AI-Powered Behavioral Therapy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

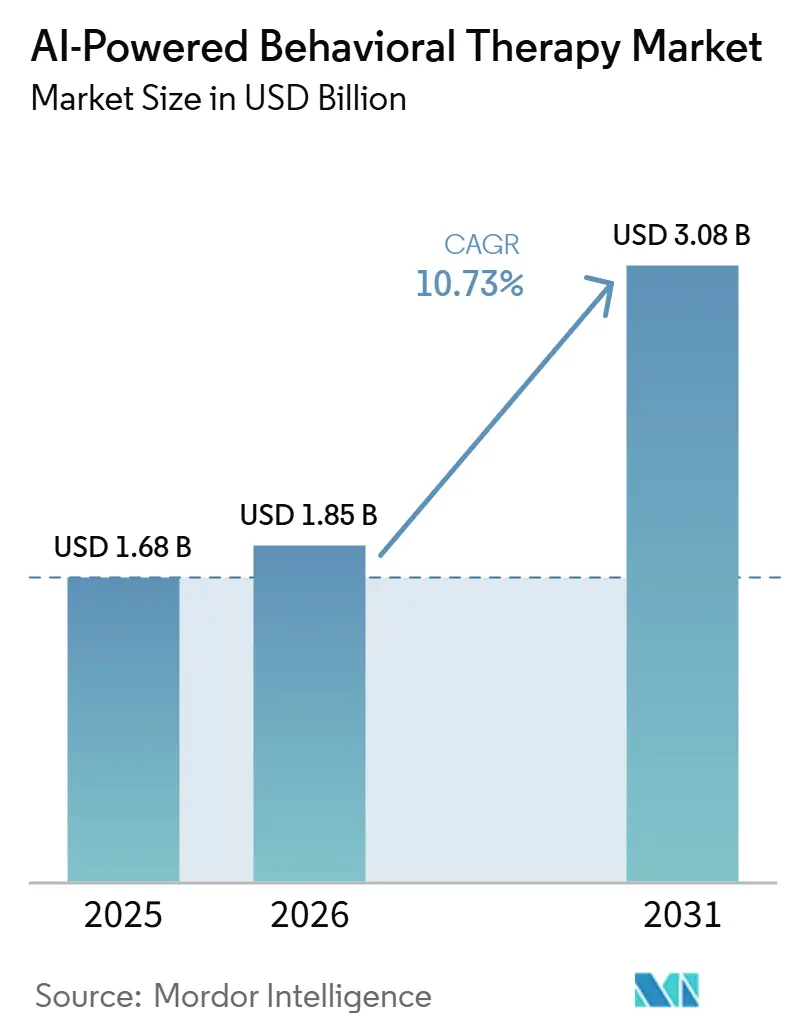

| Market Size (2026) | USD 1.85 Billion |

| Market Size (2031) | USD 3.08 Billion |

| Growth Rate (2026 - 2031) | 10.73% CAGR |

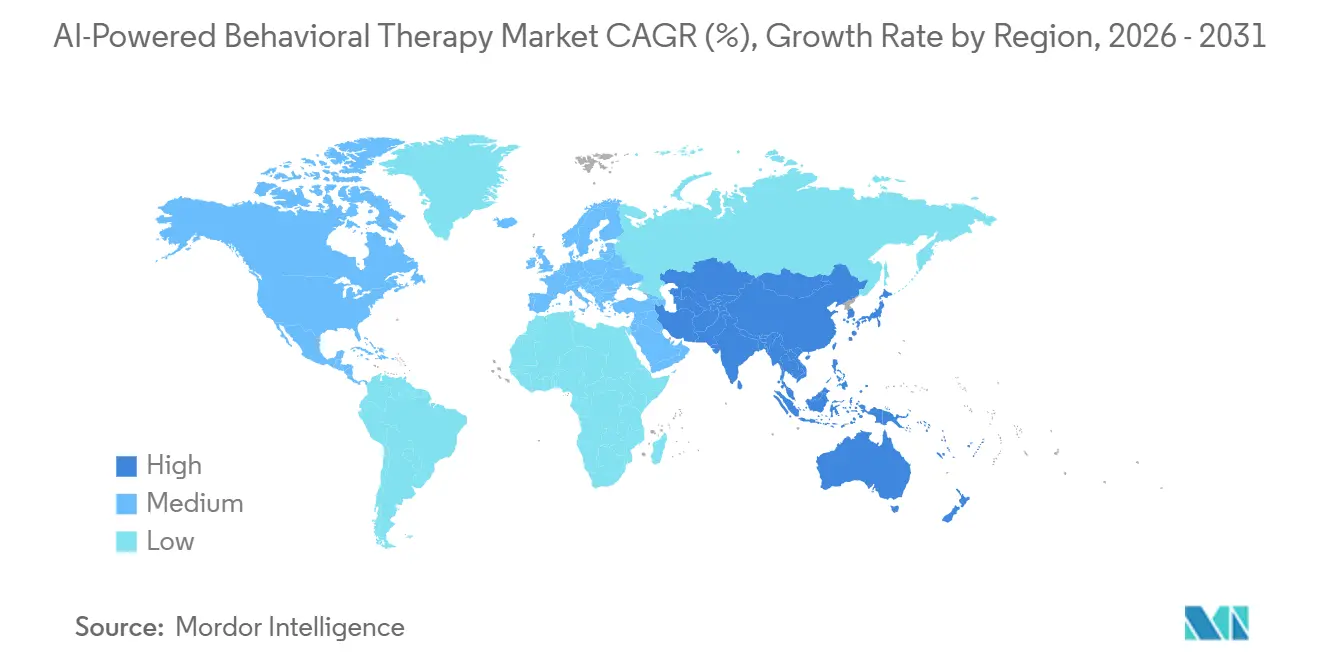

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

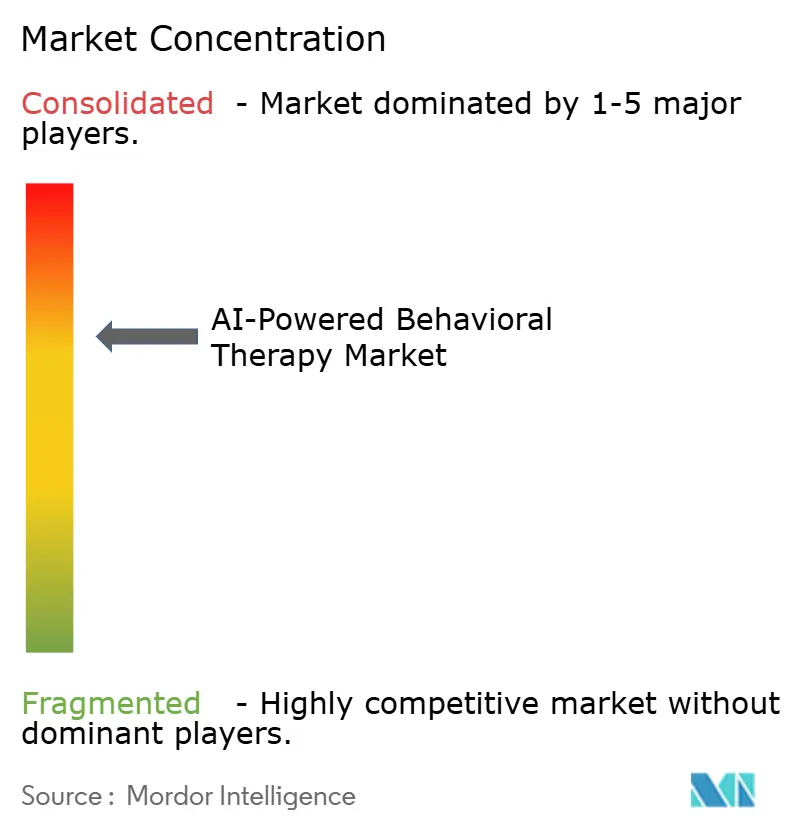

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI-Powered Behavioral Therapy Market Analysis by Mordor Intelligence

The AI-powered behavioral therapy market is expected to grow from USD 1.68 billion in 2025 to USD 1.85 billion in 2026 and is forecast to reach USD 3.08 billion by 2031 at 10.73% CAGR over 2026-2031. The AI-powered behavioral therapy market is moving on the back of a structural shortage in conventional behavioral care capacity rather than a short-term rise in app usage, as mental health shortage areas in the United States continued to widen and national need remained far above available provider supply. The policy backdrop is also becoming more supportive, with CMS creating the first direct Medicare reimbursement framework for digital mental health treatment devices in 2025 and opening the door to broader behavioral use cases in 2026. Employer benefit design is reinforcing the same direction, because large employers have expanded mental health coverage while benefits leaders report that workforce performance is being materially affected by unmet mental health needs. The AI-powered behavioral therapy market is therefore benefiting from a rare alignment of provider scarcity, payer experimentation, and employer demand, which is shifting digital behavioral tools from optional wellness products toward operational care infrastructure. Competitive positioning is also changing, because larger platforms are combining AI triage, contracted provider networks, and reimbursement readiness, while regulators are beginning to separate clinically governed products from unclassified wellness tools.

Key Report Takeaways

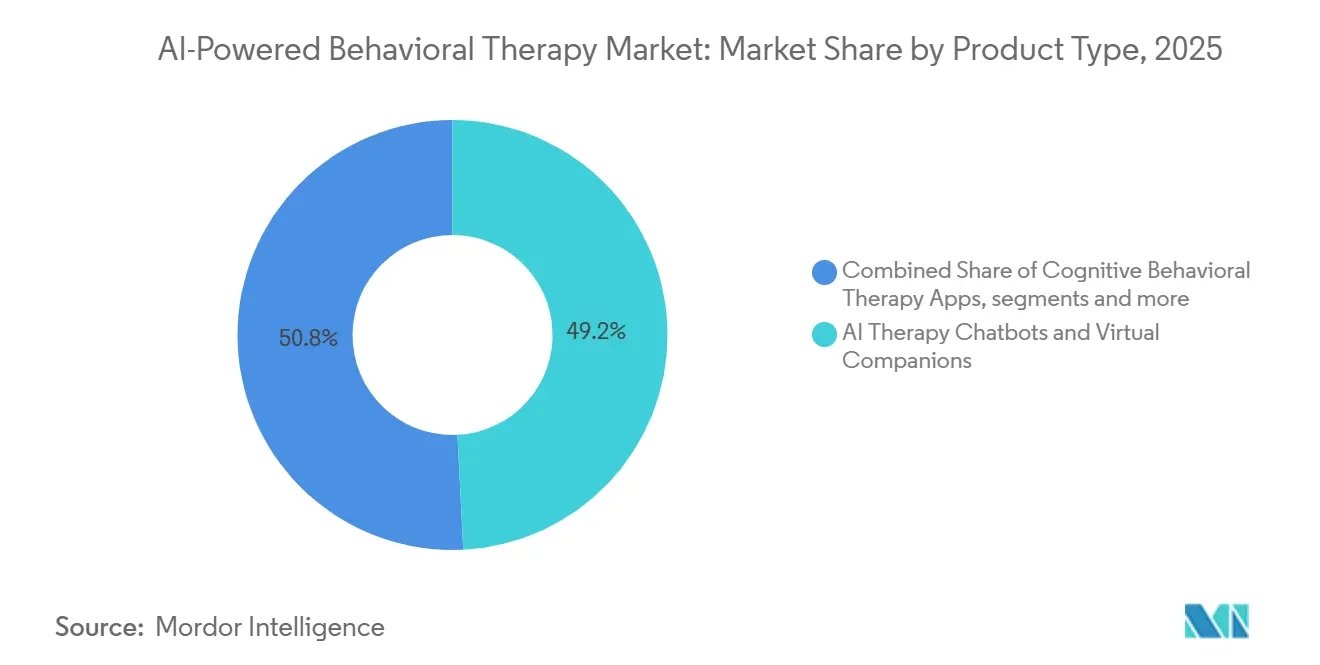

- By product type, AI therapy chatbots and virtual companions led with 49.23% of revenue in 2025, while CBT apps are forecasted to expand at 11.33% CAGR through 2031.

- By deployment mode, cloud-based platforms held 62.17% of revenue in 2025 and are also expected to be the fastest-growing deployment mode at 11.68% CAGR through 2031.

- By application, anxiety and depression accounted for 41.71% of revenue in 2025, while ADHD and cognitive disorders are expected to advance at 12.47% CAGR through 2031.

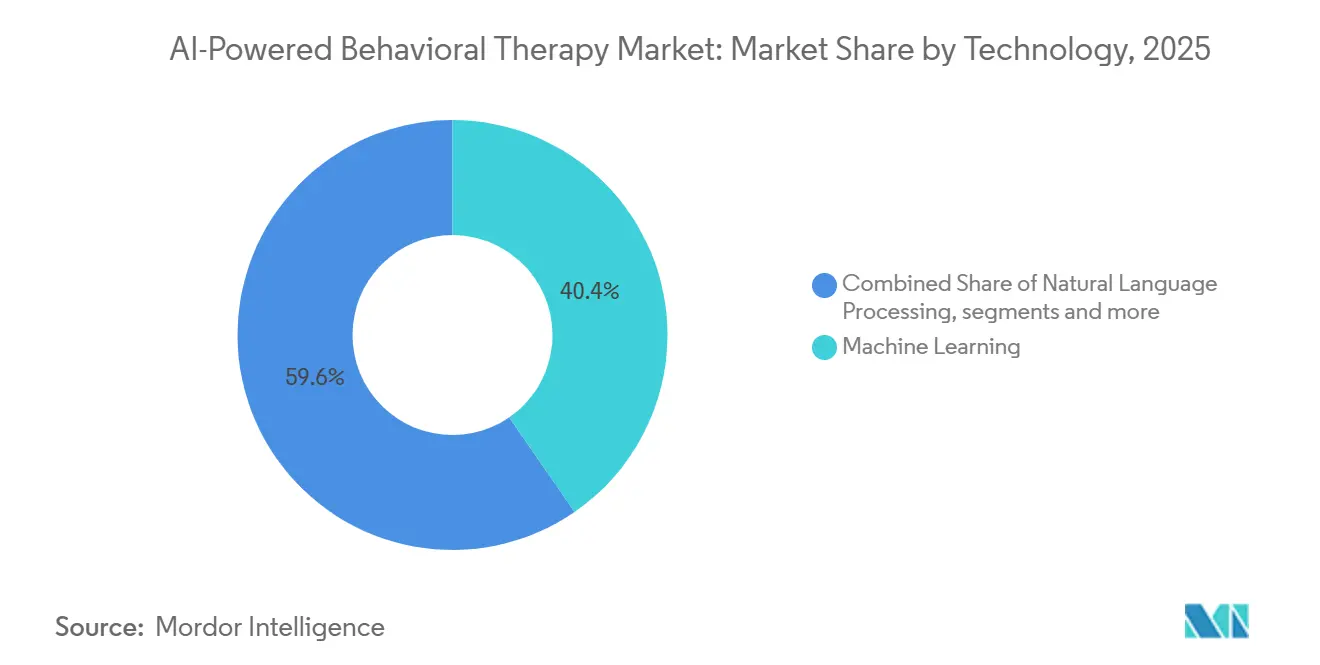

- By technology, machine learning held 40.37% of revenue in 2025, while emotion AI and affective computing are forecasted to grow at 12.11% CAGR through 2031.

- By end-user, individuals held 41.12% of revenue in 2025, while mental health clinics and hospitals are expected to expand at 13.13% CAGR through 2031.

- By geography, North America accounted for 51.55% of global revenue in 2025, while Asia-Pacific is projected to grow at 14.27% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI-Powered Behavioral Therapy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Scalable Mental Health Access | +2.5% | Global, most acute in North America and South Asia | Short term (≤ 2 years) |

| Employer-Grade Behavioral Care Benefits Expansion | +1.8% | North America & Europe | Short term (≤ 2 years) |

| AI-Assisted Clinical Triage for Shorter Wait Times | +1.5% | Global, early scaling in APAC | Medium term (2-4 years) |

| Under-Supplied Specialist Capacity in High-Burden Conditions | +2.0% | Global, most severe in non-metropolitan North America and South/Southeast Asia | Long term (≥ 4 years) |

| Reimbursement Acceptance for Digital Behavioral Interventions | +1.7% | North America, expanding to EU via Germany's DiGA and UK NHS | Medium term (2-4 years) |

| Multimodal Emotion AI Improving Engagement and Adherence | +1.0% | Global, early adoption in North America, South Korea, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Scalable Mental Health Access

The supply and demand gap in behavioral care has widened to a point that conventional hiring alone is unlikely to close in a commercially relevant period. Late 2024 data showed 6,807 designated mental health professional shortage areas in the United States, covering 137 million people, with only 27.3% of mental health needs being met and 6,800 additional practitioners needed just to remove existing shortage designations.[1]Alex Kacik, “Mental Healthcare Provider Gaps, by State,” Becker's Behavioral Health, beckersbehavioralhealth.com Separate workforce modeling projects a decline in U.S. adult psychiatrist supply from 37,470 full-time equivalents in 2026 to 36,550 by 2038, even as annual demand rises to 73,330 and workforce adequacy falls from 71.9% to 49.8%.[2]A. Satiani et al., “Supply, Demand, and Adequacy of the Adult Psychiatry Workforce in the United States, Projecting a Shortage to 2038,” Psychiatric Services, sciencedirect.com That imbalance makes the AI-powered behavioral therapy market structurally necessary for mild and moderate presentations, because digital tools can extend access without waiting for the workforce base to expand. The commercial implication is strongest in rural and non-metropolitan areas, where workforce adequacy is already far below metropolitan levels and the cost of in-person service expansion is harder to justify. In this setting, the AI-powered behavioral therapy market is gaining traction not because care systems prefer automation, but because the alternative is persistent untreated demand.

Employer-Grade Behavioral Care Benefits Expansion

Employer purchasing has become one of the clearest near-term distribution channels for the AI-powered behavioral therapy market. Lyra Health reported in March 2026 that 1 in 3 workers was merely surviving mentally and that 69% of benefits leaders said mental health challenges were materially reducing employee performance.[3]Lyra Health, “2026 State of Workforce Mental Health Report, The Workforce Mental Health Paradox,” Lyra Health, lyrahealth.comA cohort study covering 589 U.S. employers using Spring Health’s platform found that employer-sponsored digital mental health delivery produced recovery and remission outcomes aligned with evidence-based therapy norms. Businessolver’s 2025 benefits survey also found that employee assistance programs ranked among the top 3 desired benefits, while employer coverage for mental health continued to broaden across large organizations. This is shifting channel power away from consumer app stores and toward payer, employer, and HR technology ecosystems that can buy at scale. As a result, the AI-powered behavioral therapy market is increasingly favoring vendors that can show enterprise-grade reporting, navigation, and outcomes tracking rather than only daily user engagement.

AI-Assisted Clinical Triage for Shorter Wait Times

The AI-powered behavioral therapy market is also being lifted by tools that reduce the lag between intake and clinically appropriate care. A study in an outpatient Canadian psychiatric setting found that AI-assisted routing recommendations aligned closely with psychiatrist decisions, showing that care intensity can be matched accurately without requiring a specialist at the first step. Limbic Access, deployed across UK NHS Talking Therapies services, has screened more than 210,000 patients with 93% accuracy, which shows that AI-supported triage is already moving beyond pilot use and into scaled service environments. In many care settings, behavioral appointment waits still stretch to 25 days or more, which raises the risk of dropout before patients reach the right level of support. Triage tools matter because they reduce the amount of specialist time spent on intake sorting and redirect that time toward higher-acuity cases. That productivity effect strengthens the AI-powered behavioral therapy market because purchasers can link digital deployment to faster access, better routing, and lower waste in care pathways.

Under-Supplied Specialist Capacity in High-Burden Conditions

The AI-powered behavioral therapy market is also being supported by shortages in complex and high-burden conditions, where specialist capacity is under the most pressure. Psychiatric workforce modeling indicates that U.S. non-metropolitan regions already sit at 34.8% adequacy, while national adequacy is projected to continue falling over the next decade. California alone projected a need for 3,782 additional psychiatrists in 2025, with demand rising further to 2033 across all 58 counties. Several states are facing shortages across psychiatric hospitals, community providers, and crisis systems at the same time, which limits the system’s ability to absorb more demand even when screening improves. In practical terms, AI platforms are being positioned as a functional buffer for lower-acuity cases so specialist capacity can be reserved for severe presentations, substance use, PTSD, and other complex needs. That makes the AI-powered behavioral therapy market relevant not only for access expansion, but also for capacity protection inside provider systems that cannot scale specialist supply fast enough.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clinical Validation and Outcome Attribution Gaps | -1.6% | Global, most constraining in North America and Europe | Medium term (2-4 years) |

| Privacy Sensitivity of Psychiatric and Behavioral Data | -1.3% | Global, most acute in EU and North America | Long term (≥ 4 years) |

| Model Hallucination and Unsafe Escalation Risk | -1.0% | Global | Short term (≤ 2 years) |

| Workflow Friction in Provider and Payer Integration | -0.7% | North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Clinical Validation and Outcome Attribution Gaps

Clinical evidence remains one of the main factors slowing broader institutional adoption in the AI-powered behavioral therapy market. The FDA’s Digital Health Advisory Committee met in November 2025 to discuss generative AI-enabled mental health devices and recommended tools such as predetermined change control plans, randomized trials, and postmarket monitoring to manage model drift over time. Outcome attribution is also difficult when a patient improves in a mixed-care setting that includes a therapist, an app, medication, and employer navigation support at the same time. That uncertainty slows procurement because buyers want to know what part of the result belongs to the platform itself. Until real-world outcomes become easier to isolate and compare, the AI-powered behavioral therapy market will continue to face more caution from payers and clinical buyers than the underlying demand picture would otherwise suggest.

Privacy Sensitivity of Psychiatric and Behavioral Data

Psychiatric and behavioral data creates a higher trust burden than most other digital health categories, which makes privacy a meaningful restraint on the AI-powered behavioral therapy market. Multimodal systems can capture voice features, text patterns, facial signals, sleep information, and behavioral rhythms, creating longitudinal personal profiles that are more revealing than standard medical records. A 2026 survey of 3,800 European youth found that 48% had used AI conversational tools to discuss personal emotional issues, often without a clear understanding of how their data would be processed or stored. That disconnect matters because behavioral data can trigger concern from users, employers, regulators, and providers at the same time. It also raises the cost of expansion into tightly regulated regions where transparency, oversight, and storage controls are reviewed closely before clinical adoption is allowed. As more platforms move from wellness positioning into treatment pathways, privacy governance will play a larger role in deciding which vendors the AI-powered behavioral therapy market treats as scalable care partners.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: AI Chatbots Anchor Revenue, CBT Apps Gain Ground

AI therapy chatbots and virtual companions held 49.23% of the AI-powered behavioral therapy market share in 2025, making them the largest product type by revenue. Their lead reflects 24/7 availability, low marginal interaction cost, and a format that can be deployed across employer, payer, and direct consumer channels without requiring large clinician capacity. The same pattern supports the AI-powered behavioral therapy market because chatbot products can expand access at scale while also building repeated engagement between formal care episodes.

Chatbots are also moving closer to care infrastructure than to stand-alone wellness tools. A randomized clinical trial also found that a conversational AI agent delivered greater anxiety reduction than group therapy, while stronger perceived therapeutic alliance predicted both engagement and symptom improvement. Cognitive behavioral therapy apps are the fastest-growing product type at 11.33% CAGR through 2031, which reflects stronger regulatory interest in structured protocol-based therapy software and a reimbursement environment that is becoming more open to digital adjuncts. Within the AI-powered behavioral therapy industry, that balance between conversational flexibility and structured CBT delivery is likely to define the next phase of product competition.

By Deployment Mode: Cloud Leads on Scale, On-Premises Retains Institutional Relevance

Cloud-based platforms commanded 62.17% share of the AI-powered behavioral therapy market size in 2025 and are also projected to grow at 11.68% CAGR through 2031. The lead comes from faster implementation, easier cross-device continuity, and the ability to update models and content centrally without disrupting the user experience. The AI-powered behavioral therapy market has favored cloud delivery because behavioral support depends on frequent interaction, real-time updates, and integration across mobile, web, and benefits channels.

On-premises deployment still matters in parts of the market where data residency, institutional control, and third-party processing limits remain strict. Government health systems, high-security psychiatric settings, and some European deployments continue to treat local control over sensitive behavioral information as a non-negotiable requirement. The AI-powered behavioral therapy market is therefore unlikely to move to a fully cloud-only structure, even if cloud remains the default for large-scale rollout. Instead, hybrid models are likely to persist because they let vendors serve enterprise buyers that want modern AI functionality without giving up direct control over sensitive data and governance workflows.

By Application: Anxiety and Depression Dominate, ADHD Rises on Policy Momentum

ADHD and cognitive disorders are forecast to grow at 12.47% CAGR through 2031, making them the fastest-growing application area in the AI-powered behavioral therapy market. Growth in this segment is being helped by broader policy attention to digital mental health treatment reimbursement and by growing interest in software-based care models for pediatric and neurodevelopmental use cases. User confidence in this area is also benefiting from structured therapy formats that are easier to standardize, monitor, and position within regulated treatment pathways.

Anxiety and depression held 41.71% share of the AI-powered behavioral therapy market size in 2025, keeping them as the largest application base. Their scale reflects the largest validated training pools, the most mature CBT content libraries, and the deepest precedent for digital delivery in mild and moderate presentations. Other areas such as PTSD, substance abuse, addiction, and sleep disorders remain important growth opportunities, but they still face more difficult validation and safety expectations. That leaves the AI-powered behavioral therapy market anchored by anxiety and depression while newer condition-specific use cases build evidence and reimbursement support.

By Technology: Machine Learning as Infrastructure, Emotion AI as Differentiator

Machine learning held 40.37% of market technology revenue in 2025, making it the core technology layer in the AI-powered behavioral therapy market. Its lead reflects broad use in pattern recognition, scoring, recommendation engines, and risk stratification across chatbots, CBT tools, triage systems, and monitoring applications. Machine learning also remains easier to explain and audit than more opaque approaches, which is valuable when payers, providers, and regulators want visibility into how a behavioral recommendation was generated.

Emotion AI and affective computing is projected to grow at 12.11% CAGR through 2031, making it the fastest-growing technology category. Research in this area points to stronger engagement potential because multimodal systems can adjust prompts and support intensity based on inferred emotional state rather than only on declared symptoms. NLP remains a critical middle layer because it powers conversational interfaces and allows semantic analysis of therapy dialogue, with recent work showing strong multi-label emotion detection in psychotherapy text. Within the AI-powered behavioral therapy industry, the technology stack is therefore settling into a clear pattern where machine learning provides the operating base, NLP enables language interaction, and emotion AI creates room for differentiation.

By End-User: Individual Adoption as Base, Clinical Channels Drive Premium Growth

Mental health clinics and hospitals are expected to be the fastest-growing end-user segment at 13.13% CAGR through 2031, which shows how the AI-powered behavioral therapy market is moving deeper into formal care settings. Growth in this channel reflects demand for tools that can support intake, triage, documentation, navigation, and patient follow-up while fitting into governed clinical workflows. As deployment shifts toward provider organizations, vendors are being judged more heavily on escalation protocols, interoperability, privacy controls, and evidence quality than on app downloads alone.

Individuals still held the largest end-user share at 41.12% in 2025, reflecting the early period when consumer-facing subscription tools expanded faster than institutional channels. This base remains important because self-initiated use still creates the largest top-of-funnel for symptom tracking, psychoeducation, and low-acuity support. The AI-powered behavioral therapy market is therefore retaining a large individual user base while premium growth increasingly comes from channels that can embed digital tools into broader care and reimbursement pathways.

Geography Analysis

North America held 51.55% of the AI-powered behavioral therapy market share in 2025, giving the region the largest global position by revenue. The region’s lead comes from the strongest reimbursement infrastructure, the deepest employer-benefit adoption, and the clearest pressure to reduce behavioral care bottlenecks. U.S. mental health treatment costs also increased 10.9% from 2024 to 2025, which adds cost-containment pressure that can favor AI-supported lower-acuity models over specialist-only pathways. Canada and Mexico face similar provider shortages, but reimbursement systems for digital behavioral tools are still less developed, which keeps the regional story centered on the United States.

Europe does not lead on scale, but it remains important because regulatory structure is shaping which platforms can participate in the AI-powered behavioral therapy market. The United Kingdom introduced. Germany continues to matter because its digital therapeutic reimbursement system has become a reference point for structured clinical evidence and payer acceptance in Europe. The region is therefore acting less as a volume market today and more as a proving ground where compliance readiness and evidence discipline can determine market access.

Asia-Pacific is projected to grow at 14.27% CAGR through 2031, making it the fastest-growing region in the AI-powered behavioral therapy market. Growth is being supported by severe unmet need, lower specialist density in several major countries, and rising willingness to use AI tools as an early point of contact for mental health support. Japan’s first commercial pediatric ADHD digital therapeutic launch in 2026 also signals that more formal software-based behavioral treatment pathways are entering the region, even if reimbursement models remain uneven. South America and the Middle East and Africa remain earlier-stage opportunities, where digital health investment is improving but AI behavioral therapy-specific coverage structures are still less established than in North America and parts of Europe.

Competitive Landscape

The AI-powered behavioral therapy market shows moderate concentration at the top and clear fragmentation across the wider field of condition-specific apps, workflow tools, and wellness products. Larger vendors increasingly compete on payer contracts, provider network reach, clinical evidence, and operational integration rather than on model novelty alone. That dynamic is pushing the market toward platform competition, where scale and distribution matter more than a stand-alone chatbot feature set. The AI-powered behavioral therapy market is therefore separating into full-continuum behavioral platforms on one side and smaller point solutions on the other. This split is making it harder for pure direct-to-consumer products to defend position once enterprise buyers begin to prefer integrated contracting and governed escalation pathways.

Two transactions in 2026 show how quickly the upper tier is consolidating. Spring Health completed its acquisition of Alma in May 2026, creating a combined platform serving 120 million insured lives through national payer relationships and materially extending provider network depth. These moves strengthen buyers that can combine AI-native triage with contracted therapist supply, which is a structure that smaller single-function vendors struggle to match. The AI-powered behavioral therapy market is increasingly rewarding companies that can connect digital front doors to reimbursable downstream care.

Competitive differentiation is also moving toward evidence quality, workflow ownership, and regulatory readiness. Spring Health’s launch of Guide and Lyra Health’s global scaling of its clinically vetted AI Guide show that leading vendors are pairing AI rollout with outcome claims and enterprise distribution rather than positioning AI as a novelty feature. At the same time, regulatory scrutiny around hallucination risk, clinical oversight, and model updates is likely to favor vendors that can manage formal evidence generation and post-deployment governance. The AI-powered behavioral therapy market is still open to innovation, but the terms of competition are becoming more institutional, more compliance-oriented, and more difficult for lightly governed entrants to navigate.

AI-Powered Behavioral Therapy Industry Leaders

Woebot Health

Wysa Ltd.

Talkspace Inc.

Headspace Health, Inc.

Lyra Health, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Spring Health completed the acquisition of Alma, a platform connecting over 120 million insured lives with independent therapists through national payer contracts; the combined entity positions itself as the first "lifelong" AI-native mental health platform and materially expands Spring Health's provider network and care coordination capacity.

- May 2026: Lyra Health launched its Center of Excellence for Pediatric and Young Adult Mental Health, adding Behavioral Health Urgent Care, High-Risk Behavioral Skills Therapy, and Virtual Intensive Outpatient (vIOP) programs through a specialized network of over 15,500 providers globally, while simultaneously scaling its clinically vetted AI Guide to members worldwide.

- March 2026: Universal Health Services (UHS) announced a definitive agreement to acquire Talkspace for approximately USD 835 million enterprise value, marking a major health system's move to directly own digital behavioral therapy infrastructure as an integrated clinical asset.

Global AI-Powered Behavioral Therapy Market Report Scope

According to the report’s scope, the AI-powered behavioral therapy market refers to the market for artificial intelligence-driven software platforms, virtual assistants, digital therapeutics, and analytics solutions that support the assessment, monitoring, and treatment of behavioral and mental health conditions. These solutions leverage AI technologies such as machine learning, natural language processing, and generative AI to deliver personalized interventions, track patient progress, enhance clinical decision-making, and improve access to behavioral therapy services across healthcare and wellness settings.

The AI-powered behavioral therapy market is segmented into product type, deployment mode, application, technology, end-user, and geography. By product type, the market is segmented into AI therapy chatbots and virtual companions, cognitive behavioral therapy apps, AI-driven biofeedback devices, AI-powered sleep and stress management tools, and emotion recognition and monitoring systems. By deployment mode, the market is segmented into cloud-based and on-premises. By application, the market is segmented into anxiety and depression, ADHD and cognitive disorders, sleep disorders, substance abuse and addiction, and post-traumatic stress disorder. By technology, the market is segmented into machine learning, natural language processing, deep learning, and emotion AI and affective computing. By end-user, the market is segmented into individuals, mental health clinics and hospitals, corporate wellness providers, payers and insurers, and academic and research institutes. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| AI Therapy Chatbots and Virtual Companions |

| Cognitive Behavioral Therapy Apps |

| AI-Driven Biofeedback Devices |

| AI-Powered Sleep and Stress Management Tools |

| Emotion Recognition and Monitoring Systems |

| Cloud-Based |

| On-Premises |

| Anxiety and Depression |

| ADHD and Cognitive Disorders |

| Sleep Disorders |

| Substance Abuse and Addiction |

| Post-Traumatic Stress Disorder |

| Machine Learning |

| Natural Language Processing |

| Deep Learning |

| Emotion AI and Affective Computing |

| Individuals |

| Mental Health Clinics and Hospitals |

| Corporate Wellness Providers |

| Payers and Insurers |

| Academic and Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | AI Therapy Chatbots and Virtual Companions | |

| Cognitive Behavioral Therapy Apps | ||

| AI-Driven Biofeedback Devices | ||

| AI-Powered Sleep and Stress Management Tools | ||

| Emotion Recognition and Monitoring Systems | ||

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| By Application | Anxiety and Depression | |

| ADHD and Cognitive Disorders | ||

| Sleep Disorders | ||

| Substance Abuse and Addiction | ||

| Post-Traumatic Stress Disorder | ||

| By Technology | Machine Learning | |

| Natural Language Processing | ||

| Deep Learning | ||

| Emotion AI and Affective Computing | ||

| By End-User | Individuals | |

| Mental Health Clinics and Hospitals | ||

| Corporate Wellness Providers | ||

| Payers and Insurers | ||

| Academic and Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the expected value of the AI-powered behavioral therapy market by 2031?

The AI-powered behavioral therapy market is forecasted to reach USD 3.08 billion by 2031, rising from USD 1.68 billion in 2025 to USD 1.85 billion in 2026 at a 10.73% CAGR.

Which product type leads revenue in AI-powered behavioral therapy?

AI therapy chatbots and virtual companions led revenue with a 49.23% share in 2025, supported by scalability and growing clinical evidence for symptom reduction.

Which region is growing the fastest in this space?

Asia-Pacific is projected to record the fastest regional growth at 14.27% CAGR through 2031, while North America remained the largest region in 2025 with 51.55% revenue share.

Why is North America leading current revenue?

North America leads because it has the strongest reimbursement structure, broad employer benefit adoption, and increasing pressure to manage behavioral care costs and access delays.

Page last updated on: