Agentic AI In Pharmaceuticals Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

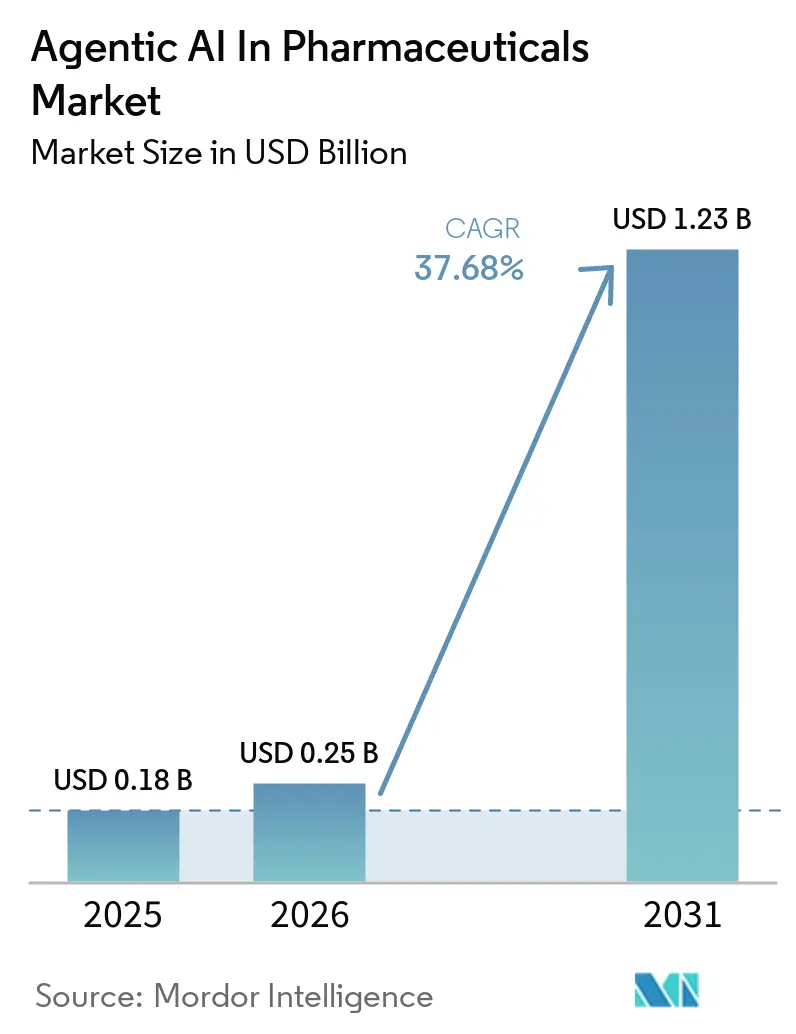

| Market Size (2026) | USD 0.25 Billion |

| Market Size (2031) | USD 1.23 Billion |

| Growth Rate (2026 - 2031) | 37.68% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agentic AI In Pharmaceuticals Market Analysis by Mordor Intelligence

The agentic AI in pharmaceuticals market size is expected to grow from USD 0.18 billion in 2025 to USD 0.25 billion in 2026 and is forecasted to reach USD 1.23 billion by 2031, registering a 37.68% CAGR over 2026–2031. Momentum stems from sponsors redirecting capital away from incremental wet-lab hiring toward computational platforms that compress lead-optimization cycles from quarters to weeks, preserving patent life and boosting risk-adjusted returns. Regulatory clarity arrived in January 2026 when the FDA and EMA ruled that AI-generated hypotheses face the same evidentiary burden as human-derived ones, removing a filing bottleneck for Phase I programs. Enterprise adopters dominate early spending because their GMP environments demand explainability controls that only mature vendors can supply, yet contract research organizations (CROs) are positioned for the fastest uptake as sponsors outsource AI-driven trial-design optimization. Cloud deployment continues to outpace hybrid and on-premise models thanks to elastic compute that eliminates large capital outlays, while North America retains purchasing leadership on the back of marquee partnerships between AI‐native discovery firms and major drug makers.

Key Report Takeaways

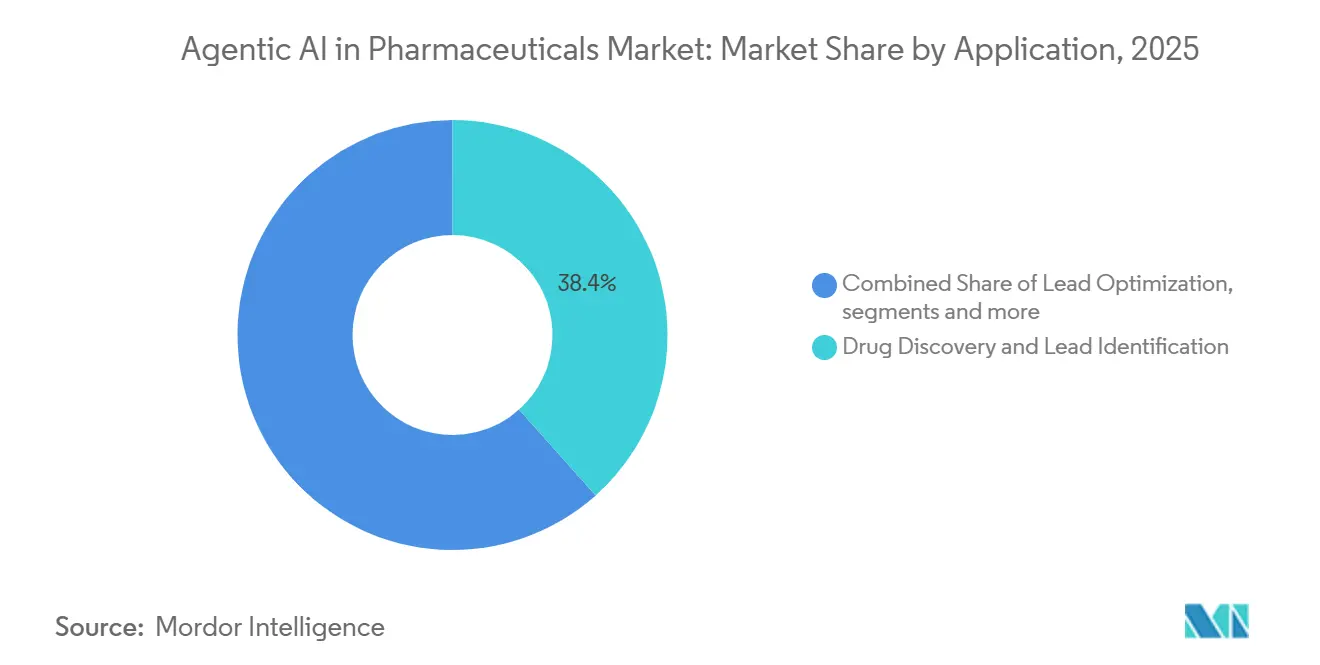

- By application, drug discovery and lead identification led the agentic AI in pharmaceuticals market in 2025 with a 38.44% share, while clinical trial design and recruitment is expected to be the fastest-growing segment, advancing at a 39.34% CAGR through 2031.

- By deployment mode, cloud-based solutions accounted for a 50.27% share of the agentic AI in pharmaceuticals market size in 2025 and are projected to maintain the highest growth rate, with a 39.12% CAGR through 2031.

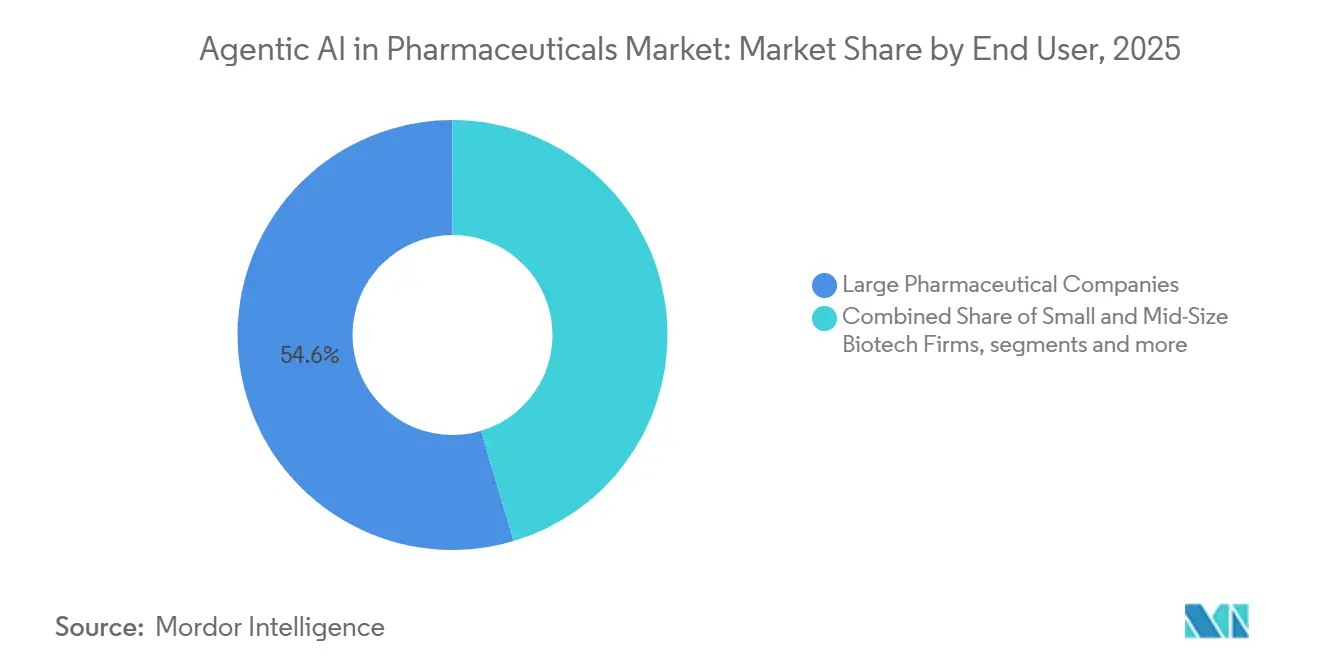

- By end user, large pharmaceutical companies held the dominant position with 54.64% of revenue in 2025, whereas CROs are expected to be the fastest-growing segment, registering a 38.33% CAGR over the same period.

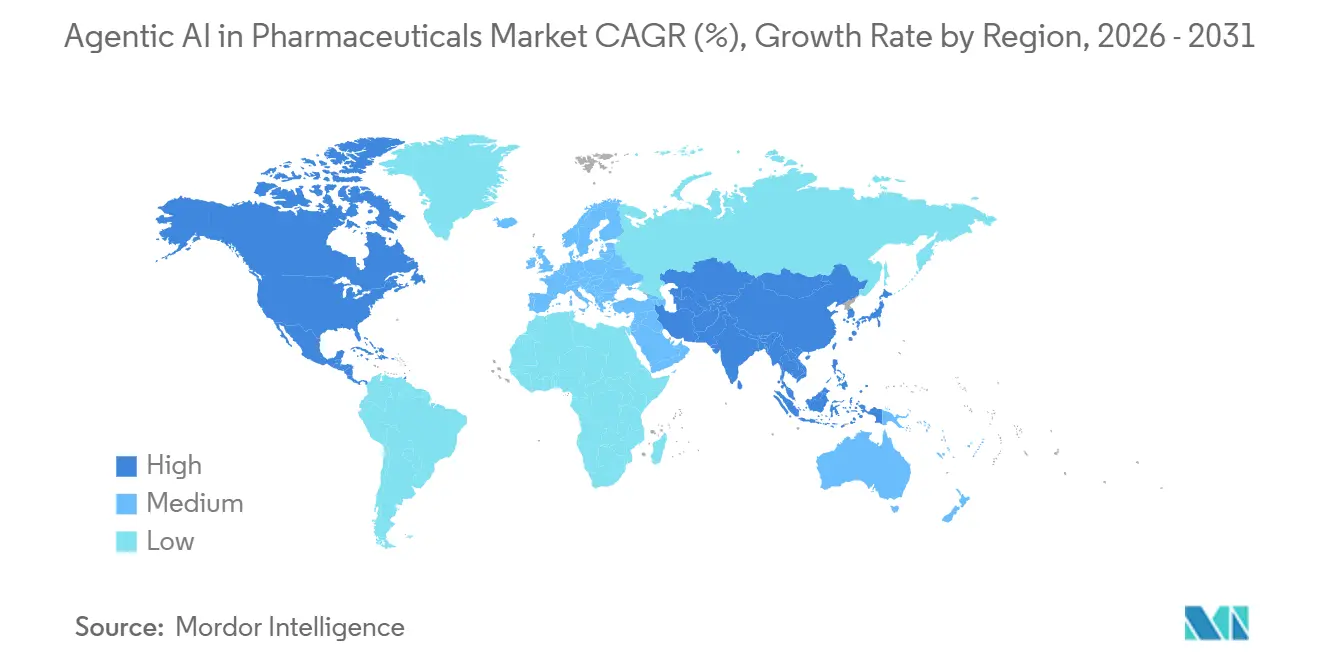

- By geography, North America led the agentic AI in pharmaceuticals market with a 50.76% share in 2025, while Asia-Pacific is expected to be the fastest-growing region, with a 40.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Agentic AI In Pharmaceuticals Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating R&D Cost Pressures Driving AI-Led Discovery | +8.5% | Global, especially North America and Europe | Medium term (2-4 years) |

| Rising Availability of High-Quality Biological Data Sets | +7.2% | Global, with rapid acceleration in Asia-Pacific | Short term (≤ 2 years) |

| Regulatory Encouragement for AI-Driven Trial Design | +6.8% | North America and Europe, early pilots in Japan and South Korea | Medium term (2-4 years) |

| Integration of Agentic AI With Self-Driving Laboratories | +5.9% | North America and select European hubs | Long term (≥ 4 years) |

| Foundation Models Targeting Rare-Disease Biology | +4.3% | Global, spurred by EU orphan-drug incentives | Medium term (2-4 years) |

| Blockchain-Secured Data Marketplaces for Federated Learning | +3.1% | North America and EU, limited traction in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating R&D Cost Pressures Driving AI-Led Discovery

The out-of-pocket cost of bringing a single molecule from target nomination to approval averaged USD 2.6 billion in 2024, with Phase II failure rates near 60%. AI-first platforms can trim preclinical timelines by 30-50% by predicting ADMET liabilities in silico, letting teams cull weak candidates before synthesis.[1]Nature Editorial Board, “AI Accelerates Drug Discovery,” nature.com Partnerships such as Recursion-Bayer (USD 50 million upfront) and Schrödinger-Eli Lilly (USD 50 million) demonstrate that sponsors perceive enough economic upside to fund external AI capabilities.[2]Recursion Pharmaceuticals, “Strategic Partnership With Bayer,” recursion.comEach month removed from preclinical work extends patent exclusivity by the same duration, translating into USD 50–100 million in peak-year sales for blockbuster assets. Firms slow to deploy AI risk forfeiting first-mover advantage in therapeutic areas where even a six-month delay can shift market leadership.

Rising Availability of High-Quality Biological Data Sets

Public data stores surpassed 200,000 experimentally solved protein structures in 2025, while AlphaFold 3 predicted coordinates for 200 million more, providing the corpus that foundation models require to generalize across targets. Real-world evidence platforms now aggregate anonymized health records for 150 million patients across North America and Europe, allowing AI models to surface biomarker-response links invisible in traditional Phase III trials. Federated-learning networks connect 20+ academic medical centers without moving raw data, ensuring compliance with privacy laws yet preserving statistical power, and Asia-Pacific adds scale through a 25% surge in 2025 trial volume.

Regulatory Encouragement for AI-Driven Trial Design

Joint FDA-EMA principles released in January 2026 permit synthetic control arms if model prediction intervals overlap historical placebo by at least 80%, a threshold already met in several oncology studies. Adaptive protocols now let sponsors narrow or expand cohorts mid-study based on interim biomarker signals, trimming sample sizes by up to 30% while safeguarding statistical rigor. Japan and South Korea adopted similar allowances in 2025, and the FDA’s Sentinel System integrates machine-learning classifiers to flag safety issues months earlier than manual monitoring.

Integration of Agentic AI With Self-Driving Laboratories

Insilico Medicine’s fully autonomous facility, operational since March 2025, designs, synthesizes, and assays 100 compounds weekly with minimal human oversight. This closed-loop cycle shrinks the design-make-test window from six months to six weeks and cuts cost per lead candidate by 68%. Relay Therapeutics achieved analogous gains by pairing agentic AI with advanced biophysics to map elusive allosteric pockets, pushing three oncology candidates into the clinic during 2025. Explainability remains the gating factor, as GMP auditors require granular logs for every automated decision.

Restraints Impact Analysis*

| Restraint | ( ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Privacy and Cybersecurity Concerns Limit Data Sharing | –4.7% | EU and North America | Short term (≤ 2 years) |

| Skill Gap in Validating and Deploying Complex AI Agents | –3.8% | Global, acute among mid-size biotech firms | Medium term (2-4 years) |

| Synthetic-Data Feedback Loops Risk Model Collapse | –2.9% | Global | Medium term (2-4 years) |

| Explainability Gaps in GMP Environments Delay Compliance | –2.4% | North America and EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data-Privacy and Cybersecurity Concerns Limit Data Sharing

A 2024 cloud misconfiguration exposed anonymized European patient genotypes, drew EUR 20 million in GDPR fines, and pushed 30% of EU sponsors back to on-premise storage.[3]Financial Times Staff, “GDPR Breach Spurs On-Premise Reversion,” ft.com HIPAA’s breach-notification mandates elevate reputational risk; the average U.S. healthcare data breach cost USD 10.9 million in 2024. Sponsors increasingly require vendors to carry at least USD 50 million in cyber-insurance, barring many early-stage AI startups from procurement lists. Differential privacy can mitigate exposure but erodes model accuracy by up to 10 percentage points, an efficiency hit acceptable only when regulatory penalties outweigh performance loss.

Skill Gap in Validating and Deploying Complex AI Agents

Fewer than 15% of R&D teams combine medicinal chemistry, software engineering, and regulatory expertise. The median time to fill a senior AI-scientist role reached nine months in 2025, double the 2020 benchmark. Universities offer limited cross-disciplinary programs, and CRO engagements that bundle AI validation services command 30–40% price premiums, inflating external spend. Regulator-defined documentation of model lineage and hyperparameter tuning adds workload that current staffing levels cannot absorb.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Clinical Trials Outpace Discovery

Clinical-trial design and recruitment is expected to grow at 39.34% CAGR through 2031, eclipsing drug discovery, which held 38.44% of 2025 revenues. AI-based patient stratification lowers screen-failure rates by 20–30 percentage points, directly trimming per-protocol costs. Adaptive designs embracing interim biomarker reads cut Phase III enrollment by one-quarter, preserving statistical power while accelerating timelines. The agentic AI in pharmaceuticals market size for clinical-trial applications is projected to reach USD 0.52 billion by 2031, underscoring sponsors’ pivot toward data-driven enrollment systems.

Manufacturing-process optimization and pharmacovigilance together represented <15% of 2025 outlays. Explainability remains the chief barrier, because GMP auditors insist upon causal chains for every automated bioreactor tweak. Uptake should rise after regulators formalize acceptance criteria for reinforcement-learning controllers, but current penetration still lags discovery and clinical segments.

By Deployment Mode: Cloud Dominance Persists

Cloud accounted for 50.27% of 2025 spending and is forecasted to post a 39.12% CAGR through 2031, buoyed by confidential-computing enclaves that encrypt data even during runtime. The agentic AI in pharmaceuticals market share for cloud deployments could top 60% by 2031 as pay-as-you-go models undercut on-premise total cost of ownership by 40–60% for bursty workloads.

Hybrid architectures serve GMP workloads that demand air-gapped validation clusters but still route non-critical compute to the cloud, seizing cost advantage while satisfying compliance mandates. On-premise clusters persist among legacy outfits, yet refresh cycles and cooling overhead make them economically unattractive for simulations running <2,000 hours annually.

By End User: Contract Research Organizations Gain Share

Large pharmaceutical companies captured 54.64% of 2025 revenue because their compliance teams require enterprise-grade controls. However, Contract Research Organizations (CROs) are expected to log a 38.33% CAGR as sponsors pursue variable-cost models that bundle AI analytics with global site networks. Turnkey AI packages priced at USD 200,000–500,000 per program let small biotechs avoid the USD 5 million annual fixed cost of in-house infrastructure. The agentic AI in pharmaceuticals market size attributed to CRO clients may therefore climb to USD 0.4 billion by 2031, eroding big-pharma dominance.

Geography Analysis

North America generated 50.76% of 2025 revenue on the strength of AI-native players like Recursion, Schrödinger, and Relay Therapeutics plus regulatory first-mover advantage after the January 2026 FDA-EMA principles. U.S. venture funding for pharmaceutical AI hit USD 4.2 billion in 2024, enabling startups to scale without early licensing deals. Canada benefits from generous R&D tax credits but lacks the domestic customer base to match U.S. scale, and Mexico remains nascent pending regulatory modernization.

Asia-Pacific is expected to grow at a 40.12% CAGR through 2031, driven by China’s subsidies for quantum-computing infrastructure and India’s significantly lower clinical trial costs, averaging about USD 2,000 per patient compared to approximately USD 15,000 in the United States. Japan’s PMDA draft guidance allows AI-guided stratification for rare diseases, unlocking previously unviable studies, while South Korea’s KRW 500 billion (USD 375 million) initiative underwrites public-private AI-pharma projects. Australia trails but may catch up after regulatory harmonization with the FDA in February 2026.

Europe remains constrained by GDPR consent hurdles that stretch multi-site approval times to 18 months. Nonetheless, hubs in the United Kingdom, France, and Germany anchor federated-learning pilots by BenevolentAI and Owkin. Middle Eastern Gulf states fund AI research as part of economic diversification but lack sufficient patient volumes for robust model training. South Africa offers genetically diverse trial cohorts yet hosts few AI vendors, and Latin American growth is stymied by currency volatility and shifting regulatory stances.

Competitive Landscape

The agentic AI in pharmaceuticals market is characterized by a moderately fragmented competitive landscape, with market presence distributed across multiple vendors rather than concentrated among a few players. Schrödinger’s FEP+ attains 95% affinity-prediction accuracy for kinase inhibitors, commanding USD 500,000 annual licenses.

Recursion’s phenomics engine processes 2 billion cellular images quarterly, winning USD 100 million in combined upfronts from Bayer and Roche. White-space remains in manufacturing-process control, where reinforcement learning has cut biologics batch-rejection from 8% to less than 2%, saving large facilities up to USD 50 million annually.

Strategic models shift from pure software licensing to outcome-based milestones, aligning vendor rewards with clinical success. Insilico’s Chemistry42 advanced a fibrosis candidate into Phase I within 18 months, proving agentic AI can compress design cycles enough to justify risk sharing. Patent filings rose 40% year-on-year in 2025, signaling that algorithms and datasets themselves are becoming protective moats. CROs capitalize by offering modular AI services that plug into sponsors’ legacy systems, broadening access for mid-size biotechs.

Agentic AI In Pharmaceuticals Industry Leaders

Insilico Medicine

Exscientia plc

Atomwise Inc.

BenevolentAI

XtalPi

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The FDA and EMA jointly clarified evidentiary standards for AI-generated hypotheses and endorsed synthetic control arms when prediction intervals overlap historical placebo by ≥80%.

- August 2025: Owkin’s federated-learning network reached 20 European centers, training oncology models on 500,000 de-identified records while remaining GDPR-compliant.

- March 2025: Insilico Medicine deployed a humanoid robot enabling design-make-test cycles of six weeks, slashing per-lead costs to USD 800,000.

Global Agentic AI In Pharmaceuticals Market Report Scope

As per the scope of report, agentic AI in pharmaceuticals refers to autonomous AI systems that can plan, execute, and optimize end‑to‑end drug development and safety workflows with minimal human intervention, spanning clinical operations, regulatory, safety, medical writing, and biostatistics, by continuously learning from data, coordinating multi‑step tasks, and triggering actions across systems to reduce cycle times, errors, and manual workload.

The agentic AI in pharmaceuticals market is segmented into application, deployment model, end user, and geography. By application, the market is segmented into drug discovery and lead identification, lead optimization, pre-clinical development, clinical-trial design and recruitment, manufacturing-process optimization, pharmacovigilance and safety monitoring, and others. By end user, the market is segmented into large pharmaceutical companies, small and mid-size biotech firms, contract research organizations, and academic and research institutes. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Drug Discovery and Lead Identification |

| Lead Optimization |

| Pre-clinical Development |

| Clinical-Trial Design and Recruitment |

| Manufacturing-Process Optimization |

| Pharmacovigilance and Safety Monitoring |

| Others |

| On-Premise |

| Cloud-Based |

| Hybrid |

| Large Pharmaceutical Companies |

| Small and Mid-Size Biotech Firms |

| Contract Research Organizations |

| Academic and Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application | Drug Discovery and Lead Identification | |

| Lead Optimization | ||

| Pre-clinical Development | ||

| Clinical-Trial Design and Recruitment | ||

| Manufacturing-Process Optimization | ||

| Pharmacovigilance and Safety Monitoring | ||

| Others | ||

| By Deployment Mode | On-Premise | |

| Cloud-Based | ||

| Hybrid | ||

| By End User | Large Pharmaceutical Companies | |

| Small and Mid-Size Biotech Firms | ||

| Contract Research Organizations | ||

| Academic and Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the agentic AI in pharmaceuticals market expected to grow through 2031?

The agentic AI in pharmaceuticals market is projected to climb from USD 0.25 billion in 2026 to USD 1.23 billion by 2031, registering a 37.68% CAGR, as per Mordor Intelligence.

Which application will add the most new spending by 2031?

Clinical trial design and recruitment is expected to expand at a 39.34% CAGR, outpacing drug discovery workloads and emerging as the largest incremental contributor over the forecast period.

What share of 2025 spending did cloud deployment capture?

Cloud-hosted solutions accounted for 50.27% of 2025 revenue and are poised to remain the dominant deployment choice.

Which region will post the highest growth rate?

Asia-Pacific is expected to be the fastest-growing region, with a 40.12% CAGR through 2031, driven by China’s subsidized quantum infrastructure and India’s cost-efficient clinical trial networks.

Page last updated on: