AI-Based Pharmacy Management Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 23.91 Billion |

| Market Size (2031) | USD 55.37 Billion |

| Growth Rate (2026 - 2031) | 18.29% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI-Based Pharmacy Management Systems Market Analysis by Mordor Intelligence

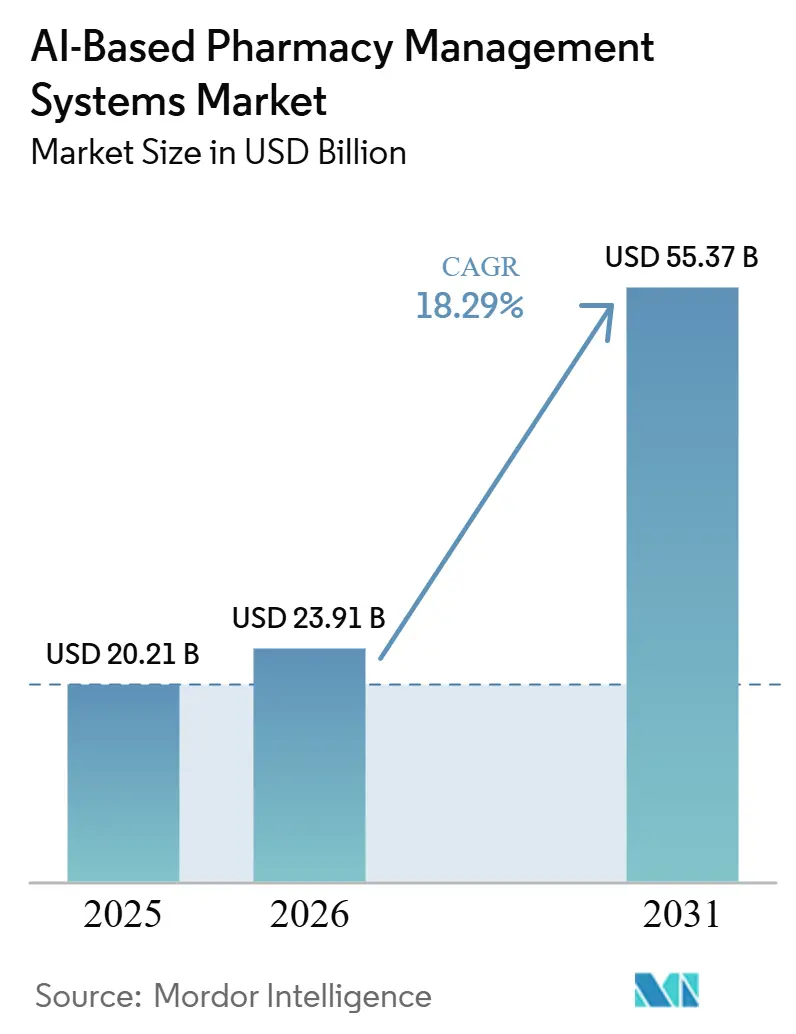

The AI-Based Pharmacy Management Systems Market size is expected to increase from USD 20.21 billion in 2025 to USD 23.91 billion in 2026 and reach USD 55.37 billion by 2031, growing at a CAGR of 18.29% over 2026-2031.

This expansion reflects a move away from manual pharmacy workflows toward platforms that combine decision support, inventory planning, and dispensing automation in a single operating layer. Demand is rising because prescription volumes keep increasing, pharmacist time remains constrained, and health systems now need software that can handle more clinical and administrative work without adding the same level of staffing. Cloud-native platforms are also reducing adoption friction because they shorten deployment cycles, simplify upgrades, and make enterprise AI functions easier to scale across hospital and retail networks. Competitive positioning is shifting toward vendors that can combine workflow intelligence, compliance readiness, and recurring service contracts instead of selling stand-alone software or hardware products. The AI-based pharmacy management systems market is also creating room for modular offerings because large enterprise buyers want full platform breadth, while smaller pharmacy networks need lower-cost tools that can automate a limited set of high-value tasks without replacing the full pharmacy stack.

Key Report Takeaways

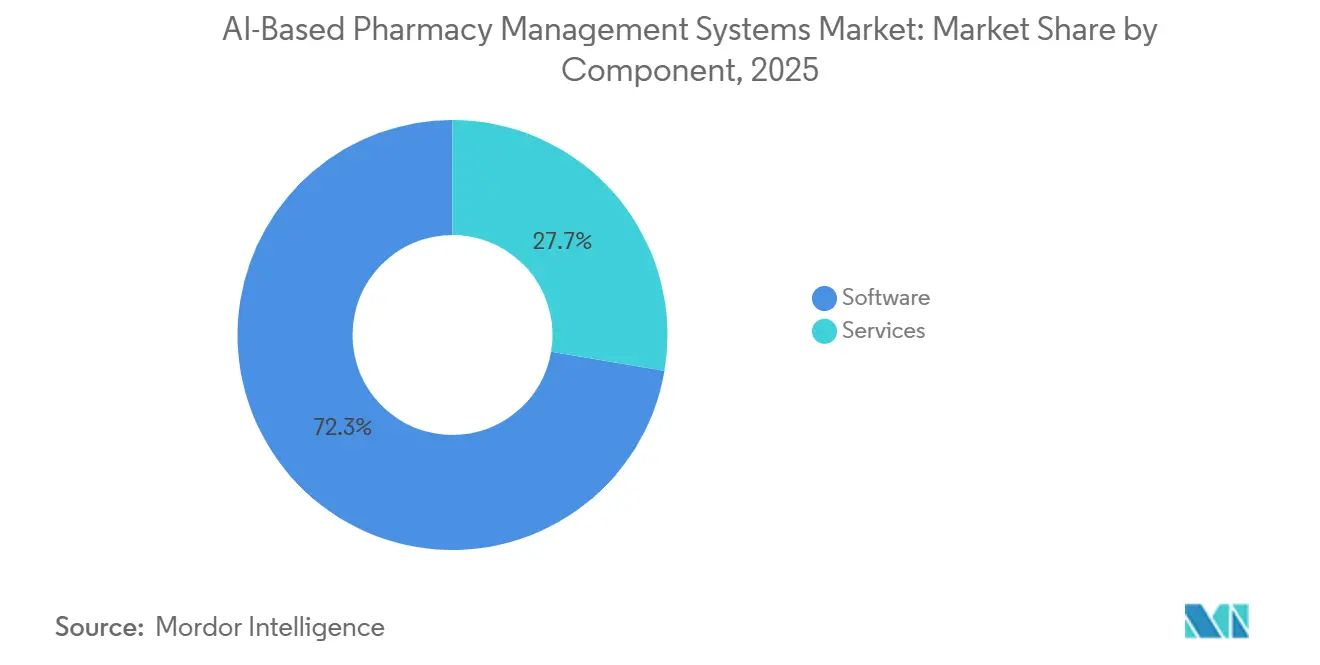

- By component, software held 72.34% of spending in 2025, while services are forecast to expand at 19.32% through 2031.

- By deployment model, cloud and SaaS accounted for 63.85% of the AI-based pharmacy management systems market share in 2025, while on-premise deployments are projected to grow at 20.47% through 2031.

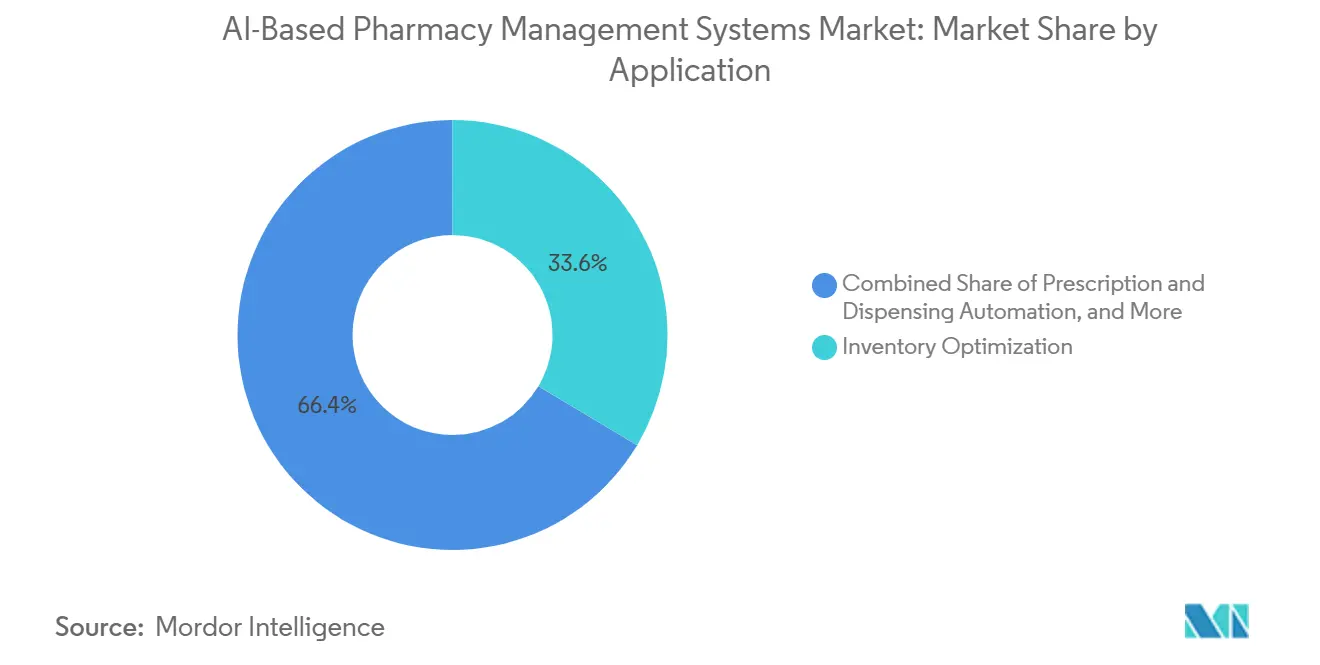

- By application, inventory optimization represented 33.56% of the AI-based pharmacy management systems market size in 2025, while prescription and dispensing automation is projected to rise at 19.86% through 2031.

- By end user, hospital and inpatient pharmacies held 48.21% share in 2025, while retail pharmacies are expected to record the highest CAGR at 21.82% through 2031.

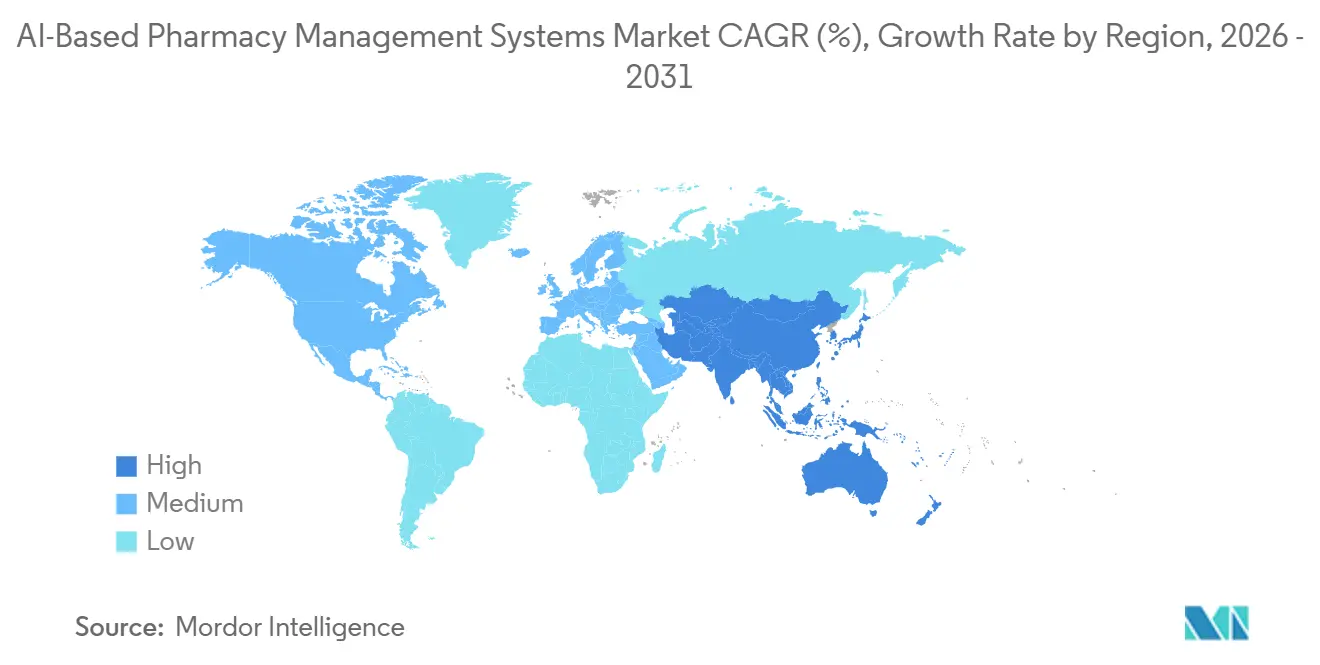

- By geography, North America captured 36.23% of the AI-based pharmacy management systems share in 2025, while Asia-Pacific is projected to expand at 22.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI-Based Pharmacy Management Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prescription Volumes and Pharmacist Workload | +3.2% | North America, Europe, APAC | Medium term (2-4 years) |

| Shift Toward Cloud-Based Pharmacy Platforms | +2.8% | North America (leading), Europe, APAC | Short term (≤ 2 years) |

| Need for Workflow Automation And Medication-Error Reduction | +3.5% | Global | Short term (≤ 2 years) |

| AI-Led Inventory Optimization and Shortage Response | +4.1% | North America, Europe, APAC core, spill-over to MEA | Medium term (2-4 years) |

| DSCSA Traceability and EPCIS Readiness | +1.9% | North America primarily, EU spillover | Short term (≤ 2 years) |

| ePA, RTPB, and Interoperability-Led Workflow Intelligence | +2.5% | North America (US primary), APAC spillover | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prescription Volumes and Pharmacist Workload

The AI-based pharmacy management systems market is gaining support from a workload problem that is becoming permanent rather than temporary. Pharmacy operators are under pressure to process more prescriptions, manage more patient records, and respond faster to benefit and authorization questions on the same staffing base. This makes automation valuable because the software can absorb repetitive verification and documentation steps that would otherwise take a pharmacist's time. Nihon Chouzai expanded its AI medication history creation support service to all 763 stores in May 2025 after a pilot confirmed lower documentation burden and better pharmacist-patient interaction quality.[1]日本調剤, “日本調剤、AI薬歴作成支援サービス「corte」を全店舗に導入へ,” Nihon Chouzai Once buyers treat AI as a capacity tool instead of a discretionary upgrade, contract duration, per-seat pricing, and renewal stability tend to improve.

Shift Toward Cloud-Based Pharmacy Platforms

The AI-based pharmacy management systems market is also advancing because cloud deployment is now a practical operating model for mainstream pharmacy networks. Amazon Pharmacy reported a 90% improvement in prescription processing time and cut development timelines from 9 months to 3 months after moving generative AI workloads onto AWS cloud infrastructure.[2]Alexandre Alves, “Amazon Pharmacy Improved Prescription Processing Time by 90% With Gen AI,” In another cloud-based implementation, Malaysia’s largest prescription pharmacy network increased daily order fulfillment from 500 to 4,000 units and improved picker productivity by 80% after centralizing warehouse operations on AWS-enabled systems.[3]Gayathiri Anpalakan and Vinay Agrawal, “Pharmacy in the Cloud, AWS Transforms Medication Safety and Operations,” CGM LAUER also introduced CGM STELLA for national rollout in Germany from June 2025, giving pharmacies a browser-based AI-supported platform aligned with DSGVO and BSI C5 security expectations.[4]CompuGroup Medical, “CGM STELLA® Die Cloudbasierte Apothekensoftware Steht Zur Verfügung,”

Need for Workflow Automation and Medication-Error Reduction

The AI-based pharmacy management systems market is benefiting from the direct link between automation and patient safety. Stanford reported in August 2025 that prescription errors in the United States cause at least 1.5 million preventable adverse events and create annual costs of USD 3.5 billion. A study in Nature Medicine found that large language model tools inside Amazon Pharmacy workflows reduced direction-related near-miss events by 33%, lowered post-adoption edits by technicians by 44.3%, and improved technician adoption by 28.5%. A February 2026 peer-reviewed review also found that Bayesian neural networks, deep-learning image classification, and robotic dispensing can detect look-alike and sound-alike medication risks that manual checking misses more often. Buyers are therefore putting more weight on clinically documented error reduction because procurement teams now prefer evidence from peer-reviewed and academic sources over simple vendor performance claims.

AI-Led Inventory Optimization and Shortage Response

The AI-based pharmacy management systems market is seeing strong interest from pharmacy operators that want better control over inventory risk and shortage response. Inventory management matters because shortages, waste, and emergency purchasing all weaken margins and disrupt patient care when pharmacies are already working with limited labor. Amazon Pharmacy reported that its cloud-based planning environment improved demand-planning forecast accuracy by 50% against standard targets and reduced weekly planning time by 13%. RedSail said in February 2026 that PrimeRx’s embedded real-time pharmaceutical marketplace can help pharmacies save more than USD 30,000 per month in inventory costs, which shows why inventory intelligence is moving closer to the center of dispensing workflows. Vendors with larger installed bases are in a stronger position because broader transaction and procurement signals tend to improve planning quality across the network over time.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Implementation and Integration Costs | -2.8% | Global, most acute in SME and community pharmacy segments | Medium term (2-4 years) |

| Cybersecurity and Patient-Data Privacy Exposure | -2.4% | Global | Short term (≤ 2 years) |

| Legacy Interoperability and Standards-Migration Friction | -2.1% | North America, Europe | Medium term (2-4 years) |

| Clearinghouse Concentration and Outage Dependence | -1.8% | North America primarily | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Implementation and Integration Costs

The AI-based pharmacy management systems market still faces a major adoption barrier in the form of uneven implementation economics. Large health systems and national retail chains can spread software, integration, retraining, hardware, and facilities costs across many dispensing locations, while independent operators often cannot. The full cost of adoption also extends beyond licensing because pharmacies need EHR integration, workflow redesign, data migration, and ongoing model maintenance after launch. This creates a bifurcated market in which enterprise buyers access advanced platform capabilities first, while many community pharmacies remain limited to lower-cost tools with narrower functionality. The gap also leaves room for modular SaaS offerings, but the market has not yet produced a dominant, scaled provider focused on that white space.

Cybersecurity and Patient-Data Privacy Exposure

The AI-based pharmacy management systems market carries a large security burden because pharmacy platforms now connect with EHRs, payer systems, wholesaler networks, and third-party transaction services. Nixon Peabody stated in November 2025 that the February 2024 Change Healthcare ransomware attack exposed data for an estimated 193 million individuals and disrupted pharmacy claims nationwide for weeks. MedImpact also disclosed a cybersecurity incident in October 2025 and said certain systems were affected, with restoration taking place in a new, segregated environment. These events show that the value of AI-enabled workflow connectivity rises alongside exposure to operational outages and data loss. Procurement teams are therefore treating certifications, incident response design, and secure architecture as core purchase criteria rather than back-end technical details.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominates While Services Emerge as the High-Growth Revenue Layer

Software accounted for 72.34% of spending in 2025, giving it the largest share of the AI-based pharmacy management systems market because pharmacies usually digitize core workflows before they purchase deeper services around those workflows. This pattern reflects a practical buying sequence in which prescription management, decision support, inventory tools, and prior authorization automation become the base layer for later optimization. The software category is attracting continued development because buyers want modular systems that can add AI features without a full platform replacement. Omnicell introduced OmniSphere in December 2024 as a cloud-native environment that connects robotics, smart devices, and AI analytics in one HITRUST-certified platform, which shows how vendors are trying to expand software control across the full medication workflow. In the AI-based pharmacy management systems industry, this concentration around software also gives leading platform providers more control over adjacent revenue streams such as analytics, managed support, and compliance tools.

Services are smaller in absolute value, but they are projected to advance at 19.32% CAGR through 2031, which makes them the fastest-growing revenue layer in the AI-based pharmacy management systems market. This growth reflects the reality that many pharmacy IT teams do not have enough internal data science, interoperability, and model management capacity to run complex AI systems on their own. Buyers increasingly want managed support for retraining, optimization, and standards-based integration rather than maintaining those capabilities in-house. Inovalon said in February 2026 that ScriptMed specialty and infusion pharmacy software was scaled on Oracle Autonomous AI Database, which illustrates the move toward outsourced infrastructure and managed performance delivery for complex pharmacy environments. As this model spreads, recurring service contracts will make vendor revenue less dependent on one-time implementation cycles and periodic hardware refreshes.

By Deployment Model: Cloud's Scale Advantage Coexists with an On-Premise Compliance Premium

Cloud and SaaS deployments represented 63.85% of the market in 2025, which means they held the leading AI-based pharmacy management systems market share at the deployment level. Buyers continue to prefer cloud systems because they avoid local hardware dependence, support faster upgrades, and let centralized teams manage multiple sites from one interface. Amazon Pharmacy’s AI stack on AWS improved prescription processing time by 90%, and its cloud planning tools also improved demand-planning forecast accuracy by 50% against standard targets. These results matter because the AI-based pharmacy management systems market now rewards platforms that can update models, workflows, and compliance functions across the customer base without long release cycles. Cloud architecture also improves vendor responsiveness because improvements can be pushed across many locations at once instead of being installed site by site.

On-premise deployments are forecast to grow at 20.47% through 2031, which makes them the fastest-growing deployment sub-segment, even though cloud remains the larger category. This growth is concentrated in highly regulated settings where data localization, privacy expectations, and internal governance make public cloud less acceptable for sensitive patient information. CGM STELLA’s rollout in Germany and its alignment with DSGVO and BSI C5 requirements show why compliance design now shapes deployment preference as much as technical performance Wemex also announced in September 2025 a generative AI medication guidance support function for pharmacies in Japan, reflecting a market that is trying to balance AI use with domestic regulatory expectations around health data handling. The AI-based pharmacy management systems industry is therefore favoring hybrid architectures because they let vendors combine scalable analytics with stricter local control over protected patient data.

By Application: Inventory Optimization Anchors Market Spend While Dispensing Automation Captures Growth Investment

Inventory optimization held 33.56% of the application mix in 2025, which gave it the largest AI-based pharmacy management systems market size among application areas. The reason is straightforward because inventory errors, shortages, expiry, and emergency procurement directly affect both service quality and margin performance. Buyers can usually justify this application more quickly than others because the savings from better planning and replenishment are visible to finance teams as well as pharmacy leaders. Amazon Pharmacy’s cloud-based planning environment improved forecast accuracy and cut weekly planning time, which strengthens the value case for AI-led inventory tools inside large pharmacy operations. RedSail’s February 2026 acquisition statement also highlighted the inventory savings potential of more than USD 30,000 per month through embedded marketplace functionality, which shows that inventory intelligence is moving closer to the dispensing workflow instead of remaining a separate back-office task.

Prescription and dispensing automation is projected to expand at 19.86% through 2031, making it the fastest-growing application in the AI-based pharmacy management systems market. Growth is being driven by the combination of direction validation, computer vision, robotics, and AI-assisted task management inside both central and point-of-care pharmacy workflows. The Nature Medicine study on medication direction errors supports this movement because it showed measurable production benefits from large language model integration in real dispensing operations. Snowisdom reported in June 2025 that its pharmacy robot picker can complete drug positioning and verification in 15 seconds with an error rate below 1 in 100,000, which reflects the direction of high-throughput automation investment. Medication therapy management, adherence support, telepharmacy coordination, and 340B software remain important adjacent niches because buyers still want specialized tools where large platforms have not fully standardized workflow needs.

By End User: Hospital Pharmacies Set Clinical Standards While Retail Networks Drive Volume Growth

Hospital and inpatient pharmacies held 48.21% share in 2025, so they represented the largest end-user base in the AI-based pharmacy management systems market. Hospitals invest earlier because patient safety, regulatory scrutiny, and medication management complexity make AI adoption harder to defer in inpatient settings. These environments also benefit from centralized planning models that connect dispensing, replenishment, and floor-level medication workflows in a single control structure. Omnicell launched Titan XT in December 2025 with AI-driven inventory prediction and DynamicRestock task management, and the company stated that the system can save pharmacy technicians 70% of task time. Specialty pharmacies also stand out within this end-user group because biologics, infusion therapy, cold-chain control, and prior authorization complexity support premium platform pricing.

Retail pharmacies are forecast to grow at 21.82% through 2031, which makes them the fastest-growing end-user segment in the AI-based pharmacy management systems market. Their growth reflects the need to process high prescription volumes with leaner staffing structures and more centralized workflow control. This operating model favors platforms that can support central fill, patient communication, delivery coordination, and inventory visibility across broad store networks. RedSail’s acquisition of PrimeRx expanded its network to nearly 16,000 pharmacies and 50 million active patients, which shows how scale platforms are being assembled to bring stronger technology to community and independent operators. The segment also remains diverse because long-term care, specialty, and smaller independent pharmacy settings still need workflow features that differ from those of national chain stores.

Geography Analysis

North America held 36.23% of global revenue in 2025, which gave the region the largest AI-based pharmacy management systems market share. The United States drives most of that position because its prescription volume, payer infrastructure, and interoperability mandates create stronger demand for workflow intelligence inside pharmacy systems. The ONC HTI-4 Final Rule, finalized in July 2025, requires RTPB and FHIR-based electronic prior authorization capabilities in Base EHR systems from January 1, 2028. That rule matters because it pushes pharmacy-related workflows toward real-time data use rather than manual follow-up, which supports deeper AI integration in existing platforms. Regional growth is therefore coming more from capability expansion inside installed systems than from first-time digitization.

Europe is following a more compliance-centered path in the AI-based pharmacy management systems market. Western Europe is adopting AI-enabled workflow tools, but deployment choices are shaped by privacy, data residency, and security standards as much as by performance. CGM LAUER launched CGM STELLA in 2025 as Germany’s first cloud-based AI-supported pharmacy management system built for national rollout and aligned with BSI C5 expectations. This suggests that vendors with certified cloud, private cloud, or hybrid options are better placed than those offering only one deployment model. European demand is therefore steady, but contract wins depend heavily on whether suppliers can satisfy local compliance rules without reducing pharmacy workflow speed.

Asia-Pacific is projected to record the fastest regional CAGR at 22.54% through 2031, giving it the strongest growth profile in the AI-based pharmacy management systems market. Japan is already showing structured adoption because the Ministry of Health, Labour and Welfare issued a second version of AI-in-healthcare guidance in July 2025, which gave providers a clearer framework for deployment. Nihon Chouzai’s rollout of AI medication history creation support across all 763 pharmacies in May 2025 shows how that policy support is translating into enterprise deployment decisions. The region also benefits from widening digital health infrastructure in large markets and from the appeal of mobile-first and cloud-first implementation models where local server investment is less attractive. Over time, this combination of policy support, infrastructure buildout, and workflow demand should make Asia-Pacific a larger share of future revenue than current figures suggest.

Competitive Landscape

The AI-based pharmacy management systems market is moderately consolidated in hospital automation hardware, but it remains highly fragmented in retail and community pharmacy software. A limited group of vendors, including Omnicell, Becton Dickinson, and Swisslog Healthcare, hold meaningful positions where integrated automation hardware and enterprise medication workflows are critical. The software side is more dispersed because many local and regional providers still serve community pharmacy customers with narrower functional depth. This split means competitive strength depends heavily on customer type, deployment model, and whether the buyer values hardware integration or workflow flexibility more.

Omnicell is pushing a platform strategy that links robotics, dispensing, analytics, and recurring services inside one cloud-supported environment. The company said in February 2026 that it had a USD 640 million product backlog and USD 636 million in annual recurring revenue, while also outlining a plan to increase the weight of SaaS and managed services in its revenue mix. That strategy matters because buyers increasingly prefer vendors that can support long operating relationships instead of one-time equipment installations. Swisslog Healthcare is also widening its reach through product and partnership moves rather than relying only on traditional dispensing hardware. Its alliance with Diligent Robotics, announced in 2025, extends pharmacy automation into hospital logistics and shows how vendors are trying to connect the pharmacy bay with broader medication movement across the facility.

AI-Based Pharmacy Management Systems Industry Leaders

ARxIUM Inc.

Becton, Dickinson and Company

Swisslog Healthcare AG

Oracle Health

Epic Systems Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: RedSail Technologies completed its acquisition of PrimeRx as an affiliate, expanding its pharmacy software network to approximately 16,000 pharmacies nationwide and 50 million active patients. The deal integrates PrimeRx's marketplace and delivery solutions, including the first-ever real-time pharmaceutical marketplace embedded in a dispensing workflow, enabling pharmacies to save over USD 30,000 per month in inventory costs, with RedSail's PioneerRx, BestRx, and Axys brands.

- February 2026: Inovalon was recognized as Oracle's "Global Leaders Champion" for scaling ScriptMed specialty and infusion pharmacy management software on Oracle Autonomous AI Database on Oracle Cloud Infrastructure, providing specialty and infusion pharmacies a scalable platform for rapidly growing transaction volumes and complex therapy management.

- December 2025: Omnicell commercially launched Titan XT, a next-generation enterprise automated dispensing system powered by the HITRUST-certified OmniSphere cloud-native platform, offering AI-driven inventory prediction, DynamicRestock task management, and 70% time savings for pharmacy technicians. Initial hardware shipments are scheduled for H2 2026, representing a USD 2.5 billion replacement opportunity.

- December 2025: Swisslog Healthcare unveiled Allegro, a modular automated high-density inventory solution with an all-electric design and web-based platform enabling remote access and seamless integration with clinical information systems, presented at the ASHP Midyear Clinical Meeting in Las Vegas.

Global AI-Based Pharmacy Management Systems Market Report Scope

As per the scope of the report, AI-based pharmacy management systems are intelligent healthcare software solutions that use artificial intelligence and machine learning to optimize pharmacy operations within healthcare facilities. They help automate medication dispensing, inventory forecasting, prescription validation, and clinical drug decision support. These systems also reduce medication errors by enabling real-time drug interaction checks and dosage recommendations. Overall, they enhance efficiency, safety, and accuracy across hospital and retail pharmacy workflows.

The AI-based pharmacy management systems are segmented by component, deployment model, application, end user, and geography. By component, the market is segmented into software and services. By deployment model, the market is segmented into cloud-based / SaaS and on-premise. By application, the market is segmented into prescription & dispensing automation, inventory optimization, billing, claims & revenue cycle, medication therapy management and adherence, and others. By end user, the market is segmented into retail pharmacies, hospital/inpatient pharmacies, specialty pharmacies, and others. The geography segment is further divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market size and forecasts in value (USD) for the above segments.

| Software |

| Services |

| Cloud-Based / SaaS |

| On-Premise |

| Prescription & Dispensing Automation |

| Inventory Optimization |

| Billing, Claims & Revenue Cycle |

| Medication Therapy Management and Adherence |

| Others |

| Retail Pharmacies |

| Hospital / Inpatient Pharmacies |

| Specialty Pharmacies |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| By Deployment Model | Cloud-Based / SaaS | |

| On-Premise | ||

| By Application | Prescription & Dispensing Automation | |

| Inventory Optimization | ||

| Billing, Claims & Revenue Cycle | ||

| Medication Therapy Management and Adherence | ||

| Others | ||

| By End User | Retail Pharmacies | |

| Hospital / Inpatient Pharmacies | ||

| Specialty Pharmacies | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving adoption of AI-based pharmacy management systems in 2026?

Adoption is being driven by rising prescription volumes, pharmacist workload, the push for workflow automation, and the need to reduce medication errors while improving inventory planning.

How large is the AI-based pharmacy management systems space expected to become by 2031?

It is forecast to reach USD 55.37 billion by 2031, up from USD 23.91 billion in 2026, which reflects an 18.29% CAGR over 2026-2031.

Why are cloud deployments leading adoption in pharmacy software?

Cloud and SaaS held 63.85% of the market in 2025 because they enable faster deployment, centralized updates, and easier scaling across large pharmacy networks.

Which application area currently leads spending?

Inventory optimization led with 33.56% of application spending in 2025 because it directly addresses shortage risk, waste, and emergency purchasing costs.

Which end-user group is growing the fastest through 2031?

Retail pharmacies are projected to grow at 21.82% CAGR through 2031 as operators centralize workflows and use automation to manage high script volumes with lean staffing.

Which region offers the strongest growth outlook?

Asia-Pacific has the fastest projected regional CAGR at 22.54% through 2031, supported by policy momentum, digital health expansion, and enterprise adoption in markets such as Japan.

Page last updated on: