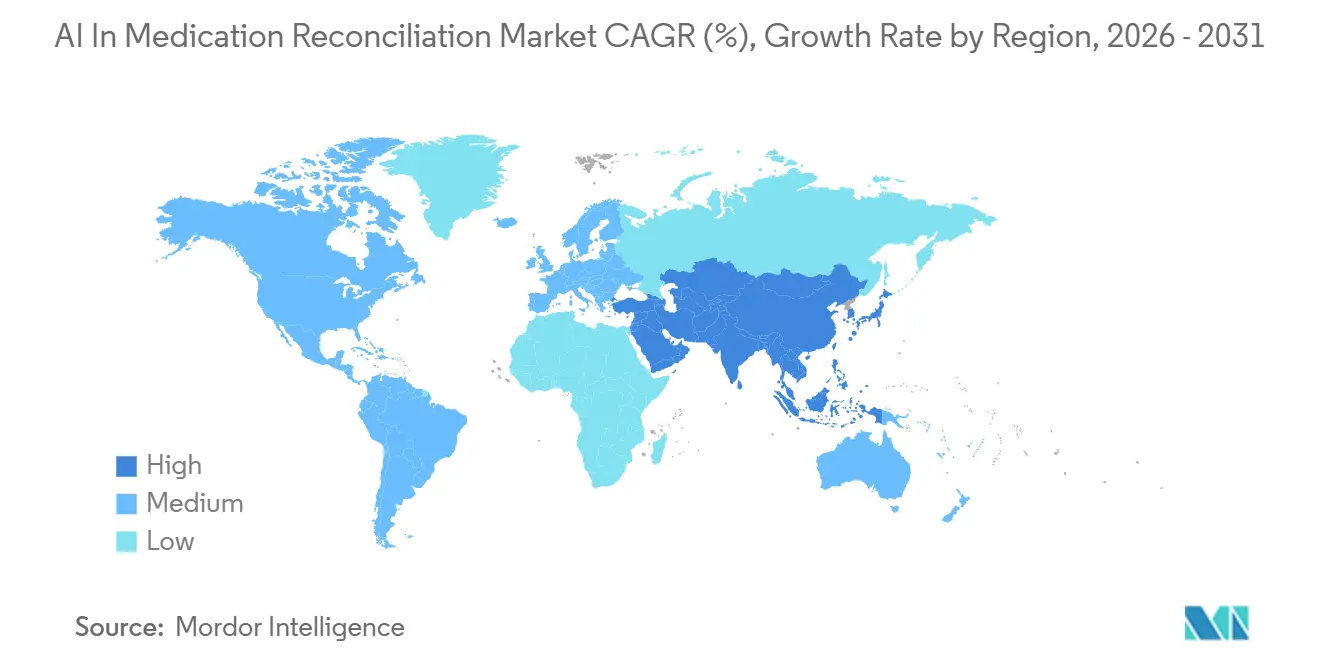

- By geography, North America captured 43.83% share in 2025, while Asia-Pacific is forecast to expand at 23.79% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Medication Reconciliation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Preventable Medication Errors at Care Transitions | +6.5% | Global, particularly North America, Northern Europe, and East Asia | Short term (≤ 2 years) |

| Polypharmacy and Chronic Disease Complexity | +4.8% | Global, highest intensity in North America, Western Europe, Japan, and Australia | Medium term (2-4 years) |

| Pharmacy and Nursing Workforce Shortages | +3.5% | North America and Europe, with spillover into Asia-Pacific | Short term (≤ 2 years) |

| Interoperability and Digital Medication Data Infrastructure | +3.2% | North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Cash-Pay and Off-Network Fill Visibility Gaps | +1.8% | North America, with emerging relevance in Latin America and Southeast Asia | Medium term (2-4 years) |

| Post-Acute Compliance and Transition-Of-Care Audit Pressure | +2.1% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Preventable Medication Errors at Care Transitions Drive Systemic Demand

The AI in medication reconciliation market is rising because medication reconciliation failure remains a routine care transition problem rather than an isolated quality issue. A 2026 prospective cohort study found that 39% of older adults discharged from hospital experienced at least 1 medication error within 7 days, and the share rose to 50% by 90 days.[1]Jiyoung Park, “Unintentional Medication Discrepancies at Care Transitions: Prevalence and Their Impact on Post-Discharge Emergency Visits in Critically Ill Older Adults,” BMC Geriatrics, doi.org In the same study, patients taking 5 or more cardiometabolic medicines had a 63% higher incidence of errors at 7 days, which shows how quickly complexity can overwhelm manual workflows. A multicenter Norwegian study also found that 80.4% of admitted medical patients had at least 1 discrepancy, with omissions making up 55.3% of all discrepancies, even after years of targeted measures. Each omission creates a downstream burden for hospitals, payers, and post-acute providers, so the AI in medication reconciliation market benefits from a direct link between safer transitions and lower avoidable utilization. The Joint Commission’s continued focus on accurate medication reconciliation as a patient safety priority also gives hospital buyers a clear quality and governance basis for adoption.

Polypharmacy and Chronic Disease Complexity Widen the Clinical Gap

The AI in medication reconciliation market is also being lifted by the growing number of patients who carry long medication lists across multiple sites of care. A 2025 systematic review covering more than 520,000 older adults with diabetes found a pooled polypharmacy prevalence of 59%, which shows how common complex medication regimens have become in high-risk populations. A 2026 European analysis of hospitalized adults aged 70 and older found that 51.3% had hyperpolypharmacy, and those patients were 1.89 times more likely to have been hospitalized in the prior year. The problem is made harder by inconsistency in how polypharmacy itself is counted, with one 2025 study showing that prevalence estimates can shift sharply depending on whether active ingredients or unique products are counted.[2]Georgie B. Lee, “Defining Polypharmacy in Older Adults: A Cross-Sectional Comparison of Prevalence Estimates Calculated According to Active Ingredient and Unique Product Counts,” International Journal of Clinical Pharmacy, link.springer.com That makes normalized medication list creation more valuable, because clinicians need a stable view of what a patient is actually taking before they can resolve discrepancies safely. The AI in medication reconciliation market gains most when high-risk drug classes such as cardiovascular agents, antidiabetics, and antithrombotics dominate the list, because those classes bring the greatest consequence when an omission, duplication, or dosing mismatch is missed.

Pharmacy and Nursing Workforce Shortages Accelerate Automation Adoption

The AI in medication reconciliation market is moving faster because staffing pressure has become structural in both pharmacy and nursing. HRSA projected in December 2025 that the United States will face a shortage of 30,400 pharmacist full-time equivalents and 245,950 licensed practical nurse full-time equivalents by 2038. Workforce stress is already visible, with the 2024 National Pharmacist Workforce Survey reporting in 2025 that 73% of full-time pharmacists rated workload as high or excessively high, and 36.1% said they were likely or very likely to seek other employment within the year. The International Pharmaceutical Federation also projected a global shortfall of 11 million health workers by 2030, with much lower pharmacy technician density in low and middle-income countries than in high-income countries. Those shortages matter because medication reconciliation is labor-intensive, repetitive, and easy to postpone when inpatient, ambulatory, or pharmacy teams are overloaded. The AI in medication reconciliation market therefore benefits from a practical adoption case, since automation is being treated less as an efficiency add-on and more as a way to protect service continuity. This is also why medication reconciliation software is gaining attention in community hospitals and ambulatory networks that cannot add clinical staff at the pace required by demand.

Interoperability and Digital Medication Data Infrastructure Create an Expanding Network Effect

The AI in medication reconciliation market is supported by improving data infrastructure, which is making medication records easier to search, exchange, and normalize. HL7 finalized the US Core v8.0 MedicationRequest profile in late 2024, establishing minimum expectations for recording and exchanging active prescription data with RxNorm as the required coding standard. Surescripts reported in March 2026 that it exchanged 30.5 billion health intelligence transactions in 2025, up 12.3% from 2024, and delivered 3.79 billion medication histories while preventing an estimated 47% of severe medication history errors at admission. In Europe, the European Health Data Space regulation entered into force in March 2025 and requires cross-border digital health connections, including ePrescription and eDispensation services, on a phased basis. A 2025 JMIR Medical Informatics study also showed that non-interoperable systems create redundant data storage, manual maintenance burden, data discrepancies, and wasted resources, which are exactly the problems AI aggregation layers are meant to reduce. As more providers connect into shared standards and exchange networks, the AI in medication reconciliation market gains a compounding data advantage, because each added source improves the value of every downstream reconciliation event. That network effect is one reason the fastest growth is shifting toward aggregation and interoperability functions rather than documentation alone.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy and Clinical Governance Concerns | -1.8% | Global, especially North America and Europe | Medium term (2-4 years) |

| EHR Integration and Workflow Reconfiguration Complexity | -2.3% | Global, strongest in fragmented multi-EHR systems | Long term (≥ 4 years) |

| Sparse Full-Process Training Data Beyond BPMH Extraction | -1.2% | Global, with stronger impact in Asia-Pacific, Latin America, and Middle East and Africa | Long term (≥ 4 years) |

| Alert Fatigue and Clinician Liability Concerns | -1.4% | Global, strongest in high-volume inpatient and emergency settings | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Privacy and Clinical Governance Concerns Slow Enterprise Deployment

The AI in medication reconciliation market still faces slower enterprise buying where privacy governance has not caught up with clinical AI experimentation. A 2026 JACEP Open study found that only 23% of health systems had executed Business Associate Agreements for HIPAA-compliant third-party AI use, even though 66% of U.S. physicians reported using AI tools in some form. Medication reconciliation increases concern because the workflow often combines pharmacy fills, clinical notes, claims information, and patient-reported medication use in a single process. That makes governance more difficult than in narrow documentation tools, since access rules, retention policies, and audit requirements can differ across data sources. Health systems that have not defined clear review, approval, and monitoring rules for clinical AI are delaying purchases, which stretches sales cycles even when the operational need is clear. The AI in medication reconciliation market therefore sees uneven timing across buyers, with adoption strongest where privacy, legal, and pharmacy leadership already share a defined governance model. This is also one reason some large providers continue to favor hybrid deployment instead of full cloud migration for medication reconciliation software.

EHR Integration and Workflow Reconfiguration Complexity Compress Vendor Win Rates

The AI in medication reconciliation market also faces a practical barrier in the work needed to embed tools inside live clinical workflows. A 2024 scoping review of 23 hospital studies on EHR-integrated medication technologies identified alert fatigue, workflow assimilation, cost, data quality, and interoperability as key implementation barriers, and 1 included study found that 95% of dose-range alerts were clinically invalid while prescribers ignored 96% of them. A 2026 qualitative study at National Taiwan University Hospital found that medication reconciliation took 15 to 30 minutes per patient under current workflows and was often deprioritized because of competing duties, unclear role assignment, and documentation ambiguity. A 2025 BMJ Quality and Safety editorial also noted that AI-enabled medication safety tools face broader barriers around usability, trustworthiness, explainability, and evidence of real effectiveness in practice. That means deployment costs are not limited to software licenses, because hospitals also need workflow redesign, clinician training, and cross-functional agreement on who reviews, escalates, and closes discrepancies. The AI in medication reconciliation market can grow quickly, but vendors that underestimate these change management demands are likely to see lower conversion and slower expansion after the first contract.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Copilot Capabilities Lead While Aggregation Scales Fastest

Clinician review and documentation Copilot held 30.95% of AI in medication reconciliation market share in 2025, making it the largest application because it addresses the most immediate workload problem faced by pharmacists and nurses during admission and discharge. This part of the AI in medication reconciliation market gained early traction because buyers could see value quickly through faster documentation, easier comparison of lists, and better annotation of medication changes. Hospitals have generally preferred to relieve the most visible manual burden first, rather than begin with a full redesign of data sourcing across every care setting. That made copilot tools easier to justify in capital reviews, especially where inpatient teams were already carrying high staffing pressure. The application also aligns well with current buyer behavior, since health systems often want a narrow first deployment that can show measurable time savings before expanding into broader automation. The AI in medication reconciliation market therefore started with assistance at the point of review and is now moving toward more upstream and network-dependent functions.

The AI in medication reconciliation market size for data aggregation and interoperability is projected to expand at 23.51% CAGR through 2031, and that makes it the fastest-growing application because the quality of every reconciliation event depends on the completeness of the underlying medication history. Surescripts stated that its network delivered 3.79 billion medication histories in 2025 and that its aggregation engine identified 1.1 drugs per patient that manual reconciliation would have missed. Medication History Capture and Normalization, along with Discrepancy Detection and Prioritization, is also expanding because clinical notes, discharge summaries, and prescription instructions still arrive in highly variable formats. A 2026 JMIR scoping review found that 71.3% of AI medication reconciliation studies relied on free-text EHR clinical notes, which confirms how central normalization remains to the overall workflow. The same review showed that 98.9% of studies still focused on information acquisition, while discrepancy resolution remained largely unautomated, so the highest-value part of the application stack is still open. That gap gives the AI in medication reconciliation market a clear next growth path, with premium potential likely to sit in tools that can move safely from data capture to meaningful discrepancy prioritization and closure.

By Deployment Model: Cloud Anchors the Present, Hybrid Defines the Future

Cloud-Based deployment held a 40.41% share in 2025, and that leadership reflects how strongly providers value quick implementation and lighter internal infrastructure requirements. In the AI in medication reconciliation market, cloud deployment has been the easiest way for vendors to shorten time to value, especially among community hospitals, ambulatory networks, and resource-constrained provider groups. DrFirst states that its MedHx cloud platform can be implemented in as little as 2 weeks, which highlights why fast rollout matters in a category tied to regulatory, staffing, and patient safety pressure. Cloud also supports continuous updates to NLP models and medication data connections, which is helpful in a field where terminology, formularies, and workflow logic change often. The AI in medication reconciliation market still benefits from cloud economics because smaller buyers cannot always support extensive local configuration and maintenance. This is why many early wins continue to center on deployments that can be activated quickly inside existing EHR environments.

The AI in medication reconciliation market size for Hybrid deployment is projected to expand at 22.07% CAGR through 2031, showing that many large systems now prefer flexible architecture over full cloud migration. Hybrid appeals to providers that want cloud-based NLP and interoperability capabilities but still need stricter control over certain protected health information and internal governance rules. In this part of the AI in medication reconciliation market, hybrid is becoming a strategic endpoint rather than a temporary stop, because health systems increasingly want to route unstructured text into scalable AI services while retaining sensitive structured records inside local or tightly governed environments. On-Premise deployments remain relevant in government facilities, academic medical centers, and countries with strong data sovereignty expectations, even though growth is slower. European digital medication management programs, including Germany’s ongoing buildout of digital medication records within the national EHR framework, continue to support buyers who want clear localization and certification controls. Procurement standards such as ISO 27001, SOC 2, and HITRUST now shape vendor credibility in practice, so deployment choice is increasingly a governance decision as much as a technical one. That dynamic also favors medication reconciliation software vendors that can support multiple operating models without forcing customers into a single architecture.

By Technology: NLP and LLMs Command Share While ML Predictive Layers Accelerate

NLP and LLMs held 34.53% revenue share in 2025, which makes them the core technology layer because medication reconciliation still starts with reading and structuring messy clinical text. The AI in medication reconciliation market depends heavily on this capability, since prescription instructions, discharge notes, medication histories, and patient-reported lists often arrive in free text that cannot be used safely without normalization. DrFirst states that 60% of incoming medication data arrives as free text, which shows why language processing remains the starting point for nearly every automated workflow in this category. The technical value is not just extraction, because the model also needs to link terms to standardized medication concepts and preserve the meaning of dose, route, frequency, and timing. That is why vendors with clinically tuned language models have gained early relevance even when they are smaller than larger network incumbents. In the AI in medication reconciliation market, the strongest NLP offerings are those that reduce manual cleanup rather than simply generate a readable summary.

ML and Predictive Analytics are growing fastest at 21.72% CAGR through 2031, which shows that buyers increasingly want tools that can help prioritize risk before the next care transition happens. This shift moves the AI in medication reconciliation market beyond transcription and into triage, where systems can flag which patients are most likely to have a clinically significant discrepancy based on medication burden, recent transitions, or history gaps. Rules engines and drug knowledge graphs still matter because many medication safety tasks demand high specificity, especially for interactions, allergy screening, and therapeutic duplication. FDB’s MedProof MCP, made generally available in 2026, reflects that need by grounding AI workflows in validated drug knowledge to reduce hallucination risk. A June 2025 preprint on Atman Health’s AMREC conversational AI agent reported 98.3% accuracy across 18 extracted prescription elements, suggesting that narrowly tuned medication models can materially improve structured extraction quality when trained on domain-specific terminology. Computer vision and OCR remain smaller but durable layers in the AI in medication reconciliation market, especially where handwritten documents, packaging labels, or home-based records still serve as the source of truth. Over time, technology competition is likely to center on how well vendors combine language models, predictive scoring, and trusted medication knowledge in a single workflow.

By End User: Hospitals Lead Revenue While Ambulatory Networks Expand Fastest

Hospitals and health systems held 27.68% share in 2025, and they remain the largest end-user group because the heaviest medication reconciliation burden still sits around admission, discharge, and internal transfers. In the AI in medication reconciliation market, hospitals have the clearest incentive to adopt because they face the highest volume of transitions, the strongest documentation pressure, and the most immediate readmission and patient safety consequences when reconciliation breaks down. Hackensack Meridian Health reported in July 2025 that its work with DrFirst increased automated prescription instruction mapping from 26% to 86% across a sample of 300,000 medications after Epic integration. DrFirst also reported that Baptist Health saved more than 19,000 clinician hours across 9 million medication instruction conversions, reinforcing the operational return that hospital buyers are seeking. These examples matter because large health systems often require a measurable time or safety benefit before widening deployment across service lines. The AI in medication reconciliation market therefore still relies on hospital procurement as the largest near-term revenue base.

Ambulatory provider networks and ACOs are expanding at the fastest pace with a 22.71% CAGR through 2031, reflecting how much medication risk now sits between settings rather than only inside the hospital itself. The AI in medication reconciliation market is moving into outpatient and care coordination environments because discrepancies often emerge when patients shift between inpatient care, primary care, specialty care, and retail pharmacy. Duke Institute for Health Innovation announced its C.L.R. AI tool in April 2026 to aggregate EHR data across settings and identify adherence gaps and discrepancies, which shows growing academic and provider attention to ambulatory medication management. Post-acute and skilled nursing workflows are also attracting interest, with Guardoc Health building pharmacy reconciliation capabilities mapped to CMS F-tags across more than 100 facilities in 14 U.S. states. Other end users such as pharmacies and pharmacy services organizations benefit from increasing transaction automation, with Surescripts stating that RxTransfer usage doubled in January 2026 versus the entirety of 2025. The AI in medication reconciliation market is therefore broadening from an inpatient workflow tool into a cross-setting coordination capability, and that should widen the addressable base for medication reconciliation software over the forecast period.

Geography Analysis

North America held 43.83% of AI in medication reconciliation market share in 2025, making it the leading region because reimbursement, compliance, and interoperability incentives are more formalized than in any other geography. The United States anchors this position through the CMS Promoting Interoperability Program, which requires clinical information reconciliation using certified EHR technology and links noncompliance to a 75% reduction in the annual market basket update under the hospital program framework. That regulatory structure gives the AI in medication reconciliation market a stable procurement floor in U.S. hospitals even when budgets tighten. Surescripts also adds scale to the regional lead, having exchanged 30.5 billion health intelligence transactions and delivered 3.79 billion medication histories in 2025. Canada is also strengthening the regional position, with Orion Health and HEALWELL AI demonstrating a FHIR R4-compliant pan-Canadian Patient Summary in June 2025 that supports real-time aggregation of medications, allergies, and conditions across provincial systems.

Asia-Pacific is the fastest-growing region at 23.79% CAGR through 2031, and that pace reflects a mix of digital health investment, workforce constraints, and rising medication complexity. The AI in medication reconciliation market is gaining room in Asia-Pacific because national programs in China, India, Japan, Singapore, and Australia are expanding the digital infrastructure needed for clinical data exchange and AI-supported workflows. Japan remains especially important because a 2024 cross-sectional study of 5,707 urgent internal medicine admissions found that 5% were caused by adverse drug reactions, and polypharmacy carried an odds ratio of 2.66 for ADR-related hospitalization. Workforce imbalance also supports adoption, with the International Pharmaceutical Federation reporting pharmacist density of 12.12 per 10,000 population in high-income Asia-Pacific economies versus 3.81 in lower-income countries. Australia adds another demand source, with a 2026 study showing polypharmacy exposure in 9.2% of adults in 2024, up from 8% in 2013 and representing 2 million people.

Europe remains a structurally favorable region because regulation is improving the consistency of medication data exchange across member states. The European Health Data Space regulation entered into force in March 2025 and is expected by the European Commission to generate EUR 11 billion in savings over the next decade, or USD 11.9 billion, while supporting broader digital health expansion across the region. Germany’s digital medication management buildout within its national ePA framework is also creating more standardized medication plan infrastructure for AI tools to use. Polypharmacy prevalence among Europeans aged 65 and older remained above 51% in Poland and Portugal in the SHARE Wave 9 update, which shows why medication burden is not confined to Western Europe alone. MiddleEast and Africa and South America remain earlier-stage opportunities in the AI in medication reconciliation market, with lower EHR penetration and thinner pharmacy workforces limiting scale today, though national digitization programs in Gulf countries point to a clearer future entry path.

Competitive Landscape

The AI in medication reconciliation market remains fragmented, and no single vendor holds a dominant global position. Competition in the AI in medication reconciliation market is shaped by 3 groups: health information network operators with broad data reach, AI specialists built around medication workflows, and broader care platform vendors that include reconciliation inside larger coordination suites. Surescripts represents the network incumbent model, using scale in transaction exchange and medication history access as its main advantage rather than positioning itself as a pure-play AI specialist. DrFirst, Asepha, Atman Health, Guardoc Health, and SyncMedAI compete more directly on workflow fit, extraction accuracy, and the ability to reduce manual effort inside live medication processes. Orion Health and Elation Health represent the platform route, where medication reconciliation sits inside a wider digital record or ambulatory workflow offering. This structure keeps the AI in medication reconciliation market open to specialist entry, because no single approach yet controls both the best data access and the best model performance across the full workflow.

DrFirst remains one of the stronger workflow-focused competitors because it combines medication history access with clinical-grade AI and clear operational outcome claims. The company states that its AI automatically converts 92% of free-text prescription instructions and reduces medication history data collection time by 60% to 80%, which is a strong selling point in high-volume hospital settings. Its July 2025 partnership with Hackensack Meridian Health is a good example of strategic execution, since the project increased automated instruction mapping from 26% to 86% after Epic integration. Orion Health is pursuing a different strategy through platform integration, with its Amadeus AI offering combining HEALWELL AI’s DARWEN engine with FHIR R4, HL7 v2, and TEFCA-ready connectivity across major EHR environments. That gives the AI in medication reconciliation market an example of consolidation at the care-platform level rather than at the single-workflow level.

White space remains largest in full-process discrepancy resolution, post-acute compliance workflows, and multilingual medication extraction. A 2026 JMIR scoping review found that 98.9% of published AI medication reconciliation studies still focused on information acquisition and that none had automated discrepancy resolution in a complete way, which leaves a major open lane for future product development. Guardoc Health is targeting one underserved niche by mapping pharmacy reconciliation outputs to CMS F-tags for skilled nursing facilities, while smaller vendors such as Rivvi are positioning around data reconciliation across payer, pharmacy, and clinical sources. Elation Health’s January 2026 partnership with Anthropic shows another route into the AI in medication reconciliation market, where general-purpose LLM capability is entering through EHR partnerships instead of standalone products. Compliance credentials such as HIPAA governance readiness, SOC 2 Type II, and HITRUST continue to act as practical filters in enterprise procurement, which raises barriers for smaller entrants that cannot document secure and auditable deployment pathways. This competitive setup supports continued innovation, but it also means that only vendors with both credible clinical performance and clean implementation discipline are likely to scale broadly.

AI In Medication Reconciliation Industry Leaders

Atman Health

Elation Health

Orion Health

Surescripts

Veryfi

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Surescripts reports 30.5 billion health intelligence transactions in 2025, a 12.3% year-over-year increase, while delivering 3.79 billion medication histories and returning prior authorization approvals in 18 seconds across 20 health systems. RxTransfer usage doubled in January 2026 versus all of 2025, demonstrating an accelerating network effect in real-time medication transfer.

- January 2026: Elation Health partners with Anthropic to embed Claude into its EHR platform, reducing time-to-first clinical insights by 61% and accelerating AI adoption among primary care clinicians. This partnership accelerates AI-native medication workflow adoption in ambulatory settings.

- September 2025: Orion Health launches Amadeus AI powered by HEALWELL AI's patented DARWEN engine, delivering SmartSearch, SmartSummary, and SmartIdentify capabilities across HIEs for over 150 million patients in 12 countries. The platform is FHIR R4, TEFCA-ready, and integrates medication management within a longitudinal digital care record.

- July 2025: Hackensack Meridian Health partners with DrFirst to integrate AI-powered medication workflow tools into its Epic EHR, increasing automated prescription instruction mapping from 26% to 86% across a sample of 300,000 medications and generating measurable reductions in manual data entry.

Global AI In Medication Reconciliation Market Report Scope

AI in Medication Reconciliation Market refers to the sector of digital health technologies that use artificial intelligence, natural language processing (NLP), and machine learning (ML) to automate and enhance the process of comparing a patient's medication list across different healthcare providers.

The AI in Medication Reconciliation Market Report is Segmented by Application (Medication History Capture and Normalization, Discrepancy Detection and Prioritization, Clinician Review and Documentation Copilot, Data Aggregation and Interoperability, Compliance Analytics and Transition-Of-Care Reporting), Deployment Model (Cloud-Based, Hybrid, On-Premise), Technology (NLP and LLMs, ML and Predictive Analytics, Rules Engines and Drug Knowledge Graphs, Other Technologies), End User (Hospitals and Health Systems, Ambulatory Provider Networks and ACOs, Post-Acute, Long-Term Care and SNFs, Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Medication History Capture and Normalization |

| Discrepancy Detection and Prioritization |

| Clinician Review and Documentation Copilot |

| Data Aggregation and Interoperability |

| Compliance Analytics and Transition-Of-Care Reporting |

| Cloud-Based |

| Hybrid |

| On-Premise |

| Natural Language Processing and Large Language Models |

| Machine Learning and Predictive Analytics |

| Rules Engines and Drug Knowledge Graphs |

| Other Technologies (Computer Vision and OCR, Etc.) |

| Hospitals and Health Systems |

| Ambulatory Provider Networks and ACOS |

| Post-Acute, Long-Term Care, and Skilled Nursing Facilities |

| Other End Users (Pharmacies and Pharmacy Services Organizations, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application | Medication History Capture and Normalization | |

| Discrepancy Detection and Prioritization | ||

| Clinician Review and Documentation Copilot | ||

| Data Aggregation and Interoperability | ||

| Compliance Analytics and Transition-Of-Care Reporting | ||

| By Deployment Model | Cloud-Based | |

| Hybrid | ||

| On-Premise | ||

| By Technology | Natural Language Processing and Large Language Models | |

| Machine Learning and Predictive Analytics | ||

| Rules Engines and Drug Knowledge Graphs | ||

| Other Technologies (Computer Vision and OCR, Etc.) | ||

| By End User | Hospitals and Health Systems | |

| Ambulatory Provider Networks and ACOS | ||

| Post-Acute, Long-Term Care, and Skilled Nursing Facilities | ||

| Other End Users (Pharmacies and Pharmacy Services Organizations, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving adoption of AI in medication reconciliation across healthcare systems?

Growth is being supported by persistent medication errors at care transitions, rising polypharmacy, staffing shortages in pharmacy and nursing, and stronger interoperability rules.

Which application area is leading revenue today?

Clinician review and documentation copilot led in 2025 with a 30.95% share because hospitals are first using AI to reduce pharmacist and nursing documentation burden before automating the full workflow.

Which application area is growing the fastest through 2031?

Data aggregation and interoperability are the fastest-growing applications with a 23.51% CAGR through 2031, reflecting the need to pull medication data from fragmented records before discrepancies can be resolved accurately.

Why are hospitals still the largest buyers?

Hospitals and health systems held 27.68% share in 2025 because they manage the highest volume of admissions, discharges, and internal transfers, and they face the strongest safety, audit, and payment consequences when medication reconciliation is incomplete.

What is the expected value of AI in medication reconciliation by 2031?

The category is projected to grow from USD 2.03 billion in 2026 to USD 5.31 billion by 2031 at a 21.16% CAGR.

Page last updated on: